Exhibit

99.1

|

Southern First Reports First Quarter 2026 Results |

Greenville,

South Carolina, April 21, 2026 – Southern First Bancshares, Inc. (NASDAQ: SFST) (Southern First), today announced its

financial results for the three months ended March 31, 2026. Strong loan growth and continued margin expansion drove year-over-year net

interest income growth of 29%. Net income was $9.9 million and diluted earnings per share was $1.19, representing a $0.54, or 83%, increase

over the first quarter of 2025, and relatively unchanged from the fourth quarter of 2025. Return on average assets was 0.91%, up 39 basis

points over the first quarter of last year, and tangible common equity to assets was 8.29%, up 41 basis points from the first quarter

of 2025. Net charge-offs were approximately $50 thousand, or 0.01% of average loans, annualized, consistent with linked quarter and year-over-year

results. Nonperforming assets were 0.26% of total assets, down from 0.32% for the fourth quarter. Provision for credit losses increased

by $650 thousand, and the allowance for credit losses represented 1.10% of loans, consistent with the past several quarters.

“We

are excited to report our first quarter 2026 results which include record retail deposit growth of nearly $210 million, representing

a 27% annualized growth rate. Our first quarter 2026 net income was $9.9 million and is 88% higher than the same quarter last year. We

have tremendous momentum in growing client relationships and raised additional capital in the form of common equity this quarter to support

our growth expectations,” stated Art Seaver, Chief Executive Officer.

On April 15, 2026, Southern First announced an underwritten public offering of

1,050,000 shares of common stock and granted the underwriters an option to purchase up to 157,500 additional shares. The offering closed

on April 17, 2026, with a total of 1,207,500 shares issued at $54.00 per share for aggregate gross proceeds of approximately $65.2 million

before discounts and expenses. The Company intends to use the net proceeds from the offering for general corporate purposes, which may

include supporting organic growth initiatives, providing capital to the Company’s bank subsidiary, redeeming or repurchasing outstanding

indebtedness, including subordinated debt, and for working capital purposes.

Financial

Highlights – First Quarter 2026:

Earnings

| ● | Diluted

earnings per common share was $1.19, up $0.54, or 83%, compared to the first quarter of 2025;

and down slightly by $0.01 from the fourth quarter of 2025 |

| ● | Net

income improved to $9.9 million, a $4.6 million increase, or 88%, compared to the first quarter

of 2025 |

| ● | Total

revenue was $33.8 million, an increase of $7.3 million, or 28%, year-over-year and $2.0 million

on a linked quarter basis |

| ● | Net

interest income improved by $6.9 million, or 29% year-over-year, driven primarily by new

loan volume |

| ● | Net

interest margin was 2.88%, a 16 basis point increase from 2.72% for the fourth quarter of

2025, and included a $543 thousand repayment of interest on one large nonaccrual loan |

| ● | Noninterest

income was $3.5 million compared to $3.1 million for the first quarter last year; the increase

was impacted by a one-time $515 thousand loss on the sale of securities in the fourth quarter

of 2025 |

| ● | Noninterest

expense to average assets was 1.84%, compared to 1.87% for first quarter of 2025 |

| ● | Return

on average equity was 10.67%, compared to 6.38% for the first quarter of 2025 |

| ● | Return

on average assets was 0.91%, compared to 0.52% for the first quarter of 2025 |

Balance

Sheet

| ● | Total

loans were $3.9 billion, up $97.1 million, or 10% (annualized), from the fourth quarter of

2025 |

| ● | Retail

deposits were $3.4 billion, up $207.8 million, or 27% (annualized) from the fourth quarter

of 2025 |

| ● | Book

value per common share was $46.00, an increase of 10% (annualized) from the fourth quarter

of 2025 |

| ● | Tangible

common equity (TCE) ratio was 8.29%, down 8 basis points on a linked quarter basis driven

by loan growth, and up from 7.88% for the first quarter of 2025 |

| ● | Common

equity Tier1 ratio (CET1) was 11.03%, down slightly from the fourth quarter of 2025, and

up from 10.75% for the first quarter 2025 |

Asset

Quality

| ● | Nonperforming

assets to total assets were 0.26%, compared to 0.32% for the linked quarter, primarily due

to the repayment of a large nonaccrual loan, while accruing loans 30 days or more past due

to total loans were 0.20%, compared to 0.14% for the fourth quarter |

| ● | Classified

assets were 3.25% as a percentage of total loans compared to 4.28% for the linked quarter

end |

| ● | Provision

for credit losses was $1.3 million and includes a $1.2 million provision for loan losses

and a $150 thousand provision for unfunded commitments driven by new loan growth; Allowance

for credit losses to total loans remained at 1.10% for the quarter |

| ● | Net

charge-offs were 0.01% as a percentage of average loans on an annualized basis |

SELECTED

FINANCIAL DATA

| |

|

|

|

|

|

|

| |

|

Quarter

Ended |

|

Mar

31 2026- |

| |

|

March

31 |

December

31 |

September 30 |

June

30 |

March

31 |

|

Mar

31 2025 |

| |

|

2026 |

2025 |

2025 |

2025 |

2025 |

|

Change |

| Income

Statement Summary ($ in thousands): |

|

|

|

|

|

|

|

|

| Net

interest income |

$ |

30,259 |

28,744 |

27,529 |

25,295 |

23,383 |

|

29.4% |

| Noninterest

income |

|

3,540 |

3,090 |

3,600 |

3,334 |

3,114 |

|

13.7% |

| Total

Revenue |

|

33,799 |

31,834 |

31,129 |

28,629 |

26,497 |

|

27.6% |

| Provision

for credit losses |

|

1,300 |

650 |

850 |

700 |

750 |

|

73.3% |

| Noninterest

expense |

|

20,015

|

18,416

|

18,946

|

19,336

|

18,836

|

|

6.3%

|

| Income

before income tax expense |

|

12,484

|

12,768

|

11,333

|

8,593

|

6,911

|

|

80.6%

|

| Income

tax expense |

|

2,597

|

2,911

|

2,671

|

2,012

|

1,645

|

|

57.9%

|

| Net

income available to common shareholders |

|

9,887

|

9,857

|

8,662

|

6,581

|

5,266

|

|

87.8%

|

| |

|

|

|

|

|

|

|

|

| Earnings

($ in thousands, except per share data): |

|

|

|

|

|

|

|

|

| Earnings

per common share, diluted |

|

1.19

|

1.20

|

1.06

|

0.81

|

0.65

|

|

83.1%

|

| Net

interest margin (tax-equivalent)(1) |

|

2.88% |

2.72% |

2.62% |

2.50% |

2.41% |

|

0.47 |

| Return

on average assets(2) |

|

0.91% |

0.90% |

0.80% |

0.63% |

0.52% |

|

0.39 |

| Return

on average equity(2) |

|

10.67% |

10.77% |

9.78% |

7.71% |

6.38% |

|

4.29 |

| Efficiency

ratio(3) |

|

59.22% |

57.85% |

60.86% |

67.54% |

71.08% |

|

(11.86) |

| Noninterest

expense to average assets (2) |

|

1.84% |

1.68% |

1.74% |

1.86% |

1.87% |

|

(0.03) |

| Balance

Sheet ($ in thousands): |

|

|

|

|

|

|

|

|

| Total

loans(4) |

$ |

3,942,219 |

3,845,124 |

3,789,021 |

3,746,841 |

3,683,919 |

|

7.0% |

| Total

deposits |

|

3,873,455 |

3,716,803 |

3,676,417 |

3,636,329 |

3,620,886 |

|

7.0% |

| Retail

deposits(5) |

|

3,371,721 |

3,163,914 |

3,108,411 |

3,075,631 |

3,020,392 |

|

11.6% |

| Total

assets |

|

4,578,402 |

4,403,494 |

4,358,589 |

4,308,067 |

4,284,311 |

|

6.9% |

| Book

value per common share |

|

46.00 |

44.89 |

43.51 |

42.23 |

41.33 |

|

11.3% |

| Loans

to deposits |

|

101.78% |

103.45% |

103.06% |

103.04% |

101.74% |

|

0.04 |

| Holding

Company Capital Ratios(6): |

|

|

|

|

|

|

|

|

| Total

risk-based capital ratio |

|

12.83% |

12.89% |

12.79% |

12.63% |

12.69% |

|

0.14 |

| Tier

1 risk-based capital ratio |

|

11.40% |

11.44% |

11.26% |

11.11% |

11.15% |

|

0.25 |

| Leverage

ratio |

|

9.05% |

8.93% |

8.72% |

8.73% |

8.79% |

|

0.26 |

| Common

equity Tier 1 ratio(7) |

|

11.03% |

11.06% |

10.88% |

10.71% |

10.75% |

|

0.28 |

| Tangible

common equity(8) |

|

8.29% |

8.37% |

8.18% |

8.02% |

7.88% |

|

0.41 |

| Asset

Quality Ratios: |

|

|

|

|

|

|

|

|

| Nonperforming

assets/total assets |

|

0.26% |

0.32% |

0.27% |

0.27% |

0.26% |

|

— |

| Classified

assets/Tier 1 capital plus allowance for credit losses |

|

3.25% |

4.28% |

3.97% |

4.35% |

4.31% |

|

(1.06) |

| Accruing

loans 30 days or more past due/loans(4) |

|

0.20% |

0.14% |

0.18% |

0.14% |

0.27% |

|

(0.07) |

| Net

charge-offs (recoveries)/average loans(4) (YTD annualized) |

|

0.01% |

0.00% |

0.00% |

0.00% |

0.00% |

|

0.01 |

| Allowance

for credit losses/loans(4) |

|

1.10% |

1.10% |

1.10% |

1.10% |

1.10% |

|

— |

| Allowance

for credit losses/nonaccrual loans |

|

378.22% |

305.65% |

364.50% |

362.35% |

378.09% |

|

0.13 |

| |

|

|

|

|

|

|

|

|

|

income

statements – Unaudited

| |

|

|

|

|

|

|

|

| |

|

Quarter

Ended |

|

Mar

31 2026 - |

| |

|

Mar

31 |

Dec

31 |

Sept

30 |

Jun

30 |

Mar

31 |

|

Mar

31 2025 |

| (in

thousands, except per share data) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

