Exhibit 99.1

Lakeland Fire + Safety Reports Fiscal Second Quarter 2026 Financial Results

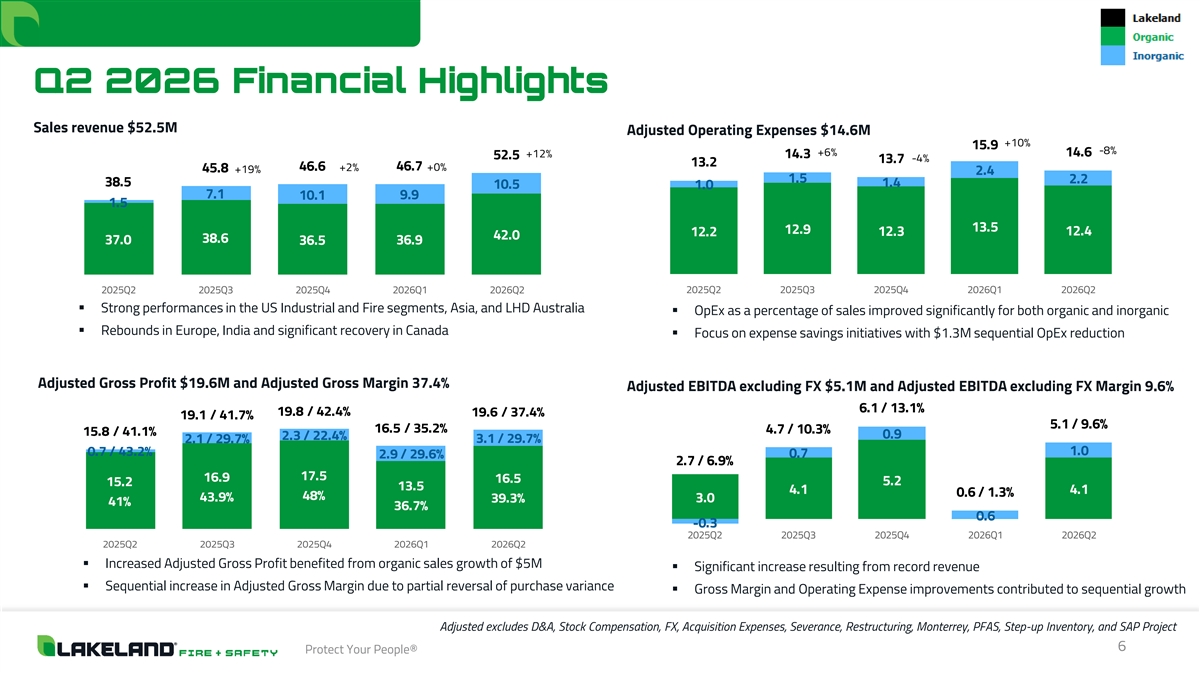

Q2’26 Net Sales Increased 36% to a Record $52.5 Million Led by a 113% Increase in Fire Services Products, Representing 49% of Total Revenue

U.S. Net Sales Increased 78% to $22.1 Million & Europe Net Sales Increased 113% to $15.1 Million

Sequential Gross Margin Improves 240 Basis Points to 35.9% and Lower Operating Expenses Drive Positive Net Income of $0.8 Million and Adjusted EBITDA Excluding FX to $5.1 Million

Updates Previously Issued FY 2026 Revenue and Adjusted EBITDA Excluding FX Guidance Range to Reflect Continued Uncertainty with Global Tariff Environment

Management to Host Conference Call Today at 4:30 p.m. Eastern Time

HUNTSVILLE, AL – September 9, 2025 - Lakeland Industries, Inc. (“Lakeland Fire + Safety” or “Lakeland”) (NASDAQ: LAKE), a leading global manufacturer of protective clothing and apparel for industry, healthcare and first responders, has reported its financial and operational results for its fiscal second quarter ended July 31, 2025.

Key Fiscal 2026 Second Quarter and Subsequent Financial and Operational Highlights

| Q2 Comparison | 1H Comparison | |||||||||||||||||||||||||||||||

| $ in millions | FY Q2’26 |

FY Q2’25 |

$ Change YoY |

% Change YoY |

1H FY2026 |

1H FY2025 |

$ Change YoY |

% Change YoY |

||||||||||||||||||||||||

| Net Sales |

$ | 52.5 | $ | 38.5 | $ | 14.0 | 36 | % | $ | 99.2 | $ | 74.8 | $ | 24.4 | 33 | % | ||||||||||||||||

| Gross Profit |

$ | 18.8 | $ | 15.2 | $ | 3.6 | 24 | % | $ | 34.5 | $ | 31.4 | $ | 3.1 | 10 | % | ||||||||||||||||

| Gross Margin |

35.9 | % | 39.6 | % | — | (370 | )BPS | 34.8 | % | 42.0 | % | — | (686 | )BPS | ||||||||||||||||||

| Net Income (Loss) |

$ | 0.8 | ($ | 1.4 | ) | $ | 2.2 | 157 | % | ($ | 3.1 | ) | $ | 0.3 | ($ | 3.4 | ) | (1,133 | %) | |||||||||||||

| Adjusted EBITDA |

$ | 5.0 | $ | 1.8 | $ | 3.2 | 176 | % | $ | 4.8 | $ | 5.7 | ($ | 0.9 | ) | (16 | %) | |||||||||||||||

| Adjusted EBITDA ex. FX |

$ | 5.1 | $ | 2.7 | $ | 2.4 | 89 | % | $ | 5.7 | $ | 6.5 | ($ | 0.8 | ) | -12 | % | |||||||||||||||

Management Commentary

“Against a continued uncertain global tariff environment, the Lakeland team delivered record fiscal second quarter 2026 net sales revenue growth of 36% to $52.5 million, led by a 113% increase in Fire Services revenue and sequential improvement with our product margins from both our organic and inorganic segments,” said Jim Jenkins, President, Chief Executive Officer and Executive Chairman. “Strong

performances in our North American Industrial and Fire segments, Asia, and LHD Australia, along with rebounds in Europe, India and a significant recovery in Canada, were partially offset by continued softness in Latin America. A large $3.1 million boot order through Jolly Scarpe also contributed materially to the quarter. While second quarter revenue approached internal expectations, shortfalls in Latin America, due mainly to continued delays in purchasing decisions due to tariff uncertainty and currency issues, impacted results. We expect a material recovery in Latin America in the fourth quarter, but not sufficient to meet our original performance expectations. To that end, we are focused on expanding sales opportunities in Latin America, including Fire Services, and expect a resumption of growth in the back half of FY26.

“Additional factors affecting revenue in the second quarter included shortfalls at Eagle and LHD Germany due to ongoing delays in governmental funding for fire services tenders, as well as Pacific Helmets resulting from updates to product offerings and production issues. Eagle and LHD are well-positioned to participate in upcoming meaningful tenders, and Pacific Helmet is now on track with production improvements. We expect to realize benefits in the following quarters as the Pacific traditional fire helmet, featuring the innovative, highly comfortable, and safety-enhancing “Halo Flex” suspension, continues to gain traction in the U.S.

“Looking ahead, we are focused on navigating the continued challenges from tariff uncertainties, growing top-line revenue in our fire services and industrial verticals, and implementing operating and manufacturing efficiencies to achieve higher margins and improved free cash flow. We have recently initiated a series of targeted actions to optimize inventory levels across specific categories. Our immediate priorities include U.S. Critical Environment, Jolly, LHD Australia, and Veridian, where we see the greatest opportunity to align balances with demand and improve efficiency. Additional inventory optimization initiatives are planned in the second half of the fiscal year in U.S. High Performance and oil and gas turnaround categories, which should further support revenue growth and improved cash flow.

