Exhibit 99.1

Media Contact: | Investor Contact: |

October 21, 2025

Bridgewater Bancshares, Inc. Announces Third Quarter 2025 Financial Results

Third Quarter 2025 Highlights

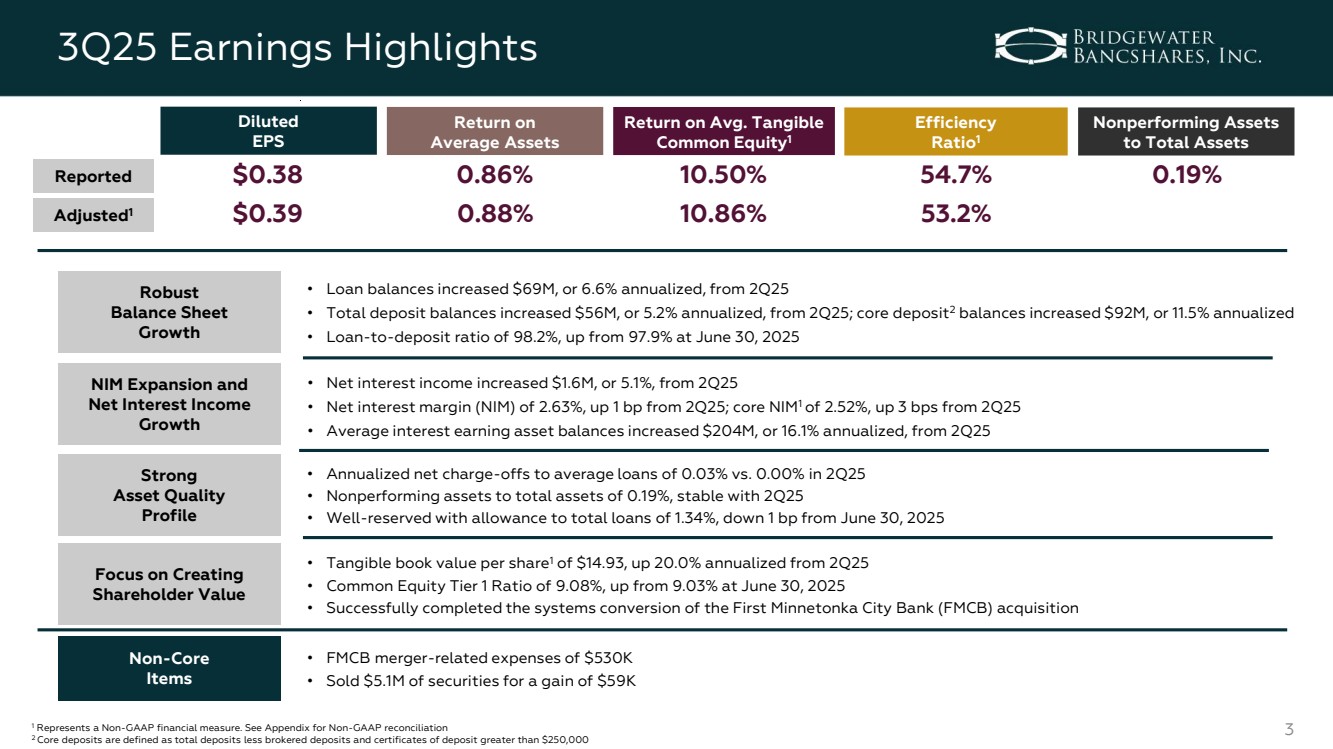

| ● | Net income of $11.6 million, or $0.38 per diluted common share; adjusted net income of $12.0 million, or $0.39 per diluted common share.(1) |

| ● | Net interest income increased $1.6 million, or 5.1%, from the second quarter of 2025. |

| ● | Net interest margin (on a fully tax-equivalent basis) of 2.63% for the third quarter of 2025, an increase of one basis point from the second quarter of 2025. |

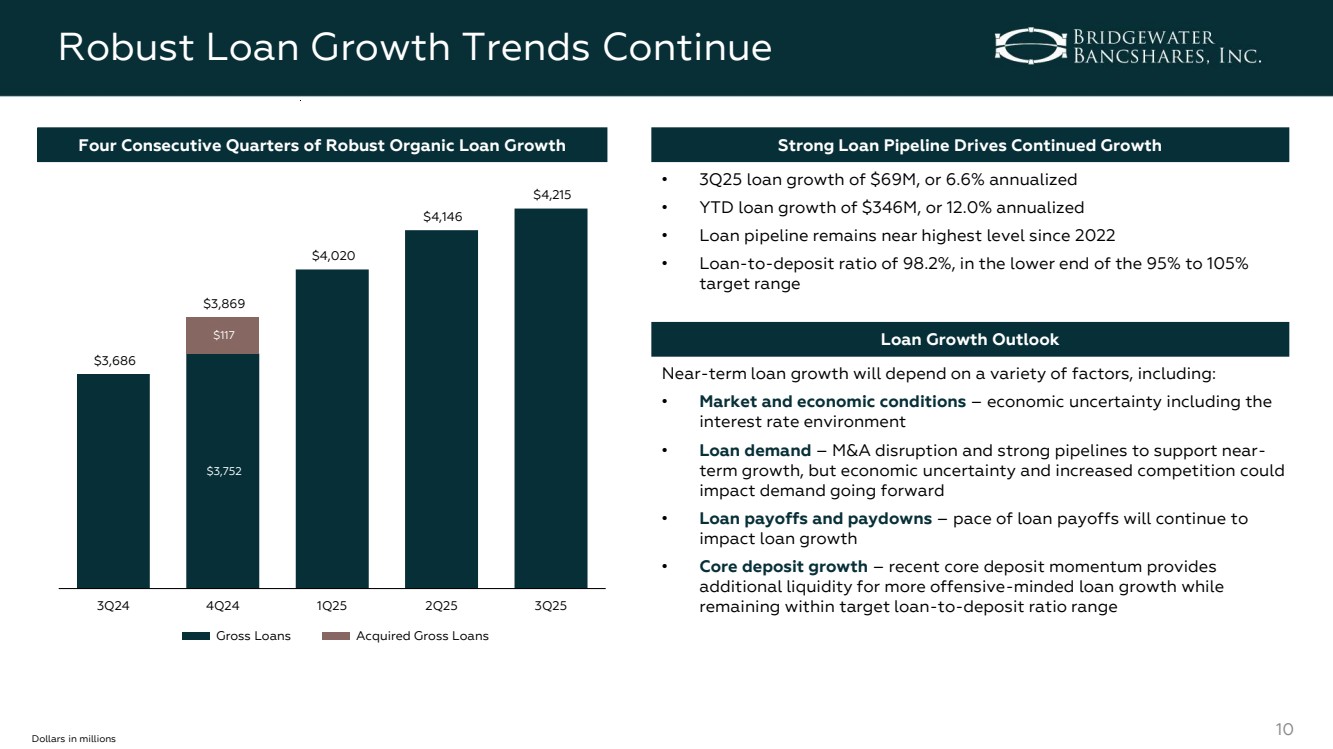

| ● | Gross loans increased by $68.8 million, or 6.6% annualized, from the second quarter of 2025. |

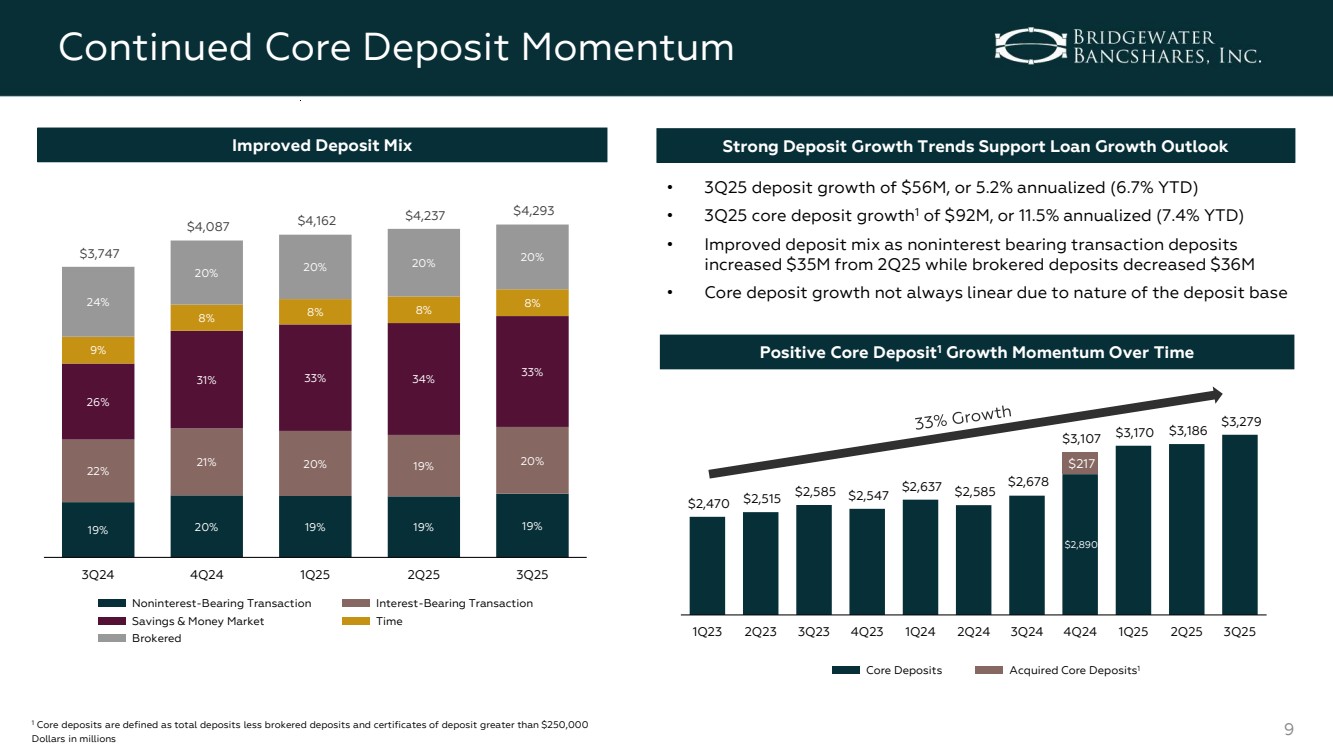

| ● | Total deposits increased by $56.0 million, or 5.2% annualized, from the second quarter of 2025; core deposits(2) increased by $92.1 million, or 11.5% annualized, from the second quarter of 2025. |

| ● | Efficiency ratio(1) of 54.7%, up from 52.6% for the second quarter of 2025; adjusted efficiency ratio(1) of 53.2%, up from 51.5% for the second quarter of 2025. |

| ● | Annualized net loan charge-offs as a percentage of average loans of 0.03%, compared to 0.00% for the second quarter of 2025. |

| ● | Nonperforming assets to total assets of 0.19% at September 30, 2025, stable with 0.19% at June 30, 2025. |

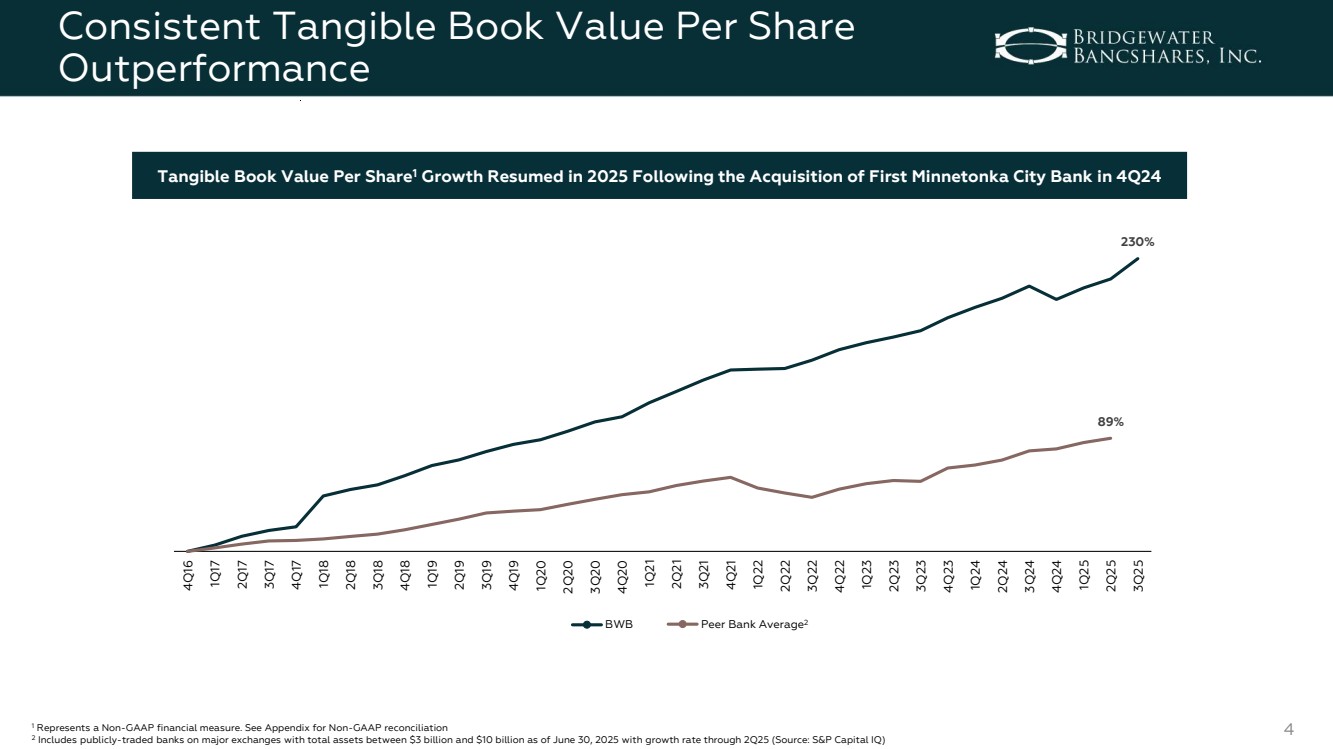

| ● | Tangible book value per share(1) of $14.93 at September 30, 2025, an increase of 20.0% annualized, from the second quarter of 2025. |

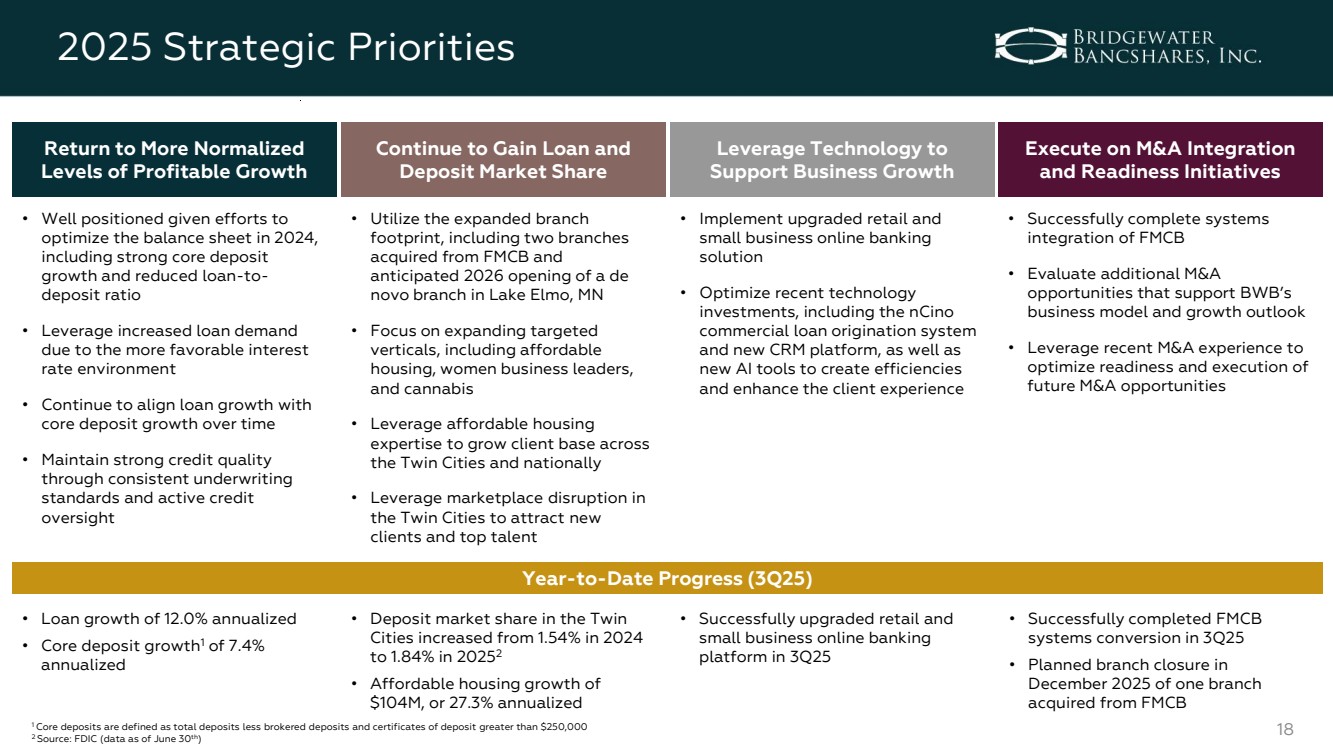

| ● | Successfully completed the systems conversion of the First Minnetonka City Bank (“FMCB”) acquisition. |

| ● | Planned branch closure in December 2025 of one of the two branches acquired from FMCB in 2024. |

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

| (2) | Core deposits are defined as total deposits less brokered deposits and certificates of deposit greater than $250,000. |

Page 1 of 19

St. Louis Park, MN – Bridgewater Bancshares, Inc. (Nasdaq: BWB) (“the Company”), the parent company of Bridgewater Bank (“the Bank”), today announced net income of $11.6 million for the third quarter of 2025, compared to $11.5 million for the second quarter of 2025, and $8.7 million for the third quarter of 2024. Earnings per diluted common share were $0.38 for the third quarter of 2025, compared to $0.38 for the second quarter of 2025, and $0.27 for the third quarter of 2024. Adjusted net income, a non-GAAP financial measure, was $12.0 million for the third quarter of 2025, compared to $11.3 million for the second quarter of 2025, and $8.9 million for the third quarter of 2024. Adjusted earnings per diluted common share, a non-GAAP financial measure, were $0.39 for the third quarter of 2025, compared to $0.37 for the second quarter of 2025, and $0.28 for the third quarter of 2024.