|

Change |

| Interest

income |

|

|

|

|

|

|

|

|

| Loans |

$ |

51,257 |

51,069

|

50,999

|

48,992

|

47,085

|

|

8.9% |

| Investment

securities |

|

1,399 |

1,268 |

1,342 |

1,357 |

1,403 |

|

(0.3%) |

| Federal

funds sold |

|

1,955 |

2,193 |

2,645 |

1,969 |

1,159 |

|

68.7% |

| Total

interest income |

|

54,611

|

54,530

|

54,986

|

52,318

|

49,647

|

|

10.0% |

| Interest

expense |

|

|

|

|

|

|

|

|

| Deposits |

|

21,697 |

23,052 |

24,703 |

24,300 |

23,569 |

|

(7.9%) |

| Borrowings |

|

2,655 |

2,734 |

2,754 |

2,723 |

2,695 |

|

(1.5%) |

| Total

interest expense |

|

24,352

|

25,786

|

27,457

|

27,023

|

26,264

|

|

(7.3%) |

| Net

interest income |

|

30,259 |

28,744 |

27,529 |

25,295 |

23,383 |

|

29.4% |

| Provision

for credit losses |

|

1,300 |

650 |

850 |

700 |

750 |

|

73.3% |

| Net

interest income after provision for credit losses |

|

28,959 |

28,094 |

26,679 |

24,595 |

22,633 |

|

27.9% |

| Noninterest

income |

|

|

|

|

|

|

|

|

| Mortgage

banking income |

|

1,493 |

1,689 |

1,600 |

1,569 |

1,424 |

|

4.8% |

| Service

fees on deposit accounts |

|

756 |

634 |

625 |

567 |

539 |

|

40.3% |

| ATM

and debit card income |

|

588 |

638 |

601 |

586 |

552 |

|

6.5% |

| Income

from bank owned life insurance |

|

446 |

450 |

439 |

413 |

403 |

|

10.7% |

| Loss

on sale of securities |

|

- |

(515) |

- |

- |

- |

|

0.0% |

| Other

income |

|

257 |

194 |

335 |

199 |

196 |

|

31.1% |

| Total

noninterest income |

|

3,540 |

3,090 |

3,600 |

3,334 |

3,114 |

|

13.7% |

| Noninterest

expense |

|

|

|

|

|

|

|

|

| Compensation

and benefits |

|

11,980 |

10,529 |

11,299 |

11,674 |

11,304 |

|

6.0% |

| Occupancy |

|

2,490 |

2,465 |

2,447 |

2,523 |

2,548 |

|

(2.3%) |

| Outside

service and data processing costs |

|

2,267 |

2,144 |

2,158 |

2,189 |

2,037 |

|

11.3% |

| Insurance |

|

892 |

994 |

961 |

910 |

1,010 |

|

(11.7%) |

| Professional

fees |

|

675 |

732 |

605 |

609 |

509 |

|

32.6% |

| Marketing |

|

399 |

346 |

412 |

397 |

374 |

|

6.7% |

| Other |

|

1,312 |

1,206 |

1,064 |

1,034 |

1,054 |

|

24.5% |

| Total

noninterest expenses |

|

20,015

|

18,416

|

18,946

|

19,336

|

18,836

|

|

6.3% |

| Income

before provision for income taxes |

|

12,484

|

12,768

|

11,333

|

8,593

|

6,911

|

|

80.6% |

| Income

tax expense |

|

2,597

|

2,911

|

2,671

|

2,012

|

1,645

|

|

57.9% |

| Net

income available to common shareholders |

$ |

9,887

|

9,857

|

8,662

|

6,581

|

5,266

|

|

87.7% |

| |

|

|

|

|

|

|

|

|

| Earnings

per common share – Basic |

$ |

1.21

|

1.22

|

1.07

|

0.81

|

0.65

|

|

86.2% |

| Earnings

per common share – Diluted |

|

1.19 |

1.20 |

1.06 |

0.81 |

0.65 |

|

83.1% |

| Basic

weighted average common shares |

|

8,163

|

8,106

|

8,091

|

8,090

|

8,078

|

|

1.1% |

| Diluted

weighted average common shares |

|

8,293

|

8,229

|

8,176

|

8,124

|

8,111

|

|

2.2% |

[Footnotes

to table located on page 6]

Net

interest income and margin - Unaudited

| |

|

|

|

| |

|

For

the Three Months Ended |

| |

March

31, 2026 |

December

31, 2025 |

March

31, 2025 |

| (dollars

in thousands) |

Average

Balance |

Income/

Expense |

Yield/

Rate(2) |

Average

Balance |

Income/

Expense |

Yield/

Rate(2) |

Average

Balance |

Income/

Expense |

Yield/

Rate(2) |

| |

|

|

|

|

|

|

|

|

|

| Interest-earning

assets |

|

|

|

|

|

|

|

|

|

| Federal

funds sold and interest-bearing deposits |

$ 211,039 |

$ 1,956 |

3.76% |

$ 218,291 |

$ 2,193 |

3.99% |

$ 107,821 |

$ 1,159 |

4.36% |

| Investment

securities, taxable |

141,309 |

1,368 |

3.93% |

138,616 |

1,229 |

3.52% |

143,609 |

1,361 |

3.84% |

| Investment

securities, nontaxable(1) |

6,332 |

40 |

2.58% |

7,641 |

51 |

2.63% |

7,914 |

55 |

2.80% |

| Loans(9) |

3,899,002 |

51,257 |

5.33% |

3,830,741 |

51,069 |

5.29% |

3,673,912 |

47,085 |

5.20% |

| Total

interest-earning assets |

4,257,682 |

54,621 |

5.20% |

4,195,289 |

54,542 |

5.16% |

3,933,256 |

49,660 |

5.12% |

| Noninterest-earning

assets |

156,466 |

|

|

151,515 |

|

|

157,053 |

|

|

| Total

assets |

$4,414,148 |

|

|

$4,346,804 |

|

|

$4,090,309 |

|

|

| Interest-bearing

liabilities |

|

|

|

|

|

|

|

|

|

| NOW

accounts |

$ 421,527 |

1,102 |

1.06% |

$ 360,509 |

834 |

0.92% |

$ 306,707 |

597 |

0.79% |

| Savings

& money market |

1,649,248 |

11,819 |

2.91% |

1,614,469 |

12,530 |

3.08% |

1,520,632 |

12,750 |

3.40% |

| Time

deposits |

895,101 |

8,776 |

3.98% |

937,557 |

9,688 |

4.10% |

930,282 |

10,222 |

4.46% |

| Total

interest-bearing deposits |

2,965,876 |

21,697 |

2.97% |

2,912,535 |

23,052 |

3.14% |

2,757,621 |

23,569 |

3.47% |

| FHLB

advances and other borrowings |

240,000 |

2,245 |

3.79% |

240,000 |

2,295 |

3.79% |

240,000 |

2,244 |

3.79% |

| Subordinated

debentures |

24,903 |

411 |

6.69% |

24,903 |

439 |

6.99% |

24,903 |

451 |

7.34% |

| Total

interest-bearing liabilities |

3,230,779 |

24,353 |

3.06% |

3,177,438 |

25,786 |

3.22% |

3,022,524 |

26,264 |

3.52% |

| Noninterest-bearing

liabilities |

807,686 |

|

|

806,235 |

|

|

732,761 |

|

|

| Shareholders’

equity |

375,683 |

|

|

363,131 |

|

|

335,024 |

|

|

| Total

liabilities and shareholders’ equity |

$4,414,148 |

|

|

$4,346,804 |

|

|

$4,090,309 |

|

|

| Net

interest spread |

|

|

2.15% |

|

|

1.94% |

|

|

1.60% |

| Net

interest income (tax equivalent) / margin |

|

$30,268 |

2.88% |

|

$28,756 |

2.72% |

|

$23,396 |

2.41% |

| Less:

tax-equivalent adjustment(1) |

|

9 |

|

|

12 |

|

|

13 |

|

| Net

interest income |

|

$30,259 |

|

|

$28,744 |

|

|

$23,383 |

|

[Footnotes

to table located on page 6]

Balance

sheets - Unaudited

| |

|

|

|

|

|

|

| |

|

Ending

Balance |

|

Mar

31 2026 - |

| |

|

Mar

31 |

Dec

31 |

Sept

30 |

Jun

30 |

Mar

31 |

|

Mar

31 2025 |

| (in

thousands, except per share data) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

|

Change |

| Assets |

|

|

|

|

|

|

|

|

| Cash

and cash equivalents: |

|

|

|

|

|

|

|

|

| Cash

and due from banks |

$ |

32,723 |

27,821 |

24,600 |

25,184 |

24,904 |

|

31.4% |

| Federal

funds sold |

|

228,235

|

183,473 |

178,534 |

180,834 |

263,612 |

|

(13.4%) |

| Interest-bearing

deposits with banks |

|

81,818 |

58,289 |

79,769 |

65,014 |

16,541 |

|

394.6% |

| Total

cash and cash equivalents |

|

342,776 |

269,583 |

282,903 |

271,032 |

305,057 |

|

12.4% |

| Investment

securities: |

|

|

|

|

|

|

|

|

| Investment

securities available for sale |

|

124,224 |

127,730 |

131,040 |

128,867 |

131,290 |

|

(5.4%) |

| Other

investments |

|

20,377 |

20,063 |

20,066 |

19,906 |

19,927 |

|

2.3% |

| Total

investment securities |

|

144,601 |

147,793 |

151,106 |

148,773 |

151,217 |

|

(4.4%) |

| Mortgage

loans held for sale |

|

13,723 |

11,569 |

6,906 |

10,739 |

11,524 |

|

19.1% |

| Loans

(5) |

|

3,942,219 |

3,845,124 |

3,789,021 |

3,746,841 |

3,683,919 |

|

7.0% |

| Less

allowance for credit losses |

|

(43,378) |

(42,280) |

(41,799) |

(41,285) |

(40,687) |

|

6.6% |

| Loans,

net |

|

3,898,841 |

3,802,844 |

3,747,222 |

3,705,556 |

3,643,232 |

|

7.0% |

| Bank

owned life insurance |

|

56,221 |

55,775 |

55,324 |

54,886 |

54,473 |

|

3.2% |

| Property

and equipment, net |

|

88,580 |

83,465 |

84,586 |

85,921 |

87,369 |

|

1.4% |

| Deferred

income taxes |

|

13,812 |

13,702 |

12,657 |

12,971 |

13,080 |

|

5.6% |

| Other

assets |

|

19,848 |

18,763 |

17,885 |

18,189 |

18,359 |

|

8.1% |

| Total

assets |

$ |

4,578,402 |

4,403,494 |

4,358,589 |

4,308,067 |

4,284,311 |

|

6.9% |

| Liabilities |

|

|

|

|

|

|

|

|

| Deposits

|

$ |

3,873,455 |

3,716,803 |

3,676,417 |

3,636,329

|

3,620,886 |

|

7.0% |

| FHLB

Advances |

|

240,000 |

240,000 |

240,000 |

240,000 |

240,000 |

|

0.0% |

| Subordinated

debentures |

|

24,903 |

24,903 |

24,903 |

24,903 |

24,903 |

|

0.0% |

| Other

liabilities |

|

60,631 |

53,131 |

60,921 |

61,373 |

60,924 |

|

(0.5%) |

| Total

liabilities |

|

4,198,989 |

4,034,837 |

4,002,241 |

3,962,605 |

3,946,713 |

|

6.4% |

| Shareholders’

