Exhibit 99.1

Boot Barn Holdings, Inc. Announces Second Quarter Fiscal Year 2024

Financial Results

IRVINE, California – November 2, 2023 – Boot Barn Holdings, Inc. (NYSE: BOOT) today announced its financial results for the second fiscal quarter ended September 30, 2023. A Supplemental Financial Presentation is available at investor.bootbarn.com.

For the quarter ended September 30, 2023:

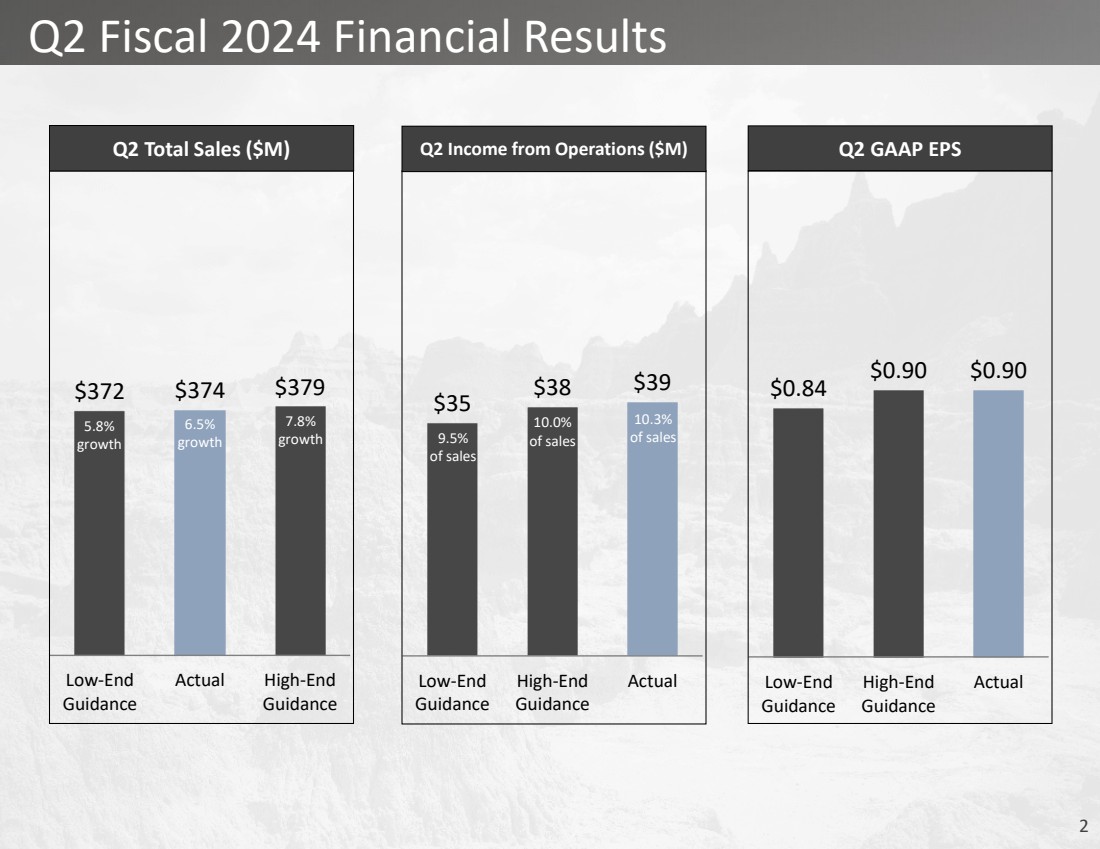

| ● | Net sales increased 6.5% over the prior-year period to $374.5 million, cycling 12.4% net sales growth in the prior-year period. |

