btbd_8k.htm0001718224false00017182242025-12-012025-12-010001718224btbd:CommonStocksMember2025-12-012025-12-010001718224btbd:WarrantsMember2025-12-012025-12-01iso4217:USDxbrli:sharesiso4217:USDxbrli:shares

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): December 1, 2025

BT BRANDS, INC. |

(Exact name of registrant as specified in its charter) |

Wyoming | | 000-56113 | | 91-1495764 |

(State or other jurisdiction of incorporation) | | (Commission File Number) | | (IRS Employer Identification No.) |

10501 Wayzata Blvd South, Suite 102, Minnetonka, MN | | 55305 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (307) 274-3055

(Former name or former address, if changed since last report.)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

☒ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425). |

☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12). |

☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)). |

☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)). |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Common Stock | | BTBD | | Nasdaq Capital Market |

Warrants | | BTBDW | | Nasdaq Capital Market |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 8.01 Other Events.

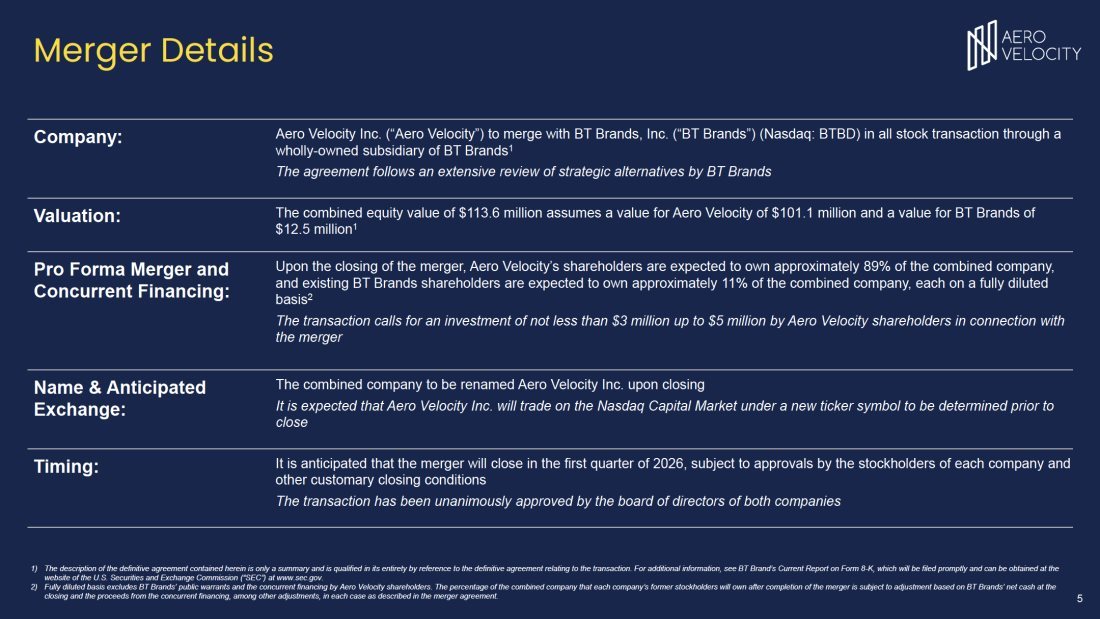

As previously reported in our Current Report on Form 8-K filed with the Securities and Exchange Commission on September 3, 2025, BT Brands, Inc. ( “BT Brands”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) among BT Brands, Aero Merger Sub Inc., a Delaware corporation and a direct, wholly owned subsidiary of Parent (“Merger Sub”), and Aero Velocity Inc., a Delaware corporation (“Aero Velocity”, “Aero” or the “Company”). The Merger Agreement contemplates that prior to closing of the transactions contemplated thereby, BT Brands shall complete a restructuring pursuant to which it will form a wholly-owned Wyoming subsidiary (“BT Group”), to which it will transfer all of its assets and liabilities. It is then contemplated that BT Brands will distribute the shares of BT Group held by it to BT Brands' common stockholders (the “Spin-Off”). It is contemplated that in connection with the Spin-Off, BT Group would pursue a listing for its common stock. If deemed required under the Warrant Agreement governing BT Brands’ outstanding public warrants, the exercise price of such warrants will be adjusted to reflect the value of the distribution of BT Group to BT Brands’ common stockholders.

BT Brands is filing this Current Report on Form 8-K to provide the following:

| · | A narrative discussion relating to the business of Aero as set both below; |

| | |

| · | Audited abbreviated financial statements of Aero as of June 5, 2024 and December 31, 2023 and for the periods ended June 5, 2024 and the six months ended December 31, 2023 attached as Exhibit 99.1; |

| | |

| · | Audited financial statements of Aero as of December 31, 2024 and for the period from June 6, 2024 to December 31, 2024 attached hereto as Exhibit 99.2; |

| | |

| · | The historical unaudited financial statements of Aero Velocity, Inc. for the three and nine months ended September 30, 2025 and the related notes thereto attached hereto as Exhibit 99.3. |

| | |

| · | Unaudited pro forma condensed combined financial statements of BT Brands and Aero and accompanying notes thereto presenting the unaudited pro forma condensed combined balance sheets as of September 30, 2025 and the unaudited pro forma condensed combined statements of operations as of and for the nine months ended September 30, 2025 and for the year ended December 31, 2024 attached hereto as Exhibit 99.4; |

| | |

| · | The consent of Boulay PLLP, independent registered public accounting firm of BT Brands, to the incorporation by reference into BT Brands registration statement on Form S-3 (No. 333-333-283830) (the “Registration Statement”) of its report dated March 31, 2025 with respect to the consolidated financial statements of BT Brands, Inc. on Form 10-K for the year ended December 29, 2024; |

| | |

| · | The consent of Barton CPA PLLC, independent registered public accounting firm of Aero, to the incorporation by reference into the Registration Statement of its report dated August 27, 2025 with respect to Aero’s abbreviated financial statements which comprise the statements of assets acquired and liabilities assumed as of June 5, 2024 and December 31, 2023, the related statements of revenues and direct expenses for the period from January 1, 2024 to June 5, 2024 and for the six months ended December 31, 2023, and the related notes to the abbreviated financial statements and Aero’s financial statements which are comprised of a balance sheet as of December 31, 2024 and the related statement of operations, stockholders’ deficit and cash flows for the year then ended and the related notes; and |

| | |

| · | An updated corporate investor deck of Aero attached hereto as Exhibit 99.5. |