equity |

|

|

|

|

|

|

|

|

| Preferred

stock - $.01 par value; 10,000,000 shares authorized |

|

- |

- |

- |

- |

- |

|

0.0% |

| Common

Stock - $.01 par value; 10,000,000 shares authorized |

|

82 |

82 |

82 |

82 |

82 |

|

0.0% |

| Nonvested

restricted stock |

|

(1,302) |

(1,338) |

(1,929) |

(2,774) |

(3,372) |

|

(61.4%) |

| Additional

paid-in capital |

|

127,168 |

125,924 |

125,035 |

124,839 |

124,561 |

|

2.1% |

| Accumulated

other comprehensive loss |

|

(7,865) |

(7,454) |

(8,426) |

(9,609) |

(10,016) |

|

(21.5%) |

| Retained

earnings |

|

261,330 |

251,443 |

241,586 |

232,924 |

226,343 |

|

15.5% |

| Total

shareholders’ equity |

|

379,413 |

368,657 |

356,348 |

345,462 |

337,598 |

|

12.4% |

| Total

liabilities and shareholders’ equity |

$ |

4,578,402 |

4,403,494 |

4,358,589 |

4,308,067 |

4,284,311 |

|

6.9% |

| |

|

|

|

|

|

|

|

|

| Common

Stock |

|

|

|

|

|

|

|

|

| Book

value per common share |

$ |

46.00 |

44.89 |

43.51 |

42.23 |

41.33 |

|

11.3% |

| Stock

price: |

|

|

|

|

|

|

|

|

| High |

|

61.08 |

55.50 |

45.54 |

38.51 |

38.50 |

|

58.6% |

| Low |

|

51.26 |

41.15 |

38.74 |

30.61 |

31.88 |

|

60.8% |

| Period

end |

|

54.50 |

51.52 |

44.12 |

38.03 |

32.92 |

|

65.6% |

| Common

shares outstanding |

|

8,248 |

8,213 |

8,189 |

8,181 |

8,169 |

|

1.0% |

| |

|

|

|

|

|

|

|

|

|

[Footnotes

to table located on page 6]

Asset

quality measures - Unaudited

| |

|

Quarter

Ended |

| |

|

March

31 |

December

31 |

September

30 |

June

30 |

March

31 |

| (dollars

in thousands) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

| Nonperforming

Assets |

|

|

|

|

|

|

| Commercial |

|

|

|

|

|

|

| Owner

occupied RE |

$ |

2,317 |

259 |

262 |

- |

- |

| Non-owner

occupied RE |

|

1,712 |

6,917 |

6,911 |

6,941 |

6,950 |

| Commercial

business |

|

909 |

189 |

195 |

717 |

1,087 |

| Consumer |

|

|

|

|

|

|

| Real

estate |

|

5,786 |

5,763 |

3,394 |

3,028 |

2,414 |

| Home

equity |

|

745 |

705 |

705 |

708 |

310 |

| Total

nonaccrual loans |

|

11,469 |

13,833 |

11,467 |

11,394 |

10,761 |

| Other

real estate owned |

|

475 |

275 |

275

|

275 |

275 |

| Total

nonperforming assets |

$ |

11,944 |

14,108 |

11,742

|

11,669 |

11,036 |

| Nonperforming

assets as a percentage of: |

|

|

|

|

|

|

| Total

assets |

|

0.26% |

0.32% |

0.27% |

0.27% |

0.26% |

| Total

loans |

|

0.30% |

0.37% |

0.31% |

0.31% |

0.30% |

| Classified

assets/Tier 1 capital plus allowance for credit losses |

|

3.14% |

4.22% |

3.90% |

4.28% |

4.24% |

| Accruing

loans 30 days or more past due/loans(4) |

|

0.20% |

0.14% |

0.18% |

0.14% |

0.27% |

| |

|

Quarter

Ended |

| |

|

March

31 |

December

31 |

September

30 |

June

30 |

March

31 |

| (dollars

in thousands) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

| Allowance

for Credit Losses |

|

|

|

|

|

|

| Balance,

beginning of period |

$ |

42,280 |

41,799 |

41,285 |

40,687 |

39,914 |

| Loans

charged-off |

|

(78) |

(150) |

(55) |

(68) |

(78) |

| Recoveries

of loans previously charged-off |

|

26 |

81 |

69 |

16 |

101 |

| Net

loans (charged-off) recovered |

|

(52) |

(69) |

14 |

(52) |

23 |

| Provision

for credit losses |

|

1,150 |

550 |

500 |

650 |

750 |

| Balance,

end of period |

$ |

43,378 |

42,280 |

41,799 |

41,285 |

40,687 |

| Allowance

for credit losses to gross loans |

|

1.10% |

1.10% |

1.10% |

1.10% |

1.10% |

| Allowance

for credit losses to nonaccrual loans |

|

378.22% |

305.65% |

364.50% |

362.35% |

378.09% |

| Net

charge-offs (recoveries) to average loans QTD (annualized) |

|

0.01

% |

0.01

% |

0.00% |

0.01% |

0.00

% |

[Footnotes

to table located on page 6]

LOAN

COMPOSITION - Unaudited

| |

|

|

|

|

|

|

|

| |

|

Quarter

Ended |

|

Qtr |

|

Yr |

| |

|

March

31 |

December 31 |

September 30 |

June

30 |

March

31 |

|

Over Qtr |

|

Over Yr |

| (dollars

in thousands) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

|

$ Change |

|

$ Change |

| Commercial |

|

|

|

|

|

|

|

|

|

|

| Owner

occupied RE |

$ |

759,602 |

736,979 |

705,383 |

686,424 |

673,865 |

|

22,623 |

|

85,737 |

| Non-owner

occupied RE |

|

950,696 |

956,812 |

943,304 |

939,163 |

926,246 |

|

(6,116) |

|

24,450 |

| Construction |

|

69,463 |

63,666 |

71,928 |

68,421 |

90,021 |

|

5,797 |

|

(20,558) |

| Business |

|

677,742 |

619,667 |

604,411 |

589,661 |

561,337 |

|

58,075 |

|

116,405 |

| Total

commercial loans |

|

2,457,503 |

2,377,124 |

2,325,026 |

2,283,669 |

2,251,469 |

|

80,379 |

|

206,034 |

| Consumer |

|

|

|

|

|

|

|

|

|

|

| Real

estate |

|

1,148,129 |

1,153,285 |

1,159,693 |

1,164,187 |

1,147,357 |

|

(5,156) |

|

772 |

| Home

equity |

|

262,530 |

248,685 |

239,996 |

234,608 |

223,061 |

|

13,845 |

|

39,469 |

| Construction |

|

33,879 |

24,997 |

25,842 |

25,210 |

23,540 |

|

8,882 |

|

10,339 |

| Other |

|

40,178 |

41,033 |

38,464 |

39,167 |

38,492 |

|

(855) |

|

1,686 |

| Total

consumer loans |

|

1,484,716 |

1,468,000 |

1,463,995 |

1,463,172 |

1,432,450 |

|

16,716 |

|

52,266 |

| Total

gross loans, net of deferred fees |

|

3,942,219 |

3,845,124 |

3,789,021 |

3,746,841 |

3,683,919 |

|

97,095 |

|

258,300 |

| Less—allowance

for credit losses |

|

(43,378) |

(42,280) |

(41,799) |

(41,285) |

(40,687) |

|

(1,098) |

|

(2,691) |

| Total

loans, net |

$ |

3,898,841 |

3,802,844 |

3,747,222 |

3,705,556 |

3,643,232 |

|

95,997 |

|

255,609 |

| |

|

|

|

|

|

|

|

|

|

|

| Yield

on average loans |

|

5.33% |

5.29% |

5.35% |

5.28% |

5.20% |

|

n/a |

|

n/a |

DEPOSIT

COMPOSITION - Unaudited

| |

|

|

|

|

|

|

|

| |

|

Quarter

Ended |

|

Qtr |

|

Yr |

| |

|

March

31 |

December

31 |

September

30 |

June

30 |

March

31 |

|

Over Qtr |

|

Over Yr |

| (dollars

in thousands) |

|

2026 |

2025 |

2025 |

2025 |

2025 |

|

$ Change |

|

$ Change |

| Non-interest

bearing |

$ |

799,692 |

732,287 |

736,518 |

761,492 |

671,609 |

|

67,405 |

|

128,083 |

| Interest

bearing: |

|

|

|

|

|

|

|

|

|

|

| NOW

accounts |

|

495,657 |

423,270 |

343,615 |

341,903 |

371,052 |

|

72,387 |

|

124,605 |

| Money

market accounts |

|

1,652,125 |

1,573,039 |

1,572,738 |

1,537,400 |

1,563,181 |

|

79,086 |

|

88,944 |

| Savings |

|

30,332 |

29,470 |

29,381 |

32,334 |

32,945 |

|

862 |

|

(2,613) |

| Time

deposits, less than $250,000 |

|

170,496 |

180,783 |

202,353 |

194,064 |

181,407 |

|

(10,287) |

|

(10,911) |

| Time

deposits, $250,000 and over(10) |

|

725,153 |

777,954 |

791,812 |

769,136 |

800,692 |

|

(52,801) |

|

(75,539) |

| Total

deposits |

$ |

3,873,455 |

3,716,803 |

3,676,417 |

3,636,329 |

3,620,886 |

|

156,652 |

|

252,569 |

| |

|

|

|

|

|

|

|

|

|

|

| Total

retail deposits |

|

3,371,721 |

3,163,914 |

3,108,411 |

3,075,631 |

3,020,392 |

|

207,807 |

|

351,329 |

| Total

wholesale deposits |

|

501,734 |

552,889 |

568,006 |

560,697 |

600,494 |

|

(51,155) |

|

(98,760) |

| Cost

of average deposits |

|

2.37% |

2.50% |

2.69% |

2.75% |

2.78% |

|

n/a |

|

n/a |

| Cost

of average retail deposits |

|

2.06% |

2.18% |

2.36% |

2.42% |

2.43% |

|

n/a |

|

n/a |

| Loans

to deposits |

|

101.78% |

103.45% |

103.06% |

103.04% |

101.74% |

|

n/a |

|

n/a |

| |

|

|

|

|

|

|

|

|

|

|

|

| Footnotes to tables: |

| (1) |

The tax-equivalent adjustment to net interest income adjusts

the yield for assets earning tax-exempt income to a comparable yield on a taxable basis. |

| (2) |

Annualized for the respective three-month period. |

| (3) |

Noninterest expense divided by the sum of net interest income

and noninterest income. |

| (4) |

Excludes mortgage loans held for sale. |

| (5) |

Excludes out of market (wholesale) deposits totaling $501.7 million. |

| (6) |

March 31, 2026 ratios are preliminary. |

| (7) |

The common equity Tier 1 ratio is calculated as the sum of common

equity divided by risk-weighted assets. |

| (8) | The

tangible common equity ratio is calculated as total equity less preferred stock divided by total assets. |

| (9) | Includes

mortgage loans held for sale. |

| (10) | Includes

out of market deposits |

About

Southern First Bancshares

Southern

First Bancshares, Inc., Greenville, South Carolina is a registered bank holding company incorporated under the laws of South Carolina.