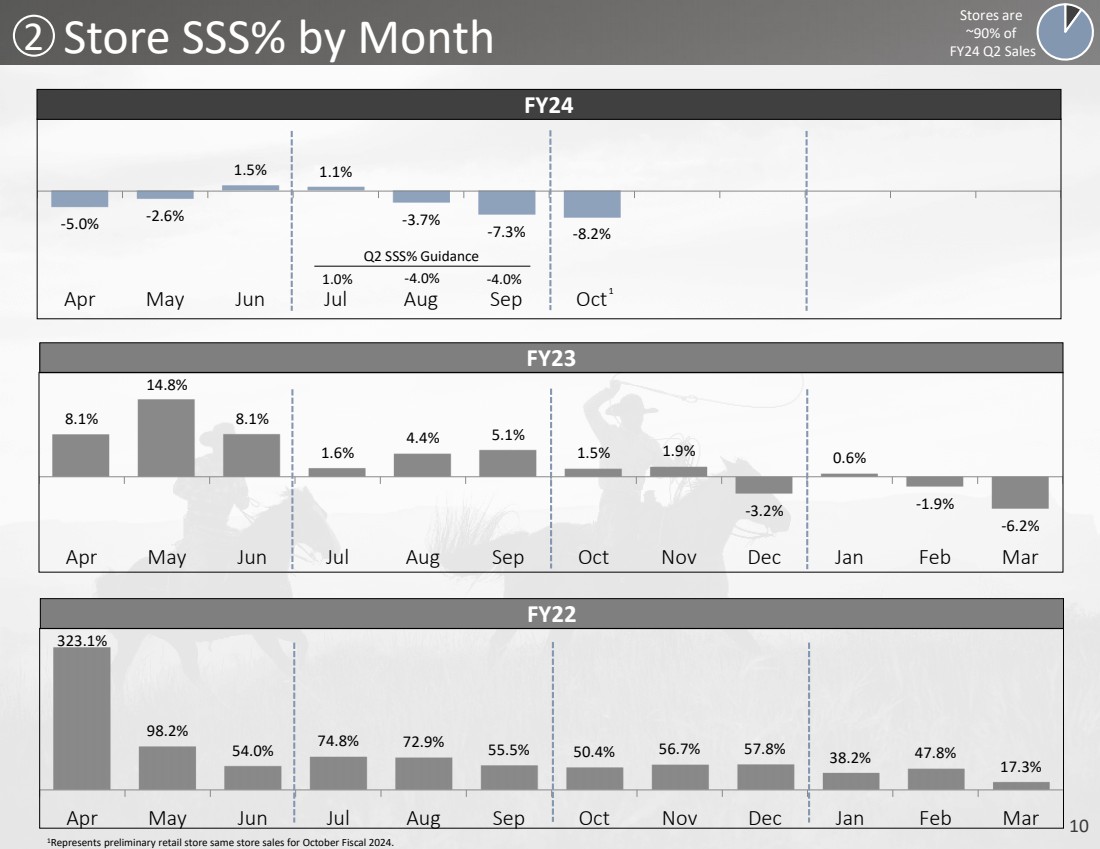

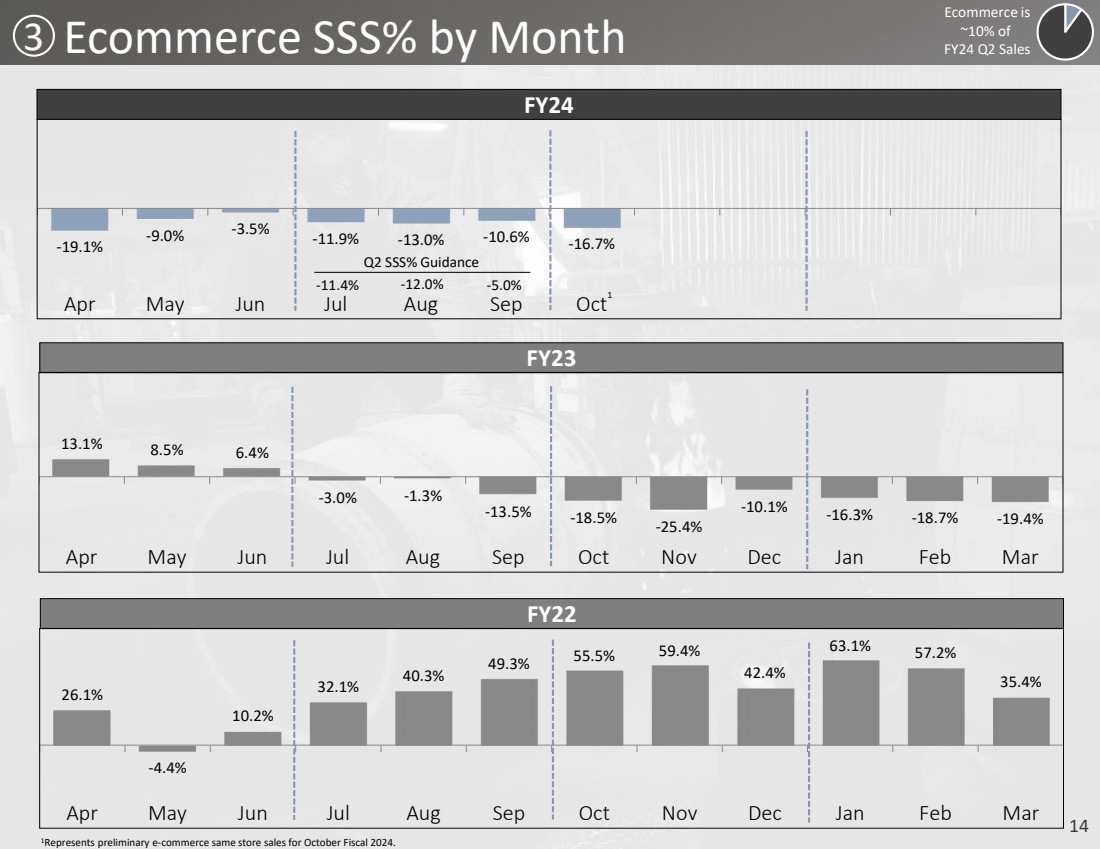

| ● | Same store sales decreased 4.8% compared to the prior-year period, cycling 64% same store sales growth on a 2-year stack basis. The 4.8% decrease in consolidated same store sales is comprised of a decrease in retail store same store sales of 3.8% and a decrease in e-commerce same store sales of 11.7%. |

| ● | Net income was $27.7 million, or $0.90 per diluted share, compared to $32.1 million, or $1.06 per diluted share in the prior-year period. Net income per diluted share in the current-year period includes an approximately $0.01 per share tax expense, primarily due to changes to state tax rates, partially offset by income tax accounting for share-based compensation. Excluding this net tax effect, net income per diluted share was $0.91 in the current-year period. |

