Exhibit 99.1

For Immediate Release Citigroup Inc. (NYSE: C) JANUARY 14, 2026 | |

|

FOURTH QUARTER AND FULL YEAR 2025 RESULTS AND KEY METRICS

| | |

Citi Chair and CEO Jane Fraser said, “With record revenues and positive operating leverage for each of our five businesses, 2025 was a year of significant progress as we demonstrated that the investments we are making are driving strong top-line growth. Growth in Services was fueled by deeper client relationships and new client mandates; Markets maintained its top 3 position and improved its returns; Banking played a key role in many of the year’s major transactions; Wealth delivered strong results and launched several significant partnerships; and USPB doubled its returns through a focus on customer engagement and new, innovative products. “We returned over $17 billion of capital to our shareholders - the most since the pandemic - including $13 billion through share buybacks. We ended the year with a CET1 Ratio of 13.2%, which is 160 basis points above our regulatory requirement. We have ample capital to support our growth while continuing to return excess capital to our shareholders. “We enter 2026 with visible momentum across the firm and are committed to reaching our target of 10-11% RoTCE for the year and positioning Citi for improved returns above that level in the years ahead,” Ms. Fraser concluded. | ||

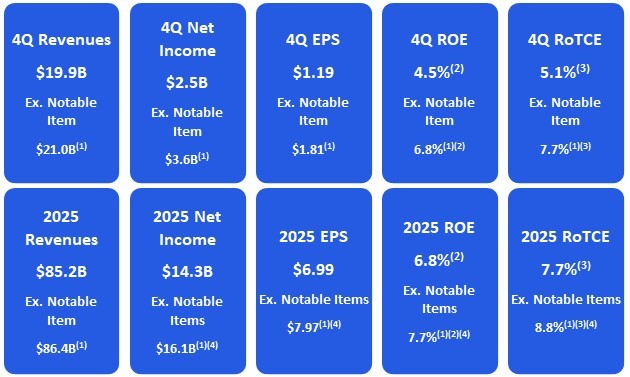

RETURNED ~$17.6 BILLION IN THE FORM OF COMMON SHARE REPURCHASES AND COMMON DIVIDENDS IN 2025 (~$5.6 BILLION IN THE QUARTER) 2025 PAYOUT RATIO OF 133%(5) COMMON EQUITY TIER 1 CAPITAL RATIO OF 13.2%(6) BOOK VALUE PER SHARE OF $110.01 TANGIBLE BOOK VALUE PER SHARE OF $97.06(7) New York, January 14, 2026 – Citigroup Inc. today reported net income for the fourth quarter 2025 of $2.5 billion, or $1.19 per diluted share, on revenues of $19.9 billion. This compares to net income of $2.9 billion, or $1.34 per diluted share, on revenues of $19.5 billion for the fourth quarter 2024. As previously disclosed(1), fourth quarter 2025 results included a notable item consisting of a loss on sale of $1.2 billion ($1.1 billion after-tax), due to the held for sale accounting treatment related to Citi's plan to sell AO Citibank in Russia, recorded in Other revenues. Revenues increased 2% from the prior-year period, on a reported basis(8), driven by growth in Banking, Services, U.S. Personal Banking (USPB) and Wealth, primarily offset by a decline in All Other. Excluding the Russia-related notable item(1), revenues were up 8%. Net income was $2.5 billion, compared to $2.9 billion in the prior-year period, driven by higher expenses, including income tax expense due to the limited tax benefit of the Russia-related notable item(1), offset by higher revenues and a lower provision for credit losses. Excluding the Russia-related notable item(1), net income was $3.6 billion. | |

1

Earnings per share of $1.19 decreased from $1.34 per diluted share in the prior-year period, reflecting lower net income, partially offset by a lower share count due to share repurchases. Excluding the Russia-related notable item(1), earnings per share was $1.81.

For the full year 2025, Citigroup reported net income of $14.3 billion on revenue of $85.2 billion, compared to net income of $12.7 billion on revenue of $80.7 billion for the full year 2024.

Excluding the Russia-related notable item(1), revenue was $86.4 billion in full year 2025. Excluding a notable item related to the Banamex goodwill impairment in the third quarter(4) and the Russia-related notable item(1), net income was $16.1 billion in full year 2025.

Percentage comparisons throughout this press release are calculated for the fourth quarter 2025 versus the fourth quarter 2024, unless otherwise specified.

Fourth Quarter Financial Results

Citigroup | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | % Δ | |||||

| | | | | | | | | | | | | | |||||||||

Total revenues, net of interest expense | | | 19,871 | | | 22,090 | | | 19,465 | | (10)% | | 2% | | | | 85,225 | | | 80,722 | | 6% |

| | | | | | | | | | | | | | |||||||||

Total operating expenses | | | 13,840 | | | 14,290 | | | 13,070 | | (3)% | | 6% | | | | 55,132 | | | 53,567 | | 3% |

| | | | | | | | | | | | | | |||||||||

Net credit losses | | | 2,190 | | | 2,214 | | | 2,242 | | (1)% | | (2)% | | | | 9,097 | | | 9,000 | | 1% |

Net ACL build / (release)(a) | | | 23 | | | 145 | | | 203 | | (84)% | | (89)% | | | | 602 | | | 607 | | (1)% |

Other provisions(b) | | | 7 | | | 91 | | | 148 | | (92)% | | (95)% | | | | 566 | | | 502 | | 13% |

Total provision for credit losses | | | 2,220 | | | 2,450 | | | 2,593 | | (9)% | | (14)% | | | | 10,265 | | | 10,109 | | 2% |

| | | | | | | | | | | | | | |||||||||

Income (loss) from continuing operations before taxes | | | 3,811 | | | 5,350 | | | 3,802 | | (29)% | | - | | | | 19,828 | | | 17,046 | | 16% |

Provision for income taxes | | | 1,288 | | | 1,559 | | | 912 | | (17)% | | 41% | | | | 5,373 | | | 4,211 | | 28% |

Income (loss) from continuing operations | | | 2,523 | | | 3,791 | | | 2,890 | | (33)% | | (13)% | | | | 14,455 | | | 12,835 | | 13% |

Income (loss) from discontinued operations, net of taxes | | | (1) | | | (1) | | | - | | - | | NM | | | | (3) | | | (2) | | (50)% |

Net income attributable to non-controlling interest | | | 51 | | | 38 | | | 34 | | 34% | | 50% | | | | 146 | | | 151 | | (3)% |

