Exhibit 99.1

ADMA Biologics Announces Preliminary Full Year 2025 Unaudited Total Revenue and Provides Business Update

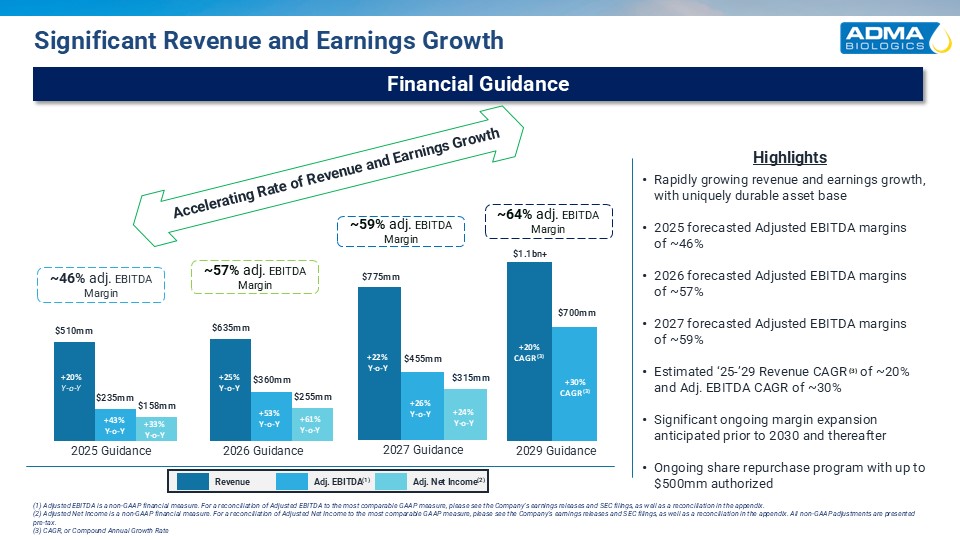

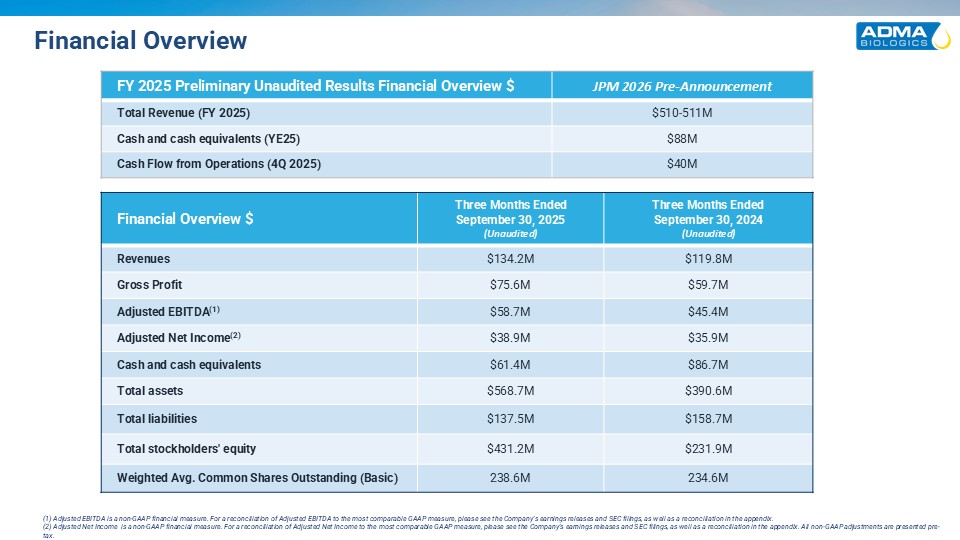

FY 2025 Preliminary Unaudited Total Revenue of Approximately $510–511 Million Meets or Exceeds Prior Guidance

Previously Provided FY 2025 Adjusted EBITDA(1) and Adjusted Net Income(2) Guidance Reiterated

Year-End 2025 Cash Grew to Approximately $88 Million with an Unaudited Operating Cash Flow Estimate of ~$40 Million in 4Q 2025