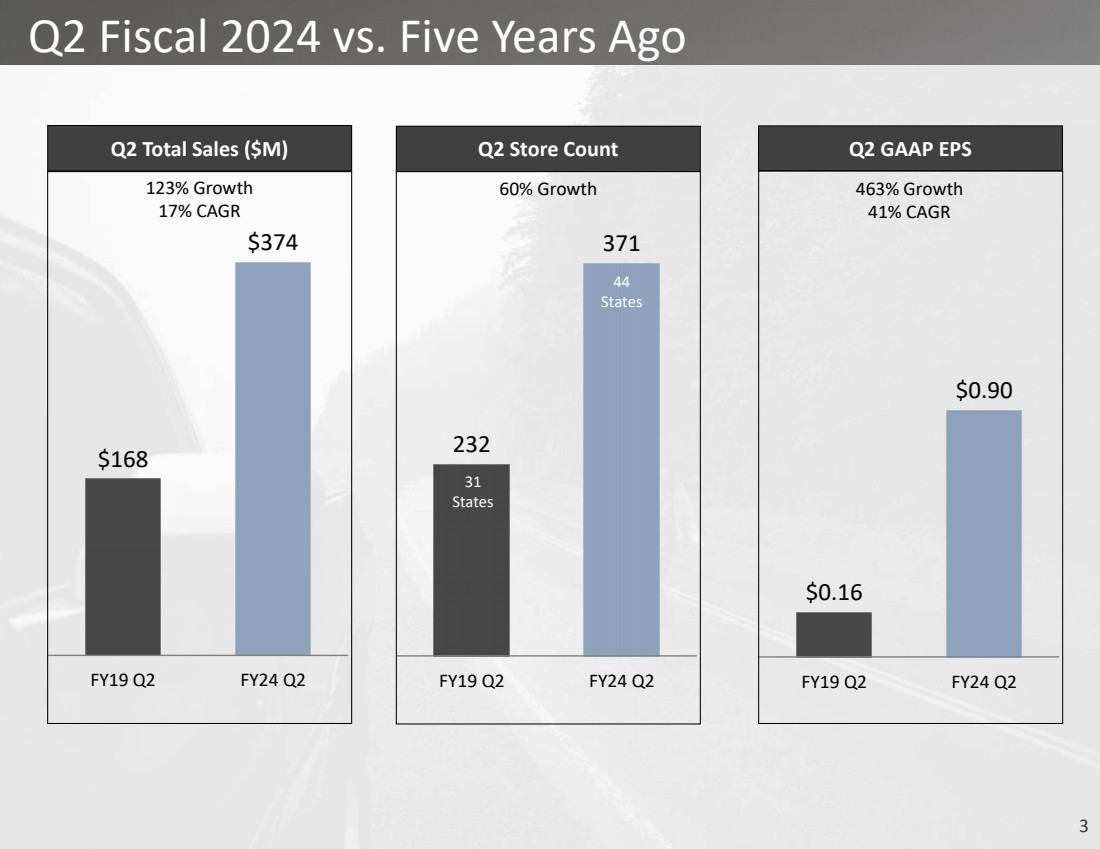

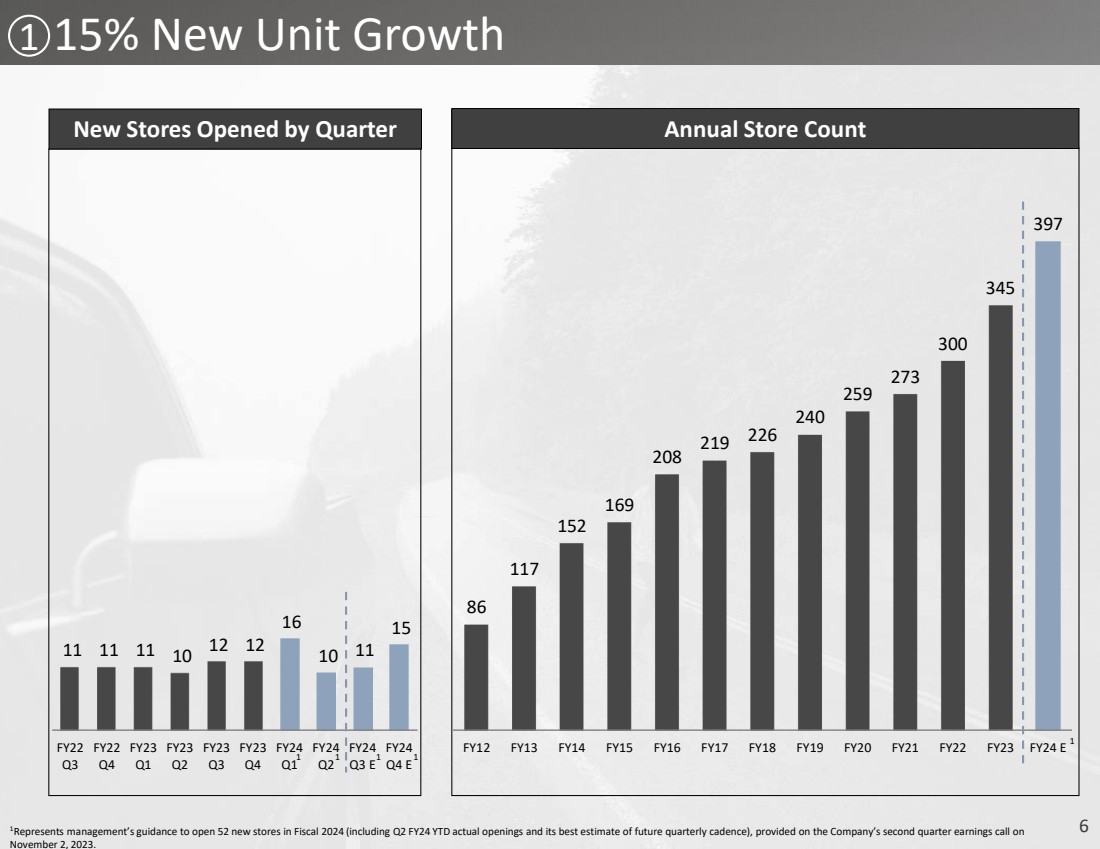

| ● | The Company opened 10 new stores, bringing its total store count to 371. |

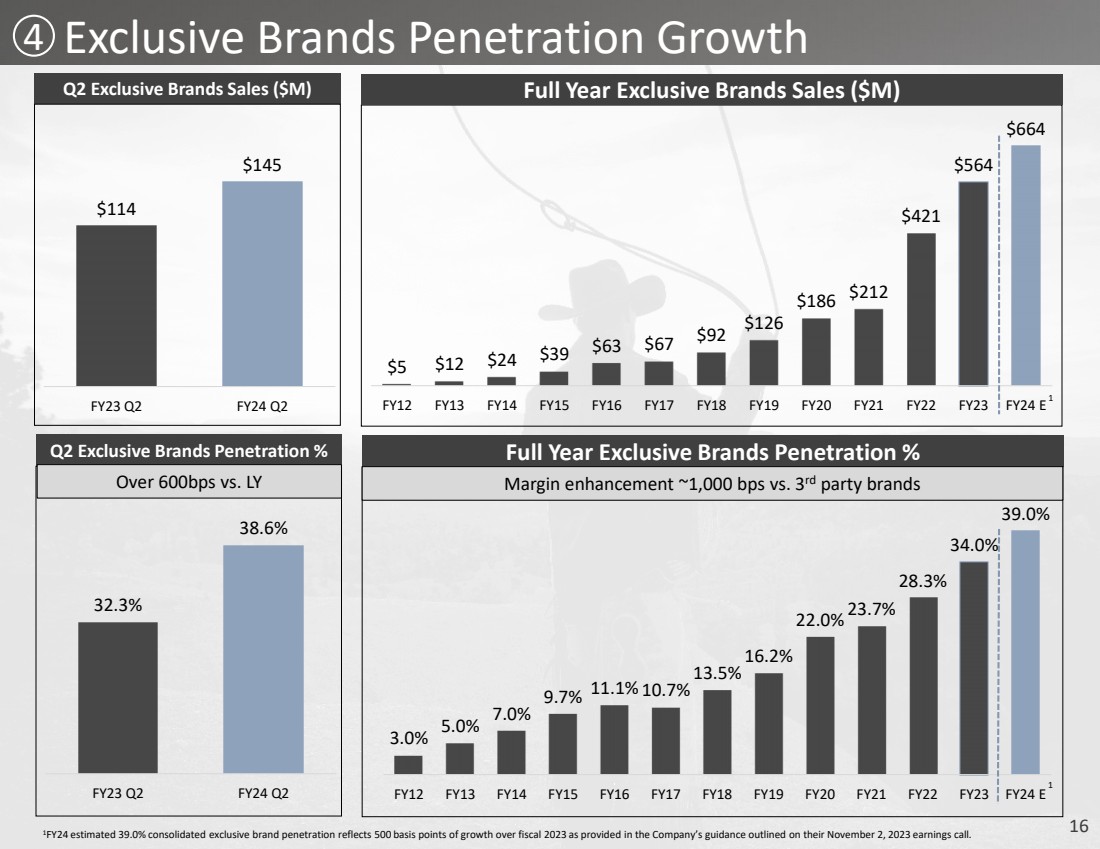

Jim Conroy, President and Chief Executive Officer, commented “I am pleased with our second quarter results which included solid sales growth, merchandise margin expansion and earnings achievement which was at the high end of our guidance range. We opened 10 new stores in the quarter and continue to be encouraged by the new store performance across the country. Exclusive brand penetration expanded more than 600 basis points as our brands are resonating well with the consumer. Our average store sales volume remains at elevated levels with a modest 3.8% decline in retail store same store sales for the quarter.

Throughout the quarter, we saw a sequential decline in same store sales, which we believe to be driven by a macro pull back in consumer demand. We believe that our inventory levels and expense structure are well positioned as we enter the holiday season.”