Citigroup’s net income (loss) | | $ | 2,471 | | $ | 3,752 | | $ | 2,856 | | (34)% | | (13)% | | | $ | 14,306 | | $ | 12,682 | | 13% |

| | | | | | | | | | | | | | |||||||||

| | | | | | | | | | | | | | |||||||||

EOP loans ($B) | | | 752 | | | 734 | | | 694 | | 2% | | 8% | | | | | | | |||

Average loans ($B) | | | 737 | | | 725 | | | 688 | | 2% | | 7% | | | | | | | |||

EOP assets ($B) | | | 2,657 | | | 2,642 | | | 2,353 | | 1% | | 13% | | | | | | | |||

EOP deposits ($B) | | | 1,404 | | | 1,384 | | | 1,284 | | 1% | | 9% | | | | | | | |||

Average deposits ($B) | | | 1,422 | | | 1,382 | | | 1,320 | | 3% | | 8% | | | | | | | |||

| | | | | | | | | | | | | | |||||||||

| | | | | | | | | | | | | | |||||||||

Book value per share | | $ | 110.01 | | $ | 108.41 | | $ | 101.62 | | 1% | | 8% | | | $ | 110.01 | | $ | 101.62 | | 8% |

Tangible book value per share(c) | | $ | 97.06 | | $ | 95.72 | | $ | 89.34 | | 1% | | 9% | | | $ | 97.06 | | $ | 89.34 | | 9% |

Common Equity Tier 1 (CET1) Capital ratio(d) | | | 13.2% | | | 13.3% | | | 13.6% | | | | | | 13.2% | | | 13.6% | | |||

Supplementary Leverage ratio (SLR)(d) | | | 5.5% | | | 5.5% | | | 5.8% | | | | | | 5.5% | | | 5.8% | | |||

Return on average common equity (ROE)(e) | | | 4.5% | | | 7.1% | | | 5.4% | | | | | | 6.8% | | | 6.1% | | |||

Return on average tangible common equity (RoTCE)(f) | | | 5.1% | | | 8.0% | | | 6.1% | | (290) bps | | (100) bps | | | | 7.7% | | | 7.0% | | 70 bps |

Efficiency Ratio (total operating expenses/total revenues, net) | | | 69.6% | | | 64.7% | | | 67.1% | | 490 bps | | 250 bps | | | | 64.7% | | | 66.4% | | (170) bps |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Includes credit reserve build / (release) for loans and provision / (release) for credit losses on unfunded lending commitments.

(b) Includes provisions on Other Assets, policyholder benefits and claims and HTM debt securities.

(c) Tangible book value per share is a non-GAAP financial measure. For additional information, refer to footnote 7.

(d) Ratios as of December 31, 2025 are preliminary. For additional information, please refer to footnote 6.

(e) Ratios as of December 31, 2025 are preliminary. For additional information, please refer to footnote 2.

(f) Ratios as of December 31, 2025 are preliminary. RoTCE is a non-GAAP financial measure. For additional information, please refer to foonote 3.

2

Citigroup

Citigroup revenues of $19.9 billion in the fourth quarter 2025 increased 2%, on a reported basis, driven by growth in Banking, Services, USPB and Wealth, primarily offset by a decline in All Other. Excluding the Russia-related notable item(1), revenues were up 8%. Reported net interest income increased 14%, driven by Markets, Services, USPB, Legacy Franchises in All Other, Wealth and Banking, partially offset by a decline in Corporate/Other in All Other. Reported non-interest revenue decreased 27%, driven by Legacy Franchises, Markets, USPB and Wealth, partially offset by increases in Banking and Services.

Citigroup operating expenses of $13.8 billion were up 6%, driven by higher compensation and benefits expenses, increases in non-income tax charges, legal expenses and technology and communication expenses, partially offset by productivity savings and lower deposit insurance expenses.

Citigroup provision for credit losses was $2.2 billion, driven by $2.2 billion of net credit losses and a net allowance for credit losses (ACL) build of $30 million, driven by higher net lending activity, primarily offset by changes in credit quality. Net credit losses were down 2% from the prior-year period, driven by a decrease in USPB, largely offset by an increase in Legacy Franchises. The provision in the prior-year period was $2.6 billion, driven by $2.2 billion of net credit losses and a net ACL build of $351 million, driven by higher net lending activity, partially offset by changes in the macroeconomic outlook.

Citigroup net income was $2.5 billion in the fourth quarter 2025, compared to net income of $2.9 billion in the prior-year period, driven by higher expenses, including income tax expense due to the limited tax benefit of the Russia-related notable item(1), offset by higher revenues and a lower provision for credit losses. Excluding the Russia-related notable item(1), net income was $3.6 billion. Citigroup’s effective tax rate was approximately 34% in the current quarter, driven by the limited tax benefit of the Russia-related notable item, compared to 24% in the fourth quarter 2024.

Citigroup’s total allowance for credit losses was approximately $21.4 billion at quarter end, compared to $22.2 billion at the end of the prior-year period. The decrease was driven by the reclassification of AO Citibank related ACL to Other Assets, resulting from the held for sale accounting for Citi’s planned sale of AO Citibank, largely offset by ACL builds and changes in foreign exchange during the year. Total ACL on loans was approximately $19.2 billion at quarter end, compared to $18.6 billion at the end of the prior-year period, with a reserve-to-funded loans ratio of 2.6%, down from 2.7% in the prior-year period. Total non-accrual loans increased $0.9 billion, or 35% from the prior-year period to $3.6 billion. Corporate non-accrual loans increased $0.6 billion, or 45% from the prior-year period to $2.0 billion, driven by idiosyncratic downgrades in Banking and Services. Consumer non-accrual loans increased $0.3 billion, or 24% from the prior-year period to $1.6 billion, primarily driven by Legacy Franchises, primarily due to higher volumes in Mexico Consumer and Wealth, driven by residential mortgage loans impacted by the California wildfires.

Citigroup’s end-of-period loans were $752 billion at quarter end, up 8% versus the prior-year period, driven by higher loans in Markets, Services and USPB, partially offset by lower loans in Banking. Citigroup’s average loans were $737 billion in the fourth quarter 2025, up 7% versus the prior-year period, driven by higher average loans in Markets, USPB and Services.

Citigroup’s end-of-period deposits were approximately $1.4 trillion at quarter end, up 9% versus the prior-year period, driven by increases in Services. Citigroup’s average deposits were approximately $1.4 trillion in the fourth quarter 2025, up 8% versus the prior-year period, driven by higher average deposits in Services.

