Exhibit 99.1

FOR IMMEDIATE RELEASE: Bank7 Corp. Announces Q2 2026 Earnings

Oklahoma City, July 16, 2026 – Bank7 Corp. (NASDAQ: BSVN) ("the Company"), the parent company of Oklahoma City-based Bank7 (the "Bank"), today reported

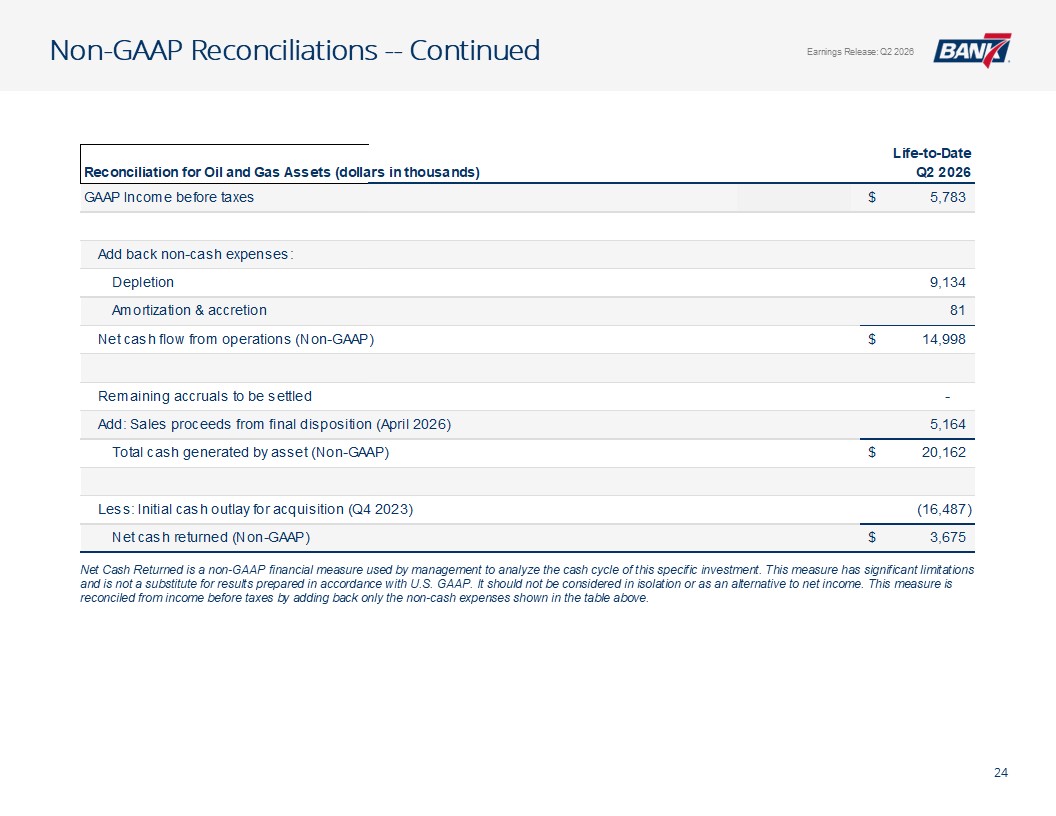

unaudited results for the quarter ended June 30, 2026. “We are pleased with our core banking results this quarter. Reported results include a non-recurring loss on the sale of energy

assets, which followed the successful maximization of our loan loss recovery related to an energy loan previously charged off in 2023. The Company continues to benefit from strong capital, robust liquidity, a solid net interest margin, and

excellent credit quality, which are all supported by our properly matched balance sheet and our location in the dynamic markets we serve,” said Thomas L. Travis, President and CEO of the Company.

For the three months ended June 30, 2026 compared to the three months ended June 30, 2025:

| - |

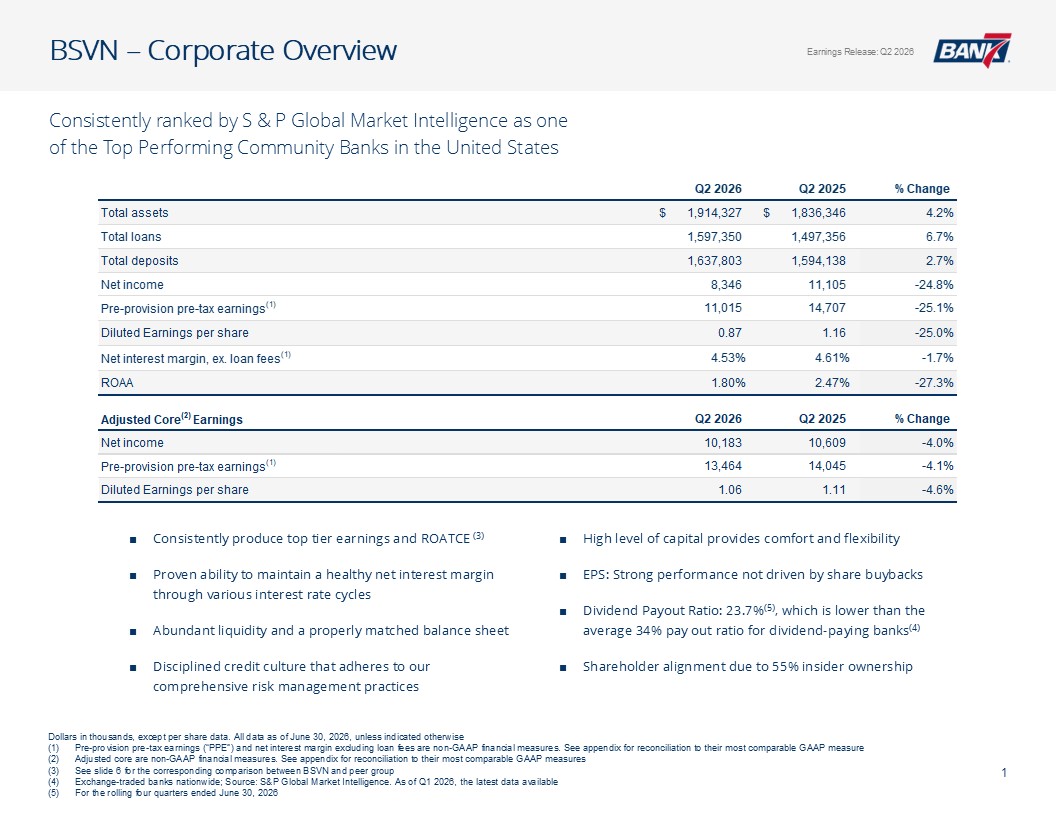

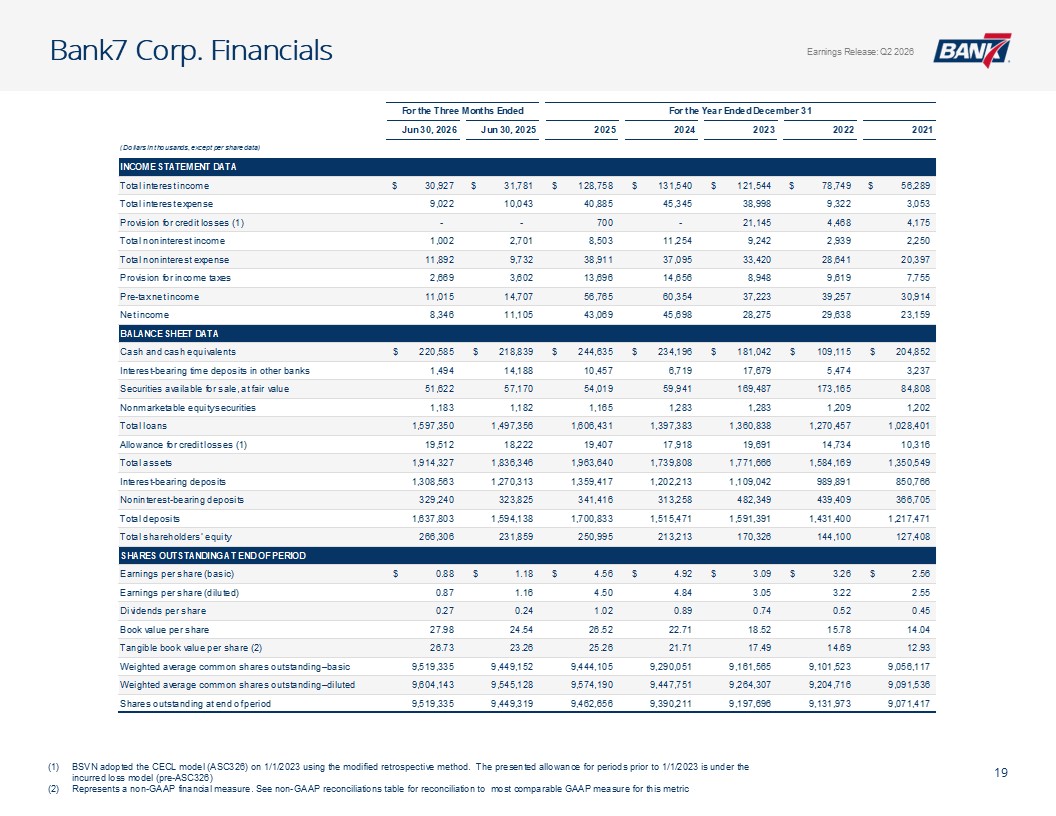

Net income of $8.35 million compared to $11.11 million, a decrease of 24.84%

|

| - |

Earnings per share of $0.87 compared to $1.16, a decrease of 25.00%

|

| - |

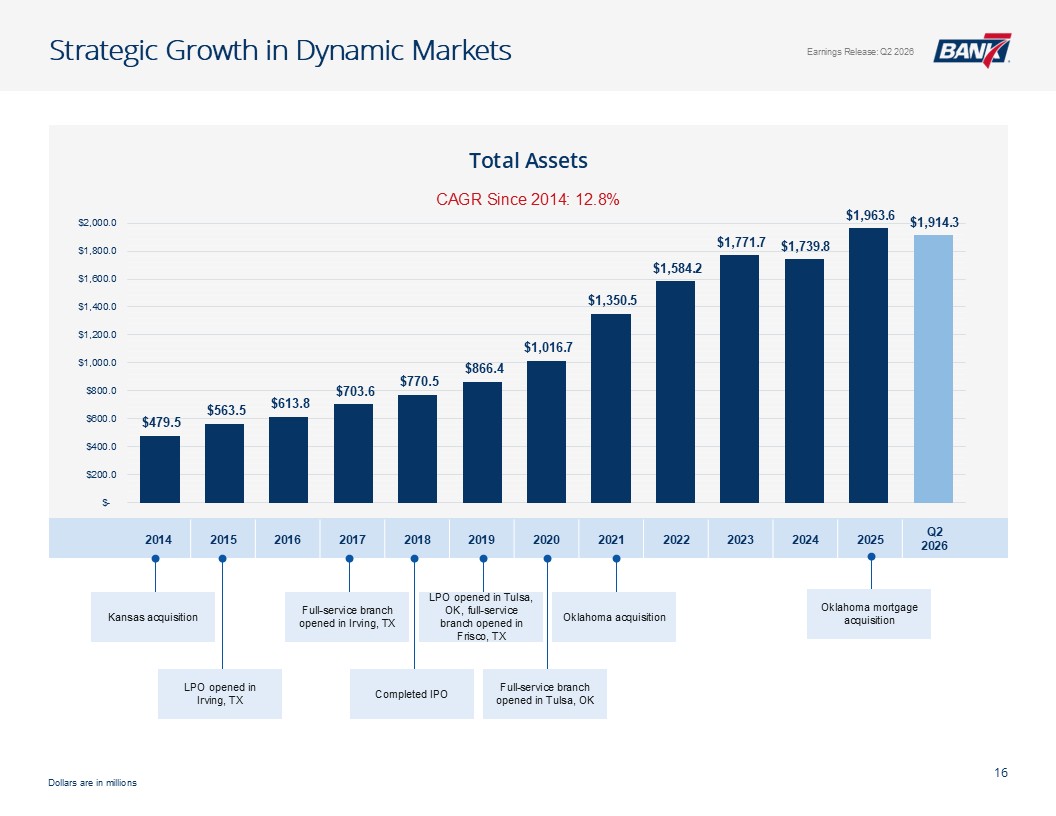

Total assets of $1.91 billion compared to $1.84 billion, an increase of 4.25%