Description of the Business of Aero

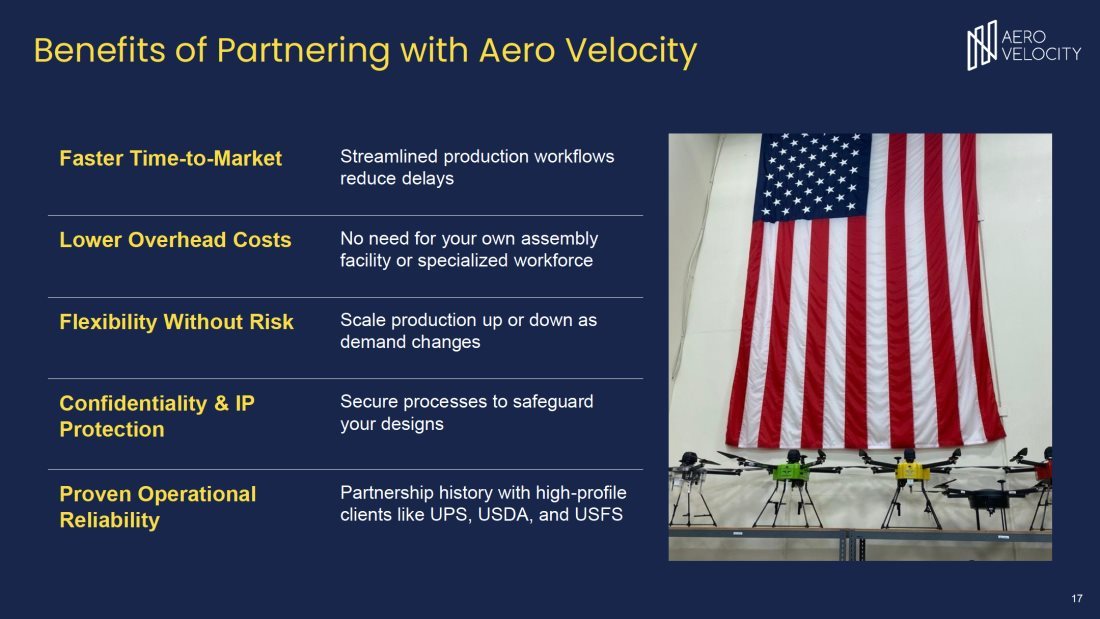

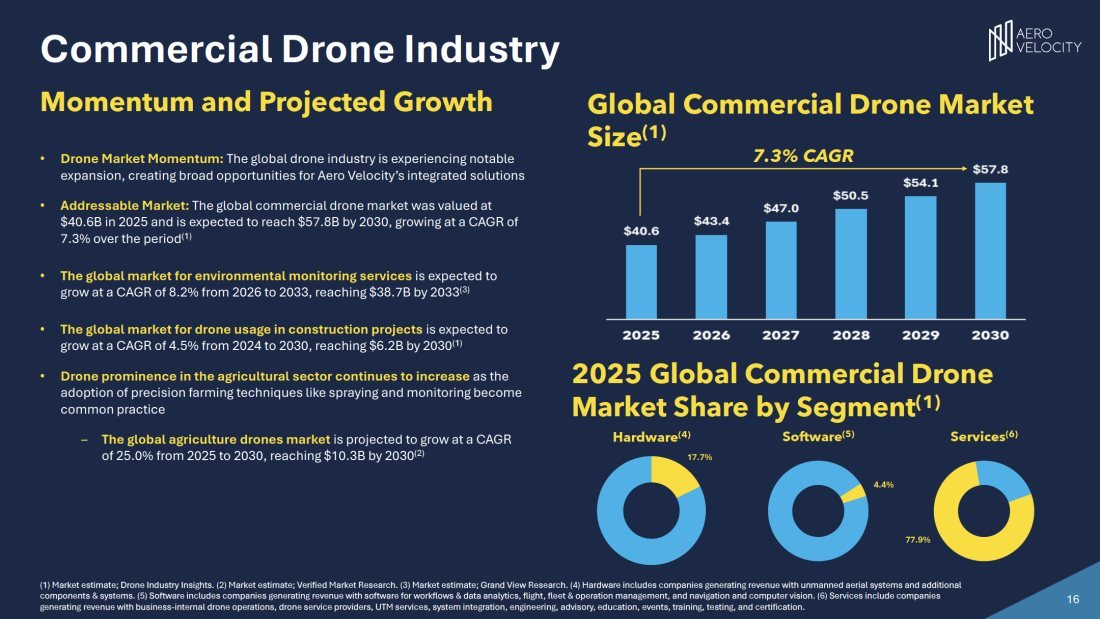

Aero Velocity delivers drone-based services, technologies, and manufacturing solutions that address critical needs worldwide across multiple industries, including agriculture, forestry, infrastructure, oil and gas, and environmental management. Through organic growth, innovation and targeted bolt-on acquisitions, Aero Velocity seeks to position itself at the forefront of the rapidly evolving drone industry. Aero is committed to being a multi-faceted leader at the intersection of drone-powered services and asset intelligence, delivering solutions that enhance operational efficiency, safety, and sustainability. Aero’s guiding vision — Propelling Progress — reflects its dedication to advancing the industry while supporting the success of its clients.

Aero Velocity operates as a fully integrated drone and drone services company, combining direct service delivery with in-house technology development and manufacturing. Aero’s approach allows it to rapidly design, deploy and scale solutions that meet the needs of both high-volume commercial operations and specialized government projects.

The Company maintains internal capabilities in unmanned aircraft systems (“UAS”) operations, systems integration, sensor deployment, and data analytics. Aero also partners with leading suppliers in the U.S. and allied countries to ensure security, performance, and compliance with domestic manufacturing standards.

Aero’s operations integrate flight services, proprietary technology, and advanced manufacturing to provide comprehensive solutions in commercial and government markets. The Company’s diversified Drone-as-a-Service (“DaaS”) portfolio, consisting of five business units — CleanSweep, TankVision, TerraVision, SiteSnap and HeatScope — address specialized needs including exterior asset cleaning, internal tank inspections, land mapping and multispectral analytics, 3D modeling/digital twinning and artificial intelligence (“AI”)-powered asset management, and thermal imaging for energy efficiency and safety. Aero Velocity’s businesses position the Company as both a service provider and a technology innovator, with capabilities spanning government contracting, commercial infrastructure solutions, and contract manufacturing/engineering.

Company DaaS Solutions

Aero Velocity currently generates revenue primarily from offering DaaS solutions for government and civilian agencies.

Aero Velocity’s DaaS solutions are currently organized into five business segments:

| · | CleanSweep – Drone-based exterior cleaning for building facades, windows, and other assets, improving safety, reducing costs, and minimizing downtime for high-rise and mid-rise structures. |

| · | TankVision – Internal tank inspection services utilizing drone-based imaging and sensor packages to eliminate confined-space entry risks and deliver actionable asset condition data. |

| | |

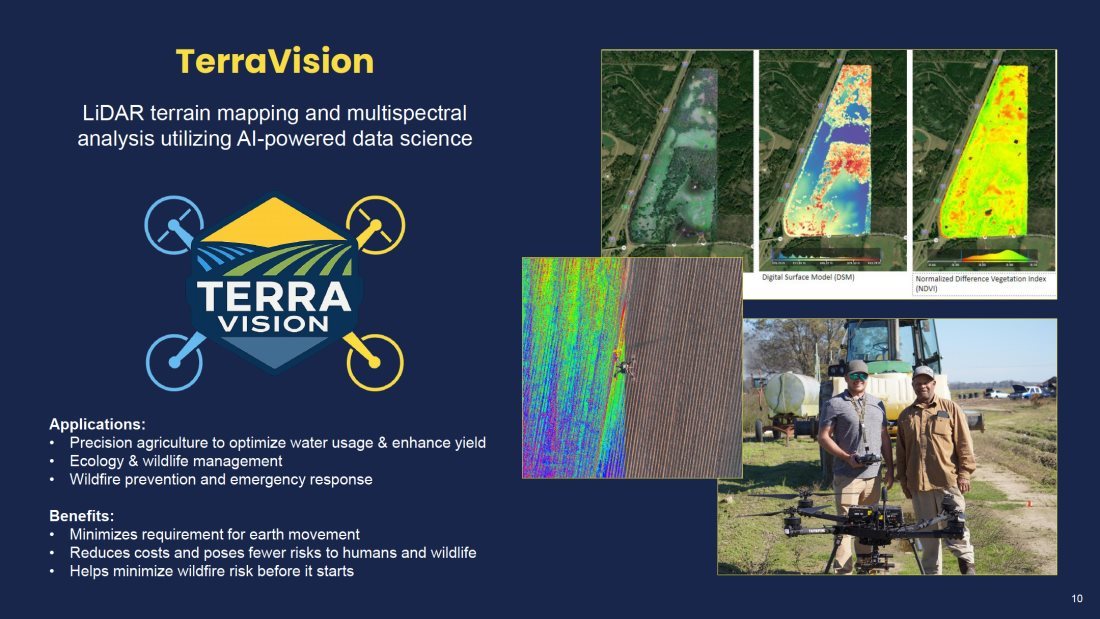

| · | TerraVision – LiDAR capture, multispectral imaging, and AI-powered data science to support disaster management, agriculture, forestry, and environmental protection applications. |

| | |

| · | SiteSnap – 3D modeling, digital twin creation, and AI-powered monitoring of critical infrastructure for lifecycle asset management and predictive maintenance. |

| | |

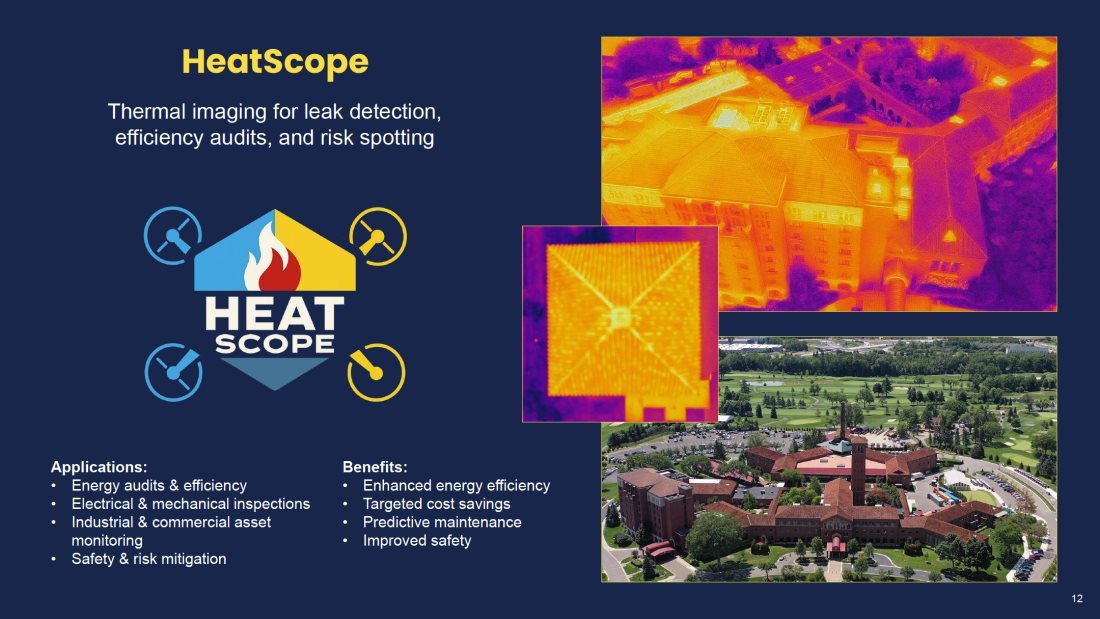

| · | HeatScope– Thermal imaging and analytics to identify energy loss, detect faults, and improve safety in industrial and commercial operations. |

In addition to these business lines, Aero Velocity engages in and is pursuing additional opportunities in contract manufacturing and engineering services for unmanned aerial systems and related technologies.

