2.10 Upset Condition.

2.10.1 The "Upset Condition" shall have occurred if both of the following conditions exist as of the last

day of the Pricing Period: (a) the Average Purchaser Closing Price is less than $22.3953 (the "Floor Purchaser Price"); and (b) the number determined by dividing the Average Purchaser

Closing Price by $27.9941 is less than the number obtained by subtracting (i) 20% from (ii) the quotient obtained by dividing the Final Index Price by the Initial Index Price. The "Initial

Index Price" means the $116.18 closing price of the KBW Nasdaq Regional Banking Index (KRX) on July 23, 2024. The "Average Purchaser Closing Price" means the average volume weighted trading price per share of Purchaser Common Stock on which shares of Purchaser Common Stock were actually traded in transactions reported on the

Nasdaq stock exchange during the ten (10) trading days immediately preceding the date that is seven (7) Business Days prior to the Closing Date (the "Pricing

Period"). The "Final Index Price" means the closing price of the KBW Nasdaq Regional Banking Index (KRX) on the last day of the Pricing Period.

2.10.2 If the Upset Condition exists as of the last day of the Pricing Period, Company shall have the right, exercisable at any time prior to 5:00 p.m., Eastern Time on

the second Business Day after the last day of the Pricing Period (the "Exercise Period") to (a) proceed with the Merger on the basis of the Per Share Merger Consideration as calculated

pursuant to Section 2.1, subject to applicable adjustment as provided in Section 2.9, by delivering to Purchaser within the Exercise Period written notice of its

decision to do so or by failing to deliver any notice to Purchaser; or (b) request Purchaser to adjust the Per Share Merger Consideration, by delivering to Purchaser within the Exercise Period written notice

to such effect (an "Increase Notice"), to a Per Share Merger Consideration computed by multiplying the Per Share Merger Consideration by a fraction that has as its numerator the Floor

Purchaser Price and that has as its denominator the Average Purchaser Closing Price (the "Adjusted Per Share Merger Consideration").

2.10.3 If the Upset Condition occurs and Purchaser receives an Increase Notice, Purchaser shall either accept or decline the Adjusted Per Share Merger Consideration by

delivering written notice of its decision to Company at or before 5:00 p.m., Eastern Time on the second Business Day after receipt of the Increase Notice (the "Acceptance Period"). If

Purchaser accepts the Adjusted Per Share Merger Consideration within the Acceptance Period, this Plan of Merger shall remain in effect in accordance with its terms except that the Per Share Merger Consideration shall be equal to the Adjusted Per

Share Merger Consideration. If Purchaser declines the Adjusted Per Share Merger Consideration or fails to deliver written notice of its decision to accept or decline the Adjusted Per Share Merger Consideration within the Acceptance Period, the

Merger shall be abandoned and this Plan of Merger shall thereupon terminate without further action by Company or Purchaser effective as of 5:00 p.m., Eastern Time on the Business Day following the expiration of the Acceptance Period; provided, that if Purchaser so declines the Adjusted Per Share Merger Consideration or fails to deliver written notice of its decision to accept or decline the Adjusted Per Share Merger Consideration within the

Acceptance Period, Company may, by written notice delivered to Purchaser at or before 5:00 p.m., Eastern Time on the Business Day following the expiration of the Acceptance Period, elect to proceed with the Merger on the basis of the Per Share

Merger Consideration calculated in accordance with Section 2.1, subject to applicable adjustment as provided in Section 2.9, and, upon such election, no abandonment

of the Merger or termination of the Plan of Merger shall be deemed to have occurred, this Plan of Merger shall remain in effect in accordance with its terms, and the Closing shall thereafter occur, in accordance with the terms of this Plan of

Merger.

2.11 Dissenting Shares. Notwithstanding any other provision of this Plan of Merger to the contrary, shares of Company Common Stock that are

outstanding immediately prior to the Effective Time and which are held by shareholders who shall have not voted in favor of the Merger or consented thereto in writing and who properly shall have demanded payment of the fair value for such shares in

accordance with the MBCA (collectively, the "Dissenters’ Shares") shall not be converted into or

represent the right to receive the Per Share Merger Consideration. Such shareholders instead shall be entitled to receive payment of the fair value of such shares held by them in accordance with the provisions of the MBCA, except that all

Dissenters’ Shares held by shareholders who shall have failed to perfect or who effectively shall have withdrawn or otherwise lost their rights as dissenting shareholders under the MBCA shall thereupon be deemed to have been converted into and to

have become exchangeable, as of the Effective Time, for the right to receive, without any interest thereon, the Per Share Merger Consideration upon surrender in the manner provided in Section 2.2 of the Certificates or Book-Entry Shares

that, immediately prior to the Effective Time, evidenced such shares. The Company shall give Purchaser: (a) prompt notice of any written demands for payment of fair value of any shares of Company Common Stock, attempted withdrawals of such demands

and any other instruments served pursuant to the MBCA and received by the Company relating to shareholders’ dissenters’ rights; and (b) the opportunity to participate in all negotiations and proceedings with respect to demands under the MBCA

consistent with the obligations of the Company thereunder. The Company shall not, except with the prior written consent of Purchaser, (i) make any payment with respect to such demand, (ii) offer to settle or settle any demand for payment of fair

value or (iii) waive any failure to timely deliver a written demand for payment of fair value or timely take any other action to perfect payment of fair value rights in accordance with the MBCA.

ARTICLE III

COMPANY'S REPRESENTATIONS AND WARRANTIES

On or prior to the date hereof, Company has delivered to Purchaser a schedule (the "Company Disclosure Letter") setting forth, among

other things, items the disclosure of which is necessary or appropriate either in response to an express disclosure requirement contained in a provision hereof or as an exception to one or more of the representations or warranties contained in this

Article III or to one or more of its covenants contained in Article V. Accordingly, Company hereby represents and warrants to Purchaser as follows, except as set

forth on the Company Disclosure Letter:

3.1 Authorization, No Conflicts, Etc.

3.1.1 Authorization of Plan of Merger. Company has the requisite corporate power and authority to execute and deliver this

Plan of Merger, to perform its obligations hereunder and, subject to the affirmative vote of the holders of at least a majority of the outstanding shares of Company Common Stock entitled to vote to approve the Plan of Merger (the "Company Shareholder Approval"), to consummate the transactions contemplated by this Plan of Merger. This Plan of Merger has been duly adopted, and the consummation of the Merger and the other

transactions contemplated by this Plan of Merger have been duly authorized, at a meeting duly called and held, by the Company Board of Directors. The Company Board of Directors at such meeting has unanimously (a) determined that the terms of this

Plan of Merger are advisable, fair to and in the best interests of Company and the Company Shareholders, and (b) adopted this Plan of Merger, approved and authorized the transactions contemplated by this Plan of Merger and, subject to Section 5.3.5, resolved to recommend approval by the Company Shareholders of this Plan of Merger and the transactions contemplated by it (such recommendation, the "Company Board Recommendation") and (c) directed this Plan of Merger and the Merger be submitted to the Company Shareholders for approval. Except for the Company Shareholder Approval, no other corporate proceedings on the part of

Company are necessary to authorize this Plan of Merger or to consummate the Merger. This Plan of Merger has been duly executed and delivered by, and (assuming due authorization, execution and delivery by Purchaser) constitutes valid and binding

obligations of, Company and is enforceable against Company in accordance with its terms, except to the extent that (i) such enforcement may be subject to applicable bankruptcy, insolvency, reorganization, moratorium or other similar Laws, now or

hereafter in effect, relating to creditors' rights generally and (ii) equitable remedies of specific performance and injunctive and other forms of equitable relief may be subject to equitable defenses and to the discretion of the court before which

any proceeding therefor may be brought.

3.1.2 No Conflict, Breach, Violation, Etc. The execution, delivery, and performance of this Plan of Merger by Company and

the consummation of the Merger, do not and will not violate, conflict with, or result in a breach of: (a) any provision of the articles of incorporation or bylaws (or similar organizational documents) of Company or any Subsidiary of Company (each a

"Company Subsidiary" and collectively, the "Company Subsidiaries"); or (b) any Law or Order applicable to Company or any Company

Subsidiary, in each case assuming the timely receipt of each of the approvals referred to in Section 3.1.4.

