Exhibit 99.1

Pure Cycle Announces Financial Results

For the Three Months Ended November 30, 2025

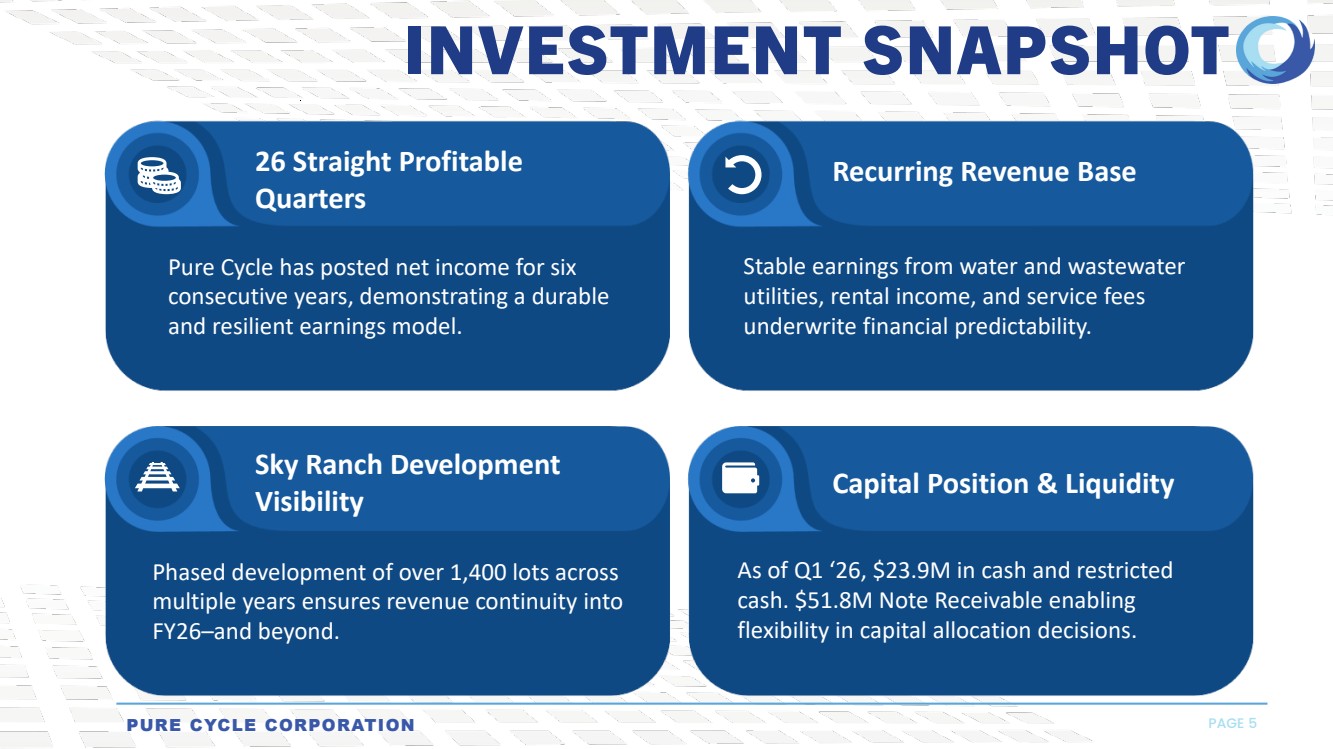

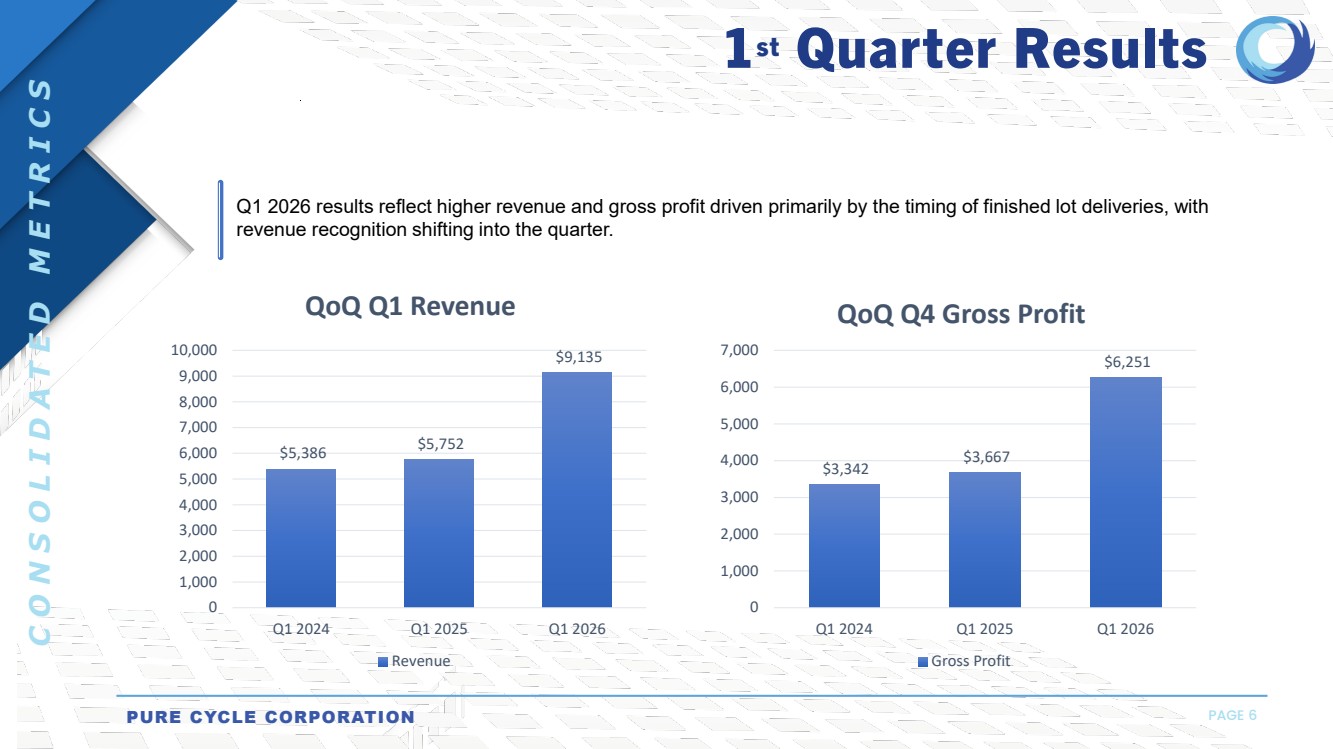

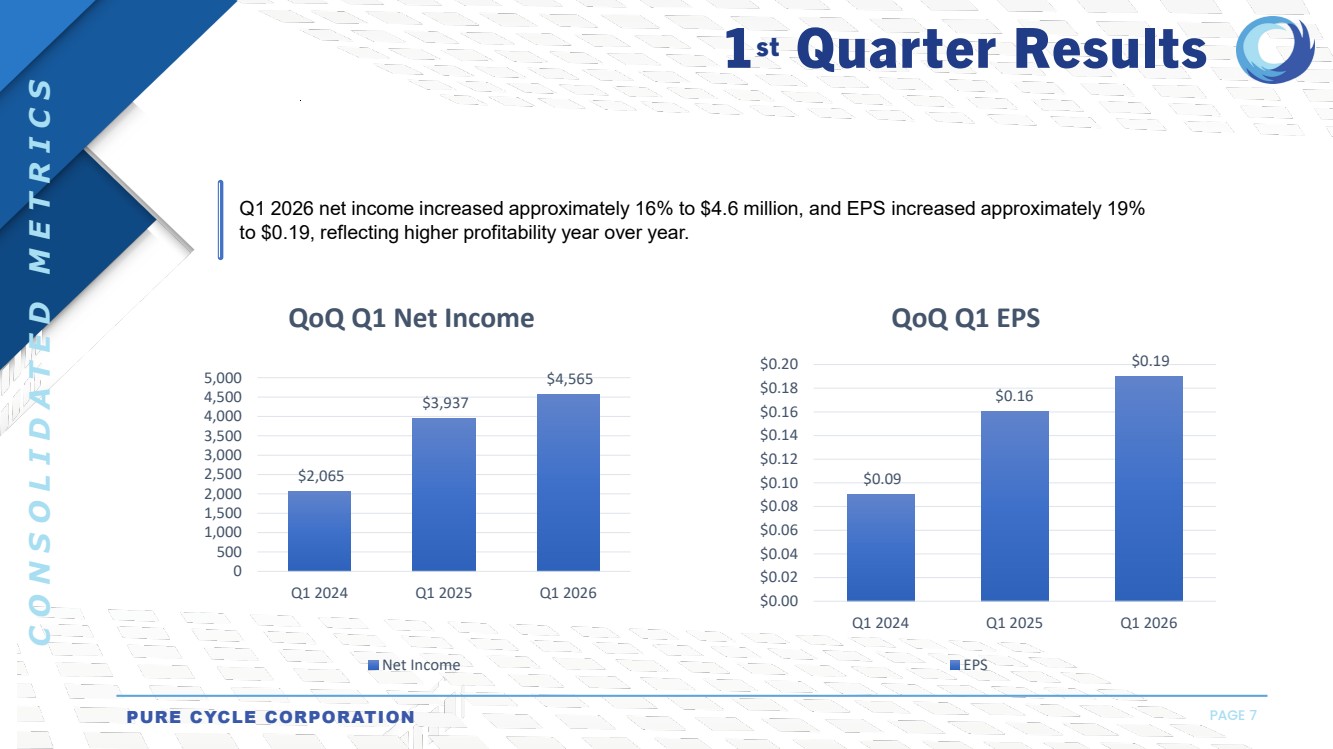

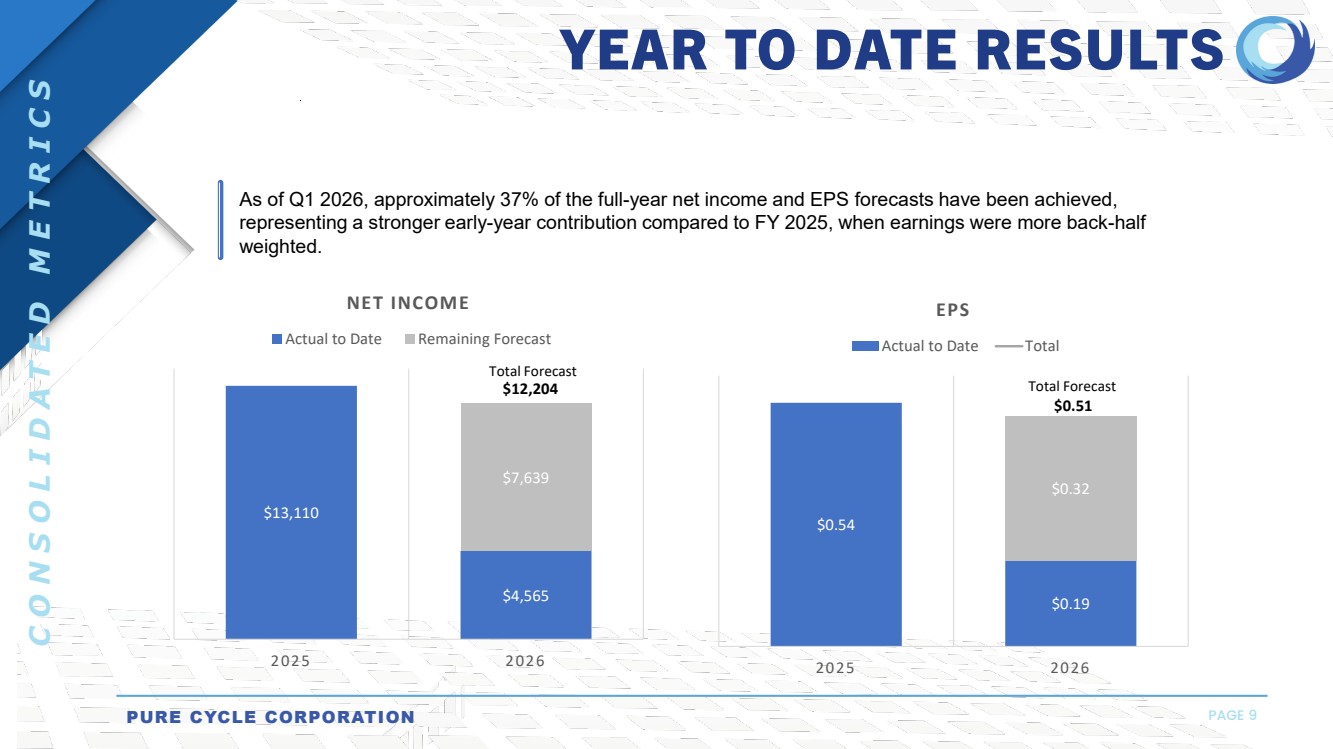

DENVER, CO / GLOBE NEWSWIRE / January 7, 2026 – Pure Cycle Corporation (NASDAQ Capital Market: PCYO) (“Pure Cycle”, “we”, “us” or “our”) announced its financial results for the three months ended November 30, 2025. Pure Cycle reported $4.5 million of net income for the three months ended November 30, 2025, which is a 16% increase in net income from the same period in 2024 and marks the twenty-sixth consecutive fiscal quarter with positive net income. Pure Cycle reported $0.19 of earnings per fully diluted common share, which is up from $0.16 in the same period in 2024, a 19% increase. Pure Cycle continues to see demand for entry level lots at our Sky Ranch Master Planned Community despite