Exhibit 99.1

PRESS RELEASE | Franklin Street Properties Corp. |

401 Edgewater Place ● Suite 200 ● Wakefield, Massachusetts 01880 ● (781) 557-1300 ● www.fspreit.com

Contact: Georgia Touma (877) 686-9496 | For Immediate Release |

Franklin Street Properties Corp. Announces

Third Quarter 2021 Results

Strong Execution on our 2021 Strategy to Reduce Debt and Lease Space

$0.04 GAAP Net Income Per Share

$0.14 Funds From Operations (FFO) Per Share

Wakefield, MA—November 8, 2021—Franklin Street Properties Corp. (the “Company”, “FSP”, “we” or “our”) (NYSE American: FSP), a real estate investment trust (REIT), announced its results for the third quarter ended September 30, 2021.

Significant Debt Reduction Improves Balance Sheet Flexibility for Future Growth Opportunities

| ● | Between September 30, 2020 and October 25, 2021, reduced total indebtedness by approximately 53%, from approximately $1.0 billion to approximately $475 million. |

| ● | Between January 1, 2021 and October 25, 2021, repaid approximately $508 million of indebtedness. |

| ● | During the three months ended September 30, 2021, repaid approximately $90 million of indebtedness. |

| ● | On October 25, 2021, repaid approximately $215 million of indebtedness. |

Ahead on Property Disposition Strategy

| ● | On October 22, 2021, sold 999 Peachtree in Atlanta, Georgia for $223.9 million in gross proceeds and recorded a gain of approximately $86.8 million. |

-2-

| ● | Due to strong demand and pricing, increased the top end of our 2021 disposition guidance from a previous range of approximately $350 million to $450 million to a new range of approximately $563 million to $600 million. |

Leasing Progress and Continuing Portfolio Upside Leasing Potential

| ● | Leased approximately 329,000 square feet during the three months ended September 30, 2021, including approximately 172,000 square feet with new tenants. |

| ● | Signed a lease for approximately 100,000 square feet with a new tenant at our Pershing Park property in Atlanta, Georgia during the three months ended September 30, 2021. |

| ● | In-place weighted average GAAP rent increased by approximately 5% during the nine months ended September 30, 2021. |

Stock Repurchases

| ● | During the three months ended September 30, 2021, we repurchased approximately 1.8 million shares of our common stock for approximately $8.2 million pursuant to our previously announced stock repurchase plan. |

| ● | Shares repurchased during the three months ended September 30, 2021 represent approximately 1.5% of the approximately $563 million in aggregate gross disposition proceeds received to date in 2021. |

| ● | Up to approximately $41.8 million remaining for potential future repurchases of our common stock pursuant to our previously announced stock repurchase plan. |

Anticipated 2021 Special Dividend

| ● | In light of the gains achieved on our dispositions to date in 2021, we anticipate declaring a special dividend in December 2021 to be paid in January 2022 in order to meet REIT requirements. |

George J. Carter, Chairman and Chief Executive Officer, commented as follows:

“I am pleased to report strong execution on our 2021 strategies to reduce debt and to lease space. Highlights include the sale of 999 Peachtree on October 22, 2021 for $223.9 million and a recorded gain of approximately $86.8 million, and the lease of approximately 100,000 square feet with a new tenant at Pershing Park. As of October 22, 2021, we have sold eight properties in 2021 for aggregate gross proceeds of approximately $563 million and an aggregate, weighted-average, in-place capitalization rate of approximately 5.8%. Between September 30, 2020 and October 25, 2021, we reduced our total indebtedness by approximately 53%, from approximately $1.0 billion to approximately $475 million.

We are encouraged by the strong level of demand that our real estate assets have received in the market to date from a diverse pool of potential buyers. Aggregate pricing on the properties sold has exceeded our expectations

-3-

and reinforced our belief that we are unlocking embedded value for our shareholders that is not currently reflected in the price of our common stock. Due to strong demand and pricing, we have increased the top end of our 2021 disposition guidance from a previous range of approximately $350 million to $450 million to a new range of approximately $563 million to $600 million.

Our criteria for selecting potential properties for disposition is asset-specific. We consider a variety of factors, including short to intermediate term value objectives and upside potential. At the same time, we remain fully committed to our historic Sunbelt and Mountain West geographic focus. Accordingly, our 2021 dispositions in the Sunbelt region should not be viewed as a statement about our commitment to such regions.

Importantly, we believe that our continuing portfolio of real estate is well located primarily in the Sunbelt and Mountain West geographic regions, and consists of high-quality assets with significant upside leasing potential in a post-COVID-19 environment. We also believe that the pricing achieved on our dispositions to date in 2021, which has exceeded our expectations, is generally indicative of the pricing that could be achieved on our continuing portfolio of real estate assets.

We continue to believe that the current price of our common stock does not accurately reflect the value of our underlying real estate assets and intend to continue our strategy of seeking to increase shareholder value through the sale of select properties where we believe that our short to intermediate term valuation objectives have been met. We believe that the net value of our continuing real estate portfolio assets (net of outstanding liabilities) would exceed $10.00 per share of common stock based on our market valuation estimates using the pricing levels we have achieved to date on our dispositions as a benchmark applied across our continuing real estate portfolio. We intend to use the proceeds from any future dispositions for debt reduction, repurchases of our common stock, any special dividends required to meet REIT requirements, and other general corporate purposes.”