“Bridgewater produced another quarter of strong net interest income growth as we continued to execute on our strategic priority of gaining both loan and deposit market share,” said Chairman and Chief Executive Officer, Jerry Baack. “Robust core deposit growth supported strong loan growth during the quarter as our loan pipelines remained near three-year highs, we continued to gain traction in the affordable housing space, and talent and client opportunities from M&A disruption in the Twin Cities remained plentiful. Meanwhile, our liability-sensitive balance sheet remains well positioned to benefit from the September interest rate cut and a rates-down environment.

“The third quarter was also highlighted by strong asset quality, consistent tangible book value per share growth, the launch of a new retail and small business online banking platform, and the successful systems conversion of our recent acquisition of First Minnetonka City Bank. With a favorable outlook for continued balance sheet growth and net interest margin expansion from here, we are poised for improved profitability trends moving forward.”

Page 2 of 19

Key Financial Measures

| | As of and for the Three Months Ended |

| | As of and for the Nine Months Ended |

| |||||||||||

| | September 30, | | June 30, | | September 30, |

| | September 30, | | September 30, |

| |||||

|

| 2025 | | 2025 | | 2024 |

|

| 2025 |

| 2024 |

| |||||

Per Common Share Data | | | | | | | | | | | | | | | | | |

Basic Earnings Per Share | | $ | 0.38 | | $ | 0.38 | | $ | 0.28 | | | $ | 1.08 | | $ | 0.79 | |

Diluted Earnings Per Share | | | 0.38 | | | 0.38 | | | 0.27 | | | | 1.06 | | | 0.77 | |

Adjusted Diluted Earnings Per Share (1) | | | 0.39 | | | 0.37 | | | 0.28 | | | | 1.08 | | | 0.77 | |

Book Value Per Share | | | 15.62 | | | 14.92 | | | 14.06 | | | | 15.62 | | | 14.06 | |

Tangible Book Value Per Share (1) | | | 14.93 | | | 14.21 | | | 13.96 | | | | 14.93 | | | 13.96 | |

| | | | | | | | | | | | | | | | | |

Financial Ratios | | | | | | | | | | | | | | | | | |

Return on Average Assets (2) | | | 0.86 | % | | 0.90 | % | | 0.73 | % | | | 0.84 | % | | 0.71 | % |

Pre-Provision Net Revenue Return on Average Assets (1)(2) | | | 1.19 | | | 1.27 | | | 0.96 | | | | 1.20 | | | 0.95 | |

Return on Average Shareholders' Equity (2) | | | 9.47 | | | 9.80 | | | 7.79 | | | | 9.23 | | | 7.55 | |

Return on Average Tangible Common Equity (1)(2) | | | 10.50 | | | 10.93 | | | 8.16 | | | | 10.23 | | | 7.87 | |

Net Interest Margin (3) | | | 2.63 | | | 2.62 | | | 2.24 | | | | 2.59 | | | 2.24 | |

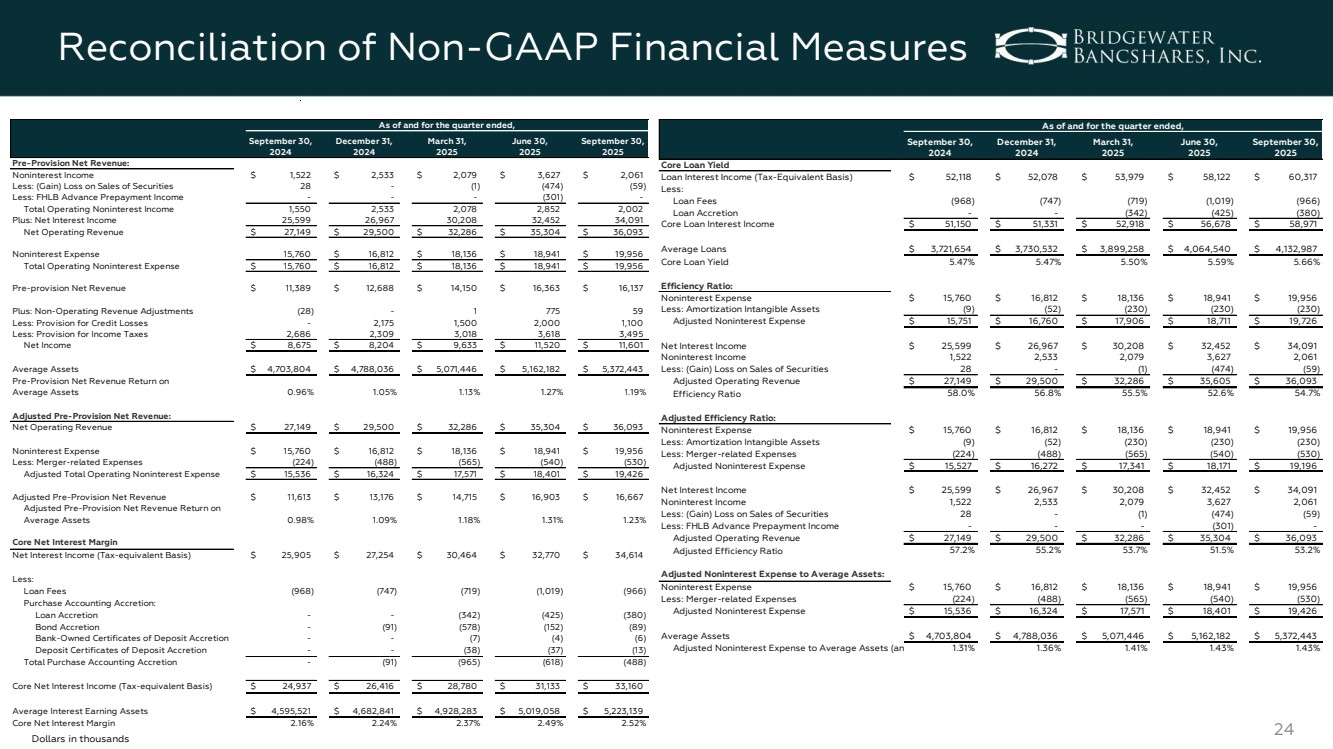

Core Net Interest Margin (1)(3) | | | 2.52 | | | 2.49 | | | 2.16 | | | | 2.46 | | | 2.17 | |

Cost of Total Deposits | | | 3.19 | | | 3.16 | | | 3.58 | | | | 3.18 | | | 3.45 | |

Cost of Funds | | | 3.25 | | | 3.19 | | | 3.54 | | | | 3.20 | | | 3.46 | |

Efficiency Ratio (1) | | | 54.7 | | | 52.6 | | | 58.0 | | | | 54.2 | | | 58.3 | |

Noninterest Expense to Average Assets (2) | | | 1.47 | | | 1.47 | | | 1.33 | | | | 1.46 | | | 1.34 | |

Tangible Common Equity to Tangible Assets (1) | | | 7.71 | | | 7.40 | | | 8.17 | | | | 7.71 | | | 8.17 | |

Common Equity Tier 1 Risk-based Capital Ratio (Consolidated) (4) | | | 9.08 | | | 9.03 | | | 9.79 | | | | 9.08 | | | 9.79 | |

| | | | | | | | | | | | | | | | | |

Adjusted Financial Ratios (1) | | | | | | | | | | | | | | | | | |

Adjusted Return on Average Assets (2) | | | 0.88 | % | | 0.88 | % | | 0.75 | % | | | 0.86 | % | | 0.70 | % |

Adjusted Pre-Provision Net Revenue Return on Average Assets (2) | | | 1.23 | | | 1.31 | | | 0.98 | | | | 1.24 | | | 0.96 | |

Adjusted Return on Average Shareholders' Equity (2) | | | 9.77 | | | 9.64 | | | 7.96 | | | | 9.41 | | | 7.51 | |

Adjusted Return on Average Tangible Common Equity (2) | | | 10.86 | | | 10.74 | | | 8.36 | | | | 10.44 | | | 7.82 | |

Adjusted Efficiency Ratio | | | 53.2 | | | 51.5 | | | 57.2 | | | | 52.8 | | | 58.0 | |

Adjusted Noninterest Expense to Average Assets (2) | | | 1.43 | | | 1.43 | | | 1.31 | | | | 1.42 | | | 1.33 | |

| | | | | | | | | | | | | | | | | |

Balance Sheet and Asset Quality (dollars in thousands) | | | | | | | | | | | | | | | | | |

Total Assets | | $ | 5,359,994 | | $ | 5,296,673 | | $ | 4,691,517 | | | $ | 5,359,994 | | $ | 4,691,517 | |

Total Loans, Gross | | | 4,214,554 | | | 4,145,799 | | | 3,685,590 | | | | 4,214,554 | | | 3,685,590 | |

Deposits | | | 4,292,764 | | | 4,236,742 | | | 3,747,442 | | | | 4,292,764 | | | 3,747,442 | |

Loan to Deposit Ratio | | | 98.2 | % | | 97.9 | % | | 98.3 | % | | | 98.2 | % | | 98.3 | % |

Net Loan Charge-Offs to Average Loans (2) | | | 0.03 | | | 0.00 | | | 0.10 | | | | 0.01 | | | 0.03 | |

Nonperforming Assets to Total Assets (5) | | | 0.19 | | | 0.19 | | | 0.19 | | | | 0.19 | | | 0.19 | |

Allowance for Credit Losses to Total Loans | | | 1.34 | | | 1.35 | | | 1.38 | | | | 1.34 | | | 1.38 | |

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

| (2) | Annualized. |

| (3) | Amounts calculated on a tax-equivalent basis using the statutory federal tax rate of 21%. |

| (4) | Preliminary data. Current period subject to change prior to filings with applicable regulatory agencies. |

| (5) | Nonperforming assets are defined as nonaccrual loans plus 90 days past due and still accruing plus foreclosed assets. |