national headwinds in homebuilding. By partnering with our national home builders, we deliver finished lots on an annual cadence that allows for steady absorption while navigating cyclical housing industry trends.

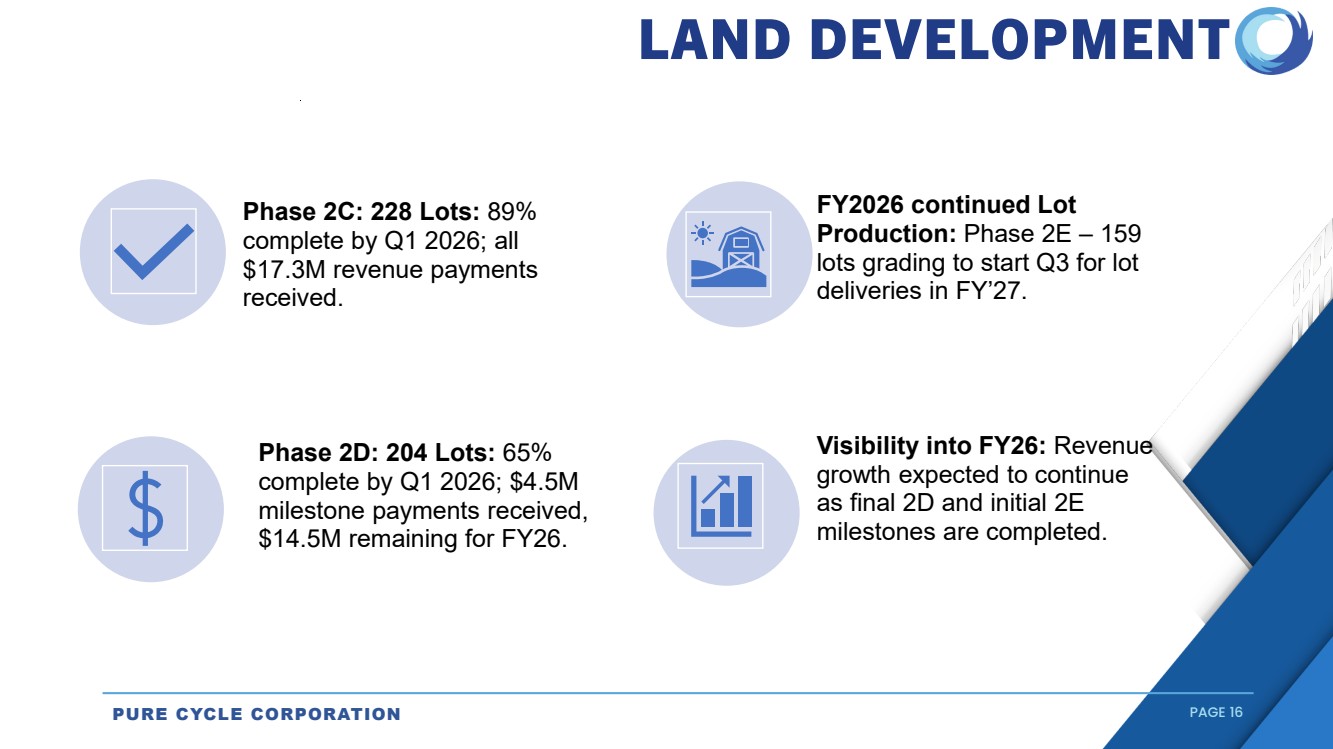

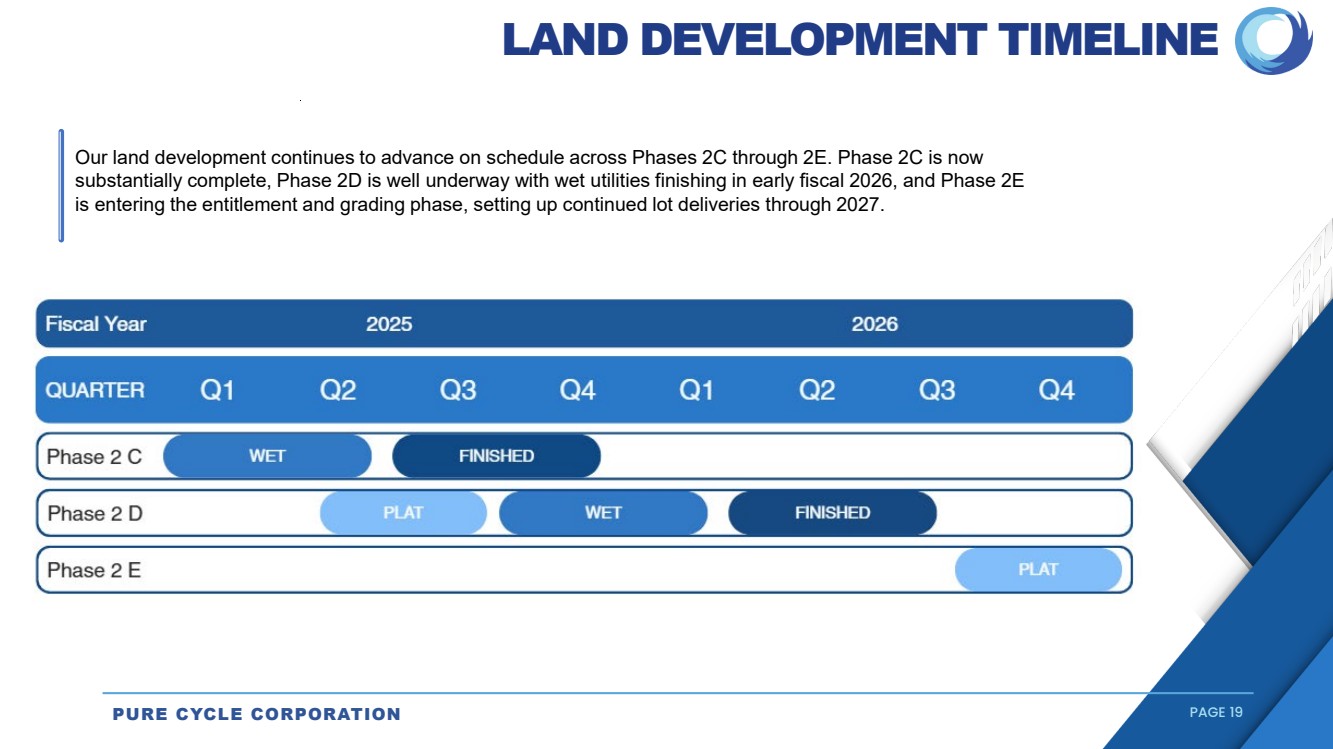

In the first quarter we completed the delivery of the remaining finished lots in Phase 2C and closed on the initial plat payment with a new homebuilder partner in Phase 2D. Our national homebuilder partners have already begun construction in Phase 2C. We expect to complete Phase 2D in fiscal 2026. Pure Cycle continues to diversify our land development segment by partnering with two new national homebuilders in Phase 2D to bring our portfolio of homebuilders to seven national builders. Finally, we have started platting our next 159 lots in Phase 2E and expect to have lots in Phase 2E completed in fiscal 2027 but will pace construction to match builder absorptions.