Citigroup’s book value per share of $110.01 at quarter end increased 8% versus the prior-year period, and tangible book value per share of $97.06 at quarter end increased 9% versus the prior-year period. The increases were driven by net income and beneficial net movements in accumulated other comprehensive income (AOCI), partially offset by the payment of common and preferred dividends and reductions in additional paid-in capital (APIC). In addition, common share repurchases were accretive to book value per share and dilutive to tangible book value per share (due to the higher average repurchase price for 2025 over the tangible book value per share as of December 31, 2024). At quarter end, Citigroup’s preliminary CET1 Capital ratio(6) was 13.2% versus 13.3% at the end of the prior quarter, primarily driven by common share repurchases, the payment of common and preferred dividends and the temporary impact of the held for sale accounting treatment related to Citi’s plan to sell AO Citibank in Russia(1), primarily offset by net income and the temporary impact from the sale of a 25% equity stake in Grupo Financiero Banamex, S.A. de C.V.(4) Citigroup’s Supplementary Leverage ratio(6) for the fourth quarter 2025 was 5.5%, unchanged from the prior quarter. During the quarter, Citigroup returned approximately $5.6 billion to common shareholders in the form of share repurchases and dividends.

3

Services | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | % Δ | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Net interest income | | | 3,303 | | | 3,121 | | | 2,840 | | 6% | | 16% | | | | 12,238 | | | 10,923 | | 12% |

Non-interest revenue | | | 879 | | | 761 | | | 1,095 | | 16% | | (20)% | | | | 3,140 | | | 3,578 | | (12)% |

Treasury and Trade Solutions | | | 4,182 | | | 3,882 | | | 3,935 | | 8% | | 6% | | | | 15,378 | | | 14,501 | | 6% |

Net interest income | | | 747 | | | 702 | | | 606 | | 6% | | 23% | | | | 2,763 | | | 2,500 | | 11% |

Non-interest revenue | | | 1,013 | | | 779 | | | 624 | | 30% | | 62% | | | | 3,115 | | | 2,617 | | 19% |

Securities Services | | | 1,760 | | | 1,481 | | | 1,230 | | 19% | | 43% | | | | 5,878 | | | 5,117 | | 15% |

Total Services revenues(a) | | | 5,942 | | | 5,363 | | | 5,165 | | 11% | | 15% | | | | 21,256 | | | 19,618 | | 8% |

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 2,843 | | | 2,707 | | | 2,601 | | 5% | | 9% | | | | 10,813 | | | 10,568 | | 2% |

| | | | | | | | | | | | | | | | | | | | | | |

Net credit losses | | | 19 | | | 11 | | | 28 | | 73% | | (32)% | | | | 56 | | | 48 | | 17% |

Net ACL build / (release)(b) | | | (15) | | | (12) | | | (75) | | (25)% | | 80% | | | | 38 | | | (113) | | NM |

Other provisions(c) | | | (15) | | | 62 | | | 159 | | NM | | NM | | | | 360 | | | 341 | | 6% |

Total provision for credit losses | | | (11) | | | 61 | | | 112 | | NM | | NM | | | | 454 | | | 276 | | 64% |

| | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 2,246 | | $ | 1,802 | | $ | 1,871 | | 25% | | 20% | | | $ | 7,075 | | $ | 6,483 | | 9% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Services Key Statistics and Metrics ($B) | | | | | | | | | | | | | | | | | | | | | | |

Allocated Average TCE(d) | | | 25 | | | 25 | | | 25 | | - | | (1)% | | | | 25 | | | 25 | | (1)% |

RoTCE(d) | | | 36.1% | | | 28.9% | | | 29.9% | | 720 bps | | 620 bps | | | | 28.6% | | | 26.0% | | 260 bps |

Fee revenue ($MM) | | | 1,630 | | | 1,626 | | | 1,441 | | - | | 13% | | | | 6,385 | | | 6,012 | | 6% |

Average loans | | | 96 | | | 94 | | | 87 | | 2% | | 10% | | | | 93 | | | 85 | | 9% |

Average deposits | | | 935 | | | 893 | | | 839 | | 5% | | 11% | | | | 878 | | | 819 | | 7% |

Cross border transaction value | | | 115 | | | 105 | | | 101 | | 10% | | 14% | | | | 416 | | | 380 | | 10% |

US dollar clearing volume (#MM)(e) | | | 45 | | | 45 | | | 44 | | 1% | | 3% | | | | 177 | | | 168 | | 5% |

Commercial card spend volume | | | 18 | | | 18 | | | 17 | | (4)% | | 2% | | | | 71 | | | 70 | | 1% |

Assets under custody and/or administration (AUC/AUA) ($T)(f) | | | 31 | | | 30 | | | 25 | | 6% | | 24% | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Services revenues reflect the impact of a revenue sharing agreement with Banking – Corporate Lending, for Services products sold to Corporate Lending clients. This generally results in a reduction in Services reported revenue.

(b) Includes credit reserve build / (release) for loans and provision / (release) for credit losses on unfunded lending commitments.

(c) Includes provisions on Other Assets and for HTM debt securities.

(d) TCE and RoTCE are non-GAAP financial measures. For additional information, refer to Footnote 3.

(e) U.S. dollar clearing volume is defined as the number of USD clearing payment instructions processed by Citi on behalf of U.S. and foreign-domiciled entities (primarily financial institutions). Amounts in the table are stated in millions of payment instructions processed.

(f) 4Q25 is preliminary.

Services

Services revenues of $5.9 billion were up 15%. Excluding the Russia-related notable item(1), revenues increased 8%, driven by growth in Treasury and Trade Solutions and Securities Services. Net interest income increased 18%, primarily driven by an increase in average deposit balances and deposit spreads. Non-interest revenue increased 10%. Excluding the Russia-related notable item(1), non-interest revenue decreased 11%, driven by higher lending revenue share, partially offset by fee revenue growth of 13%.

Treasury and Trade Solutions revenues of $4.2 billion were up 6%, driven by a 16% increase in net interest income, partially offset by a 20% decrease in non-interest revenue. The increase in net interest income was primarily driven by higher average deposit balances and deposit spreads. The decrease in non-interest revenue was driven by the impact of the higher lending revenue share, partially offset by growth in fees and underlying fee drivers, including an increase in cross-border transaction value of 14%, an increase in U.S. dollar clearing volume of 3% and an increase in commercial card spend volume of 2%.