Operating Results for the Second Quarter Ended September 30, 2023 Compared to the Second Quarter Ended September 24, 2022

| ● | Net sales increased 6.5% to $374.5 million from $351.5 million in the prior-year period. Consolidated same store sales decreased 4.8% with retail store same store sales decreasing 3.8% and e-commerce same store sales decreasing 11.7%. The increase in net sales was the result of the incremental sales from new stores opened over the past twelve months, partially offset by the decrease in consolidated same store sales. |

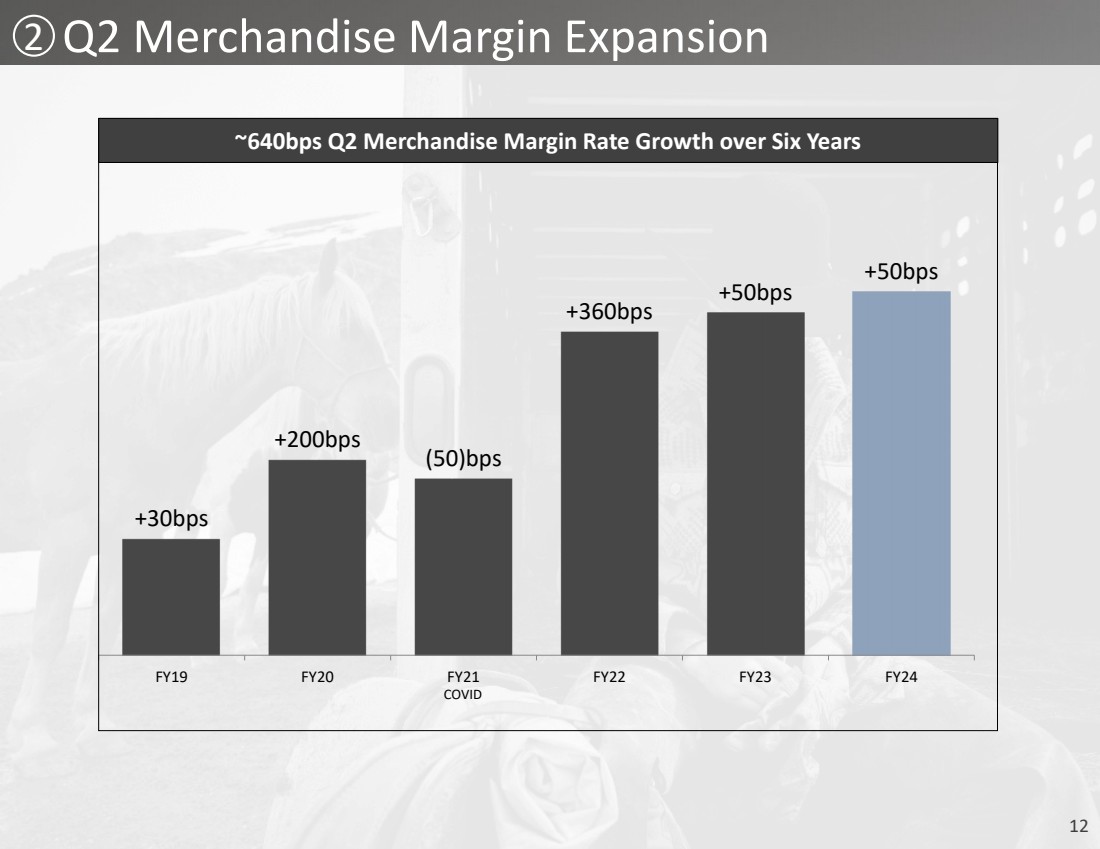

| ● | Gross profit was $133.9 million, or 35.8% of net sales, compared to $129.1 million, or 36.7% of net sales, in the prior-year period. Gross profit increased primarily due to higher sales. The decrease in gross profit rate of 90 basis points was driven primarily by 140 basis points of deleverage in buying, occupancy and distribution center costs driven primarily by occupancy costs of 50 new stores and operating costs related to the new Kansas City distribution center, partially offset by a 50 basis-point increase in merchandise margin rate. The increase in merchandise margin |

1

| rate was driven by 35 basis points of product margin expansion resulting primarily from growth in exclusive brand penetration and a 15 basis-point improvement from lower freight expense as a percentage of net sales. |

| ● | Selling, general and administrative expenses were $95.3 million, or 25.5% of net sales, compared to $84.9 million, or 24.2% of net sales, in the prior-year period. The increase in selling, general and administrative expenses as compared to the prior-year period was primarily a result of higher store payroll and store-related expenses associated with operating 50 new stores and general and administrative expenses in the current year. Selling, general and administrative expenses as a percentage of net sales increased by 130 basis points primarily as a result of higher store payroll and store-related expenses. |

| ● | Income from operations decreased $5.6 million to $38.6 million, or 10.3% of net sales, compared to $44.2 million, or 12.6% of net sales, in the prior-year period, primarily due to the factors noted above. |

| ● | Net income was $27.7 million, or $0.90 per diluted share, compared to net income of $32.1 million, or $1.06 per diluted share in the prior-year period. The decrease in net income is primarily attributable to the factors noted above. Net income per diluted share in the current-year period includes an approximately $0.01 per share tax expense, primarily due to changes to state tax rates, partially offset by income tax accounting for share-based compensation. Excluding this net tax effect, net income per diluted share was $0.91 in the current-year period. |

Operating Results for the Six Months Ended September 30, 2023 Compared to the Six Months Ended September 24, 2022

| ● | Net sales increased 5.7% to $758.2 million from $717.4 million in the prior-year period. Consolidated same store sales decreased 3.8% with retail store same store sales decreasing 2.8% and e-commerce same store sales decreasing 11.3%. The increase in net sales was the result of the incremental sales from new stores opened over the past twelve months, partially offset by the decrease in consolidated same store sales. |

| ● | Gross profit was $275.9 million, or 36.4% of net sales, compared to $266.9 million, or 37.2% of net sales, in the prior-year period. Gross profit increased primarily due to higher sales. The decrease in gross profit rate of 80 basis points was driven primarily by 150 basis points of deleverage in buying, occupancy and distribution center costs driven primarily by occupancy costs of 50 new stores and operating costs related to the new Kansas City distribution center, partially offset by a 70 basis-point increase in merchandise margin rate. The increase in merchandise margin rate was driven by 60 basis points of product margin expansion resulting primarily from growth in exclusive brand penetration and a 10 basis-point improvement from lower freight expense as a percentage of net sales. |

| ● | Selling, general and administrative expenses were $191.1 million, or 25.2% of net sales, compared to $170.4 million, or 23.7% of net sales, in the prior-year period. The increase in selling, general and administrative expenses as compared to the prior-year period was primarily a result of higher store payroll and store-related expenses associated with operating 50 new stores and general and administrative expenses in the current year. Selling, general and administrative expenses as a percentage of net sales increased by 150 basis points primarily as a result of higher store payroll, store-related expenses and general and administrative expenses. |

| ● | Income from operations decreased $11.8 million to $84.8 million, or 11.2% of net sales, compared to $96.6 million, or 13.5% of net sales, in the prior-year period, primarily due to the factors noted above. |

| ● | Net income was $61.9 million, or $2.03 per diluted share, compared to net income of $71.4 million, or $2.35 per diluted share in the prior-year period. Net income per diluted share in the current-year period includes an approximately $0.01 per share tax benefit, primarily due to income tax accounting for share-based compensation, partially offset by changes to state tax rates. Net income per diluted share in the prior-year period includes an approximately $0.03 per share tax benefit, primarily due to income tax accounting for share-based compensation. |