“While these inventory optimization initiatives have only just begun, we expect to see measurable progress by year-end. We believe that our proactive approach to inventory management, combined with the upcoming tender cycle, will position us for stronger execution in the back half of FY26 and build momentum heading into FY27. In parallel, U.S. and EMEA Fire Services tender cycles are expected to restart in late FY26 and into the first quarter of FY27. This renewed tender activity is expected to increase demand for fire services in the U.S. and contribute to improved performance at Eagle and LHD Germany.

“Looking further ahead, Lakeland is incredibly well-positioned to capitalize on long-term industry tailwinds and structural shifts in global safety standards. Over the next three to five years, we expect to unlock substantial value through our ongoing transition to higher-margin product and service categories, accelerated innovation, and enhanced customer engagement across both developed and emerging markets. Our expanded commercial and operational footprint, combined with a relentless focus on efficiency and agility, supports our ambition to become the most trusted name in high-performance protective gear globally. We see a clear path to scaling our business profitably, achieving record levels of revenue, margin, and free cash flow, while deepening our role as a mission-critical partner for safety professionals worldwide. We look forward to sharing upcoming milestones in the weeks and months ahead and at the upcoming Lake Street 9th Annual Best Ideas Growth (BIG9) Conference and the D.A. Davidson 24th Annual Diversified Industrials & Services Conference this month,” concluded Mr. Jenkins.

Fiscal 2026 Second Quarter Financial Highlights

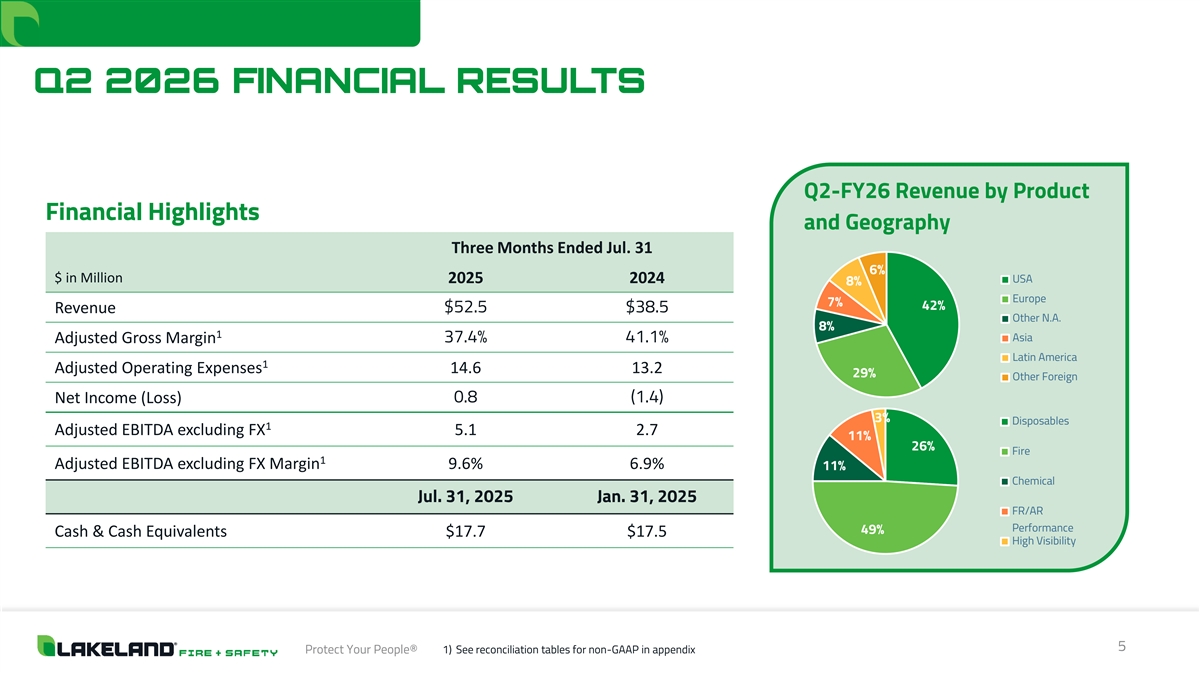

| • | Net sales were a record $52.5 million for the second quarter of fiscal 2026, an increase of $14.0 million or 36% compared to $38.5 million for the second quarter of fiscal 2025, driven by a 113% increase in Fire Services. |

| • | Organic revenue(1) increased 14% to $42.0 million for the second quarter of fiscal 2026, compared to $37.0 million for the second quarter of fiscal 2025, due to strong growth in the U.S., Canada, India and Jolly, partially offset by weakness in Latin America, Mexico and Pacific Helmets. |

| • | Organic gross margin(1) decreased by 0.9 margin points to 38.6% for the second quarter of fiscal 2026, compared to 41.0% for the second quarter of fiscal 2025, due primarily to higher sales with lower margins in Jolly, and lower sales and lower margins in Latin America. |

| • | Sales of the Fire Services product line were $25.6 million for the second quarter of fiscal 2026, an increase of $13.6 million or 113% compared to $12.0 million for the second quarter of fiscal 2025. |

| • | Fire segment as a percentage of revenue grew to 49%. |

| • | U.S. net sales were $22.1 million for the second quarter of fiscal 2026, an increase of $9.7 million or 78% compared to $12.4 million for the second quarter of fiscal 2025. |

| • | Europe net sales, including Eagle, Jolly and LHD, were $15.1 million for the second quarter of fiscal 2026, an increase of $8.0 million or 113% compared to $7.1 million for the second quarter of fiscal 2025. |

| • | LATAM net sales were $4.3 million for the second quarter of fiscal 2026, a decrease of $3.1 million or 42% compared to $7.4 million for the second quarter of fiscal 2025. |

| • | Asia net sales were $3.7 million for the second quarter of fiscal 2026, an increase of $0.2 million or 6% compared to $3.5 million for the second quarter of fiscal 2025. |