Financial Highlights

| ● | GAAP net income was $4.5 million, or $0.04 per share, for the three months ended September 30, 2021. |

| ● | Funds From Operations (FFO) was $14.8 million, or $0.14 per basic and diluted share, for the three months ended September 30, 2021. |

| ● | Adjusted Funds From Operations (AFFO) was $0.04 per basic and diluted share for the three months ended September 30, 2021. |

| ● | During the three months ended September 30, 2021, we repaid approximately $90 million of indebtedness. As of September 30, 2021, our total debt outstanding was approximately $675 million. |

| ● | On October 25, 2021, we repaid approximately $215 million of indebtedness and our total debt outstanding decreased to approximately $475 million. |

Leasing Highlights

| ● | During the three months ended September 30, 2021, we leased approximately 329,000 square feet, including 172,000 square feet of new leases. |

| ● | On September 28, 2021, we signed a lease with a new tenant at our Pershing Park property for approximately 100,000 square feet that will substantially backfill the recent vacancy from the departure of Jones Day. |

| ● | During the nine months ended September 30, 2021, we leased approximately 892,000 square feet, of which approximately 622,000 square feet was with existing tenants. During the year ended December 31, 2020, we leased approximately 1,130,000 square feet, of which approximately 762,000 square feet was with existing tenants. |

| ● | Our directly owned real estate portfolio of 27 owned properties (including one redevelopment |

-4-

| property) totaling approximately 7.8 million square feet, was approximately 78.8% leased as of September 30, 2021, compared to approximately 78.5% leased as of June 30, 2021. The increase in the leased percentage is primarily a result of 172,000 square feet of new leases executed during the three months ended September 30, 2021. |

| ● | Lease expirations for the remainder of 2021 are approximately 72,000 square feet, representing approximately 0.9% of our owned portfolio. |

| ● | The weighted average GAAP base rent per square foot achieved on leasing activity during the nine months ended September 30, 2021 was $30.10, or 2.0% higher than average rents in the respective properties as applicable compared to the year ended December 31, 2020. The average lease term on leases in the nine months ended September 30, 2021, was 7.8 years compared to 8.3 years for the full year of 2020. Overall the portfolio weighted average rent per occupied square foot was $30.97 as of September 30, 2021 compared to $29.60 as of December 31, 2020, representing an increase of approximately 5%. |

Investment Highlights

Dividend Update

On October 8, 2021, the Company announced that its Board of Directors declared a regular quarterly cash dividend for the three months ended September 30, 2021 of $0.09 per share of common stock that will be paid on November 11, 2021 to stockholders of record on October 22, 2021.

Non-GAAP Financial Information

A reconciliation of Net income to FFO, AFFO and Sequential Same Store NOI and our definitions of FFO, AFFO and Sequential Same Store NOI can be found on Supplementary Schedules H and I.

2021 Net Income, FFO and Disposition Guidance

-5-

At this time, due primarily to uncertainty surrounding the timing and amount of proceeds received from property dispositions, we are continuing suspension of Net Income and FFO guidance. However, we are updating our previously announced disposition guidance for full-year 2021, as we execute on our strategy to dispose of certain properties that we believe have met their short to intermediate term valuation objectives and whose value may not be accurately reflected in our share price. Anticipated dispositions in 2021 are estimated to result in aggregate gross proceeds in the range of approximately $563 million to $600 million, inclusive of the approximately $563 million of gross proceeds in 2021 realized to date. We intend to use the proceeds of any future dispositions for debt reduction, repurchases of our stock, any special distributions required to meet REIT requirements, and other general corporate purposes. This guidance reflects our current expectations of economic and market conditions and is subject to change. We will update our disposition guidance quarterly in our earnings releases. There can be no assurance that the Company’s actual results will not differ materially from the estimates set forth above.

Real Estate Update

Supplementary schedules provide property information for the Company’s owned and managed real estate portfolio as of September 30, 2021. The Company will also be filing an updated supplemental information package that will provide stockholders and the financial community with additional operating and financial data. The Company will file this supplemental information package with the SEC and make it available on its website at www.fspreit.com.

Today’s news release, along with other news about Franklin Street Properties Corp., is available on the Internet at www.fspreit.com. We routinely post information that may be important to investors in the Investor Relations section of our website. We encourage investors to consult that section of our website regularly for important information about us and, if they are interested in automatically receiving news and information as soon as it is posted, to sign up for E-mail Alerts.

Earnings Call

A conference call is scheduled for November 9, 2021 at 11:00 a.m. (ET) to discuss the third quarter 2021 results. To access the call, please dial 1-800-464-8240. Internationally, the call may be accessed by dialing 1-412-902-6521. To access the call from Canada, please dial 1-866-605-3852. To listen via live audio webcast, please visit the Webcasts & Presentations section in the Investor Relations section of the Company's website (www.fspreit.com) at least ten minutes prior to the start of the call and follow the posted directions. The webcast will also be available via replay from the above location starting one hour after the call is finished.

About Franklin Street Properties Corp.

Franklin Street Properties Corp., based in Wakefield, Massachusetts, is focused on infill and central business district (CBD) office properties in the U.S. Sunbelt and Mountain West, as well as select opportunistic markets. FSP seeks value-oriented investments with an eye towards long-term growth and appreciation, as well as current income. FSP is a Maryland corporation that operates in a manner intended to qualify as a real estate investment trust (REIT) for federal income tax purposes. To learn more about FSP please visit our website at www.fspreit.com.

-6-

Forward-Looking Statements

Statements made in this press release that state FSP’s or management’s intentions, beliefs, expectations, or predictions for the future may be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. This press release may also contain forward-looking statements, such as those relating to our ability to lease space in the future, expectations for dispositions, potential stock repurchases, the payment of special dividends and the repayment of debt in future periods, value creation/enhancement in future periods, the net value of our continuing real estate portfolio per share of common stock, and expectations for growth and leasing activities in future periods that are based on current judgments and current knowledge of management and are subject to certain risks, trends and uncertainties that could cause actual results to differ materially from those indicated in such forward-looking statements. Accordingly, readers are cautioned not to place undue reliance on forward-looking statements. Investors are cautioned that our forward-looking statements involve risks and uncertainty, including without limitation, adverse changes in general economic or local market conditions, including as a result of the COVID-19 pandemic and other potential infectious disease outbreaks and terrorist attacks or other acts of violence, which may negatively affect the markets in which we and our tenants operate, increasing interest rates, disruptions in the debt markets, economic conditions in the markets in which we own properties, risks of a lessening of demand for the types of real estate owned by us, adverse changes in energy prices, which if sustained, could negatively impact occupancy and rental rates in the markets in which we own properties, including energy-influenced markets such as Dallas, Denver and Houston, uncertainty relating to the completion and timing of the disposition of properties under agreement, any inability to dispose of real estate properties at pricing levels comparable to recent historical portfolio dispositions, and any delays in the timing of any such anticipated dispositions, changes in government regulations and regulatory uncertainty, uncertainty about governmental fiscal policy, geopolitical events and expenditures that cannot be anticipated such as utility rate and usage increases, delays in construction schedules, unanticipated increases in construction costs, increases in the level of general and administrative costs as a percentage of revenues as revenues decrease as a result of property dispositions, unanticipated repairs, additional staffing, insurance increases and real estate tax valuation reassessments. See the “Risk Factors” set forth in Part I, Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2020, as the same may be updated from time to time in subsequent filings with the United States Securities and Exchange Commission. Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, acquisitions, dispositions, performance or achievements. We will not update any of the forward-looking statements after the date of this press release to conform them to actual results or to changes in our expectations that occur after such date, other than as required by law.