Page 3 of 19

Income Statement

Net Interest Margin and Net Interest Income

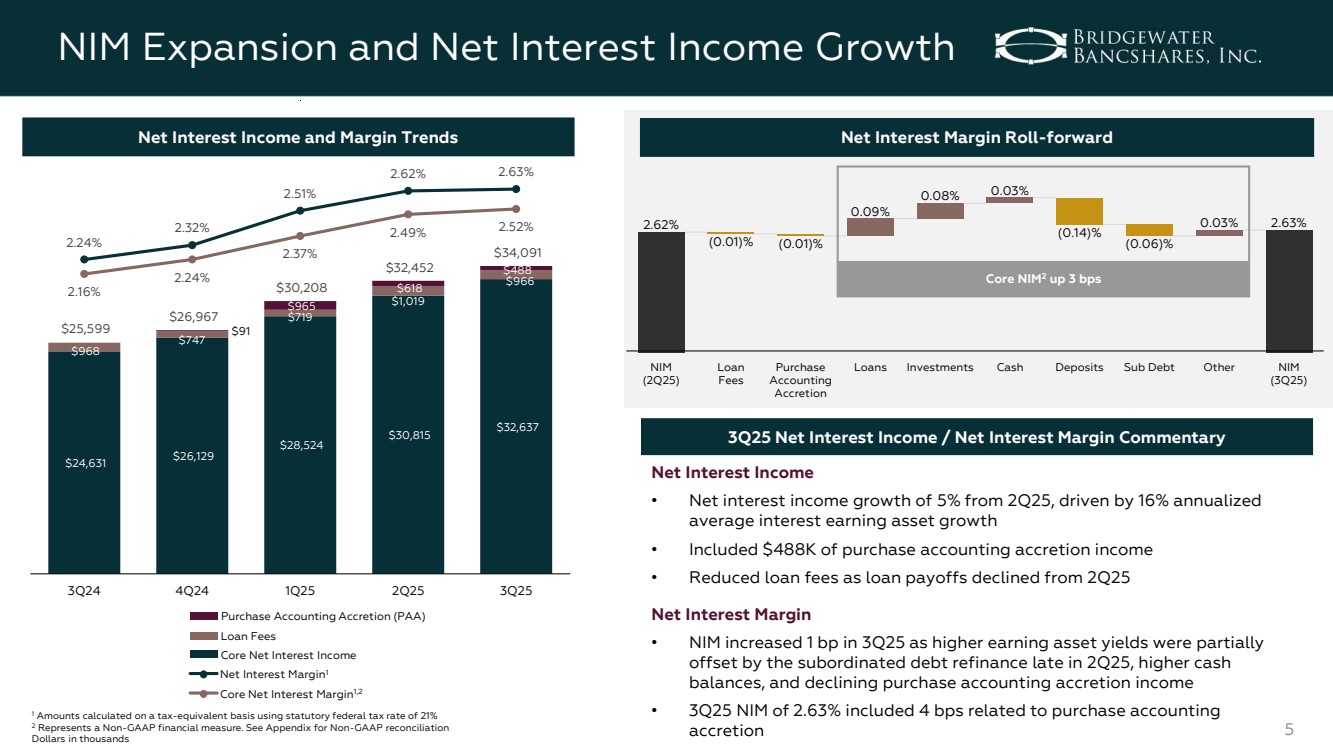

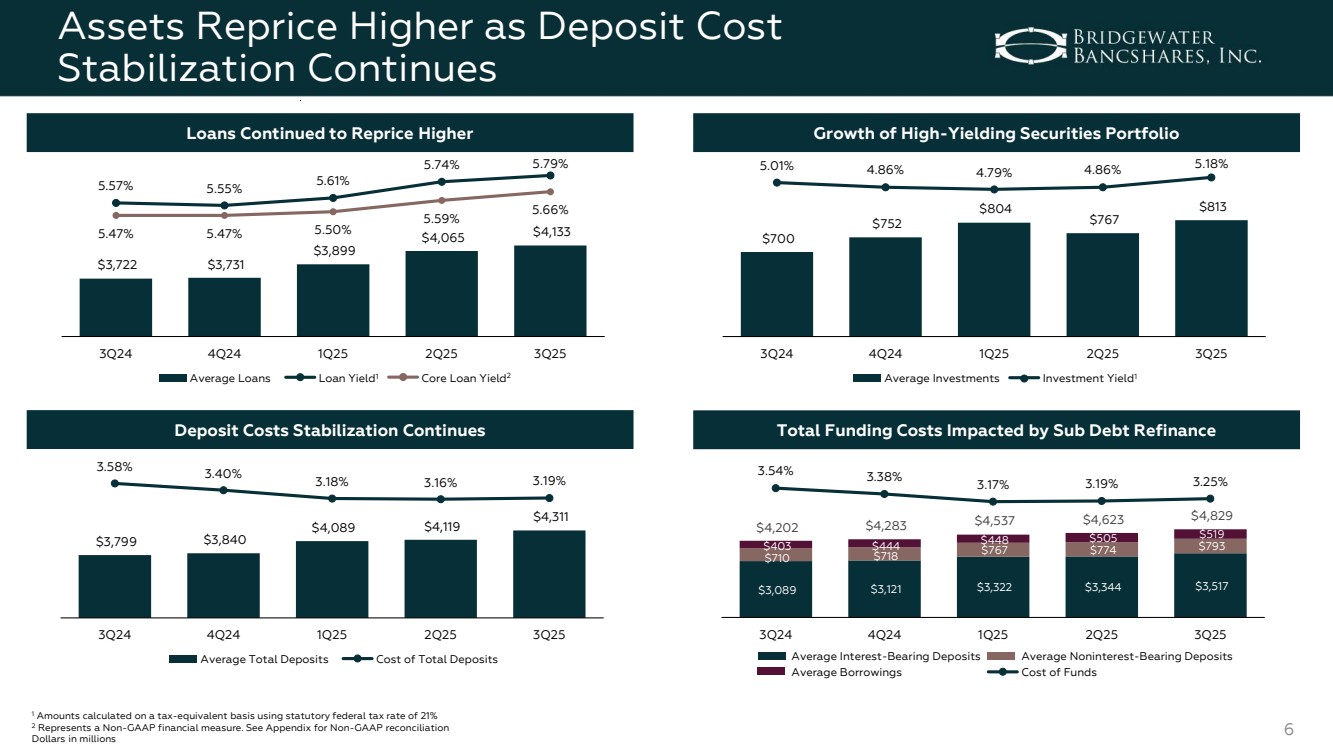

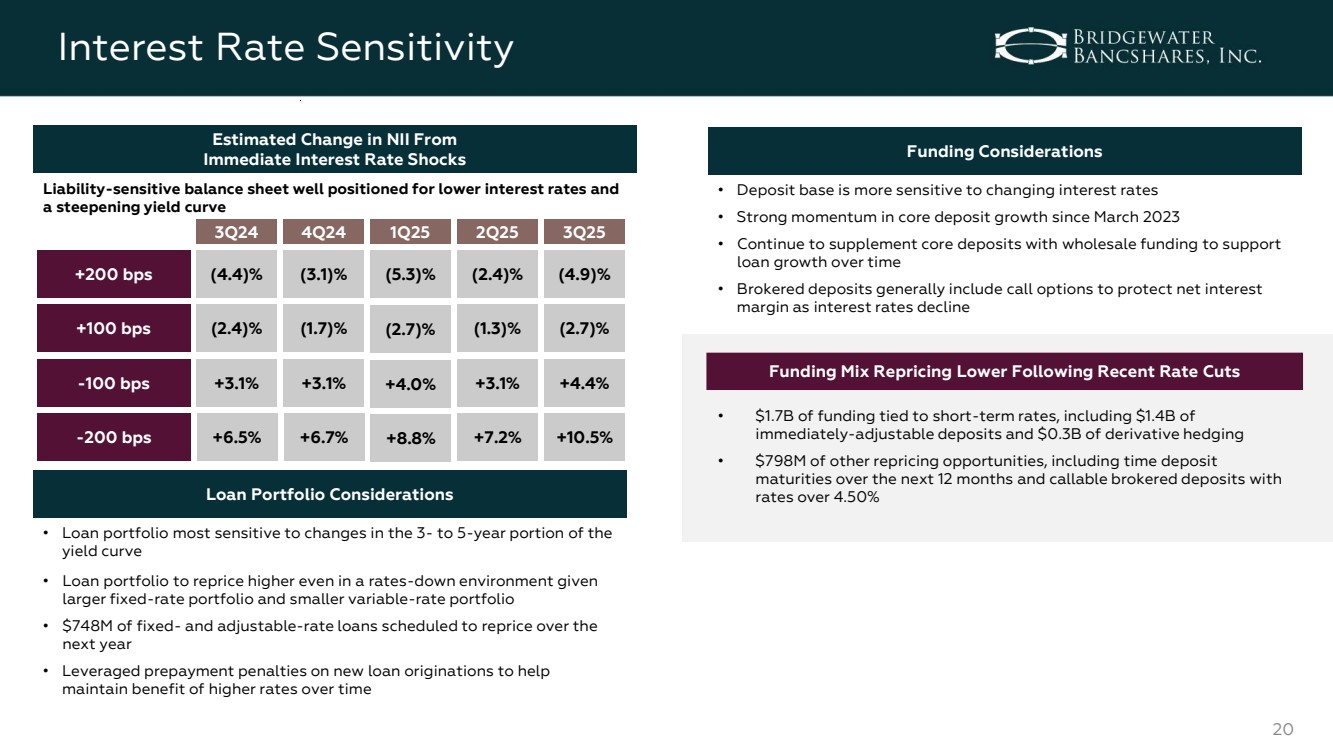

Net interest margin (on a fully tax-equivalent basis) for the third quarter of 2025 was 2.63%, a one basis point increase from 2.62% in the second quarter of 2025, and a 39 basis point increase from 2.24% in the third quarter of 2024. Core net interest margin (on a fully tax-equivalent basis), a non-GAAP financial measure which excludes the impact of loan fees and purchase accounting accretion attributable to the acquisition of FMCB, was 2.52% for the third quarter of 2025, a three basis point increase from 2.49% in the second quarter of 2025, and a 36 basis point increase from 2.16% in the third quarter of 2024.

| ● | Net interest margin expanded to 2.63% in the third quarter of 2025 primarily due to higher earning asset yields, offset partially by the subordinated debt refinance in the second quarter of 2025, higher cash balances, and declining purchase accounting accretion income. |

Net interest income was $34.1 million for the third quarter of 2025, an increase of $1.6 million from $32.5 million in the second quarter of 2025, and an increase of $8.5 million from $25.6 million in the third quarter of 2024.

| ● | The linked-quarter increase in net interest income was primarily due to growth in the loan and securities portfolios, offset partially by higher deposit balances. |

| ● | The year-over-year increase in net interest income was primarily due to growth in the loan portfolio and purchase accounting accretion, offset partially by higher deposit balances. |

Interest income was $73.6 million for the third quarter of 2025, an increase of $4.4 million from $69.2 million in the second quarter of 2025, and an increase of $10.6 million from $63.0 million in the third quarter of 2024.

| ● | The yield on interest earning assets (on a fully tax-equivalent basis) was 5.63% in the third quarter of 2025, compared to 5.56% in the second quarter of 2025, and 5.48% in the third quarter of 2024. |

| ● | The linked-quarter increase in the yield on interest earning assets was primarily due to growth and repricing of the loan and securities portfolios. |

| ● | The year-over-year increase in the yield on interest earning assets was primarily due to growth and repricing of the loan and securities portfolios and purchase accounting accretion. |

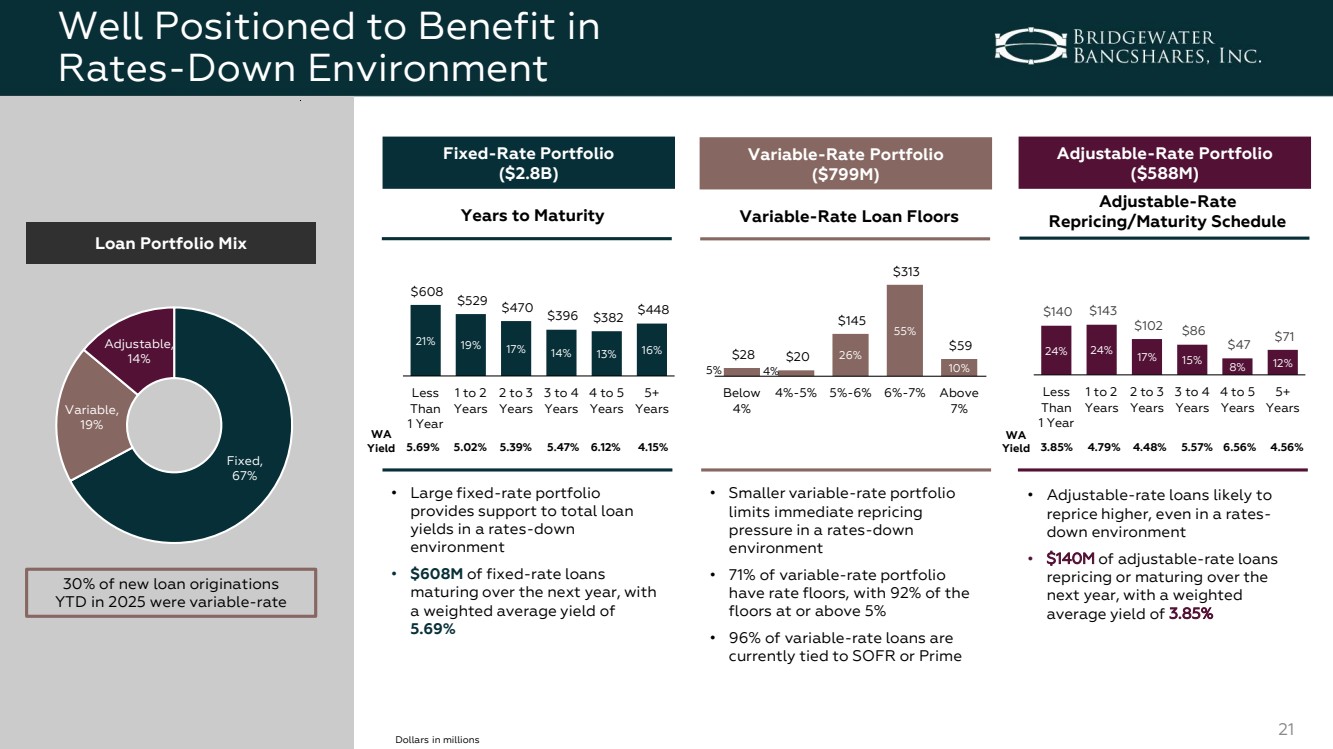

| ● | The aggregate loan yield increased to 5.79% in the third quarter of 2025, five basis points higher than 5.74% in the second quarter of 2025, and 22 basis points higher than 5.57% in the third quarter of 2024. |

| ● | Core loan yield, a non-GAAP financial measure, increased to 5.66% in the third quarter of 2025, seven basis points higher than 5.59% in the second quarter of 2025, and 19 basis points higher than 5.47% in the third quarter of 2024. |

A summary of interest and fees recognized on loans for the periods indicated is as follows:

| | Three Months Ended | ||||||||||||||

| | September 30, 2025 | | | June 30, 2025 | | | March 31, 2025 | | | December 31, 2024 | | | September 30, 2024 | | |

Interest | | 5.66 | % | | 5.59 | % | | 5.50 | % | | 5.47 | % | | 5.47 | % | |

Fees | | 0.09 | | | 0.11 | | | 0.07 | | | 0.08 | | | 0.10 | | |

Accretion | | 0.04 | | | 0.04 | | | 0.04 | | | — | | | — | | |

Yield on Loans | | 5.79 | % | | 5.74 | % | | 5.61 | % | | 5.55 | % | | 5.57 | % | |

Interest expense was $39.5 million for the third quarter of 2025, an increase of $2.8 million from $36.7 million in the second quarter of 2025, and an increase of $2.1 million from $37.4 million in the third quarter of 2024.

| ● | The cost of interest bearing liabilities was 3.89% in the third quarter of 2025, compared to 3.83% in the second quarter of 2025, and 4.27% in the third quarter of 2024. |

| ● | The linked-quarter increase in the cost of interest bearing liabilities was primarily due to higher interest bearing deposit balances and higher balances and rates paid on subordinated debentures following the payoff of $50.0 million of outstanding subordinated notes and the issuance of $80.0 million of new subordinated notes at the end of the second quarter. |

| ● | The year-over-year decrease in the cost of interest bearing liabilities was primarily due to lower interest bearing deposit costs, offset partially by higher balances and rates paid on FHLB advances and subordinated debentures. |

Page 4 of 19

Interest expense on deposits was $34.6 million for the third quarter of 2025, an increase of $2.1 million from $32.5 million in the second quarter of 2025, and an increase of $428,000 from $34.2 million in the third quarter of 2024.

| ● | The cost of total deposits was 3.19% in the third quarter of 2025, three basis points higher than 3.16% in the second quarter of 2025, and 39 basis points lower than 3.58% in the third quarter of 2024. |

| ● | The linked-quarter increase in the cost of total deposits was primarily due to time and brokered deposits repricing in the higher rate environment. |

| ● | The year-over-year decrease in the cost of total deposits was primarily due to lower rates paid on deposits following interest rate cuts in 2024 and 2025 and decreases in average brokered deposit balances. |

Provision for Credit Losses

The provision for credit losses on loans and leases was $900,000 for the third quarter of 2025, compared to $2.0 million for the second quarter of 2025 and $-0- for the third quarter of 2024.

| ● | The provision for credit losses on loans recorded in the third quarter of 2025 was primarily attributable to growth in the loan portfolio and an increase in specific reserves for loans individually evaluated. |

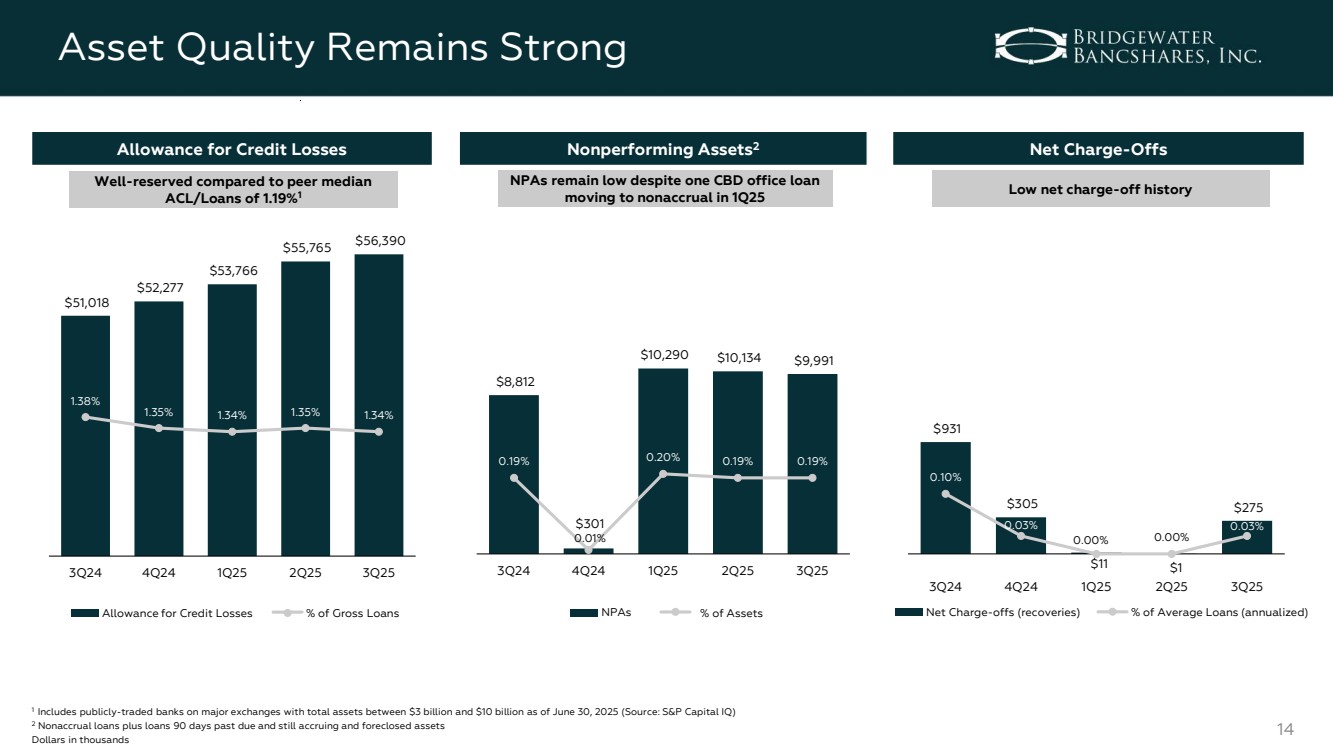

| ● | The allowance for credit losses on loans to total loans was 1.34% at September 30, 2025, compared to 1.35% at June 30, 2025, and 1.38% at September 30, 2024. |

The provision for credit losses for off-balance sheet credit exposures was $200,000 for the third quarter of 2025, and $-0- for each of the second quarter of 2025 and the third quarter of 2024.

| ● | A provision was recorded during the third quarter of 2025 due to an increase in the volume of newly originated loans with unfunded commitments in the commercial and construction and land development segments. |

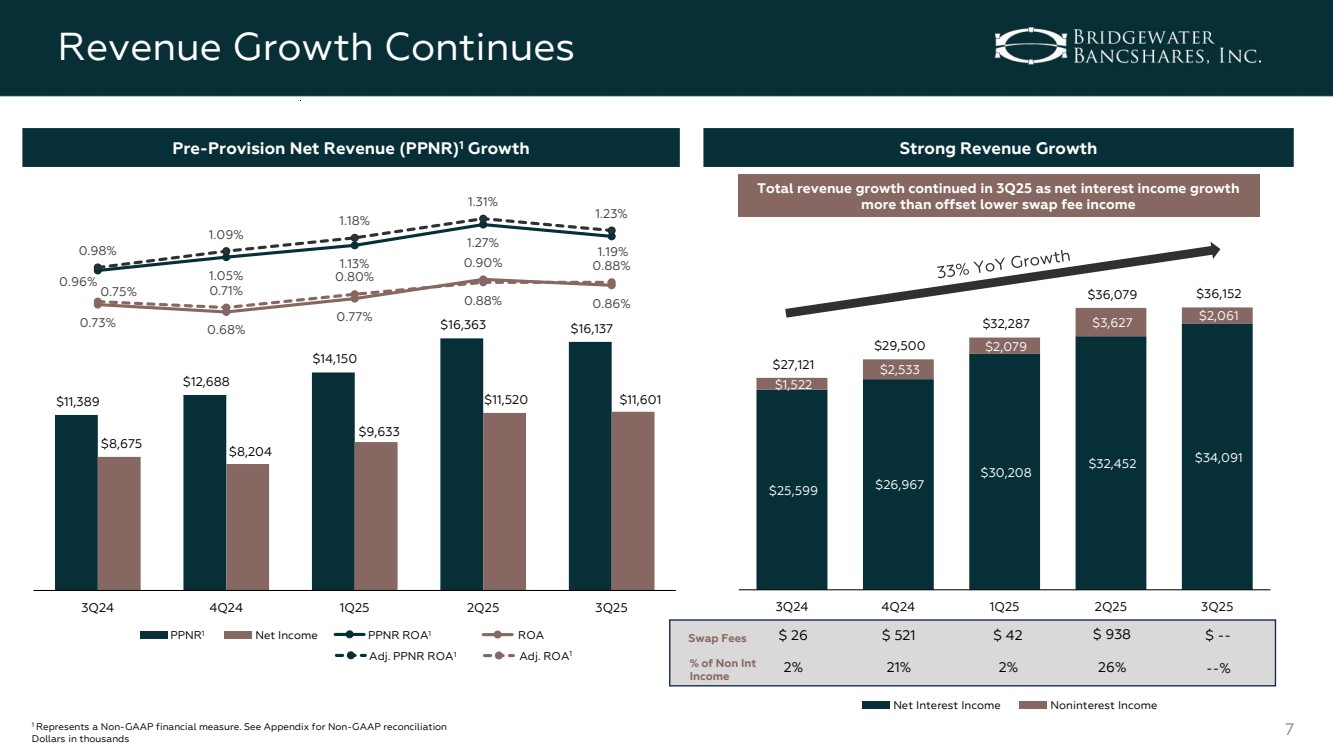

Noninterest Income

Noninterest income was $2.1 million for the third quarter of 2025, a decrease of $1.6 million from $3.6 million for the second quarter of 2025, and an increase of $539,000 from $1.5 million for the third quarter of 2024.

| ● | The linked-quarter decrease was primarily due to lower swap fees, gains on sales of securities, and FHLB prepayment income. |

| ● | The year-over-year increase was primarily due to higher investment advisory fees and customer service fees. |