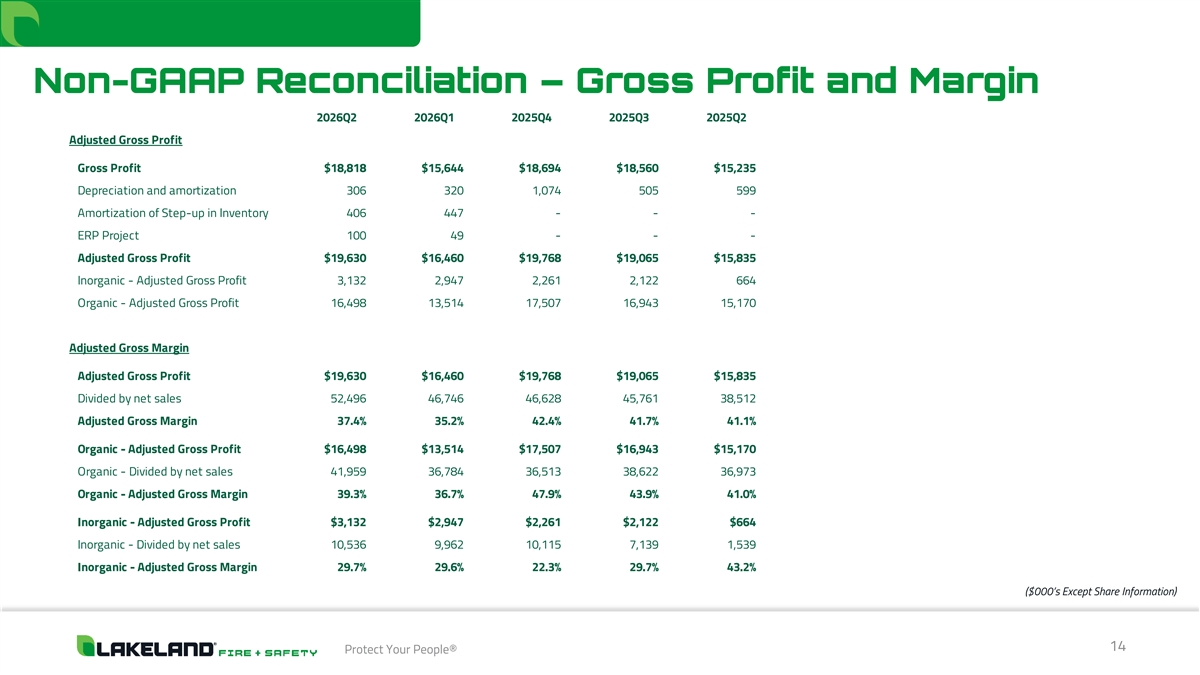

| • | Gross profit for the second quarter of fiscal 2026 was $18.8 million, an increase of $3.6 million, or 24%, compared to $15.2 million for the second quarter of fiscal 2025. |

| • | Adjusted EBITDA excluding FX(2) for the second quarter of fiscal year 2026 was $5.1 million, an increase of $2.4 million, or 89%, compared with $2.7 million for the second quarter of fiscal 2025. |

| • | Adjusted EBITDA excluding FX margin in the second quarter of fiscal year 2026 was 9.6%, an increase of 270 basis points from 6.9% in the second quarter of fiscal 2025 and an increase of 830 basis points from 1.3% in the first quarter of fiscal 2026. |

Fiscal 2026 Second Quarter and Subsequent Operational Highlights

| • | Completed a $6.1 million sale and partial leaseback of its Decatur, Alabama, warehouse property to an unrelated party, in connection with capital reallocation initiatives, strengthening the balance sheet and providing financial flexibility for future growth. |

| • | Shipment of a $3.1 million order through its Jolly Scarpe brand for fire intervention boots from the Italian Ministry of the Interior—Firefighters Department, as part of a previously awarded four-year supply contract. |

| • | Announced the closures of its warehouse facility in Hull, England and its Veridian manufacturing facility in Quitman, Arkansas, part of Lakeland’s broader operational consolidation strategy aimed at enhancing efficiency and reducing costs. |

| • | Achieved significant reduction in the run rate of operational expenses as part of an anticipated $4 million OpEx reduction |

| • | Added to the broad-market Russell 3000® and Russell 2000® Indices. |

| • | Attended the 15th Annual ROTH London Conference. |

| • | Attending the Lake Street 9th Annual Best Ideas Growth (BIG9) Conference and the D.A. Davidson 24th Annual Diversified Industrials & Services Conference in September 2025. |

| (1) | Organic revenue and organic gross margin are non-GAAP financial measures representing total revenue and total gross margin, each excluding the effects of recent acquisitions, which management uses to assess the growth of its legacy business. Reconciliations are provided in the tables of this press release. |

| (2) | Adjusted EBITDA and Adjusted EBITDA excluding FX are non-GAAP financial measures. Reconciliations are provided in the tables of this press release. |

Fiscal 2026 Second Quarter Financial Results

Net sales were $52.5 million for the second quarter of fiscal 2026, an increase of $14.0 million or 36% compared to $38.5 million for the second quarter of fiscal 2025. Sales from our recent acquisitions accounted for $9.0 million of the increase, while organic sales increased $5.0 million, or 14%, over the prior year. Sales of the Fire Services product line increased by $13.6 million year-over-year, driven by $5.2 million in sales from Veridian, and a net increase in sales of $7.3 million from LHD and Jolly, as well as organic Fire Services growth of $1.1 million.

On a consolidated basis, for the second quarter of fiscal year 2026, domestic sales were $22.1 million, or 42% of total revenues, and international sales were $30.4 million, or 58% of total revenues. This compares with domestic sales of $12.4 million, or 32% of the total, and international sales of $26.1 million, or 68%, in the second quarter of fiscal year 2025, as our recent Veridian acquisition contributed to increased U.S. revenue in the current quarter.

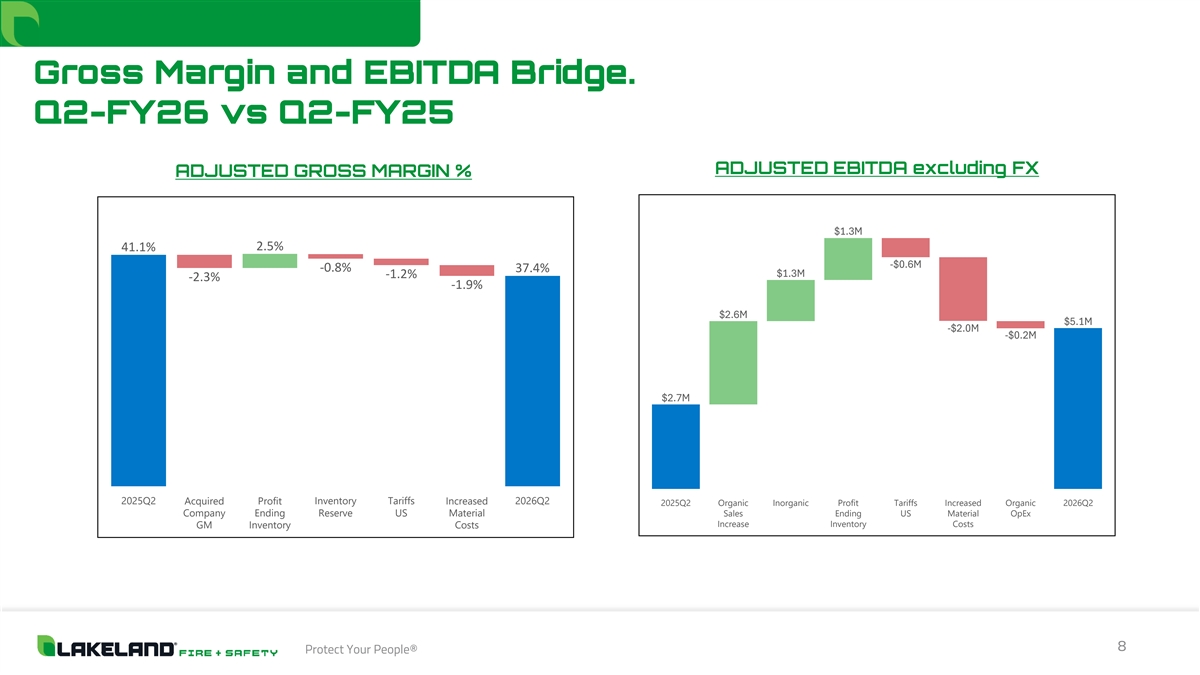

Gross profit for the second quarter of fiscal 2026 was $18.8 million, an increase of $3.6 million, or 24%, compared to $15.2 million for the second quarter of fiscal 2025. Gross profit as a percentage of net sales decreased to 35.9% for the second quarter of fiscal 2026 from 39.6% for the second quarter of fiscal 2025. The gross margin percentage decreased in the second quarter of fiscal 2026 due to increased supply chain costs and tariffs, higher inbound freight expenses, and amortization of the step-up in the basis of acquired inventory. Margins in the acquired businesses were impacted by increased material costs and amortization of the write-up in inventory as part of purchase accounting. Organic gross margin percentage decreased to 38.6% from 39.5% for the second quarter of fiscal 2026, primarily due to increased sales in lower-margin regions, partially offset by a lower profit in ending inventory.