|

| - |

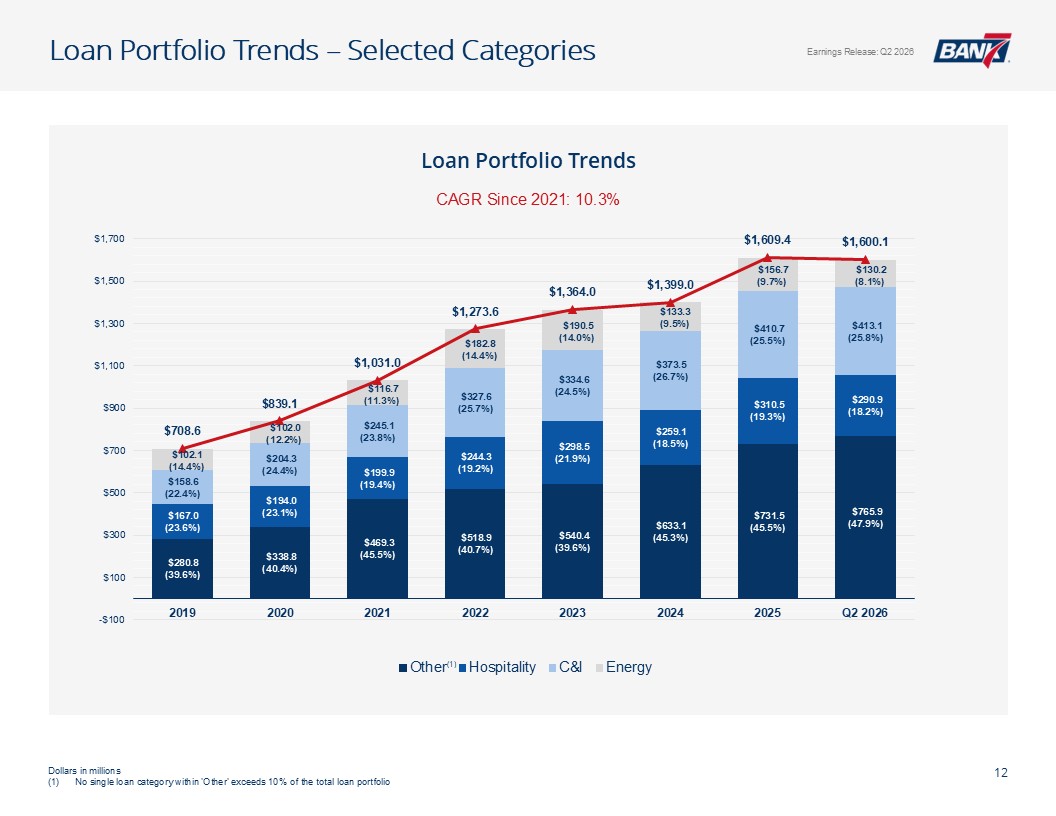

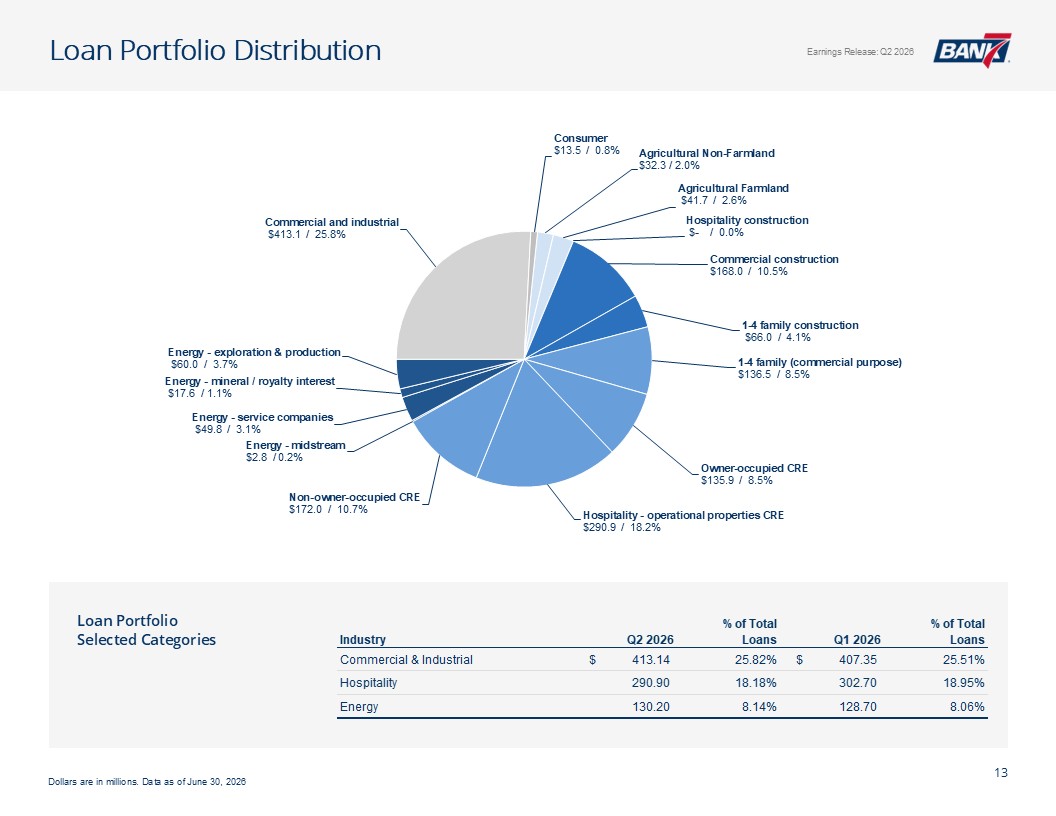

Total loans of $1.60 billion compared to $1.50 billion, an increase of 6.68%

|

| - |

Pre-provision pre-tax earnings of $11.02 million compared to $14.71 million, a decrease of 25.10%

|

| - |

Total interest income of $30.93 million compared to $31.78 million, a decrease of 2.69%