Contract Drone Manufacturing/Maintenance

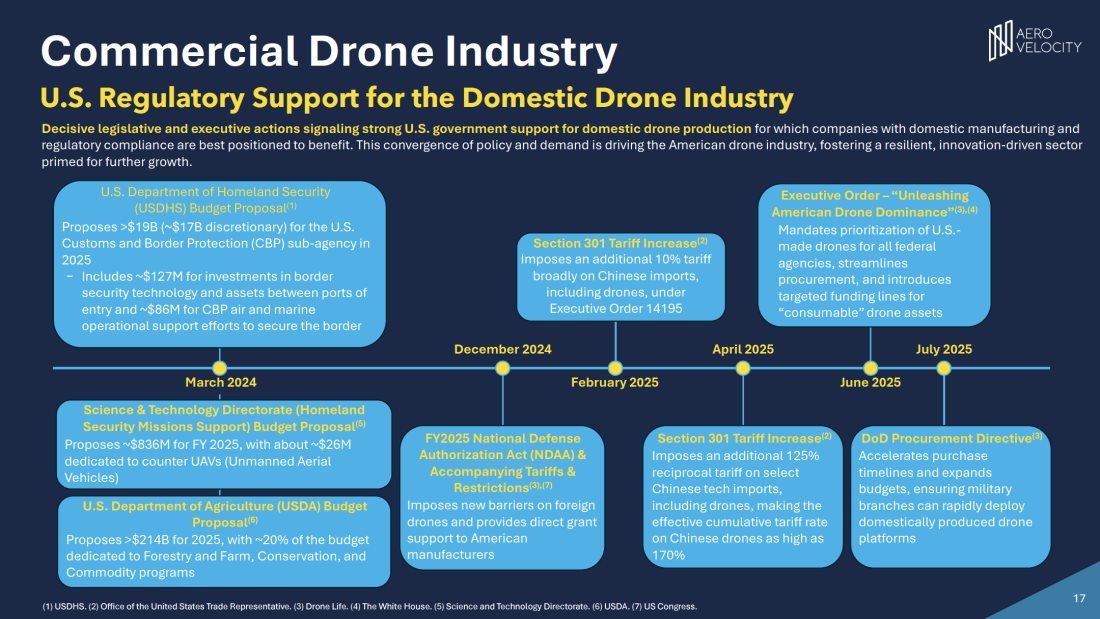

Aero Velocity is currently negotiating with several U.S. and non-U.S. based drone original equipment manufacturers (“OEMs”) regarding establishing contract manufacturing/assembly partnerships whereby Aero would serve as the U.S.-based builder of these drones. Although not assured, Aero Velocity believes it could reach agreements for this business as early as the end of 2025. Aero further believes it is well-positioned to enter the drone manufacturing business, given its long history of drone design, manufacturing, and maintenance capabilities, and its built-for-purpose drone assembly line. In addition, the recent executive “Unleashing American Drone Dominance” from Washington is putting increased emphasis on U.S.-based UAS manufacturing and has resulted in heightened interest from potential partners. Further, Aero’s operations, which are centrally located in Ohio, position it favorably from a distribution standpoint.

Markets and Customers

Aero Velocity serves a diverse array of industries, with a particular emphasis on the federal/defense and commercial sectors. Aero’s clients include federal and local governmental agencies, including the military, enterprises, and operators in:

| · | Government & Defense – Federal contracting for inspection, mapping, and tactical support missions. |

| | |

| · | Infrastructure & Utilities – Powerline, pipeline, bridge, and critical infrastructure inspection and management. |

| | |

| · | Agriculture & Forestry – Precision agriculture, crop health monitoring, and forestry management using advanced aerial imaging. |

| | |

| · | Oil & Gas – Inspection of assets, leak detection, and safety compliance monitoring. |

| | |

| · | Commercial & Industrial – Asset cleaning, facility optimization, and operational risk reduction. |

Competitive Strengths

Aero Velocity believes its competitive advantages include:

| · | Diversified Capabilities Across Five Businesses – A service suite that addresses multiple market needs from cleaning and inspections to mapping and analytics. |

| | |

| · | Hybrid Business Model – Combining service delivery, technology innovation, and manufacturing under one brand. |

| | |

| · | Made-in-USA Commitment – Domestic manufacturing and sourcing for security, quality, and compliance with U.S. regulations. |

| | |

| · | Government Contracting Experience – A history of successful federal contract fulfillment and established relationships and compliance processes to serve federal agencies and defense clients. |

| | |

| · | Scalable Growth Strategy – Active pursuit of acquisitions to expand capacity, enter new markets, and enhance technological leadership. |

Government Regulation

Aero Velocity is subject to industry-specific regulations governing the operation of UAS. In the United States, its activities are regulated by the Federal Aviation Administration (“FAA”), which oversees the use of the U.S. National Airspace System (“NAS”) for all air vehicles, including small UAS (“sUAS”).

In August 2016, the FAA’s final rules for the routine commercial use of certain small, unmanned aircraft systems (sUAS) weighing less than 55 pounds became effective. These rules establish safety and operational requirements for non-recreational flight, generally mandating visual line-of-sight operations during daylight hours or during twilight with anti-collision lighting, and imposing restrictions on altitude, airspeed, and proximity to persons not directly involved in the operation. The regulations also require aircraft registration, operator certification, marking requirements, and adherence to operational limitations, including prohibitions on flights over unprotected individuals absent specific authorization.

Aero Velocity operates under FAA Part 107 regulations employing a team of certified remote pilots who comply with all applicable operational requirements. For missions requiring Operations Over People (“OOP”), Over Moving Vehicles, Beyond Visual Line of Sight, or at night, the Company either obtains the necessary FAA waivers or deploys aircraft that are compliant with the applicable FAA operational categories. Aero Velocity’s fleet includes aircraft that are compliant with the National Defense Authorization Act, ensuring eligibility for federal procurement and adherence to U.S. national security requirements.

In April 2021, the FAA’s final rule for Remote Identification (“Remote ID”) of UAS became effective, alongside updated provisions for operations of sUAS over people. These rules permit certain categories of routine operations over people, moving vehicles, and at night, provided that the aircraft and operation meet specified technical and safety standards. Aero Velocity ensures that all deployed aircraft and flight operations are Remote ID compliant in accordance with applicable FAA deadlines.

In addition to U.S. regulations, Aero’s international operations are subject to the aviation laws and regulatory requirements of the foreign jurisdictions in which we operate. Such laws may, in some cases, be more stringent than U.S. regulations, particularly with respect to airspace access, equipment certification, and operational approvals. Aero Velocity maintains compliance through active regulatory monitoring, operator training, and fleet configuration tailored to the specific requirements of each jurisdiction.

Research and Development

Aero Velocity has historically devoted significant resources to the design and development of UAS for manufacturing and deployment in both commercial and defense markets. Aero continues to invest in advancing its platforms, with a particular emphasis on incorporating AI and machine learning technologies to enhance mission execution, data analysis, and operational efficiency.

Current research and development initiatives include the application of machine learning algorithms within inspection and monitoring workflows, the development of automated fault detection and predictive maintenance capabilities, as well as advancements in imaging technologies and flight performance. The Company is also creating AI- and machine learning–based analytical solutions for use by its Data Science and Engineering teams, enabling faster, more accurate interpretation of aerial data and improved decision-making for customers. These efforts are intended to maintain Aero Velocity’s competitive position, expand its technical capabilities, and address the evolving requirements of its government and commercial client base.

Intellectual Property

Aero Velocity invests in the protection and development of its intellectual property portfolio, including proprietary processes, designs, and trade secrets related to unmanned aerial systems, data analytics, and drone-powered service delivery. Aero maintains confidentiality agreements with employees, partners, and clients to safeguard its competitive position.

Aero Velocity maintains access to and benefits from a portfolio of patents, trademarks, software, and other intellectual property assets originating from its predecessor operations and technology partnerships. This intellectual property supports the Company’s service lines, enhances operational efficiency, and strengthens competitive positioning in both commercial and federal markets.

Patents –The Company’s portfolio includes U.S. and international patents providing protection for key innovations in unmanned aerial systems. These protections extend across the United States, Canada, Europe, and Mexico, with several applications pending. Core patent families include:

| · | Flying Vehicle Systems and Methods – These patents cover aerodynamic designs, propulsion systems, navigation architectures, and operational control methods for UAVs, supporting safe, efficient, and reliable flight performance. |

| | |

| · | Unmanned Aerial Vehicle Delivery Systems –These patents protect systems and methods for autonomous and semi-autonomous payload delivery, including vehicle-to-drone transfer mechanisms, secure payload housing, navigation protocols for last-mile delivery, and integrated control logic for mission execution. |

| | |

| · | Automated Multi-Copter UAS/UAV Dispatch from Vehicle –These patents cover apparatus, systems, and methods for launching and recovering multi-copter drones from ground vehicles, enabling mobile deployment, mission readiness, and coordinated fleet operations. |

The Company believes that its patents, together with ongoing development activities, reinforce Aero Velocity’s competitive position in both commercial and defense markets by protecting mission-critical technologies in UAV design, payload handling, and operational integration.