2

| Excluding these net tax effects, net income per diluted share was $2.02 in the current-year period, compared to $2.32 in the prior-year period. |

Sales by Channel

The following table includes total net sales growth, same store sales (“SSS”) growth/(decline) and e-commerce as a percentage of net sales for the periods indicated below.

|

| Thirteen Weeks |

|

| |

| |

| |

|

| Preliminary |

|

| | Ended | | | Four Weeks | | Four Weeks | | Five Weeks | | | Four Weeks |

|

| | September 30, 2023 | | | Fiscal July | | Fiscal August | | Fiscal September | | | Fiscal October |

|

| | | | | | | | | | | | | |

Total Net Sales Growth |

| 6.5 | % | | 13.2 | % | 4.8 | % | 3.1 | % | | 2.8 | % |

| | | | | | | | | | | | | |

Retail Stores SSS |

| (3.8) | % | | 1.1 | % | (3.7) | % | (7.3) | % | | (8.2) | % |

E-commerce SSS |

| (11.7) | % | | (11.9) | % | (13.0) | % | (10.6) | % | | (16.7) | % |

Consolidated SSS |

| (4.8) | % | | (0.5) | % | (4.8) | % | (7.7) | % | | (9.2) | % |

| | | | | | | | | | | | | |

E-commerce as a % of Net Sales |

| 9.9 | % | | 9.5 | % | 9.8 |

| 10.4 | % | | 9.6 | % |

| | | | | | | | | | | | | |

Balance Sheet Highlights as of September 30, 2023

| ● | Cash of $38.7 million. |

| ● | Zero drawn under our $250 million revolving credit facility. |

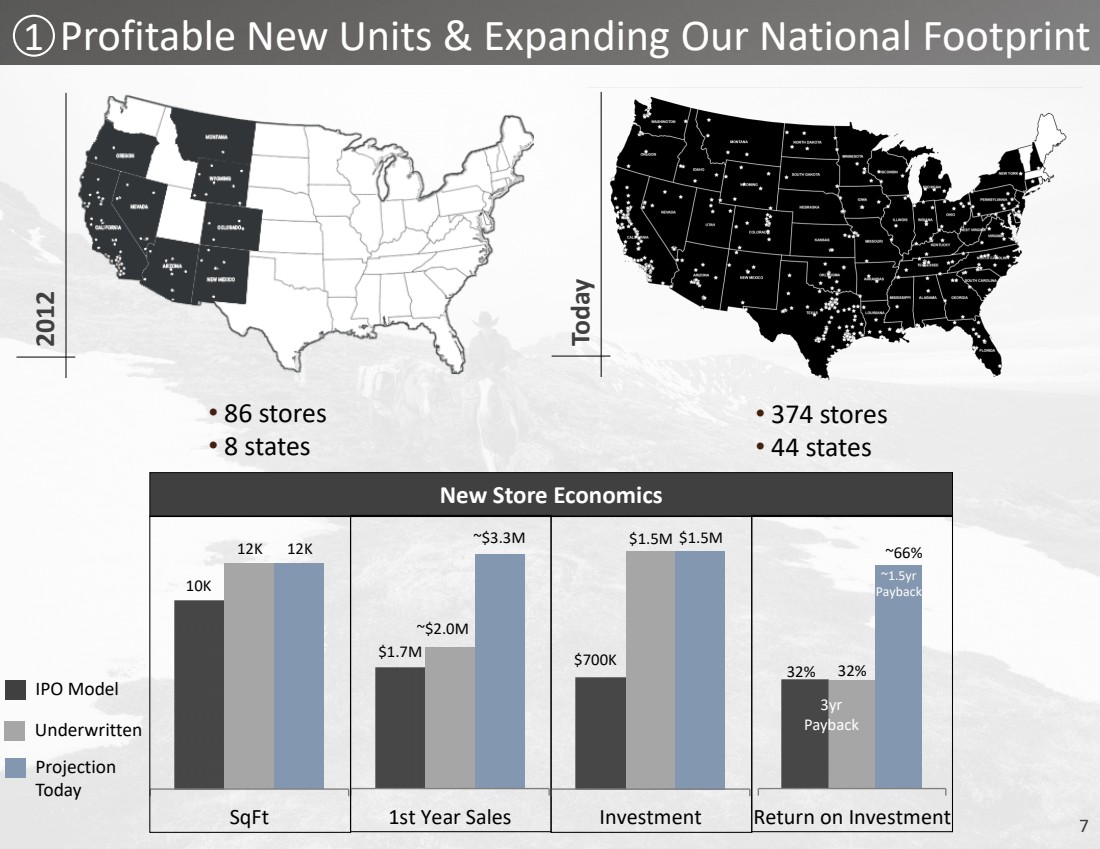

| ● | Average inventory per store decreased approximately 14% on a same store basis compared to September 24, 2022. |

Fiscal Year 2024 Outlook

The Company is providing updated guidance for the fiscal year ending March 30, 2024, superseding in its entirety the previous guidance issued in its first quarter earnings report on August 2, 2023. As a result, for the fiscal year ending March 30, 2024, the Company now expects:

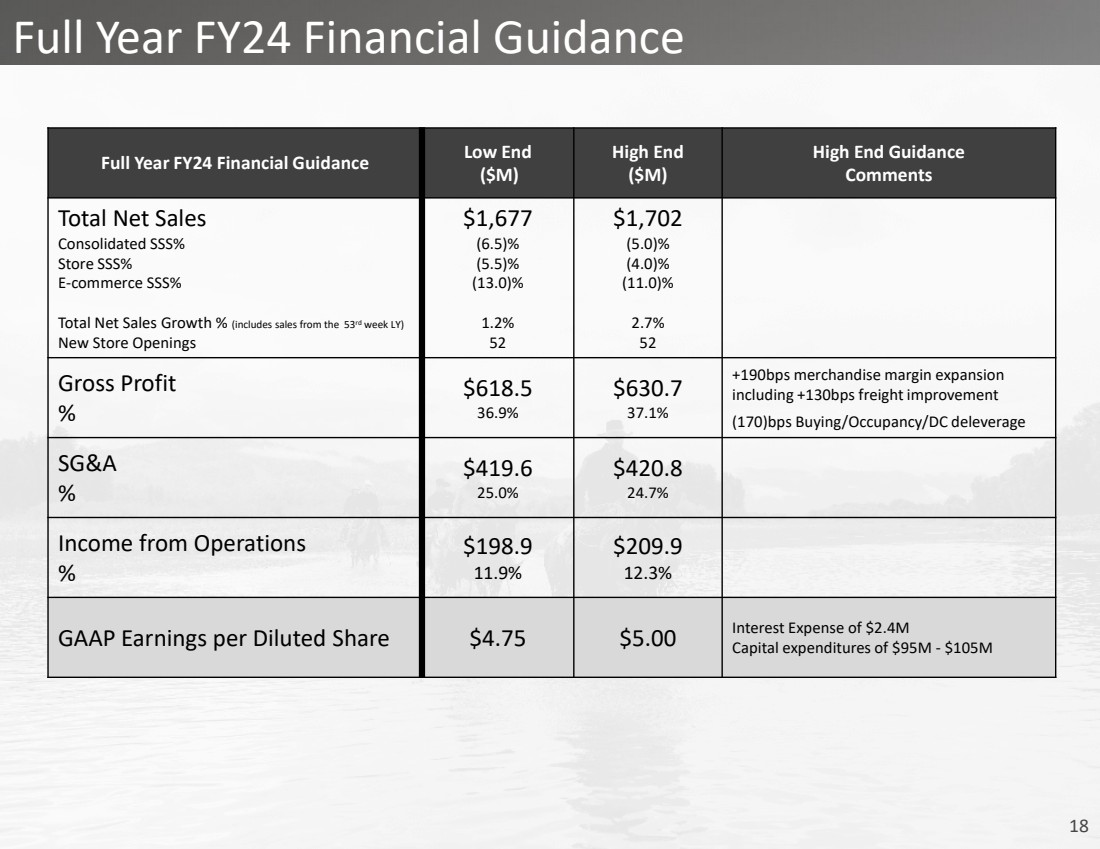

| ● | To open 52 new stores. |

| ● | Total sales of $1.677 billion to $1.702 billion, representing growth of 1.2% to 2.7% over the prior year, which was a 53-week year. |

| ● | Same store sales decline of approximately (6.5)% to (5.0)%, with retail store same store sales declines of (5.5)% to (4.0)% and an e-commerce same store sales decline of (13.0)% to (11.0)%. |

| ● | Gross profit between $618.5 million and $630.7 million, or approximately 36.9% to 37.1% of sales. Gross profit reflects an estimated 190 basis-point increase in merchandise margin, including a 130 basis-point improvement from freight expense. We anticipate 170 basis points of deleverage in buying, occupancy and distribution center costs. |

| ● | Selling, general and administrative expenses between $419.6 million and $420.8 million. This represents approximately 25.0% to 24.7% of sales. |

| ● | Income from operations between $198.9 million and $209.9 million. This represents approximately 11.9% to 12.3% of sales. |

| ● | Interest expense of $2.4 million. |

| ● | Net income of $145.2 million to $153.4 million. |

| ● | Net income per diluted share of $4.75 to $5.00 based on 30.7 million weighted average diluted shares outstanding. |

| ● | Capital expenditures between $95 million and $105 million. |

3

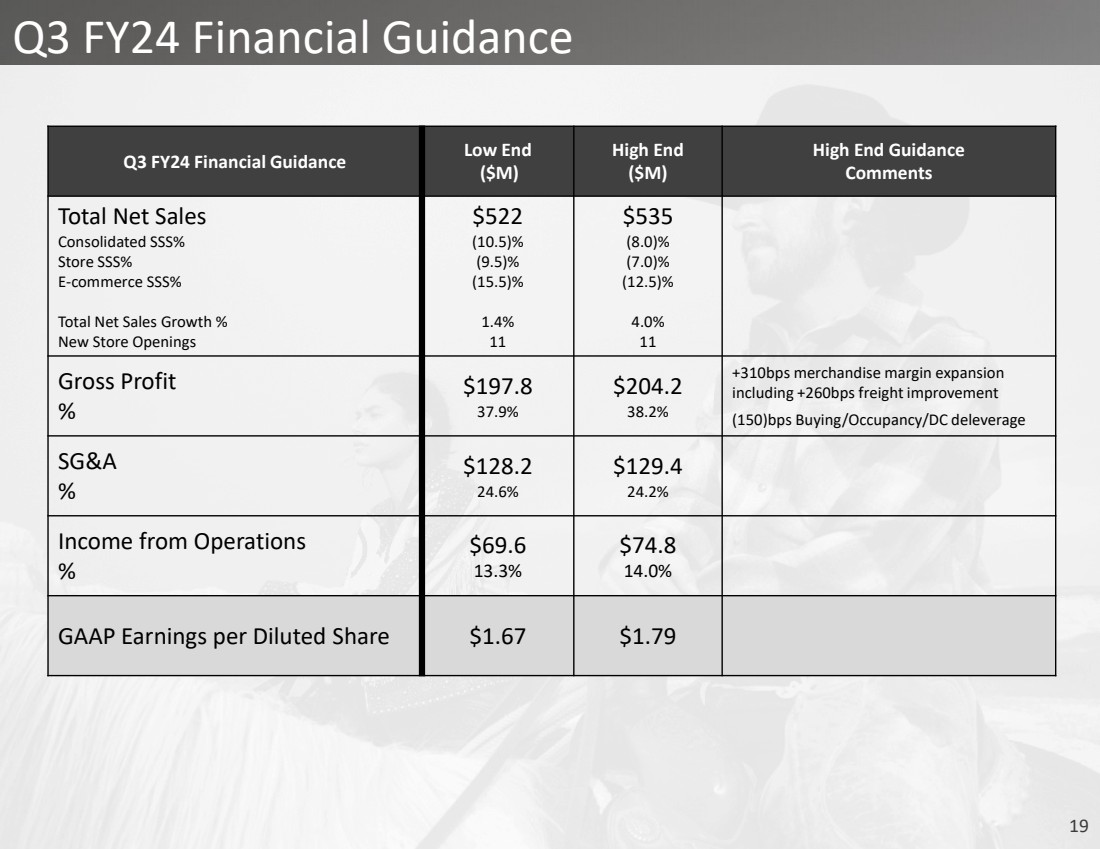

For the fiscal third quarter ending December 30, 2023, the Company expects:

| ● | Total sales of $522 million to $535 million, representing growth of 1.4% to 4.0% over the prior year. |

| ● | Same store sales decline of approximately (10.5)% to (8.0)%, with retail store same store sales declines of (9.5)% to (7.0)% and e-commerce same store sales declines of (15.5)% to (12.5)%. |

| ● | Gross profit between $197.8 million and $204.2 million, or approximately 37.9% to 38.2% of sales. Gross profit reflects an estimated 310 basis-point increase in merchandise margin, including a 260 basis-point improvement from freight expense. We anticipate 150 basis points of deleverage in buying, occupancy and distribution center costs. |

| ● | Selling, general and administrative expenses between $128.2 and $129.4 million. This represents approximately 24.6% to 24.2% of sales. |

| ● | Income from operations between $69.6 million and $74.8 million. This represents approximately 13.3% to 14.0% of sales. |

| ● | Net income per diluted share of $1.67 to $1.79 based on 30.7 million weighted average diluted shares outstanding. |