-7-

Franklin Street Properties Corp.

Earnings Release

Supplementary Information

Table of Contents

| |

Franklin Street Properties Corp. Financial Results | A-C |

Real Estate Portfolio Summary Information | D |

Portfolio and Other Supplementary Information | E |

Percentage of Leased Space | F |

Largest 20 Tenants – FSP Owned Portfolio | G |

Reconciliation and Definitions of Funds From Operations (FFO) and Adjusted | |

Funds From Operations (AFFO) | H |

Reconciliation and Definition of Sequential Same Store results to Property Net | |

Operating Income (NOI) and Net Loss | I |

| |

-8-

Franklin Street Properties Corp. Financial Results

Supplementary Schedule A

Condensed Consolidated Statements of Operations

(Unaudited)

| | For the | | For the | | ||||||||

| | Three Months Ended | | Nine Months Ended | | ||||||||

| | September 30, | | September 30, | | ||||||||

(in thousands, except per share amounts) |

| 2021 |

| 2020 |

| 2021 |

| 2020 |

| ||||

| | | | | | | | | | | | | |

Revenue: | | | | | | | | | | | | | |

Rental | | $ | 50,326 | | $ | 61,834 | | $ | 164,671 | | $ | 184,799 | |

Related party revenue: | | | | | | | | | | | | | |

Management fees and interest income from loans | | | 419 | | | 400 | | | 1,246 | | | 1,208 | |

Other | | | 57 | | | 13 | | | 69 | | | 31 | |

Total revenue | | | 50,802 | | | 62,247 | | | 165,986 | | | 186,038 | |

| | | | | | | | | | | | | |

Expenses: | | | | | | | | | | | | | |

Real estate operating expenses | | | 14,373 | | | 16,730 | | | 45,664 | | | 49,498 | |

Real estate taxes and insurance | | | 10,200 | | | 12,279 | | | 34,461 | | | 36,348 | |

Depreciation and amortization | | | 18,862 | | | 22,076 | | | 62,379 | | | 66,659 | |

General and administrative | | | 3,749 | | | 3,817 | | | 11,857 | | | 11,159 | |

Interest | | | 7,928 | | | 8,953 | | | 26,582 | | | 26,996 | |

Total expenses | | | 55,112 | | | 63,855 | | | 180,943 | | | 190,660 | |

| | | | | | | | | | | | | |

Loss on extinguishment of debt | | | (236) | | | — | | | (403) | | | — | |

Gain on sale of properties, net | | | 8,632 | | | — | | | 29,258 | | | — | |

Income (loss) before taxes | | | 4,086 | | | (1,608) | | | 13,898 | | | (4,622) | |

Tax expense | | | 51 | | | 71 | | | 174 | | | 203 | |

Equity in income of non-consolidated REITs | | | 421 | | | — | | | 421 | | | — | |

Net income (loss) | | $ | 4,456 | | $ | (1,679) | | $ | 14,145 | | $ | (4,825) | |

| | | | | | | | | | | | | |

Weighted average number of shares outstanding, basic and diluted | | | 106,905 | | | 107,328 | | | 107,196 | | | 107,295 | |

| | | | | | | | | | | | | |

Net income (loss) per share, basic and diluted | | $ | 0.04 | | $ | (0.02) | | $ | 0.13 | | $ | (0.04) | |

-9-

Franklin Street Properties Corp. Financial Results

Supplementary Schedule B

Condensed Consolidated Balance Sheets

(Unaudited)

| | September 30, | | December 31, | | ||

(in thousands, except share and par value amounts) |

| 2021 |

| 2020 |

| ||

Assets: | | | | | | | |

Real estate assets: | | | | | | | |

Land | | $ | 161,767 | | $ | 189,155 | |

Buildings and improvements | | | 1,630,729 | | | 1,938,629 | |

Fixtures and equipment | | | 11,727 | | | 12,949 | |

| | | 1,804,223 | | | 2,140,733 | |

Less accumulated depreciation | | | 459,531 | | | 538,717 | |

Real estate assets, net | | | 1,344,692 | | | 1,602,016 | |

Acquired real estate leases, less accumulated amortization of $50,302 and $55,447, respectively | | | 19,864 | | | 28,206 | |

Cash, cash equivalents and restricted cash | | | 9,731 | | | 4,150 | |

Tenant rent receivables | | | 2,681 | | | 7,656 | |

Straight-line rent receivable | | | 58,132 | | | 67,789 | |

Prepaid expenses and other assets | | | 5,547 | | | 5,752 | |

Related party mortgage loan receivables | | | 21,000 | | | 21,000 | |

Office computers and furniture, net of accumulated depreciation of $1,180 and $1,443, respectively | | | 153 | | | 163 | |

Deferred leasing commissions, net of accumulated amortization of $24,013 and $30,411, respectively | | | 44,729 | | | 56,452 | |

Total assets | | $ | 1,506,529 | | $ | 1,793,184 | |

| | | | | | | |

Liabilities and Stockholders’ Equity: | | | | | | | |

Liabilities: | | | | | | | |

Bank note payable | | $ | — | | $ | 3,500 | |

Term loans payable, less unamortized financing costs of $1,352 and $2,677, respectively | | | 473,648 | | | 717,323 | |

Series A & Series B Senior Notes, less unamortized financing costs of $699 and $822, respectively | | | 199,301 | | | 199,178 | |