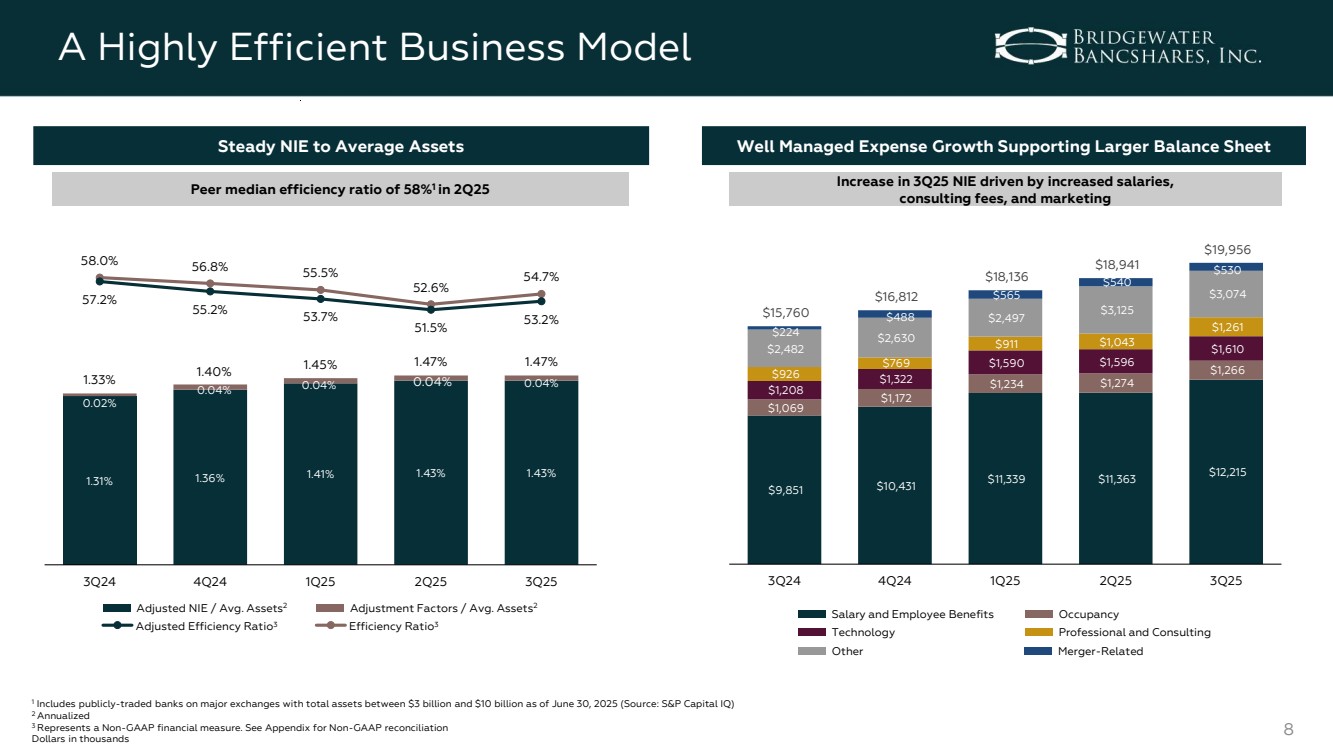

Noninterest Expense

Noninterest expense was $20.0 million for the third quarter of 2025, an increase of $1.0 million from $18.9 million for the second quarter of 2025 and an increase of $4.2 million from $15.8 million for the third quarter of 2024.

| ● | Noninterest expense for the third quarter of 2025 included $530,000 of merger-related expenses associated with the acquisition of FMCB, compared to $540,000 for the second quarter of 2025. |

| ● | The linked-quarter increase was primarily due to increases in salaries and employee benefits, marketing and advertising, and professional and consulting fees. |

| ● | The year-over-year increase was primarily attributable to increases in salaries and employee benefits, marketing and advertising, operating costs related to the FMCB acquisition, and merger-related expenses. |

| ● | The efficiency ratio, a non-GAAP financial measure, was 54.7% for the third quarter of 2025, compared to 52.6% for the second quarter of 2025, and 58.0% for the third quarter of 2024. |

| ● | The Company had 325 full-time equivalent employees at September 30, 2025, compared to 308 at June 30, 2025, and 265 at September 30, 2024. The year-over-year increase was largely driven by the addition of employees from the acquisition of FMCB and the hiring of key talent across the organization. |

Income Taxes

The effective combined federal and state income tax rate was 23.2% for the third quarter of 2025, compared to 23.9% for the second quarter of 2025, and 23.6% for the third quarter of 2024.

Page 5 of 19

Balance Sheet

Loans

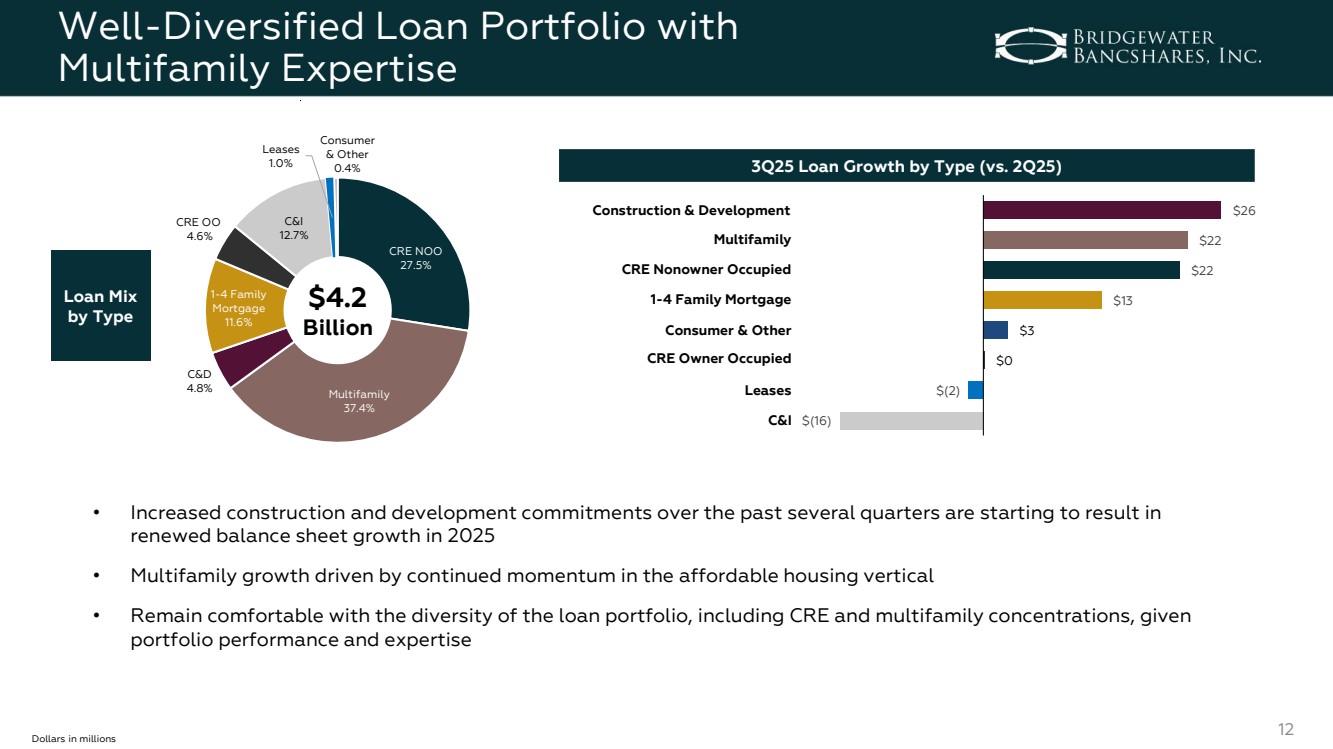

(dollars in thousands) | | September 30, 2025 | | June 30, 2025 | | March 31, 2025 | | December 31, 2024 | | September 30, 2024 | | |||||

Commercial | | $ | 533,476 | | $ | 549,259 | | $ | 528,801 | | $ | 497,662 | | $ | 493,403 | |

Leases | | | 43,186 | | | 44,817 | | | 43,958 | | | 44,291 | | | — | |

Construction and Land Development | | | 159,991 | | | 136,438 | | | 128,073 | | | 97,255 | | | 118,596 | |

1-4 Family Construction | | | 41,739 | | | 39,095 | | | 39,438 | | | 41,961 | | | 45,822 | |

Real Estate Mortgage: | | | | | | | | | | | | | | | | |

1 - 4 Family Mortgage | | | 487,297 | | | 474,269 | | | 479,461 | | | 474,383 | | | 421,179 | |

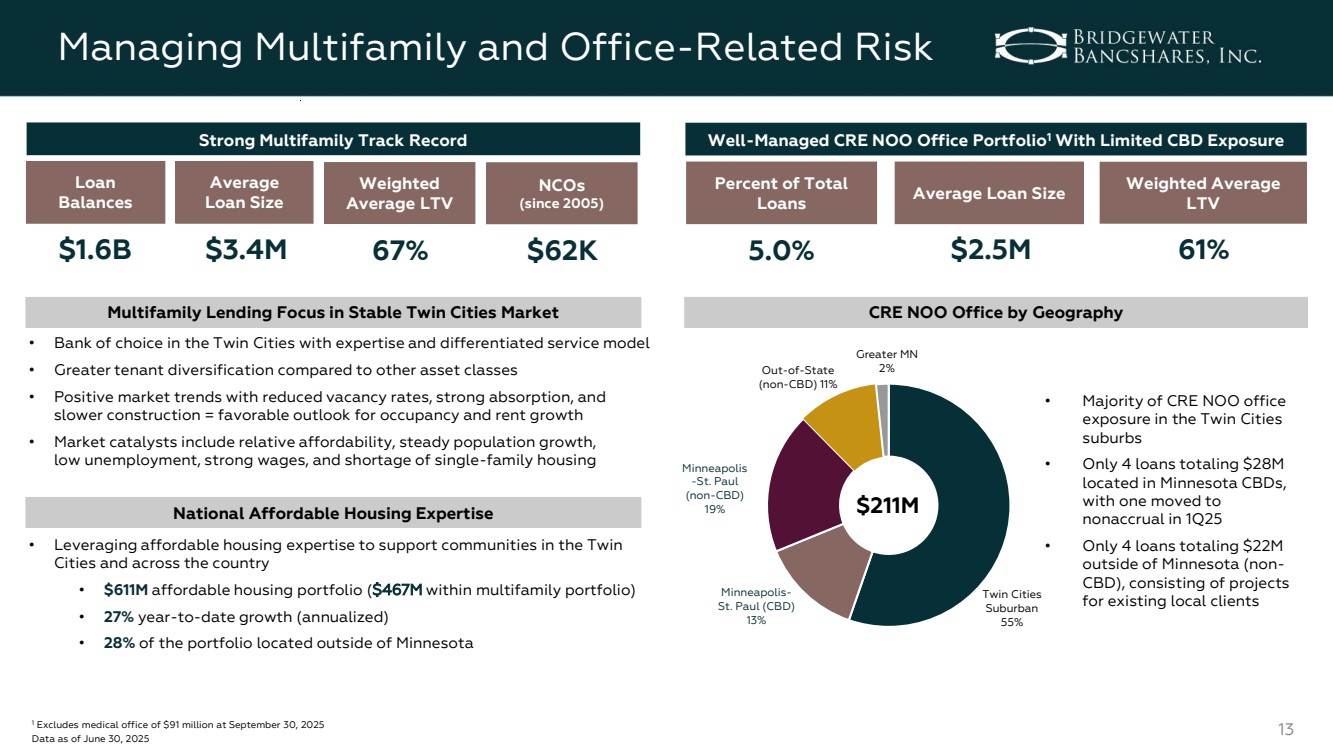

Multifamily | | | 1,578,223 | | | 1,555,731 | | | 1,534,747 | | | 1,425,610 | | | 1,379,814 | |

CRE Owner Occupied | | | 192,966 | | | 192,837 | | | 196,080 | | | 191,248 | | | 182,239 | |

CRE Nonowner Occupied | | | 1,158,622 | | | 1,137,007 | | | 1,055,157 | | | 1,083,108 | | | 1,032,142 | |

Total Real Estate Mortgage Loans | |

| 3,417,108 | |

| 3,359,844 | |

| 3,265,445 | |

| 3,174,349 | |

| 3,015,374 | |

Consumer and Other | | | 19,054 | | | 16,346 | | | 14,361 | | | 12,996 | | | 12,395 | |

Total Loans, Gross | |

| 4,214,554 | |

| 4,145,799 | |

| 4,020,076 | |

| 3,868,514 | |

| 3,685,590 | |

Allowance for Credit Losses on Loans | | | (56,390) | | | (55,765) | | | (53,766) | | | (52,277) | | | (51,018) | |

Net Deferred Loan Fees | | | (8,282) | | | (7,629) | | | (7,218) | | | (6,801) | | | (5,705) | |

Total Loans, Net | | $ | 4,149,882 | | $ | 4,082,405 | | $ | 3,959,092 | | $ | 3,809,436 | | $ | 3,628,867 | |

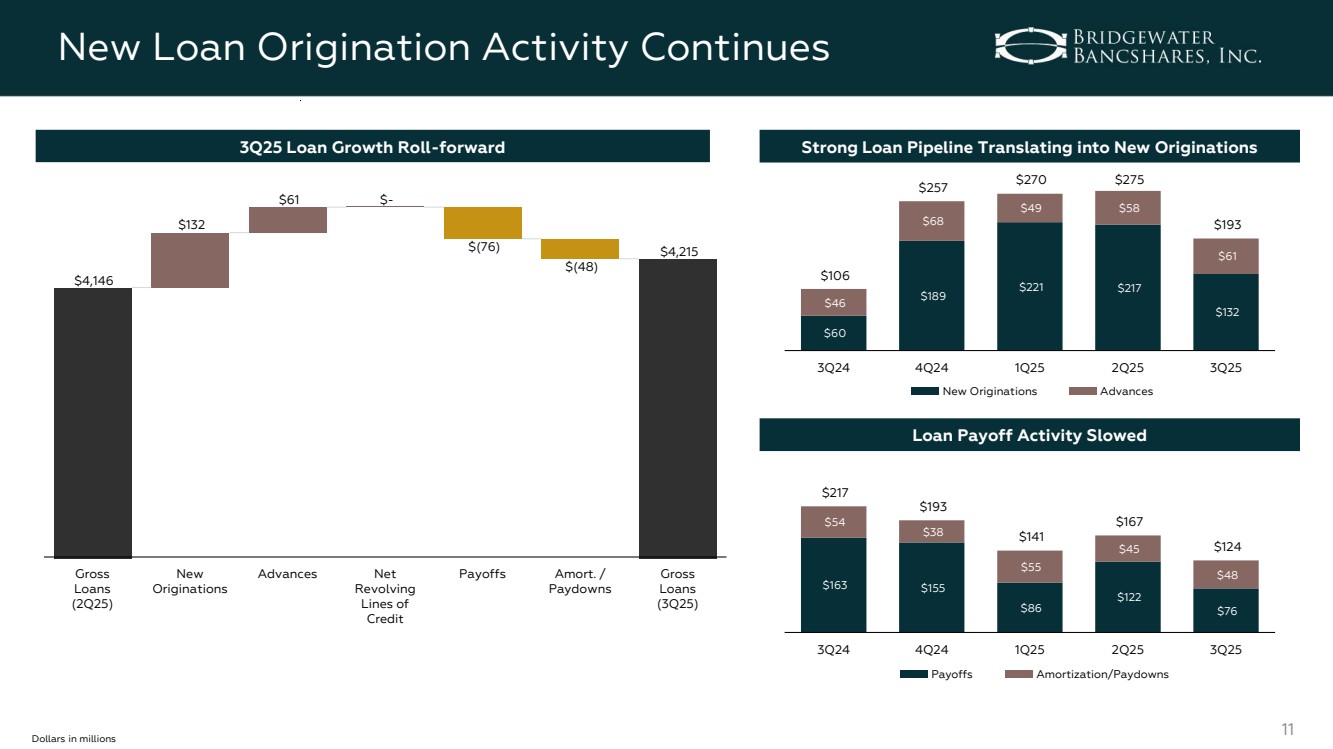

Total gross loans at September 30, 2025 were $4.21 billion, an increase of $68.8 million, or 6.6% annualized, over total gross loans of $4.15 billion at June 30, 2025, and an increase of $529.0 million, or 14.4%, over total gross loans of $3.69 billion at September 30, 2024.

| ● | The increase in the loan portfolio during the third quarter of 2025 was due to strong loan originations and lower loan payoffs and paydowns. |

Deposits

(dollars in thousands) | | September 30, 2025 | | June 30, 2025 | | March 31, 2025 | | December 31, 2024 | | September 30, 2024 | | |||||

Noninterest Bearing Transaction Deposits | | $ | 822,632 | | $ | 787,868 | | $ | 791,528 | | $ | 800,763 | | $ | 713,309 | |

Interest Bearing Transaction Deposits | | | 860,774 | | | 791,748 | | | 840,378 | | | 862,242 | | | 805,756 | |

Savings and Money Market Deposits | | | 1,428,726 | | | 1,441,694 | | | 1,372,191 | | | 1,259,503 | | | 980,345 | |

Time Deposits | | | 346,214 | | | 344,882 | | | 326,821 | | | 338,506 | | | 347,080 | |

Brokered Deposits | | | 834,418 | | | 870,550 | | | 831,539 | | | 825,753 | | | 900,952 | |

Total Deposits | | $ | 4,292,764 | | $ | 4,236,742 | | $ | 4,162,457 | | $ | 4,086,767 | | $ | 3,747,442 | |