Our capital management and balance sheet strategy remains focused on growth and shareholder returns. We are prioritizing investment in our ongoing development projects while utilizing available liquidity to continue our share repurchase program and reserving sufficient capital for strategic development initiatives and land acquisitions.

Q1 2026 Highlights

| Ø | Net income for the three months ended November 30, 2025 and 2024 of $4.6 million and $3.9 million, respectively (a 16% increase). |

| Ø | Earnings per fully diluted common share for the three months ended November 30, 2025 and 2024 of $0.19 and $0.16, respectively (a 19% increase). |

| Ø | EBITDA for the three months ended November 30, 2025 and 2024 of $6.7 million and $7.6 million, respectively (a 12% decrease) (see table below for reconciliation of net income to EBITDA); and |

| Ø | Cash & cash equivalents totaled $17.1 million on November 30, 2025. |

Net Income to EBITDA Reconciliation

We continue our profitability as shown in the table below:

| | Three Months Ended | ||||

(In thousands) | | November 30, 2025 | | November 30, 2024 | ||

Net Income | | $ | 4,565 | | $ | 3,937 |

Add back: | | | | | | |

Interest expense, net | | | 94 | | | 109 |

Taxes | | | 1,465 | | | 1,271 |

Depreciation / amortization | | | 566 | | | 2,297 |

EBITDA | | $ | 6,690 | | $ | 7,614 |

| | | | | | |

Earnings per common share - basic and diluted | | | | | | |

Basic | | $ | 0.19 | | $ | 0.16 |

Diluted | | $ | 0.19 | | $ | 0.16 |

| | | | | | |

Weighted average common shares outstanding: | | | | | | |

Basic | | | 24,080,086 | | | 24,071,907 |

Diluted | | | 24,156,378 | | | 24,157,347 |

| | | | | | |

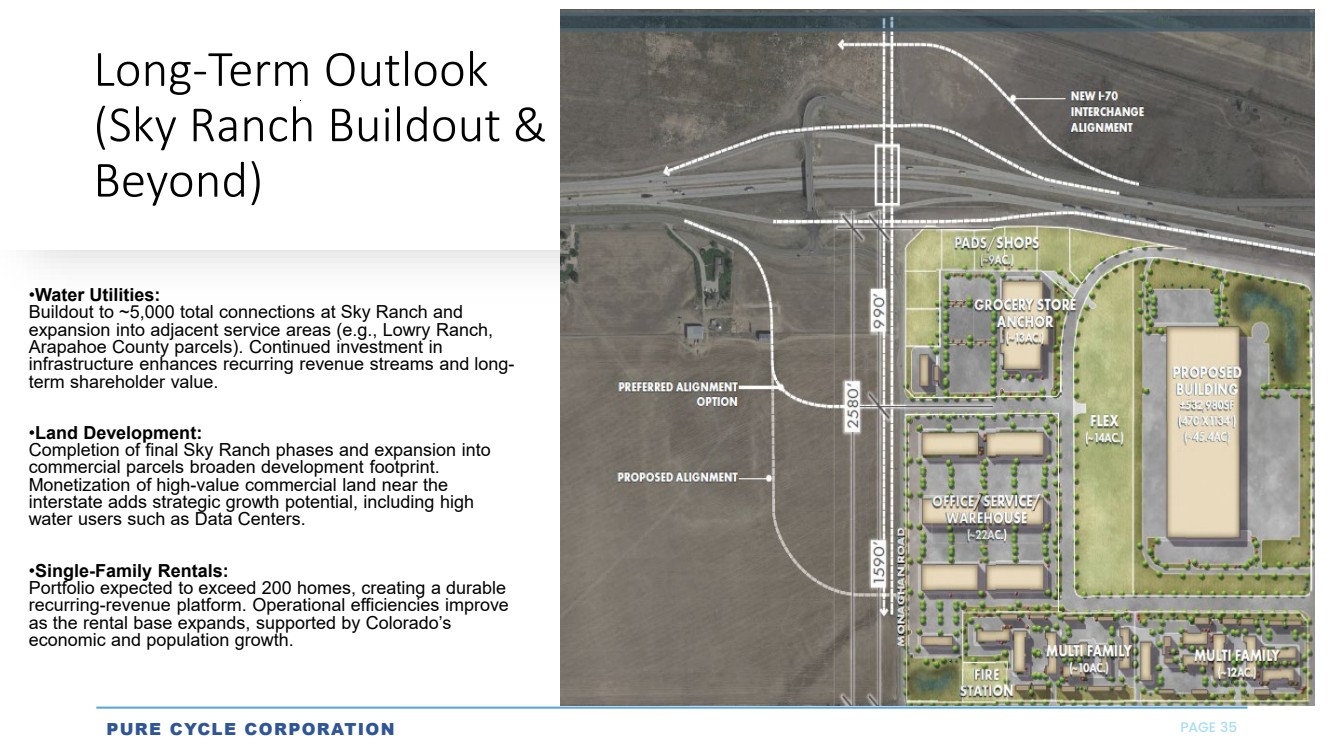

“We are pleased to welcome two new national home builders to our portfolio of customers Pulte Group and Oakwood who together with our other builders including Lennar, DR Horton, KB, Taylor Morrison, and Challenger are producing some of the finest entry level homes in the Denver metropolitan area. Sky Ranch continues to rank as one of the most affordable master planned communities in Denver. This year also brings the start of construction for our Charter High School, scheduled to open in the fall of 2026, which will bring a full K-12 school campus to Sky Ranch. We are grateful for our continued partnership with National Heritage Academy as our Charter operator at Sky Ranch and having a walkable school campus for our community,” commented Mark Harding, CEO of Pure Cycle. “We look forward to investing in improvements in 2026 such as beginning construction of a new interchange at I-70 which will allow continued expansion of the remaining residential phases as well as our valuable commercial opportunities at Sky Ranch,” continued Mr. Harding.