Securities Services revenues of $1.8 billion were up 43%, driven by a 62% increase in non-interest revenue and a 23% increase in net interest income. The increase in non-interest revenue was driven by the Russia-related notable item(1) and higher fees, which benefited from a 24% increase in assets under custody and administration, partially offset by higher lending revenue share. The increase in net interest income was primarily driven by higher average deposit balances and deposit spreads.

Services operating expenses of $2.8 billion increased 9%, primarily driven by higher technology expenses, compensation and benefits expenses and volume-related expenses.

Services provision for credit losses was a benefit of $11 million, driven by $19 million of net credit losses and a net ACL release of $30 million. The provision in the prior-year period was $112 million, driven by a net ACL build of $84 million, driven by transfer risk, and $28 million of net credit losses.

Services net income of $2.2 billion increased 20%, driven by higher revenues, including the impact of the Russia-related notable item(1), and a lower provision for credit losses, partially offset by higher expenses.

4

Markets | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | %Δ | |||||

| | | | | | | | | | | | | | | | | | |||||

Rates and currencies | | | 2,413 | | | 2,823 | | | 2,421 | | (15)% | | - | | | | 11,418 | | | 10,152 | | 12% |

Spread products / other fixed income | | | 1,045 | | | 1,200 | | | 1,057 | | (13)% | | (1)% | | | | 4,808 | | | 4,598 | | 5% |

Fixed Income markets | | | 3,458 | | | 4,023 | | | 3,478 | | (14)% | | (1)% | | | | 16,226 | | | 14,750 | | 10% |

Equity markets | | | 1,084 | | | 1,540 | | | 1,098 | | (30)% | | (1)% | | | | 5,744 | | | 5,086 | | 13% |

Total Markets revenues(a) | | | 4,542 | | | 5,563 | | | 4,576 | | (18)% | | (1)% | | | | 21,970 | | | 19,836 | | 11% |

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 3,609 | | | 3,491 | | | 3,174 | | 3% | | 14% | | | | 14,077 | | | 13,202 | | 7% |

| | | | | | | | | | | | | | | | | | | | | | |

Net credit losses | | | (12) | | | 68 | | | - | | NM | | NM | | | | 206 | | | 168 | | 23% |

Net ACL build / (release)(b) | | | (80) | | | (31) | | | 136 | | (158)% | | NM | | | | (9) | | | 230 | | NM |

Other provisions(c) | | | (12) | | | (5) | | | (2) | | (140)% | | (500)% | | | | 40 | | | 65 | | (38)% |

Total provision for credit losses | | | (104) | | | 32 | | | 134 | | NM | | NM | | | | 237 | | | 463 | | (49)% |

| | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 783 | | $ | 1,562 | | $ | 1,009 | | (50)% | | (22)% | | | $ | 5,855 | | $ | 4,930 | | 19% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Markets Key Statistics and Metrics ($B) | | | | | | | | | | | | | | | | | | | | | | |

Allocated Average TCE(d) | | | 50 | | | 50 | | | 54 | | - | | (7)% | | | | 50 | | | 54 | | (7)% |

RoTCE(d) | | | 6.2% | | | 12.3% | | | 7.4% | | (610) bps | | (120) bps | | | | 11.6% | | | 9.1% | | 250 bps |

Average trading account assets | | | 557 | | | 556 | | | 449 | | - | | 24% | | | | 535 | | | 436 | | 23% |

Average loans | | | 152 | | | 147 | | | 122 | | 3% | | 25% | | | | 141 | | | 120 | | 18% |

Average VaR ($ in MM)(e) | | | 109 | | | 117 | | | 118 | | (7)% | | (8)% | | | | 115 | | | 123 | | (6)% |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Markets revenues reflect the impact of a revenue sharing agreement with Banking – Corporate Lending, for Markets products sold to Corporate Lending clients. This generally results in a reduction in Markets reported revenue.

(b) Includes credit reserve build / (release) for loans and provision / (release) for credit losses on unfunded lending commitments.

(c) Includes provisions on Other Assets and HTM debt securities.

(d) TCE and RoTCE are non-GAAP financial measures. For additional information, refer to Footnote 3.

(e) VaR estimates, at a 99% confidence level, the potential decline in the value of a position or a portfolio under normal market conditions assuming a one-day holding period. VaR statistics, which are based on historical data, can be materially different across firms due to differences in portfolio composition, VaR methodologies and model parameters.

Markets

Markets revenues of $4.5 billion decreased 1%, driven by lower Fixed Income markets and Equity markets revenues compared to a strong quarter in the prior-year period.

Fixed Income markets revenues of $3.5 billion decreased 1%, largely driven by a decline in spread products and other fixed income. Rates and currencies revenues were unchanged, as growth in foreign exchange revenue and the impact of continued optimization of the balance sheet were offset by higher lending revenue share and lower revenues in rates. Spread products and other fixed income revenues declined 1%, driven by lower commodities revenues, offset by the impact of continued optimization of the balance sheet and higher financing activity in spread products.

Equity markets revenues of $1.1 billion decreased 1%, driven by lower cash equities revenues, compared to a strong quarter in the prior-year period, primarily offset by continued momentum in prime services, with record prime balances(9) (up by more than 50%), and higher derivatives revenues.

Markets operating expenses of $3.6 billion increased 14%, primarily driven by higher legal expenses, compensation and benefits, technology expenses and volume-related expenses.

Markets provision for credit losses was a benefit of $104 million, driven by a net ACL release of $92 million, resulting from a refinement of loss assumptions for certain portfolios in spread products, and $12 million of net credit recoveries. The provision in the prior-year period was $134 million, driven by a net ACL build of $134 million, driven by changes in credit quality, partially offset by changes in the macroeconomic outlook.

Markets net income of $783 million decreased 22%, driven by higher expenses and lower revenues, largely offset by a lower provision for credit losses.