3.1.3 Regulatory Restrictions. Subject to Section 3.1.4, the execution, delivery,

and performance of this Plan of Merger by Company and the consummation of the Merger do not and will not violate, conflict with, result in a breach of, constitute a default under, or require any consent, approval, waiver, extension, amendment,

authorization, notice, or filing under, any cease and desist order, written agreement, memorandum of understanding, board resolutions or other regulatory agreement or commitment with or from a Governmental Entity to which Company or any Company

Subsidiary is a party or subject, or by which Company or any Company Subsidiary is bound or affected.

3.1.4 Required Approvals. No notice to, filing with, authorization of, exemption by, or consent or approval of any

Governmental Entity or any stock market, stock exchange or over-the-counter market on which Company Common Stock is listed or quoted for trading is required for the consummation of the transactions contemplated by this Plan of Merger by Company

other than in connection or compliance with (a) the filing of the Certificate of Merger in accordance with the MBCA, (b) such consents, approvals, orders, authorizations, registrations, declarations, notices and

filings as may be required under applicable federal securities, state securities or "blue sky" Laws, and (c) the consents, authorizations, approvals, or

exemptions required under the Bank Holding Company Act, the Federal Reserve Act, and the Michigan Banking Code. Company has no Knowledge of any reason why the regulatory approvals referred to in this Section

3.1.4 cannot be obtained or why the regulatory approval process would be materially impeded.

3.2 Organization and Good Standing.

Company is a corporation duly organized, validly existing, and in good standing under the Laws of the State of Michigan. Company has all requisite corporate power and authority to own, operate, and lease its

properties and assets and to carry on its business as it is now being conducted in all material respects. Company is a bank holding company duly registered as such with the Federal Reserve Board under the Bank Holding Company Act. Company is not,

and is not required to be, qualified or admitted to conduct business as a foreign corporation in any other state, except where such failure to be so qualified has not had, and would not reasonably be expected to have, individually or in the

aggregate, a Company Material Adverse Effect.

3.3 Subsidiaries.

3.3.1 Ownership. Section 3.3.1 of the Company Disclosure Letter sets forth a true and complete list of each Company

Subsidiary as of the date of this Plan of Merger. Other than the Company Subsidiaries, Company does not have "control" (as defined in Section 2(a)(2) of the Bank Holding Company Act, using 5 percent rather than 25 percent), either directly or

indirectly, of any Person engaged in an active trade or business or that holds any significant assets. Except as set forth in Section 3.3.1 of the Company Disclosure Letter, Company or a Company Subsidiary owns all of the issued and

outstanding capital stock or other equity interests of each of the Company Subsidiaries, free and clear of any claim or Lien of any kind. All of the issued and outstanding shares of capital stock or other equity

interests of each Company Subsidiary have been, as applicable, duly authorized and validly issued and are fully paid and nonassessable and except as set forth in Section 3.3.1 of the Company Disclosure Letter, not subject to or issued in

violation of any purchase option, call option, right of first refusal, preemptive right, subscription right or any similar right. Except as set forth in Section 3.3.1 of the Company Disclosure Letter, there is no legally binding

and enforceable subscription, option, warrant, right to acquire, or any other similar agreement pertaining to the capital stock or other equity interests of any Company Subsidiary.

3.3.2 Organization and Good Standing. Each of the Company Subsidiaries (a) is duly organized, validly existing and in good

standing under the Laws of its jurisdiction of organization; (b) is duly qualified to do business and in good standing in all jurisdictions (whether federal, state, or local) where its ownership or leasing of property or the conduct of its business

requires it to be so qualified; and (c) has all requisite corporate power and authority to own or lease its properties and assets and to carry on its business as now conducted, except in each of (b) and (c) as has not had, and would not reasonably

be expected to have, individually or in the aggregate, a Company Material Adverse Effect. Company has made available to Purchaser true, correct and complete copies of the organizational documents of each Company

Subsidiary (and all amendments thereto) as currently in effect, and no Company Subsidiary is in default in the performance, observation or fulfillment of its obligations under such documents, except for such defaults that, individually or in the

aggregate, have not had and would not reasonably be expected to have a Company Material Adverse Effect.

3.3.3 Deposit Insurance; Other Assessments. The deposit accounts of each Company Subsidiary that is a depository institution

are insured by the FDIC to the fullest extent permitted by Law, and all premiums and assessments to be paid in connection therewith have been paid by each such Company Subsidiary when due. No proceeding for the revocation or termination of such

deposit insurance is pending or, to the Knowledge of Company, threatened. Company and each Company Subsidiary has paid as and when due all material fees, charges, assessments, and the like as required by Law to each and every Governmental Entity

having jurisdiction over Company or each Company Subsidiary.

3.4 Capital Stock.

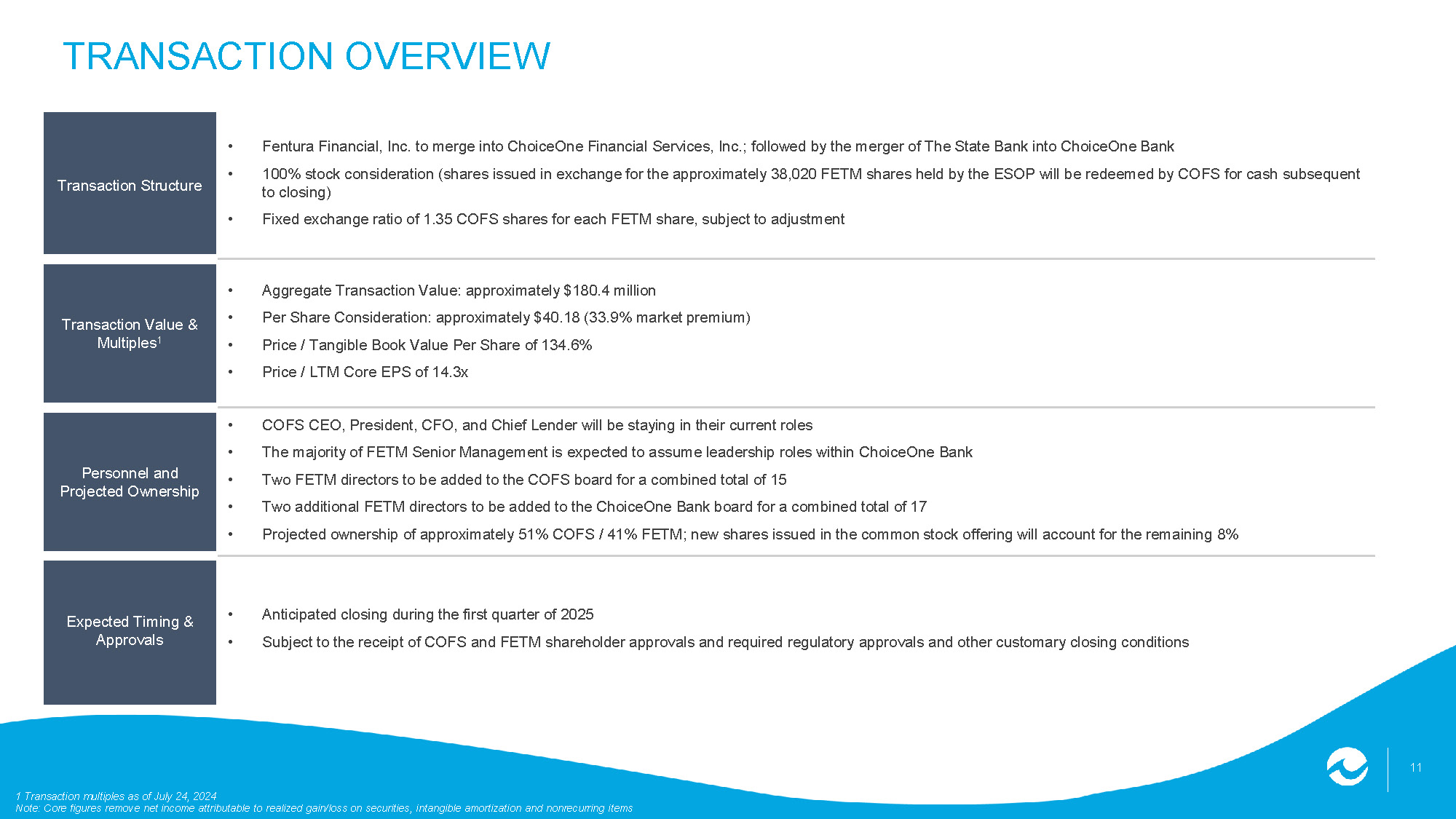

3.4.1 Classes and Shares. The authorized capital stock of Company consists of 10,200,000 shares, divided into two

classes, as follows: (a) 10,000,000 shares of common stock, no par value ("Company Common Stock"), of which 4,490,087 shares were issued and outstanding as of the close of business on

July 24, 2024 and (b) 200,000 shares of preferred stock, no par value, none of which were issued and outstanding as of the date of this Plan of Merger. As of the date of this Plan of Merger, there is no security or class of securities

outstanding that represents or is convertible into capital stock of Company. All of the issued and outstanding shares of Company Common Stock have been duly authorized and validly issued and are fully paid,

nonassessable and free of preemptive rights, with no personal liability attaching to the ownership thereof.