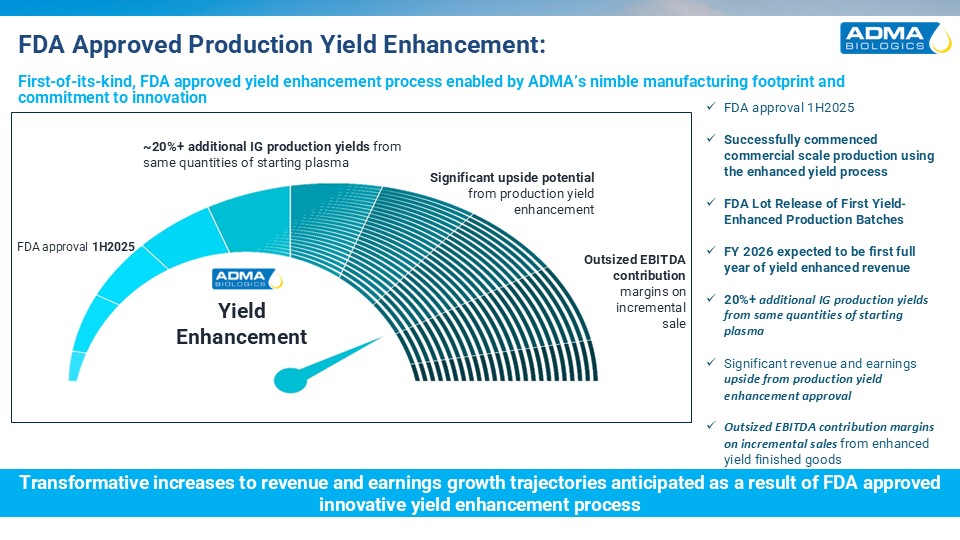

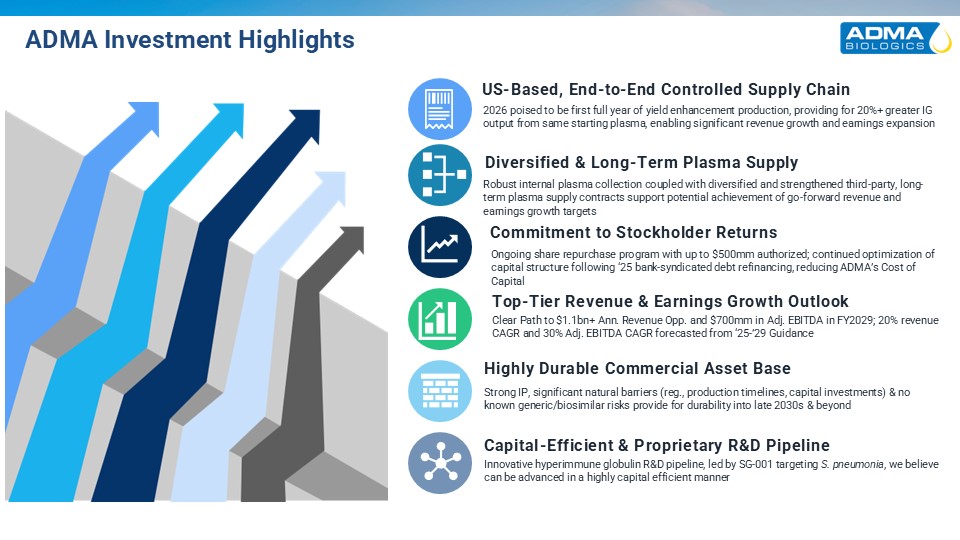

2026 Expected to be ADMA’s First Full Year of Yield-Enhanced Production, Supporting Anticipated Sustained Margin Expansion

Strategic Plasma Network Repositioning Expected to Enhance Margins and Strengthen Long-Term Supply Visibility

Positive, Statistically Significant Real-World ASCENIV™ Outcomes to be Presented at CIS in May 2026; Additional ASCENIV Data Expected Throughout

2026

Advancing SG-001 Pipeline Program with Anticipated FDA Pre-IND Submission in 2026

Ongoing Share Repurchases and Capital Structure Strengthening to Enhance Stockholder Value

FY 2026 and FY 2027 Revenue Expected to be Approximately $635 Million and $775 Million, Respectively

FY 2026 and FY 2027 Adjusted Net Income Expected to be Approximately $255 Million and $315 Million, Respectively

FY 2026 and FY 2027 Adjusted EBITDA Expected to be Approximately $360 Million and $455 Million, Respectively

ADMA Targets Greater Than $1.1 Billion in Annual Revenue in FY 2029, Representing ~20% CAGR(3)

ADMA Targets Greater Than $700 Million in Adjusted EBITDA in FY 2029, Representing ~30% CAGR

RAMSEY, N.J. and BOCA RATON, FL, January 12, 2026 - ADMA Biologics, Inc. (Nasdaq: ADMA) (“ADMA” or the “Company”), a U.S. based end-to-end commercial biopharmaceutical

company dedicated to manufacturing, marketing and developing specialty biologics, today announced its preliminary unaudited full year 2025 revenue and provided a business update. Based on unaudited financial information, ADMA preliminarily

estimates that its total revenue for the full year ended December 31, 2025 will be approximately $510-$511 million. ADMA’s total cash holdings at year-end 2025 grew to approximately $88 million, including an unaudited approximately $40 million in

estimated operating cash flow generated in the fourth quarter of 2025.

“We are pleased with our performance in 2025 and the strong exit momentum we are carrying into 2026,” said Adam Grossman, President and Chief Executive Officer of ADMA.

“Record ASCENIV demand, anticipated payer coverage expansion, and increasing confidence in long-term plasma supply availability are expected to reinforce the durability of our growth engine and provide clear visibility into accelerating revenue

generation as we enter 2026.”

“Operationally, 2025 marked a pivotal transition year for ADMA,” Mr. Grossman continued. “Yield-enhanced production is now successfully implemented at commercial scale,

with 2026 expected to be the first full year of monetizing yield-enhanced product. In parallel, we strategically repositioned our plasma collection center network to enhance margins, strengthen long-term high-titer plasma supply visibility, and

improve capital efficiency, which we believe positions the Company for sustained operating leverage and expanding earnings power entering 2026.”