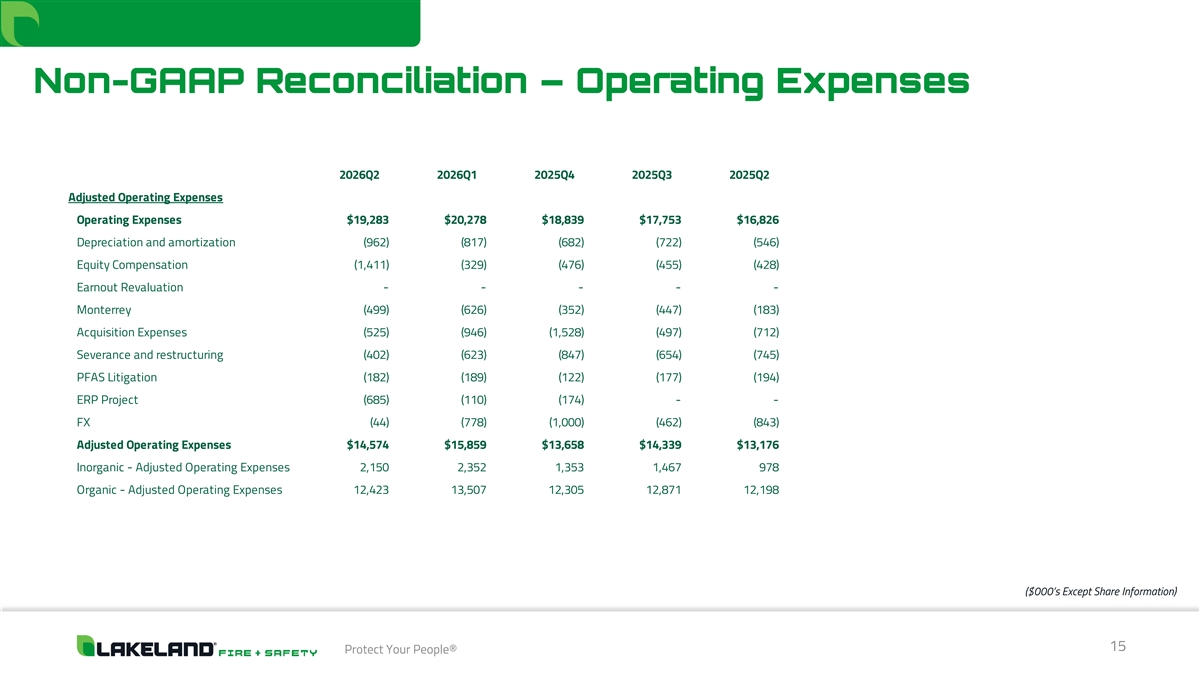

Operating expenses increased by $2.5 million, or 15%, from $16.8 million for the second quarter of fiscal 2025 to $19.3 million for the second quarter of fiscal 2026. Operating expenses increased due to the acquisitions of Veridian and LHD, which added $1.6 million to operating expenses, as well as higher equity compensation and depreciation and amortization expenses. These increases were offset by reductions in acquisition expenses, restructuring costs, and professional fees. Adjusted operating expenses excluding FX increased by $1.4 million, primarily due to acquired companies’ operating expenses, partially offset by lower professional fees and cost reduction initiatives. Operating loss was $4.0 million for the second quarter of fiscal 2026, compared to an operating loss of $1.6 million for the second quarter of fiscal 2025, primarily due to the impairment of the Monterrey, Mexico facility lease of $3.6 million and the aforementioned impacts. Operating margins were (7.6%) for the second quarter of fiscal 2026, as compared to (4.1%) for the second quarter of fiscal 2025.

Net income was $0.8 million, or $0.08 per diluted earnings per share, for the second quarter of fiscal 2026, compared to a net loss of ($1.4) million, or ($0.19) per diluted earnings per share, for the second quarter of fiscal 2025.

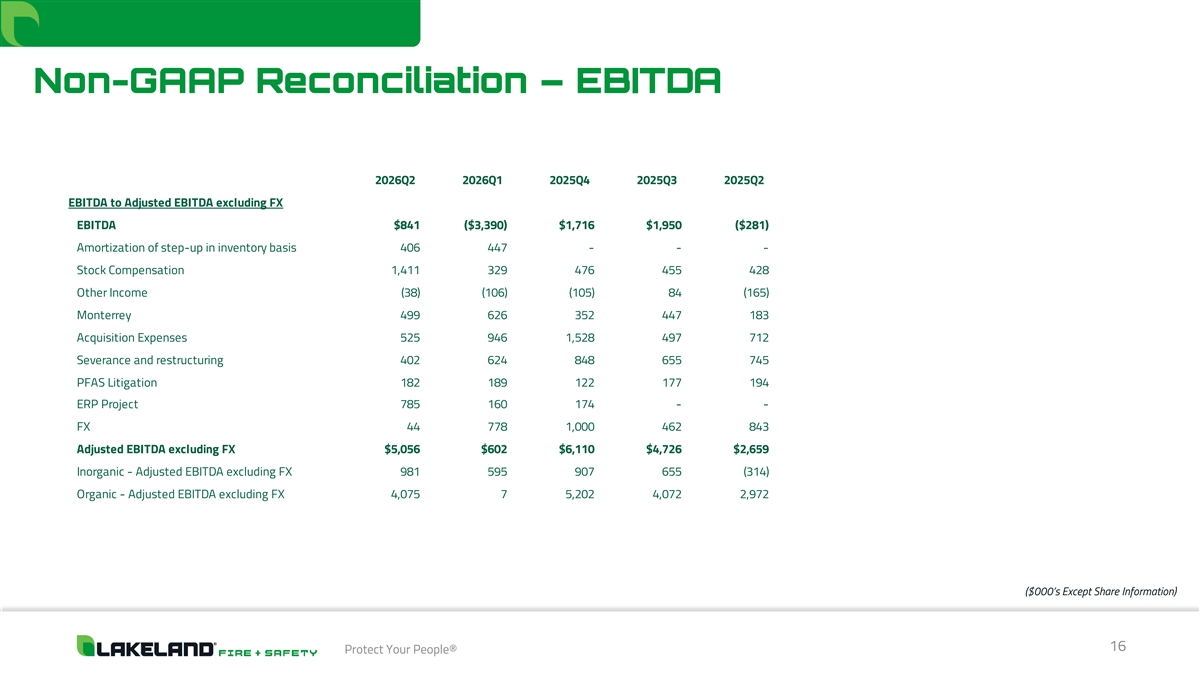

Adjusted EBITDA excluding FX for the second quarter of fiscal year 2026 was $5.1 million, an increase of $2.4 million, or 89%, compared with $2.7 million for the second quarter of fiscal year 2025. The increase was driven by strong performances in North America and reductions in operating expenses, partially offset by lower sales in the higher margin LATAM region.

Adjusted EBITDA excluding FX margin in the second quarter of fiscal year 2026 was 9.6%, an increase of 270 basis points from 6.9% in the second quarter of fiscal 2025 and an increase of 830 basis points from 1.3% in the first quarter of fiscal 2026.