3.4.2 Stock Plans. Section 3.4.2 of the Company Disclosure Letter sets forth, as of the date of this Plan of Merger,

(a) the number of shares of Company Common Stock that are authorized and reserved for issuance under the Company Stock Plan, and (b) the number of outstanding unvested shares of restricted stock awarded under the Company Stock Plan, including the

name of each holder thereof, the applicable grant date thereof, the vesting conditions thereof, and the dollar amount of any accrued dividend equivalents thereon. As of the date of this Plan of Merger, there are no other compensatory awards

outstanding pursuant to which Company Common Stock is issuable, or that relate to or are determined by reference to the value of Company Common Stock. All outstanding shares of Company Common Stock, and all Company Common Stock reserved for

issuance under the Company Stock Plan, when issued in accordance with the terms of the Company Stock Plan, are or will be duly authorized, validly issued, fully paid and non-assessable and not issued in violation of any preemptive rights, purchase

option, call or right of first refusal rights. Company has made available to Purchaser complete and accurate copies of the Company Stock Plan and forms of agreements evidencing restricted stock awards. All

outstanding Company restricted stock awards have been granted pursuant to, and in compliance with, the Company Stock Plan, and have been granted pursuant to one of the forms made available pursuant to the foregoing sentence, without any material

deviation therefrom.

3.4.3 Issuance of Shares. After the date of this Plan of Merger, the number of issued and outstanding shares of capital

stock of Company is not subject to change before the Effective Time, other than the issuance of shares of restricted stock in the ordinary course of business and consistent with past practice and as otherwise set forth on Section 5.1.3 of the

Company Disclosure Letter.

3.4.4 Voting Rights. Other than the issued and outstanding shares of Company Common Stock described in Section 3.4.1, neither Company nor any Company Subsidiary has outstanding any security or issue of securities the holder or holders of which have the right to vote on the approval of the Merger or this Plan of

Merger, or that entitle the holder or holders to consent to, or withhold consent on, the Merger or this Plan of Merger. Company is not party to a shareholder rights agreement, “poison pill” or similar anti-takeover agreement or plan.

3.4.5 Appraisal Rights. Except as set forth on Section 3.4.5 of the Company Disclosure Letter, no Company

Shareholder will be entitled to appraisal rights, whether pursuant to the MBCA, Company's articles of incorporation or bylaws, or any resolution of Company's Board of Directors, as a result of the consummation of the Merger.

3.5 Financial Statements. The consolidated financial statements of Company as of and for each of the three years ended December 31, 2023, 2022 and

2021 as audited by Company's independent auditors and the unaudited consolidated financial statements of Company as of and for the six months ended June 30, 2024, including all schedules and notes relating to such statements (collectively, "Company Financial Statements") fairly present, and the unaudited consolidated financial statements of Company as of and for each quarter ending after the date of this Plan of Merger until the

Effective Time, including all schedules and notes, if any, relating to such statements, will fairly present, the consolidated financial condition and the results of operations, changes in shareholders' equity, and cash flows of Company as of the

respective dates of and for the periods referred to in such financial statements, all in accordance in all material respects with GAAP, consistently applied, subject, in the case of unaudited interim financial statements, to normal, recurring

year-end adjustments (the effect of which has not had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect) and the absence of notes (that, if presented, would not differ materially from

those included in the Company Financial Statements). No financial statements of any entity or enterprise other than the Company Subsidiaries are required by GAAP to be included in the consolidated financial statements of Company. The Company

Financial Statements have been prepared from, and are in accordance with, the books and records of the Company and the Company Subsidiaries.

3.6 Absence of Certain Changes or Events. Since December 31, 2023, (a) Company and the Company Subsidiaries have conducted their respective

businesses in the ordinary course consistent with past practice (other than discussions and negotiations related to this Plan of Merger), and (b) no event or events have occurred that have had, individually or in the aggregate, or would reasonably

be expected to have, individually or in the aggregate, a Company Material Adverse Effect.

3.7 Legal Proceedings. There is no Action pending or, to the Knowledge of Company, threatened, against Company or any of the Company Subsidiaries

or any of their respective properties, rights or assets (a) as of the date of this Plan of Merger, that challenges or seeks to enjoin, alter, prevent or materially delay the Merger or (b) except as set forth in Section 3.7 of the Company

Disclosure Letter, has had, or would reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect. There is no material unsatisfied judgment, penalty or award against Company or any of the Company

Subsidiaries. Neither Company nor any of the Company Subsidiaries, nor any of their respective properties, rights or assets, is subject to any (i) Order or any investigation by a Governmental Entity, (ii) unresolved violation, criticism or

exception by any Governmental Entity, or (iii) formal or informal inquiry by, or disagreements or disputes with, any Governmental Entity with respect to the business, operations, policies or procedures of Company or any Company Subsidiary, in each

case of clauses (i) through (iii), which has had, or would reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect. No officer or director of Company or any of the Company Subsidiaries is a defendant in

any Action commenced by any shareholder of Company or any of the Company Subsidiaries with respect to the performance of his or her duties as an officer or a director of Company or any of the Company Subsidiaries under any applicable Law, except

for any Action arising out of or relating to the Merger and the transactions contemplated by this Plan of Merger.

3.8 Regulatory Filings. Since January 1, 2021, Company and each Company Subsidiary has timely filed or furnished all material reports,

registrations, statements and filings, together with any amendments required to be made with respect thereto, that they were required to file or furnish with Governmental Entities as required by applicable Law, including filings with (a) the

Michigan Secretary of State, the Michigan Department of Insurance and Financial Services, and any other state regulatory authority, (b) the Federal Reserve Board, (c) the FDIC and (d) the FFIEC. All such filings, as of their respective filing

dates, complied in all material respects with all Laws, forms, and guidelines applicable to such filings.

3.9 No Indemnification Claims. To the Knowledge of Company, no claims are outstanding against the Company or any Company Subsidiaries for

indemnification or reimbursement of any Person.

3.10 Conduct of Business; Compliance with Law.

3.10.1 Company and each Company Subsidiary has conducted its business and used its properties in compliance in all material respects with all, and are not in material

default or violation under any, applicable Orders and Laws.

3.10.2 None of Company, any Company Subsidiary, nor, to the Knowledge of Company, any director, officer, employee or agent acting in

such capacity on behalf and at the direction of Company or any Company Subsidiary, has, directly or indirectly, (a) used any funds of Company or any Company Subsidiary for unlawful contributions, unlawful gifts, unlawful entertainment or other

expenses relating to political activity, (b) made any unlawful payment to foreign or domestic governmental officials or employees or to foreign or domestic political parties or campaigns from funds of Company or any Company Subsidiary, (c)

violated any provision that would result in the violation of the Foreign Corrupt Practices Act of 1977, as amended, or any similar law, (d) established or maintained any unlawful fund of monies or other assets of Company or any Company

Subsidiary, (e) made any fraudulent entry on the books or records of Company or any Company Subsidiary, or (f) made any unlawful bribe, unlawful rebate, unlawful payoff, unlawful influence payment, unlawful kickback or other unlawful payment to

any person, private or public, regardless of form, whether in money, property or services, to obtain favorable treatment in securing business to obtain special concessions for Company or any Company Subsidiary, to pay for favorable treatment for

business secured or to pay for special concessions already obtained for Company or any Company Subsidiary, or is currently subject to any United States sanctions administered by the Office of Foreign Assets Control of the United States Treasury

Department.