|

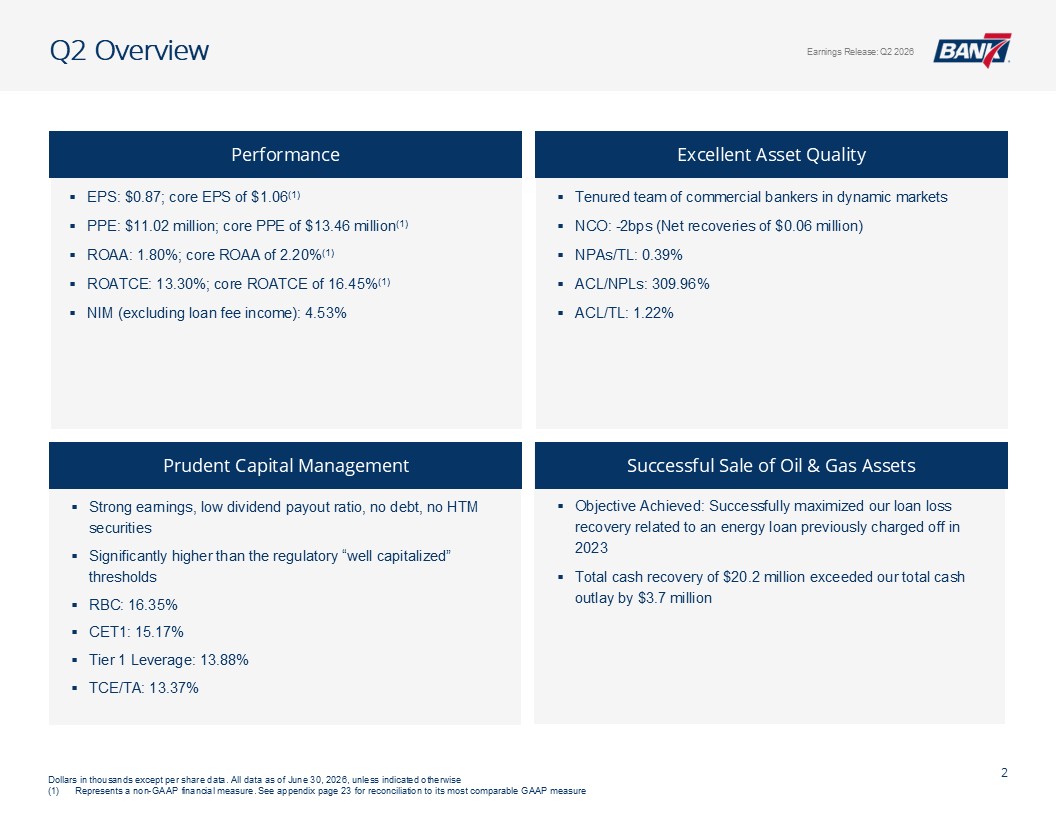

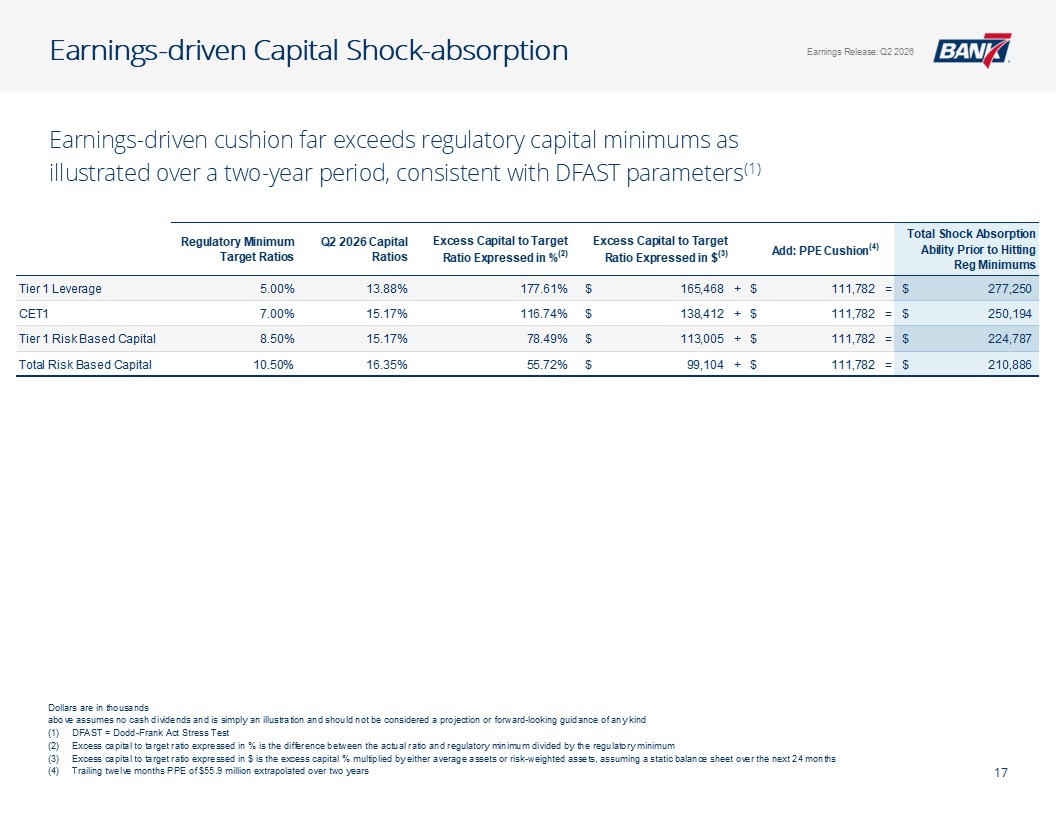

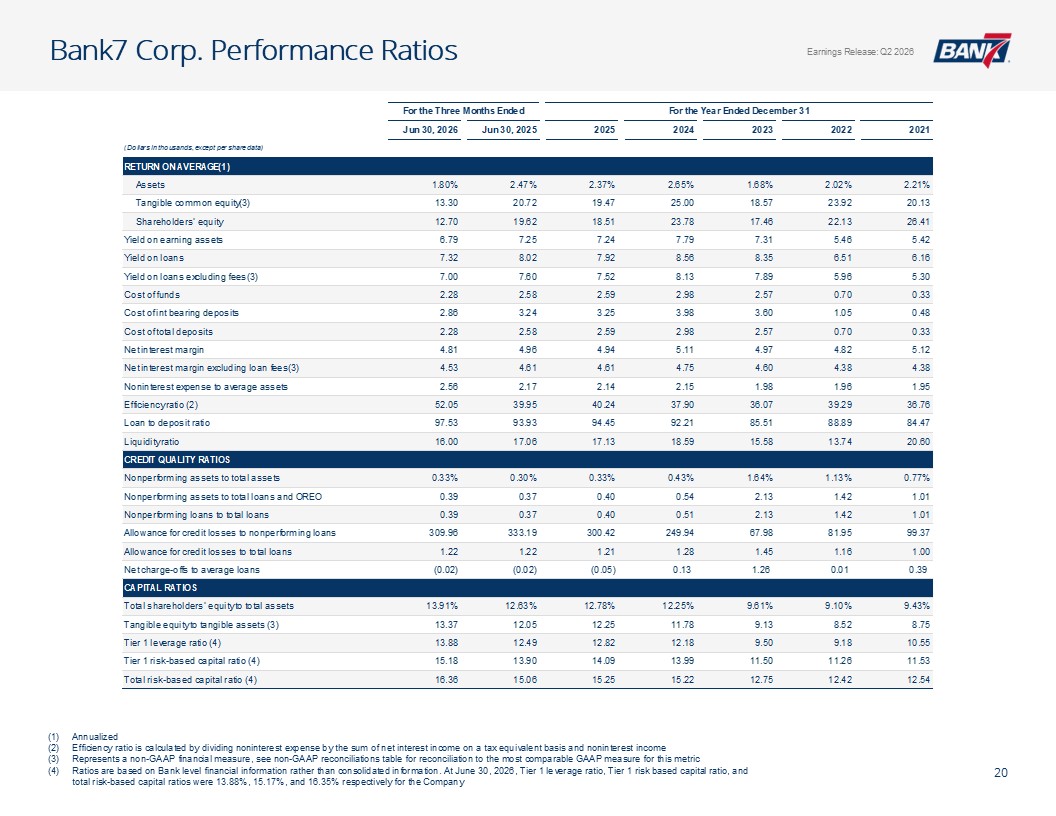

Both the Bank’s and the Company’s capital levels continue to be significantly above the minimum levels required to be designated as “well-capitalized” for regulatory purposes. On June 30, 2026, the Bank’s Tier 1

leverage ratio, Tier 1 risk-based capital ratio, and total risk-based capital ratios were 13.88%, 15.18%, and 16.36%, respectively. On June 30, 2026, on a consolidated basis, the Company’s Tier 1 leverage ratio, Tier 1 risk-based capital ratio,

and total risk-based capital ratios were 13.88%, 15.17%, and 16.35%, respectively. Designation as a well-capitalized institution under regulations does not constitute a recommendation or endorsement by bank regulators.