5

Banking | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | %Δ | |||||

| | | | | | | | | | | | | | | | | | |||||

Investment Banking | | | 1,272 | | | 1,146 | | | 925 | | 11% | | 38% | | | | 4,434 | | | 3,637 | | 22% |

Corporate Lending(a) | | | 964 | | | 1,030 | | | 322 | | (6)% | | 199% | | | | 3,899 | | | 2,744 | | 42% |

Total Banking revenues(a)(b) | | | 2,236 | | | 2,176 | | | 1,247 | | 3% | | 79% | | | | 8,333 | | | 6,381 | | 31% |

Gain / (loss) on loan hedges(a) | | | (26) | | | (44) | | | (6) | | 41% | | (333)% | | | | (118) | | | (180) | | 34% |

Total Banking revenues including gain/(loss) on loan hedges(a) | | | 2,210 | | | 2,132 | | | 1,241 | | 4% | | 78% | | | | 8,215 | | | 6,201 | | 32% |

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 1,152 | | | 1,139 | | | 1,051 | | 1% | | 10% | | | | 4,462 | | | 4,477 | | - |

Net credit losses | | | 25 | | | 9 | | | 7 | | 178% | | 257% | | | | 84 | | | 149 | | (44)% |

Net ACL build / (release)(c) | | | 150 | | | 136 | | | (204) | | 10% | | NM | | | | 610 | | | (328) | | NM |

Other provisions(d) | | | 1 | | | 12 | | | (43) | | (92)% | | NM | | | | 26 | | | (45) | | NM |

Total provision for credit losses | | | 176 | | | 157 | | | (240) | | 12% | | NM | | | | 720 | | | (224) | | NM |

| | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 685 | | $ | 638 | | $ | 356 | | 7% | | 92% | | | $ | 2,329 | | $ | 1,524 | | 53% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Banking Key Statistics and Metrics | | | | | | | | | | | | | | | | | | | | | | |

Allocated Average TCE(e) ($B) | | | 21 | | | 21 | | | 22 | | - | | (6)% | | | | 21 | | | 22 | | (6)% |

RoTCE(e) | | | 13.2% | | | 12.3% | | | 6.5% | | 90 bps | | 670 bps | | | | 11.3% | | | 7.0% | | 430 bps |

Average loans ($B) | | | 79 | | | 81 | | | 84 | | (2)% | | (6)% | | | | 82 | | | 88 | | (7)% |

| | | | | | | | | | | | | | | | | | | | | | |

Advisory | | | 649 | | | 427 | | | 353 | | 52% | | 84% | | | | 1,908 | | | 1,245 | | 53% |

Equity underwriting | | | 180 | | | 174 | | | 214 | | 3% | | (16)% | | | | 699 | | | 688 | | 2% |

Debt underwriting | | | 458 | | | 568 | | | 384 | | (19)% | | 19% | | | | 2,011 | | | 1,924 | | 5% |

Investment Banking fees | | | 1,287 | | | 1,169 | | | 951 | | 10% | | 35% | | | | 4,618 | | | 3,857 | | 20% |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Excludes gain / (loss) on credit derivatives as well as the mark-to-market on loans at fair value. For additional information, see Footnote 10.

(b) Banking revenues reflect the impact of a revenue sharing agreement with Banking – Corporate Lending, for Investment Banking, Markets and Services products sold to Corporate Lending clients. This generally results in an increase in Banking reported revenue.

(c) Includes credit reserve build / (release) for loans and provision for credit losses on unfunded lending commitments.

(d) Includes provisions on Other Assets and HTM debt securities.

(e) TCE and RoTCE are non-GAAP financial measures. For additional information, refer to Footnote 3.

Banking

Banking revenues of $2.2 billion increased 78%, driven by growth in Corporate Lending, excluding mark-to-market gain/(loss) on loan hedges(10), and Investment Banking.

Investment Banking revenues of $1.3 billion increased 38%, driven by an increase in Investment Banking fees of 35%, reflecting growth in Advisory and Debt Capital Markets (DCM), partially offset by a decline in Equity Capital Markets (ECM). Advisory fees increased 84%, driven by momentum across several sectors and continued share gains. ECM fees were down 16%, driven by lower follow-on volumes, partially offset by higher initial public offerings. DCM fees were up 19%, driven by investment grade and leveraged finance debt, partially offset by lower participation in loans.

Corporate Lending revenues of $964 million, excluding mark-to-market on loan hedges(10), increased 199%, driven by an increase in lending revenue share.

Banking operating expenses of $1.2 billion increased 10%, driven by higher compensation and benefits, including investments in the business.

Banking provision for credit losses was $176 million, driven by a net ACL build of $151 million, driven by changes in portfolio composition, including credit quality and exposure growth, and $25 million of net credit losses. The provision in the prior-year period was a benefit of $240 million, driven by a net ACL release of $247 million, primarily driven by changes in the macroeconomic outlook, changes in credit quality and transfer risk, and $7 million of net credit losses.

Banking net income of $685 million increased 92%, driven by higher revenues, largely offset by a higher provision for credit losses and higher expenses.

6

Wealth | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | % r | |||||

| | | | | | | | | | | | | | | | | | |||||

Private Bank | | 625 | | 656 | | 590 | | (5)% | | 6% | | | | 2,676 | | | 2,386 | | 12% | |||

Wealth at Work | | | 227 | | | 214 | | | 256 | | 6% | | (11)% | | | | 930 | | | 876 | | 6% |

Citigold | | | 1,281 | | | 1,294 | | | 1,148 | | (1)% | | 12% | | | | 4,953 | | | 4,221 | | 17% |

Total revenues, net of interest expense | | | 2,133 | | | 2,164 | | | 1,994 | | (1)% | | 7% | | | 8,559 | | 7,483 | | 14% | ||

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | 1,650 | | 1,654 | | 1,561 | | - | | 6% | | | 6,501 | | 6,326 | | 3% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Net credit losses | | | 36 | | | 56 | | | 30 | | (36)% | | 20% | | | | 170 | | | 121 | | 40% |

Net ACL build / (release)(a) | | | 3 | | | (26) | | | (11) | | NM | | NM | | | | (29) | | | (245) | | 88% |

Other provisions(b) | | | (1) | | | - | | | 1 | | NM | | NM | | | | (1) | | | (2) | | 50% |

Total provision for credit losses | | 38 | | 30 | | 20 | | 27% | | 90% | | | 140 | | (126) | | NM | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 338 | | $ | 374 | | $ | 334 | | (10)% | | 1% | | | $ | 1,490 | | $ | 1,002 | | 49% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Wealth Key Statistics and Metrics ($B) | | | | | | | | | | | | | | | | | | | | | | |

Allocated Average TCE(c) | | | 12 | | | 12 | | | 13 | | - | | (7)% | | | | 12 | | | 13 | | (7)% |

RoTCE(c) | | | 10.9% | | | 12.1% | | | 10.1% | | (120) bps | | 80 bps | | | | 12.1% | | | 7.6% | | 450 bps |

| | | | | | | | | | | | | | | | | | | | | | |

Loans | | | 150 | | | 151 | | | 148 | | (1)% | | 2% | | | | | | | | | |

Deposits | | | 324 | | | 318 | | | 313 | | 2% | | 4% | | | | | | | | | |

Client investment assets(d) | | | 670 | | | 660 | | | 587 | | 2% | | 14% | | | | | | | | | |

EOP client balances | | | 1,144 | | | 1,129 | | | 1,048 | | 1% | | 9% | | | | | | | | | |

Net New Investment Assets (NNIA)(e) | | | 7.2 | | | 18.6 | | | 15.6 | | (61)% | | (54)% | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Includes credit reserve build / (release) for loans and provision / (release) for credit losses on unfunded lending commitments.