Mr. Grossman concluded, “With long-term plasma supply secured, a streamlined operating footprint, a strengthening balance sheet, and increasing visibility across both

demand and production, we believe ADMA has established a strong foundation to execute against both near- and longer-term growth objectives. We remain confident in our long-term target to generate more than $1.1 billion in annual revenue and

forecast greater than $700 million in Adjusted EBITDA in 2029, while continuing to deploy capital in a disciplined, stockholder-focused manner as we accelerate our growth trajectory.”

Increased Financial Guidance Highlights Expected Accelerating Growth, Margin Expansion and Enhanced Visibility Into 2026:

| • |

FY 2025 preliminary unaudited total revenue expected to be approximately $510-511 million

|

| • |

FY 2025 expected Adjusted Net Income and Adjusted EBITDA reiterated

|

| • |

FY 2026 expected total revenue increased to approximately $635 million, up from $630 million previously

|

| • |

FY 2026 expected Adjusted Net Income reiterated at approximately $255 million

|

| • |

FY 2026 expected Adjusted EBITDA increased to approximately $360 million, up from $355 million previously

|

| • |

FY 2027 total revenue expected to be approximately $775 million

|

| • |

FY 2027 Adjusted Net Income expected to be approximately $315 million

|

| • |

FY 2027 Adjusted EBITDA expected to be approximately $455 million

|

| • |

Targeting greater than $1.1 billion of total annual revenue in fiscal year 2029, translating to at least $700 million in Adjusted EBITDA

|

Operational and Commercial Momentum Support Sustained Growth and Expanding Earnings Power Entering 2026:

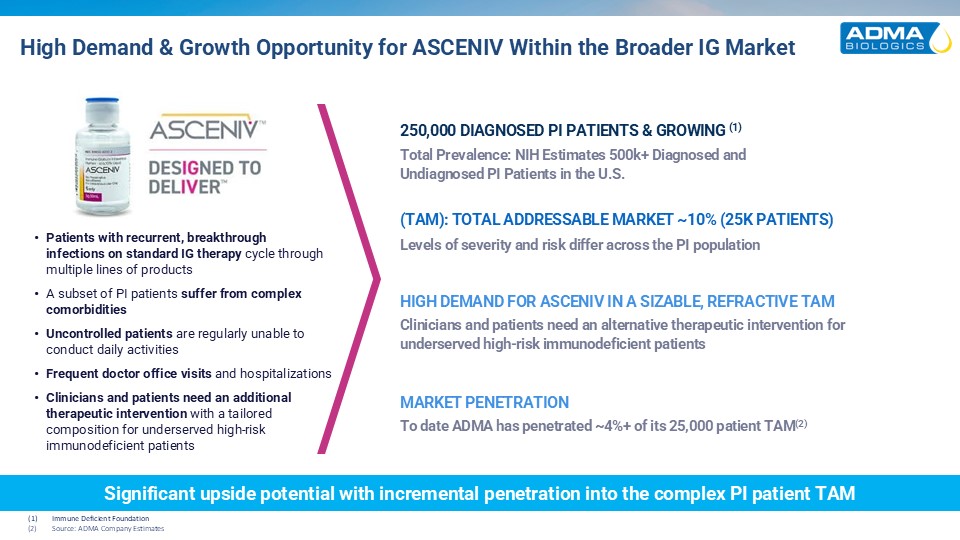

| • |

Accelerating Demand Momentum. Exiting 2025, ASCENIV

utilization accelerated, driven by record demand and expanding prescriber adoption. ASCENIV demand momentum is expected to continue with anticipated payer coverage expansion and increasing confidence in long-term supply continuity.

Year-end utilization trends provide clear visibility into sustained demand growth throughout 2026.

|

| • |

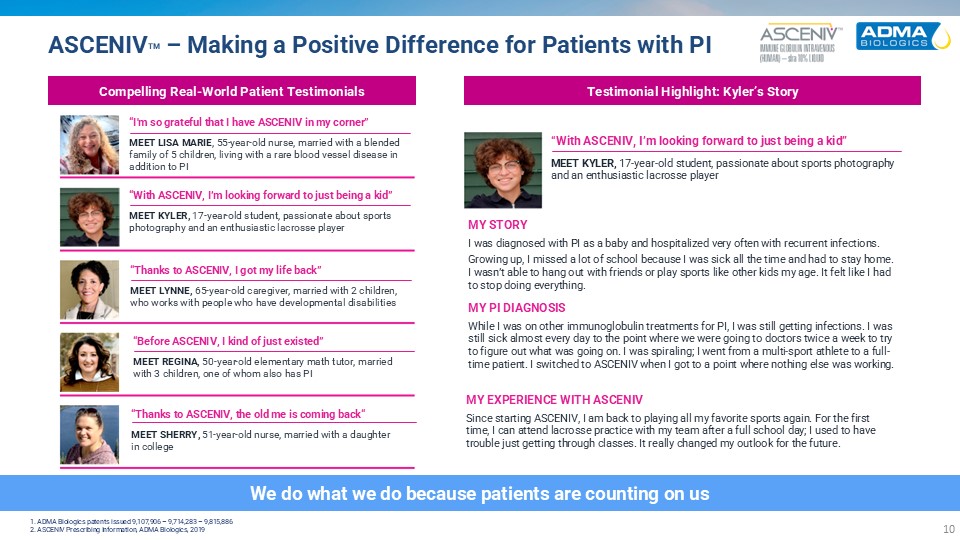

Compelling Clinical Differentiation. Multiple,

independent sets of real-world outcomes data generated during 2025 reinforce ASCENIV’s clinical differentiation. Statistically significant reductions in infection