Trademarks – Aero Velocity’s registered trademarks include HORSEFLY®, covering civilian drones and package delivery systems; SQUADRON™, which applies to UAV mission management software and mobile applications; and Liberty Drones™, covering drone-based exterior cleaning and related aerial asset services. The Company also utilizes unregistered brand identifiers and imagery tied to its historical Workhorse Aero branding.

Domain Names – The Company controls relevant domain names supporting brand presence and market visibility, including workhorsedrones.com, workhorseuav.com, libertybelldrones.com, daaset.com, tankvzn.com, and droneservicesonline.com.

Software Assets – Proprietary software includes the MetronAir / Squadron software suite for UAV mission planning, control, video streaming, and route optimization; DaaS operational tools for data processing and system monitoring; and the Falcon Delivery System UAV control application, deployed on Skynode companion computers.

Health, Safety and Environment (HSE)

Aero Velocity maintains policies and procedures to protect the health and safety of our employees, clients, and the communities we serve. The Company is committed to operating in compliance with all applicable environmental regulations and industry best practices, and to continuously improving its HSE performance.

Aero Velocity is an Equal Opportunity Employer, fostering a safe and respectful workplace for all employees.

Human Capital Resources

As of October 1, 2025, Aero employed 17 full-time employees, two part-time employees, and seven full-time “inside” contract personnel. The Company believes its employees are among its most valued assets and are the driving force behind success. For this reason, Aero aspires to be an employer of choice, recognized for cultivating a positive and welcoming work environment, fostering personal and professional growth, and providing a safe work environment.

In addition to its team members, Aero utilizes an extensive and valued network of “outside” contractors and strategic partners numbering in the hundreds of professionals. Each contractor and partner is held to the same high standards as the Company’s employees and is thoroughly vetted and insured. This extended workforce enables Aero Velocity to deliver projects at scale, expand its operational reach, and maintain flexibility in meeting the diverse needs of its government and commercial clients.

To support these objectives, Aero’s human resources programs are designed to develop talent to prepare individuals for critical roles and leadership positions for the future; reward and support employees through competitive pay, benefits, and perquisite programs; enhance the Company’s culture through initiatives aimed at making the workplace more engaging; acquire talent and facilitate internal talent mobility to create a high-performing workforce; engage employees as brand ambassadors of the Company’s products; and continually invest in technology, tools, and resources to enable employees to perform at the highest level.

Company History

Aero Velocity was formed as a result of the purchase of drone business assets from Workhorse Group, Inc. (“Workhorse”) in June 2024. Prior to the sale of assets to Aero, Workhorse operated the business for nearly a decade as Workhorse Aero, designing, developing and manufacturing delivery drones for various customers in the package delivery business. Aero completed the asset purchase from Workhorse on June 6, 2024. In 2025, Aero Velocity acquired Liberty Drones, a pioneering provider of drone-based exterior cleaning services.

Aero Corporate Headquarters

Aero’s principal executive offices are located at 3600 Park 42 Drive, Cincinnati, Ohio 45241. Its telephone number is 513-224-4439, and its website address is www.aerovelocity.com. The information that is contained in, or that can be accessed through, the Company’s website is not incorporated into this report. Aero’s website address is provided solely for reference purposes.

Cautionary Statement Regarding Forward-Looking Statements

This Current Report on Form 8-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including, without limitation, statements regarding the anticipated timing of the consummation of the proposed transaction. Forward-looking statements provide current expectations of future events based on certain assumptions and include any statement that does not directly relate to any historical or current fact. Forward-looking statements can also be identified by words such as “anticipates,” “believes,” “plans,” “expects,” “future,” “intends,” “may,” “will,” “would,” “could,” “should,” “estimates,” “predicts,” “potential,” “continues,” “target,” “outlook” and similar terms and expressions, but the absence of these words does not mean that the statement is not forward-looking. These forward-looking statements include, but are not limited to, statements regarding Aero’s industry and market sizes, future opportunities for Aero, Aero’s estimated future results and the transactions contemplated by the Merger Agreement, including the implied enterprise value, the expected transaction and ownership structure and the likelihood and ability of the parties to successfully consummate the transactions contemplated by the Merger Agreement. Such forward-looking statements are based upon the current beliefs and expectations of Aero’s management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are difficult to predict and generally beyond our control. Actual results and the timing of events may differ materially from the results anticipated in these forward-looking statements. Actual results may differ significantly from management’s expectations due to various risks and uncertainties including, without limitation: (i) the risk that the proposed transaction may not be completed in a timely manner, or at all; (ii) the failure to satisfy the conditions to the consummation of the proposed transaction, including, without limitation, the receipt of shareholder approvals; (iii) unanticipated difficulties or expenditures relating to the proposed transaction; (iv) the effect of the announcement or pendency of the proposed transaction on the plans, business relationships, operating results and operations; (v) potential difficulties retaining employees, suppliers and customers as a result of the announcement and pendency of the proposed transaction; (vi) the response of employees, suppliers and customers to the announcement of the proposed transaction; (vii) risks related to diverting management’s attention from Aero’s ongoing business operations; and (viii) legal proceedings, including those that may be instituted against Aero, its board of directors, its executive officers or others following the announcement of the proposed transaction. Forward-looking statements regarding Aero reflect management of Aero’s good faith beliefs, assumptions and expectations but are not guarantees of future performance or events. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Current Report on Form 8-K. The Company undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date hereof, except as may be required by law.

Item 9.01. Financial Statements and Exhibits.

(d) Exhibits.

Exhibit No. | | Description |

| | |

23.1 | | Consent of Boulay PLLP |

| | |

23.2 | | Consent of Barton CPA PLLC |

| | |

99.1 | | Audited abbreviated financial statements of Aero Velocity, Inc., a former business of Workhorse Group, Inc., including the statements of assets acquired and liabilities assumed as of June 5, 2024 and December 31, 2023, the related statements of revenues and direct expenses for the period from January 1, 2024 to June 5, 2024 and for the six months ended December 31, 2023, and the related notes to the abbreviated financial statements |

| | |

99.2 | | Audited balance sheet of Aero Velocity, Inc. as of December 31, 2024 and the related statements of operations, stockholders' deficit and cash flows for the period then ended, |

| | |

99.3 | | The historical unaudited financial statements of Aero Velocity, Inc. for the three and nine months ended September 30, 2025 and the related notes thereto. |

| | |

99.4 | | Unaudited pro forma condensed combined financial statements of BT Brands, Inc. and Aero Velocity Inc. and notes thereto present the unaudited pro forma condensed combined balance sheets as of September 30, 2025 and the unaudited pro forma condensed combined statements of operations as of and for the nine months ended September 30, 2025 and for the year ended December 31, 2024. |

| | |

99.5 | | Aero Velocity Inc. Corporate Investor Deck as of November 24, 2025. |

| | |

104 | | Cover Page Interactive Data File (Embedded within the Inline XBRL document and included in Exhibit) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| BT BRANDS, INC. | |

| | | |

Dated: December 1, 2025 | By: | /s/ Gary Copperud | |

| | Gary Copperud | |

| | Chief Executive Officer | |

EXHIBIT 23.1

CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

We hereby consent to the incorporation by reference in this Registration Statement on Form S-3 of BT Brands, Inc. of our report dated March 31, 2025, with respect to the consolidated financial statements of BT Brands, Inc. on Form 10-K for the year ended December 29, 2024. We also consent to the reference to us under the heading "Experts" in such Registration Statement.

/s/ Boulay PLLP

Minneapolis, Minnesota

December 1, 2025

EXHIBIT 23.2

Certified Public Accountants and Advisors

A PCAOB Registered Firm

713-489-5635 bartoncpafirm.com Cypress, Texas

Consent of Independent Registered Public Accounting Firm

We consent to the use, in this Registration Statement on Form S-3, of our report dated August 27, 2025, with respect to our audit of the financial statements of Aero Velocity, Inc. as of December 31, 2024 and to our report dated August 27, 2025, with respect to our audits of the abbreviated financial statements for the period from July 1, 2023 to December 31, 2023 as well as for the period from January 1, 2024 to June 5, 2024. We also consent to the reference to us under the heading “Experts” in such Registration Statement.

Very truly yours,

Cypress, Texas

December 1, 2025

EXHIBIT 99.1

AERO VELOCITY, INC.

ABBREVIATED FINANCIAL STATEMENTS

As of June 5, 2024 and December 31, 2023 and for the Period from January 1, 2024 and Ended June 5, 2024 and for the

Six Months Ended December 31, 2023

With Report of Independent Registered Public Accounting Firm

AERO VELOCITY, INC.