The company’s wholly owned subsidiary, Southern First Bank, is the second largest bank headquartered in South Carolina. Southern

First Bank has been providing financial services since 1999 and now operates in 12 locations in the Greenville, Columbia, and Charleston

markets of South Carolina as well as the Charlotte, Triangle and Triad regions of North Carolina and Atlanta, Georgia. Southern First

Bancshares has consolidated assets of approximately $4.6 billion and its common stock is traded on The NASDAQ Global Market under the

symbol “SFST.” More information can be found at www.southernfirst.com.

FORWARD-LOOKING STATEMENTS

Certain

statements in this news release contain “forward-looking statements" within the meaning of the Private Securities Litigation

Reform Act of 1995, such as statements relating to future plans and expectations, and are thus prospective. Such forward-looking

statements are identified by words such as “believe,” “expect,” “anticipate,” “estimate,”

“preliminary”, “intend,” “plan,” “target,” “continue,” “lasting,”

and “project,” as well as similar expressions. Such statements are subject to risks, uncertainties, and other factors

which could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Although

we believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove to be inaccurate. Therefore,

we can give no assurance that the results contemplated in the forward-looking statements will be realized. The inclusion of this

forward-looking information should not be construed as a representation by our company or any person that the future events, plans, or

expectations contemplated by our company will be achieved.

The

following factors, among others, could cause actual results to differ materially from the anticipated results or other expectations expressed

in the forward-looking statements: (1) competitive pressures among depository and other financial institutions may increase significantly

and have an effect on pricing, spending, third-party relationships and revenues; (2) the strength of the United States economy in general

and the strength of the local economies in which the company conducts operations may be different than expected; (3) the rate of delinquencies

and amounts of charge-offs, the level of allowance for credit loss, the rates of loan and deposit growth as well as pricing of each product,

or adverse changes in asset quality in our loan portfolio, which may result in increased credit risk-related losses and expenses; (4)

changes in legislation, regulation, policies, or administrative practices, whether by judicial, governmental, or legislative action,

including, but not limited to, changes affecting oversight of the financial services industry or consumer protection; (5) the impact

of changes to Congress and the office of the President on the regulatory landscape and capital markets; (6) adverse conditions in the

stock market, the public debt market and other capital markets (including changes in interest rate conditions) could continue to have

a negative impact on the company; (7) changes in interest rates, which may continue to affect the company’s net income, interest

expense, prepayment penalty income, mortgage banking income, and other future cash flows, or the market value of the company’s

assets, including its investment securities; (8) trade wars, government shutdowns, or a potential recession which may cause adverse risk

to the overall economy, and could indirectly pose challenges to our clients and to our business; (9) any increase in FDIC assessments

which have increased and may continue to increase our cost of doing business; and (10) changes in accounting principles, policies, practices,

or guidelines. Additional factors that could cause our results to differ materially from those described in the forward-looking

statements can be found in our reports (such as Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form

8-K) filed with the SEC and available at the SEC’s Internet site (http://www.sec.gov). All subsequent written and oral forward-looking

statements concerning the company or any person acting on its behalf are expressly qualified in its entirety by the cautionary statements

above. We do not undertake any obligation to update any forward-looking statement to reflect circumstances or events that occur after

the date the forward-looking statements are made, except as required by law.

MEDIA CONTACT:

ART SEAVER 864-679-9010

FINANCIAL CONTACT:

CHRIS ZYCH 864-679-9070

WEB SITE: www.southernfirst.com

SOURCE: Southern First

Bancshares, Inc.

FIRST QUARTER 2026 INVESTOR PRESENTATION April 21, 2026 Exhibit 99.2

FORWARD - LOOKING STATEMENTS Greensboro Raleigh Charlotte Charleston Summerville Greenville Columbia Atlanta GEORGI A South Carolina North Carolina 2 During the course of this presentation, management may make projections and forward - looking statements regarding events or the future financial performance of Southern First Bancshares, Inc. We wish to caution you that these forward - looking statements involve certain risks and uncertainties, including a variety of factors (including a downturn in the economy, greater than expected interest and non - interest expenses, increased competition, fluctuations in interest rates, regulatory actions, excessive loan losses and other factors) that may cause Southern First’s actual results to differ materially from the anticipated results expressed or implied in these forward - looking statements. Therefore, we can give no assurance that the results contemplated in the forward - looking statements will be realized. Investors are cautioned not to place undue reliance on these forward - looking statements and are advised to review the risk factors that may affect Southern First’s operating results in documents filed by Southern First Bancshares, Inc. with the Securities and Exchange Commission, including the annual report on Form 10 - K and other required filings. Southern First assumes no duty to update the forward - looking statements made in this presentation.

Company Overview A CORPORATE PROFILE □ Headquartered in Greenville, SC x Founded in 2000 □ Efficient branch footprint in some of the most dynamic markets in the Southeast x 12 branches located in 8 fast - growing Southeast metropolitan markets □ Relationship - driven commercial banking model x Targeted clients include small to medium sized businesses, business owners and professionals x Supported by significant investment in technology □ Focused on organic growth versus M&A □ Simple business model OPERATING MARKETS Greensboro Raleigh Charlotte Charleston Summerville Greenville Columbia Atlanta GEORGI A South Carolina North Carolina Relationship Banking with 25+ Years of Service Excellence 3

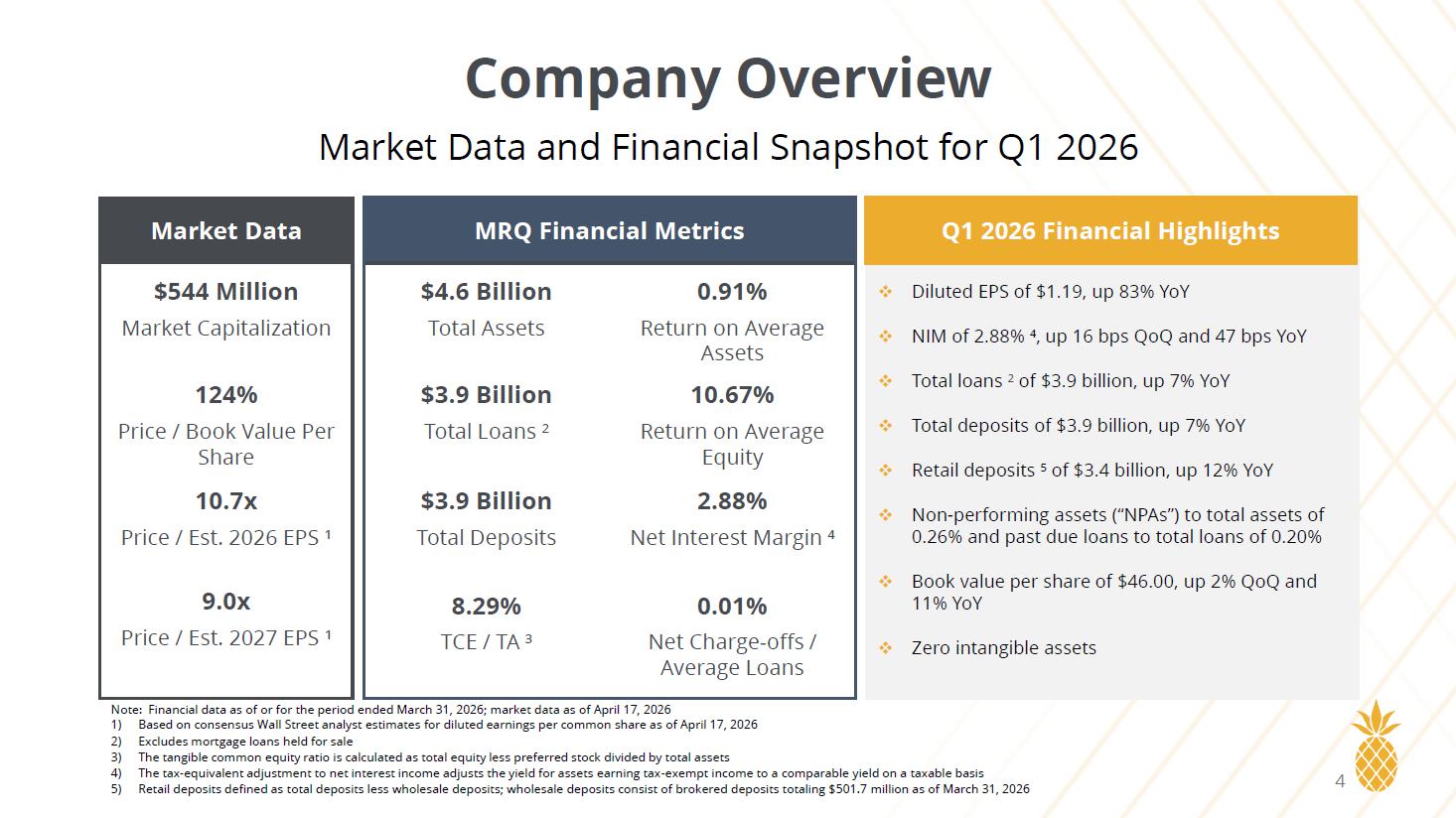

Company Overview Greensboro Raleigh Charlotte Charleston Summerville Greenville Columbia Atlanta GEORGI A South Carolina North Carolina Market Data and Financial Snapshot for Q1 2026 Market Data MRQ Financial Metrics Q1 2026 Financial Highlights □ Diluted EPS of $1.19, up 83% YoY □ NIM of 2.88% ⁴, up 16 bps QoQ and 47 bps YoY □ Total loans ² of $3.9 billion, up 7% YoY □ Total deposits of $3.9 billion, up 7% YoY □ Retail deposits ⁵ of $3.4 billion, up 12% YoY □ Non - performing assets (“NPAs”) to total assets of 0.26% and past due loans to total loans of 0.20% □ Book value per share of $46.00, up 2% QoQ and 11% YoY □ Zero intangible assets $544 Million Market Capitalization 124% Price / Book Value Per Share 10.7x Price / Est. 2026 EPS ¹ 9.0x Price / Est. 2027 EPS ¹ $4.6 Billion Total Assets $3.9 Billion Total Loans ² $3.9 Billion Total Deposits 8.29% TCE / TA ³ 0.91% Return on Average Assets 10.67% Return on Average Equity 2.88% Net Interest Margin ⁴ 0.01% Net Charge - offs / Average Loans Note: Financial data as of or for the period ended March 31, 2026; market data as of April 17, 2026 1) Based on consensus Wall Street analyst estimates for diluted earnings per common share as of April 17, 2026 2) Excludes mortgage loans held for sale 3) The tangible common equity ratio is calculated as total equity less preferred stock divided by total assets 4) The tax - equivalent adjustment to net interest income adjusts the yield for assets earning tax - exempt income to a comparable yiel d on a taxable basis 5) Retail deposits defined as total deposits less wholesale deposits; wholesale deposits consist of brokered deposits totaling $ 501 .7 million as of March 31, 2026 4

Company Overview Key Investment Highlights Profitability momentum highlighted by continued balance sheet repricing opportunities, improving cost of funds, and efficient delivery model Experienced, founder - led management team with 25+ year focus on creating a unique client experience and producing returns for shareholders Strong asset quality results driven by a robust risk management culture and a focus on relationship banking Long track record and demonstrated ability to produce balance sheet growth organically and through de novo market expansion Operating in highly attractive dynamic Southeast metro markets, resulting in scarcity value and a differentiated growth profile 5