Q1 2026 Financial Summary

Revenues

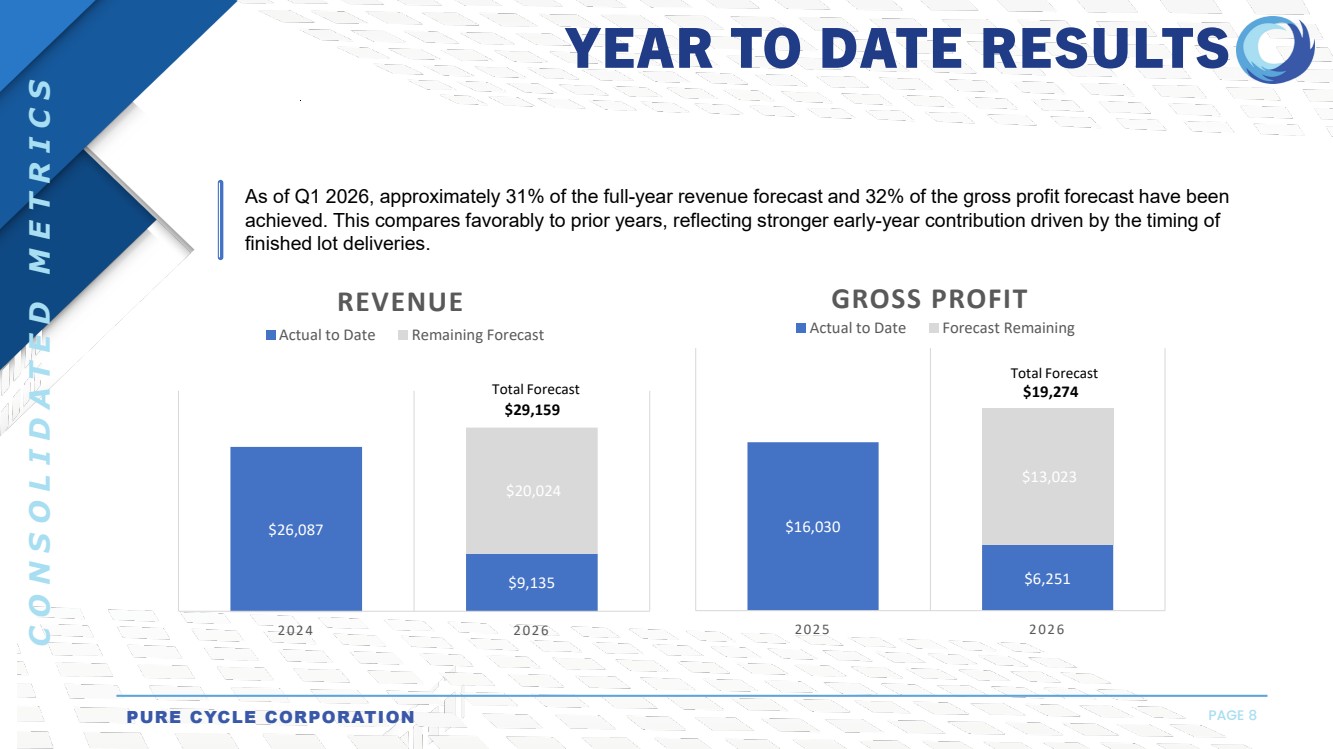

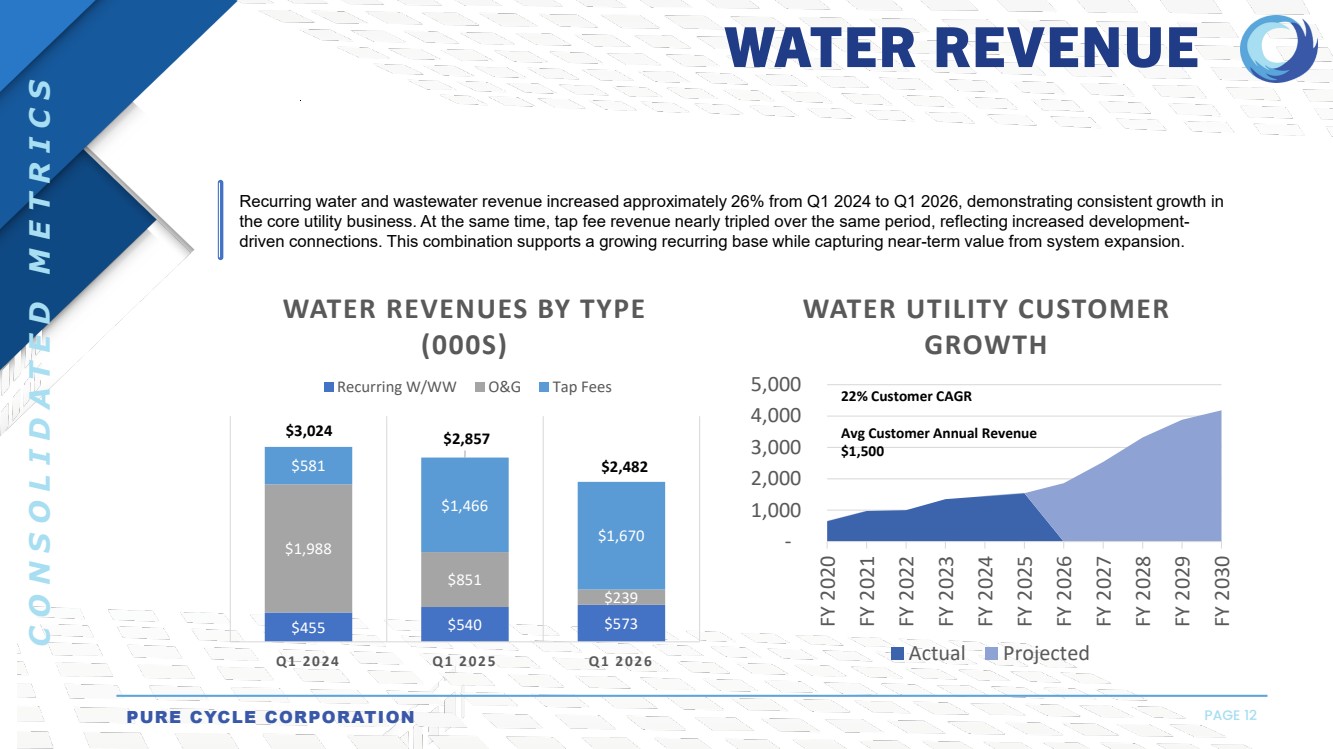

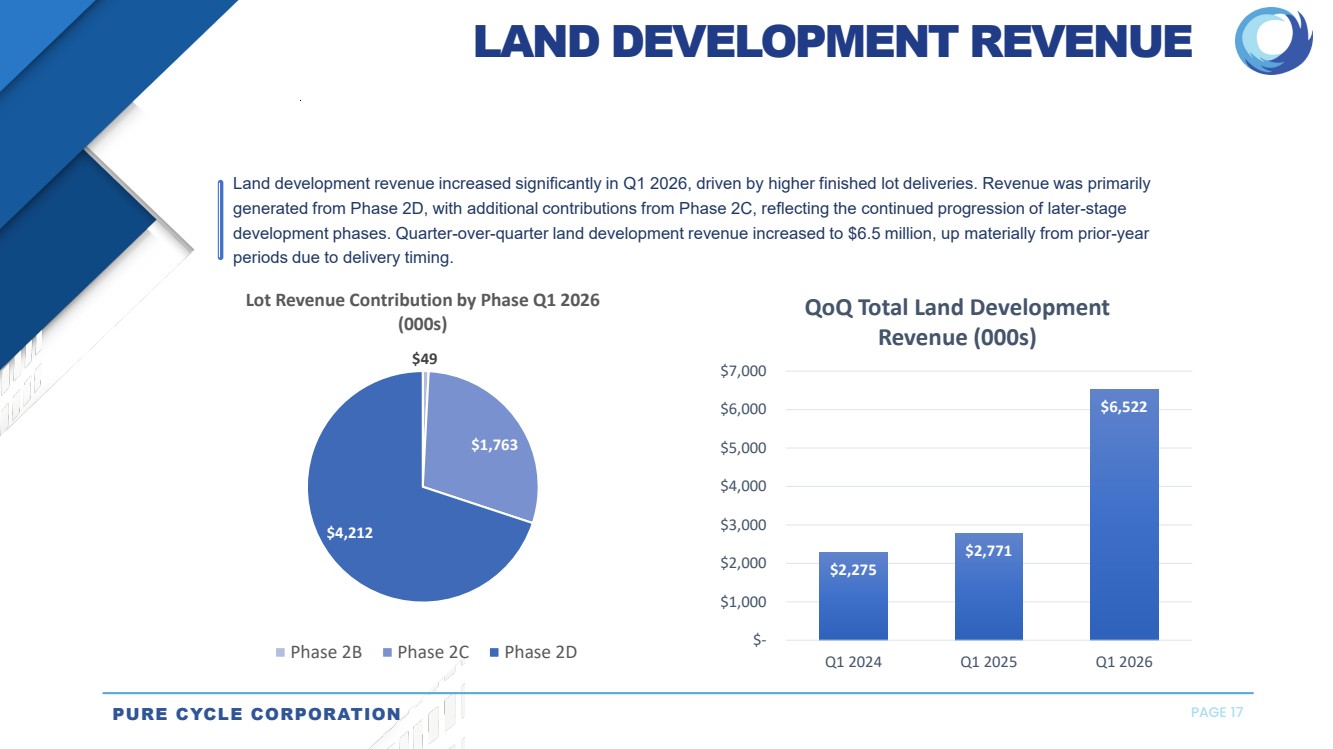

For the three months ended November 30, 2025, and 2024, we reported total revenue of $9.1 million and $5.8 million, respectively, with $2.5 million and $2.9 million being generated in our water and wastewater resource development segment, $6.5 million and $2.8 million in our land development segment, and $0.1 million and $0.1 million in our single-family rental business.

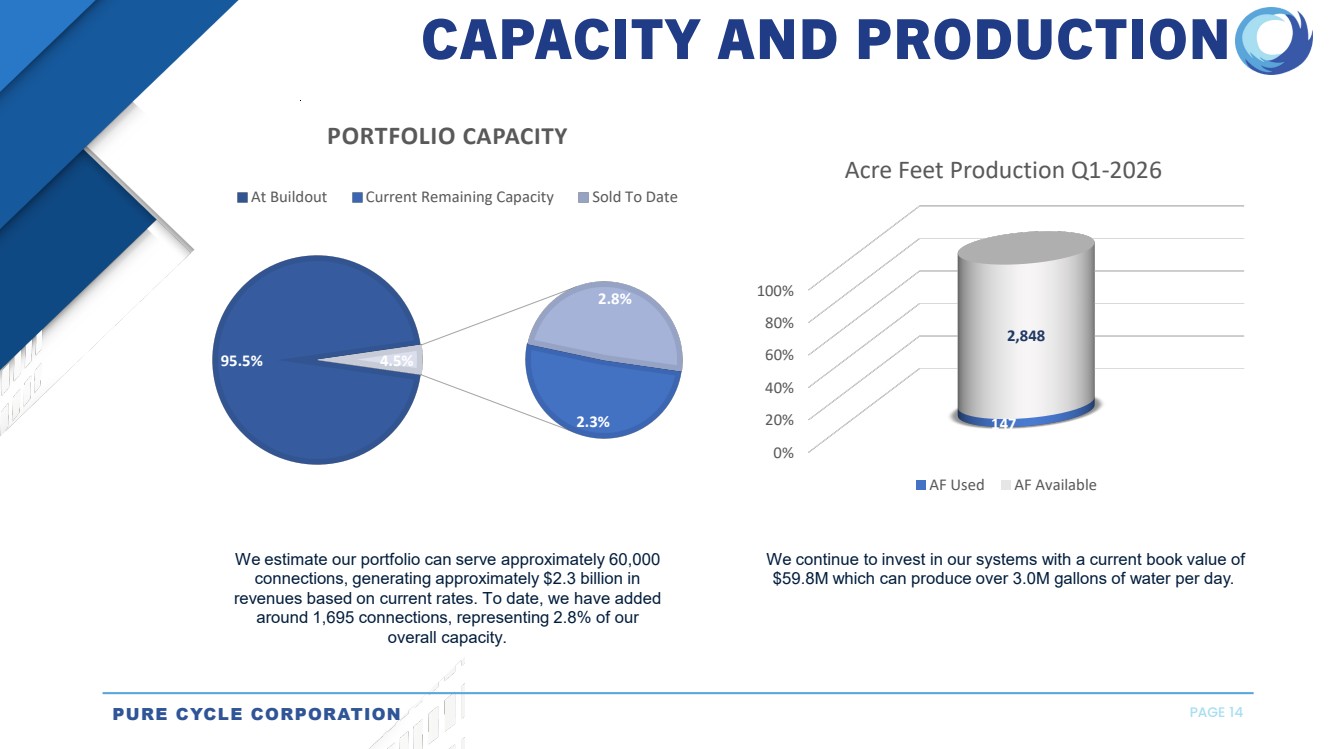

For the three months ended November 30, 2025, and 2024, we sold 51 and 38 water or water and wastewater taps, respectively for $1.7 million and $1.5 million. As of November 30, 2025, we have sold 1,016 water and wastewater taps at Sky Ranch in Phases 1, 2A, 2B, 2C and 2D. Based on current prices and engineering estimates, we believe Phase 2 of Sky Ranch will produce additional tap fee revenue of more than $19.0 million in water and wastewater tap fee revenue over the next three years.