rates observed in an investigator-initiated analysis support physician confidence, payer engagement, and expanded medical education initiatives expected to further drive utilization in 2026.

|

| o |

An independent, peer-reviewed publication by Tan et al., presented at ACAAI 2025 and published in Clinical Immunology evaluated real-world outcomes in patients with primary or secondary

immunodeficiencies who failed prior standard immunoglobulin replacement therapy (IgRT) and were subsequently treated with ASCENIV. The analysis demonstrated significant reductions in infections and hospitalizations, with 71% of patients

showing clinical improvement and the greatest impact observed within the first six months of treatment. These findings reinforce ASCENIV’s effectiveness in patients with recurrent respiratory infections who have not responded adequately to

conventional intravenous immunoglobulin (IVIG) therapy.

|

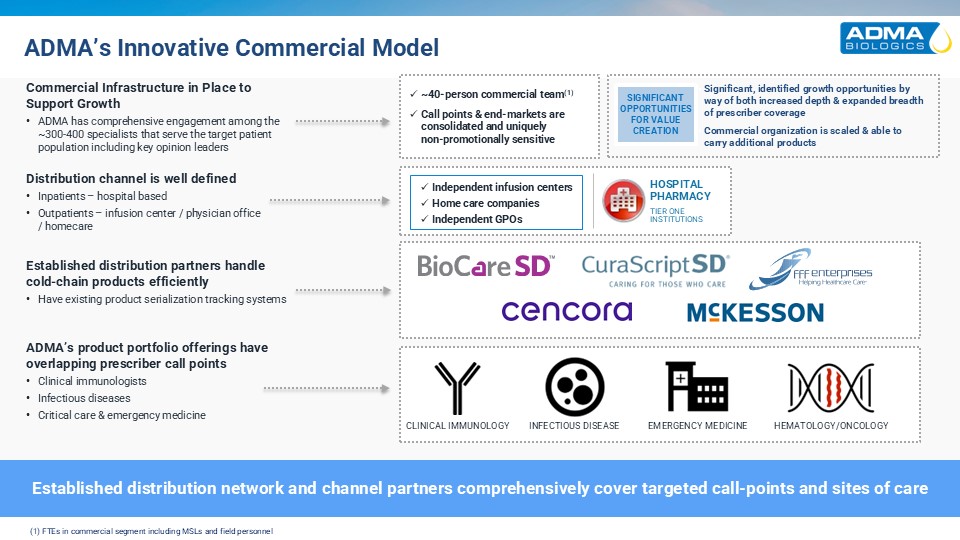

| • |

Strong Payer Access. ASCENIV and BIVIGAM benefit from

strong payer coverage supported by long-standing strategic agreements that have maintained broad access across key commercial, Medicare, and Medicaid segments. These partnerships have reinforced coverage stability while preserving

favorable positioning, resulting in sustainable—and in some cases expanded—coverage that supports consistent patient access and provider confidence.

|

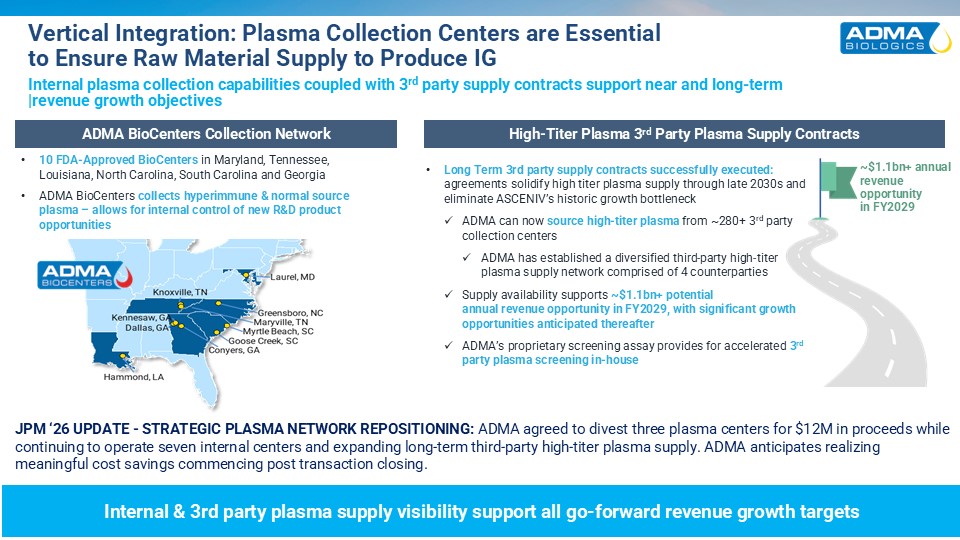

| • |

Strategic Plasma Network Repositioning and Enhanced Supply Visibility. In December 2025, ADMA entered into a purchase agreement for the divestiture of three plasma centers for total proceeds of $12 million. After the divestiture, ADMA will continue to own and operate seven internal