Accounts payable and accrued expenses | | | 59,309 | | | 72,058 | |

Accrued compensation | | | 3,482 | | | 3,918 | |

Tenant security deposits | | | 6,169 | | | 8,677 | |

Lease liability | | | 1,256 | | | 1,536 | |

Other liabilities: derivative liabilities | | | 7,583 | | | 17,311 | |

Acquired unfavorable real estate leases, less accumulated amortization of $3,377 and $4,031, respectively | | | 708 | | | 1,592 | |

Total liabilities | | | 751,456 | | | 1,025,093 | |

| | | | | | | |

Commitments and contingencies | | | | | | | |

| | | | | | | |

Stockholders’ Equity: | | | | | | | |

Preferred stock, $.0001 par value, 20,000,000 shares authorized, none issued or outstanding | | | — | | | — | |

Common stock, $.0001 par value, 180,000,000 shares authorized, 105,632,725 and 107,328,199 shares issued and outstanding, respectively | | | 11 | | | 11 | |

Additional paid-in capital | | | 1,349,225 | | | 1,357,131 | |

Accumulated other comprehensive loss | | | (7,583) | | | (17,311) | |

Accumulated distributions in excess of accumulated earnings | | | (586,580) | | | (571,740) | |

Total stockholders’ equity | | | 755,073 | | | 768,091 | |

Total liabilities and stockholders’ equity | | $ | 1,506,529 | | $ | 1,793,184 | |

-10-

Franklin Street Properties Corp. Financial Results

Supplementary Schedule C

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| | For the | | ||||

| | Nine Months Ended | | ||||

| | September 30, | | ||||

(in thousands) |

| 2021 |

| 2020 |

| ||

Cash flows from operating activities: | | | | | | | |

Net income (loss) | | $ | 14,145 | | $ | (4,825) | |

Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | | | | | |

Depreciation and amortization expense | | | 64,390 | | | 68,859 | |

Amortization of above and below market leases | | | (38) | | | (234) | |

Shares issued as compensation | | | 338 | | | 337 | |

Equity in income of non-consolidated REITs | | | (421) | | | — | |

Distributions from non-consolidated REITs | | | 421 | | | — | |

Loss on extinguishment of debt | | | 403 | | | — | |

Gain on sale of properties, net | | | (29,258) | | | — | |

Decrease in allowance for doubtful accounts and write-off of accounts receivable | | | — | | | (13) | |

Changes in operating assets and liabilities: | | | | | | | |

Tenant rent receivables | | | 4,975 | | | (143) | |

Straight-line rents | | | (3,103) | | | (2,636) | |

Lease acquisition costs | | | (1,666) | | | (1,516) | |

Prepaid expenses and other assets | | | (1,035) | | | (504) | |

Accounts payable and accrued expenses | | | (8,389) | | | 2,527 | |

Accrued compensation | | | (436) | | | 234 | |

Tenant security deposits | | | (2,508) | | | 89 | |

Payment of deferred leasing commissions | | | (10,857) | | | (6,168) | |

Net cash provided by operating activities | | | 26,961 | | | 56,007 | |

Cash flows from investing activities: | | | | | | | |

Property improvements, fixtures and equipment | | | (55,008) | | | (61,989) | |

Proceeds received from sale of properties | | | 319,357 | | | — | |

Net cash provided by (used in) investing activities | | | 264,349 | | | (61,989) | |

Cash flows from financing activities: | | | | | | | |

Distributions to stockholders | | | (28,985) | | | (28,968) | |

Stock repurchases | | | (8,244) | | | — | |

Borrowings under bank note payable | | | 76,500 | | | 85,000 | |

Repayments of bank note payable | | | (80,000) | | | (55,000) | |

Repayment on term loan payable | | | (245,000) | | | — | |

Net cash provided by (used in) financing activities | | | (285,729) | | | 1,032 | |

Net increase (decrease) in cash, cash equivalents and restricted cash | | | 5,581 | | | (4,950) | |

Cash, cash equivalents and restricted cash, beginning of year | | | 4,150 | | | 9,790 | |

Cash, cash equivalents and restricted cash, end of period | | $ | 9,731 | | $ | 4,840 | |

-11-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule D

Real Estate Portfolio Summary Information

(Unaudited & Approximated)