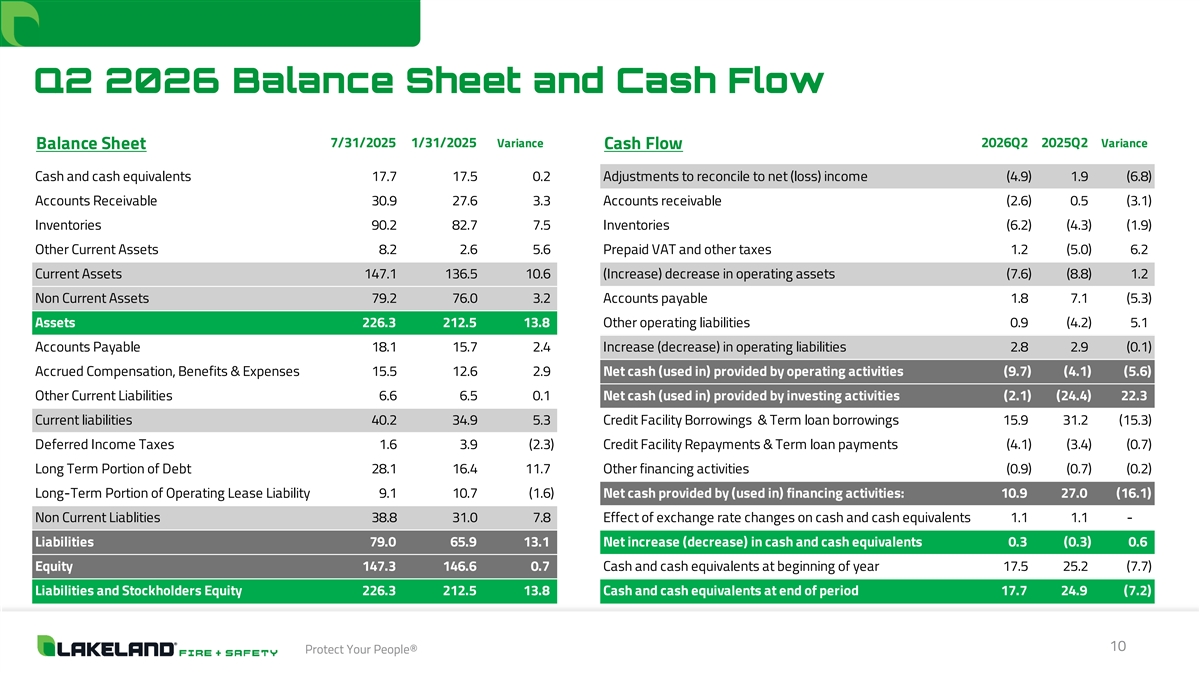

Cash and cash equivalents totaled $17.7 million as of July 31, 2025, and working capital was approximately $106.9 million. Cash and cash equivalents increased by $0.3 million and working capital increased by $4.3 million from January 31, 2025, due primarily to increases in raw materials and finished goods inventory.

As of July 31, 2025, we had borrowings of $24.9 million outstanding under the revolving credit facility, with an additional $15.1 million of available credit under the Loan Agreement. Following the Q2 quarter-end, we sold our Decatur, Alabama, property for $6.1 million, less customary commissions and closing fees, and applied 100% of the proceeds to repay our revolving credit facility.

Net cash used in operating activities was $9.7 million in the six months ended July 31, 2025, compared to $4.1 million in the six months ended July 31, 2024. The increase was driven by an increase in net loss of $3.4 million and changes in non-cash charges of $3.3 million, offset by a decrease in working capital of $1.1 million.

The Company’s quarterly dividend of $0.03 per share was paid on August 22, 2025, to stockholders of record as of August 15, 2025.

Roger Shannon, Lakeland’s Chief Financial Officer, added, “Strong performance in our U.S. and Canadian Fire Services and Industrial divisions continued to support revenue growth in the fiscal second quarter. Revenue grew $14.0 million, or 36%, compared to the second quarter of fiscal year 2025. Organic revenue increased 14% to $42.0 million in the second quarter, driven by a return to growth in the U.S., Canada, Europe and Asia.

“Our second quarter consolidated gross margin decreased to 35.9% due to increased tariffs and supply chain expenses, partially offset by lower profit in ending inventory. Our margins in the acquired businesses were impacted by increased material costs and the amortization of the inventory write-up as part of the purchase accounting. This accounting treatment affected reported margins by $0.4 million. On a sequential basis, consolidated gross margin increased 240 basis points from 33.5% last quarter due primarily to an anticipated reduction in purchase price variance, partially offset by higher tariff expenses.

“Operating expenses increased by $2.5 million for the quarter, of which $1.6 million was attributable to the acquisition of Veridian and LHD, as well as equity compensation, and depreciation and amortization expenses, offset by reductions in acquisition, restructuring expenses and legal fees. On a sequential basis, operating expenses declined $1.0 million, or 5%, to $19.3 million in the fiscal second quarter from $20.3

million in the fiscal first quarter of 2026, as a result of our focused expense reduction initiatives. On an adjusted basis, operating expenses were $14.6 million in the fiscal second quarter, more accurately showcasing the decreases in both our organic and inorganic segments resulting from the new cost reduction initiatives. On a sequential basis, adjusted operating expenses decreased $1.3 million, or 8.1%.

“Adjusted EBITDA excluding FX was $5.1 million for the fiscal second quarter, an increase of $2.4 million, or 89%, compared with

$2.7 million for the second quarter of fiscal 2025, and an increase of $4.5 million, or 740%, compared with $0.6 million for the first quarter of fiscal 2026. This significant increase was the result of record revenue, sequential

margin improvement, and OpEx improvements, which drove Adjusted EBITDA excluding FX margin higher by 270 basis points to 9.6% in the most recent quarter, an increase from 6.9% in the second quarter of fiscal 2025 and 1.3% in the first quarter of

fiscal 2026.

“Our balance sheet remains strong, and we believe it will become even stronger as our $4 million in annual cost reduction initiatives progress. These actions include the previously announced closures of our warehouse facility in Hull, England, and the Veridian manufacturing facility in Quitman, Arkansas, as part of a broader operational consolidation strategy aimed at enhancing efficiency and reducing costs. The closures are expected to generate annual savings of approximately $1 million for the remainder of fiscal year 2026, supporting ongoing efforts to streamline global operations and improve profitability. Further, the $6.1 million sale and partial leaseback of the Decatur, Alabama, warehouse facility further strengthens our balance sheet and provides financial flexibility for operational enhancements. In addition to these closures and sales, we have identified and are executing further initiatives expected to yield an additional $3 million in annualized savings in the second half of fiscal 2026.

“Given the ongoing uncertainty with the global tariff environment, we are adjusting our fiscal year 2026 outlook for Adjusted EBITDA excluding FX to the $20 - $24 million range and expect fiscal year 2026 revenue to be near the lower of the $210 -$220 million range.

“We continue to actively assess the financial impact of tariffs across our sourcing and manufacturing footprint. While it is too early to fully quantify the effect, we are committed to protecting margins through pricing adjustments, operational efficiencies, and further diversification of our supply chain.

“This situation underscores the importance of the strategic actions we have already undertaken to streamline our cost base, improve flexibility, and strengthen our global operations. We remain confident in our ability to drive sustained EBITDA improvement—even amid macroeconomic headwinds,” concluded Shannon.

FY 2026 Guidance and Outlook Update

This guidance is based on our current backlog of orders and current expectations. These metrics constitute forward-looking statements and are based on current expectations and assumptions. For a discussion of factors that could cause actual results to differ materially from these metrics, see “Safe Harbor Statement Under the Private Securities Litigation Reform Act of 1995” below.

Revenue—We expect FY26 revenue to be between $210 million and $220 million. This revenue expectation includes the recently completed acquisition of Veridian.