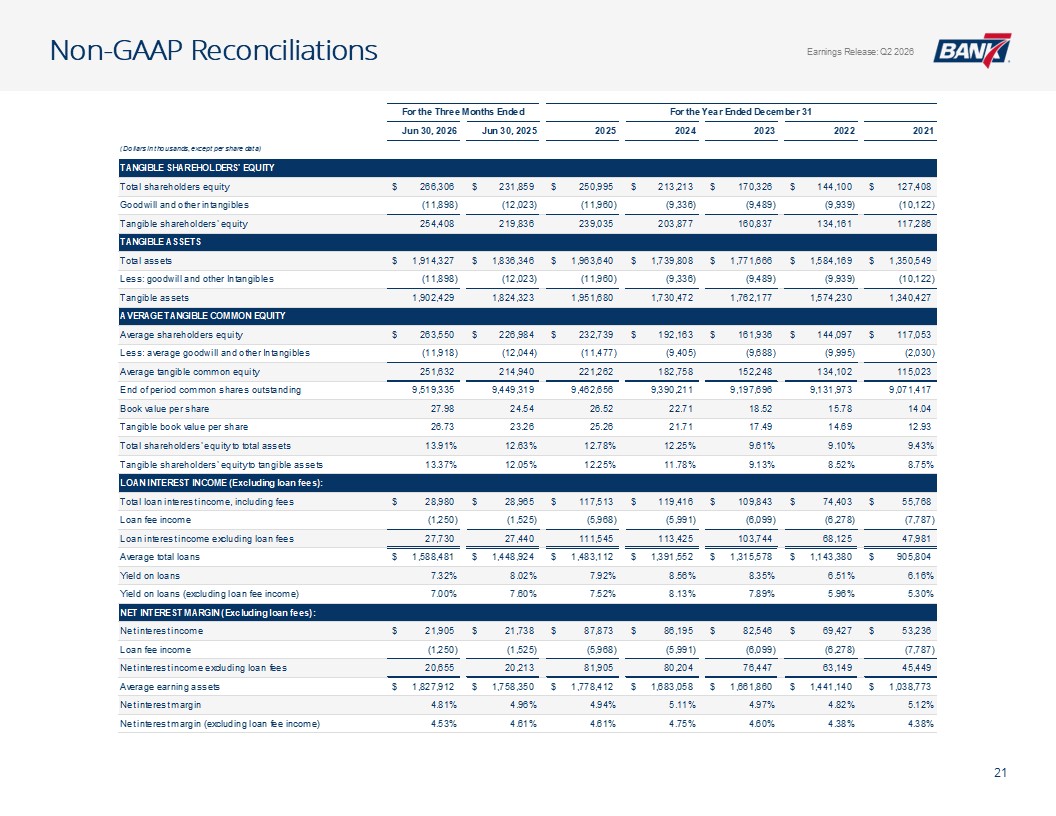

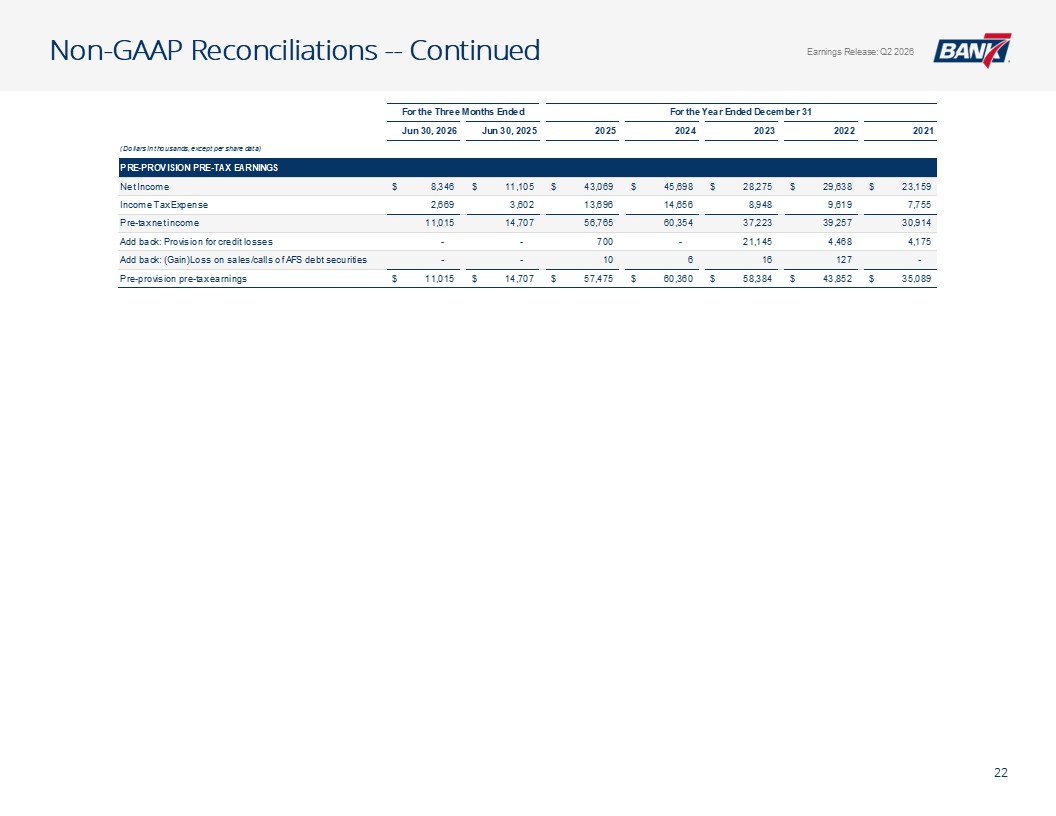

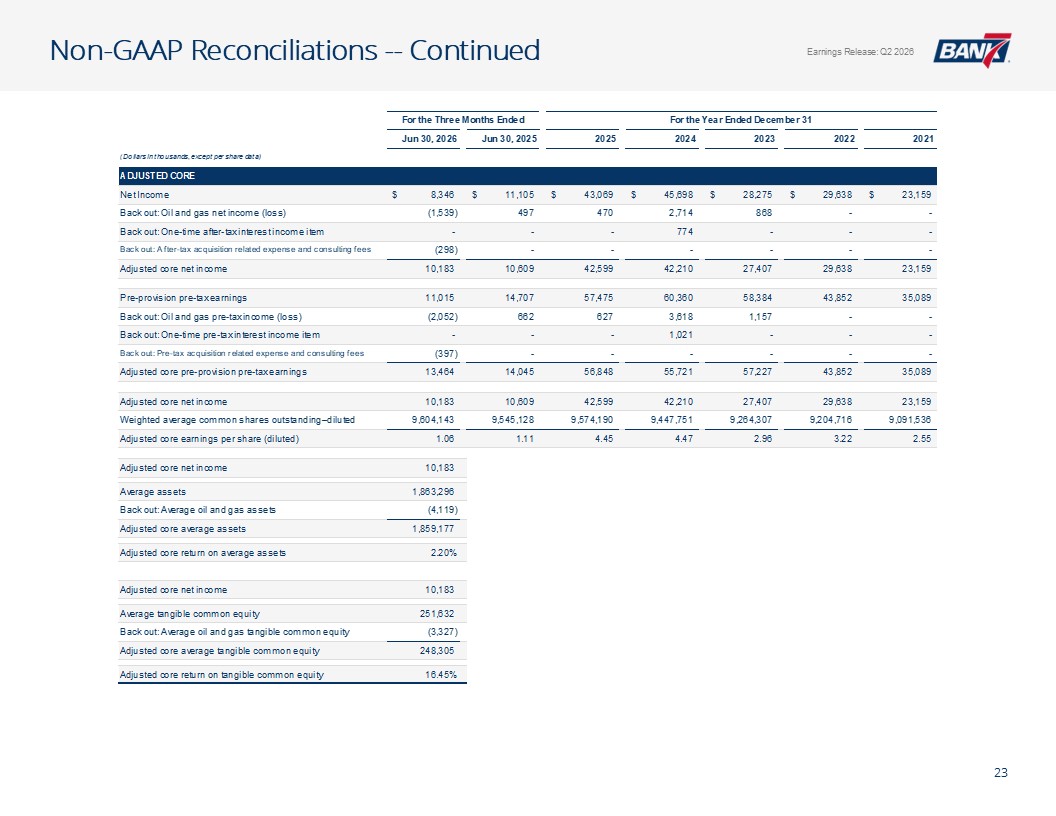

Non-GAAP Financial Measures:

This earnings release contains the non-GAAP financial measure pre-provision pre-tax earnings. The Company’s management uses this non-GAAP measure in their analysis of the Company’s performance. This measure adjusts

GAAP performance to exclude from net income, income tax expense, provision for credit losses, and loss on sales and calls of available-for-sale debt securities.

|

|

For the Three Months Ended

|

|||||||

|

|

June 30,

|

June 30,

|

||||||

|

|

2026

|

2025

|

||||||

|

Calculation of Pre-Provision Pre-Tax Earnings

|

(Dollars in thousands)

|

|||||||

|

Net Income

|

$

|

8,346

|

$

|

11,105

|

||||

|

Income Tax Expense

|

2,669

|

3,602

|

||||||

|

Pre-tax net income

|

11,015

|

14,707

|

||||||

|

Add back: Provision for credit losses

|

-

|

-

|

||||||

|

Add back: (Gain)Loss on sales/calls of AFS debt securities

|

-

|

-

|

||||||

|

Pre-provision pre-tax earnings

|

$

|

11,015

|

$

|

14,707

|

||||

Unaudited Condensed Consolidated Balance Sheets

(Dollar amounts in thousands, except par value)

(Dollar amounts in thousands, except par value)

|

Assets

|

June 30,

2026 (unaudited) |

December 31,

2025

|

||||||

|

|

(Dollars in thousands)

|

|||||||

|

Cash and due from banks

|

$

|

220,585

|

$

|

244,635

|

||||

|

Interest-bearing time deposits in other banks

|

1,494

|

10,457

|

||||||

|

Available-for-sale debt securities (amortized cost of $54,950 and $57,316 at June 30, 2026 and December 31, 2025, respectively)

|

51,622

|

54,019

|

||||||

|

Loans, net of allowance for credit losses of $19,512 and $19,407 at June 30, 2026 and December 31, 2025, respectively