plasma collection centers. In conjunction with the transaction, the Company entered into long-term plasma supply agreements with the purchaser, further diversifying its third-party high-titer plasma supply base. During 2025, third-party

suppliers outperformed initial expectations, expanding access to approximately 280+ plasma collection centers and materially improving long-term high-titer plasma supply visibility. Collectively, these actions reflect a deliberate shift

toward a more flexible, capital-efficient supply model and are expected to deliver accretive cost savings beginning in 2026, improve capital efficiency, support increased ASCENIV production capacity, and provide durable supply confidence

through the late 2030s.

|

| • |

Disciplined Commercial Execution. Disciplined commercial

execution and operating leverage continued to strengthen during 2025. Targeted field execution, expanded medical education, and patient engagement initiatives supported accelerating utilization while maintaining cost discipline, which

should position ADMA for expanding operating leverage and margin growth in 2026.

|

| • |

Strengthened Financial Position. Balance sheet strength and

liquidity improved meaningfully during the fourth quarter of 2025. ADMA exited the year with approximately $88 million in total cash, representing approximately $40 million of operating cash flow generated during the fourth quarter. This

cash balance substantially excludes anticipated proceeds expected to be received from plasma center divestitures. Entering 2026, the Company anticipates accelerated cash generation, accretive cost savings from plasma center divestitures,

and increased financial flexibility to support growth initiatives, balance sheet optimization, and stockholder capital returns.

|

| • |

Expanding Distribution Footprint. ADMA is engaged in

constructive discussions with potential distributors to further diversify its commercial network. During the fourth quarter of 2025, the Company entered into a new authorized distribution agreement for both ASCENIV and BIVIGAM with

McKesson Specialty, which is anticipated to open additional sites of care and patient populations. In 2026, ADMA anticipates further diversification of its distribution and customer network, supporting expanded reach and continued growth

for both products.

|

| • |

Yield-Enhanced Production Execution. Yield-enhanced

production moved into routine commercial execution during 2025, with continued FDA lot releases of yield-enhanced batches. These developments position 2026 as ADMA’s first full year of yield-enhanced production, supporting sustained gross

margin expansion and increasing earnings power.

|

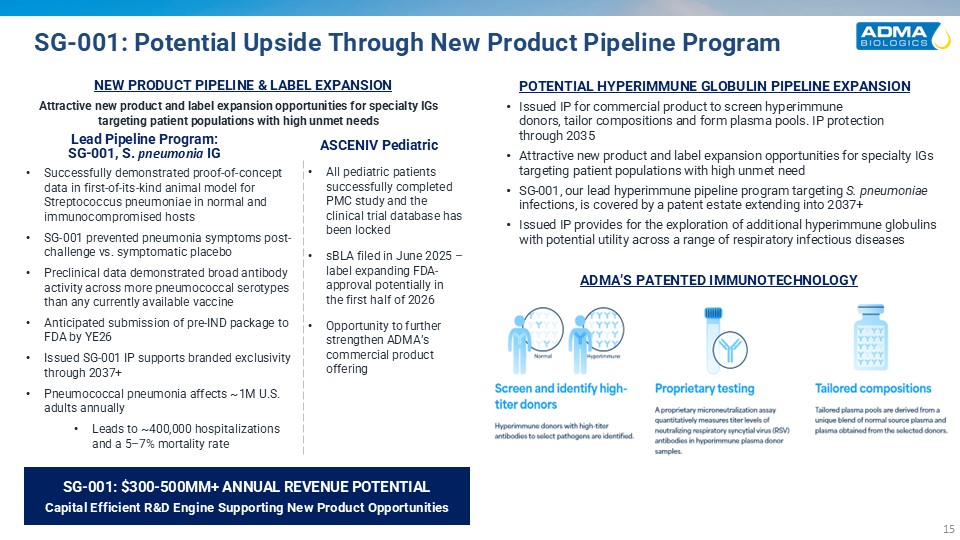

| • |

Pipeline Optionality. Pipeline progress provides long-term

optionality beyond current guidance. The SG-001 pre-clinical development program advanced during 2025, with anticipated submission of a pre-IND package to the FDA in 2026, which would potentially enable the Company to progress development