Adjusted EBITDA excluding FX — Due to lower margins, near-term order delays, uncertainty related to tariffs and higher operating expenses, we expect FY 2026 adjusted EBITDA, excluding any material negative impact from foreign exchange, to be in the range of $20 million to $24 million.(1)

(1) Excluding revenue, the Company does not provide guidance on a GAAP basis as certain items that impact adjusted EBITDA, such as equity compensation, foreign exchange gains or losses, acquisition expenses and employee separation expenses, which may be significant, are outside the Company’s control and/or cannot be reasonably predicted. Please see the “Reconciliation of GAAP Results to Non-GAAP Results” and the related footnotes at the end of this press release for detailed information on calculating non-GAAP measures. See the non-GAAP financial reconciliation tables in this release for a reconciliation of other non-GAAP financial measures.

Fiscal Second Quarter 2026 Financial Results Conference Call

Lakeland President, Chief Executive Officer and Executive Chairman Jim Jenkins and Chief Financial Officer Roger Shannon will host the conference call, followed by a question-and-answer period. The conference call will be accompanied by a presentation, which can be viewed during the webcast or accessed via the investor relations section of the Company’s website here.

To access the call, please use the following information:

| Date: |

Tuesday, September 9, 2025 | |

| Time: |

4:30 p.m. Eastern Time (1:30 p.m. Pacific Time) | |

| Dial-in: |

1-877-407-9208 | |

| International Dial-in: |

1-201-493-6784 | |

| Conference Code: |

13754808 | |

| Webcast: |

Q2 2026 Financial Results Conference Call |

A telephone replay will be available commencing approximately three hours after the call and will remain available through December 9, 2025, by dialing 1-844-512-2921 from the U.S., or 1-412-317-6671 from international locations, and entering replay pin number: 13754808. The replay can also be viewed through the webcast link above, and the presentation utilized during the call will be available via the investor relations section of the Company’s website here.

LAKELAND INDUSTRIES, INC. AND SUBSIDIARIES

Operating Results ($000) (Unaudited)