|

1,577,838

|

1,587,024

|

||||||

|

Loans held for sale

|

5,156

|

2,078

|

||||||

|

Premises and equipment, net

|

25,897

|

21,884

|

||||||

|

Nonmarketable equity securities

|

1,183

|

1,165

|

||||||

|

Core deposit intangibles

|

690

|

752

|

||||||

|

Goodwill

|

11,208

|

11,208

|

||||||

|

Interest receivable and other assets

|

18,654

|

30,418

|

||||||

|

|

||||||||

|

Total assets

|

$

|

1,914,327

|

$

|

1,963,640

|

||||

|

|

||||||||

|

Liabilities and Shareholders’ Equity

|

||||||||

|

|

||||||||

|

Deposits

|

||||||||

|

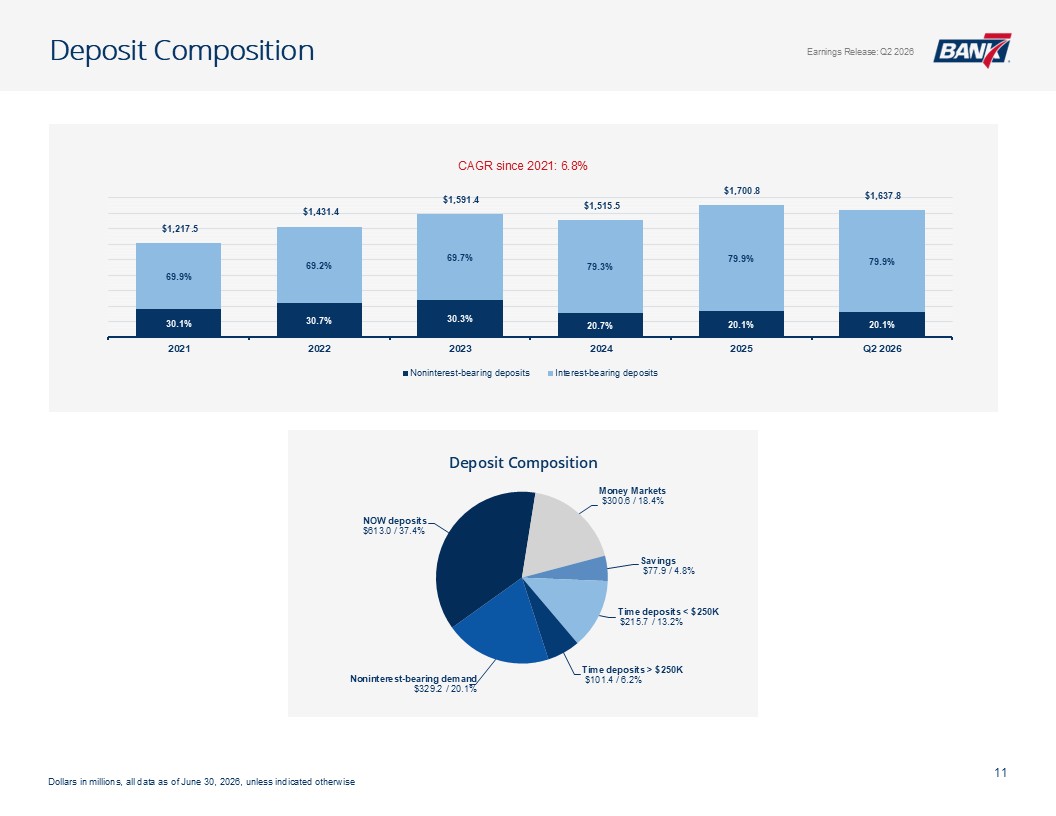

Noninterest-bearing

|

$

|

329,240

|

$

|

341,416

|

||||

|

Interest-bearing

|

1,308,563

|

1,359,417

|

||||||

|

|

||||||||

|

Total deposits

|

1,637,803

|

1,700,833

|

||||||

|

|

||||||||

|

Income taxes payable

|

839

|

594

|

||||||

|

Interest payable and other liabilities

|

9,379

|

11,218

|

||||||

|

|

||||||||

|

Total liabilities

|

1,648,021

|

1,712,645

|

||||||

|

|

||||||||

|

Shareholders’ equity

|

||||||||

|

Common stock, $0.01 par value; 50,000,000 shares authorized; shares issued and outstanding: 9,519,335 and 9,462,656 at June 30, 2026 and December 31, 2025, respectively

|

95

|

95

|

||||||

|

Additional paid-in capital

|

103,865

|

103,739

|

||||||

|

Retained earnings

|

164,919

|

149,707

|

||||||

|

Accumulated other comprehensive loss

|

(2,573

|

)

|

(2,546

|

)

|

||||

|

|

||||||||

|

Total shareholders’ equity

|

266,306

|

250,995

|

||||||

|

|

||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,914,327

|

$

|

1,963,640

|

||||

Unaudited Condensed Consolidated Statements of Comprehensive Income

(Dollar amounts in thousands, except per share data)

(Dollar amounts in thousands, except per share data)

|

|

Three Months Ended

|

Six Months Ended

|

||||||||||||||

|

|

June 30,

|

June 30,

|

||||||||||||||

|

|

2026

(unaudited) |

2025

(unaudited) |

2026

(unaudited) |

2025

(unaudited) |

||||||||||||

|

Interest Income

|

(Dollars in thousands)