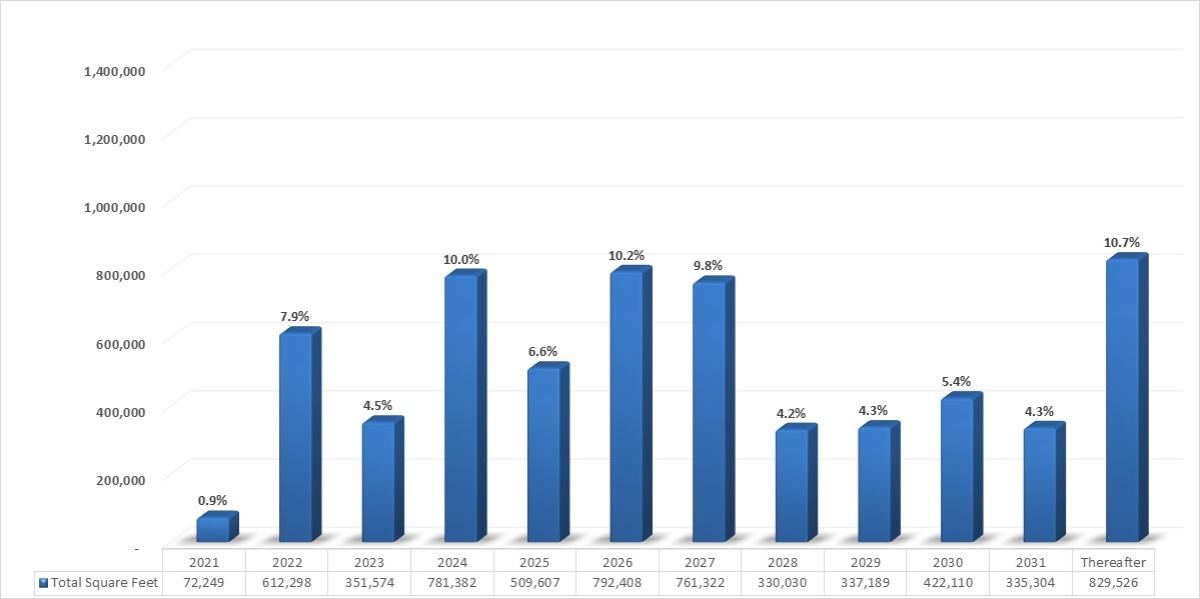

Commercial portfolio lease expirations (1) | | | | | |

| | Total | | % of | |

Year |

| Square Feet |

| Portfolio |

|

2021 | | 72,249 | | 0.9% | |

2022 | | 612,298 | | 7.9% | |

2023 | | 351,574 | | 4.5% | |

2024 | | 781,382 | | 10.0% | |

2025 | | 509,607 | | 6.6% | |

Thereafter (2) | | 5,455,634 | | 70.1% | |

| | 7,782,744 | | 100.0% | |

| (1) | Percentages are determined based upon total square footage. |

| (2) | Includes 1,536,276 square feet of vacancies at our operating properties and 111,469 square feet of vacancies at our redevelopment property as of September 30, 2021. We define redevelopment properties as properties being developed, redeveloped or where redevelopment is complete, but are in lease-up and that are not stabilized. |

(dollars & square feet in 000's) | | As of September 30, 2021 (a) | | |||||||||

| | # of | | | | | % of | | Square | | % of | |

State |

| Properties |

| Investment |

| Portfolio |

| Feet |

| Portfolio |

| |

| | | | | | | | | | | | |

Colorado | | 6 | | $ | 542,006 | | 40.3% | | 2,625 | | 33.7% | |

Texas | | 9 | | | 335,206 | | 24.9% | | 2,421 | | 31.1% | |

Georgia | | 2 | | | 154,380 | | 11.4% | | 782 | | 10.1% | |

Minnesota | | 3 | | | 124,433 | | 9.3% | | 758 | | 9.8% | |

Virginia | | 3 | | | 67,790 | | 5.0% | | 548 | | 7.0% | |

Florida | | 1 | | | 67,962 | | 5.1% | | 213 | | 2.7% | |

Illinois | | 2 | | | 45,118 | | 3.4% | | 372 | | 4.8% | |

North Carolina | | 1 | | | 7,797 | | 0.6% | | 64 | | 0.8% | |

Total | | 27 | | $ | 1,344,692 | | 100.0% | | 7,783 | | 100.0% | |

| (a) | Includes investment in our redevelopment property. We define redevelopment properties as properties being developed, redeveloped or where redevelopment is complete, but are in lease-up and that are not stabilized. |

-12-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule E

Portfolio and Other Supplementary Information

(Unaudited & Approximated)

Recurring Capital Expenditures

| | | | | Nine Months | | |||||||

(in thousands) | | For the Three Months Ended | | Ended | | ||||||||

|

| 31-Mar-21 |

| 30-Jun-21 |

| 30-Sep-21 |

| 30-Sep-21 | | ||||

Tenant improvements | | $ | 4,491 | | $ | 4,277 | | $ | 3,952 | | $ | 12,720 | |

Deferred leasing costs | | | 2,597 | | | 1,922 | | | 2,371 | | | 6,890 | |

Non-investment capex | | | 5,336 | | | 3,793 | | | 4,528 | | | 13,657 | |

| | $ | 12,424 | | $ | 9,992 | | $ | 10,851 | | $ | 33,267 | |

| | | | | | |||||||||||

| | For the Three Months Ended | | Year Ended | | |||||||||||

|

| 31-Mar-20 |

| 30-Jun-20 |

| 30-Sep-20 |

| 31-Dec-20 |

| 31-Dec-20 | | |||||

Tenant improvements | | $ | 10,716 | | $ | 13,531 | | $ | 8,022 | | $ | 837 | | $ | 33,106 | |

Deferred leasing costs | | | 2,730 | | | 603 | | | 2,033 | | | 7,432 | | | 12,798 | |

Non-investment capex | | | 4,527 | | | 6,581 | | | 6,373 | | | 6,105 | | | 23,586 | |

| | $ | 17,973 | | $ | 20,715 | | $ | 16,428 | | $ | 14,374 | | $ | 69,490 | |

Square foot & leased percentages | | September 30, | | December 31, | |

|

| 2021 |

| 2020 |

|

Operating Properties: | | | | | |

Number of properties | | 26 | | 32 | |

Square feet | | 7,671,275 | | 9,331,489 | |

Leased percentage | | 80.0% | | 85.0% | |

| | | | | |

Redevelopment Properties (a): | | | | | |

Number of properties | | 1 | | 2 | |

Square feet | | 111,469 | | 324,651 | |

Leased percentage | | 0.0% | | 48.0% | |

| | | | | |

Total Owned Properties: | | | | | |

Number of properties | | 27 | | 34 | |

Square feet | | 7,782,744 | | 9,656,140 | |

Leased percentage | | 78.8% | | 83.8% | |

| | | | | |

Managed Properties - Single Asset REITs (SARs): | | | | | |

Number of properties | | 2 | | 2 | |

Square feet | | 348,545 | | 348,545 | |

| | | | | |

Total Operating, Redevelopment and Managed Properties: | | | | | |

Number of properties | | 29 | | 36 | |

Square feet | | 8,131,289 | | 10,004,685 | |

| (a) | We define redevelopment properties as properties being developed, redeveloped or where redevelopment is complete, but are in lease-up and that are not stabilized. |

-13-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule F

Percentage of Leased Space

(Unaudited & Estimated)

| | | | | | | | | | Second | | | | Third | |

| | | | | | | | % Leased (1) | | Quarter | | % Leased (1) | | Quarter | |

| | | | | | | | as of | | Average % | | as of | | Average % | |

|

| Property Name |

| Location |

| Square Feet |

| 30-Jun-21 |

| Leased (2) |

| 30-Sep-21 |

| Leased (2) |

|

| | | | | | | | | | | | | | | |

1 | | FOREST PARK | | Charlotte, NC | | 64,198 | | 78.4% | | 78.4% | | 78.4% | | 78.4% | |