3.11 Transaction Documents. None of the information supplied or to be supplied by Company for inclusion or incorporation by reference and contained

in any Transaction Document will contain any untrue statement of material fact or omit to state a material fact required to be stated therein or necessary to make the statements therein, in light of the circumstances under which they were made, not

misleading, (a) in the case of any Transaction Document (other than the Registration Statement and the Proxy Statement) at the time it is filed or at any time it is amended or supplemented, (b) in the case of the Registration Statement, at the time

it is filed with the SEC, at any time it is amended or supplemented and at the time it becomes effective under the Securities Act, and (c) in the case of the Proxy Statement, at the date it is first mailed to the Company Shareholders and at the

time of the Company Shareholder Meeting.

3.12 Agreements With Bank Regulators. Neither Company nor any Company Subsidiary is a party to any Contract, cease and desist order, written

agreement or memorandum of understanding with, or a party to any commitment letter, board resolution or similar undertaking to, or is subject to any Order by, or, since January 1, 2021, has been ordered to pay any

civil money penalty by, or is a recipient of any extraordinary supervisory letter from, any Governmental Entity that restricts materially the conduct of Company's or a Company Subsidiary's business, or in any manner relates to the capital

adequacy, credit or reserve policies or management of Company or any Company Subsidiary (a "Regulatory Agreement"), nor has Company nor any Company Subsidiary been advised by any

Governmental Entity since January 1, 2021 that a Governmental Entity is contemplating issuing or requesting an Order or a Regulatory Agreement. Neither Company nor any Company Subsidiary is required by Section 32 of the FDI Act or FDIC Regulation

Part 359 or the Federal Reserve Board to give prior notice to a federal banking agency of the proposed addition of an individual to its board of directors or the employment of an individual as a senior executive officer or to limit golden parachute

payments or indemnification. Neither Company nor any Company Subsidiary has been designated as in "troubled condition" by any Governmental Entity.

3.13 Tax Matters.

3.13.1 Except as set forth in Section 3.13.1 of the Company Disclosure Letter, all Tax Returns required by applicable Law to have been filed by Company and

each Company Subsidiary have been filed when due (taking into account any applicable extensions), and each such Tax Return was true, correct and complete in all material respects when filed. Except as set forth in Section 3.13.1 of the

Company Disclosure Letter, Company and each Company Subsidiary has withheld and paid all material Taxes required to have been withheld and paid in connection with amounts paid to any third party. Except as set forth in Section 3.13.1

of the Company Disclosure Letter, all income and other material Taxes that are due and payable by Company and each Company Subsidiary have been paid.

3.13.2 None of the Tax Returns of Company, the Company Subsidiaries, or any entity treated as a partnership for tax purposes in which the Company or any Company

Subsidiary is an owner (“Partnership”), filed for any Tax year beginning after December 31, 2018 have been audited by the IRS or any federal, state, local or foreign taxing authority. There is no tax audit

or legal or administrative proceeding concerning Tax Returns or the assessment or collection of Taxes ongoing or pending or, to Company's Knowledge, threatened with respect to Company, any Company Subsidiary or Partnership and the Company has not

been notified in writing of any such threatened audit or proceeding. No claim concerning the calculation, assessment or collection of Taxes has been asserted with respect to Company, any Company Subsidiary or Partnership except for any claim that

has been fully resolved and the costs of such resolution fully paid and reflected in the Company Financial Statements. There are no Liens on any of the assets of Company or any of the Company Subsidiaries that arose in connection with any failure

(or alleged failure) to pay any Tax, other than Liens for Taxes not yet due and payable.

3.13.3 No claim has been made by any taxing authority in any jurisdiction where the Company does not file Tax Returns that it is, or

may be, subject to Tax by that jurisdiction.

3.13.4 The amount of the Company's Liability for unpaid Taxes for all periods ending on or before June 30, 2024 does not, in the

aggregate, exceed the amount of accruals for Taxes (excluding reserves for deferred Taxes) reflected on the Financial Statements. The amount of the Company's Liability for unpaid Taxes for all periods following June 30, 2024 shall not, in the

aggregate, exceed the amount of accruals for Taxes (excluding reserves for deferred Taxes) as adjusted for the passage of time in accordance with the past custom and practice of the Company (and which accruals shall not exceed comparable amounts

incurred in similar periods in prior years).

3.13.5 No private letter rulings, technical advice memoranda or similar agreement or rulings have been requested, entered into or

issued by any taxing authority with respect to the Company.

3.13.6 Neither Company, any Company Subsidiary nor Partnership has waived any statute of limitations in respect of Taxes or agreed to any extension of time with respect

to any Taxes, which waiver or extension is still open.

3.13.7 Neither Company nor any Company Subsidiary has been included in any "consolidated," "unitary" or "combined" Tax Return for any taxable period for which the statute

of limitations has not expired (other than a group of which Company is the common parent). Neither Company nor any Company Subsidiary is a general partner in any partnership.

3.13.8 In any year for which the applicable statute of limitations remains open, neither Company nor any Company Subsidiary has been or has purported to be a

"distributing corporation" or a "controlled corporation" in a distribution intended to qualify for tax-free treatment under Section 355 of the Code.

3.13.9 The Company is not, nor has it been, a United States real property holding corporation (as defined in Section 897(c)(2) of the

Code) during the applicable period in Section 897(c)(1)(a) of the Code.

3.13.10 The tax and audit positions taken by Company and the Company Subsidiaries in connection with Tax Returns were reasonable and asserted in good faith. No listed or

other reportable transaction within the meaning of Sections 6011, 6111 or 6112 of the Code or any comparable provision of any other applicable Tax Law has been engaged in by, or with respect to, Company or any Company Subsidiary. Company and the

Company Subsidiaries have disclosed on their federal income Tax Returns all positions taken therein that could give rise to a substantial understatement of federal income tax within the meaning of Section 6662 of the Code.

3.13.11 Neither Company nor any Company Subsidiary has participated in or been a party to a transaction that, as of the date of this Plan of Merger, constitutes a "listed

transaction" for purposes of Section 6011 of the Code (or a similar provision of state Law).

3.13.12 Neither Company nor any Company Subsidiary has taken any action or has Knowledge of any fact that would reasonably be expected to prevent the Merger from

qualifying for the Intended Tax Treatment.

3.13.13 Except as set forth in Section 3.13.13 of the Company Disclosure Letter, there has been no disallowance of a deduction under Section 162(m) of the Code

or excise tax imposed under Section 280G of the Code for any amount paid or payable by Company or any Company Subsidiary as employee compensation, whether under any contract, plan, program or arrangement, understanding or otherwise, and neither

Company nor any Company Subsidiary has taken any action or has Knowledge of any fact that would reasonably be expected to cause any such disallowance or imposition of excise tax in the future.

3.13.14 Company and the Company Subsidiaries have each maintained all necessary and appropriate accounting records to support the positions taken on all filed Tax Returns

and all exemptions from filing Tax Returns.

3.13.15 Each of Company and the Company Subsidiaries has withheld and paid over all material Taxes required to have been withheld and paid over, and has complied with all

information reporting and backup withholding requirements, including maintenance of required records with respect thereto, in connection with amounts paid or owing to any employee, creditor, independent contractor or other third parties. The

provisions made for Taxes on the Company Financial Statements are sufficient for the payment of all accrued but unpaid Taxes as of the dates of the applicable Company Financial Statement, whether or not disputed.

3.13.16 Neither Company nor any Company Subsidiary will be required to include any item of income in, or exclude any item of deduction from, taxable income for any taxable

period (or portion thereof) ending after the Closing Date as a result of any: (a) change in method of accounting for a taxable period ending on or prior to the Closing Date; (b) "closing agreement" as described in Section 7121 of the Code (or any

corresponding or similar provision of state, local or foreign income Tax Law) executed on or prior to the Closing Date; (c) intercompany transactions or any excess loss account described in Treasury Regulations under Section 1502 of the Code (or

any corresponding or similar provision of state, local or foreign income Tax Law); (d) installment sale or open transaction disposition made on or prior to the Closing Date; or (e) prepaid amounts received or deferred revenue accrued on or prior to

the Closing Date. No property of Company or any Company Subsidiary is "tax exempt use property" within the meaning of Section 168(h) of the Code or directly or indirectly secures any debt the interest on which is exempt from tax under Section

103(a) of the Code. Any federal income tax liability related to bad debt deductions of Company or any Company Subsidiary are recorded in the Company Financial Statements.