Reconciliation of GAAP Results to Non-GAAP Results

| Three Months Ended July 31, |

Six Months Ended July 31, |

|||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||

| Net income (loss) to EBITDA |

||||||||||||||||

| Net income (loss) to EBITDA |

$ | 766 | ($ | 1,376 | ) | ($ | 3,147 | ) | $ | 277 | ||||||

| Interest expense |

445 | 370 | 1,028 | 542 | ||||||||||||

| Taxes (1) |

(5,215 | ) | (420 | ) | (6,413 | ) | (32 | ) | ||||||||

| Depreciation and amortization |

1,268 | 1,145 | 2,406 | 1,792 | ||||||||||||

| Impairment—Leases (2) |

3,577 | — | 3,577 | — | ||||||||||||

| EBITDA |

$ | 841 | ($ | 281 | ) | ($ | 2,550 | ) | $ | 2,580 | ||||||

| EBITDA to Adjusted EBITDA |

||||||||||||||||

| (excluding non-cash expenses) |

||||||||||||||||

| EBITDA |

$ | 841 | ($ | 281 | ) | ($ | 2,550 | ) | $ | 2,580 | ||||||

| Equity compensation (3) |

1,411 | 428 | 1,740 | 627 | ||||||||||||

| Other income (expense) (4) |

(38 | ) | (165 | ) | (144 | ) | (177 | ) | ||||||||

| Acquisition expenses (5) |

525 | 712 | 1,471 | 1,684 | ||||||||||||

| Earnout revaluation (6) |

— | — | — | (689 | ) | |||||||||||

| Severance and restructuring (7) |

402 | 745 | 1,025 | 745 | ||||||||||||

| New Monterrey, Mexico facility start-up costs (8) |

499 | 183 | 1,125 | 459 | ||||||||||||

| PFAS Litigation (9) |

182 | 194 | 371 | 441 | ||||||||||||

| ERP Project (10) |

785 | — | 944 | — | ||||||||||||

| Amortization of step-up in inventory basis (11) |

406 | — | 854 | — | ||||||||||||

| Adjusted EBITDA |

$ | 5,013 | $ | 1,816 | $ | 4,836 | $ | 5,669 | ||||||||

| Adjusted EBITDA Margin |

||||||||||||||||

| Adjusted EBITDA |

$ | 5,013 | $ | 1,816 | $ | 4,836 | $ | 5,669 | ||||||||

| Divided by net sales |

52,496 | 38,512 | 99,242 | 74,822 | ||||||||||||

| Adjusted EBITDA Margin |

9.6 | % | 4.7 | % | 4.9 | % | 7.6 | % | ||||||||

| Adjusted EBITDA to Adjusted EBITDA excluding FX |

||||||||||||||||

| Adjusted EBITDA |

$ | 5,013 | $ | 1,816 | $ | 4,836 | $ | 5,669 | ||||||||

| Currency Fluctuation |

$ | 43 | $ | 843 | $ | 822 | $ | 850 | ||||||||

| Adjusted EBITDA excluding FX |

$ | 5,056 | $ | 2,659 | $ | 5,658 | $ | 6,519 | ||||||||

| Adjusted EBITDA Margin to Adjusted EBITDA excluding FX Margin |

|

|||||||||||||||

| Adjusted EBITDA excluding FX |

$ | 5,056 | $ | 2,659 | $ | 4,836 | $ | 5,669 | ||||||||

| Divided by net sales |

52,496 | 38,512 | 99,242 | 74,822 | ||||||||||||

| Adjusted EBITDA excluding FX Margin |

9.6 | % | 6.9 | % | 4.9 | % | 7.6 | % | ||||||||

| Operating Expenses to Adjusted Operating Expenses excluding FX |

||||||||||||||||

| Operating Expenses |

$ | 19,283 | $ | 16,826 | $ | 39,561 | $ | 30,809 | ||||||||

| Depreciation and amortization |

(962 | ) | (546 | ) | (1,779 | ) | (1,008 | ) | ||||||||

| Equity compensation (3) |

(1,411 | ) | (428 | ) | (1,740 | ) | (627 | ) | ||||||||

| Acquisition expenses (5) |

(525 | ) | (712 | ) | (1,471 | ) | (1,684 | ) | ||||||||

| Earnout revaluation (6) |

— | — | — | 689 | ||||||||||||

| Severance and restructuring (7) |

(402 | ) | (745 | ) | (1,025 | ) | (745 | ) | ||||||||

| New Monterrey, Mexico facility start-up costs (8) |

(499 | ) | (183 | ) | (1,125 | ) | (459 | ) | ||||||||

| PFAS Litigation (9) |

(182 | ) | (194 | ) | (371 | ) | (441 | ) | ||||||||

| ERP Project (10) |

(685 | ) | — | (796 | ) | — | ||||||||||

| FX |

(44 | ) | (843 | ) | (822 | ) | (850 | ) | ||||||||

| Adjusted Operating Expenses excluding FX |

$ | 14,574 | $ | 13,176 | $ | 30,433 | $ | 25,685 | ||||||||

| Organic Revenue |

||||||||||||||||

| Net Sales |

$ | 52,496 | $ | 38,512 | $ | 99,242 | $ | 74,822 | ||||||||

| Revenue from previous year acquisitions |

(10,536 | ) | (1,539 | ) | (20,498 | ) | (1,539 | ) | ||||||||

| Organic Revenue |

$ | 41,959 | $ | 36,973 | $ | 78,743 | $ | 73,282 | ||||||||

| Organic Gross Margin |

||||||||||||||||

| Gross Profit |

18,818 | 15,235 | 34,462 | 31,420 | ||||||||||||

| Gross Profit from previous year acquisitions |

2,635 | 624 | 4,450 | 624 | ||||||||||||

| Organic Gross Profit |

16,183 | 14,612 | 30,012 | 30,796 | ||||||||||||

| Divided by Organic Revenue |

41,959 | 36,973 | 78,743 | 73,282 | ||||||||||||

| Organic Gross Margin |

38.6 | % | 39.5 | % | 38.1 | % | 42.0 | % |

The financial data above includes non-GAAP financial measures, including EBITDA, adjusted EBITDA, adjusted EBITDA Margin, adjusted EBITDA excluding FX, adjusted EBITDA excluding FX Margin, Adjusted Operating Expenses, organic revenue, and organic gross margin. Management excludes from EBITDA and adjusted EBITDA all expenses for interest, taxes, depreciation and amortization, and Other Income which is comprised of interest income and gains (losses) from equity method investments. For adjusted EBITDA management also excludes equity compensation, acquisition-related expenses, severance and restructuring costs, start-up costs for our Mexican operations, PFAS litigation expenses, ERP Project related costs, and earnout revaluation. This press release also discusses (i) Adjusted EBITDA margin, which is calculated by dividing Adjusted EBITDA by GAAP net sales; (ii) Adjusted EBITDA excluding FX, which is calculated by subtracting foreign currency losses from Adjusted EBITDA and (iii) Adjusted EBITDA excluding FX margin, which is calculated by dividing Adjusted EBITDA excluding FX by GAAP net sales. Management excludes from organic revenue and organic gross margin the revenues and expenses associated with acquisitions completed within the previous fiscal year.

Management excludes these items principally because such charges or benefits are not directly related to the Company’s ongoing core business operations. We use such non-GAAP measures in order to (1) make more meaningful period-to-period comparisons of the Company’s operations, both internally and externally, (2) guide management in assessing the performance of the business, internally allocating resources and making decisions in furtherance of the Company’s strategic plan, and (3) provide investors with a better understanding of how management plans and measures the business. For organic revenue and organic gross margin, management excludes the effects of acquisitions completed within the prior twelve months to understand the trends in growth and profitability in the ongoing business without such effects. The material limitations to management’s approach include the fact that the charges, benefits and expenses excluded are nonetheless charges, benefits and expenses required to be recognized under GAAP and, in some cases, consume cash which reduces the Company’s liquidity. Management compensates for these limitations primarily by reviewing GAAP results to obtain a complete picture of the Company’s performance and by including a reconciliation of non-GAAP results to GAAP results in its earnings releases. Non-GAAP financial measures are not alternatives for measures of financial performance prepared in accordance with GAAP and may be different from similarly titled non-GAAP measures presented by other companies, limiting their usefulness as comparative measures.

Additional information regarding the adjustments is provided below.

(1) Adjustments for Taxes, which consist of the tax effects of the various adjustments that we exclude from our non-GAAP measures, and adjustments related to deferred tax and discrete tax items. Including these adjustments permits more accurate comparisons of the Company’s core results with those of its competitors.

(2) The Company recorded an impairment primarily related to the right of use asset for the Monterrey, Mexico facility.

(3) Adjustments for Equity Compensation, which consist of non-cash expenses for the grant of equity awards.

(4) Adjustments for Other Income, which consists of interest income and gains/(losses) from Investments accounted for under the equity method of accounting.

(5) Adjustments for acquisition-related expenses included advisory fees, due diligence expenses and legal fees related to the Company’s acquisitions.

(6) Adjustments for the reduction of the estimated earnout payment related to the Eagle acquisition. Reduction to the accrued earnout payment reflected in operating expenses.

(7) Adjustments for accrued employee severance and restructuring costs.

(8) Adjustments for costs for our Mexican operations consist of external services and legal fees associated with a property-related dispute with the landlord of our manufacturing site in Monterrey, Mexico.

(9) Adjustment for PFAS Litigation legal fees.

(10) Adjustments for the implementation of new ERP consisted of external services and employee related expenses.

(11) Adjustments for amortization of the step-up in basis for inventory acquired related to the Company’s acquisitions.

About Lakeland Fire + Safety

Lakeland Fire + Safety manufactures and sells a comprehensive line of fire services and industrial protective clothing and accessories for the industrial and first responder markets. Our products are sold globally by our in-house sales teams, our customer service group, and authorized independent sales representatives to a strategic global network of selective fire and industrial distributors and wholesale partners. Our authorized distributors supply end users across various industries, such as integrated oil, chemical/petrochemical, automobile, transportation, steel, glass, construction, smelting, cleanroom, janitorial, pharmaceutical, and high-tech electronics manufacturers, as well as scientific, medical laboratories and the utilities industry. In addition, we supply federal, state and local governmental agencies and departments, including fire and law enforcement, airport crash rescue units, the Department of Defense, the Department of Homeland Security and the Centers for Disease Control. Internationally, we sell to a mix of end-users directly and to industrial distributors, depending on the particular country and market. In addition to the United States, sales are made into more than 50 foreign countries, the majority of which were into China, the European Economic Community (“EEC”), Canada, Chile, Argentina, Russia, Kazakhstan, Colombia, Mexico, Ecuador, India, Uruguay, Middle East, Southeast Asia, Australia, Hong Kong and New Zealand.

For more information concerning Lakeland, please visit the Company online at www.lakeland.com.

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995

This press release contains estimates, predictions, opinions, goals and other “forward-looking statements” as that phrase is defined in the Private Securities Litigation Reform Act of 1995. Such statements include, without limitation, references to the Company’s predictions or expectations of future business or financial performance as well as its goals and objectives for future operations, financial and business trends, business prospects, and management’s expectations for earnings, revenues, expenses, inventory levels, capital levels, liquidity levels, or other future financial or business performance, strategies or expectations, including without limitation our M&A strategy and tariff mitigation plans. All statements, other than statements of historical facts, which address Lakeland’s expectations of sources or uses for capital, or which express the Company’s expectation for the future with respect to financial performance or operating strategies, can be identified as forward-looking statements. Forward-looking statements involve risks, uncertainties and assumptions as described from time to time in press releases and Forms 8-K, registration statements, quarterly and annual reports and other reports and filings filed with the Securities and Exchange Commission or made by management. As a result, there can be no assurance that Lakeland’s future results will not be materially different from those described herein as “believed,” “projected,” “planned,” “intended,” “anticipated,” “can,” “estimated” or “expected,” or other words which reflect the current view of the Company with respect to future events. We caution readers that these forward-looking statements speak only as of the date hereof. With respect to our guidance for revenue and Adjusted EBITDA excluding FX, such metrics are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control of the Company and its management; actual results will vary, and those variations may be material. The Company hereby expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any such statements to reflect any change in the Company’s expectations or any change in events, conditions or circumstances on which such statement is based, except as may be required by law.