Company Overview Who We Are Our Mission Our mission is to impact lives in the communities we serve Our Culture We focus on the things that matter most: family, community, and teamwork Our Purpose We exist to enable dreams, earn trust, and exceed expectations Relationship driven with a focus on exceptional service and authentic hospitality Embrace technology and the evolution of our industry Committed to organic growth versus M&A Superb at managing risk – credit risk and enterprise risk Highly efficient delivery system – branch light footprint Located in major metro, high - growth Southeastern markets Dedicated to an entrepreneurial, team - focused culture that results in high career satisfaction Utilize a strong relationship mortgage component to augment noninterest income Proven and driven leadership team Lead and operate with wisdom and clarity 6

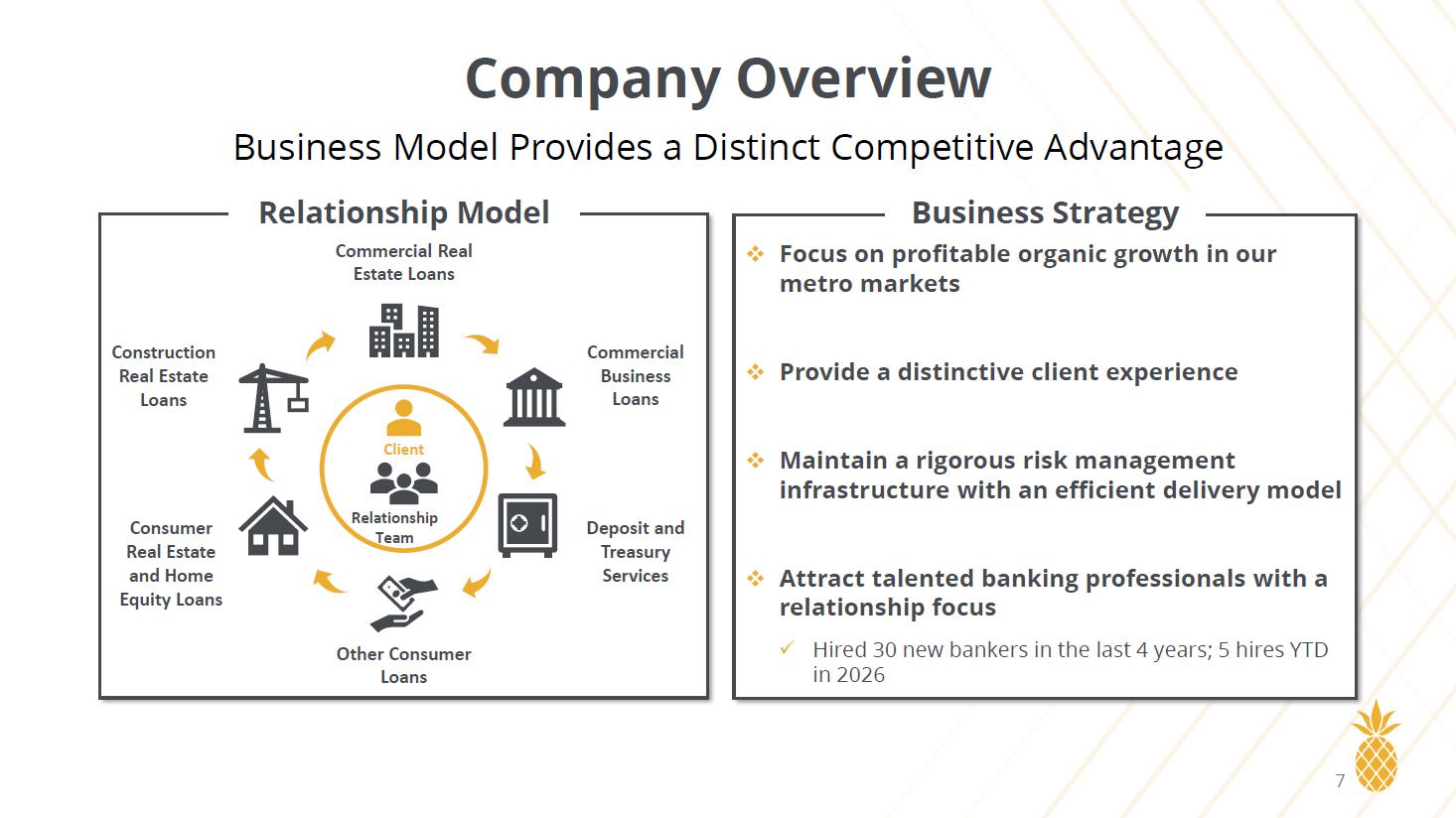

Company Overview Business Model Provides a Distinct Competitive Advantage A Relationship Model Commercial Real Estate Loans Commercial Business Loans Deposit and Treasury Services Other Consumer Loans Consumer Real Estate and Home Equity Loans Construction Real Estate Loans Relationship Team Client A Business Strategy □ Focus on profitable organic growth in our metro markets □ Provide a distinctive client experience □ Maintain a rigorous risk management infrastructure with an efficient delivery model □ Attract talented banking professionals with a relationship focus x Hired 30 new bankers in the last 4 years; 5 hires YTD in 2026 7

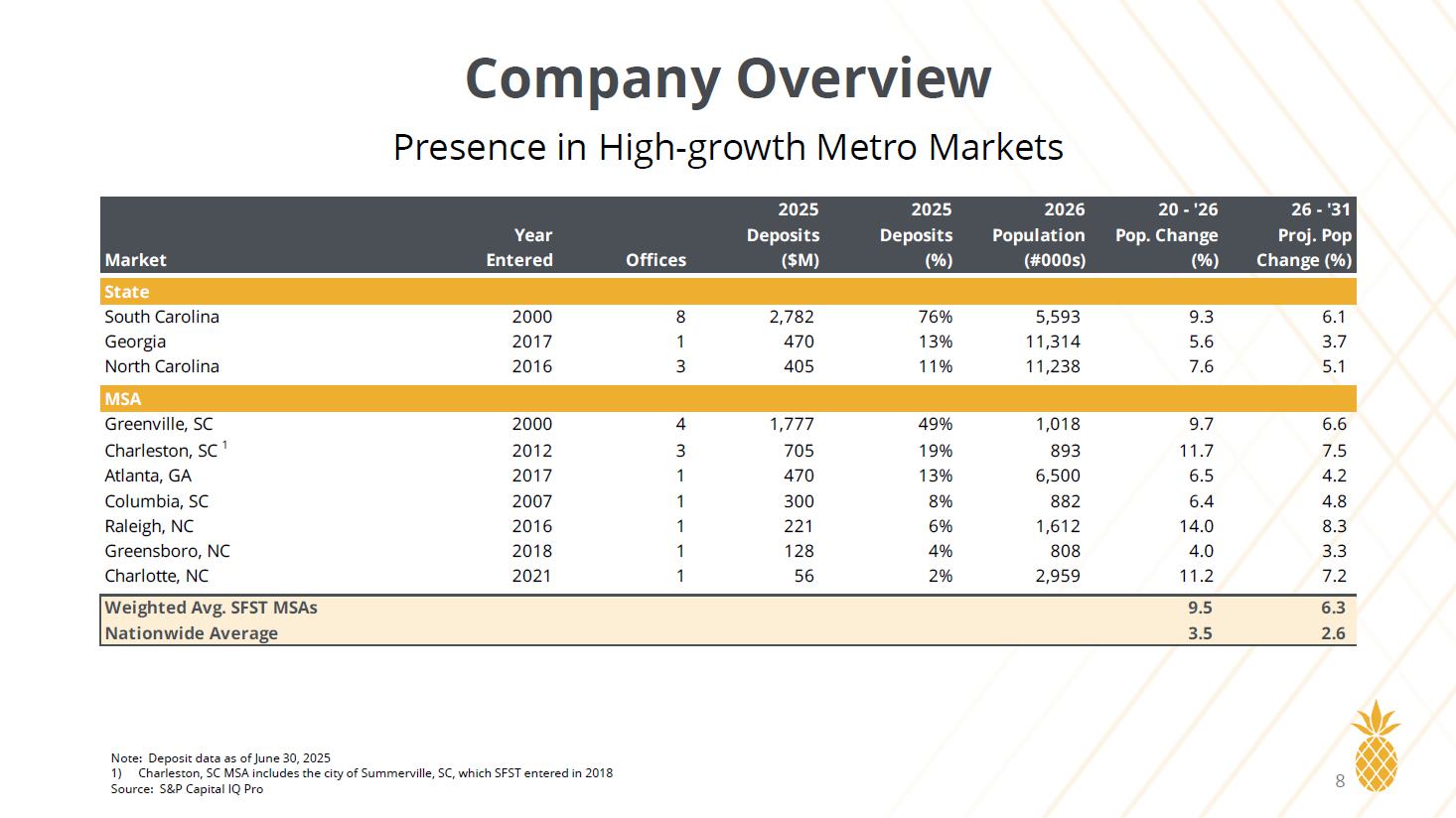

Company Overview Presence in High - growth Metro Markets 2025 2025 2026 20 - '26 26 - '31 Year Deposits Deposits Population Pop. Change Proj. Pop Market Entered Offices ($M) (%) (#000s) (%) Change (%) State South Carolina 2000 8 2,782 76% 5,593 9.3 6.1 Georgia 2017 1 470 13% 11,314 5.6 3.7 North Carolina 2016 3 405 11% 11,238 7.6 5.1 MSA Greenville, SC 2000 4 1,777 49% 1,018 9.7 6.6 Charleston, SC 1 2012 3 705 19% 893 11.7 7.5 Atlanta, GA 2017 1 470 13% 6,500 6.5 4.2 Columbia, SC 2007 1 300 8% 882 6.4 4.8 Raleigh, NC 2016 1 221 6% 1,612 14.0 8.3 Greensboro, NC 2018 1 128 4% 808 4.0 3.3 Charlotte, NC 2021 1 56 2% 2,959 11.2 7.2 Weighted Avg. SFST MSAs 9.5 6.3 Nationwide Average 3.5 2.6 Note: Deposit data as of June 30, 2025 1) Charleston, SC MSA includes the city of Summerville, SC, which SFST entered in 2018 Source: S&P Capital IQ Pro 8