2

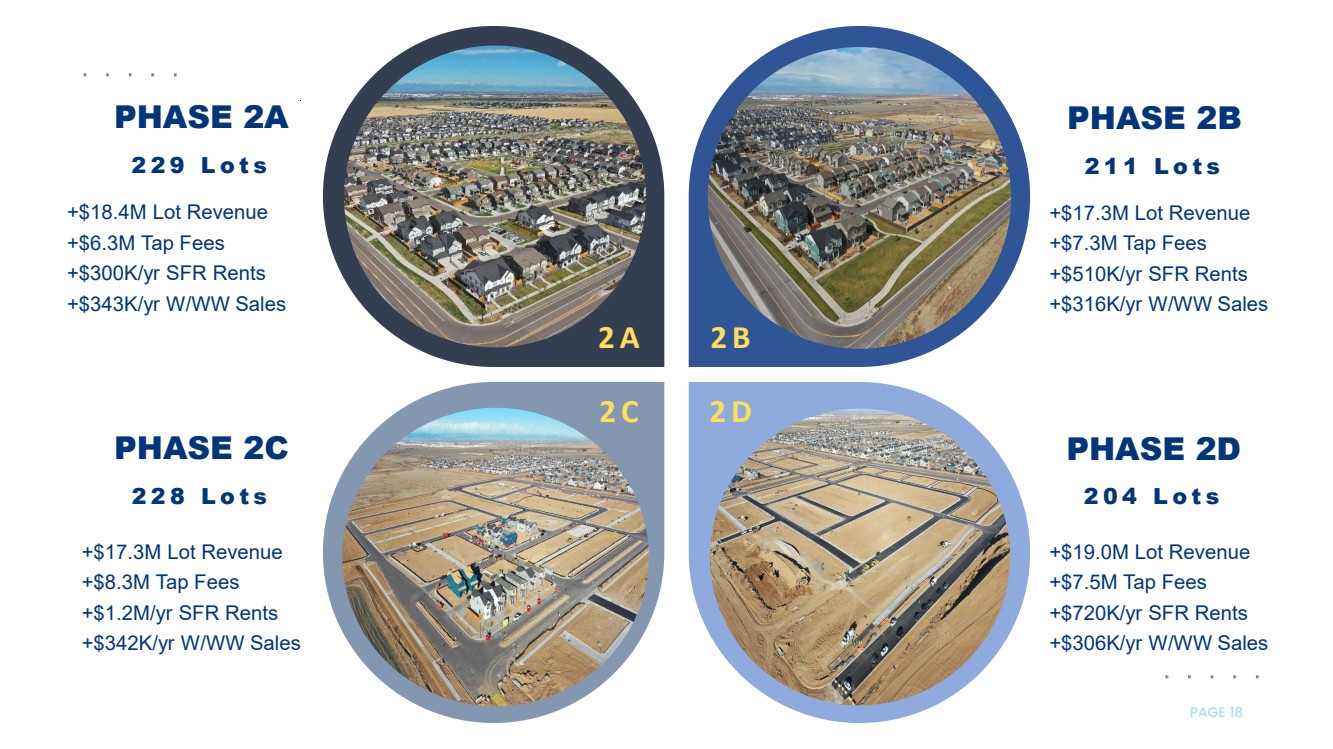

As of November 30, 2025, the first development phase (509 lots) is complete and the second development phase (1,031 lots) is being developed in five subphases, referred to as Phase 2A (229 lots), Phase 2B (211 lots), Phase 2C (228 lots), Phase 2D (204 lots) and Phase 2E (159 lots). As of November 30, 2025, Phase 2A is complete, Phase 2B is approximately 98% complete, Phase 2C is approximately 89% complete, and Phase 2D is approximately 65% complete. Phases 2B and 2C are substantially completed with some landscaping and warranty items remaining. Phase 2D is expected to be substantially complete by the end of Pure Cycle’s fiscal 2026 and Phase 2E is expected to be complete by the end of fiscal 2027.