Total deposits at September 30, 2025 were $4.29 billion, an increase of $56.0 million, or 5.2% annualized, over total deposits of $4.24 billion at June 30, 2025, and an increase of $545.3 million, or 14.6%, over total deposits of $3.75 billion at September 30, 2024.

| ● | Core deposits, defined as total deposits excluding brokered deposits and certificates of deposits greater than $250,000, increased $92.1 million, or 11.5% annualized, from the second quarter of 2025, and increased $600.2 million, or 22.4%, from the third quarter of 2024. |

Asset Quality

Overall asset quality remained strong due to the Company’s measured risk selection, consistent underwriting standards, active credit oversight, and experienced lending and credit teams.

| ● | Annualized net charge-offs as a percentage of average loans were 0.03%, compared to 0.00% for the second quarter of 2025, and 0.10% for the third quarter of 2024. |

| ● | At September 30, 2025, the Company’s nonperforming assets, which include nonaccrual loans, loans past due 90 days and still accruing, and foreclosed assets, were $10.0 million, or 0.19% of total assets, compared to $10.3 million, or 0.19% of total assets, at June 30, 2025, and $8.8 million, or 0.19% of total assets, at September 30, 2024. |

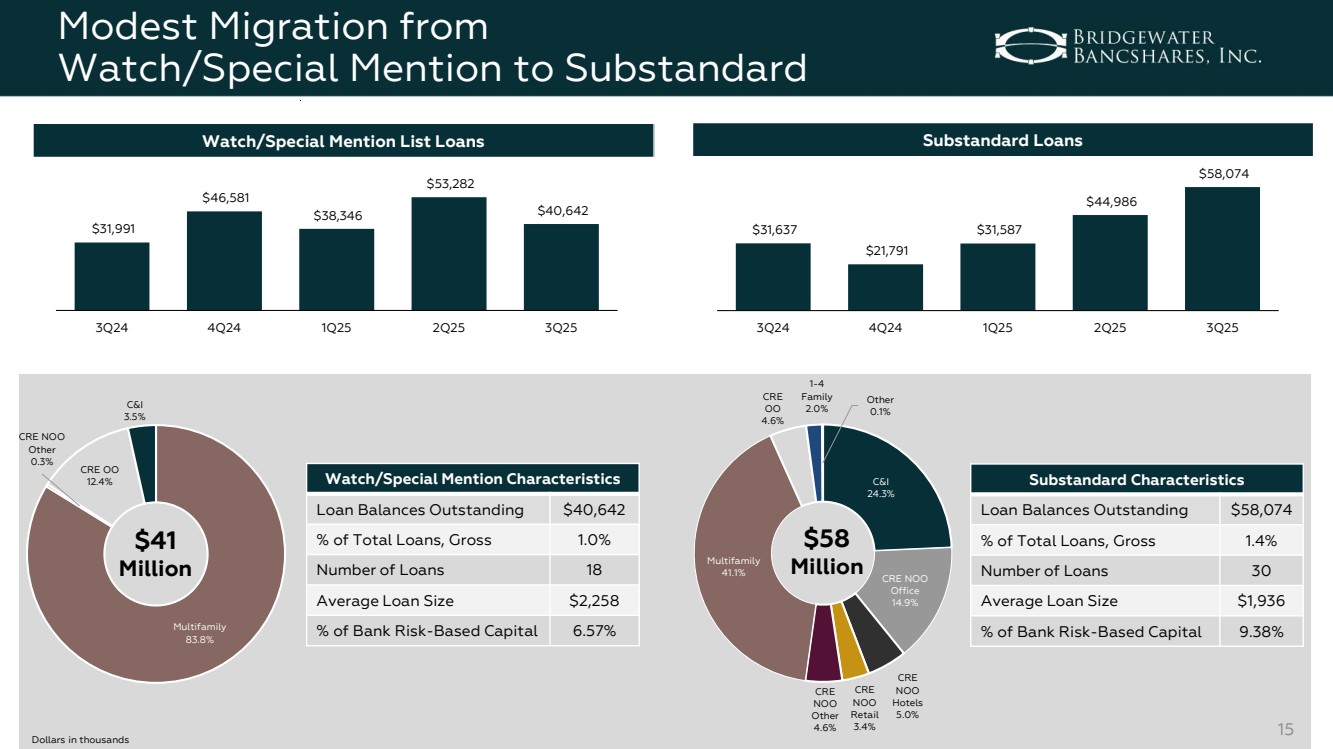

| ● | Loans with potential weaknesses that warranted a watch/special mention risk rating at September 30, 2025 totaled $40.6 million, compared to $53.3 million at June 30, 2025, and $32.0 million at September 30, 2024. |

| ● | Loans that warranted a substandard risk rating at September 30, 2025 totaled $58.1 million, compared to $45.0 million at June 30, 2025, and $31.6 million at September 30, 2024. |

Page 6 of 19

| ● | The linked-quarter increase in loans that warranted a substandard risk rating was primarily due to one loan that migrated from special mention to substandard. |

Capital

Total shareholders’ equity at September 30, 2025 was $497.5 million, an increase of $21.2 million, or 17.6% annualized, compared to total shareholders’ equity of $476.3 million at June 30, 2025, and an increase of $45.3 million, or 10.0%, over total shareholders’ equity of $452.2 million at September 30, 2024.

| ● | The linked-quarter increase was primarily due to net income retained and a decrease in unrealized losses in the securities portfolio, offset partially by a decrease in unrealized gains in the derivatives portfolio and preferred stock dividends. |

| ● | The year-over-year increase was primarily due to net income retained and a decrease in unrealized losses in the securities portfolio, offset partially by a decrease in unrealized gains in the derivatives portfolio, preferred stock dividends, and stock repurchases. |

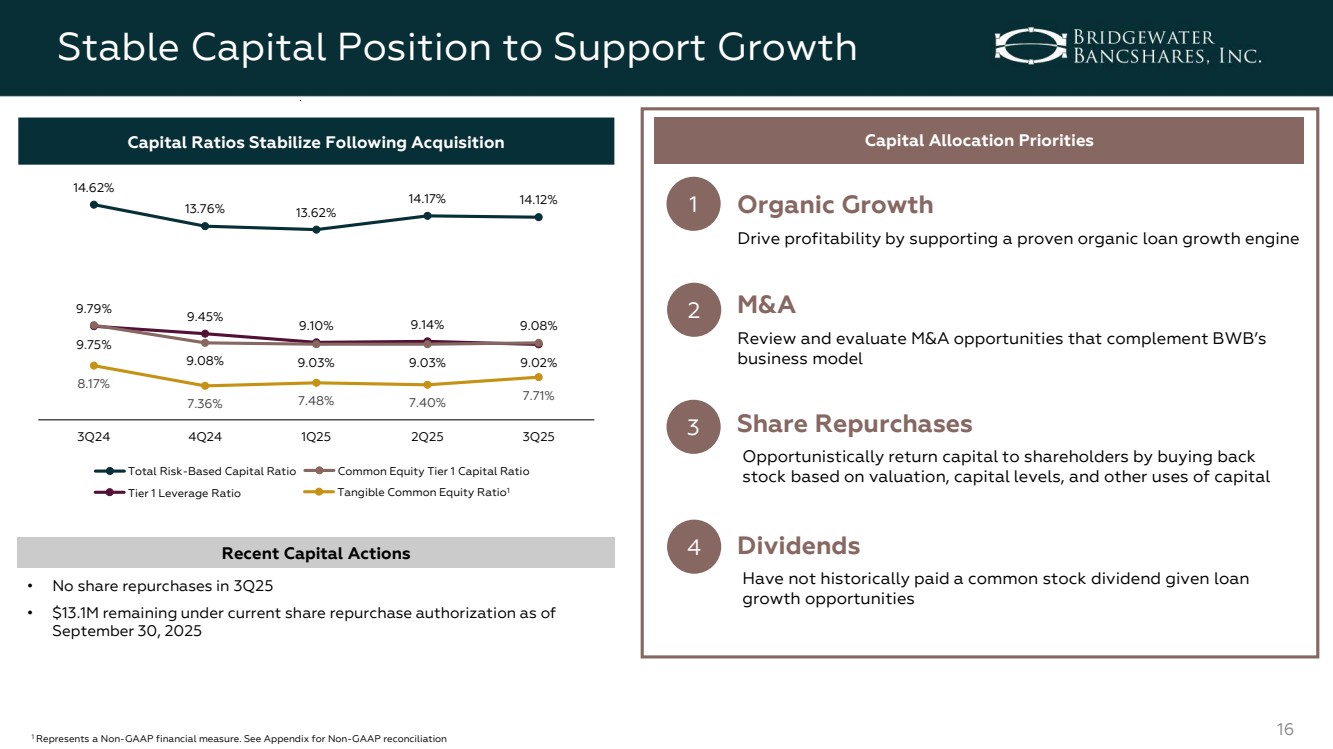

| ● | The Consolidated Common Equity Tier 1 Risk-Based Capital Ratio was 9.08% at September 30, 2025, compared to 9.03% at June 30, 2025, and 9.79% at September 30, 2024. |

| ● | Tangible common equity as a percentage of tangible assets, a non-GAAP financial measure, was 7.71% at September 30, 2025, compared to 7.40% at June 30, 2025, and 8.17% at September 30, 2024. |

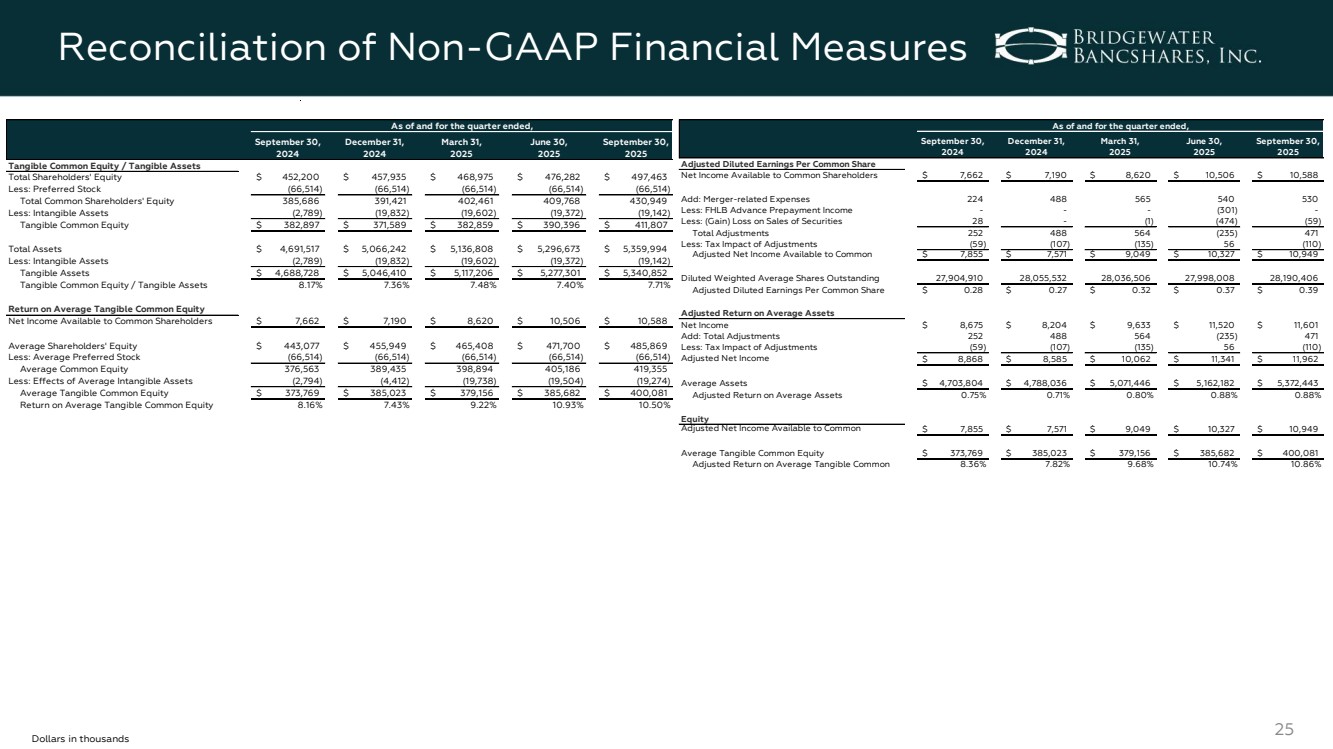

Tangible book value per share, a non-GAAP financial measure, was $14.93 as of September 30, 2025, an increase of 20.0% annualized from $14.21 as of June 30, 2025, and an increase of 6.9% from $13.96 as of September 30, 2024.

The Company did not repurchase any shares of its common stock during the third quarter of 2025.

| ● | The Company had $13.1 million remaining under its current share repurchase authorization at September 30, 2025. |

Today, the Company also announced that its Board of Directors has declared a quarterly cash dividend on its 5.875% Non-Cumulative Perpetual Preferred Stock, Series A (“Series A Preferred Stock”). The quarterly cash dividend of $36.72 per share, equivalent to $0.3672 per depositary share, each representing a 1/100th interest in a share of the Series A Preferred Stock (Nasdaq: BWBBP), is payable on December 1, 2025 to shareholders of record of the Series A Preferred Stock at the close of business on November 14, 2025.

Conference Call and Webcast

The Company will host a conference call to discuss its third quarter 2025 financial results on Wednesday, October 22, 2025 at 8:00 a.m. Central Time. The conference call can be accessed by dialing 844-481-2913 and requesting to join the Bridgewater Bancshares earnings call. To listen to a replay of the conference call via phone, please dial 877-344-7529 and enter access code 1563263. The replay will be available through October 29, 2025. The conference call will also be available via a live webcast on the Investor Relations section of the Company’s website, investors.bridgewaterbankmn.com, and archived for replay.

About the Company

Bridgewater Bancshares, Inc. (Nasdaq: BWB) is a St. Louis Park, Minnesota-based financial holding company founded in 2005. Its banking subsidiary, Bridgewater Bank, is a premier, full-service bank dedicated to providing responsive support and simple solutions to businesses, entrepreneurs, and successful individuals across the Twin Cities. Bridgewater offers a comprehensive suite of products and services spanning deposits, lending, and treasury management solutions. Bridgewater has also received numerous awards for its banking services and esteemed corporate culture. With total assets of $5.4 billion and nine strategically located branches as of September 30, 2025, Bridgewater is one of the largest locally-led banks in Minnesota and is committed to being the finest entrepreneurial bank. For more information, please visit www.bridgewaterbankmn.com.

Use of Non-GAAP Financial Measures

In addition to the results presented in accordance with U.S. Generally Accepted Accounting Principles (“GAAP”), the Company routinely supplements its evaluation with an analysis of certain non-GAAP financial measures. The Company believes these non-GAAP financial measures, in addition to the related GAAP measures, provide meaningful information to investors to help them understand the Company’s operating performance and trends, and to facilitate comparisons with the performance of peers. These disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. Reconciliations of non-GAAP disclosures used in this earnings

Page 7 of 19

release to the comparable GAAP measures are provided in the accompanying tables.

Forward-Looking Statements

This earnings release contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements include, without limitation, statements concerning plans, estimates, calculations, forecasts and projections with respect to the anticipated future performance of the Company. These statements are often, but not always, identified by words such as “may”, “might”, “should”, “could”, “predict”, “potential”, “believe”, “expect”, “continue”, “will”, “anticipate”, “seek”, “estimate”, “intend”, “plan”, “projection”, “would”, “annualized”, “target” and “outlook”, or the negative version of those words or other comparable words of a future or forward-looking nature.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: interest rate risk, including the effects of changes in interest rates; effects on the U.S. economy resulting from the threat or implementation of new, or changes to, existing policies, regulations, regulatory and governmental agencies and executive orders, including with respect to tariffs, immigration, DEI and ESG initiatives, consumer protection, foreign policy, and tax regulations; fluctuations in the values of the securities held in our securities portfolio, including as the result of changes in interest rates; business and economic conditions generally and in the financial services industry, nationally and within our market area, including the level and impact of inflation, including future monetary policies of the Federal Reserve in response thereto, and possible recession; the effects of developments and events in the financial services industry, including the large-scale deposit withdrawals over a short period of time that resulted in several bank failures; credit risk and risks from concentrations (by type of borrower, geographic area, collateral and industry) within the Company’s loan portfolio or large loans to certain borrowers (including CRE loans); the overall health of the local and national real estate market; our ability to successfully manage credit risk; our ability to maintain an adequate level of allowance for credit losses on loans; new or revised accounting standards as may be adopted by state and federal regulatory agencies, the Financial Accounting Standards Board, Securities and Exchange Commission or Public Company Accounting Oversight Board; the concentration of large deposits from certain clients, including those who have balances above current Federal Deposit Insurance Corporation insurance limits; our ability to successfully manage liquidity risk, which may increase our dependence on non-core funding sources such as brokered deposits, and negatively impact our cost of funds; our ability to raise additional capital to implement our business plan; our ability to implement our growth strategy and manage costs effectively; the composition of our senior leadership team and our ability to attract and retain key personnel; talent and labor shortages and employee turnover; the occurrence of fraudulent activity, breaches or failures of our or our third-party vendors’ information security controls or cybersecurity-related incidents, including as a result of sophisticated attacks using artificial intelligence and similar tools or as a result of insider fraud; interruptions involving our information technology and telecommunications systems or third-party servicers; competition in the financial services industry, including from nonbank competitors such as credit unions, “fintech” companies and digital asset service providers; the effectiveness of our risk management framework; rapid technological changes implemented by us and other parties in the financial services industry, including third-party vendors, which may be more difficult to implement or more expensive than anticipated or which may have unforeseen consequence to us and our customers, including the development and implementation of tools incorporating artificial intelligence; the commencement, cost and outcome of litigation and other legal proceedings and regulatory actions against us; the impact of recent and future legislative and regulatory changes, domestic or foreign; risks related to climate change and the negative impact it may have on our customers and their businesses; the imposition of tariffs or other governmental policies impacting the global supply chain and the value of products produced by our commercial borrowers; severe weather, natural disasters, wide spread disease or pandemics, acts of war or terrorism or other adverse external events, including ongoing conflicts in the Middle East and the Russian invasion of Ukraine; potential impairment to the goodwill the Company recorded in connection with acquisitions; risks associated with our integration of FMCB, including the possibility that the merger may be more difficult or expensive to integrate than anticipated, and the effect of the merger on the Company’s customer and employee relationships and operating results; changes to U.S. or state tax laws, regulations and governmental policies concerning the Company’s general business, including changes in interpretation or prioritization of such rules and regulations; the impact of bank failures or adverse developments at other banks and related negative publicity about the banking industry in general on investor and depositor sentiment regarding the stability and liquidity of banks; the effects of the current U.S. government shutdown and its impact on our customers; and any other risks described in the “Risk Factors” sections of reports filed by the Company with the Securities and Exchange Commission.