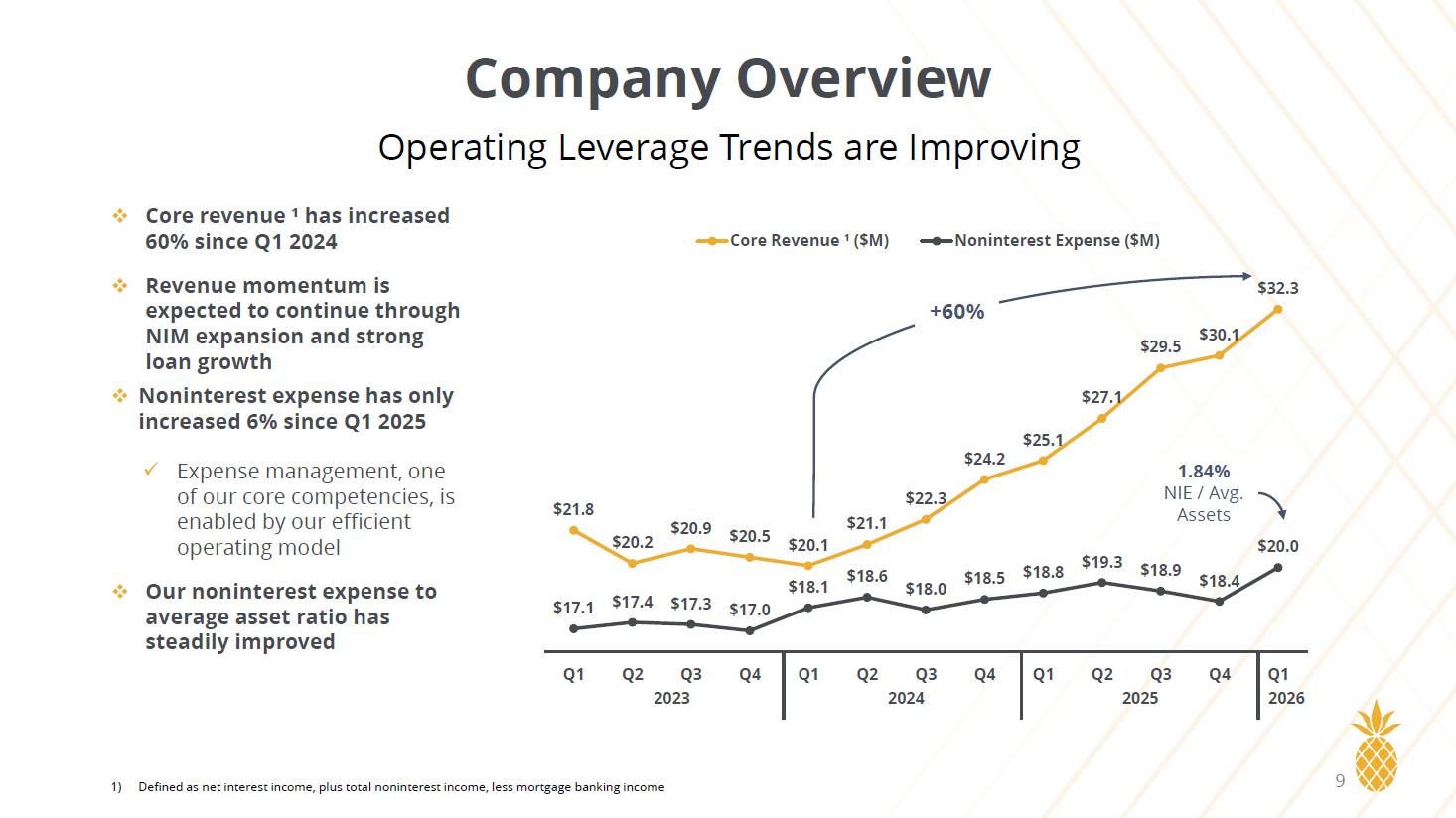

$21.8 $20.2 $20.9 $20.5 $20.1 $21.1 $22.3 $24.2 $25.1 $27.1 $29.5 $30.1 $32.3 $17.1 $17.4 $17.3 $17.0 $18.1 $18.6 $18.0 $18.5 $18.8 $19.3 $18.9 $18.4 $20.0 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Core Revenue ¹ ($M) Noninterest Expense ($M) □ Core revenue ¹ has increased 60% since Q1 2024 □ Revenue momentum is expected to continue through NIM expansion and strong loan growth □ Noninterest expense has only increased 6% since Q1 2025 x Expense management, one of our core competencies, is enabled by our efficient operating model □ Our noninterest expense to average asset ratio has steadily improved Company Overview Operating Leverage Trends are Improving 1) Defined as net interest income, plus total noninterest income, less mortgage banking income 2023 2024 2025 2026 1.84% NIE / Avg. Assets +60% 9

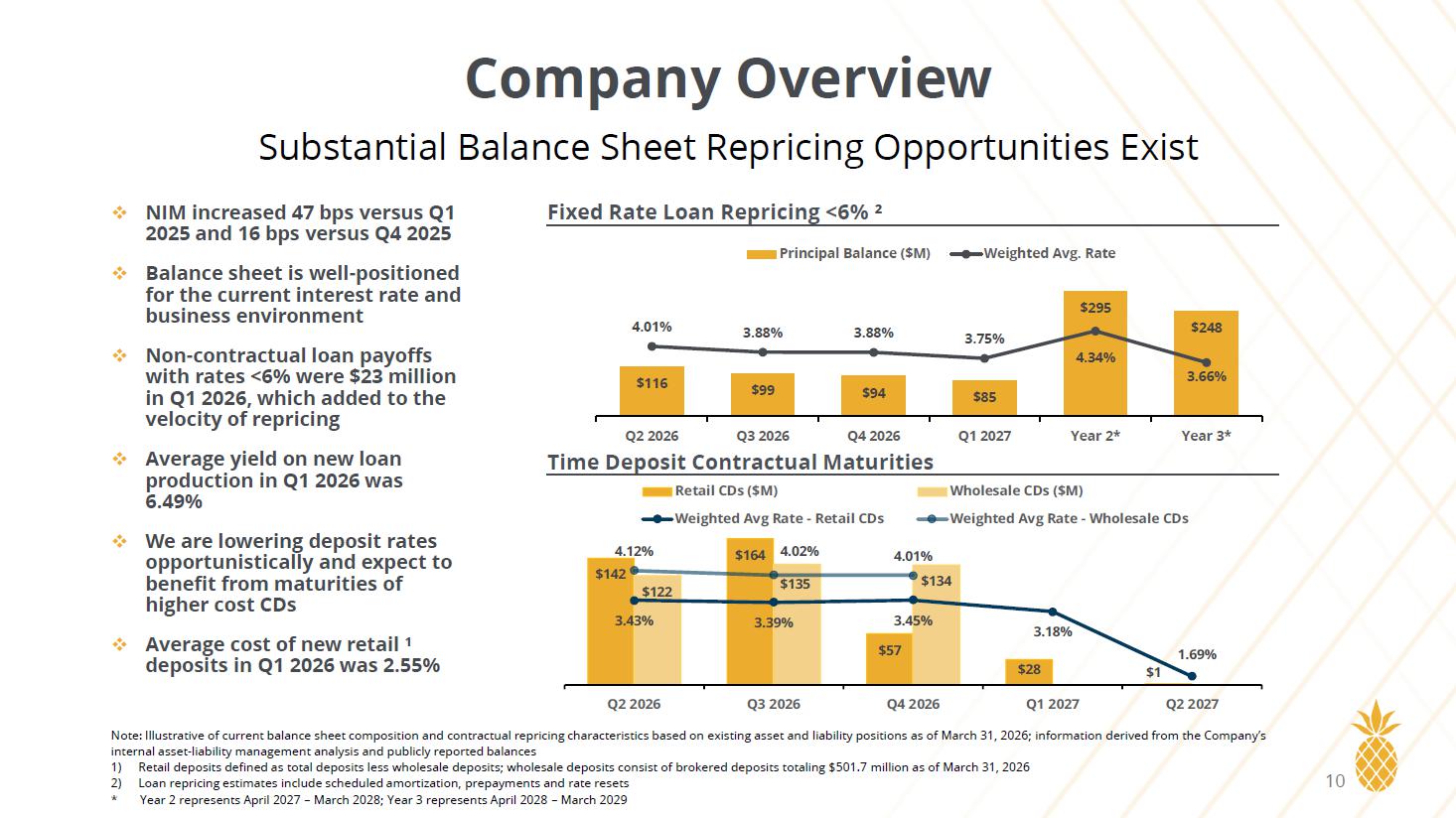

$142 $164 $57 $28 $1 $122 $135 $134 3.43% 3.39% 3.45% 3.18% 1.69% 4.12% 4.02% 4.01% Q2 2026 Q3 2026 Q4 2026 Q1 2027 Q2 2027 Retail CDs ($M) Wholesale CDs ($M) Weighted Avg Rate - Retail CDs Weighted Avg Rate - Wholesale CDs □ NIM increased 47 bps versus Q1 2025 and 16 bps versus Q4 2025 □ Balance sheet is well - positioned for the current interest rate and business environment □ Non - contractual loan payoffs with rates <6% were $23 million in Q1 2026, which added to the velocity of repricing □ Average yield on new loan production in Q1 2026 was 6.49% □ We are lowering deposit rates opportunistically and expect to benefit from maturities of higher cost CDs □ Average cost of new retail ¹ deposits in Q1 2026 was 2.55% Company Overview Substantial Balance Sheet Repricing Opportunities Exist Note: Illustrative of current balance sheet composition and contractual repricing characteristics based on existing asset and li ability positions as of March 31, 2026; information derived from the Company’s internal asset - liability management analysis and publicly reported balances 1) Retail deposits defined as total deposits less wholesale deposits; wholesale deposits consist of brokered deposits totaling $ 501 .7 million as of March 31, 2026 2) Loan repricing estimates include scheduled amortization, prepayments and rate resets * Year 2 represents April 2027 – March 2028; Year 3 represents April 2028 – March 2029 Fixed Rate Loan Repricing <6% ² Time Deposit Contractual Maturities 10 $116 $99 $94 $85 $295 $248 4.01% 3.88% 3.88% 3.75% 4.34% 3.66% Q2 2026 Q3 2026 Q4 2026 Q1 2027 Year 2* Year 3* Principal Balance ($M) Weighted Avg. Rate