ABBREVIATED FINANCIAL STATEMENTS

For the Period Ended June 5, 2024 and the Six Months Ended December 31, 2023

TABLE OF CONTENTS

Certified Public Accountants and Advisors

A PCAOB Registered Firm

713-489-5635 bartoncpafirm.com Cypress, Texas

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Members of Management of Aero Velocity, Inc.

Opinion on the Financial Statements

We have audited the abbreviated financial statements of Aero Velocity, Inc, (the “Company”) a former business of Workhorse Group, Inc., which comprise the statements of assets acquired and liabilities assumed as of June 5, 2024 and December 31, 2023, the related statements of revenues and direct expenses for the period from January 1, 2024 to June 5, 2024 and for the six months ended December 31, 2023, and the related notes to the abbreviated financial statements (collectively referred to as the “financial statements”). In our opinion, the accompanying financial statements present fairly, in all material respects, the assets acquired and liabilities assumed of the Company as of December 31, 2023 and June 5, 2024, and its revenues and direct expenses for the six months ended December 31, 2023 and the period from January 1, 2024 to June 5, 2024 in accordance with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Emphasis of Matter

As discussed in Note 2 to the financial statements, the financial statements have been prepared for the purposes of complying with the rules and regulations of the U.S. Securities and Exchange Commission and are not intended to be a complete presentation of the Business’ assets, liabilities, revenues and expenses, and cash flows. Our opinion is not modified with respect to this matter.

We have served as the Company’s auditor since 2024.

Cypress, Texas

August 27 2025

AERO VELOCITY, INC.

STATEMENT OF ASSETS ACQUIRED AND LIABILITIES ASSUMED

| (in thousands) | | As of June 5, 2024 | | | As of December 31, 2023 | |

| Assets | |

| Property and equipment, net | | $ | 199 | | | $ | 232 | |

| Total assets acquired | | | 199 | | | | 232 | |

| Liabilities |

| | | | | | | | | |

| Total liabilities assumed | | | - | | | | - | |

| | | | | | | | | |

| Net assets acquired | | $ | 199 | | | $ | 232 | |

The accompanying notes are an integral part of these abbreviated financial statements

AERO VELOCITY, INC.

STATEMENT OF REVENUES AND DIRECT EXPENSES

| (in thousands) | | Period from January 1, 2024 to June 5, 2024 | | | Six Months Ended December 31, 2023 | |

| Revenue: | |

| Service | | $ | 828 | | | $ | 239 | |

| Product | | | - | | | | 201 | |

| Total Revenue | | | 828 | | | | 440 | |

| Direct expenses: |

| Depreciation and amortization | | | 33 | | | | 40 | |

| General and administrative | | | 479 | | | | 787 | |

| Total direct expenses | | | 512 | | | | 827 | |

| Shortfall of revenues over direct expenses | | $ | 316 | | | $ | (387 | ) |

The accompanying notes are an integral part of these abbreviated financial statements

AERO VELOCITY, INC.

NOTES TO THE ABBREVIATED FINANCIAL STATEMENTS

1. Description of the Transaction

On June 6, 2024, the Aero Velocity, Inc. (“Aero” or “the Company”) entered into an agreement with Workhorse Group, Inc. (“Workhorse”) to purchase the assets of their drone business in exchange for 50% of operating cash flow for the first 12 months following the agreement. No cash was exchanged at the time of the agreement. The acquisition was accounted for as a business combination using the acquisition method in accordance with Accounting Standards Codification (ASC) 805, Business Combinations because the acquired assets met the definition of a business, which includes inputs, processes, and outputs capable of generating revenue.

Under this agreement, Aero is obligated to pay Workhorse 50% of Aero's operating cash flow for the 12-month period ending June 30, 2025. The payment is contingent upon the operating cash flow (defined as “revenue paid in cash minus operating expenses paid in cash” per the agreement) generated during this period and will be due in 2025 pending agreement of the calculation of operating cash flows between Aero. The Company has assessed this obligation and recognizes the potential financial impact in accordance with applicable accounting standards. At the date of the acquisition, the estimated fair value of the contingent liability was $0 as the projected operating cash flow is expected to be negative. The liability will continue to be remeasured at fair value at each reporting date, with changes recognized in earnings.

Description of the Business

The Company is a leading provider of advanced drone services, specializing in lidar and multispectral data acquisition for diverse industries. The Company serves as a trusted partner to its customers, leveraging its expertise in cutting- edge data capture and drone technology solutions developed through collaborations with industry innovators. Aero also provides comprehensive drone maintenance, repair, warranty, and fleet support services, drawing on over 10 years of experience in drone maintenance and manufacturing. The Company actively seeks industry partners to enhance service offerings and expand market reach, while also supporting drone fleet operators through tailored maintenance and operational services.

2. Summary of Significant Accounting Policies

A summary of the company’s significant accounting policies consistently applied in the preparation of the accompanying abbreviated financial statements follows:

Basis of Presentation – The accompanying financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP). The Statements of Assets Acquired and Liabilities Assumed and Statements of Revenues and Direct Expenses are prepared for the sole purpose of complying with the rules and regulations of Rule 3-05 of Regulation S-X of the U.S. Securities and Exchange Commission and are not intended to be a complete presentation of the Company’s assets, liabilities, revenues and expenses.

The financial statements have been prepared in an abbreviated format as prior to the divestiture the business was treated as a product line of Workhorse and did not rise to the level of a reportable segment. Under US SEC Regulation S-X 3-05(e), the financial statements of an acquisition of net assets that constitutes a business can be prepared and audited as abbreviated financial statements if the business meets certain qualifying conditions as follows:

| | · | The total assets and total revenues (both after intercompany eliminations) of the acquired or to be acquired business constitute 20 percent or less of such corresponding amounts of the seller and its subsidiaries consolidated as of and for the most recently completed fiscal year. |

| | · | Separate financial statements for the business have not previously been prepared; |

| | · | The acquired business was not a separate entity, subsidiary, operating segment (as defined in U.S. GAAP) or division during the periods for which the acquired business financial statements would be required; and |

| | · | The seller has not maintained the distinct and separate accounts necessary to present financial statements that, absent this paragraph , would satisfy the requirements of this section and it is impracticable to prepare such financial statements. |

The Company meets these qualifying conditions and as a result, it is impracticable to prepare full financial statements as required by Regulation S-X. These abbreviated financial statements may not be indicative of what they would have been had the Company been an independent stand-alone entity, nor are they necessarily indicative of future results of the Company’s operations going forward due to the omission of various operating expenses. The Statements of Revenues and Direct Expenses do not include cost of revenues, corporate overhead expense, and interest expense for debt that is not assumed by the new Company given that financial statements of the Company under Workhorse including this information were not available and to include such costs would involve making assumptions. The Company has presented only payroll-related general and administrative expenses due to the unavailability of complete information required to allocate and present other components of general and administrative costs. These financial statements are not intended to present a full depiction of general and administrative expenses under U.S. GAAP and should be read with that limitation in mind.

Use of Estimates – The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the condensed financial statements and the reported amounts of revenues and expenses during the period. Significant items subject to such estimates and assumptions include the (i) estimates of future costs to complete customer contracts recognized over time, (ii) fair value of assets acquired, and (iii) fair value of contingent consideration related to the acquisition. Actual results could differ from those estimates.

Revenue – The Company recognizes revenue in accordance with ASC 606, Revenue from Contracts with Customers. Revenue is recognized when control of the promised goods or services is transferred to the customer in an amount that reflects the consideration the Company expects to receive in exchange for those goods or services. The determination of the timing of revenue recognition and the measurement of the transaction price involves judgments and estimates that may impact the amounts reported.

The Company recognizes revenue based on a five-step model when all of the following criteria have been met: (i) a contract with a customer exists, (ii) performance obligations have been identified, (iii) the price to the customer has been determined, (iv) the price to the customer has been allocated to the performance obligations, and (v) performance obligations are satisfied.

The performance obligations under service agreements generally are satisfied over time as the service is provided. Revenue under these contracts is recognized over time using an input measure of progress (typically based on acres scanned to date.)

Performance obligations for product sales are typically satisfied at a point in time. This occurs when control of the products is transferred to the customer, which generally is when title and risk of loss have passed to the customer.

Taxes Collected from Customers - In the course of doing business, the company collects taxes from customers, including but not limited to sales taxes. It is the company’s policy to record these taxes on a net basis in the statement of operations; therefore, the company does not include the taxes collected as a component of revenues.

Cost of Revenue – Cost of revenue primarily include direct and indirect materials, manufacturing overhead, and shipping and logistics costs.

General and Administrative Expenses – General and administrative expenses generally consist of payroll -related costs due to the unavailability of complete information required to allocate and present other components of general and administrative expenses.

Concentrations of Credit Risk – The Company has a limited number of customers. For the period from January 1, 2024 to June 5, 2024, two customers accounted for approximately 89% of total revenues, with individual customer concentrations of 46% and 43%, respectively. For the six months ended December 31, 2023, two customers accounted for approximately 86% of total revenues, with individual customer concentrations of 53% and 33%, respectively.