Page 8 of 19

Any forward-looking statement made by us in this press release is based only on information currently available to us and speaks only as of the date on which it is made. The Company undertakes no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

Page 9 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Financial Highlights

(dollars in thousands, except share data)

| | As of and for the Three Months Ended | | |||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, |

| |||||

(dollars in thousands) |

| 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 |

| |||||

| | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | |

Income Statement | | | | | | | | | | | | | | | | |

Net Interest Income | | $ | 34,091 | | $ | 32,452 | | $ | 30,208 | | $ | 26,967 | | $ | 25,599 | |

Provision for Credit Losses | | | 1,100 | | | 2,000 | | | 1,500 | | | 2,175 | | | — | |

Noninterest Income | | | 2,061 | | | 3,627 | | | 2,079 | | | 2,533 | | | 1,522 | |

Noninterest Expense | | | 19,956 | | | 18,941 | | | 18,136 | | | 16,812 | | | 15,760 | |

Net Income | | | 11,601 | | | 11,520 | | | 9,633 | | | 8,204 | | | 8,675 | |

Net Income Available to Common Shareholders | | | 10,588 | | | 10,506 | | | 8,620 | | | 7,190 | | | 7,662 | |

| | | | | | | | | | | | | | | | |

Per Common Share Data | | | | | | | | | | | | | | | | |

Basic Earnings Per Share | | $ | 0.38 | | $ | 0.38 | | $ | 0.31 | | $ | 0.26 | | $ | 0.28 | |

Diluted Earnings Per Share | | | 0.38 | | | 0.38 | | | 0.31 | | | 0.26 | | | 0.27 | |

Adjusted Diluted Earnings Per Share (1) | | | 0.39 | | | 0.37 | | | 0.32 | | | 0.27 | | | 0.28 | |

Book Value Per Share | | | 15.62 | | | 14.92 | | | 14.60 | | | 14.21 | | | 14.06 | |

Tangible Book Value Per Share (1) | | | 14.93 | | | 14.21 | | | 13.89 | | | 13.49 | | | 13.96 | |

Basic Weighted Average Shares Outstanding | | | 27,504,840 | | | 27,460,982 | | | 27,568,772 | | | 27,459,433 | | | 27,382,798 | |

Diluted Weighted Average Shares Outstanding | | | 28,190,406 | | | 27,998,008 | | | 28,036,506 | | | 28,055,532 | | | 27,904,910 | |

Shares Outstanding at Period End | | | 27,584,732 | | | 27,470,283 | | | 27,560,150 | | | 27,552,449 | | | 27,425,690 | |

| | | | | | | | | | | | | | | | |

Financial Ratios | | | | | | | | | | | | | | | | |

Return on Average Assets (2) | | | 0.86 | % | | 0.90 | % | | 0.77 | % | | 0.68 | % | | 0.73 | % |

Pre-Provision Net Revenue Return on Average Assets (1)(2) | | | 1.19 | | | 1.27 | | | 1.13 | | | 1.05 | | | 0.96 | |

Return on Average Shareholders' Equity (2) | | | 9.47 | | | 9.80 | | | 8.39 | | | 7.16 | | | 7.79 | |

Return on Average Tangible Common Equity (1)(2) | | | 10.50 | | | 10.93 | | | 9.22 | | | 7.43 | | | 8.16 | |

Net Interest Margin (3) | | | 2.63 | | | 2.62 | | | 2.51 | | | 2.32 | | | 2.24 | |

Core Net Interest Margin (1)(3) | | | 2.52 | | | 2.49 | | | 2.37 | | | 2.24 | | | 2.16 | |

Cost of Total Deposits | | | 3.19 | | | 3.16 | | | 3.18 | | | 3.40 | | | 3.58 | |

Cost of Funds | | | 3.25 | | | 3.19 | | | 3.17 | | | 3.38 | | | 3.54 | |

Efficiency Ratio (1) | | | 54.7 | | | 52.6 | | | 55.5 | | | 56.8 | | | 58.0 | |

Noninterest Expense to Average Assets (2) | | | 1.47 | | | 1.47 | | | 1.45 | | | 1.40 | | | 1.33 | |

| | | | | | | | | | | | | | | | |

Adjusted Financial Ratios (1) | | | | | | | | | | | | | | | | |

Adjusted Return on Average Assets | | | 0.88 | % | | 0.88 | % | | 0.80 | % | | 0.71 | % | | 0.75 | % |

Adjusted Pre-Provision Net Revenue Return on Average Assets (2) | | | 1.23 | | | 1.31 | | | 1.18 | | | 1.09 | | | 0.98 | |

Adjusted Return on Average Shareholders' Equity | | | 9.77 | | | 9.64 | | | 8.77 | | | 7.49 | | | 7.96 | |

Adjusted Return on Average Tangible Common Equity | | | 10.86 | | | 10.74 | | | 9.68 | | | 7.82 | | | 8.36 | |

Adjusted Efficiency Ratio | | | 53.2 | | | 51.5 | | | 53.7 | | | 55.2 | | | 57.2 | |

Adjusted Noninterest Expense to Average Assets | | | 1.43 | | | 1.43 | | | 1.41 | | | 1.36 | | | 1.31 | |

| | | | | | | | | | | | | | | | |

Balance Sheet | | | | | | | | | | | | | | | | |

Total Assets | | $ | 5,359,994 | | $ | 5,296,673 | | $ | 5,136,808 | | $ | 5,066,242 | | $ | 4,691,517 | |

Total Loans, Gross | | | 4,214,554 | | | 4,145,799 | | | 4,020,076 | | | 3,868,514 | | | 3,685,590 | |

Deposits | | | 4,292,764 | | | 4,236,742 | | | 4,162,457 | | | 4,086,767 | | | 3,747,442 | |

Total Shareholders' Equity | | | 497,463 | | | 476,282 | | | 468,975 | | | 457,935 | | | 452,200 | |

Loan to Deposit Ratio | | | 98.2 | % | | 97.9 | % | | 96.6 | % | | 94.7 | % | | 98.3 | % |

Core Deposits to Total Deposits (4) | | | 76.4 | | | 75.2 | | | 76.2 | | | 76.0 | | | 71.5 | |

| | | | | | | | | | | | | | | | |

Asset Quality |

| | |

| | |

| | |

| | |

| | | |

Net Loan Charge-Offs to Average Loans (2) | | | 0.03 | % | | 0.00 | % | | 0.00 | % | | 0.03 | % | | 0.10 | % |

Nonperforming Assets to Total Assets (5) | | | 0.19 | | | 0.19 | | | 0.20 | | | 0.01 | | | 0.19 | |

Allowance for Credit Losses to Total Loans | | | 1.34 |

| | 1.35 |

| | 1.34 |

| | 1.35 |

| | 1.38 |

|

Page 10 of 19

| | As of and for the Three Months Ended | | |||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | | |||||

(dollars in thousands) |

| 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 | | |||||

| | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | |

Capital Ratios (Consolidated) (6) | | | | | | | | | | | | | | | | |

Tier 1 Leverage Ratio | | | 9.02 | % | | 9.14 | % | | 9.10 | % | | 9.45 | % | | 9.75 | % |

Common Equity Tier 1 Risk-based Capital Ratio | | | 9.08 | | | 9.03 | | | 9.03 | | | 9.08 | | | 9.79 | |

Tier 1 Risk-based Capital Ratio | | | 10.52 | | | 10.51 | | | 10.55 | | | 10.64 | | | 11.44 | |

Total Risk-based Capital Ratio | | | 14.12 | | | 14.17 | | | 13.62 | | | 13.76 | | | 14.62 | |

Tangible Common Equity to Tangible Assets (1) | | | 7.71 | | | 7.40 | | | 7.48 | | | 7.36 | | | 8.17 | |

| (1) | Represents a non-GAAP financial measure. See "Non-GAAP Financial Measures" for further details. |

| (2) | Annualized. |

| (3) | Amounts calculated on a tax-equivalent basis using the statutory federal tax rate of 21%. |

| (4) | Core deposits are defined as total deposits less brokered deposits and certificates of deposit greater than $250,000. |

| (5) | Nonperforming assets are defined as nonaccrual loans plus 90 days past due and still accruing plus foreclosed assets. |

| (6) | Preliminary data. Current period subject to change prior to filings with applicable regulatory agencies. |

Page 11 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Consolidated Balance Sheets

(dollars in thousands, except share data)

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | |||||

| | 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 | |||||

| | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | | | | (Unaudited) |

Assets | | | | | | | | | | | | | | | |

Cash and Cash Equivalents | | $ | 131,818 | | $ | 217,495 | | $ | 166,205 | | $ | 229,760 | | $ | 191,859 |

Bank-Owned Certificates of Deposit | |

| 3,658 | |

| 3,897 | |

| 4,139 | |

| 4,377 | |

| — |

Securities Available for Sale, at Fair Value | |

| 826,473 | |

| 743,889 | |

| 764,626 | |

| 768,247 | |

| 664,715 |

Loans, Net of Allowance for Credit Losses | |

| 4,149,882 | | | 4,082,405 | | | 3,959,092 | |

| 3,809,436 | |

| 3,628,867 |

Federal Home Loan Bank (FHLB) Stock, at Cost | |

| 21,373 | |

| 21,472 | |

| 18,984 | |

| 19,297 | |

| 18,626 |

Premises and Equipment, Net | |

| 50,955 | |

| 49,979 | |

| 49,442 | |

| 49,533 | |

| 47,777 |

Foreclosed Assets | | | — | | | 185 | | | — | | | — | | | 434 |

Accrued Interest | |

| 19,244 | |

| 17,711 | |

| 17,700 | |

| 17,711 | |

| 16,750 |

Goodwill | |

| 11,982 | |

| 11,982 | |

| 11,982 | |

| 11,982 | |

| 2,626 |

Other Intangible Assets, Net | |

| 7,160 | |

| 7,390 | |

| 7,620 | |

| 7,850 | |

| 163 |

Bank-Owned Life Insurance | | | 46,121 | | | 45,413 | | | 45,025 | | | 44,646 | | | 38,219 |

Other Assets | |

| 91,328 | |

| 94,855 | |

| 91,993 | |

| 103,403 | |

| 81,481 |

Total Assets | | $ | 5,359,994 | | $ | 5,296,673 | | $ | 5,136,808 | | $ | 5,066,242 | | $ | 4,691,517 |

| | | | | | | | | | | | | | | |

Liabilities and Equity | |

| | |

| | |

| | |

| | |

| |

Liabilities | |

| | |

| | |

| | |

| | |

| |

Deposits: | |

| | |

| | |

| | |

| | |

| |

Noninterest Bearing | | $ | 822,632 | | $ | 787,868 | | $ | 791,528 | | $ | 800,763 | | $ | 713,309 |

Interest Bearing | |

| 3,470,132 | |

| 3,448,874 | |

| 3,370,929 | |

| 3,286,004 | |

| 3,034,133 |

Total Deposits | |

| 4,292,764 | |

| 4,236,742 | |

| 4,162,457 | |

| 4,086,767 | |

| 3,747,442 |

Notes Payable | |

| — | |

| 13,750 | |

| 13,750 | |

| 13,750 | |

| 13,750 |

FHLB Advances | |

| 404,500 | |

| 404,500 | |

| 349,500 | |

| 359,500 | |

| 349,500 |

Subordinated Debentures, Net of Issuance Costs | |

| 108,588 | |

| 108,689 | |

| 79,766 | |

| 79,670 | |

| 79,574 |

Accrued Interest Payable | |

| 5,208 | |

| 4,110 | |

| 4,525 | |

| 4,008 | |

| 3,458 |

Other Liabilities | |

| 51,471 | |

| 52,600 | |

| 57,835 | |

| 64,612 | |

| 45,593 |

Total Liabilities | | | 4,862,531 | | | 4,820,391 | | | 4,667,833 | | | 4,608,307 | | | 4,239,317 |

| | | | | | | | | | | | | | | |

Shareholders' Equity | |

| | |

| | |

| | |

| | |

| |

Preferred Stock- $0.01 par value; Authorized 10,000,000 | | | | | | | | | | | | | | | |

Preferred Stock - Issued and Outstanding 27,600 Series A shares ($2,500 liquidation preference) at September 30, 2025 (unaudited), June 30, 2025 (unaudited), March 31, 2025 (unaudited), December 31, 2024, and September 30, 2024 (unaudited) | |

| 66,514 | | | 66,514 | | | 66,514 | |

| 66,514 | |

| 66,514 |

Common Stock- $0.01 par value; Authorized 75,000,000 | |

| | |

| | |

| | |

| | |

| |

Common Stock - Issued and Outstanding 27,584,732 at September 30, 2025 (unaudited), 27,470,283 at June 30, 2025 (unaudited), 27,560,150 at March 31, 2025 (unaudited), 27,552,449 at December 31, 2024, and 27,425,690 at September 30, 2024 (unaudited) | |

| 276 | | | 275 | | | 276 | |

| 276 | |

| 274 |

Additional Paid-In Capital | |

| 97,101 | |

| 95,174 | |

| 95,503 | |

| 95,088 | |

| 94,597 |

Retained Earnings | |

| 339,135 | |

| 328,547 | |

| 318,041 | |

| 309,421 | |

| 302,231 |

Accumulated Other Comprehensive Loss | |

| (5,563) | |

| (14,228) | |

| (11,359) | |

| (13,364) | |

| (11,416) |

Total Shareholders' Equity | |

| 497,463 | |

| 476,282 | |

| 468,975 | |

| 457,935 | |

| 452,200 |

Total Liabilities and Equity | | $ | 5,359,994 | | $ | 5,296,673 | | $ | 5,136,808 | | $ | 5,066,242 | | $ | 4,691,517 |

Page 12 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Consolidated Statements of Income

(dollars in thousands, except per share data)

| | Three Months Ended | | Nine Months Ended | |||||||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | | September 30, | | September 30, | |||||||

| | 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 |

| 2025 |

| 2024 | |||||||

| | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) | | | (Unaudited) |

Interest Income | | | | | | | | | | | | | | | | | | | | | |

Loans, Including Fees | | $ | 60,038 | | $ | 57,888 | | $ | 53,820 | | $ | 51,870 | | $ | 51,895 | | $ | 171,746 | | $ | 152,861 |

Investment Securities | |

| 10,371 | |

| 9,200 | |

| 9,397 | |

| 9,109 | |

| 8,725 | |

| 28,968 | |

| 24,818 |

Other | |

| 3,224 | |

| 2,110 | |

| 2,491 | |

| 2,345 | |

| 2,407 | |

| 7,825 | |

| 4,895 |

Total Interest Income | |

| 73,633 | |

| 69,198 | |

| 65,708 | |

| 63,324 | |

| 63,027 | |

| 208,539 | |

| 182,574 |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

Interest Expense | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

Deposits | |

| 34,615 | |

| 32,497 | |

| 32,103 | |

| 32,810 | |

| 34,187 | |

| 99,215 | |

| 95,995 |

Federal Funds Purchased | |

| — | |

| 16 | |

| — | |

| 42 | |

| 2 | |

| 16 | |

| 1,159 |

Notes Payable | |

| 106 | |

| 260 | |

| 258 | |

| 275 | |

| 296 | |

| 624 | |

| 887 |

FHLB Advances | |

| 2,933 | |

| 2,852 | |

| 2,156 | |

| 2,229 | |

| 1,942 | |

| 7,941 | |

| 6,325 |

Subordinated Debentures | |

| 1,888 | |

| 1,121 | |

| 983 | |

| 1,001 | |

| 1,001 | |

| 3,992 | |

| 2,982 |

Total Interest Expense | |

| 39,542 | |

| 36,746 | |

| 35,500 | |

| 36,357 | |

| 37,428 | |

| 111,788 | |

| 107,348 |

| | | | | | | | | | | | | | | | | | | | | |

Net Interest Income | |

| 34,091 | |

| 32,452 | |

| 30,208 | |

| 26,967 | |

| 25,599 | |

| 96,751 | |

| 75,226 |

Provision for Credit Losses | |

| 1,100 | |

| 2,000 | |

| 1,500 | |

| 2,175 | |

| — | |

| 4,600 | |

| 1,350 |

| | | | | | | | | | | | | | | | | | | | | |

Net Interest Income After Provision for Credit Losses | |

| 32,991 | |

| 30,452 | |

| 28,708 | |

| 24,792 | |

| 25,599 | |

| 92,151 | |

| 73,876 |

| | | | | | | | | | | | | | | | | | | | | |

Noninterest Income | | | | | | | | | | | | | | | | | | | | | |

Customer Service Fees | | | 501 | | | 496 | | | 495 | | | 394 | | | 373 | | | 1,492 | | | 1,081 |