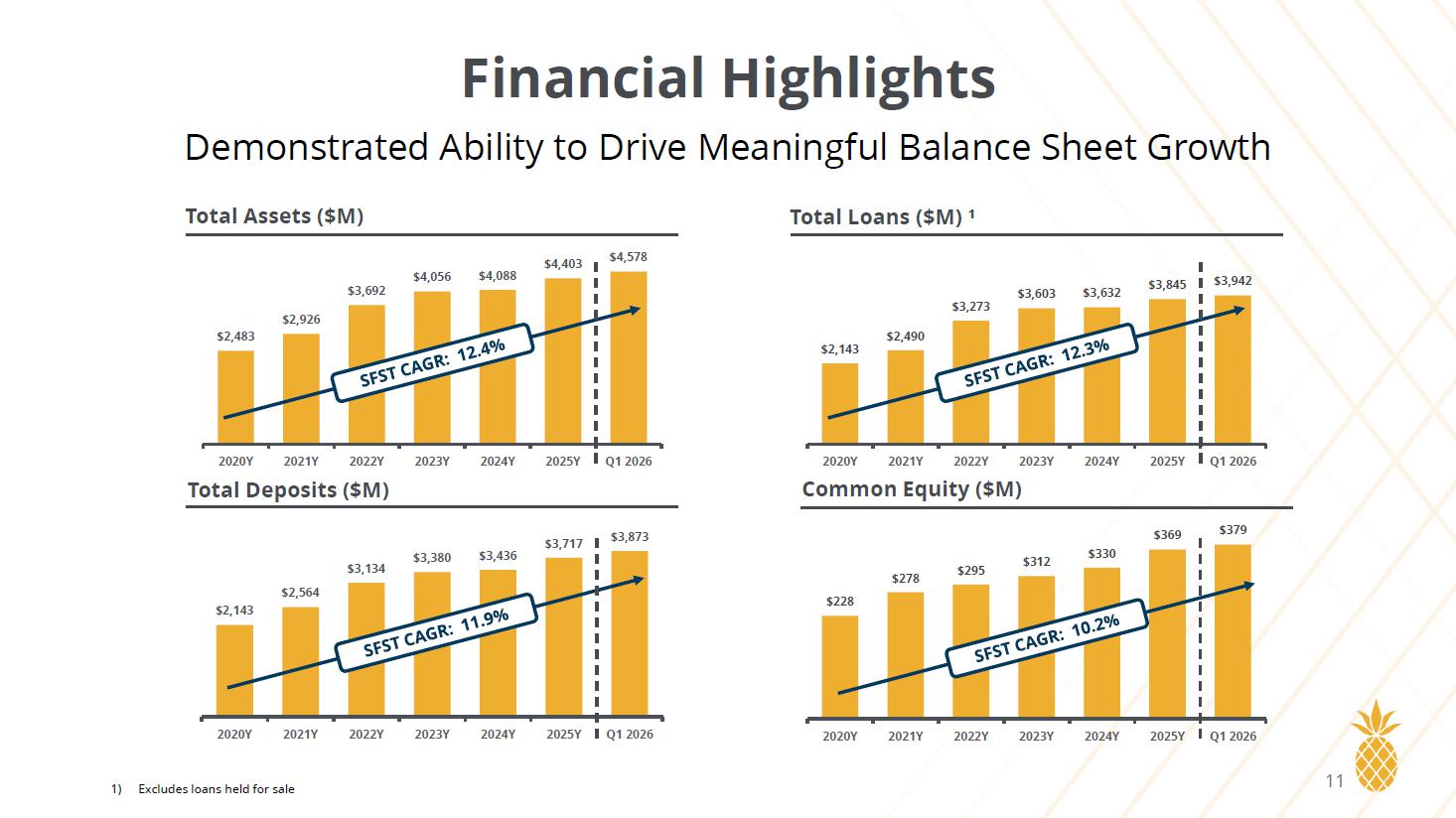

Financial Highlights Demonstrated Ability to Drive Meaningful Balance Sheet Growth 1) Excludes loans held for sale Total Assets ($M) Total Loans ($M) ¹ Common Equity ($M) $2,483 $2,926 $3,692 $4,056 $4,088 $4,403 $4,578 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 $2,143 $2,490 $3,273 $3,603 $3,632 $3,845 $3,942 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 $228 $278 $295 $312 $330 $369 $379 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 Total Deposits ($M) $2,143 $2,564 $3,134 $3,380 $3,436 $3,717 $3,873 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 11

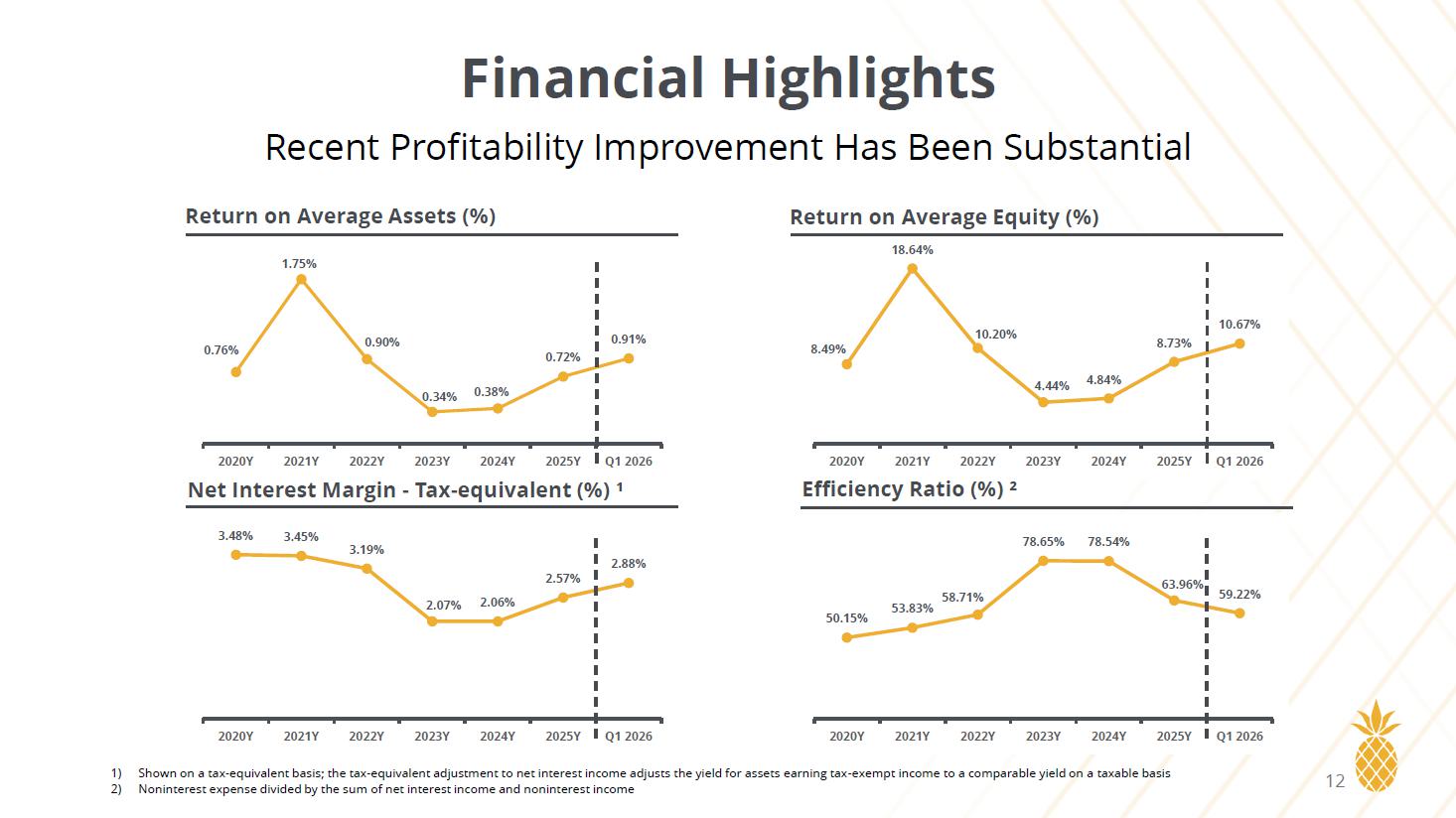

Financial Highlights Recent Profitability Improvement Has Been Substantial 1) Shown on a tax - equivalent basis; the tax - equivalent adjustment to net interest income adjusts the yield for assets earning tax - e xempt income to a comparable yield on a taxable basis 2) Noninterest expense divided by the sum of net interest income and noninterest income Return on Average Assets (%) Return on Average Equity (%) Efficiency Ratio (%) ² 0.76% 1.75% 0.90% 0.34% 0.38% 0.72% 0.91% 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 8.49% 18.64% 10.20% 4.44% 4.84% 8.73% 10.67% 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 50.15% 53.83% 58.71% 78.65% 78.54% 63.96% 59.22% 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 Net Interest Margin - Tax - equivalent (%) ¹ 3.48% 3.45% 3.19% 2.07% 2.06% 2.57% 2.88% 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 12

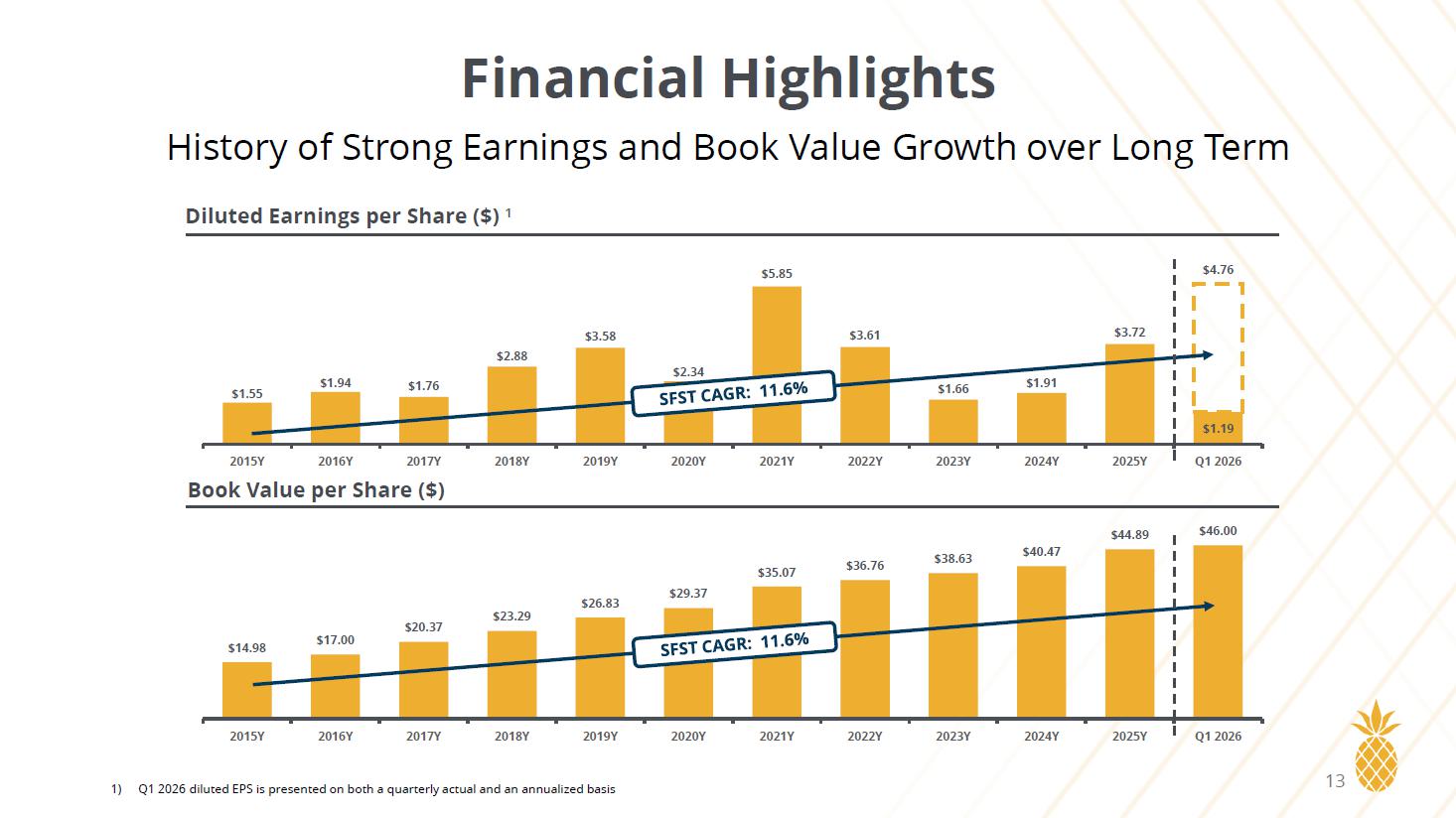

Financial Highlights History of Strong Earnings and Book Value Growth over Long Term 1) Q1 2026 diluted EPS is presented on both a quarterly actual and an annualized basis Diluted Earnings per Share ($) ¹ $1.55 $1.94 $1.76 $2.88 $3.58 $2.34 $5.85 $3.61 $1.66 $1.91 $3.72 $1.19 $4.76 2015Y 2016Y 2017Y 2018Y 2019Y 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 Book Value per Share ($) $14.98 $17.00 $20.37 $23.29 $26.83 $29.37 $35.07 $36.76 $38.63 $40.47 $44.89 $46.00 2015Y 2016Y 2017Y 2018Y 2019Y 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 13