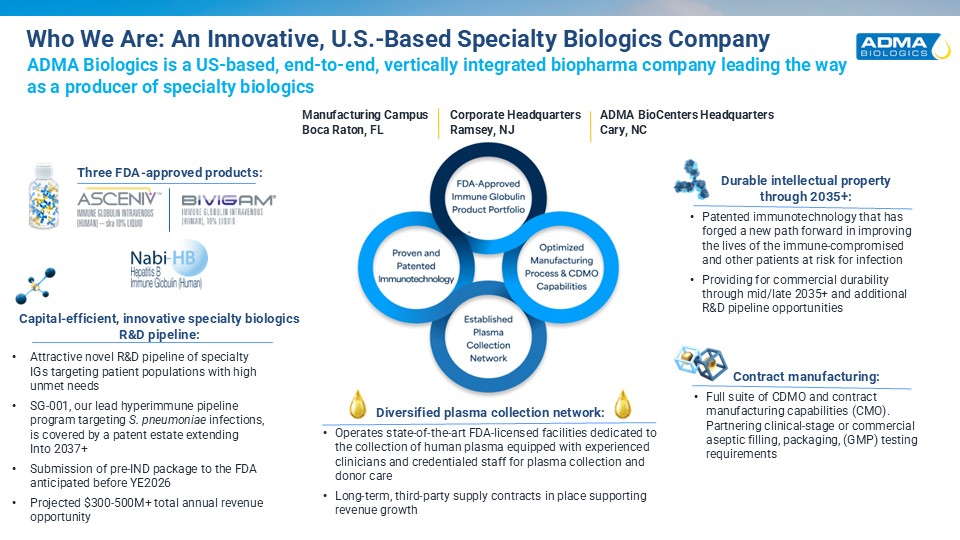

of SG-001 directly into a registrational clinical trial and further strengthen ADMA’s long-term pipeline outlook. The Company continues to believe SG-001 represents a potential $300–500 million annual revenue opportunity at peak.

|

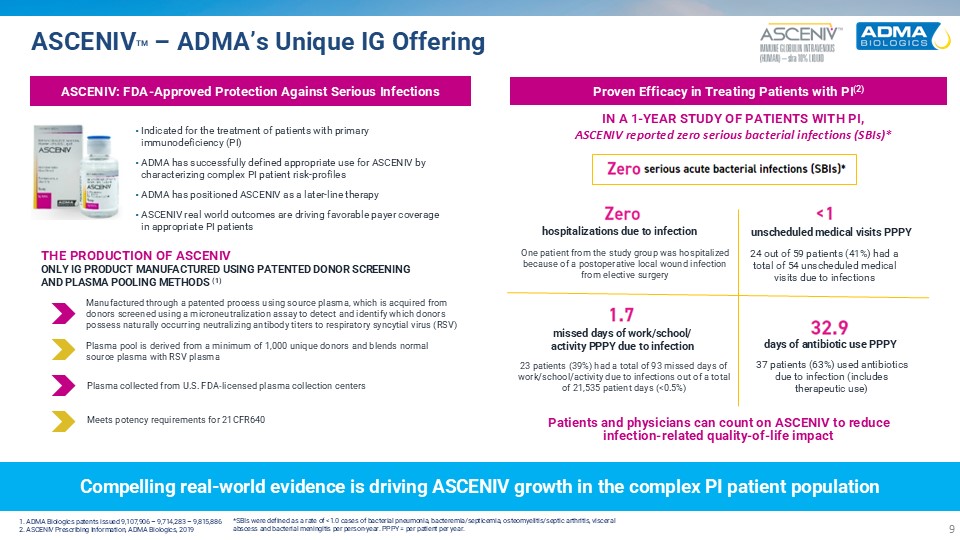

About ASCENIV™

ASCENIV (immune globulin intravenous, human – slra 10% liquid) is a plasma-derived, polyclonal, intravenous immune globulin (IVIG). ASCENIV was approved by the United

States Food and Drug Administration (FDA) in April 2019 and is indicated for the treatment of primary humoral immunodeficiency (PI), also known as primary immune deficiency disease (PIDD), in adults and adolescents (12 to 17 years of age). ASCENIV

is manufactured using ADMA’s unique, patented plasma donor screening methodology and tailored plasma pooling design, which blends normal source plasma and respiratory syncytial virus (RSV) plasma obtained from donors tested using the Company’s

proprietary microneutralization assay. ASCENIV contains naturally occurring polyclonal antibodies, which are proteins that are used by the body’s immune system to neutralize microbes such as bacteria and viruses that safeguard against infection and

disease. ASCENIV is protected by numerous issued patents in the United States and internationally and a wide range of patent applications worldwide. Certain data and other information about ASCENIV can be found by visiting www.asceniv.com.

Information about ADMA and its products can be found on the Company’s website at www.admabiologics.com.

Additional Important Safety Information About ASCENIV™

|

WARNING: THROMBOSIS, RENAL DYSFUNCTION AND ACUTE RENAL FAILURE

|

|

Thrombosis may occur with immune globulin intravenous (IGIV) products, including ASCENIV. Risk factors may include: advanced age, prolonged immobilization,

hypercoagulable conditions, history of venous or arterial thrombosis, use of estrogens, indwelling vascular catheters, hyperviscosity, and cardiovascular risk factors.

Renal dysfunction, acute renal failure, osmotic nephrosis, and death may occur with the administration of IGIV products in predisposed patients.

Renal dysfunction and acute renal failure occur more commonly in patients receiving IGIV products containing sucrose. ASCENIV does not contain sucrose.