Net Gain (Loss) on Sales of Securities | | | 59 | | | 474 | | | 1 | | | — | | | (28) | | | 534 | | | 385 |

Net Gain on Sales of Foreclosed Assets | | | — | | | — | | | — | | | 62 | | | — | | | — | | | — |

Letter of Credit Fees | | | 383 | | | 323 | | | 455 | | | 849 | | | 424 | | | 1,161 | | | 1,127 |

Debit Card Interchange Fees | | | 173 | | | 152 | | | 137 | | | 145 | | | 152 | | | 462 | | | 448 |

Swap Fees | | | — | | | 938 | | | 42 | | | 521 | | | 26 | | | 980 | | | 26 |

Bank-Owned Life Insurance | | | 440 | | | 387 | | | 379 | | | 362 | | | 352 | | | 1,206 | | | 965 |

Investment Advisory Fees | | | 208 | | | 213 | | | 325 | | | — | | | — | | | 746 | | | — |

FHLB Prepayment Income | | | — | | | 301 | | | — | | | — | | | — | | | 301 | | | — |

Other Income | | | 297 | | | 343 | | | 245 | | | 200 | | | 223 | | | 885 | | | 803 |

Total Noninterest Income | | | 2,061 | | | 3,627 | | | 2,079 | | | 2,533 | | | 1,522 | | | 7,767 | | | 4,835 |

| | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense | | | | | | | | | | | | | | | | | | | | | |

Salaries and Employee Benefits | | | 12,229 | | | 11,363 | | | 11,371 | | | 10,605 | | | 9,851 | | | 34,963 | | | 28,959 |

Occupancy and Equipment | | | 1,266 | | | 1,274 | | | 1,234 | | | 1,181 | | | 1,069 | | | 3,774 | | | 3,218 |

FDIC Insurance Assessment | | | 775 | | | 750 | | | 450 | | | 609 | | | 750 | | | 1,975 | | | 2,350 |

Data Processing | | | 637 | | | 625 | | | 619 | | | 445 | | | 368 | | | 1,881 | | | 1,252 |

Professional and Consulting Fees | | | 1,261 | | | 1,110 | | | 994 | | | 989 | | | 1,149 | | | 3,365 | | | 2,890 |

Derivative Collateral Fees | | | 309 | | | 372 | | | 451 | | | 426 | | | 381 | | | 1,132 | | | 1,395 |

Information Technology and Telecommunications | | | 973 | | | 971 | | | 971 | | | 877 | | | 840 | | | 2,915 | | | 2,448 |

Marketing and Advertising | | | 658 | | | 435 | | | 327 | | | 479 | | | 367 | | | 1,420 | | | 1,006 |

Intangible Asset Amortization | | | 230 | | | 230 | | | 230 | | | 52 | | | 9 | | | 690 | | | 26 |

Other Expense | | | 1,618 | | | 1,811 | | | 1,489 | | | 1,149 | | | 976 | | | 4,918 | | | 2,944 |

Total Noninterest Expense | | | 19,956 | | | 18,941 | | | 18,136 | | | 16,812 | | | 15,760 | | | 57,033 | | | 46,488 |

| | | | | | | | | | | | | | | | | | | | | |

Income Before Income Taxes | | | 15,096 | | | 15,138 | | | 12,651 | | | 10,513 | | | 11,361 | | | 42,885 | | | 32,223 |

Provision for Income Taxes | | | 3,495 | | | 3,618 | | | 3,018 | | | 2,309 | | | 2,686 | | | 10,131 | | | 7,602 |

Net Income | | | 11,601 | | | 11,520 | | | 9,633 | | | 8,204 | | | 8,675 | | | 32,754 | | | 24,621 |

Preferred Stock Dividends | | | (1,013) | | | (1,014) | | | (1,013) | | | (1,014) | | | (1,013) | | | (3,040) | | | (3,040) |

Net Income Available to Common Shareholders | | $ | 10,588 | | $ | 10,506 | | $ | 8,620 | | $ | 7,190 | | $ | 7,662 | | $ | 29,714 | | $ | 21,581 |

| | | | | | | | | | | | | | | | | | | | | |

Earnings Per Share | | | | | | | | | | | | | | | | | | | | | |

Basic | | $ | 0.38 | | $ | 0.38 | | $ | 0.31 | | $ | 0.26 | | $ | 0.28 | | $ | 1.08 | | $ | 0.79 |

Diluted | | | 0.38 | | | 0.38 | | | 0.31 | | | 0.26 | | | 0.27 | | | 1.06 | | | 0.77 |

Page 13 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Analysis of Average Balances, Yields and Rates

(dollars in thousands, except per share data)

(Unaudited)

| | For the Three Months Ended |

| ||||||||||||||||||||||

| | September 30, 2025 | | June 30, 2025 |

| September 30, 2024 |

| ||||||||||||||||||

| | Average | | Interest | | Yield/ | | Average | | Interest | | Yield/ |

| Average | | Interest | | Yield/ |

| ||||||

(dollars in thousands) |

| Balance |

| & Fees |

| Rate |

| Balance |

| & Fees |

| Rate |

| Balance |

| & Fees |

| Rate |

| ||||||

Interest Earning Assets: | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash Investments | | $ | 256,174 | | $ | 2,732 | | 4.23 | % | $ | 166,164 | | $ | 1,681 | | 4.06 | % | $ | 157,114 | | $ | 1,971 | | 4.99 | % |

Investment Securities: | | | | | | | | | | | | | | | | | | | | | | | | | |

Taxable Investment Securities | |

| 730,643 | | | 9,448 | | 5.13 | |

| 734,998 | | | 8,883 | | 4.85 | |

| 668,429 | |

| 8,406 | | 5.00 | |

Tax-Exempt Investment Securities (1) | |

| 81,962 | | | 1,168 | | 5.66 | |

| 31,940 | | | 401 | | 5.04 | |

| 31,496 | |

| 402 | | 5.08 | |

Total Investment Securities | |

| 812,605 | |

| 10,616 | | 5.18 | |

| 766,938 | |

| 9,284 | | 4.86 | |

| 699,925 | |

| 8,808 | | 5.01 | |

Loans (1)(2) | |

| 4,132,987 | | | 60,317 | | 5.79 | |

| 4,064,540 | | | 58,122 | | 5.74 | |

| 3,721,654 | | | 52,118 | | 5.57 | |

Federal Home Loan Bank Stock | |

| 21,373 | | | 492 | | 9.12 | |

| 21,416 | | | 429 | | 8.03 | |

| 16,828 | | | 436 | | 10.31 | |

Total Interest Earning Assets | |

| 5,223,139 | |

| 74,157 | | 5.63 | % |

| 5,019,058 | |

| 69,516 | | 5.56 | % |

| 4,595,521 | |

| 63,333 | | 5.48 | % |

Noninterest Earning Assets | | | 149,304 | | | | | | | | 143,124 | | | | | | | | 108,283 | | | | | | |

Total Assets | | $ | 5,372,443 | | | | | | | $ | 5,162,182 | | | | | | | $ | 4,703,804 | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Interest Bearing Liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | |

Deposits: | | | | | | | | | | | | | | | | | | | | | | | | | |

Interest Bearing Transaction Deposits | | $ | 843,905 | | $ | 8,037 | | 3.78 | % | $ | 813,906 | | $ | 7,769 | | 3.83 | % | $ | 804,161 | | $ | 9,369 | | 4.63 | % |

Savings and Money Market Deposits | |

| 1,473,465 | | | 13,465 | | 3.63 | |

| 1,370,831 | | | 12,692 | | 3.71 | |

| 939,665 | | | 10,262 | | 4.34 | |

Time Deposits | |

| 342,926 | | | 3,703 | | 4.28 | |

| 326,024 | | | 3,268 | | 4.02 | |

| 355,050 | | | 3,918 | | 4.39 | |

Brokered Deposits | |

| 856,516 | | | 9,410 | | 4.36 | |

| 833,629 | | | 8,768 | | 4.22 | |

| 989,712 | | | 10,638 | | 4.28 | |

Total Interest Bearing Deposits | | | 3,516,812 | | | 34,615 | | 3.90 | | | 3,344,390 | | | 32,497 | | 3.90 | | | 3,088,588 | | | 34,187 | | 4.40 | |

Federal Funds Purchased | | | — | | | — | | — | |

| 1,369 | | | 16 | | 4.64 | |

| 141 | | | 2 | | 5.72 | |

Notes Payable | | | 5,679 | | | 106 | | 7.40 | |

| 13,750 | | | 260 | | 7.58 | |

| 13,750 | | | 296 | | 8.58 | |

FHLB Advances | | | 404,500 | | | 2,933 | | 2.88 | |

| 404,473 | | | 2,852 | | 2.83 | |

| 309,120 | | | 1,942 | | 2.50 | |

Subordinated Debentures | | | 108,639 | | | 1,888 | | 6.89 | |

| 83,892 | | | 1,121 | | 5.36 | |

| 79,519 | | | 1,001 | | 5.01 | |

Total Interest Bearing Liabilities | |

| 4,035,630 | |

| 39,542 | | 3.89 | % |

| 3,847,874 | |

| 36,746 | | 3.83 | % |

| 3,491,118 | |

| 37,428 | | 4.27 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Bearing Liabilities: | | | | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Bearing Transaction Deposits | |

| 793,760 | | | | | | |

| 774,424 | | | | | | |

| 710,192 | | | | | | |

Other Noninterest Bearing Liabilities | | | 57,184 | | | | | | | | 68,184 | | | | | | | | 59,417 | | | | | | |

Total Noninterest Bearing Liabilities | |

| 850,944 | | | | | | |

| 842,608 | | | | | | |

| 769,609 | | | | | | |

Shareholders' Equity | | | 485,869 | | | | | | | | 471,700 | | | | | | | | 443,077 | | | | | | |

Total Liabilities and Shareholders' Equity | | $ | 5,372,443 | | | | | | | $ | 5,162,182 | | | | | | | $ | 4,703,804 | | | | | | |

Net Interest Income / Interest Rate Spread | | | | |

| 34,615 | | 1.74 | % | | | |

| 32,770 | | 1.73 | % | | | |

| 25,905 | | 1.21 | % |

Net Interest Margin (3) | | | | | | | | 2.63 | % | | | | | | | 2.62 | % | | | | | | | 2.24 | % |

Taxable Equivalent Adjustment: | | | | | | | | | | | | | | | | | | | | | | | | | |

Tax-Exempt Investment Securities and Loans | | | | |

| (524) | | | | | | |

| (318) | | | | | | |

| (306) | | | |

Net Interest Income | | | | | $ | 34,091 | | | | | | | $ | 32,452 | | | | | | | $ | 25,599 | | | |

| (1) | Interest income and average rates for tax-exempt investment securities and loans are presented on a tax-equivalent basis, assuming a statutory federal income tax rate of 21%. |

| (2) | Average loan balances include nonaccrual loans. Interest income on loans includes amortization of deferred loan fees, net of deferred loan costs. |

| (3) | Net interest margin includes the tax equivalent adjustment and represents the annualized results of: (i) the difference between interest income on interest earning assets and the interest expense on interest bearing liabilities, divided by (ii) average interest earning assets for the period. |

Page 14 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Analysis of Average Balances, Yields and Rates

(dollars in thousands, except per share data)

(Unaudited)

| | For the Nine Months Ended |

| ||||||||||||||

| | September 30, 2025 | | September 30, 2024 |

| ||||||||||||

| | Average | | Interest | | Yield/ | | Average | | Interest | | Yield/ | | ||||

(dollars in thousands) |

| Balance |

| & Fees |

| Rate |

| Balance |

| & Fees |

| Rate |

| ||||

Interest Earning Assets: | | | | | | | | | | | | | | | | | |

Cash Investments | | $ | 210,525 | | $ | 6,469 | | 4.11 | % | $ | 104,831 | | $ | 3,722 | | 4.74 | % |

Investment Securities: | | | | | | | | | | | | | | | | | |

Taxable Investment Securities | |

| 744,605 | |

| 27,364 | | 4.91 | |

| 649,538 | |

| 23,867 | | 4.91 | |

Tax-Exempt Investment Securities (1) | |

| 49,987 | |

| 2,030 | | 5.43 | |

| 31,597 | |

| 1,203 | | 5.09 | |

Total Investment Securities | |

| 794,592 | |

| 29,394 | | 4.95 | |

| 681,135 | |

| 25,070 | | 4.92 | |

Loans (1)(2) | | | 4,034,656 | | | 172,418 | | 5.71 | | | 3,740,855 | | | 153,568 | | 5.48 | |

Federal Home Loan Bank Stock | |

| 20,601 | | | 1,356 | | 8.80 | |

| 18,111 | | | 1,173 | | 8.65 | |

Total Interest Earning Assets | |

| 5,060,374 | |

| 209,637 | | 5.54 | % |

| 4,544,932 | |

| 183,533 | | 5.39 | % |

Noninterest Earning Assets | | | 145,373 | | | | | | | | 102,993 | | | | | | |

Total Assets | | $ | 5,205,747 | | | | | | | $ | 4,647,925 | | | | | | |

Interest Bearing Liabilities: | | | | | | | | | | | | | | | | | |

Deposits: | | | | | | | | | | | | | | | | | |

Interest Bearing Transaction Deposits | | $ | 837,504 | | $ | 23,995 | | 3.83 | % | $ | 757,409 | | $ | 25,332 | | 4.47 | % |

Savings and Money Market Deposits | |

| 1,383,876 | | | 38,092 | | 3.68 | |

| 917,051 | | | 28,502 | | 4.15 | |

Time Deposits | |

| 333,199 | | | 10,280 | | 4.13 | |

| 344,484 | | | 10,935 | | 4.24 | |

Brokered Deposits | |

| 841,750 | | | 26,848 | | 4.26 | |

| 993,445 | | | 31,226 | | 4.20 | |

Total Interest Bearing Deposits | | | 3,396,329 | | | 99,215 | | 3.91 | | | 3,012,389 | | | 95,995 | | 4.26 | |

Federal Funds Purchased | |

| 456 | | | 16 | | 4.64 | |

| 27,605 | | | 1,159 | | 5.61 | |

Notes Payable | |

| 11,030 | | | 624 | | 7.57 | |

| 13,750 | | | 887 | | 8.62 | |

FHLB Advances | |

| 388,026 | | | 7,941 | | 2.74 | |

| 311,380 | | | 6,325 | | 2.71 | |

Subordinated Debentures | |

| 90,853 | | | 3,992 | | 5.87 | |

| 79,424 | | | 2,982 | | 5.02 | |

Total Interest Bearing Liabilities | |

| 3,886,694 | |

| 111,788 | | 3.85 | % |

| 3,444,548 | |

| 107,348 | | 4.16 | % |

Noninterest Bearing Liabilities: | | | | | | | | | | | | | | | | | |

Noninterest Bearing Transaction Deposits | |

| 779,897 | | | | | | |

| 700,308 | | | | | | |

Other Noninterest Bearing Liabilities | | | 64,878 | | | | | | | | 67,405 | | | | | | |

Total Noninterest Bearing Liabilities | |

| 844,775 | | | | | | |

| 767,713 | | | | | | |

Shareholders' Equity | | | 474,278 | | | | | | | | 435,664 | | | | | | |

Total Liabilities and Shareholders' Equity | | $ | 5,205,747 | | | | | | | $ | 4,647,925 | | | | | | |

Net Interest Income / Interest Rate Spread | | | | |

| 97,849 | | 1.69 | % | | | |

| 76,185 | | 1.23 | % |

Net Interest Margin (3) | | | | | | | | 2.59 | % | | | | | | | 2.24 | % |

Taxable Equivalent Adjustment: | | | | | | | | | | | | | | | | | |

Tax-Exempt Investment Securities and Loans | | | | |

| (1,098) | | | | | | |

| (959) | | | |

Net Interest Income | | | | | $ | 96,751 | | | | | | | $ | 75,226 | | | |

Page 15 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Asset Quality Summary

(unaudited)

| | As of and for the Three Months Ended | | As of and for the Nine Months Ended | | |||||||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, |

| September 30, | | September 30, | | |||||||

(dollars in thousands) |

| 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 |

| 2025 |

| 2024 | | |||||||

Allowance for Credit Losses | | | | | | | | | | | | | | | | | | | | | | |

Balance at Beginning of Period | | $ | 55,765 | | $ | 53,766 | | $ | 52,277 | | $ | 51,018 | | $ | 51,949 | | $ | 52,277 | | $ | 50,494 | |

Day 1 PCD Allowance | | | — | | | — | | | — | | | 114 | | | — | | | — | | | — | |

Provision for Credit Losses(1) | | | 900 | | | 2,000 | | | 1,500 | | | 1,450 | | | — | | | 4,400 | | | 1,450 | |

Charge-offs | | | (276) | | | (6) | | | (12) | | | (317) | | | (937) | | | (294) | | | (949) | |

Recoveries | | | 1 | | | 5 | | | 1 | | | 12 | | | 6 | | | 7 | | | 23 | |

Net Charge-offs | | $ | (275) | | $ | (1) | | $ | (11) | | $ | (305) | | $ | (931) | | $ | (287) | | $ | (926) | |

Balance at End of Period | | | 56,390 | | | 55,765 | | | 53,766 | | | 52,277 | | | 51,018 | | | 56,390 | | | 51,018 | |

Allowance for Credit Losses to Total Loans | | | 1.34 | % | | 1.35 | % | | 1.34 | % | | 1.35 | % | | 1.38 | % | | 1.34 | % | | 1.38 | % |

| (1) | Includes a day 1 provision for credit losses for non-PCD loans acquired in the FMCB transaction of $950,000 for the three months ended December 31, 2024. |

| | As of and for the Three Months Ended | | As of and for the Nine Months Ended | |||||||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | | September 30, | | September 30, | |||||||