(b) Includes provisions on Other Assets and policyholder benefits and claims.

(c) TCE and RoTCE are non-GAAP financial measures. For additional information, refer to Footnote 3.

(d) Includes assets under management, and trust and custody assets. 4Q25 Client investment assets are preliminary.

(e) 4Q25 Net new investment assets are preliminary. Represents investment asset inflows, including dividends, interest and distributions, less investment asset outflows.

Wealth

Wealth revenues of $2.1 billion increased 7%, driven by growth in Citigold and the Private Bank, partially offset by lower revenues in Wealth at Work. Net interest income of $1.4 billion increased 12%, driven by higher deposit spreads and average deposit balances, partially offset by lower mortgage spreads. Non-interest revenue of $736 million decreased 1%, driven by the loss of fee revenue from the sale of the trust business in the third quarter 2025, largely offset by other net fee growth, with client investment assets up 14%.

Private Bank revenues of $625 million increased 6%, driven by higher deposit spreads, largely offset by lower mortgage spreads.

Wealth at Work revenues of $227 million decreased 11%, driven by lower mortgage spreads, largely offset by higher deposit spreads and higher investment fee revenues.

Citigold revenues of $1.3 billion increased 12%, primarily driven by higher deposit spreads and higher investment fee revenues.

Wealth operating expenses of $1.7 billion increased 6%, primarily driven by investments in technology and higher volume and other revenue-related expenses.

Wealth provision for credit losses was $38 million, driven by $36 million of net credit losses and a net ACL build of $2 million. The provision in the prior-year period was $20 million, driven by $30 million of net credit losses and a net ACL release of $10 million.

Wealth net income of $338 million increased 1%, driven by higher revenues, primarily offset by higher expenses and a higher provision for credit losses.

7

USPB ($ in millions, except as otherwise noted) | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | %r | |||||

| | | | | | | | | | | | | | | | | | |||||

Branded Cards | | 2,952 | | 2,970 | | 2,806 | | (1)% | | 5% | | | | 11,636 | | | 10,735 | | 8% | |||

Retail Services | | | 1,612 | | | 1,686 | | | 1,741 | | (4)% | | (7)% | | | | 6,622 | | | 7,070 | | (6)% |

Retail Banking | | | 729 | | | 675 | | | 603 | | 8% | | 21% | | | | 2,713 | | | 2,250 | | 21% |

Total revenues, net of interest expense | | | 5,293 | | | 5,331 | | | 5,150 | | (1)% | | 3% | | | 20,971 | | 20,055 | | 5% | ||

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | 2,521 | | 2,365 | | 2,465 | | 7% | | 2% | | | 9,709 | | 9,646 | | 1% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Net credit losses | | | 1,783 | | | 1,776 | | | 1,920 | | - | | (7)% | | | | 7,431 | | | 7,579 | | (2)% |

Net ACL build / (release)(a) | | | (113) | | | 64 | | | 246 | | NM | | NM | | | | (225) | | | 1,006 | | NM |

Other provisions(b) | | | 3 | | | 2 | | | 4 | | 50% | | (25)% | | | | 5 | | | 13 | | (62)% |

Total provision for credit losses | | 1,673 | | 1,842 | | 2,170 | | (9)% | | (23)% | | | 7,211 | | 8,598 | | (16)% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 845 | | $ | 858 | | $ | 392 | | (2)% | | 116% | | | $ | 3,097 | | $ | 1,382 | | 124% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

USPB Key Statistics and Metrics ($B) | | | | | | | | | | | | | | | | | | | | | | |

Allocated average TCE(c) | | | 23 | | | 23 | | | 25 | | - | | (7)% | | | | 23 | | | 25 | | (7)% |

RoTCE(c) | | | 14.3% | | | 14.5% | | | 6.2% | | (20) bps | | 810 bps | | | | 13.2% | | | 5.5% | | 770 bps |

Average loans | | | 226 | | | 220 | | | 216 | | 3% | | 5% | | | | 220 | | | 209 | | 5% |

Average deposits | | | 88 | | | 90 | | | 86 | | (2)% | | 2% | | | | 89 | | | 91 | | (2)% |

US credit card average loans | | | 169 | | | 167 | | | 165 | | 1% | | 2% | | | | | | | | | |

US credit card spend volume | | | 166 | | | 157 | | | 161 | | 6% | | 4% | | | | | | | | | |

New credit cards account acquisitions (in thousands) | | | 3,687 | | | 3,211 | | | 3,520 | | 15% | | 5% | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Includes credit reserve build / (release) for loans.

(b) Includes provisions on policyholder benefits and claims and Other Assets.

(c) TCE and RoTCE are non-GAAP financial measures. For additional information, refer to Footnote 3.

U.S. Personal Banking (USPB)

USPB revenues of $5.3 billion increased 3%, driven by growth in Branded Cards and Retail Banking, partially offset by a decline in Retail Services. Net interest income increased 5%, driven by higher loan spreads and higher interest-earning balances in Branded Cards, as well as higher deposit spreads and average deposit balances in Retail Banking, partially offset by lower interest-earning balances and lower loan spreads in Retail Services. Non-interest revenue decreased 42%, driven by higher rewards costs, partially offset by higher gross interchange fees in Branded Cards.

Branded Cards revenues of $3.0 billion increased 5%, driven by higher loan spreads, higher interest-earning balances, which were up 4%, and higher gross interchange fees, largely offset by higher rewards costs.

Retail Services revenues of $1.6 billion decreased 7%, primarily driven by lower interest-earning balances and lower loan spreads.

Retail Banking revenues of $729 million increased 21%, driven by the impact of higher deposit spreads and average deposit balances.

USPB operating expenses of $2.5 billion increased 2%, driven by higher transactional and marketing expenses, partially offset by a reduction in other expenses.