Conference Call Information

A conference call to discuss the financial results for the second quarter of fiscal year 2024 is scheduled for today, November 2, 2023, at 4:30 p.m. ET (1:30 p.m. PT). Investors and analysts interested in participating in the call are invited to dial (877) 451-6152. The conference call will also be available to interested parties through a live webcast at investor.bootbarn.com. Please visit the website and select the “Events and Presentations” link at least 15 minutes prior to the start of the call to register and download any necessary software. A Supplemental Financial Presentation is also available on the investor relations section of the Company’s website. A telephone replay of the call will be available until December 2, 2023, by dialing (844) 512-2921 (domestic) or (412) 317-6671 (international) and entering the conference identification number: 13742403. Please note participants must enter the conference identification number in order to access the replay.

About Boot Barn

Boot Barn is the nation’s leading lifestyle retailer of western and work-related footwear, apparel and accessories for men, women and children. The Company offers its loyal customer base a wide selection of work and lifestyle brands. As of the date of this release, Boot Barn operates 374 stores in 44 states, in addition to an e-commerce channel www.bootbarn.com. The Company also operates www.sheplers.com, the nation’s leading pure play online western and work retailer and www.countryoutfitter.com, an e-commerce site selling to customers who live a country lifestyle. For more information, call 888-Boot-Barn or visit www.bootbarn.com.

Forward Looking Statements

This press release contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this press release are forward-looking statements. Forward-looking statements refer to our current expectations and projections relating to, by way of example and without limitation, our financial condition, liquidity, profitability, results of operations, margins, plans, objectives, strategies, future performance, business and industry. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipate”, “estimate”, “expect”, “project”, “plan“, “intend”, “believe”, “may”, “might”, “will”, “could”, “should”, “can have”, “likely”, “outlook” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events, but not all forward-looking statements contain these identifying words. These forward-looking statements are based on assumptions that the Company’s management has made in light of their industry experience and on their perceptions of historical trends, current conditions, expected future developments and other factors they believe are appropriate under the circumstances. As you consider this press release, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond the Company’s control) and assumptions. These risks, uncertainties and assumptions include, but

4

are not limited to, the following: decreases in consumer spending due to declines in consumer confidence, local economic conditions or changes in consumer preferences; the Company’s ability to effectively execute on its growth strategy; and the Company’s failure to maintain and enhance its strong brand image, to compete effectively, to maintain good relationships with its key suppliers, and to improve and expand its exclusive product offerings. The Company discusses the foregoing risks and other risks in greater detail under the heading “Risk factors” in the periodic reports filed by the Company with the Securities and Exchange Commission. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect the Company’s actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. Because of these factors, the Company cautions that you should not place undue reliance on any of these forward-looking statements. New risks and uncertainties arise from time to time, and it is impossible for the Company to predict those events or how they may affect the Company. Further, any forward-looking statement speaks only as of the date on which it is made. Except as required by law, the Company does not intend to update or revise the forward-looking statements in this press release after the date of this press release.

Investor Contact:

ICR, Inc.

Brendon Frey, 203-682-8216

or

Company Contact:

Boot Barn Holdings, Inc.

Mark Dedovesh, 949-453-4489

Senior Vice President, Investor Relations & Financial Planning

5

Boot Barn Holdings, Inc.

Consolidated Balance Sheets

(In thousands, except per share data)

(Unaudited)

|

| September 30, |

| April 1, | ||

| | 2023 |

| 2023 | ||

Assets |

| |

|

| |

|

Current assets: |

| |

|

| |

|

Cash and cash equivalents | | $ | 38,665 | | $ | 18,193 |

Accounts receivable, net | |

| 9,321 | |

| 13,145 |

Inventories | |

| 585,573 | |

| 589,494 |

Prepaid expenses and other current assets | |

| 39,044 | |

| 48,341 |

Total current assets | |

| 672,603 | |

| 669,173 |

Property and equipment, net | |

| 293,702 | |

| 257,143 |

Right-of-use assets, net | |

| 348,788 | | | 326,623 |

Goodwill | |

| 197,502 | |

| 197,502 |

Intangible assets, net | |

| 60,724 | |

| 60,751 |

Other assets | |

| 4,887 | |

| 6,189 |

Total assets | | $ | 1,578,206 | | $ | 1,517,381 |

Liabilities and stockholders’ equity | |

| | | | |

Current liabilities: | |

| | | | |

Line of credit | | $ | — | | $ | 66,043 |

Accounts payable | |

| 139,762 | | | 134,246 |

Accrued expenses and other current liabilities | |

| 132,860 | |

| 122,958 |

Short-term lease liabilities | |

| 56,209 | | | 51,595 |

Total current liabilities | |

| 328,831 | |

| 374,842 |

Deferred taxes | |

| 36,253 | |

| 33,260 |

Long-term lease liabilities | |

| 357,478 | | | 330,081 |

Other liabilities | |

| 3,258 | |

| 2,748 |

Total liabilities | |

| 725,820 | | | 740,931 |

| | | | | | |

Stockholders’ equity: | |

| | | | |

Common stock, $0.0001 par value; September 30, 2023 - 100,000 shares authorized, 30,511 shares issued; April 1, 2023 - 100,000 shares authorized, 30,072 shares issued | |

| 3 | |

| 3 |

Preferred stock, $0.0001 par value; 10,000 shares authorized, no shares issued or outstanding | |

| — | |

| — |

Additional paid-in capital | |

| 226,379 | |

| 209,964 |

Retained earnings | |

| 637,963 | |

| 576,030 |

Less: Common stock held in treasury, at cost, 227 and 192 shares at September 30, 2023 and April 1, 2023, respectively | |

| (11,959) | | | (9,547) |

Total stockholders’ equity | |

| 852,386 | |

| 776,450 |

Total liabilities and stockholders’ equity | | $ | 1,578,206 | | $ | 1,517,381 |

6

Boot Barn Holdings, Inc.