3.13.17 Neither Company nor any Company Subsidiary is a party to a Tax sharing, indemnification or similar agreement, is or has been a member of an affiliated group filing

consolidated or combined tax returns (other than a group over which Company is the common parent) or otherwise has any liability for the Taxes of any party other than Company and the Company Subsidiaries.

3.13.18 There is currently no limitation on the utilization of net operating losses, capital losses, built-in losses, tax credits or

similar items of the Company under Sections 269, 382, 383, 384 or 1502 of the Code and the Treasury Regulations thereunder (and comparable provisions of state, local or foreign Law). Neither Company nor any Company Subsidiary (a) has

failed to report any compensation as required by Section 409A of the Code; or (b) has taken any action or has Knowledge of any fact that could reasonably be expected to result in any liability under Section 409A of the Code.

3.14 Properties. With respect to each parcel of real property owned by Company or any Company Subsidiary, including all other real estate owned (but

only for purposes of Sections 3.14.1 and 3.14.4) ("Company Real Property"), and also with respect to

each parcel of real property leased by Company or any Company Subsidiary ("Company-Leased Real Property") (Section 3.14 of the Company Disclosure Letter sets forth a complete and

correct list and brief description of all Company Real Property and Company-Leased Real Property):

3.14.1 Title to and Interest in Properties. Company and each Company Subsidiary has good and valid title to, or valid

leasehold interests in, all of their Company Real Property and Company-Leased Real Property free and clear of all Liens, except for Permitted Liens.

3.14.2 No Encroachments. Except for encroachments that have been insured by a title insurance policy benefitting Company or a

Company Subsidiary, no building or improvement to Company Real Property or, to the Knowledge of Company, Company-Leased Real Property encroaches on any easement or property owned by another Person. No building or property owned by another Person

encroaches on Company Real Property or, to the Knowledge of Company, Company-Leased Real Property or on any easement benefiting Company Real Property or Company-Leased Real Property. No claim of encroachment has been asserted by any Person with

respect to any of Company Real Property or, to the Knowledge of Company, Company-Leased Real Property.

3.14.3 Buildings. All buildings and improvements to Company Real Property and, to the Knowledge of Company, Company-Leased Real

Property are in good condition (normal wear and tear excepted and subject to maintenance and repair in the ordinary course), are structurally sound and are not in need of material repairs, are fit for their intended purposes, and are adequately

serviced by all utilities necessary for the effective operation of business as presently conducted at that location.

3.14.4 No Condemnation. None of Company Real Property or, to the Knowledge of Company, Company-Leased Real Property is the

subject of any condemnation action. To the Knowledge of Company, there is no proposal under active consideration by any public or governmental authority or entity to acquire Company Real Property or Company-Leased Real Property for any

governmental purpose.

3.14.5 Validity. Each premises comprising Company Real Property and, to the Knowledge of Company, Company-Leased Real Property

is a lawfully existing parcel that is: (a) a valid platted parcel; (b) a valid condominium unit; or (c) a lawfully existing parcel within the meaning of the Land Division Act, Act No. 288 of the Public Acts of 1967, as amended.

3.14.6 Access. Each premises comprising Company Real Property and, to the Knowledge of Company, Company-Leased Real Property

has both legal and practical pedestrian and vehicular access to a public street.

3.14.7 Obligations. Company and each Company Subsidiary, as applicable, has paid all amounts due and owing and performed in

all material respects all obligations under each agreement that affects any of Company Real Property or Company-Leased Real Property.

3.14.8 Additional Representations Regarding Real and Personal Property Leases. With respect to each lease and license pursuant

to which Company or any Company Subsidiary, as lessor, lessee, licensor or licensee, has possession or leases or licenses to others any real or personal property, excluding any personal property lease with payments of less than $50,000 per year

(each, a "Company Lease"):

(a) Valid. Each of Company's Leases is valid, effective, and enforceable against the lessor or licensor in accordance

with its terms, except as limited by bankruptcy, insolvency, moratorium, reorganization or similar Laws affecting the rights of creditors generally and the availability of equitable remedies.

(b) No Default. There is no existing default under any of Company's Leases or any event that with notice or passage of

time, or both, would constitute a default with respect to Company, any Company Subsidiary or, to the Knowledge of Company, any other party to the contract, which default is reasonably expected to have a Company Material Adverse Effect.

3.14.9 Personal Property. Company or a Company Subsidiary, as applicable, has good,

valid and insurable title to, or a valid leasehold interest in, all tangible and intangible assets used, intended or required for use by Company and the Company Subsidiaries in the conduct of their businesses, free and clear of any Liens, except

for Permitted Liens, and all such tangible personal property is in good working condition and repair, normal wear and tear excepted and subject to maintenance and repair in the ordinary course.

3.15 Intellectual Property. Company and the Company Subsidiaries exclusively own, or have a valid license or other valid right to use, all material

Intellectual Property as used in their business as presently conducted; it being understood that the foregoing shall not be construed to expand or diminish the scope of the non-infringement representations and warranties that follow in this Section 3.15. No Actions, suits or other proceedings are pending or, to the Knowledge of Company, threatened that Company or any of the Company Subsidiaries is infringing, misappropriating or otherwise

violating the rights of any Person with regard to any Intellectual Property. To the Knowledge of Company, no Person is infringing, misappropriating or otherwise violating the rights of Company or any of the Company Subsidiaries with respect to any

Intellectual Property owned or purported to be owned by Company or any of the Company Subsidiaries, all of which registered Intellectual Property is listed on Section 3.15 of the Company Disclosure Letter (collectively the "Company-Owned Intellectual Property"). Except as have not had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect, to the

Knowledge of Company: (a) no circumstances exist which could reasonably be expected to give rise to any (i) Action that challenges the rights of Company or any of the Company Subsidiaries with respect to the validity or enforceability of the

Company-Owned Intellectual Property or (ii) claim of infringement, misappropriation, or violation by the Company of the Intellectual Property rights of any Person, and (b) the consummation of the transactions contemplated by this Plan of Merger

will not give rise to any claim by any Person to a right to own, purchase, transfer, use, alter, impair, extinguish or restrict any Company-Owned Intellectual Property or Intellectual Property licensed to Company or any Company Subsidiary.

3.16 Required Licenses, Permits, Etc. Company and each Company Subsidiary hold all material Permits and other rights from all appropriate

Governmental Entities necessary for the conduct of its business substantially as presently conducted. All such material Permits and rights are in full force and effect, and none of Company or any Company

Subsidiaries has received any notice (whether written or, to the Knowledge of the Company, oral) of any pending or threatened action by any Governmental Entity to suspend, revoke, cancel or limit any Permit.

3.17 Material Contracts and Change of Control.

3.17.1 "Material Contracts" Defined. For the purposes of this Plan of Merger, the term "Company Material Contract" means any of the following Contracts to which Company or any of the Company Subsidiaries is a party or to which any of them or their assets are bound as of the date of this Plan of Merger:

3.17.1.1 Each Contract that would be required to be filed by Company as a material contract pursuant to Item 601(b)(10) of Regulation S-K on Form 10-K under the

Exchange Act as if Company were required to file a Form 10-K;

3.17.1.2 Each Contract, other than any Contracts contemplated by this Plan of Merger, that limits in any material respect the ability of Company or any of the Company

Subsidiaries to engage or compete in any business (including geographic restrictions and exclusive or preferential arrangements);

3.17.1.3 Each Contract that creates a partnership or joint venture to which Company or any of the Company Subsidiaries is a party;

3.17.1.4 Each Contract between or among Company and any Company Subsidiary or Company Subsidiaries;

3.17.1.5 Each employment Contract with an employee of Company or any Company Subsidiary or any other compensatory Contract or plan in which any executive officer of

Company or any Company Subsidiary participates (other than any compensatory Contract or plan which pursuant to its terms is available to employees, officers, or directors generally and which in operation provides for the same method of allocation

of benefits between management and non-management participants);