|

|||||||||||||||

|

Loans, including fees

|

$

|

28,980

|

$

|

28,965

|

$

|

60,592

|

$

|

56,293

|

||||||||

|

Interest-bearing time deposits in other banks

|

38

|

145

|

150

|

246

|

||||||||||||

|

Debt securities, taxable

|

249

|

278

|

499

|

561

|

||||||||||||

|

Debt securities, tax-exempt

|

59

|

63

|

119

|

126

|

||||||||||||

|

Other interest and dividend income

|

1,601

|

2,330

|

3,350

|

4,997

|

||||||||||||

|

|

||||||||||||||||

|

Total interest income

|

30,927

|

31,781

|

64,710

|

62,223

|

||||||||||||

|

|

||||||||||||||||

|

Interest Expense

|

||||||||||||||||

|

Deposits

|

9,022

|

10,043

|

18,613

|

19,643

|

||||||||||||

|

|

||||||||||||||||

|

Total interest expense

|

9,022

|

10,043

|

18,613

|

19,643

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income

|

21,905

|

21,738

|

46,097

|

42,580

|

||||||||||||

|

|

||||||||||||||||

|

Provision for Credit Losses

|

-

|

-

|

-

|

-

|

||||||||||||

|

|

||||||||||||||||

|

Net Interest Income After Provision for Credit Losses

|

21,905

|

21,738

|

46,097

|

42,580

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Income

|

||||||||||||||||

|

Mortgage lending income

|

476

|

520

|

851

|

610

|

||||||||||||

|

Service charges on deposit accounts

|

215

|

232

|

464

|

450

|

||||||||||||

|

Other

|

311

|

1,949

|

1,653

|

3,396

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest income

|

1,002

|

2,701

|

2,968

|

4,456

|

||||||||||||

|

|

||||||||||||||||

|

Noninterest Expense

|

||||||||||||||||

|

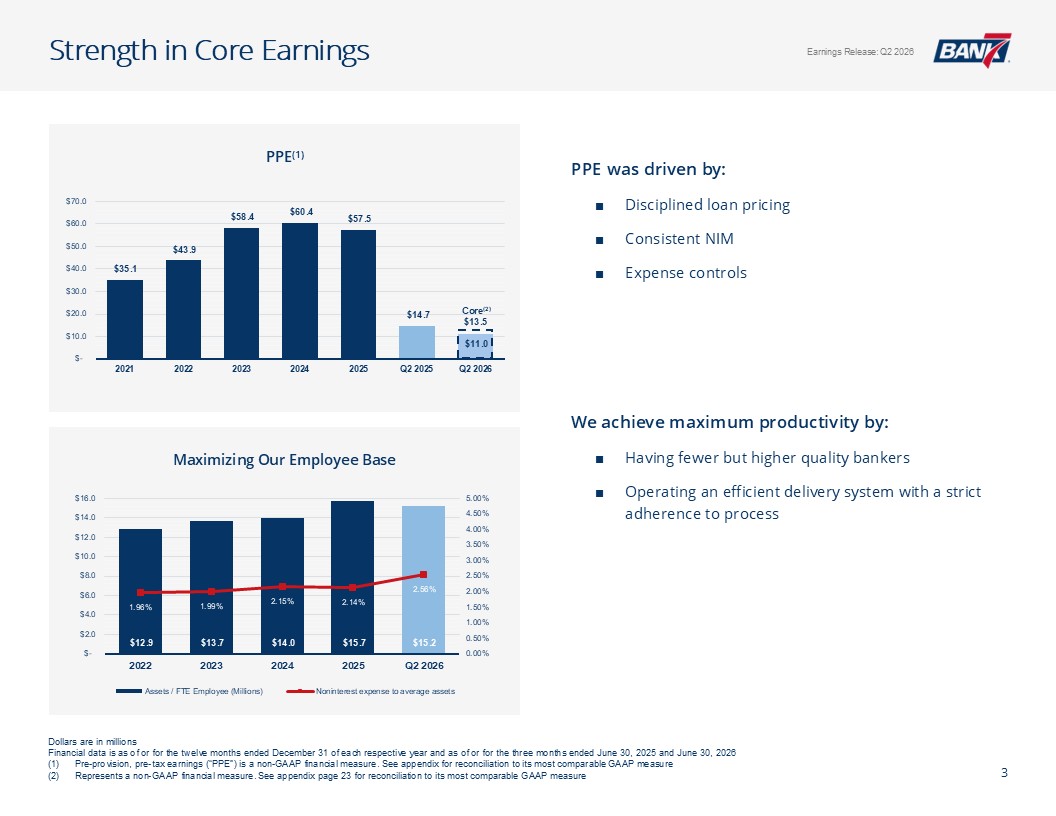

Salaries and employee benefits

|

6,196

|

5,721

|

12,527

|

11,000

|

||||||||||||

|

Furniture and equipment

|

422

|

361

|

763

|

612

|

||||||||||||

|

Occupancy

|

724

|

630

|

1,410

|

1,222

|

||||||||||||

|

Data and item processing

|

546

|

590

|

1,089

|

1,100

|

||||||||||||

|

Accounting, marketing and legal fees

|

437

|

158

|

1,022

|

263

|

||||||||||||

|

Regulatory assessments

|

259

|

213

|

518

|

297

|

||||||||||||

|

Advertising and public relations

|

98

|

223

|

270

|

417

|

||||||||||||

|

Travel, lodging and entertainment

|

104

|

121

|

174

|

177

|

||||||||||||

|

Other

|

3,106

|

1,715

|

4,456

|

3,528

|

||||||||||||

|

|

||||||||||||||||

|

Total noninterest expense

|

11,892

|

9,732

|

22,229

|

18,616

|

||||||||||||

|

|

||||||||||||||||

|

Income Before Taxes

|

11,015

|

14,707

|

26,836

|

28,420

|

||||||||||||

|

Income tax expense

|

2,669

|

3,602

|

6,484

|

6,979

|

||||||||||||

|

Net Income

|

$

|

8,346

|

$

|

11,105

|

$

|

20,352

|

$

|

21,441

|

||||||||

|

|

||||||||||||||||

|

Earnings per common share - basic

|

$

|

0.88

|

$

|

1.18

|

$

|

2.14

|

$

|

2.27

|

||||||||

|

Earnings per common share - diluted

|

0.87

|

1.16

|

2.12

|

2.25

|

||||||||||||

|

Weighted average common shares outstanding - basic

|

9,519,335

|

9,449,152

|

9,505,283

|

9,435,414

|

||||||||||||

|

Weighted average common shares outstanding - diluted

|

9,604,143

|

9,545,128

|

9,600,421

|

9,548,583

|

||||||||||||

|

|

||||||||||||||||

|

Other Comprehensive Income (Loss)

|

||||||||||||||||

|

Unrealized (losses) gains on securities, net of tax expense of $50 and $189 for the three months ended June 30, 2026 and 2025, respectively; net of tax (benefit) expense of ($5) and $419

for the six months ended June 30, 2026 and 2025, respectively

|

$

|

114

|

$

|

587

|

$

|

(27

|

)

|

$

|

1,229

|

|||||||

|

Other comprehensive income (loss)

|

$

|

114

|

$

|

587

|

$

|

(27

|

)