2 | | MEADOW POINT | | Chantilly, VA | | 138,537 | | 91.1% | | 91.1% | | 100.0% | | 97.0% | |

| | TIMBERLAKE | | Chesterfield, MO | | — | | 100.0% | | 100.0% | | (4) | | (4) | |

| | TIMBERLAKE EAST | | Chesterfield, MO | | — | | 100.0% | | 100.0% | | (4) | | (4) | |

3 | | NORTHWEST POINT | | Elk Grove Village, IL | | 177,095 | | 100.0% | | 100.0% | | 100.0% | | 100.0% | |

4 | | PARK TEN | | Houston, TX | | 157,609 | | 71.7% | | 71.7% | | 72.0% | | 72.0% | |

5 | | PARK TEN PHASE II | | Houston, TX | | 156,746 | | 95.0% | | 95.0% | | 95.0% | | 95.0% | |

6 | | GREENWOOD PLAZA | | Englewood, CO | | 196,236 | | 100.0% | | 100.0% | | 100.0% | | 100.0% | |

7 | | ADDISON | | Addison, TX | | 289,325 | | 83.7% | | 83.7% | | 85.6% | | 85.6% | |

8 | | COLLINS CROSSING | | Richardson, TX | | 300,887 | | 84.4% | | 84.4% | | 84.4% | | 84.4% | |

9 | | INNSBROOK | | Glen Allen, VA | | 298,183 | | 57.2% | | 57.2% | | 57.2% | | 57.2% | |

| | RIVER CROSSING | | Indianapolis, IN | | — | | 100.0% | | 100.0% | | (5) | | (5) | |

10 | | LIBERTY PLAZA | | Addison, TX | | 217,191 | | 79.0% | | 79.0% | | 73.9% | | 79.3% | |

11 | | 380 INTERLOCKEN | | Broomfield, CO | | 240,359 | | 60.5% | | 60.5% | | 60.5% | | 60.5% | |

12 | | 390 INTERLOCKEN | | Broomfield, CO | | 241,512 | | 99.4% | | 99.4% | | 99.4% | | 99.4% | |

13 | | BLUE LAGOON | | Miami, FL | | 213,182 | | 73.1% | | 73.1% | | 73.6% | | 73.2% | |

14 | | ELDRIDGE GREEN | | Houston, TX | | 248,399 | | 100.0% | | 100.0% | | 100.0% | | 100.0% | |

15 | | 4807 STONECROFT (3) | | Chantilly, VA | | 111,469 | | 0.0% | | 0.0% | | 0.0% | | 0.0% | |

16 | | 121 SOUTH EIGHTH ST | | Minneapolis, MN | | 298,121 | | 91.6% | | 91.8% | | 90.7% | | 91.3% | |

17 | | 801 MARQUETTE AVE | | Minneapolis, MN | | 129,821 | | 91.8% | | 91.8% | | 91.8% | | 91.8% | |

18 | | LEGACY TENNYSON CTR | | Plano, TX | | 207,049 | | 41.1% | | 41.1% | | 41.1% | | 41.1% | |

19 | | ONE LEGACY | | Plano, TX | | 214,110 | | 56.4% | | 56.4% | | 57.9% | | 57.9% | |

20 | | 909 DAVIS | | Evanston, IL | | 195,098 | | 93.3% | | 93.3% | | 93.3% | | 93.3% | |

21 | | WESTCHASE I & II | | Houston, TX | | 629,025 | | 54.4% | | 54.4% | | 57.6% | | 55.7% | |

22 | | 1999 BROADWAY | | Denver, CO | | 680,255 | | 66.5% | | 66.5% | | 67.3% | | 67.3% | |

23 | | 999 PEACHTREE | | Atlanta, GA | | 621,946 | | 85.0% | | 84.8% | | 85.8% | | 85.5% | |

24 | | 1001 17TH STREET | | Denver, CO | | 655,420 | | 95.2% | | 95.5% | | 95.2% | | 95.2% | |

25 | | PLAZA SEVEN | | Minneapolis, MN | | 330,096 | | 85.5% | | 85.5% | | 85.5% | | 85.5% | |

26 | | PERSHING PLAZA | | Atlanta, GA | | 160,145 | | 12.4% | | 70.1% | | 76.6% | | 33.8% | |

27 | | 600 17TH STREET | | Denver, CO | | 610,730 | | 84.9% | | 85.5% | | 85.8% | | 85.2% | |

| | OWNED PORTFOLIO | | | | 7,782,744 | | 78.5% | | 79.8% | | 78.8% | | 78.7% | |

| (1) | % Leased as of month's end includes all leases that expire on the last day of the quarter. |

| (2) | Average quarterly percentage is the average of the end of the month leased percentage for each of the three months during the quarter. |

| (3) | We define redevelopment properties as properties being developed, redeveloped or where redevelopment is complete, but are in lease-up and that are not stabilized. |

| (4) | Properties sold on September 23, 2021. |

| (5) | Property sold on August 31, 2021. |

-14-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule G

Largest 20 Tenants – FSP Owned Portfolio

(Unaudited & Estimated)

The following table includes the largest 20 tenants in FSP’s owned portfolio based on total square feet:

As of September 30, 2021

| | | | | | % of | |

|

| Tenant |

| Sq Ft |

| Portfolio |

|

1 | | CITGO Petroleum Corporation | | 248,399 | | 3.2% | |

2 | | Ovintiv USA Inc. | | 234,495 | | 3.0% | |

3 | | Eversheds Sutherland (US) LLP (a) | | 179,868 | | 2.3% | |

4 | | EOG Resources, Inc. | | 169,167 | | 2.2% | |

5 | | US Government | | 168,573 | | 2.2% | |

6 | | The Vail Corporation | | 164,636 | | 2.1% | |

7 | | Lennar Homes, LLC | | 155,808 | | 2.0% | |

8 | | Citicorp Credit Services, Inc | | 146,260 | | 1.9% | |

9 | | Kaiser Foundation Health Plan | | 120,979 | | 1.5% | |

10 | | Argo Data Resource Corporation | | 114,200 | | 1.5% | |

11 | | VMWare, Inc. | | 100,853 | | 1.3% | |

12 | | Deluxe Corporation | | 98,922 | | 1.3% | |

13 | | Swift, Currie, McGhee & Hiers, LLP | | 98,831 | | 1.3% | |

14 | | Ping Identity Corp. | | 89,856 | | 1.1% | |

15 | | Common Grounds, LLC (a) | | 76,984 | | 1.0% | |

16 | | Booz Allen Hamilton, Inc. | | 75,338 | | 1.0% | |

17 | | ADS Alliance Data Systems, Inc. | | 67,274 | | 0.9% | |

18 | | PricewaterhouseCoopers LLP | | 66,304 | | 0.8% | |

19 | | DirecTV, Inc. | | 66,226 | | 0.8% | |

20 | | Hall and Evans LLC | | 65,878 | | 0.8% | |

| | Total | | 2,508,851 | | 32.2% | |

| (a) | On October 22, 2021, the property that has the lease with Eversheds Sutherland (US) LLP and one lease with Common Grounds, LLC for 49,506 square feet was sold. |