3.17.1.6 Each Contract with a correspondent bank;

3.17.1.7 Any commitment made to Company or the Company Subsidiaries relating to outstanding Indebtedness, permitting it to borrow money, any letter of credit, any

pledge, any security agreement, any guarantee or any subordination agreement, or other similar or related type of understanding, as to which Company or any of the Company Subsidiaries is a debtor or pledgor, other than Contracts evidencing deposit

liabilities, purchases of federal funds, fully secured repurchase agreements, FHLB advances, or trade payables made in the ordinary course of business consistent with past practices;

3.17.1.8 Each Contract that relates to the acquisition or disposition of any material business (whether by merger, sale of stock, sale of assets or otherwise) or

material asset, other than this Plan of Merger, pursuant to which Company or any of the Company Subsidiaries has any continuing obligations, contingent or otherwise;

3.17.1.9 Each Contract that grants any right of first refusal or right of first offer or similar right or that limits the ability of Company or any of the Company

Subsidiaries to own, operate, sell, transfer, pledge or otherwise dispose of any material amount of assets or businesses;

3.17.1.10 Other than as contemplated by this Plan of Merger, each voting agreement or registration rights agreement with respect to the capital stock of Company or any

of the Company Subsidiaries;

3.17.1.11 Each Contract granting Company or any Company Subsidiary the right to use, restricting Company's or any Company Subsidiary's right to use, or granting any

other Person the right to use Intellectual Property that is material to the conduct of Company's or any Company Subsidiary's business (including any license, franchise agreement, co-existence agreement, concurrent-use agreement, settlement

agreement or other similar type Contract) (other than “off the shelf” shrink-wrap license agreements or other similar license agreements);

3.17.1.12 Each Contract that limits the payment of dividends by Company or any Company Subsidiary;

3.17.1.13 Except agreements made in accordance with Regulation O and agreements entered into in the ordinary course of business consistent with past practice for

compensation or indemnity, any Contract between Company or any Company Subsidiary, on the one hand, and, on the other hand (a) any officer or director of Company or a Company Subsidiary, or (b) to the Knowledge of Company, any (i) record or

beneficial owner of 5 percent or more of the voting securities of Company, (ii) Affiliate or “immediate family member” (as defined by the Federal Reserve Board in Regulation Y) of any such officer, director, or record or beneficial owner, or (iii)

other Affiliate of Company, except in each case those Contracts of a type available to employees of Company generally;

3.17.1.14 Each Contract for any one capital expenditure or a series of capital expenditures, the aggregate amount of which is in excess of $100,000;

3.17.1.15 As of June 30, 2024, each Contract or commitment to make a loan not yet fully disbursed or funded to any Person, wherein the undisbursed or unfunded amount

exceeds $1,000,000;

3.17.1.16 Each Contract or commitment for a loan participation agreement with any other Person in excess of $500,000; and

3.17.1.17 Each Contract with a labor union, including any Collective Bargaining Agreement.

3.17.2 Full Force and Effect. Prior to the date of this Plan of Merger, Company has provided or made available to Purchaser a

true and complete copy of each Company Material Contract in effect as of the date of this Plan of Merger. Each such Company Material Contract is listed on Section 3.17.2 of the Company Disclosure Letter. Except for matters that have not

had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect, (a) all Company Material Contracts are, valid, binding and in full force and effect as of the date of this Plan of Merger, (b)

neither Company nor any of the Company Subsidiaries is in violation or breach of or default under (or with notice or lapse of time, or both, would be in violation or breach of or default under) the terms of any Company Material Contract, (c) to the

Knowledge of Company, no other party to any Company Material Contract is in breach of or in default under any Company Material Contract, and (d) neither Company nor any Company Subsidiary has received written notice of breach or termination (or

proposed breach or termination) of any Company Material Contract.

3.17.3 Effect of Merger and Related Transactions. There is no Company Material Contract under which (a) except as set forth

on Section 3.17.3(a) of the Company Disclosure Letter consent or approval is required from any Person, (b) a prohibited assignment by operation of Law could occur, (c) a waiver or loss of any right of Company or any Company Subsidiary could

occur, or (d) an acceleration of any obligation, or the creation or imposition of a Lien on any asset, property or right, of the Company or any Company Subsidiary, could occur, in each case as a result of the execution and delivery of this Plan of

Merger or the consummation of the transactions contemplated herein, where any such occurrence would reasonably be expected to (i) materially interfere with the ordinary course of business consistent with past practices conducted by Company or any

Company Subsidiary or (ii) have a Company Material Adverse Effect.

3.17.4 Except as set forth in Section 3.17.4 of the Company Disclosure Letter, all data processing contracts of Company or the Company Subsidiaries are

cancelable by Company or the Company Subsidiaries on or before the Effective Time without cost, penalty, or further obligation, except for costs, penalties or further obligations that, in the aggregate with respect to any Contract, do not exceed

$150,000. Except as set forth in Section 3.17.4 of the Company Disclosure Letter, neither Company nor any Company Subsidiary is a party to any contract, agreement, arrangement, or understanding (other than ordinary and customary banking

relationships) that would require any payment to another party upon termination in excess of $150,000.

3.18 Labor and Employment Matters.

3.18.1 Compliance with Labor and Employment Laws. (a) Company and all of the Company Subsidiaries are in compliance with all

applicable Laws relating to labor and employment practices, including those relating to wages, employee benefits, hours and overtime, workplace safety and health, immigration, individual and collective termination, non-discrimination,

non-harassment, non-retaliation, accommodations, leave (paid and unpaid), workers’ compensation insurance, unemployment insurance, and data privacy, the identification of particular employees or job classifications as "exempt" or "non-exempt" for

purposes of such obligations, and any and all other matters involving compensation or benefits afforded to or not afforded to employees, contractors or consultants except for such noncompliance as has not had, and would not reasonably be expected

to have, individually or in the aggregate, a Company Material Adverse Effect; (b) there is no unfair labor practice charge or complaint pending before the NLRB or, to the Knowledge of Company, threatened against Company or any of the Company

Subsidiaries; (c) during the past three years, there has been no labor strike, slowdown, work stoppage or lockout pending or, to the Knowledge of Company, threatened against or affecting Company or any of the Company Subsidiaries; (d) to the

Knowledge of the Company, there is no current claim or activity by any labor organization seeking representational status with respect to the employees of the Company or any Company Affiliate, and there is no representation claim or petition

pending before the NLRB or any similar foreign agency relating to the employees of Company or any Company Subsidiary; (e) Company has not received written notice of any charge or complaint with respect to or relating to Company or any Company

Subsidiary pending before the Equal Employment Opportunity Commission or any other Governmental Entity responsible for the enforcement of labor or employment laws; and (f) neither Company nor any Company Subsidiary has received any written notice

from any Governmental Entity responsible for the enforcement of labor or employment Laws of an intention to conduct an investigation or audit of Company or any Company Subsidiary and, to the Knowledge of Company, no such investigation or audit is

in progress.

3.18.2 Collective Bargaining Agreements. Neither Company nor any Company Subsidiary is party to, bound by, or negotiating any

Collective Bargaining Agreement or any other Contract with any labor organization, union, works council, employee representative or association relating to the employees of Company or any Company Subsidiary.

3.18.3 At-Will Employment. Except as set forth on Section 3.18.3 of the Company Disclosure Letter, all salaried

employees, hourly employees, and temporary employees of Company and any of the Company Subsidiaries are employed on an at-will basis by Company or any of the Company Subsidiaries and may be terminated at any time with or without cause and without

any severance or other liabilities to Company or any Company Subsidiary, and have signed an agreement or acknowledged in writing that their employment is at will. There has been no written representation by Company or any Company Subsidiary made

to any employees that commits Company, any Company Subsidiary, or the Surviving Corporation to retain them as employees for any period of time subsequent to the Closing.

3.18.4 WARN Act. Since January 1, 2011, neither Company nor any Company Subsidiary has effectuated a "plant closing" or a

"mass lay off" (in each case, as defined in the WARN Act or any applicable state laws pertaining to such matters), in either case affecting any site of employment or facility of Company or any Company Subsidiary, except in compliance with the WARN

Act and any applicable state laws pertaining to such matters.

3.18.5 Occupational Health and Safety. There is no audit, investigation, charge or proceeding with respect to a material

violation of any occupational health and safety standards that is pending or unremedied, or to the Knowledge of Company, threatened against Company or any Company Subsidiary. Company and all of the Company Subsidiaries are in compliance with all

applicable occupational health and safety Laws, except for such failures to comply as have not had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect.