Consolidated Statements of Operations

(In thousands, except per share data)

(Unaudited)

|

| Thirteen Weeks Ended |

| Twenty-Six Weeks Ended | ||||||||

|

| September 30, | | September 24, | | September 30, | | September 24, | ||||

| | 2023 |

| 2022 |

| 2023 |

| 2022 | ||||

Net sales | | $ | 374,456 | | $ | 351,545 | | $ | 758,151 | | $ | 717,401 |

Cost of goods sold | |

| 240,540 | |

| 222,449 | |

| 482,272 | |

| 450,475 |

Gross profit | |

| 133,916 | |

| 129,096 | |

| 275,879 | |

| 266,926 |

Selling, general and administrative expenses | |

| 95,338 | |

| 84,946 | |

| 191,056 | |

| 170,351 |

Income from operations | |

| 38,578 | |

| 44,150 | |

| 84,823 | |

| 96,575 |

Interest expense | |

| 463 | |

| 1,362 | |

| 1,486 | |

| 2,087 |

Other (loss)/income, net | |

| (50) | |

| — | |

| 174 | |

| (273) |

Income before income taxes | |

| 38,065 | |

| 42,788 | |

| 83,511 | |

| 94,215 |

Income tax expense | |

| 10,385 | |

| 10,734 | |

| 21,578 | |

| 22,843 |

Net income | | $ | 27,680 | | $ | 32,054 | | $ | 61,933 | | $ | 71,372 |

| | | | | | | | | | | | |

Earnings per share: | |

| | |

| | |

| | |

| |

Basic | | $ | 0.92 | | $ | 1.08 | | $ | 2.06 | | $ | 2.40 |

Diluted | | $ | 0.90 | | $ | 1.06 | | $ | 2.03 | | $ | 2.35 |

Weighted average shares outstanding: | |

| | |

| | |

| | |

| |

Basic | |

| 30,137 | |

| 29,808 | |

| 30,029 | |

| 29,778 |

Diluted | |

| 30,627 | |

| 30,313 | |

| 30,540 | |

| 30,351 |

7

Boot Barn Holdings, Inc.

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

|

| Twenty-Six Weeks Ended | ||||

| | September 30, | | September 24, | ||

| | 2023 | | 2022 | ||

Cash flows from operating activities |

| |

|

| |

|

Net income | | $ | 61,933 | | $ | 71,372 |

Adjustments to reconcile net income to net cash provided by/(used in) operating activities: | |

| | |

| |

Depreciation | |

| 22,597 | |

| 16,792 |

Stock-based compensation | |

| 7,833 | |

| 7,143 |

Amortization of intangible assets | |

| 27 | |

| 32 |

Noncash lease expense | |

| 26,487 | |

| 22,951 |

Amortization and write-off of debt issuance fees and debt discount | |

| 54 | |

| 74 |

Loss on disposal of assets | |

| 298 | |

| 250 |

Deferred taxes | |

| 2,993 | |

| 1,479 |

Changes in operating assets and liabilities: | |

| | |

| |

Accounts receivable, net | |

| 3,046 | |

| (972) |

Inventories | |

| 3,921 | |

| (166,721) |

Prepaid expenses and other current assets | |

| 9,243 | |

| (5,857) |

Other assets | |

| 1,302 | |

| (3,329) |

Accounts payable | |

| 7,051 | |

| 36,472 |

Accrued expenses and other current liabilities | |

| 13,600 | |

| (27,199) |

Other liabilities | |

| 510 | |

| 244 |

Operating leases | |

| (15,435) | |

| (14,868) |

Net cash provided by/(used in) operating activities | | $ | 145,460 | | $ | (62,137) |

Cash flows from investing activities | |

| | |

| |

Purchases of property and equipment | | $ | (64,687) | | $ | (52,459) |

Net cash used in investing activities | | $ | (64,687) | | $ | (52,459) |

Cash flows from financing activities | |

| | |

| |

(Payments)/Borrowings on line of credit, net | | $ | (66,043) | | $ | 118,281 |

Repayments on debt and finance lease obligations | |

| (428) | |

| (419) |

Tax withholding payments for net share settlement | |

| (2,412) | |

| (4,501) |

Proceeds from the exercise of stock options | |

| 8,582 | |

| 247 |

Net cash (used in)/provided by financing activities | | $ | (60,301) | | $ | 113,608 |

| | | | | | |

Net increase/(decrease) in cash and cash equivalents | |

| 20,472 | |

| (988) |

Cash and cash equivalents, beginning of period | |

| 18,193 | |

| 20,674 |

Cash and cash equivalents, end of period | | $ | 38,665 | | $ | 19,686 |

| | | | | | |

Supplemental disclosures of cash flow information: | |

| | |

| |

Cash paid for income taxes | | $ | 2,822 | | $ | 45,519 |

Cash paid for interest | | $ | 1,399 | | $ | 1,642 |

Supplemental disclosure of non-cash activities: | |

| | |

| |

Unpaid purchases of property and equipment | | $ | 14,103 | | $ | 21,551 |

8

Boot Barn Holdings, Inc.

Store Count

|

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| Quarter Ended |

| | September 30, | | July 1, | | April 1, | | December 24, | | September 24, | | June 25, | | March 26, | | December 25, |

| | 2023 | | 2023 | | 2023 | | 2022 | | 2022 | | 2022 | | 2022 | | 2021 |

Store Count (BOP) |

| 361 | | 345 | | 333 | | 321 | | 311 | | 300 | | 289 | | 278 |

Opened/Acquired |

| 10 | | 16 | | 12 | | 12 | | 10 | | 11 | | 11 | | 11 |

Closed |

| — | | — | | — | | — | | — | | — | | — | | — |

Store Count (EOP) |

| 371 | | 361 | | 345 | | 333 | | 321 | | 311 | | 300 | | 289 |

Boot Barn Holdings, Inc.

Selected Store Data

| | | | | |

| | | | | | | | | | | | | | | | |

| ||

| | Thirteen Weeks Ended | | Fourteen | | Thirteen Weeks Ended | | ||||||||||||||||||

| | September 30, | | July 1, | | April 1, | | December 24, | | September 24, | | June 25, | | March 26, | | December 25, |

| ||||||||

|

| 2023 |

| 2023 |

| 2023 |

| 2022 |

| 2022 |

| 2022 |

| 2022 |

| 2021 |

| ||||||||

Selected Store Data: | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

|

Same Store Sales (decline)/growth |

| | (4.8) | % | | (2.9) | % | | (5.5) | % | | (3.6) | % | | 2.3 | % | | 10.0 | % | | 33.3 | % | | 54.2 | % |

Stores operating at end of period |

| | 371 |

| | 361 |

| | 345 |

| | 333 |

| | 321 |

| | 311 |

| | 300 |

| | 289 | |

Total retail store square footage, end of period (in thousands) |

| | 4,027 |

| | 3,914 |

| | 3,735 |

| | 3,598 |

| | 3,451 |

| | 3,333 |

| | 3,194 |

| | 3,063 | |

Average store square footage, end of period |

| | 10,855 |

| | 10,841 |

| | 10,825 |

| | 10,806 |

| | 10,751 |

| | 10,717 |

| | 10,648 |

| | 10,597 | |

Average net sales per store (in thousands) | | $ | 909 | | $ | 958 | | $ | 1,088 | | $ | 1,320 | | $ | 966 | | $ | 1,031 | | $ | 1,094 | | $ | 1,372 | |

9