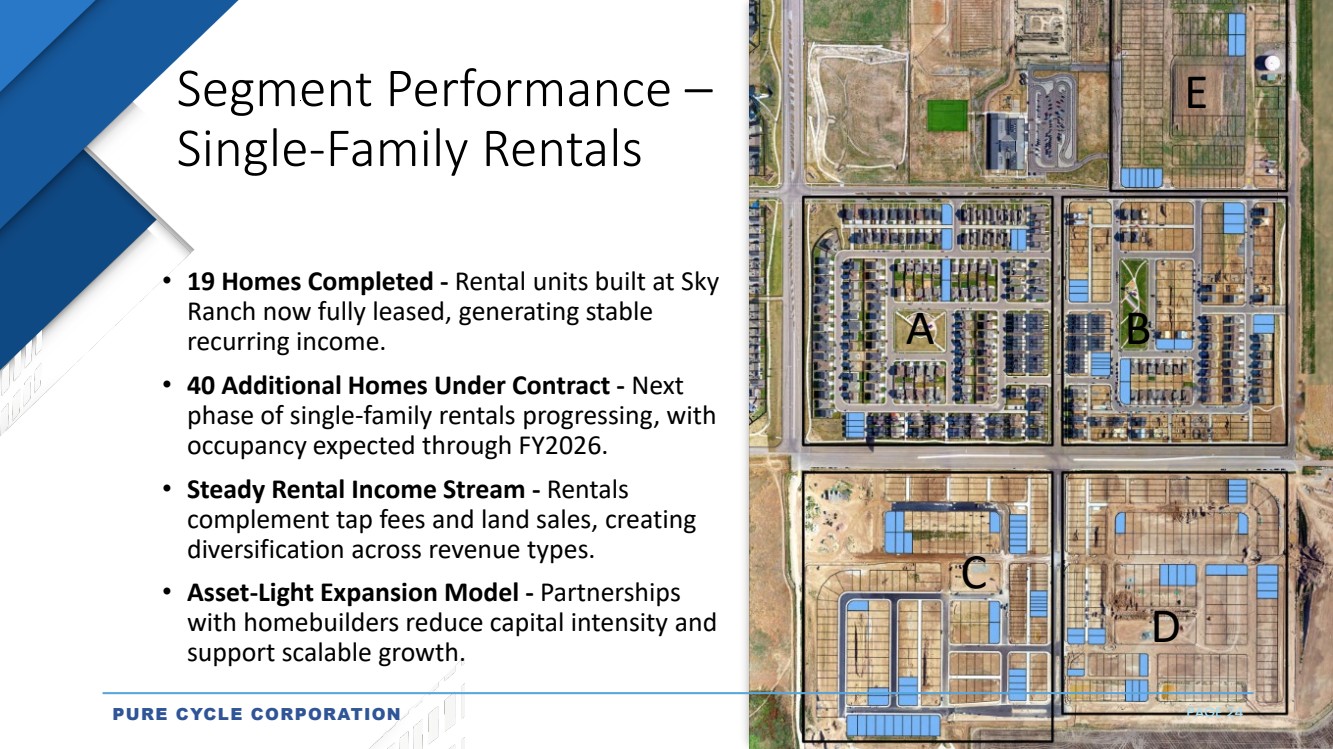

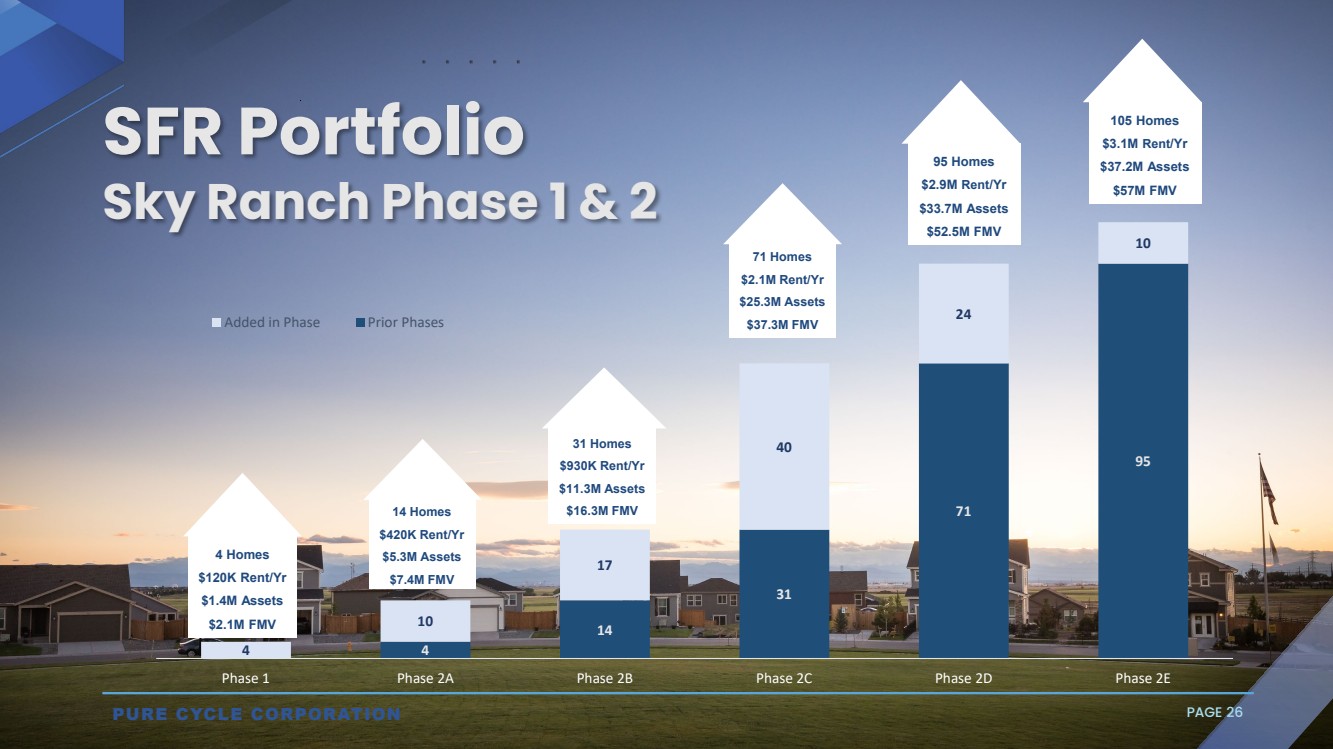

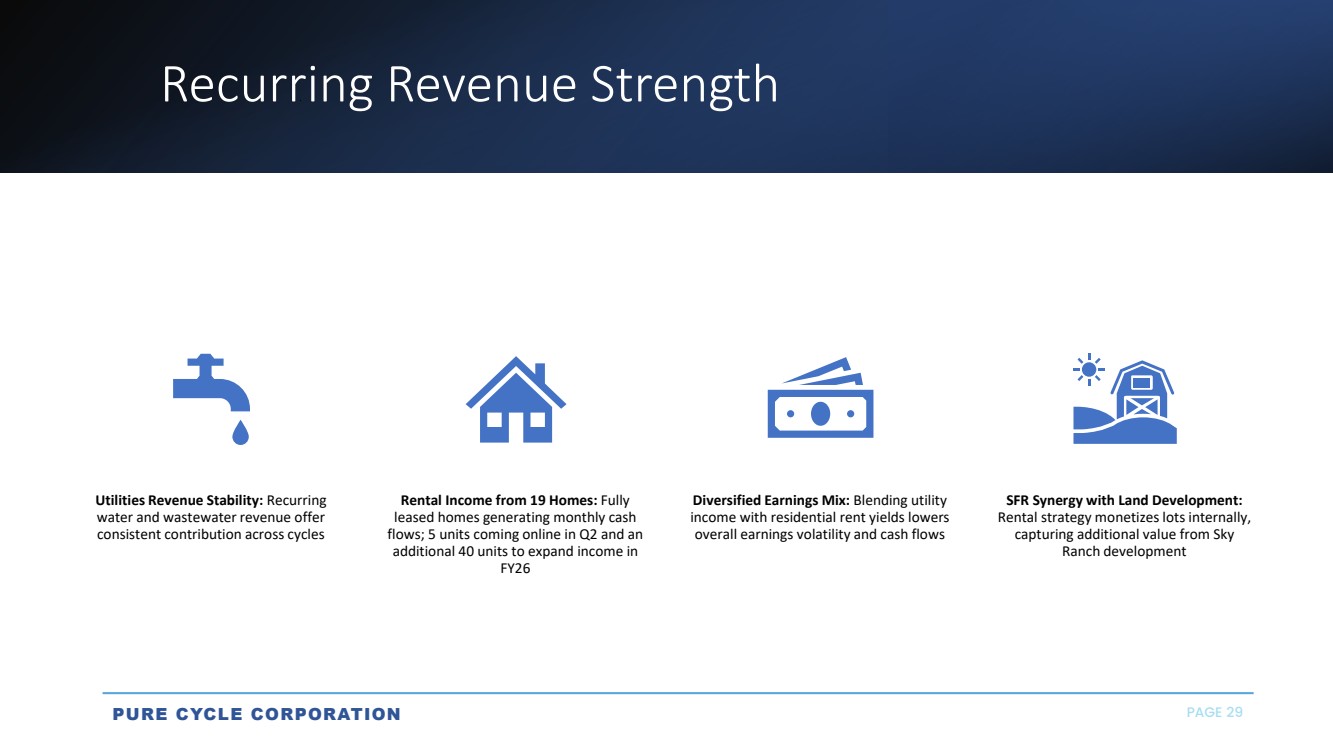

As of November 30, 2025, the single-family rental business had 19 homes built and rented or available for rent in Sky Ranch. During the fall of 2025, we brought five townhomes online that were constructed by one of our national homebuilder partners and we are currently under contract with several other national home builders to construct the next 40 single-family detached homes in Phases 2B and 2C at Sky Ranch for delivery in fiscal 2026. As noted in prior releases, due to strong demand for rental homes at Sky Ranch, we expect to have a total of 100 homes in Phase 2 with the ability to add up to 200 homes as Sky Ranch builds out.

“We achieved strong lot sales revenue in Q1 by capitalizing on demand for entry-level homes at Sky Ranch and expanding our partnerships with national homebuilders. We expect this momentum to carry into fiscal 2026 as we advance development in Phase 2D,” stated Marc Spezialy, CFO of Pure Cycle. “Construction is currently underway on 218 lots in Phase 2D, with finished lot deliveries scheduled for fiscal 2026. Additionally, we are marketing an additional 159 lots in Phase 2E, which are slated to begin development in the summer of 2026," concluded Mr. Spezialy.

Working Capital

We reported working capital (current assets less current liabilities) of $14.8 million as of November 30, 2025, with $17.1 million of cash and cash equivalents.