Commitments and Contingencies – From time to time, the Company may be subject to litigation and other claims in the normal course of business. As of June 5, 2024, the Company was not subject to any material commitments or contingencies, including legal proceedings, guarantees, environmental obligations, or other contractual commitments, that would require disclosure under U.S. GAAP, and no amounts have been accrued in the financial statements with respect to any matters.

Property and Equipment, net – The property and equipment balance presented herein has been adjusted to reflect only those property and equipment items that were acquired through the acquisition. Property and equipment not transferred as part of the transaction have been excluded from the presented balances. Accumulated depreciation has also been adjusted accordingly to reflect only the acquired assets.

Property and equipment is stated at cost, less accumulated depreciation. Depreciation is provided on the straight-line method over the assets’ estimated service lives. Leasehold improvements are amortized using the straight-line method over the shorter of the remaining lives of the respective leases or the services of the improvements. Expenditures for maintenance and repairs are charged to expense in the period in which they are incurred, and betterments are capitalized.

3. Property and Equipment, net

Property and equipment acquired consisted of the following (in thousands):

| | | Useful Life (years) | | | As of June 5, 2024 | | | As of December 31, 2023 | |

| Property & equipment | | 5 | | | $ | 373 | | | $ | 373 | |

| Technology hardware equipment | | 3 | | | | 16 | | | | 16 | |

| Total | | | | | | | 389 | | | | 389 | |

| Less: Accumulated depreciation | | | | | | | (190 | ) | | | (157 | ) |

| Total Property & equipment, net | | | | | | $ | 199 | | | $ | 232 | |

Depreciation expense for the period from January 1, 2024 to June 5, 2024 and for the six months ended December 31, 2023 was $33 thousand and $40 thousand, respectively.

4. Subsequent Events

The Company has evaluated the effects of events that have occurred through August 27, 2025, the date the abbreviated financials statements were available for issuance, and there have been no material events that would require recognition or disclosure in the abbreviated financial statements and the associated notes accompanying the abbreviated financial statements.

EXHIBIT 99.2

AERO VELOCITY, INC.

FINANCIAL STATEMENTS

As of December 31, 2024 and for the Period from June 6, 2024 to December 31, 2024

With Report of Independent Registered Independent Accounting Firm

AERO VELOCITY, INC.

FINANCIAL STATEMENTS

For the Period from June 6, 2024 to December 31, 2024

TABLE OF CONTENTS

Certified Public Accountants and Advisors

A PCAOB Registered Firm

713-489-5635 bartoncpafirm.com Cypress, Texas

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Members of Management of Aero Velocity, Inc.

Opinion on the Financial Statements

We have audited the accompanying balance sheet of Aero Velocity, Inc. (the “Company”) as of December 31, 2024, and the related statement of operations, stockholders’ deficit, and cash flows for the year then ended and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2024 and the results of its operations and its cash flows for the year then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provide a reasonable basis for our opinion.

Other Matters

Abbreviated financial statements

As discussed in Note 2 to the financial statements, the financial statements have been prepared for the purposes of complying with the rules and regulations of the U.S. Securities and Exchange Commission and are not intended to be a complete presentation of the Business’ assets, liabilities, revenues and expenses, and cash flows. Our opinion is not modified with respect to this matter.

Going Concern

Management plans to identify adequate sources of funding to provide operating capital for continued growth are disclosed in Note 2. Auditing the Company’s assessment and related disclosures regarding the Company’s ability to continue as a going concern required significant auditor judgment. This is due to the high level of uncertainty surrounding the projections and assumptions related to the timing and likelihood of future cash flows, including external funding. Assessing whether the Company’s disclosures adequately reflect the uncertainty and risks associated with its going concern status also demanded considerable auditor judgment and effort.

We have served as the Company’s auditor since 2024.

Cypress, Texas

August 27, 2025

AERO VELOCITY, INC.

BALANCE SHEET

| (in thousands) | | December 31, 2024 | |

| Assets | | | |

| Current Assets: | | | |

| Cash and cash equivalents | | $ | 544 | |

| Accounts receivable, net | | | 240 | |

| Accounts receivable unbilled | | | 46 | |

| Prepaid expenses | | | 104 | |

| Total current assets | | | 934 | |

| | | | | |

| Property and equipment, net | | | 624 | |

| Intangible assets, net | | | 14 | |

| Total Assets | | $ | 1,572 | |

| | | | | |

| Liabilities and Stockholders’ Deficit | | | | |

| Current liabilities: | | | | |

| Accounts payable | | $ | 507 | |

| Accrued liabilities | | | 28 | |

| Contract liabilities | | | 348 | |

| Notes payable, current | | | 35 | |

| Total current liabilities | | | 918 | |

| | | | | |

| Notes payable - long-term, net of discount | | | 1,210 | |

| Other Liabilities | | | 18 | |

| Total Liabilities | | | 2,146 | |

| | | | | |

| Commitments and Contingencies (Note 8) | | | | |

| | | | | |

| Total Stockholders’ Deficit | | | (574 | ) |

| | | | | |

| Total Liabilities and Stockholders’ Deficit | | $ | 1,572 | |

The accompanying notes are an integral part of these financial statements

AERO VELOCITY, INC.

STATEMENT OF OPERATIONS

| (in thousands) | | Period from June 6, 2024 to December 31, 2024 | |

| Revenue: | | | |

| Service | | $ | 1,107 | |

| Product | | | 25 | |

| Total revenue | | | 1,132 | |

| Costs and expenses | | | | |

| Cost of revenue (exclusive of depreciation and amortization presented below) | | | 540 | |

| Depreciation and amortization | | | 46 | |

| General and administrative | | | 1,410 | |

| Total costs and expenses | | | 1,996 | |

| Operating income (loss) | | | (864 | ) |

| | | | | |

| Other (income) expense: | | | | |

| Gain on bargain purchase | | | (309 | ) |

| Other income, net | | | (20 | ) |

| Interest expense | | | 21 | |

| Total other income, net | | | (308 | ) |

| Income before income taxes | | | (556 | ) |

| Income tax expense | | | 18 | |

| Net loss | | $ | (574 | ) |

The accompanying notes are an integral part of these financial statements

AERO VELOCITY, INC.

STATEMENT OF CHANGES IN STOCKHOLDERS’ DEFICIT

| (in thousands) | | Accumulated Deficit | | | Total Stockholders’ Deficit | |

| Balance at June 6, 2024 | | $ | - | | | $ | - | |

| Net loss | | | (574 | ) | | | (574 | ) |

| Balance at December 31, 2024 | | $ | (574 | ) | | $ | (574 | ) |

The accompanying notes are an integral part of these financial statements

AERO VELOCITY, INC.

STATEMENT OF CASH FLOWS

| (in thousands) | | For the period from June 6 to December 31, 2024 | |

| Cash flows from operating activities: | | | |

| Net loss | | $ | (574 | ) |

| Adjustments to reconcile net loss to net cash from operating activities: | | | | |

| Depreciation and amortization | | | 46 | |

| Non-cash interest expense | | | 21 | |

| Gain on sale of property and equipment | | | (6 | ) |

| Gain on bargain purchase | | | (309 | ) |

| Deferred income taxes | | | 18 | |

| Changes in operating assets and liabilities: | | | | |

| Accounts receivable (including unbilled) | | | (286 | ) |

| Other current assets | | | (104 | ) |

| Accounts payable | | | 114 | |

| Accrued liabilities | | | 7 | |

| Contract liabilities | | | 348 | |

| Net cash used in operating activities | | | (725 | ) |

| | | | | |

| Cash flows from investing activities: | | | | |

| Capital expenditures | | | (4 | ) |

| Proceeds from sale of property and equipment | | | 28 | |

| Net cash provided by investing activities | | | 24 | |

| | | | | |

| Cash flows from financing activities: | | | | |

| Payments on notes payable | | | (41 | ) |

| Proceeds from notes payable | | | 1,286 | |

| Net cash from financing activities | | | 1,245 | |

| | | | | |

| Net change in cash and cash equivalents | | | 544 | |

| | | | | |

| Cash and cash equivalents, beginning of period | | | - | |

| Cash and cash equivalents, end of period | | $ | 544 | |

| | | | | |

| Supplemental disclosure of cash flow information: | | | | |

| Cash paid for interest | | $ | - | |

| Cash paid for taxes | | $ | - | |

| | | | | |

| Non-cash investing and financing activities: | | | | |

| Assets assumed in acquisition | | $ | 309 | |

| Capital expenditures included in Accounts payable at year-end | | $ | 393 | |

The accompanying notes are an integral part of these financial statements

AERO VELOCITY, INC.

NOTES TO THE FINANCIAL STATEMENTS

1. Description of the Business

Aero Velocity, Inc. (“the Company” or “Aero”) is a private equity-backed company that emerged from a divesture of Workhorse Group, Inc. (“Workhorse”) in June 2024, after nearly a decade of operating as Workhorse Aero. On June 6, 2024, the Company entered into an agreement with Workhorse to purchase the assets of their drone business in exchange for 50% of operating cash flow for the first 12 months following the agreement. No cash was exchanged at the time of the agreement. The acquisition was completed as a part of the divestiture. The acquisition was accounted for as a business combination using the acquisition method in accordance with Accounting Standards Codification (ASC) 805, Business Combinations, because the acquired assets met the definition of a business, which includes inputs, processes, and outputs capable of generating revenue.