-15-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule H

Reconciliation and Definitions of Funds From Operations (“FFO”) and

Adjusted Funds From Operations (“AFFO”)

A reconciliation of Net income to FFO and AFFO is shown below and a definition of FFO and AFFO is provided on Supplementary Schedule I. Management believes FFO and AFFO are used broadly throughout the real estate investment trust (REIT) industry as measurements of performance. The Company has included the National Association of Real Estate Investment Trusts (NAREIT) FFO definition as of May 17, 2016 in the table and notes that other REITs may not define FFO in accordance with the current NAREIT definition or may interpret the current NAREIT definition differently. The Company’s computation of FFO and AFFO may not be comparable to FFO or AFFO reported by other REITs or real estate companies that define FFO or AFFO differently.

Reconciliation of Net Income to FFO and AFFO: | | Three Months Ended | | Nine Months Ended | | ||||||||

| | September 30, | | September 30, | | ||||||||

(In thousands, except per share amounts) |

| 2021 |

| 2020 | | 2021 |

| 2020 |

| ||||

Net income (loss) | | $ | 4,456 | | $ | (1,679) | | $ | 14,145 | | $ | (4,825) | |

Gain on sale of properties, net | | | (8,632) | | | — | | | (29,258) | | | — | |

Equity in income from non-consolidated REITs | | | (421) | | | — | | | (421) | | | — | |

FFO from non-consolidated REITs | | | 421 | | | — | | | 421 | | | — | |

Depreciation & amortization | | | 18,861 | | | 21,989 | | | 62,340 | | | 66,424 | |

NAREIT FFO | | | 14,685 | | | 20,310 | | | 47,227 | | | 61,599 | |

Lease Acquisition costs | | | 112 | | | 136 | | | 297 | | | 333 | |

Funds From Operations (FFO) | | $ | 14,797 | | $ | 20,446 | | $ | 47,524 | | $ | 61,932 | |

| | | | | | | | | | | | | |

Funds From Operations (FFO) | | $ | 14,797 | | $ | 20,446 | | $ | 47,524 | | $ | 61,932 | |

Reverse FFO from non-consolidated REITs | | | (421) | | | — | | | (421) | | | — | |

Distributions from non-consolidated REITs | | | 421 | | | — | | | 421 | | | — | |

Amortization of deferred financing costs | | | 854 | | | 727 | | | 2,414 | | | 2,201 | |

Shares issued as compensation | | | — | | | — | | | 338 | | | 337 | |

Straight-line rent | | | (245) | | | (1,293) | | | (3,190) | | | (2,636) | |

Tenant improvements | | | (3,952) | | | (8,022) | | | (12,720) | | | (32,269) | |

Leasing commissions | | | (2,371) | | | (2,033) | | | (6,890) | | | (5,366) | |

Non-investment capex | | | (4,528) | | | (6,373) | | | (13,657) | | | (17,481) | |

Adjusted Funds From Operations (AFFO) | | $ | 4,555 | | $ | 3,452 | | $ | 13,819 | | $ | 6,718 | |

| | | | | | | | | | | | | |

Per Share Data | | | | | | | | | | | | | |

EPS | | $ | 0.04 | | $ | (0.02) | | $ | 0.13 | | $ | (0.04) | |

FFO | | $ | 0.14 | | $ | 0.19 | | $ | 0.44 | | $ | 0.58 | |

AFFO | | $ | 0.04 | | $ | 0.03 | | $ | 0.13 | | $ | 0.06 | |

| | | | | | | | | | | | | |

Weighted average shares (basic and diluted) | | | 106,905 | | | 107,328 | | | 107,196 | | | 107,295 | |

-16-

Funds From Operations (“FFO”)

The Company evaluates performance based on Funds From Operations, which we refer to as FFO, as management believes that FFO represents the most accurate measure of activity and is the basis for distributions paid to equity holders. The Company defines FFO as net income or loss (computed in accordance with GAAP), excluding gains (or losses) from sales of property, hedge ineffectiveness, acquisition costs of newly acquired properties that are not capitalized and lease acquisition costs that are not capitalized plus depreciation and amortization, including amortization of acquired above and below market lease intangibles and impairment charges on mortgage loans, properties or investments in non-consolidated REITs, and after adjustments to exclude equity in income or losses from, and, to include the proportionate share of FFO from, non-consolidated REITs.

FFO should not be considered as an alternative to net income or loss (determined in accordance with GAAP), nor as an indicator of the Company’s financial performance, nor as an alternative to cash flows from operating activities (determined in accordance with GAAP), nor as a measure of the Company’s liquidity, nor is it necessarily indicative of sufficient cash flow to fund all of the Company’s needs.

Other real estate companies and the National Association of Real Estate Investment Trusts, or NAREIT, may define this term in a different manner. We have included the NAREIT FFO as of May 17, 2016 in the table and note that other REITs may not define FFO in accordance with the current NAREIT definition or may interpret the current NAREIT definition differently than we do.

We believe that in order to facilitate a clear understanding of the results of the Company, FFO should be examined in connection with net income or loss and cash flows from operating, investing and financing activities in the consolidated financial statements.