Contacts

Lakeland Fire + Safety

256-600-1390

Roger Shannon

Chief Financial Officer

Investor Relations

Chris Tyson

Executive Vice President

MZ Group - MZ North America

949-491-8235

www.mzgroup.us

LAKELAND INDUSTRIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(UNAUDITED)

($000’s except for share and per share information)

| Three Months Ended July 31, |

Six Months Ended July 31, |

|||||||||||||||

| 2025 | 2024 | 2025 | 2024 | |||||||||||||

| Net sales |

$ | 52,496 | $ | 38,512 | $ | 99,242 | $ | 74,822 | ||||||||

| Cost of goods sold |

33,678 | 23,277 | 64,780 | 43,403 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

18,818 | 15,235 | 34,462 | 31,419 | ||||||||||||

| Operating expenses |

19,283 | 16,826 | 39,561 | 30,809 | ||||||||||||

| Lease impairments |

3,577 | — | 3,577 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating (loss) income |

(4,042 | ) | (1,591 | ) | (8,676 | ) | 610 | |||||||||

| Other income, net |

38 | 165 | 144 | 177 | ||||||||||||

| Interest expense |

(445 | ) | (370 | ) | (1,028 | ) | (542 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (Loss) income before taxes |

(4,449 | ) | (1,796 | ) | (9,560 | ) | 245 | |||||||||

| Income tax benefit |

(5,215 | ) | (420 | ) | (6,413 | ) | (32 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

$ | 766 | $ | (1,376 | ) | $ | (3,147 | ) | $ | 277 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) per common share: |

||||||||||||||||

| Basic |

$ | 0.08 | $ | (0.19 | ) | $ | (0.33 | ) | $ | 0.04 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted |

$ | 0.08 | $ | (0.19 | ) | $ | (0.33 | ) | $ | 0.04 | ||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares outstanding: |

||||||||||||||||

| Basic |

9,530,082 | 7,390,873 | 9,506,604 | 7,371,358 | ||||||||||||

| Diluted |

10,093,855 | 7,390,873 | 9,506,604 | 7,648,300 | ||||||||||||

LAKELAND INDUSTRIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

(000’s except for share information)

| July 31, 2025 |

January 31, 2025 |

|||||||

| ASSETS |

||||||||

| Current assets |

||||||||

| Cash and cash equivalents |

$ | 17,749 | $ | 17,476 | ||||

| Accounts receivable, net of allowance for doubtful accounts of $1,028 and $1,237 at July 31, 2025 and January 31, 2025, respectively |

30,931 | 27,607 | ||||||

| Inventories, net |

90,202 | 82,739 | ||||||

| Prepaid VAT and other taxes |

1,869 | 2,598 | ||||||

| Assets held for sale |

1,384 | — | ||||||

| Income tax receivable and other current assets |

4,929 | 6,111 | ||||||

|

|

|

|

|

|||||

| Total current assets |

147,064 | 136,531 | ||||||

| Property and equipment, net |

13,539 | 13,948 | ||||||

| Operating leases right-of-use assets |

9,031 | 13,917 | ||||||

| Deferred tax assets |

14,232 | 6,270 | ||||||

| Other assets |

1,384 | 122 | ||||||

| Goodwill |

15,047 | 16,240 | ||||||

| Intangible assets, net |

26,007 | 25,503 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 226,304 | $ | 212,531 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities |

||||||||

| Accounts payable |

$ | 18,116 | $ | 15,742 | ||||

| Accrued compensation and benefits |

5,136 | 4,501 | ||||||

| Other accrued expenses |

10,347 | 8,130 | ||||||

| Income tax payable |

1,375 | 1,993 | ||||||

| Current portion of loans payable |

1,639 | 939 | ||||||

| Current portion of operating lease liabilities |

3,608 | 3,602 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

40,221 | 34,907 | ||||||

| Deferred income taxes |

1,578 | 3,891 | ||||||

| Loans payable – long term |

28,100 | 16,426 | ||||||

| Long-term portion of operating lease liabilities |

9,143 | 10,681 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

79,042 | 65,905 | ||||||

|

|

|

|

|

|||||

| Commitments and contingencies (Note 12) |

||||||||

| Stockholders’ equity |

||||||||

| Preferred stock, $0.01 par; authorized 1,500,000 shares (none issued) |

— | — | ||||||

| Common stock, $0.01 par; authorized 20,000,000 shares Issued 10,909,279 and 10,856,812; outstanding 9,551,071 and 9,498,604 at July 31, 2025 and January 31, 2025, respectively |

109 | 109 | ||||||

| Treasury stock, at cost; 1,358,208 shares at July 31, 2025 and January 31, 2025, respectively |

(19,979 | ) | (19,979 | ) | ||||

| Additional paid-in capital |

124,594 | 123,136 | ||||||

| Retained earnings |

46,602 | 50,320 | ||||||

| Accumulated other comprehensive loss |

(4,064 | ) | (6,960 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

147,262 | 146,626 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 226,304 | $ | 212,531 | ||||

|

|

|

|

|

|||||

LAKELAND INDUSTRIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

($000’s)

| Six Months Ended July 31, |

||||||||

| 2025 | 2024 | |||||||

| Cash flows from operating activities: |

||||||||

| Net (loss) income |

($ | 3,147 | ) | $ | 277 | |||

| Adjustments to reconcile net (loss) income to net cash (used in) operating activities |

||||||||

| Deferred income taxes |

(10,279 | ) | (355 | ) | ||||

| Depreciation and amortization |

2,406 | 1,792 | ||||||

| Lease impairments |

3,577 | — | ||||||

| Amortization of step-up in inventory basis |

854 | — | ||||||

| Stock based and restricted stock compensation |

1,740 | 627 | ||||||

| Gain on disposal of property and equipment |

(3 | ) | — | |||||

| Equity in loss of equity investment |

— | 245 | ||||||

| Change in fair value of earnout consideration |

— | (711 | ) | |||||

| Change in operating assets and liabilities, net of effect of business acquisitions |

||||||||

| Accounts receivable, net |

(2,589 | ) | 475 | |||||

| Inventories |

(6,163 | ) | (4,265 | ) | ||||

| Prepaid VAT and other taxes |

(225 | ) | 735 | |||||

| Other assets |

1,409 | (5,751 | ) | |||||

| Accounts payable |

1,846 | 7,063 | ||||||

| Accrued expenses and other liabilities |

1,146 | (4,251 | ) | |||||

| Operating lease liabilities |

(232 | ) | 66 | |||||

|

|

|

|

|

|||||

| Net cash (used in) operating activities |

(9,660 | ) | (4,053 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from investing activities: |

||||||||

| Purchases of property and equipment |

(2,130 | ) | (842 | ) | ||||

| Acquisitions, net of cash acquired |

— | (22,950 | ) | |||||

| Investments in convertible debt instruments |

— | (639 | ) | |||||

|

|

|

|

|

|||||

| Net cash (used in) investing activities: |

(2,130 | ) | (24,431 | ) | ||||

|

|

|

|

|

|||||

| Cash flows from financing activities: |

||||||||

| Term loan borrowings |

2,066 | 2,912 | ||||||

| Payments on debt facilities |

(4,101 | ) | (3,418 | ) | ||||

| Credit line - borrowings |

13,830 | 28,300 | ||||||

| Dividends paid |

(571 | ) | (442 | ) | ||||

| Shares returned to pay employee taxes under restricted stock program |

(283 | ) | (304 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

10,941 | 27,048 | ||||||

|

|

|

|

|

|||||

| Effect of exchange rate changes on cash and cash equivalents |

1,122 | 1,094 | ||||||

|

|

|

|

|

|||||

| Net increase (decrease) in cash and cash equivalents |

273 | (342 | ) | |||||

| Cash and cash equivalents at beginning of period |

17,476 | 25,222 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 17,749 | $ | 24,880 | ||||

|

|

|

|

|

|||||

| Supplemental disclosure of cash flow information: |

||||||||

| Cash paid for interest |

$ | 1,024 | $ | 542 | ||||

|

|

|

|

|

|||||

| Cash paid for taxes |

$ | 1,692 | $ | 1,972 | ||||

|

|

|

|

|

|||||