Under this agreement, Aero is obligated to pay Workhorse 50% of Aero's operating cash flow for the 12-month period ended June 30, 2025. The payment is contingent upon the operating cash flow (defined as “revenue paid in cash minus operating expenses paid in cash” per the agreement) generated during this period and will be due in 2025 pending agreement of the calculation of operating cash flows between Aero and Workhorse. The Company has assessed this obligation and recognizes the potential financial impact in accordance with applicable accounting standards. At the date of the acquisition, the estimated fair value of the contingent liability was $0 as the projected operating cash flow is expected to be negative. The fair value of the net assets acquired exceeded the total consideration transferred, resulting in a gain on bargain purchase of $309 thousand, which is recognized in the consolidated statement of operations as of the acquisition date. The contingent liability will continue to be remeasured at fair value at each reporting date, with changes recognized in earnings. As of December 31, 2024, the estimated value of the contingent liability has not changed and remains at $0 and therefore there are no subsequent changes recognized in earnings.

The following table summarizes the allocation of the purchase price to the identifiable assets acquired, based on their estimated fair values as of the acquisition date:

| | | June 6, 2024 | |

| Accounts receivable - Workhorse | | $ | 120 | |

| Property and equipment | | | 297 | |

| Intangible assets | | | 12 | |

| Contract liability | | | (120 | ) |

| Consideration transferred | | | - | |

| Gain on bargain purchase | | $ | 309 | |

In connection with the acquisition, the Company measured the identifiable assets acquired and the contingent consideration at fair value in accordance with ASC 820, Fair Value Measurement. Property and equipment and intangible assets acquired were measured using a market approach and considered Level 2 measurements due to the use of observable inputs of equivalent assets, such as market listings for similar assets. The contingent consideration was measured using the twelve-month operating cash flow forecast.

The Company is a leading provider of advanced drone services, specializing in lidar and multispectral data acquisition for diverse industries. The Company serves as a trusted partner to its customers, leveraging its expertise in cutting-edge data capture and drone technology solutions developed through collaborations with industry innovators. Aero also provides comprehensive drone maintenance, repair, warranty, and fleet support services, drawing on over 10 years of experience in drone maintenance and manufacturing.

2. Summary of Significant Accounting Policies

The Company was established on June 6, 2024 as an acquisition from Workhorse Group, as a result the Statements of Operations and of Cash Flows presented herein represents the activity from the acquisition date to December 31, 2024. The financial information prior to the acquisition date will be presented separately as abbreviated financial statements prepared in accordance with the rules and regulations of Rule 3-05 of Regulation S-X of the U.S. Securities and Exchange Commission.

A summary of the Company’s significant accounting policies consistently applied in the preparation of the accompanying financial statements follows:

Basis of Presentation – The accompanying financial statements have been prepared using the accrual basis of accounting in accordance with accounting principles generally accept in the United States of America (“U.S. GAAP”), and in the opinion of management, include all adjustments (consisting of normal, recurring adjustments, unless otherwise disclosed) necessary for a fair statement of the results of operations, financial position, cash flows and changes in stockholders’ equity (deficit) for each period presented.

Going Concern – The accompanying financial statements have been prepared on the basis that the Company is a going concern, which contemplates the realization of assets and satisfaction of liabilities in the normal course of business. In assessing the appropriateness of the going concern assumption, management has considered the Company’s current financial position, future cash flow forecasts, and available financing facilities. While the Company incurred a net loss and had negative operating cash flows during the period from June 6, 2024 to December 31, 2024, subsequent developments including improved recent financial performance, access to additional financing, and continued expansion in operations, have supported the going concern assessment. Based on this evaluation, management has concluded that there is no substantial doubt about the Company’s ability to continue as a going concern for a period of at least one year from the date the financial statements are issued.

Use of Estimates – The preparation of consolidated financial statements in conformity with (U.S. GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the period. Significant items subject to such estimates and assumptions include the (i) estimates of future costs to complete customer contracts recognized over time, (ii) valuation allowances for deferred income tax assets, (iii) fair value of assets acquired, and (iv) fair value of contingent consideration related to the acquisition. Actual results could differ from those estimates.

Cash and Cash Equivalents – The Company classifies all highly-liquid instruments with an original maturity of three months or less as cash equivalents. The Company maintains cash and cash equivalents in bank deposit accounts, which at times may exceed federally insured limits of $250,000.

Accounts Receivable – Accounts receivable are stated at amounts management expects to collect from outstanding balances. Credit is extended to customers based upon evaluation of the customer’s financial condition, and collateral is not required. Management provides for probable uncollectible amounts through a General and administrative expense within the Statement of Operations and a credit to a valuation allowance based on its assessment of the status of individual accounts. Balances still outstanding after management has used reasonable collection efforts are written off from the valuation allowance and a credit to accounts receivable. As of December 31, 2024, there were no allowances for doubtful accounts.

Revenue – The Company recognizes revenue in accordance with ASC 606, Revenue from Contracts with Customers. Revenue is recognized when control of the promised goods or services is transferred to the customer in an amount that reflects the consideration the Company expects to receive in exchange for those goods or services. The determination of the timing of revenue recognition and the measurement of the transaction price involves judgments and estimates that may impact the amounts reported.

The Company recognizes revenue based on a five-step model when all of the following criteria have been met: (i) a contract with a customer exists, (ii) performance obligations have been identified, (iii) the price to the customer has been determined, (iv) the price to the customer has been allocated to the performance obligations, and (v) performance obligations are satisfied.

AERO VELOCITY, INC.

NOTES TO THE FINANCIAL STATEMENTS

The performance obligations under service agreements generally are satisfied over time as the service is provided. Revenue under these contracts is recognized over time using an input measure of progress (typically based on acres scanned to date.)

Performance obligations for product sales are typically satisfied at a point in time. This occurs when control of the products is transferred to the customer, which generally is when title and risk of loss have passed to the customer.

Taxes Collected from Customers - In the course of doing business, the company collects taxes from customers, including but not limited to sales taxes. It is the Company’s policy to record these taxes on a net basis in the statement of operations; therefore, the company does not include the taxes collected as a component of revenues.

Cost of revenue – Cost of revenue primarily include direct and indirect materials, manufacturing overhead, and shipping and logistics costs.

General and Administrative Expenses – General and administrative expenses generally consist of personnel and facilities costs as well as fees for professional and contract services.

Concentrations of Credit Risk – The Company has a limited number of customers. For the period from June 6, 2024 to December 31, 2024, two customers accounted for approximately 90% of total revenues, with individual customer concentrations of 77% and 13%. As of December 31, 2024, three customers accounted for approximately 90% of total accounts receivable, with individual customer concentrations of 48%, 27%, and 15%. Loss of these customers could have a material adverse impact on the Company.

Contract Assets and Liabilities – Contracts with customers usually stipulate the timing of payment, which is defined by the terms found within the various contracts under which work was performed during the period. Therefore, contract assets and liabilities are created when the timing of costs incurred on work performed does not coincide with the billing terms, which frequently include retention provisions contained in each contract.

The Company’s balance sheet may present contract assets which would include unbilled revenue associated with contract work that has been completed and billed but not paid by customers, which are presented in accounts receivable. The Company’s balance sheets may also present contract liabilities, which contain deferred revenue, which represent amounts received for which revenue has not yet been earned as the service has not yet been provided.

Property and Equipment, net – Property and equipment, net are carried at cost net of accumulated depreciation. Certain assets were acquired in accordance with the agreement concluded with Workhorse Group in June 2024, the value of the acquired assets represents fair value of the assets as of the date of the agreement. Depreciation is provided on the straight-line method over the assets’ estimated service lives. Leasehold improvements are amortized using the straight -line method over the shorter of the remaining lives of the respective leases or the services of the improvements. Expenditures for maintenance and repairs are charged to expense in the period in which they are incurred, and betterments are capitalized if the life of the underlying asset is extended. The cost of assets sold or abandoned, and the related accumulated depreciation are eliminated from the balance sheet and any gains or losses are reflected in the accompanying Statement of Operations of the respective period.

Intangible Assets, net – Intangible assets include domains and internal use software. Certain of the intangible assets were acquired in accordance with the agreement concluded with Workhorse Group in June 2024 and the value of the acquired assets represents fair value of the assets as of the date of the agreement. Intangible assets are recognized at cost when acquired or as the accumulation of certain costs when internally developed (in accordance with ASC 350-40, Internal-Use Software and are carried net of accumulated amortization and impairment losses, if any. The Company reviews intangible assets for impairment whenever events or changes in circumstances indicate the carrying amount may not be recoverable. Once placed in service, intangible assets are amortized using the straight-line method over the assets’ estimated useful lives.

Income Taxes – The Company accounts for income taxes in accordance with ASC 740, Income Taxes, which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the financial statement carrying amounts of assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years the temporary differences are expected to reverse.

AERO VELOCITY, INC.