|

$

|

1,229

|

|||||||

|

Comprehensive Income

|

$

|

8,460

|

$

|

11,692

|

$

|

20,325

|

$

|

22,670

|

||||||||

|

|

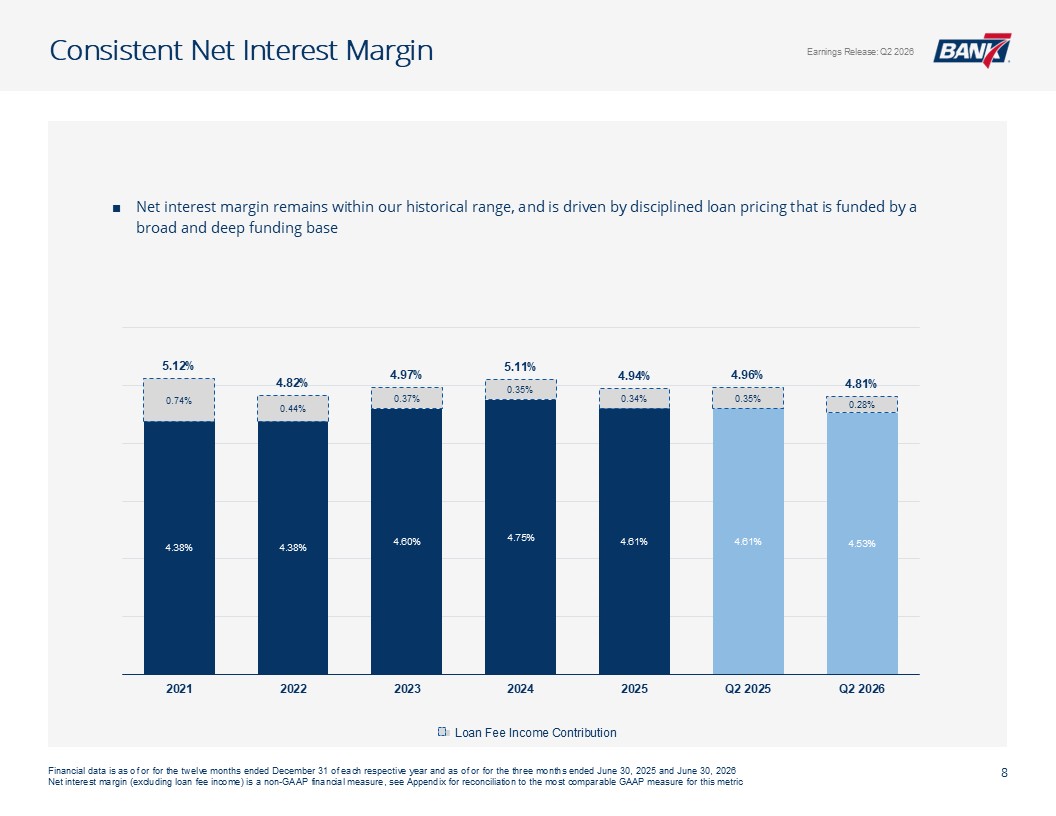

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Three Months Ended June 30,

|

|||||||||||||||||||||||

|

|

2026

(unaudited) |

2025

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

184,292

|

$

|

1,639

|

3.57

|

%

|

$

|

247,652

|

$

|

2,475

|

4.01

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

42,166

|

249

|

2.37

|

47,285

|

278

|

2.36

|

||||||||||||||||||

|

Debt securities, tax exempt

|

10,975

|

59

|

2.16

|

12,502

|

63

|

2.02

|

||||||||||||||||||

|

Loans held for sale

|

1,998

|

-

|

-

|

1,987

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,588,481

|

28,980

|

7.32

|

1,448,924

|

28,965

|

8.02

|

||||||||||||||||||

|

Total interest-earning assets

|

1,827,912

|

30,927

|

6.79

|

1,758,350

|

31,781

|

7.25

|

||||||||||||||||||

|

Noninterest-earning assets

|

35,384

|

43,048

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,863,296

|

$

|

1,801,398

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

1,003,124

|

$

|

6,721

|

2.69

|

%

|

$

|

1,006,484

|

$

|

7,676

|

3.06

|

%

|

||||||||||||

|

Time deposits

|

262,081

|

2,301

|

3.52

|

236,108

|

2,367

|

4.02

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,265,205

|

9,022

|

2.86

|

1,242,592

|

10,043

|

3.24

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

1,265,205

|

9,022

|

2.86

|

$

|

1,242,592

|

10,043

|

3.24

|

||||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

325,384

|

$

|

321,351

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

9,157

|

10,471

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

334,541

|

331,822

|

||||||||||||||||||||||

|

Shareholders' equity

|

263,550

|

226,984

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,863,296

|

$

|

1,801,398

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

21,905

|

$

|

21,738

|

||||||||||||||||||||

|

Net interest spread

|

3.93

|

%

|

4.01

|

%

|

||||||||||||||||||||

|

Net interest margin

|

4.81

|

%

|

4.96

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|

|

|

Net Interest Margin

|

|||||||||||||||||||||||

|

|

For the Six Months Ended June, 30

|

|||||||||||||||||||||||

|

|

2026

(unaudited) |

2025

(unaudited) |

||||||||||||||||||||||

|

|

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

Average

Balance |

Interest

Income/ Expense |

Average

Yield/ Rate |

||||||||||||||||||

|

|

(Dollars in thousands)

|

|||||||||||||||||||||||

|

Interest-Earning Assets:

|

||||||||||||||||||||||||

|

Short-term investments

|

$

|

197,098

|

$

|

3,500

|

3.58

|

%

|

$

|

242,876

|

$

|

5,243

|

4.35

|

%

|

||||||||||||

|

Debt securities, taxable-equivalent

|

42,861

|

499

|

2.35

|

47,957

|

561

|

2.36

|

||||||||||||||||||

|

Debt securities, tax exempt

|

11,013

|

119

|

2.18

|

12,508

|

126

|

2.03

|

||||||||||||||||||

|

Loans held for sale

|

1,991

|

-

|

-

|

1,287

|

-

|

-

|

||||||||||||||||||

|

Total loans(1)

|

1,592,320

|

60,592

|

7.67

|

1,423,776

|

56,293

|

7.97

|

||||||||||||||||||

|

Total interest-earning assets

|

1,845,283

|

64,710

|

7.07

|

1,728,404

|

62,223

|

7.26

|

||||||||||||||||||

|

Noninterest-earning assets

|

38,323

|

41,511

|

||||||||||||||||||||||

|

Total assets

|

$

|

1,883,606

|

$

|

1,769,915

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Funding sources:

|

||||||||||||||||||||||||

|

Interest-bearing liabilities:

|

||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||

|

Transaction accounts

|

$

|

1,030,802

|

$

|

13,944

|

2.73

|

%

|

$

|

981,833

|

$

|

14,794

|

3.04

|

%

|

||||||||||||

|

Time deposits

|

263,338

|

4,669

|

3.58

|

236,216

|

4,849

|

4.14

|

||||||||||||||||||

|

Total interest-bearing deposits

|

1,294,140

|

18,613

|

2.90

|

1,218,049

|

19,643

|

3.25

|

||||||||||||||||||

|

Total interest-bearing liabilities

|

$

|

1,294,140

|

$

|

18,613

|

2.90

|

$

|

1,218,049

|

$

|

19,643

|

3.25

|

||||||||||||||

|

|

||||||||||||||||||||||||

|

Noninterest-bearing liabilities:

|

||||||||||||||||||||||||

|

Noninterest-bearing deposits

|

$

|

320,326

|

$

|

318,952

|

||||||||||||||||||||

|

Other noninterest-bearing liabilities

|

9,335

|

10,228

|

||||||||||||||||||||||

|

Total noninterest-bearing liabilities

|

329,661

|

329,180

|

||||||||||||||||||||||

|

Shareholders' equity

|

259,805

|

222,686

|

||||||||||||||||||||||

|

Total liabilities and shareholders' equity

|

$

|

1,883,606

|

$

|

1,769,915

|

||||||||||||||||||||

|

|

||||||||||||||||||||||||

|

Net interest income

|

$

|

46,097

|

$

|

42,580

|

||||||||||||||||||||

|

Net interest spread

|

4.17

|

%

|

4.01

|

%

|

||||||||||||||||||||

|

Net interest margin

|

5.04

|

%

|

4.97

|

%

|

||||||||||||||||||||

|

(1)

|

Nonaccrual loans are included in total loans

|

About Bank7 Corp.

We are Bank7 Corp., a bank holding company headquartered in Oklahoma City, Oklahoma. Through our wholly-owned subsidiary, Bank7, we operate twelve locations in Oklahoma, the Dallas/Fort Worth,

Texas metropolitan area and Kansas. We are focused on serving business owners and entrepreneurs by delivering fast, consistent and well-designed loan and deposit products to meet their financing needs. We intend to grow organically by selectively

opening additional branches in our target markets as well as pursue strategic acquisitions.

Conference Call

Bank7 Corp. has scheduled a conference call to discuss its first quarter results, which will be broadcast live over the Internet, on Thursday, July 16, 2026 at 10:00 a.m. central standard time. To participate in the

call, dial 1-888-348-6421, or access it live over the Internet at https://app.webinar.net/ZB5xN3Bnq1w. For those not able to participate in the live call, an archive of the webcast will be

available at https://app.webinar.net/ZB5xN3Bnq1w shortly after the call for 1 year.

Cautionary Statements Regarding Forward-Looking Information

This communication contains a number of forward-looking statements. These forward-looking statements reflect Bank7 Corp.’s current views with respect to, among other things, future events and Bank7 Corp.’s financial

performance. Any statements about Bank7 Corp.’s expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not

always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends” and similar words or

phrases. Any or all of the forward-looking statements in (or conveyed orally regarding) this presentation may turn out to be inaccurate. The inclusion of or reference to forward-looking information in this presentation should not be regarded as a

representation by Bank7 Corp. or any other person that the future plans, estimates or expectations contemplated by Bank7 Corp. will be achieved.

These forward-looking statements are subject to significant uncertainties because they are based upon: the amount and timing of future changes in interest rates, market behavior, and other economic conditions;

future laws, regulations, and accounting principles; changes in regulatory standards and examination policies, and a variety of other matters. These other matters include, among other things, the impact the direct and indirect effect of economic

conditions on interest rates, credit quality, loan demand, liquidity, and monetary and supervisory policies of banking regulators. Bank7 Corp. has based these forward-looking statements largely on its current expectations and projections about

future events and financial trends that Bank7 Corp. believes may affect its financial condition, results of operations, business strategy and financial needs. Bank7 Corp.’s actual results could differ materially from those anticipated in such

forward-looking statements as a result of risks, uncertainties and assumptions that are difficult to predict. If one or more events related to these or other risks or uncertainties materialize, or if Bank7 Corp.’s underlying assumptions prove to be

incorrect, actual results may differ materially from what Bank7 Corp. anticipates. You are cautioned not to place undue reliance on forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made

and Bank7 Corp. undertakes no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as may be

required by law. All forward-looking statements herein are qualified by these cautionary statements.

Contact:

Thomas Travis

President & CEO

(405) 810-8600