(dollars in thousands) |

| 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 | | 2025 |

| 2024 | |||||||

Provision for Credit Losses on Loans and Leases | | $ | 900 | | $ | 2,000 | | $ | 1,500 | | $ | 1,450 | | $ | — | | $ | 4,400 | | $ | 1,450 |

Provision for (Recovery of) Credit Losses for Off-Balance Sheet Credit Exposures | | | 200 | | | — | | | — | | | 725 | | | — | | | 200 | | | (100) |

Provision for Credit Losses | | $ | 1,100 | | $ | 2,000 | | $ | 1,500 | | $ | 2,175 | | $ | — | | $ | 4,600 | | $ | 1,350 |

| | As of and for the Three Months Ended | | |||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | | |||||

(dollars in thousands) | | 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 | | |||||

Selected Asset Quality Data |

| | |

| | |

| | | | | | | | | |

Loans 30-89 Days Past Due | | $ | 2,906 |

| $ | 12,492 |

| $ | 466 |

| $ | 1,291 |

| $ | 65 |

|

Loans 30-89 Days Past Due to Total Loans | | | 0.07 | % | | 0.30 | % | | 0.01 | % | | 0.03 | % | | 0.00 | % |

Nonperforming Loans | | $ | 9,991 |

| $ | 10,134 |

| $ | 10,290 |

| $ | 301 |

| $ | 8,378 |

|

Nonperforming Loans to Total Loans | | | 0.24 | % | | 0.24 | % | | 0.26 | % | | 0.01 | % | | 0.23 | % |

Nonaccrual Loans to Total Loans | | | 0.24 | | | 0.24 | | | 0.26 | | | 0.01 | | | 0.23 | |

Nonaccrual Loans and Loans Past Due 90 Days and Still Accruing to Total Loans | | | 0.24 | | | 0.24 | | | 0.26 | | | 0.01 | | | 0.23 | |

Foreclosed Assets | | $ | — |

| $ | 185 |

| $ | — |

| $ | — |

| $ | 434 |

|

Nonperforming Assets (1) | | | 9,991 |

| | 10,319 |

| | 10,290 |

| | 301 |

| | 8,812 |

|

Nonperforming Assets to Total Assets (1) | | | 0.19 | % | | 0.19 | % | | 0.20 | % | | 0.01 | % | | 0.19 | % |

Net Loan Charge-Offs (Annualized) to Average Loans | | | 0.03 |

| | 0.00 |

| | 0.00 |

| | 0.03 |

| | 0.10 |

|

Watchlist/Special Mention Risk Rating Loans | | $ | 40,642 | | $ | 53,282 | | $ | 38,346 | | $ | 46,581 | | $ | 31,991 | |

Substandard Risk Rating Loans | | | 58,074 | | | 44,986 | | | 31,587 | | | 21,791 | | | 31,637 | |

| (1) | Nonperforming assets are defined as nonaccrual loans plus 90 days past due and still accruing plus foreclosed assets. |

Page 16 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Non-GAAP Financial Measures

(unaudited)

| | For the Three Months Ended | | For the Nine Months Ended | | |||||||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, |

| September 30, | | September 30, | | September 30, | | |||||||

(dollars in thousands) | | 2025 |

| 2025 |

| 2025 |

| 2024 |

| 2024 | | 2025 |

| 2024 |

| |||||||

Pre-Provision Net Revenue | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Income | | $ | 2,061 | | $ | 3,627 | | $ | 2,079 | | $ | 2,533 | | $ | 1,522 | | $ | 7,767 | | $ | 4,835 | |

Less: (Gain) Loss on Sales of Securities | | | (59) | | | (474) | | | (1) | | | — | | | 28 | | | (534) | | | (385) | |

Less: FHLB Advance Prepayment Income | | | — | | | (301) | | | — | | | — | | | — | | | (301) | | | — | |

Total Operating Noninterest Income | | | 2,002 | | | 2,852 | | | 2,078 | | | 2,533 | | | 1,550 | | | 6,932 | | | 4,450 | |

Plus: Net Interest Income | | | 34,091 | | | 32,452 | | | 30,208 | | | 26,967 | | | 25,599 | | | 96,751 | | | 75,226 | |

Net Operating Revenue | | $ | 36,093 | | $ | 35,304 | | $ | 32,286 | | $ | 29,500 | | $ | 27,149 | | $ | 103,683 | | $ | 79,676 | |

| | | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense | | $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

Total Operating Noninterest Expense | | $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

| | | | | | | | | | | | | | | | | | | | | | |

Pre-Provision Net Revenue | | $ | 16,137 | | $ | 16,363 | | $ | 14,150 | | $ | 12,688 | | $ | 11,389 | | $ | 46,650 | | $ | 33,188 | |

| | | | | | | | | | | | | | | | | | | | | | |

Plus: | | | | | | | | | | | | | | | | | | | | | | |

Non-Operating Revenue Adjustments | | | 59 | | | 775 | | | 1 | | | — | | | (28) | | | 835 | | | 385 | |

Less: | | | | | | | | | | | | | | | | | | | | | | |

Provision for Credit Losses | | | 1,100 | | | 2,000 | | | 1,500 | | | 2,175 | | | — | | | 4,600 | | | 1,350 | |

Provision for Income Taxes | | | 3,495 | | | 3,618 | | | 3,018 | | | 2,309 | | | 2,686 | | | 10,131 | | | 7,602 | |

Net Income | | $ | 11,601 | | $ | 11,520 | | $ | 9,633 | | $ | 8,204 | | $ | 8,675 | | $ | 32,754 | | $ | 24,621 | |

| | | | | | | | | | | | | | | | | | | | | | |

Average Assets | | $ | 5,372,443 | | $ | 5,162,182 | | $ | 5,071,446 | | $ | 4,788,036 | | $ | 4,703,804 | | $ | 5,205,747 | | $ | 4,647,925 | |

Pre-Provision Net Revenue Return on Average Assets | | | 1.19 | % | | 1.27 | % | | 1.13 | % | | 1.05 | % | | 0.96 | % | | 1.20 | % | | 0.95 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Adjusted Pre-Provision Net Revenue | | | | | | | | | | | | | | | | | | | | | | |

Net Operating Revenue | | $ | 36,093 | | $ | 35,304 | | $ | 32,286 | | $ | 29,500 | | $ | 27,149 | | $ | 103,683 | | $ | 79,676 | |

| | | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense | | $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

Less: Merger-related Expenses | | | (530) | | | (540) | | | (565) | | | (488) | | | (224) | | | (1,635) | | | (224) | |

Adjusted Total Operating Noninterest Expense | | $ | 19,426 | | $ | 18,401 | | $ | 17,571 | | $ | 16,324 | | $ | 15,536 | | $ | 55,398 | | $ | 46,264 | |

| | | | | | | | | | | | | | | | | | | | | | |

Adjusted Pre-Provision Net Revenue | | $ | 16,667 | | $ | 16,903 | | $ | 14,715 | | $ | 13,176 | | $ | 11,613 | | $ | 48,285 | | $ | 33,412 | |

Adjusted Pre-Provision Net Revenue Return on Average Assets | | | 1.23 | % | | 1.31 | % | | 1.18 | % | | 1.09 | % | | 0.98 | % | | 1.24 | % | | 0.96 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Core Net Interest Margin | | | | | | | | | | | | | | | | | | | | | | |

Net Interest Income (Tax-equivalent Basis) |

| $ | 34,614 | | $ | 32,770 | | $ | 30,464 | | $ | 27,254 | | $ | 25,905 | | $ | 97,848 | | $ | 76,185 | |

Less: | | | | | | | | | | | | | | | | | | | | | | |

Loan Fees | | | (966) | | | (1,019) | | | (719) | | | (747) | | | (968) | | | (2,704) | | | (2,342) | |

Purchase Accounting Accretion: | | | | | | | | | | | | | | | | | | | | | | |

Loan Accretion | | | (380) | | | (425) | | | (342) | | | — | | | — | | | (1,147) | | | — | |

Bond Accretion | | | (89) | | | (152) | | | (578) | | | (91) | | | — | | | (819) | | | — | |

Bank-Owned Certificates of Deposit Accretion | | | (6) | | | (4) | | | (7) | | | — | | | — | | | (17) | | | — | |

Deposit Certificates of Deposit Accretion | | | (13) | | | (37) | | | (38) | | | — | | | — | | | (88) | | | — | |

Total Purchase Accounting Accretion | | | (488) | | | (618) | | | (965) | | | (91) | | | — | | | (2,071) | | | — | |

Core Net Interest Income (Tax-equivalent Basis) | | $ | 33,160 | | $ | 31,133 | | $ | 28,780 | | $ | 26,416 | | $ | 24,937 | | $ | 93,073 | | $ | 73,843 | |

| | | | | | | | | | | | | | | | | | | | | | |

Average Interest Earning Assets | | $ | 5,223,139 | | $ | 5,019,058 | | $ | 4,928,283 | | $ | 4,682,841 | | $ | 4,595,521 | | $ | 5,060,374 | | $ | 4,544,932 | |

Core Net Interest Margin | | | 2.52 | % | | 2.49 | % | | 2.37 | % | | 2.24 | % |

| 2.16 | % |

| 2.46 | % |

| 2.17 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Core Loan Yield | | | | | | | | | | | | | | | | | | | | | | |

Loan Interest Income (Tax-equivalent Basis) | | $ | 60,317 | | $ | 58,122 | | $ | 53,979 | | $ | 52,078 | | $ | 52,118 | | $ | 172,418 | | $ | 153,567 | |

Less: | | | | | | | | | | | | | | | | | | | | | | |

Loan Fees | | | (966) | | | (1,019) | | | (719) | | | (747) | | | (968) | | | (2,704) | | | (2,342) | |

Loan Accretion | | | (380) | | | (425) | | | (342) | | | — | | | — | | | (1,147) | | | — | |

Core Loan Interest Income | | $ | 58,971 | | $ | 56,678 | | $ | 52,918 | | $ | 51,331 | | $ | 51,150 | | $ | 168,567 | | $ | 151,225 | |

| | | | | | | | | | | | | | | | | | | | | | |

Average Loans | | $ | 4,132,987 | | $ | 4,064,540 | | $ | 3,899,258 | | $ | 3,730,532 | | $ | 3,721,654 | | $ | 4,034,656 | | $ | 3,740,855 | |

Core Loan Yield | | | 5.66 | % |

| 5.59 | % |

| 5.50 | % | | 5.47 | % |

| 5.47 | % |

| 5.59 | % |

| 5.40 | % |

Page 17 of 19

Bridgewater Bancshares, Inc. and Subsidiaries

Non-GAAP Financial Measures

(unaudited)

| | For the Three Months Ended | | For the Nine Months Ended | | |||||||||||||||||

| | September 30, | | June 30, | | March 31, | | December 31, | | September 30, | | September 30, | | September 30, | | |||||||

(dollars in thousands) | | 2025 |

| 2025 |

| 2025 |

| 2024 | | 2024 | | 2025 | | 2024 | | |||||||

Efficiency Ratio | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense |

| $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

Less: Amortization of Intangible Assets | | | (230) | | | (230) | | | (230) | | | (52) | | | (9) | | | (690) | | | (26) | |

Adjusted Noninterest Expense | | $ | 19,726 | | $ | 18,711 | | $ | 17,906 | | $ | 16,760 | | $ | 15,751 | | $ | 56,343 | | $ | 46,462 | |

| | | | | | | | | | | | | | | | | | | | | | |

Net Interest Income | | $ | 34,091 | | $ | 32,452 | | $ | 30,208 | | $ | 26,967 | | $ | 25,599 | | $ | 96,751 | | $ | 75,226 | |

Noninterest Income | | | 2,061 | | | 3,627 | | | 2,079 | | | 2,533 | | | 1,522 | | | 7,767 | | | 4,835 | |

Less: (Gain) Loss on Sales of Securities | | | (59) | | | (474) | | | (1) | | | — | | | 28 | | | (534) | | | (385) | |

Adjusted Operating Revenue | | $ | 36,093 | | $ | 35,605 | | $ | 32,286 | | $ | 29,500 | | $ | 27,149 | | $ | 103,984 | | $ | 79,676 | |

Efficiency Ratio | |

| 54.7 | % |

| 52.6 | % |

| 55.5 | % |

| 56.8 | % |

| 58.0 | % |

| 54.2 | % |

| 58.3 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Adjusted Efficiency Ratio | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense | | $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

Less: Amortization of Intangible Assets | | | (230) | | | (230) | | | (230) | | | (52) | | | (9) | | | (690) | | | (26) | |

Less: Merger-related Expenses | | | (530) | | | (540) | | | (565) | | | (488) | | | (224) | | | (1,635) | | | (224) | |

Adjusted Noninterest Expense | | $ | 19,196 | | $ | 18,171 | | $ | 17,341 | | $ | 16,272 | | $ | 15,527 | | $ | 54,708 | | $ | 46,238 | |

| | | | | | | | | | | | | | | | | | | | | | |

Net Interest Income | | $ | 34,091 | | $ | 32,452 | | $ | 30,208 | | $ | 26,967 | | $ | 25,599 | | $ | 96,751 | | $ | 75,226 | |

Noninterest Income | | | 2,061 | | | 3,627 | | | 2,079 | | | 2,533 | | | 1,522 | | | 7,767 | | | 4,835 | |

Less: (Gain) Loss on Sales of Securities | | | (59) | | | (474) | | | (1) | | | — | | | 28 | | | (534) | | | (385) | |

Less: FHLB Advance Prepayment Income | | | — | | | (301) | | | — | | | — | | | — | | | (301) | | | — | |

Adjusted Operating Revenue | | $ | 36,093 | | $ | 35,304 | | $ | 32,286 | | $ | 29,500 | | $ | 27,149 | | $ | 103,683 | | $ | 79,676 | |

Adjusted Efficiency Ratio | |

| 53.2 | % |

| 51.5 | % |

| 53.7 | % |

| 55.2 | % |

| 57.2 | % |

| 52.8 | % |

| 58.0 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Adjusted Noninterest Expense to Average Assets (Annualized) | | | | | | | | | | | | | | | | | | | | | | |

Noninterest Expense | | $ | 19,956 | | $ | 18,941 | | $ | 18,136 | | $ | 16,812 | | $ | 15,760 | | $ | 57,033 | | $ | 46,488 | |

Less: Merger-related Expenses | | | (530) | | | (540) | | | (565) | | | (488) | | | (224) | | | (1,635) | | | (224) | |

Adjusted Noninterest Expense | | $ | 19,426 | | $ | 18,401 | | $ | 17,571 | | $ | 16,324 | | $ | 15,536 | | $ | 55,398 | | $ | 46,264 | |

| | | | | | | | | | | | | | | | | | | | | | |

Average Assets | | $ | 5,372,443 | | $ | 5,162,182 | | $ | 5,071,446 | | $ | 4,788,036 | | $ | 4,703,804 | | $ | 5,205,747 | | $ | 4,647,925 | |

Adjusted Noninterest Expense to Average Assets (Annualized) | | | 1.43 | % | | 1.43 | % | | 1.41 | % | | 1.36 | % | | 1.31 | % | | 1.42 | % | | 1.33 | % |

| | | | | | | | | | | | | | | | | | | | | | |

Tangible Common Equity and Tangible Common Equity/Tangible Assets | | | | | | | | | | | | | | | | | | | | | | |

Total Shareholders' Equity | | $ | 497,463 | | $ | 476,282 | | $ | 468,975 | | $ | 457,935 | | $ | 452,200 | | | | | | | |

Less: Preferred Stock | | | (66,514) | | | (66,514) | | | (66,514) | | | (66,514) | | | (66,514) | | | | | | | |

Total Common Shareholders' Equity | | | 430,949 | | | 409,768 | | | 402,461 | | | 391,421 | | | 385,686 | | | | | | | |

Less: Intangible Assets | | | (19,142) | | | (19,372) | | | (19,602) | | | (19,832) | | | (2,789) | | | | | | | |

Tangible Common Equity | | $ | 411,807 | | $ | 390,396 | | $ | 382,859 | | $ | 371,589 | | $ | 382,897 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Total Assets | | $ | 5,359,994 | | $ | 5,296,673 | | $ | 5,136,808 | | $ | 5,066,242 | | $ | 4,691,517 | | | | | | | |

Less: Intangible Assets | | | (19,142) | | | (19,372) | | | (19,602) | | | (19,832) | | | (2,789) | | | | | | | |

Tangible Assets | | $ | 5,340,852 | | $ | 5,277,301 | | $ | 5,117,206 | | $ | 5,046,410 | | $ | 4,688,728 | | | | | | | |

Tangible Common Equity/Tangible Assets | |

| 7.71 | % |

| 7.40 | % |

| 7.48 | % |

| 7.36 | % |

| 8.17 | % | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Tangible Book Value Per Share | | | | | | | | | | | | | | | | | | | | | | |

Book Value Per Common Share | | $ | 15.62 | | $ | 14.92 | | $ | 14.60 | | $ | 14.21 | | $ | 14.06 | | | | | | | |

Less: Effects of Intangible Assets | | | (0.69) | | | (0.71) | | | (0.71) | | | (0.72) | | | (0.10) | | | | | | | |

Tangible Book Value Per Common Share | | $ | 14.93 | | $ | 14.21 | | $ | 13.89 | | $ | 13.49 | | $ | 13.96 | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Return on Average Tangible Common Equity | | | | | | | | | | | | | | | | | | | | | | |

Net Income Available to Common Shareholders | | $ | 10,588 | | $ | 10,506 | | $ | 8,620 | | $ | 7,190 | | $ | 7,662 | | $ | 29,714 | | $ | 21,581 | |

| | | | | | | | | | | | | | | | | | | | | | |