USPB provision for credit losses was $1.7 billion, driven by $1.8 billion of net credit losses and a net ACL release of $110 million, driven by improvements in portfolio quality, including seasonal mix changes, primarily offset by higher volume and changes in the macroeconomic outlook. Net credit losses were down 7% from the prior-year period, driven by improved credit performance in Retail Services. The provision in the prior-year period was $2.2 billion, driven by $1.9 billion of net credit losses and a net ACL build of $250 million, driven by higher volume, partially offset by changes in credit quality.

USPB net income of $845 million increased 116%, driven by a lower provision for credit losses and higher revenues, partially offset by higher expenses.

8

All Other (Managed Basis)(a)(b) | | 4Q’25 | | 3Q’25 | | 4Q’24 | | QoQ% | | YoY% | | | 2025 | | 2024 | | %Δ | |||||

| | | | | | | | | | | | | | | | | | |||||

Legacy Franchises (managed basis) | | 329 | | 1,871 | | 1,563 | | (82)% | | (79)% | | | 5,512 | | 6,835 | | (19)% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Corporate / Other | | | (577) | | | (336) | | | (228) | | (72)% | | (153)% | | | (1,082) | | 668 | | NM | ||

| | | | | | | | | | | | | | | | | | | | | | |

Total revenues | | | (248) | | | 1,535 | | | 1,335 | | NM | | NM | | | 4,430 | | 7,503 | | (41)% | ||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses | | | 2,025 | | | 2,168 | | | 2,162 | | (7)% | | (6)% | | | 8,693 | | 9,030 | | (4)% | ||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Net credit losses | | | 341 | | | 297 | | | 257 | | 15% | | 33% | | | | 1,150 | | | 928 | | 24% |

| | | | | | | | | | | | | | | | | | | | | | |

Net ACL build / (release)(c) | | 77 | | 10 | | 111 | | NM | | (31)% | | | 223 | | 57 | | 291% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Other provisions(d) | | 31 | | 24 | | 29 | | 29% | | 7% | | | 140 | | 130 | | 8% | |||||

| | | | | | | | | | | | | | | | | | | | | | |

Total provision for credit losses | | | 449 | | | 331 | | | 397 | | 36% | | 13% | | | | 1,513 | | | 1,115 | | 36% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Net (loss) | | $ | (2,316) | | $ | (705) | | $ | (1,070) | | (229)% | | (116)% | | | $ | (4,458) | | $ | (2,432) | | (83)% |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

All Other Key Statistics and Metrics ($B) | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Allocated Average TCE(e) | | | 39 | | | 41 | | | 30 | | (5)% | | 32% | | | | 39 | | | 28 | | 42% |

| | | | | | | | | | | | | | | | | | | | | | |

(a) Includes Legacy Franchises and certain unallocated costs of global staff functions (including finance, risk, human resources, legal and compliance-related costs), other corporate expenses, and unallocated global operations and technology expenses and income taxes, as well as Corporate Treasury investment activities and discontinued operations.

(b) Reflects results on a managed basis, which excludes divestiture-related impacts related to Citi's divestitures of its Asia consumer banking businesses and the planned divestiture of Mexico Consumer/ SBMM within Legacy Franchises. For additional information, please refer to Footnote 11.

(c) Includes credit reserve build / (release) for loans and provision / (release) for credit losses on unfunded lending commitments.

(d) Includes provisions on Other Assets, policyholder benefits and claims and HTM debt securities.

(e) TCE is a non-GAAP financial measure. For additional information, refer to Footnote 3.

All Other (Managed Basis)(11)

All Other (managed basis) revenues were $(248) million, compared to $1.3 billion in the prior-year period, driven by declines in Legacy Franchises and Corporate/Other.

Legacy Franchises (managed basis)(11) revenues of $329 million decreased 79%, driven by the Russia-related notable item(1) and lower revenues related to closed exits and wind-downs, partially offset by growth in Mexico, including the impact of foreign exchange translation.

Corporate/Other revenues of $(577) million decreased from $(228) million in the prior-year period, driven by lower net interest income due to a lower benefit from cash and securities reinvestment, driven by actions taken over the last few quarters to reduce Citi’s asset sensitivity in a declining interest rate environment.

All Other (managed basis) expenses of $2.0 billion decreased 6%, driven by lower deposit insurance expenses in Corporate/Other, lower compensation and benefits and lower expenses related to closed exits and wind-downs in Legacy Franchises, largely offset by higher non-income tax charges, higher investment in technology, and the impact of foreign exchange translation.

All Other (managed basis) provision for credit losses was $449 million, driven by $341 million of net credit losses and a net ACL build of $108 million, primarily driven by higher volume, largely in Mexico. Net credit losses were up 33% from the prior-year period, driven by higher consumer volume and portfolio seasoning in Mexico Consumer. The provision in the prior-year period was $397 million, driven by $257 million of net credit losses and a net ACL build of $140 million, driven by higher consumer volume, changes in the macroeconomic outlook and changes in credit quality in Mexico Consumer.

All Other (managed basis) net loss was $(2.3) billion, compared to $(1.1) billion in the prior-year period, driven by lower revenues and a higher provision for credit losses, partially offset by lower expenses.

9

Citigroup will host a conference call today at 11:00 AM (ET). A live webcast of the presentation, as well as financial results and presentation materials, will be available at https://www.citigroup.com/global/investors. The live webcast of the presentation can also be accessed at https://www.veracast.com/webcasts/citigroup/webinars/CITI4Q25.cfm

Additional financial, statistical and business-related information, as well as business and segment trends, is included in a Quarterly Financial Data Supplement. Both this earnings release and Citigroup’s Fourth Quarter 2025 Quarterly Financial Data Supplement are available on Citigroup’s website at www.citigroup.com.

Citi is a preeminent banking partner for institutions with cross-border needs, a global leader in wealth management and a valued personal bank in its home market of the United States. Citi does business in more than 180 countries and jurisdictions, providing corporations, governments, investors, institutions and individuals with a broad range of financial products and services.