Q1 2026 Operational Summary

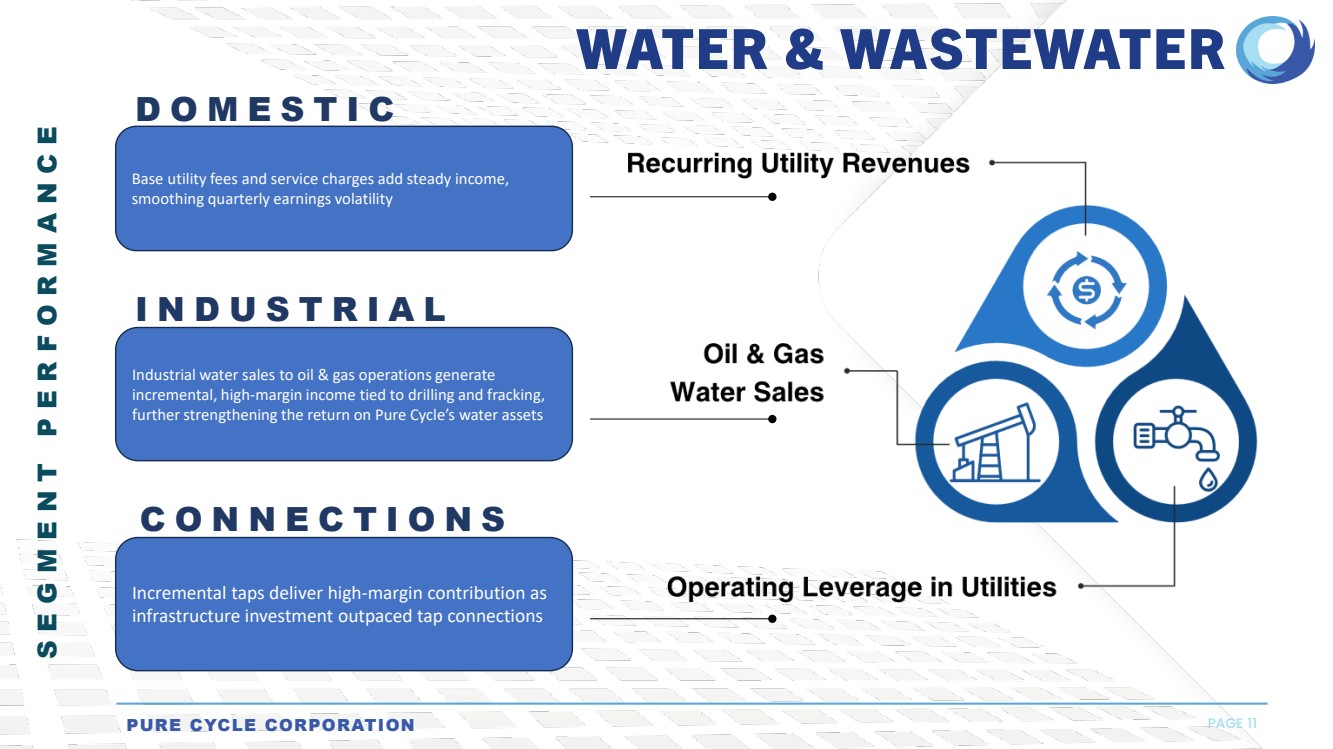

Water and Wastewater

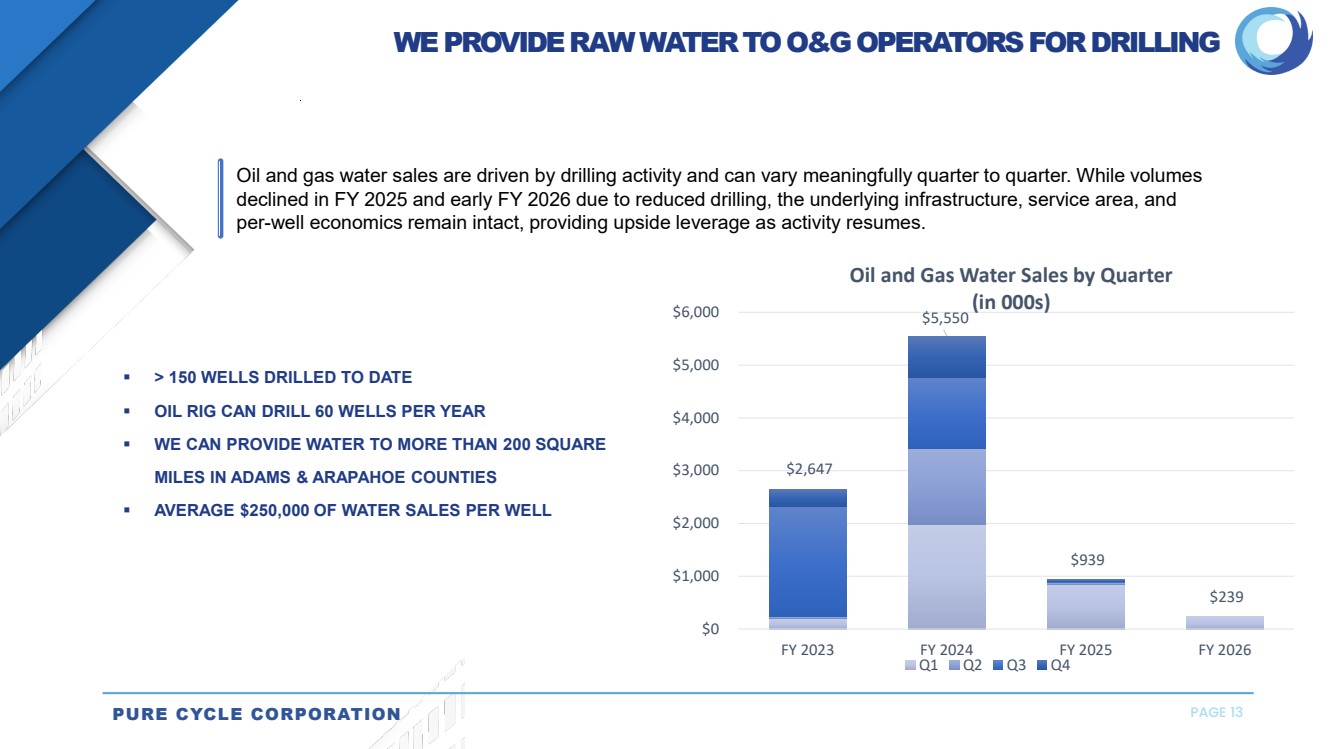

Water deliveries decreased for the three months ended November 30, 2025, to 147 acre-feet delivered as compared to 301 acre-feet delivered in the same period in 2024. The decrease in water deliveries is due to a decrease in demand from our oil and gas customers because of reduced drilling activity. Oil and gas operations are highly variable and dependent on oil prices, demand for gas, and timing of development of other leases in our service areas; however, our current expectation is for continued strong demand for oil and gas water sales for the coming years. As Sky Ranch continues to develop, we anticipate continued growth in our residential water and wastewater service revenues, which increased to 103 acre-feet delivered in the three months ending November 30, 2025 compared to 93 acre-feet delivered in the same period in 2024. Water and wastewater tap sales increased in 2025 to 51 taps sold compared to 38 taps in the same period in 2024. Water and wastewater taps are sold to home builders at the time a building permit is issued and are dependent on when the home builder constructs homes and are not contractually driven in terms of timing; therefore, the timing of tap sales fluctuates with demand for new construction. During fiscal 2026, the average price of a Sky Ranch water and wastewater tap held at approximately $42,000 per tap due to the mix of products being developed, despite an increase in the price of a tap per single-family equivalent.

Land Development

Lot sales revenue increased to $6.0 million for the three months ended November 30, 2025 compared to $2.3 million in the same period in 2024. The number of lots delivered in the first quarter was the result of the delays in closings in Phase 2D experienced at year-end. We recognized certain milestones from our Lot Delivery Agreements with home builders in 2025 which accounted for less than $0.1 million in lot sales revenue for Phase 2B, $1.8 million in lot sales revenue for Phase 2C and $4.2 million in lot sales revenue for Phase 2D. We expect to be substantially complete with the delivery of all 180 lots in Phase 2D during fiscal 2026. Despite lots being transferred to the homebuilders, we will continue to conduct minor construction activities to complete Phases 2B and 2C and to turn over the completed infrastructure to the applicable governmental agency for maintenance.

3

Single Family Rentals

During the first quarter of fiscal 2026, an additional five townhomes were brought online and were either rented or available for rent by quarter-end, bringing our total single-family rental count to 19. We are currently under contract with several national home builders to construct the next 40 single-family detached homes in Phases 2B and 2C at Sky Ranch for delivery in fiscal 2026.

Earnings Presentation Information

Pure Cycle will host an earnings presentation on Thursday January 8, 2026, at 8:30AM Eastern (6:30AM Mountain) to discuss the financial results and answer questions. For an interactive experience, including the ability to ask questions and view the slide presentation, please register and join the event via the link below. Call in access will be in listen-only mode. See below for event details. Additionally, we will post a detailed slide presentation on our website, which will provide an overview of Pure Cycle and present summary financial results and can be accessed at www.purecyclewater.com.

When:8:30AM Eastern (6:30AM Mountain) on January 8, 2026

Event link:https://www.purecyclewater.com/Q12026

Call in number:872-240-8702 (access code: 384 040 539#)

Replay:https://www.purecyclewater.com/investors/news-events/ir-calendar

4

Other Important Information

The table below presents our consolidated results of operations for the three months ended November 30, 2025 and 2024 (unaudited):

| | Three Months Ended | ||||

(In thousands, except share information) | | November 30, 2025 | | November 30, 2024 | ||

REVENUES: |

| | |

| | |

Water and Wastewater | | | | | | |

Water and wastewater activities | | $ | 812 | | $ | 1,391 |

Water and wastewater tap fees | |

| 1,670 | |

| 1,466 |

Total water and wastewater | | | 2,482 | | | 2,857 |

Land Development | | | | | | |

Lot sales | |

| 6,024 | |

| 2,319 |

Project management fees | | | 296 | | | 253 |

Special facility projects and other | |

| 202 | |

| 199 |

Total land development | | | 6,522 | | | 2,771 |

| | | | | | |

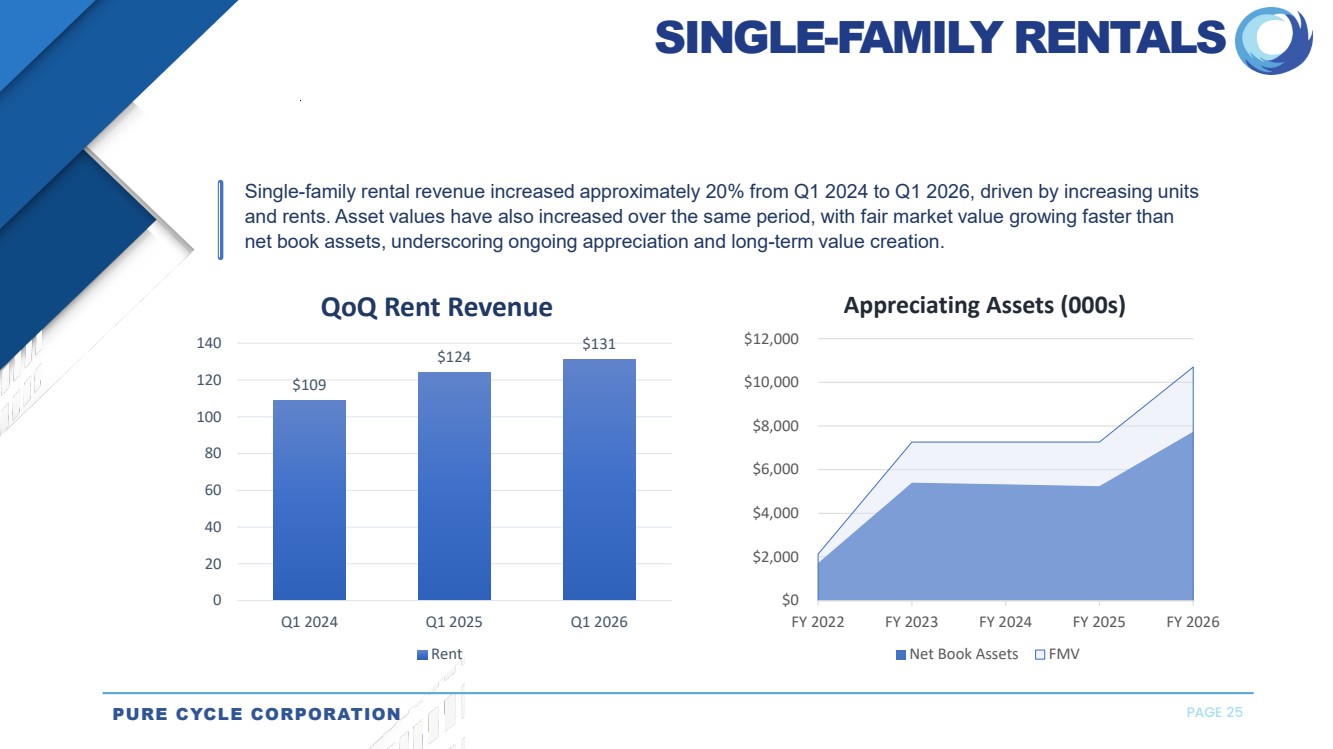

Single-family rentals | | | 131 | | | 124 |

Total revenues | |

| 9,135 | |

| 5,752 |

| | | | | | |

COST OF REVENUES: | | | | | | |

Water and wastewater | |

| 1,112 | |

| 1,061 |

Lot development | |

| 1,717 | |

| 956 |

Single-family rental | |

| 55 | |

| 68 |

Total cost of revenues | |

| 2,884 | |

| 2,085 |

| | | | | | |

General and administrative expenses | |

| 1,709 | |

| 1,792 |

Depreciation | |

| 159 | |

| 155 |

Operating income | |

| 4,383 | |

| 1,720 |

| | | | | | |

Other income (expense): | | | | | | |

Interest income | | | 949 | | | 731 |

Interest expense | | | (94) | | | (109) |

Oil and gas royalty income, net | | | 740 | | | 2,807 |

Other, net | | | 52 | | | 59 |

Income from operations before income taxes | |

| 6,030 | |

| 5,208 |

Income tax expense | |

| (1,465) | |

| (1,271) |

Net income | | $ | 4,565 | | $ | 3,937 |

| | | | | | |

Earnings per common share - basic and diluted | | | | | | |

Basic | | $ | 0.19 | | $ | 0.16 |

Diluted | | $ | 0.19 | | $ | 0.16 |

Weighted average common shares outstanding: | | | | | | |

Basic | |

| 24,080,086 | | | 24,071,907 |

Diluted | |

| 24,156,378 | | | 24,157,347 |

5

The following table presents our consolidated financial position as of November 30, 2025 (unaudited) and August 31, 2025 (audited):