For patients at risk of thrombosis, renal dysfunction or renal failure, administer ASCENIV at the minimum dose and infusion rate practicable. Ensure adequate

hydration in patients before administration. Monitor for signs and symptoms of thrombosis and assess blood viscosity in patients at risk for hyperviscosity.

|

ASCENIV™ Contraindications:

History of anaphylactic or severe systemic reactions to human immunoglobulin.

IgA deficient patients with antibodies to IgA and a history of hypersensitivity.

ASCENIV™ Warnings and Precautions:

IgA-deficient patients with antibodies against IgA are at greater risk of developing severe hypersensitivity and anaphylactic reactions. Have medications such as

epinephrine available to treat any acute severe hypersensitivity reactions. [4, 5.1]

Thrombotic events have occurred in patients receiving IGIV treatments. Monitor patients with known risk factors for thrombotic events; consider baseline assessment of

blood viscosity for patients at risk of hyperviscosity. [5.2, 5.4]

In patients at risk of developing acute renal failure. monitor renal function, including blood urea nitrogen (BUN), serum creatinine, and urine output. [5.3, 5.9]

Hyperproteinemia, increased serum viscosity, and hyponatremia or pseudohyponatremia can occur in patients receiving IGIV treatment.

Aseptic meningitis syndrome (AMS) has been reported with IGIV treatments, especially with high doses or rapid infusion. [5.5]

Hemolytic anemia can develop subsequent to IGIV treatment. Monitor patients for hemolysis and hemolytic anemia. [5.6]

Monitor patients for pulmonary adverse reactions (Transfusion-related acute lung injury [TRALI]). If transfusion related acute lung injury is suspected, test the

product and patient for antineutrophil antibodies. [5.7]

Because this product is made from human blood, it may carry a risk of transmitting infectious agents, e.g., viruses, and theoretically, the Creutzfeldt-Jakob disease

(CJD) agent.

ASCENIV™ Adverse Reactions:

The most common adverse reactions to ASCENIV (≥5% of study subjects) were headache, sinusitis, diarrhea, gastroenteritis viral, nasopharyngitis, upper respiratory

tract infection, bronchitis, and nausea

To report SUSPECTED ADVERSE REACTIONS, contact ADMA Biologics at (800) 458-4244 or the FDA at 1-800-FDA-1088 or www.fda.gov/medwatch.

About ADMA Biologics, Inc. (ADMA)

ADMA Biologics is a U.S.-based, end-to-end commercial biopharmaceutical company dedicated to manufacturing, marketing and developing specialty biologics for the

treatment of immunodeficient patients at risk for infection and others at risk for certain infectious diseases. ADMA currently manufactures and markets three United States Food and Drug Administration (FDA)-approved plasma-derived biologics for the

treatment of immune deficiencies and the prevention of certain infectious diseases: ASCENIV™ (immune globulin intravenous, human – slra 10% liquid) for the treatment of primary humoral immunodeficiency (PI); BIVIGAM® (immune globulin

intravenous, human) for the treatment of PI; and NABI-HB® (hepatitis B immune globulin, human) to provide enhanced immunity against the hepatitis B virus. Additionally, ADMA is developing SG-001, a pre-clinical, investigative hyperimmune

globulin targeting S. pneumonia. ADMA manufactures its immune globulin products and product candidates at its FDA-licensed plasma fractionation and purification facility

located in Boca Raton, Florida. Through its ADMA BioCenters subsidiary, ADMA also operates as an FDA-approved source plasma collector in the U.S., which provides its blood plasma for the manufacture of its products and product candidates. ADMA’s

mission is to manufacture, market and develop specialty plasma-derived, human immune globulins targeted to niche patient populations for the treatment and prevention of certain infectious diseases and management of immune compromised patient

populations who suffer from an underlying immune deficiency, or who may be immune compromised for other medical reasons. ADMA holds numerous U.S. and foreign patents related to and encompassing various aspects of its products and product

candidates. For more information, please visit www.admabiologics.com.