Adjusted Funds From Operations (“AFFO”)

The Company also evaluates performance based on Adjusted Funds From Operations, which we refer to as AFFO. The Company defines AFFO as (1) FFO, (2) excluding our proportionate share of FFO and including distributions received, from non-consolidated REITs, (3) excluding the effect of straight-line rent, (4) plus the amortization of deferred financing costs, (5) plus the value of shares issued as compensation and (6) less recurring capital expenditures that are generally for maintenance of properties, which we call non-investment capex or are second generation capital expenditures. Second generation costs include re-tenanting space after a tenant vacates, which include tenant improvements and leasing commissions.

We exclude development/redevelopment activities, capital expenditures planned at acquisition and costs to reposition a property. We also exclude first generation leasing costs, which are generally to fill vacant space in properties we acquire or were planned for at acquisition.

AFFO should not be considered as an alternative to net income or loss (determined in accordance with GAAP), nor as an indicator of the Company’s financial performance, nor as an alternative to cash flows from operating activities (determined in accordance with GAAP), nor as a measure of the Company’s liquidity, nor is it necessarily indicative of sufficient cash flow to fund all of the Company’s needs. Other real estate companies may define this term in a different manner. We believe that in order to facilitate a clear understanding of the results of the Company, AFFO should be examined in connection with net income or loss and cash flows from operating, investing and financing activities in the consolidated financial statements.

-17-

Franklin Street Properties Corp. Earnings Release

Supplementary Schedule I

Reconciliation and Definition of Sequential Same Store results to property Net Operating Income (NOI) and Net Income

Net Operating Income (“NOI”)

The Company provides property performance based on Net Operating Income, which we refer to as NOI. Management believes that investors are interested in this information. NOI is a non-GAAP financial measure that the Company defines as net income or loss (the most directly comparable GAAP financial measure) plus general and administrative expenses, depreciation and amortization, including amortization of acquired above and below market lease intangibles and impairment charges, interest expense, less equity in earnings of nonconsolidated REITs, interest income, management fee income, hedge ineffectiveness, gains or losses on extinguishment of debt, gains or losses on the sale of assets and excludes non-property specific income and expenses. The information presented includes footnotes and the data is shown by region with properties owned in the periods presented, which we call Sequential Same Store. The comparative Sequential Same Store results include properties held for the periods presented and exclude our redevelopment properties. We also exclude properties that have been placed in service, but that do not have operating activity for all periods presented, dispositions and significant nonrecurring income such as bankruptcy settlements and lease termination fees. NOI, as defined by the Company, may not be comparable to NOI reported by other REITs that define NOI differently. NOI should not be considered an alternative to net income or loss as an indication of our performance or to cash flows as a measure of the Company’s liquidity or its ability to make distributions. The calculations of NOI and Sequential Same Store are shown in the following table:

| | Rentable | | | | | | | | | | | |

|

| | Square Feet | | Three Months Ended | | Three Months Ended | | Inc | | % |

| |||

(in thousands) |

| or RSF |

| 30-Sep-21 |

| 30-Jun-21 |

| (Dec) |

| Change |

| |||

Region | | | | | | | | | | | | | | |

East |

| 437 |

| $ | 642 |

| $ | 685 | | $ | (43) |

| (6.3) | % |

MidWest |

| 1,000 | |

| 3,470 | |

| 3,184 | |

| 286 |

| 9.0 | % |

South |

| 3,202 | |

| 8,482 | |

| 9,207 | |

| (725) |

| (7.9) | % |

West |

| 2,625 | |

| 10,144 | |

| 9,901 | |

| 243 |

| 2.5 | % |

Property NOI* from Operating Properties |

| 7,264 | |

| 22,738 | |

| 22,977 | |

| (239) |

| (1.0) | % |

Dispositions and Redevelopment Properties (a) | | 519 | |

| 2,625 | |

| 5,023 | |

| (2,398) |

| (8.4) | % |

NOI* | | 7,783 |

| $ | 25,363 |

| $ | 28,000 | | $ | (2,637) |

| (9.4) | % |

| | | | | | | | | | | | | | |

Sequential Same Store | | |

| $ | 22,738 |

| $ | 22,977 | | $ | (239) |

| (1.0) | % |

| | | | | | | | | | | | | | |

Less Nonrecurring | | | | | | | | | | | | | | |

Items in NOI* (b) | | | |

| 281 | |

| 34 | |

| 247 |

| (1.1) | % |

| | | | | | | | | | | | | | |

Comparative | | | | | | | | | | | | | | |

Sequential Same Store | | |

| $ | 22,457 |

| $ | 22,943 | | $ | (486) |

| (2.1) | % |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

-18-

| | | | | | | | | | | | | | |

| | | | Three Months Ended | | Three Months Ended | | | | | | | ||

Reconciliation to Net income | | | | 30-Sep-21 | | 30-Jun-21 | | | | | | | ||

Net income | | |

| $ | 4,456 |

| $ | 16,149 | | | | | | |

Add (deduct): | | | | | | | | | | | | | | |

Loss on extinguishment of debt | | | |

| 236 | |

| 167 | | | | | | |

Gain on sale of properties, net | | | |

| (8,632) | |

| (20,626) | | | | | | |

Management fee income | | | |

| (380) | |

| (403) | | | | | | |

Depreciation and amortization | | | |

| 18,861 | |

| 19,136 | | | | | | |

Amortization of above/below market leases | | | |

| — | |

| (6) | | | | | | |

General and administrative | | | |

| 3,749 | |

| 3,962 | | | | | | |

Interest expense | | | |

| 7,928 | |

| 10,054 | | | | | | |

Interest income | | | |

| (404) | |

| (399) | | | | | | |

Equity in (income) loss of non-consolidated REITs | | | |

| (421) | |

| — | | | | | | |

Non-property specific items, net | | | |

| (30) | |

| (34) | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

NOI* | | |

| $ | 25,363 |

| $ | 28,000 | | | | | | |

| (a) | We define redevelopment properties as properties being developed, redeveloped or where redevelopment is complete, but are in lease-up and that are not stabilized. We also include properties that have been placed in service, but that do not have operating activity for all periods presented. |

| (b) | Nonrecurring Items in NOI include proceeds from bankruptcies, lease termination fees or other significant nonrecurring income or expenses, which may affect comparability. |

*Excludes NOI from investments in and interest income from secured loans to non-consolidated REITs.