(In thousands, except shares) | | November 30, 2025 | | August 31, 2025 | ||

ASSETS: | | | | | | |

Current Assets: | | | | | | |

Cash and cash equivalents | | $ | 17,135 | | $ | 21,931 |

Accounts receivable, net | |

| 2,502 | |

| 1,330 |

Prepaid expenses and other assets | | | 414 | | | 1,004 |

Land under development | | | 6,212 | | | 7,388 |

Total current assets | | | 26,263 | | | 31,653 |

Restricted cash | | | 6,734 | | | 6,448 |

Investment in water and wastewater systems, net | |

| 68,708 | |

| 67,523 |

Land and mineral rights held for development | | | 4,486 | | | 4,168 |

Single-family rental units | | | 7,739 | | | 5,240 |

Related party notes receivable, including accrued interest, less current portion | |

| 51,813 | |

| 45,002 |

Other assets | | | 2,326 | |

| 2,245 |

Total assets | | $ | 168,069 | | $ | 162,279 |

| | | | | | |

LIABILITIES & SHAREHOLDERS’ EQUITY: | | | | | | |

Current Liabilities: | | | | | | |

Accounts payable | | $ | 3,284 | | $ | 3,518 |

Accrued and other liabilities | | | 5,322 | | | 4,335 |

Deferred revenue | | | 2,442 | |

| 3,355 |

Debt, current portion | | | 440 | | | 411 |

Total current liabilities | | | 11,488 | | | 11,619 |

Debt, less current portion | | | 7,554 | |

| 6,380 |

Deferred tax liability, net | |

| 1,541 | |

| 1,541 |

Lease obligations, less current portion | | | — | | | 1 |

Total liabilities | |

| 20,583 | |

| 19,541 |

| | | | | | |

Series B preferred shares: par value $0.001 per share, 25 million authorized; | |

| — | |

| — |

Common shares: par value 1/3 of $.01 per share, 40.0 million authorized; | |

| 80 | |

| 80 |

Additional paid-in capital | |

| 175,631 | |

| 175,448 |

Accumulated deficit | |

| (28,225) | |

| (32,790) |

Total shareholders’ equity | |

| 147,486 | |

| 142,738 |

| | $ | 168,069 | | $ | 162,279 |

6

Company Information

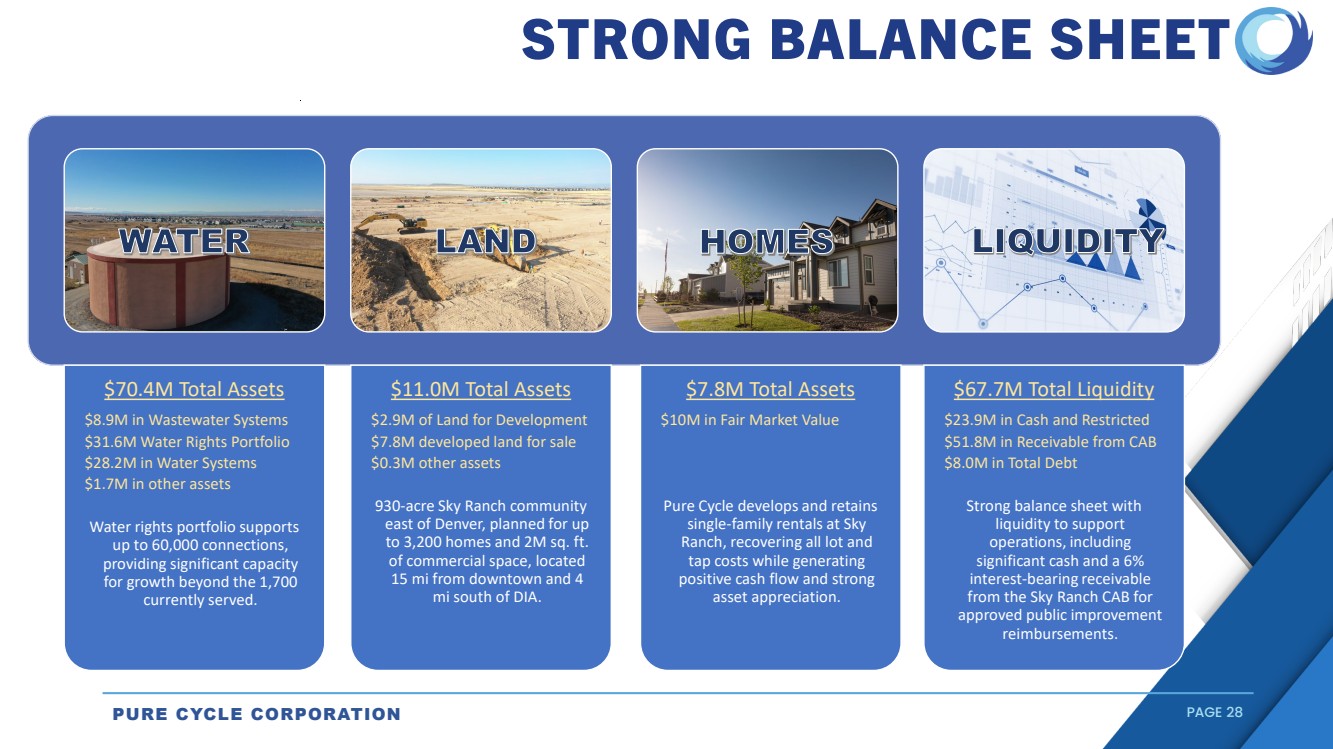

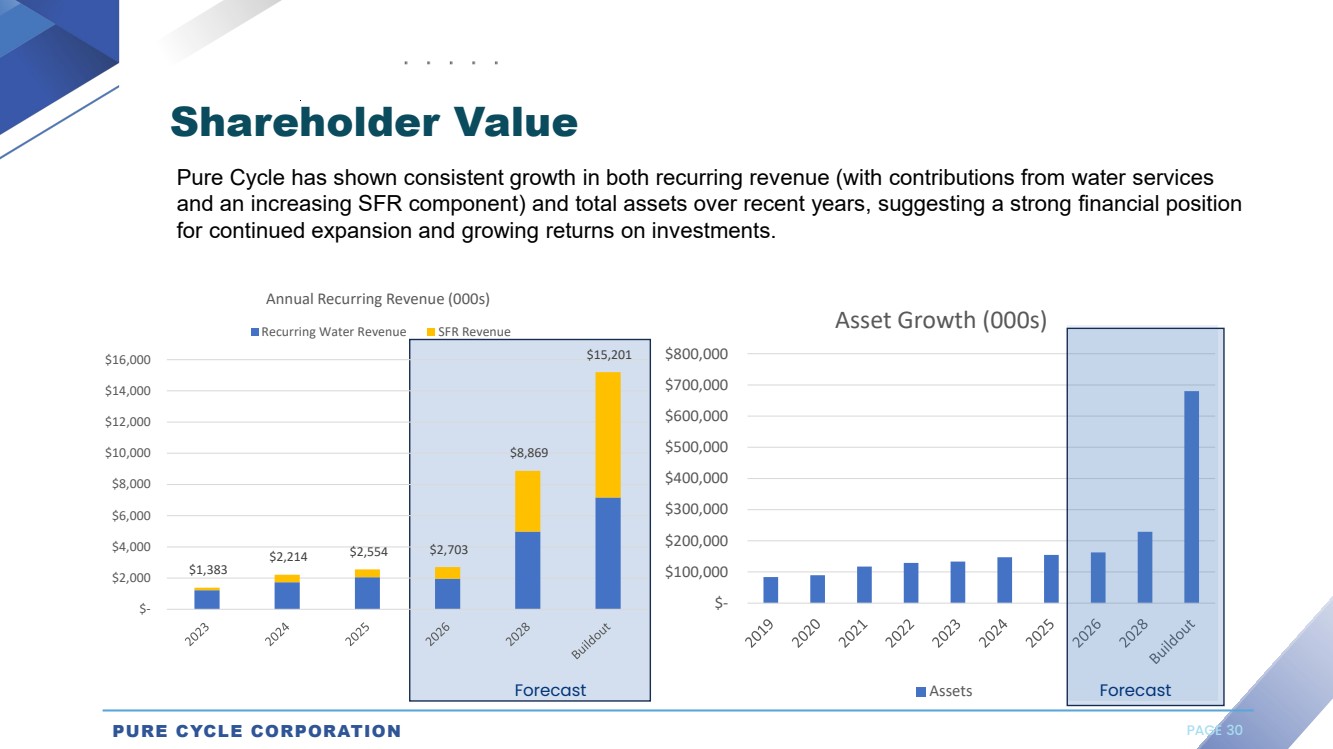

Pure Cycle continues to grow and strengthen its operations, grow its balance sheet, and drive recurring revenues. We operate in three distinct business segments, each of which complements the other. At our core, we are an innovative and vertically integrated wholesale water and wastewater service provider. In 2017, we launched our land development segment, which develops master planned communities on land we own and to which we provide water and wastewater services. In 2021, we launched our newest line of business, the rental of single-family homes located at Sky Ranch, which provides long-term recurring revenues, furthers our land development operations, and adds more customers to our water resource segment.

Additional information, including our recent press releases and SEC filings, is available at www.purecyclewater.com, or you may contact our President, Mark W. Harding, or our CFO, Marc Spezialy, at 303-292-3456 or [email protected].

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are all statements, other than statements of historical facts, included in this press release that address activities, events or developments that we expect or anticipate will or may occur in the future, such as statements about the following: factors that differentiate us in the market and our belief that we are well positioned in the market; the timing of completion and availability for rent of our rental units; the number of rental units we may be able to add as Sky Ranch builds out; timing of development at Sky Ranch, including timing of delivery of finished lots and plans to pace construction to match builder absorptions; future water and wastewater tap sales and revenues; timing of future home construction by our home builder customers; the strength of the Sky Ranch market, including the demand for entry-level and rental homes; future demand for oil and gas water; and forecasts about our expected financial results. The words "anticipate," "likely," "may," "should," "could," "will," "believe," "estimate," "expect," "plan," "intend," "potential" and similar expressions are intended to identify forward-looking statements. Investors are cautioned that forward-looking statements are inherently uncertain and involve risks and uncertainties that could cause actual results to differ materially. Factors that could cause actual results to differ from projected results include, without limitation: home mortgage interest rates, inflation, trade policies, tariffs, and other factors impacting the housing market and home sales; the risk factors discussed in Part I, Item 1A of our Annual Report on Form 10-K for the fiscal year ended August 31, 2025; and those factors discussed from time to time in our press releases, public statement and documents filed or furnished with the U.S. Securities and Exchange Commission.

SOURCE: Pure Cycle Corporation

7