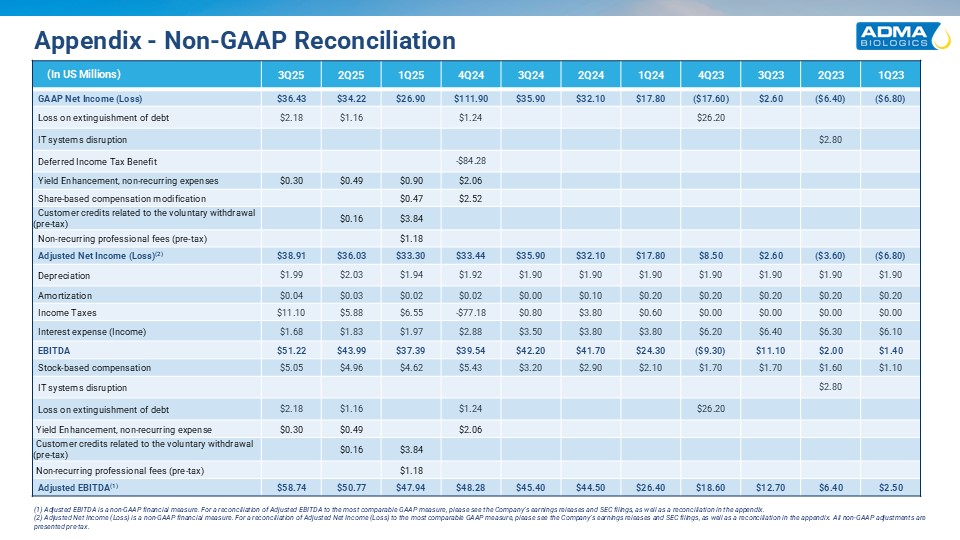

Use of Non-GAAP Financial Measures

This press release includes certain non-GAAP financial measures that are not prepared in accordance with accounting principles generally accepted in the United States

(“GAAP”). The Company believes Adjusted EBITDA and Adjusted Net Income are useful to investors in evaluating the Company’s financial performance. The Company uses Adjusted EBITDA and Adjusted Net Income as key performance measures because we

believe that they facilitate operating performance comparisons from period to period that exclude potential differences driven by the impact of variations of non-cash items such as depreciation and amortization, as well as, in the case of Adjusted

EBITDA, stock-based compensation or certain non-recurring items, and in the case of Adjusted Net Income, certain non-recurring items. The Company believes that investors should have access to the same set of tools used by our management and board

of directors to assess our operating performance. Adjusted EBITDA and Adjusted Net Income should not be considered as measures of financial performance under GAAP, and the items excluded from Adjusted EBITDA and Adjusted Net Income are significant

components in understanding and assessing the Company’s financial performance. Accordingly, these key business metrics have limitations as an analytical tool. They should not be considered as an alternative to net income/loss, cash flows from

operations, or any other performance measures derived in accordance with GAAP and may be different from similarly titled non-GAAP measures used by other companies. The estimated Adjusted EBITDA and Adjusted Net Income amounts included herein are

preliminary and reconciliations cannot be produced at this time without unreasonable effort. The Company expects to provide a reconciliation of Adjusted EBITDA and Adjusted Net Income to the most comparable GAAP measure in its earnings release

relating to the fourth quarter and full year 2025 audited financial results.

Cautionary Note Regarding Forward-Looking Statements

This press release contains “forward-looking statements” pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, about ADMA

Biologics, Inc. (“we,” “our” or the “Company”). Forward-looking statements include, without limitation, any statement that may predict, forecast, indicate, or imply future results, performance or achievements, and may contain such words as

“confident,” “estimate,” “project,” “intend,” “forecast,” “target,” “anticipate,” “plan,” “planning,” “expect,” “believe,” “will,” “is likely,” “will likely,” “position us,” “support,” “should,” “could,” “would,” “may,” “potential,” “opportunity”

or, in each case, their negative, or words or expressions of similar meaning. These forward-looking statements include, but are not limited to, statements about the Company’s total revenue, Adjusted Net Income, Adjusted EBITDA, cash and cash flow,

CAGR and margins guidance in 2025 and future periods and related timing in connection therewith; our balance sheet and financial position; our long-term plasma supply agreements and impact on both ASCENIV growth and overall financial performance;

the repositioning of our plasma network and intended operational and financial benefits; our yield enhancement production process and its resulting impact on our financial operations; ASCENIV real-world outcomes data; payor coverage of our

products; ASCENIV revenue growth, demand and utilization; expanding the distribution network and expected benefits; share repurchases or capital structuring; ability to deliver stockholder value; and statements regarding SG-001, its regulatory

filings timeline and revenue potential. Actual events or results may differ materially from those described in this press release due to a number of important factors. Current and prospective security holders are cautioned that there also can be no

assurance that the forward-looking statements included in this press release will prove to be accurate. Except to the extent required by applicable laws or rules, ADMA does not undertake any obligation to update any forward-looking statements or to

announce revisions to any of the forward-looking statements. Forward-looking statements are subject to many risks, uncertainties and other factors that could cause our actual results, and the timing of certain events, to differ materially from any

future results expressed or implied by the forward-looking statements, including, but not limited to, the risks and uncertainties described in our filings with the SEC, including our most recent reports on Form 10-K, 10-Q and 8-K, and any

amendments thereto.

(1) Adjusted EBITDA is a non-GAAP financial measure. The estimated Adjusted EBITDA amounts included herein are preliminary and reconciliations cannot be produced at this

time without unreasonable effort. The Company expects to provide a reconciliation of Adjusted EBITDA to the most comparable GAAP measure in its earnings release relating to the fourth quarter and full year 2025 audited financial results.

(2) Adjusted Net Income is a non-GAAP financial measure. The estimated Adjusted Net Income amounts included herein are preliminary and reconciliations cannot be produced

at this time without unreasonable effort. The Company expects to provide a reconciliation of Adjusted Net Income to the most comparable GAAP measure in its earnings release relating to the fourth quarter and full year 2025 audited financial

results.

(3) CAGR, or Compound Annual Growth Rate.

INVESTOR RELATIONS CONTACT:

Argot Partners | 212-600-1902 | [email protected]