3.18.6 Liabilities under Employment and Benefit Contracts. Except as set forth in Section 3.18.6 of the Company

Disclosure Letter, the consummation of the transactions contemplated by this Plan of Merger will not create Liabilities for any act by Company or any Company Subsidiary on or prior to the Closing under any Collective Bargaining Agreement,

employment or benefit Contract or Company Benefit Plan.

3.18.7 Eligibility Verification. Company has implemented commercially reasonable procedures to ensure that all employees who

are performing services for Company or any Company Subsidiary in the United States are legally permitted to work in the United States and will be legally permitted to work in the United States for the Surviving Corporation or any of its Affiliates

following the consummation of the transactions contemplated by this Plan of Merger.

3.18.8 Employment Policies, Programs, and Procedures. The policies, programs, and practices of Company and all Company

Subsidiaries relating to equal opportunity and affirmative action, wages, employee classifications (including independent contractor versus employee and exempt versus non-exempt), hours of work, employee disabilities, employment termination,

employment discrimination, employee safety, labor relations, and other terms and conditions of employment are in compliance in all material respects with applicable Law governing or relating to employment and employer practices and facilities.

3.18.9 Record of Payments. There is no existing or outstanding material obligation of Company or the Company Subsidiaries,

whether arising by operation of Law, civil or common, by contract, or by past custom, for any Employment-Related Payment to any trust, fund, company, governmental agency, or any person that has not been duly recorded on the books and records of

Company and/or the Company Subsidiaries and paid when due or duly accrued in the ordinary course of business in accordance with GAAP. For purposes of this Plan of Merger, "Employment-Related

Payments" include any payment to be made with respect to any contract for employment or severance agreement; unemployment compensation benefits, profit sharing, pension, employee stock ownership plan or retirement benefits; social security

benefits; compensation; fringe benefits, including vacation or holiday pay, bonuses, and other forms of compensation; or for medical insurance or medical expenses; any of which are payable with respect to any present or former director, officer,

employee, or agent, or his or her survivors, heirs, legatees, or legal representatives.

3.18.10 Additional Employment Related Agreements. Except as set forth in Section 3.18.10 of the Company Disclosure

Letter, Company and the Company Subsidiaries are not parties to, or bound by, any oral or written, express or implied, (a) plan, contract, arrangement, understanding, or practice providing for bonuses, pensions, options, stock purchases,

restricted stock, stock appreciation rights, stock awards, deferred compensation, retirement payments, retirement benefits of the type described Accounting Standard Codification 715 (Compensation – Retirement Benefits), or profit sharing; or (b)

plan, contract, arrangement, understanding or practice with respect to payment of medical expenses, insurance (except insurance continuation limited to that required under provisions of Consolidated Omnibus Budget Reconciliation Act), or other

benefits for any former director, employee or any spouse, child, member of the same household, estate or survivor of any director or employee or former director or employee.

3.19 Employee Benefits.

3.19.1 Section 3.19.1 of the Company Disclosure Letter sets for a true and complete list of each Company Benefit Plan. Company has delivered or made available

to Purchaser true and complete copies of the following, to the extent applicable, (i) all Company Benefit Plans, including amendments thereto, (ii) each trust agreement, group annuity contract, summary plan description and summary of material

modifications, relating to such Company Benefit Plan, (iii) the most recent actuarial report, financial statement or valuation report for such Company Benefit Plan, and (iv) all material correspondence to or from any Governmental Entity relating to

any audit or investigation of such Company Benefit Plan in the six year period prior to the date hereof. Each Company Benefit Plan is in compliance with all applicable requirements of ERISA, the Code and all other applicable Laws and has been

administered in accordance with its terms and such Laws, except for such noncompliance that has not had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect.

3.19.2 Each Company Benefit Plan intended to qualify under Section 401(a) of the Code or under Section 501(c)(9) of the Code is listed in Section 3.19.2 of the

Company Disclosure Letter and has received a favorable determination, advisory, or opinion letter from the IRS that it is so qualified, and the related trusts have been determined to be exempt from taxation, or is established on a

pre-approved form or prototype of plan document that has received or requested a favorable opinion or advisory letter from the IRS that such form or plan document is so qualified or exempt. A copy of the most recent determination, advisory, or

opinion letter with respect to each such Company Benefit Plan has been delivered to Purchaser, and to the Knowledge of Company, no condition exists or existed and nothing has occurred prior to or since the date of such letter that would cause the

loss of such qualification or exemption. All contributions, payments or premiums required to be made with respect to any Company Benefit Plan by Company have been timely made, and all benefits accrued under any unfunded Company Benefit Plan have

been paid, accrued or otherwise adequately reserved in accordance with GAAP.

3.19.3 Neither Company nor any ERISA Affiliate of Company participates in nor has ever participated in any Multiemployer Plan, and neither Company nor any ERISA

Affiliate of Company maintains or contributes to, or is party to, and, nor has it ever maintained, contributed to, or was a party to, any plan, program, agreement or policy that (a) is a "defined benefit plan" within the meaning of Section 414(j)

of the Code or Section 3(35) of ERISA, (b) is a "multiple employer plan" as defined in ERISA or the Code (whether or not subject thereto), (c) is described in Section 401(a)(1) of ERISA (whether or not subject thereto), (d) is a multiple employer

welfare arrangement within the meaning of Section 3(40)(A) of the Code, (e) is a voluntary employees beneficiary association within the meaning of Code Section 501(c)(9), or (f) is primarily for the benefit of employees who reside outside of the

United States.

3.19.4 Except as required by Part 6 of Subtitle B of Title I of ERISA or Section 4980B of the Code or any state Laws requiring continuation of benefits coverage

following termination of employment, neither Company nor any Company Subsidiary provides health or welfare benefits for any retired or former employee or service provider to the Company or a Company Subsidiary following such individual's retirement

or other termination of service.

3.19.5 Except as disclosed in Section 3.19.5 of the Company Disclosure Letter, the execution, delivery of, and performance by Company of its obligations under the

transactions contemplated by this Plan of Merger (either alone or upon the occurrence of any additional or subsequent event) will not (a) result in any payment (whether of severance pay or otherwise), acceleration, forgiveness of Indebtedness,

vesting, distribution, increase in benefits or obligation to fund benefits with respect to any current, former or retired employees, officers, consultants, independent contractors, agents or directors of Company or any of the Company Subsidiaries;

(b) result in the triggering or imposition of any restrictions or limitations on the right of Company or any of the Company Subsidiaries to amend or terminate any Company Benefit Plan; or (c) result in any payment that is non-deductible to

Purchaser or that is an "excess parachute payment" within the meaning of Section 280G(b)(1) of the Code.

3.19.6 Except as set forth in Section 3.19.6 of the Company Disclosure Letter, Company and the Company Subsidiaries may, subject to the limitations imposed by

applicable Law and the terms of the applicable Company Benefit Plan, without the consent of any employee, beneficiary, or other person, prospectively terminate, modify, or amend any such Company Benefit Plan effective as of any date on or after

the date of this Plan of Merger.

3.19.7 Each Company Benefit Plan that is a "nonqualified deferred compensation plan" (as defined under Section 409A(d)(1) of the Code) has been operated and administered

in compliance with Section 409A of the Code in all material respects. Neither Company nor any of the Company Subsidiaries have entered into any agreement or arrangement to, and do not otherwise have any obligation to, indemnify or hold harmless

any Person for any Liability that results from the failure to comply with the requirements of Section 409A of the Code and the regulations promulgated thereunder.

3.19.8 No stock options, stock appreciation rights or other grants of stock-based awards by Company or any Company Subsidiaries were backdated, spring‑loaded, or granted

at less than fair market value.

3.19.9 There is no pending or, to the Knowledge of Company, threatened Action with respect to any Company Benefit Plans, other than ordinary and usual claims for

benefits by participants and beneficiaries.

3.19.10 No Company Benefit Plan and no trust created thereunder has been involved in any nonexempt "prohibited transaction" as defined in Section 4975 of the Code or in

Sections 406 and 408 of ERISA which has subjected, or would reasonably be expected to subject, a Company Benefit Plan or related trust or Company or any Company Subsidiary to any material Tax or penalty imposed under Section 4975 of the Code or

Section 502 of ERISA.