NOTES TO THE FINANCIAL STATEMENTS

The Company’s income tax obligations commenced upon its formation on June 6, 2024. The Company is not responsible for, and has no liability related to, any income taxes incurred prior to this date.

During the period from June 6, 2024 to December 31, 2024, the Company recognized income tax expense along with a partially offsetting income tax benefit, resulting from its deferred tax assets and liabilities. Deferred tax assets primarily relate to net operating loss carryforwards and accrued expenses not yet deductible for tax purposes. Deferred tax liabilities primarily related to temporary differences associated with depreciation of property and equipment for tax purposes in excess of book depreciation and the timing of revenue recognition related to deferred revenue.

The Company has evaluated the realizability of its deferred tax assets and determined that it is more likely than not that the full amount will be realized based on expected future taxable income and the reversal of existing taxable temporary differences. Accordingly, no valuation allowance has been recorded as of December 31, 2024.

Deferred tax assets and liabilities are presented net by tax jurisdiction in accordance with ASC 740-10-45. Additional quantitative details are disclosed in Note 7.

The Company recognizes the effect of income tax positions only if those positions are more likely than not of being sustained. Recognized income tax positions are measured at the largest amount that is greater than 50% likely of being realized. Changes in recognition or measurement are reflected in the period in which a change in judgment occurs. The Company had no material uncertain tax positions as of December 31, 2024.

3. Prepaid Expenses

Prepaid expenses consisted of the following (in thousands):

| | | December 31, 2024 | |

| Prepaid insurance | | $ | 45 | |

| Other prepayments | | | 59 | |

| Total prepaid expenses | | $ | 104 | |

4. Property and Equipment, net

Property and equipment consisted of the following (in thousands):

| | | Useful | | | December 31, | |

| | Life (years) | | | 2024 | |

| Property & equipment | | 5 | | | $ | 656 | |

| Technology hardware equipment | | 3 | | | | 10 | |

| Total | | | | | | | 666 | |

| Less accumulated depreciation | | | | | | | (42 | ) |

| Total property & equipment, net | | | | | | $ | 624 | |

Depreciation expense for the period from June 6, 2024 to December 31, 2024 was $44 thousand.

AERO VELOCITY, INC.

NOTES TO THE FINANCIAL STATEMENTS

5. Intangible Assets, net

Intangible assets consisted of the following (in thousands):

| | | Useful | | | December 31, | |

| | | Life (years) | | | 2024 | |

| Domains | | 3 | | | $ | 12 | |

| Internal use software | | 1 | | | | 4 | |

| Total | | | | | | | 16 | |

| Less accumulated amortization | | | | | | | (2 | ) |

| Total intangible assets, net | | | | | | $ | 14 | |

Amortization expense for the period from June 6, 2024 to December 31, 2024 was $2 thousand.

6. Long-Term Debt

The Company’s long-term debt arrangements consist of the following (in thousands):

| | | December 31, 2024 | |

| Promissory Notes | | $ | 1,210 | |

| Insurance Financing | | | 35 | |

| Total debt | | | 1,245 | |

| Less: current portion | | | (35 | ) |

| Total long-term debt | | $ | 1,210 | |

On Jul 18, 2024, Aero Velocity Inc. (“Borrower”) and ATW Opportunities Master Fund II, L.P., (“Lender”) concluded the agreement on a Promissory Note for the principal amount of $5,000,000 or the aggregate amount of all unpaid advances made under the terms of the Note. The Note accrues interest at an annual rate of 5.06%, calculated on a 360-day year basis. All outstanding principal and accrued interest are due on the 24-month anniversary of the Note, with repayment first applied to accrued interest and then to principal. As of December 31, 2024, the amount of debt outstanding was $1.2 million. Interest expense related to notes payable was $18 thousand for the period from June 6, 2024 to December 31, 2024.

Insurance financing – The Company finances a portion of its insurance premiums through third-party lenders. These financing arrangements with Assured Partners are typically short-term in nature and are used to manage working capital. Under the terms of these agreements, the Company makes a down payment at the inception of the policy and agrees to repay the remaining premium balance in equal monthly installments, including applicable interest and fees, over the term of the insurance policy, generally not exceeding 12 months. The agreements bear an annual interest rate of 12.6% for the period from June 6, 2024 to December 31, 2024. All agreements will mature in July 2025. As of December 31, 2024, the total outstanding balance under these arrangements was $35 thousand. Interest expense related to insurance financing was $3 thousand for the period from June 6, 2024 to December 31, 2024.

AERO VELOCITY, INC.

NOTES TO THE FINANCIAL STATEMENTS

7. Income Taxes

The expense (benefit) for income taxes consists of the following for the period from June 6, 2024 to December 31, 2024:

| Current income taxes: | | $ | - | |

| Deferred income taxes: | | | 18 | |

| Income tax expense | | $ | 18 | |

The significant components of the Company’s deferred tax assets and liabilities as of December 31, 2024 are as follows:

| Deferred tax assets: | | | |

| Accrued expenses | | $ | 6 | |

| Net operating losses | | | 65 | |

| Gross deferred tax assets | | | 71 | |

| Less: Valuation allowance | | | - | |

| Net deferred tax assets | | | 71 | |

| | | | | |

| Deferred tax liabilities: | | | | |

| Fixed assets | | | 21 | |

| Deferred revenue | | | 68 | |

| Total deferred tax liabilities | | | 89 | |

| | | | | |

| Net deferred tax assets (liabilities) | | $ | (18 | ) |

As of June 30, 2025, the Company has not recorded a valuation allowance against its deferred tax assets, as management believes it is more likely than not that these assets will be fully realized.

8. Commitments and Contingencies

Litigation – From time to time, we may be subject to litigation and other claims in the normal course of business. As of December 31, 2024, the Company was not subject to any material commitments or contingencies, including legal proceedings, guarantees, environmental obligations, or other contractual commitments, that would require disclosure under U.S. GAAP, and no amounts have been accrued in the financial statements with respect to any matters.

9. Employee Benefit Plan

The Company provides a 401(k) retirement plan (the “Plan”) for eligible employees as stated in the Plan agreement whereby participating employees may elect to contribute any amount not less than one percent and not more than 100 percent of their compensation, subject to a limit on calendar year contributions as set forth by the Internal Revenue Service. The Company matching contribution is discretionary and may be made on behalf of an employee. The Plan highlights state that the Company may contribute a matching amount determined at the employer's discretion. For the period from June 6, 2024 to December 31, 2024, the Company contributed approximately $11 thousand, in matching funds to the Plan, and is included in general and administrative expenses within the accompanying Statement of Operations.

10. Related Party Transactions

As of December 31, 2024, the Company had an outstanding note payable to its sole investor, ATW Opportunities Master Fund II, L.P., who is considered a related party. The loan was made to fund working capital requirements. Additional details regarding this note, including its terms, are disclosed in Note 7 – Long-Term Debt. The balance of the related party note payable as of December 31, 2024 was $1.2 million, and interest expense of $21 thousand was incurred during the period from June 6, 2024 to December 31, 2024. The transaction was measured at the exchange amount, which is the amount of consideration established and agreed to by the related parties.

11. Subsequent Events

We have evaluated the effects of events that have occurred subsequent to December 31, 2024, for potential recognition or disclosure through August 27, 2025, the date the financial statements were available for issuance, and there have been no material events that would require recognition in the December 31, 2024 financial statements or disclosure in the associated notes accompanying the financial statements.

EXHIBIT 99.3

AERO VELOCITY, INC.

INTERIM FINANCIAL STATEMENTS

For the quarterly period ended September 30, 2025

AERO VELOCITY, INC.

FINANCIAL STATEMENTS

For the quarterly period ended September 30, 2025

TABLE OF CONTENTS

AERO VELOCITY, INC.

UNAUDITED BALANCE SHEETS

| | | September 30, 2025 | | | December 31, 2024 | |

| Assets | | | | | | |

| Current Assets: | | | | | | |

| Cash and cash equivalents | | $ | 289,285 | | | $ | 544,182 | |

| Accounts receivable, net | | | 178,200 | | | | 240,322 | |

| Accounts receivable unbilled | | | - | | | | 45,984 | |

| Prepaid expenses | | | 6,582 | | | | 104,313 | |

| Total current assets | | | 474,067 | | | | 934,801 | |

| | | | | | | | | |

| Property and equipment, net | | | 617,219 | | | | 624,456 | |

| Intangible assets, net | | | 1,000 | | | | 13,667 | |

| Other assets | | | 196,028 | | | | - | |

| Total Assets | | $ | 1,288,314 | | | $ | 1,572,924 | |

| | | | | | | | | |

| Liabilities and Stockholders’ Deficit | | | | | | | | |

| Current liabilities: | | | | | | | | |

| Accounts payable | | $ | 109,195 | | | $ | 507,536 | |

| Accrued liabilities | | | 161,887 | | | | 28,312 | |

| Contract liabilities | | | 125,189 | | | | 347,671 | |

| Notes payable - current | | | 1,296 | | | | 35,273 | |

| Other current liabilities | | | 25,457 | | | | - | |