Additional information may be found at www.citigroup.com | X: @Citi | YouTube: www.youtube.com/citi | Blog: http://blog.citigroup.com | Facebook: www.facebook.com/citi | LinkedIn: www.linkedin.com/company/citi

Certain statements in this release are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on management's current expectations and are subject to uncertainty and changes in circumstances. These statements are not guarantees of future results or occurrences. Actual results and capital and other financial condition may differ materially from those included in these statements due to a variety of factors. These factors include, among others: (i) macroeconomic, geopolitical and other challenges and uncertainties, including impacts related to slowing economic growth; elevated unemployment rates and inflation; changes in interest rates; any deterioration in business and consumer confidence and spending; changes in U.S. laws or policies, including those related to credit card interest rates, trade and tariffs; any U.S. government shutdown; and geopolitical tensions and hostilities; (ii) the execution and efficacy of Citi’s priorities regarding its simplification, transformation and enhanced business performance, including those related to revenues, net interest income, expenses, capital-related, credit and return expectations, as well as divestitures such as Grupo Financiero Banamex, S.A. de C.V.; (iii) changes in regulatory capital requirements, interpretations or rules; and (iv) the precautionary statements included in this release. These factors also consist of those contained in Citigroup's filings with the U.S. Securities and Exchange Commission, including without limitation the “Risk Factors” section of Citigroup’s 2024 Form 10-K. Any forward-looking statements made by or on behalf of Citigroup speak only as to the date they are made, and Citi does not undertake to update forward-looking statements to reflect the impact of circumstances or events that arise after the date the forward-looking statements were made.

Contacts: | |

| |

Investors: Jennifer Landis (212) 559-2718 | |

| |

Press: Danielle Romero-Apsilos (212) 816-2264 | |

10

(1) The impact of the Russia-related notable item includes:

($ in MM) | | Citigroup | | Services | | Markets | | Banking | | Legacy Franchises(a) | | Corporate/Other | ||||

| | | | | | | | | | | | | ||||

Total Non-interest Revenue Impact | | (1,173) | | 356 | | 19 | | 40 | | (1,556) | | (32) | ||||

Income Tax Benefit / (Expense) | | | 50 | | | - | | | - | | - | | 50 | | - | |

Total Net Income Impact | | | (1,123) | | | 356 | | | 19 | | 40 | | (1,506) | | (32) | |

(a) Includes approximately $1.6 billion related to the currency translation adjustment (CTA) losses that will remain in Accumulated Other Comprehensive Income (AOCI) until the closing of a sale.

For additional information on the Russia-related notable item in the fourth quarter 2025, see Citi’s Current Report on Form 8-K filed on December 29, 2025 with the U.S. Securities and Exchange Commission. Results of operations excluding the impact of the notable item are non-GAAP financial measures. Citi believes the presentation of its results of operations and financial condition excluding the notable item provides a meaningful depiction of the underlying fundamentals of its broader results for investors, industry analysts and others. For a reconciliation to reported results, please refer to the financial supplement included as Exhibit 99.1 to Citigroup's Current Report on Form 8-K filed with the SEC on January 14, 2026 (the 4Q25 Financial Supplement).

Services revenues and non-interest revenue, excluding the Russia-related notable item, are non-GAAP financial measures. For a reconciliation to reported results, please refer to the 4Q25 Financial Supplement.

(2) Ratios as of December 31, 2025 are preliminary. Citigroup’s return on average common stockholders’ equity (ROE) is calculated using net income less preferred stock dividends divided by average common stockholders’ equity.

(3) Ratios as of December 31, 2025 are preliminary. Citigroup’s allocated average tangible common equity (TCE) and return on average tangible common equity (RoTCE) are non-GAAP financial measures. RoTCE represents annualized net income available to common shareholders as a percentage of average TCE. For the components of these calculations, refer to the 4Q25 Financial Supplement. For a reconciliation of common equity to TCE, refer to the 4Q25 Financial Supplement.

As used herein, 2026 RoTCE is a forward-looking non-GAAP financial measure. From time to time, management may discuss forward-looking non-GAAP financial measures, such as forward-looking estimates or targets for revenue, expenses and RoTCE. Citi is unable to provide a reconciliation of forward-looking non-GAAP financial measures to their most directly comparable GAAP financial measures because Citi is unable to provide, without unreasonable effort, a meaningful or accurate calculation or estimation of amounts that would be necessary for the reconciliation due to the complexity and inherent difficulty in forecasting and quantifying future amounts or when they may occur. Such unavailable information could be significant for future results.

(4) As previously disclosed, third quarter 2025 results included a notable item consisting of a goodwill impairment of $726 million ($714 million after-tax), recorded in Other expenses, related to Citi’s agreement to sell a 25% equity stake in Grupo Financiero Banamex, S.A. de C.V. For additional information on the notable item in the third quarter 2025, see Citi’s Current Report on Form 8-K filed on September 24, 2025 with the U.S. Securities and Exchange Commission. On December 15, 2025, Citi completed the sale of the 25% equity stake in Grupo Financiero Banamex, S.A. de C.V. Results of operations excluding the impact of the notable item are non-GAAP financial measures. For a reconciliation to reported results, please refer to the 4Q25 Financial Supplement.

(5) Citigroup’s payout ratio is the sum of common dividends and common share repurchases divided by net income available to common shareholders.

(6) Ratios as of December 31, 2025 are preliminary. For the composition of Citigroup’s CET1 Capital and ratio and Citigroup’s Supplementary Leverage Ratio, refer to the 4Q25 Financial Supplement.

(7) Citigroup’s tangible book value per share is a non-GAAP financial measure. For a reconciliation of common equity to tangible common equity and resulting calculation of tangible book value per share, refer to the 4Q25 Financial Supplement.

(8) Included in Citi's reported revenues was an immaterial decrease in divestiture-related revenues of $(1) million in the fourth quarter 2025 compared to $4 million in the fourth quarter 2024. Accordingly, Citi is not adjusting for these amounts.

(9) Prime balances are defined as clients’ billable balances where Citigroup provides cash or synthetic prime brokerage services.

(10) Credit derivatives are used to economically hedge a portion of the Corporate Lending portfolio that includes both accrual loans and loans at fair value. Gain/(loss) on loan hedges includes the mark-to-market on the credit derivatives and the mark-to-market on the loans in the portfolio that are at fair value. The fixed premium costs of these hedges are netted against the Corporate Lending revenues to reflect the cost of credit protection. Citigroup’s results of operations excluding the impact of gain/(loss) on loan hedges are non-GAAP financial measures. For a reconciliation to reported results, refer to the 4Q25 Financial Supplement.

(11) All Other (managed basis) reflects results on a managed basis, which excludes divestiture-related impacts, for all periods, related to Citigroup’s divestitures of its Asia consumer banking businesses and the planned divestiture of Mexico Consumer/SBMM businesses within Legacy Franchises. Certain of the results of operations of All Other (managed basis) and Legacy Franchises (managed basis) that exclude divestiture-related impacts are non-GAAP financial measures. For additional information and a reconciliation of these results, refer to the 4Q25 Financial Supplement.

11