3.19.11 Except as set forth in Section 3.19.11 of the Company Disclosure Letter, no payment that is owed or may become due to any director, officer,

employee, or agent of Company or any Company Subsidiary will be non-deductible or subject to any penalty or excise tax; nor do any Company Benefit Plans require Company or a Company Subsidiary to "gross up" or otherwise compensate any such person

because of the imposition of any excise tax on a payment to such person.

3.19.12 There is no payment that has become due from any Company Benefit Plan, any trust created thereunder, or from Company or any Company Subsidiary that has not been

paid through normal administrative procedures to the plan participants or beneficiaries entitled thereto, except for claims for benefits for which administrative claims procedures under such plan have not been exhausted.

3.19.13 No statement, either written or oral, has been made by Company or any Company Subsidiary to any person with regard to any Company Benefit Plan that was not in

accordance with the Company Benefit Plan and that could have a Company Material Adverse Effect.

3.19.14 Neither Company nor any Company Subsidiary provides health or welfare benefits that are self-insured. To the extent Company or a Company Subsidiary provides

self-insured health or welfare benefits, all such benefits are covered by a stop-loss policy.

3.19.15 Neither Company nor any Company Subsidiary has any liability to any governmental or regulatory body with respect to any Company Benefit Plan or any related trust,

account or other funding vehicle.

3.19.16 The assets and liabilities of each Company Benefit Plan have been reported on the Company Financial Statements in accordance with GAAP.

3.20 Environmental Matters.

3.20.1 Except for any matters that have not had, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse Effect: (a)

Company and each of the Company Subsidiaries is and has been in compliance with and has no Liability under applicable Environmental Laws; (b) Company and each of the Company Subsidiaries possesses, has possessed and is and has been in compliance

with all required Environmental Permits; (c) there are no Environmental Claims pending or, to the Knowledge of Company, threatened against Company or any of the Company Subsidiaries, and, to the Knowledge of Company, there are no facts or

circumstances which could reasonably be expected to form the basis for any Environmental Claim against Company or any of the Company Subsidiaries; (d) no Releases of Hazardous Materials have occurred and no Person has been exposed to any Hazardous

Materials at, from, in, to, on, or under any Company Site and no Hazardous Materials are present in, on, about or migrating to or from any Company Site that could give rise to an Environmental Claim against Company or any of the Company

Subsidiaries; (e) neither Company nor any of the Company Subsidiaries has entered into or is subject to, any judgment, decree, order or other similar requirement of or agreement with any Governmental Entity under any Environmental Laws; (f) neither

Company nor any of the Company Subsidiaries has assumed responsibility for or agreed to indemnify or hold harmless any Person for any Liability arising under or relating to Environmental Laws; and (g) neither Company, any predecessors of Company or

any of the Company Subsidiaries, nor any entity previously owned by Company or any of the Company Subsidiaries, has transported or arranged for the treatment, storage, handling, disposal, containment, generation, manufacture, management or

transportation of any Hazardous Material to any off-Site location which has or could result in an Environmental Claim against Company or any of the Company Subsidiaries.

3.20.2 Without limiting the generality of Section 3.20.1, to the Knowledge of Company, the Company Sites are free of asbestos

except for asbestos that has been properly sealed and encapsulated to the extent required by all applicable Environmental Laws and all workplace safety and health Laws and regulations.

3.20.3 No Company Site contains, and to the Knowledge of Company has ever contained, any underground tanks for the storage of Hazardous Materials. Each underground

storage tank presently or previously located on any Company Site has been operated, maintained and removed or closed in place, as applicable, in compliance with all applicable Environmental Laws, and to the Knowledge of the Company has not been the

source of any Release of a Hazardous Material to the environment that has not been fully remediated.

3.21 Duties as Fiduciary. Company and each Company Subsidiary has performed all of its respective duties in any capacity as trustee, executor,

administrator, registrar, guardian, custodian, escrow agent, receiver, or other fiduciary in a fashion that complies in all material respects with all applicable Laws, Contracts, wills, instruments and common law standards. Neither Company nor any

Company Subsidiary has received any notice of any Action, claim, allegation or complaint from any Person that Company or any Company Subsidiary failed to perform these duties in a manner that complies in all material respects with all applicable

Laws, Contracts, wills, instruments and common law standards, except for notices involving matters that have been resolved and any cost of such resolution is reflected in the Company Financial Statements.

3.22 Investment Bankers and Brokers. Company has employed Hovde Group, LLC ("Company Investment

Banker") in connection with the Merger. Company, the Company Subsidiaries, and their respective Representatives have not employed, engaged, or consulted with any broker, finder, or investment banker other than Company Investment Banker in

connection with this Plan of Merger or the Merger. Other than the fees and expenses payable by Company to Company Investment Banker in connection with the Merger, as described in Section 3.22 of the Company Disclosure Letter, there is no

investment banking fee, financial advisory fee, brokerage fee, finder's fee, commission, or compensation of a similar type payable by Company or any Company Subsidiary to any Person with respect to the Plan of Merger or the consummation of the

Merger.

3.23 Company-Related Persons. For purposes of this Plan of Merger, the term "Company-Related

Person" shall mean any shareholder owning 5% or more of the Company Common Stock, any director or executive officer of Company or any Company Subsidiary, their spouses and any children or other persons who share the same household with

such persons, and any corporation, limited liability company, partnership, proprietorship, trust, or other entity of which any such persons, alone or together, have control.

3.23.1 Insider Loans. No Company-Related Person has any loan, credit or other Contract outstanding with Company or any Company

Subsidiary that does not conform to applicable rules and regulations of the FDIC, the Federal Reserve Board, or any other Governmental Entity with jurisdiction over Company or any Company Subsidiary.

3.23.2 Control of Material Assets. Except as set forth in Section 3.23.2 of the Company Disclosure Letter, other

than in a capacity as a shareholder, director, or executive officer of Company or any Company Subsidiary, no Company-Related Person owns or controls any material assets or properties that are used in the business of Company or any Company

Subsidiary.

3.23.3 Contractual Relationships. Except as set forth in Section 3.23.3 of the Company Disclosure Letter, other

than ordinary and customary banking relationships, no Company-Related Person has any contractual relationship with Company or any Company Subsidiary.

3.23.4 Loan Relationships. Except as set forth in Section 3.23.4 of the Company Disclosure Letter, no

Company-Related Person has any outstanding loan or loan commitment from, or on whose behalf an irrevocable letter of credit has been issued by, Company or any Company Subsidiary in a principal amount of $500,000 or more.

3.24 Change in Business Relationships. As of the date of this Plan of Merger, the Company has no actual knowledge, whether on account of the Merger

or otherwise, that any customer, agent, representative, supplier of Company or any Company Subsidiary, or other person with whom Company or any Company Subsidiary has a contractual relationship, intends to discontinue, diminish, or change its

relationship with Company or any Company Subsidiary, the effect of which would reasonably be expected to have a Company Material Adverse Effect.

3.25 Insurance. Except as would not have, and would not reasonably be expected to have, individually or in the aggregate, a Company Material Adverse

Effect, Company and the Company Subsidiaries maintain in full force and effect insurance policies on their respective assets, properties, premises, operations, and personnel in such amounts and against such risks and losses as are customary and

adequate for comparable entities engaged in the same business and industry, and the Company and the Company Subsidiaries are in compliance with, and not in default under, any such insurance policy. There is no unsatisfied claim of $50,000 or more

under such insurance as to which the insurance carrier has denied liability. Since January 1, 2021, no insurance company has canceled or failed to renew a policy of insurance covering Company's or any Company Subsidiary's assets, properties,

premises, operations, directors or personnel. Company and the Company Subsidiaries have given adequate and timely notice to each insurance carrier, and have complied with all policy provisions, with respect to any material known claim for which a

defense or indemnification or both may be available to Company or the Company Subsidiaries. Section 3.25 of the Company Disclosure Letter sets forth a true and correct listing of all Company and Company Subsidiaries insurance policies,

policy expiration dates, carriers, coverage limits, premiums and deductibles.

3.26 Allowance for Credit Losses. The allowance for credit losses as reflected in Company's consolidated financial statements and the Company’s