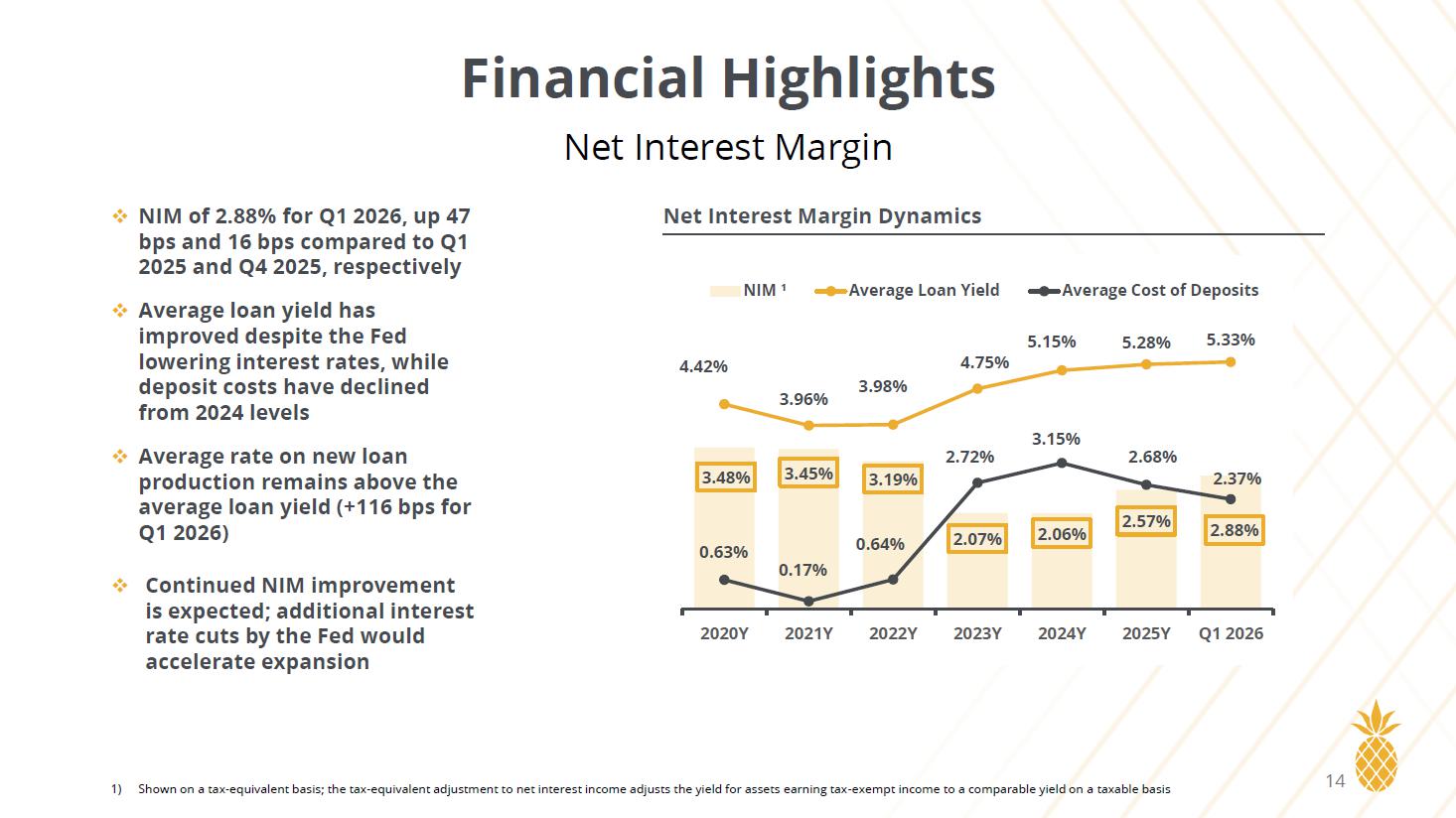

□ NIM of 2.88% for Q1 2026, up 47 bps and 16 bps compared to Q1 2025 and Q4 2025, respectively □ Average loan yield has improved despite the Fed lowering interest rates, while deposit costs have declined from 2024 levels □ Average rate on new loan production remains above the average loan yield (+116 bps for Q1 2026) □ Continued NIM improvement is expected; additional interest rate cuts by the Fed would accelerate expansion Financial Highlights Net Interest Margin 1) Shown on a tax - equivalent basis; the tax - equivalent adjustment to net interest income adjusts the yield for assets earning tax - e xempt income to a comparable yield on a taxable basis Net Interest Margin Dynamics 14 3.48% 3.45% 3.19% 2.07% 2.06% 2.57% 2.88% 4.42% 3.96% 3.98% 4.75% 5.15% 5.28% 5.33% 0.63% 0.17% 0.64% 2.72% 3.15% 2.68% 2.37% 2020Y 2021Y 2022Y 2023Y 2024Y 2025Y Q1 2026 NIM ¹ Average Loan Yield Average Cost of Deposits

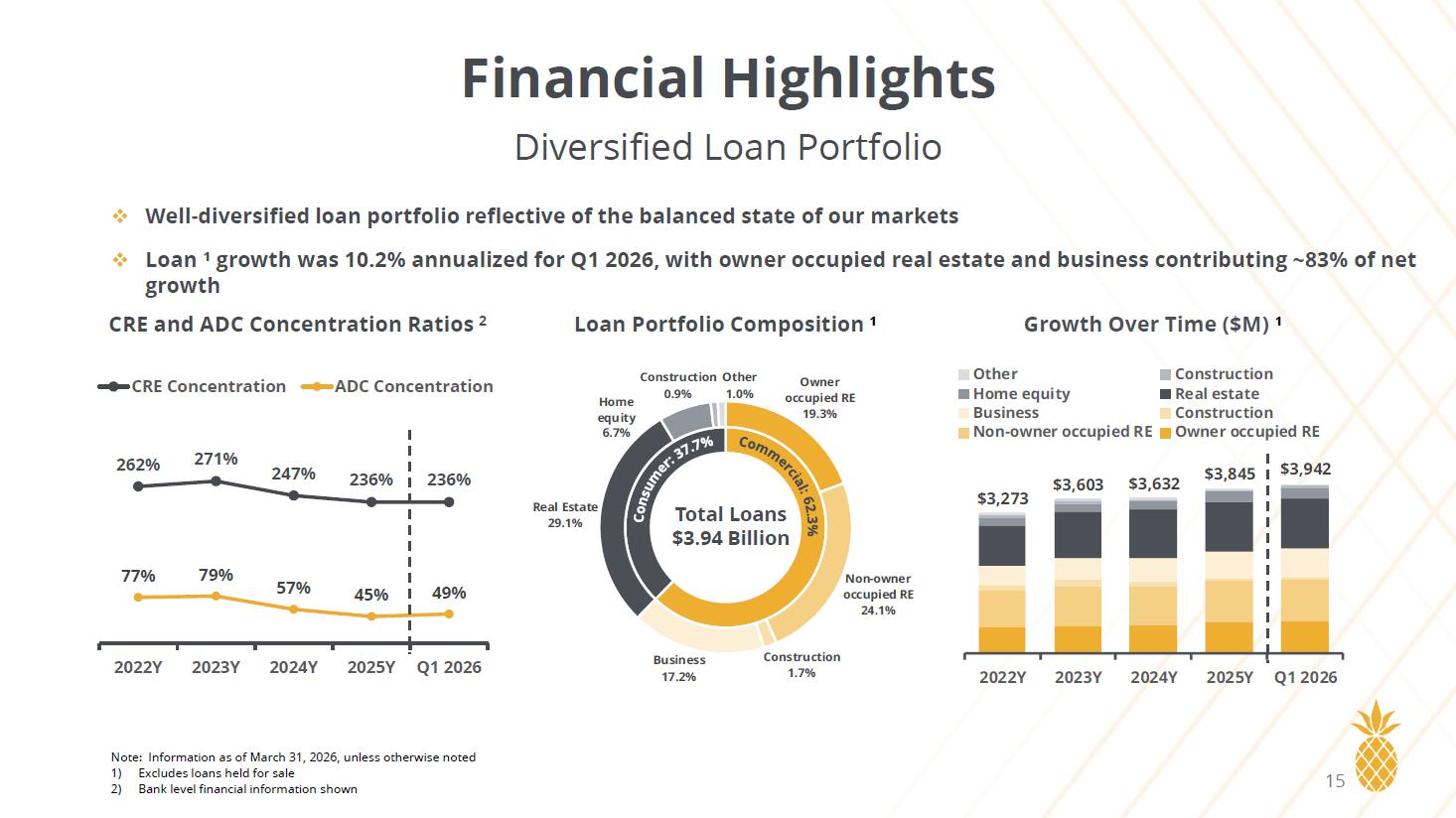

262% 271% 247% 236% 236% 77% 79% 57% 45% 49% 2022Y 2023Y 2024Y 2025Y Q1 2026 CRE Concentration ADC Concentration □ Well - diversified loan portfolio reflective of the balanced state of our markets □ Loan ¹ growth was 10.2% annualized for Q1 2026, with owner occupied real estate and business contributing ~83% of net growth Financial Highlights Diversified Loan Portfolio Note: Information as of March 31, 2026, unless otherwise noted 1) Excludes loans held for sale 2) Bank level financial information shown CRE and ADC Concentration Ratios 2 Loan Portfolio Composition ¹ Growth Over Time ($M) ¹ 2ZQHU RFFXSLHG5( 1RQ RZQHU RFFXSLHG5( &RQVWUXFWLRQ %XVLQHVV 5HDO(VWDWH +RPH HTXLW\ &RQVWUXFWLRQ 2WKHU Total Loans $3.94 Billion 15

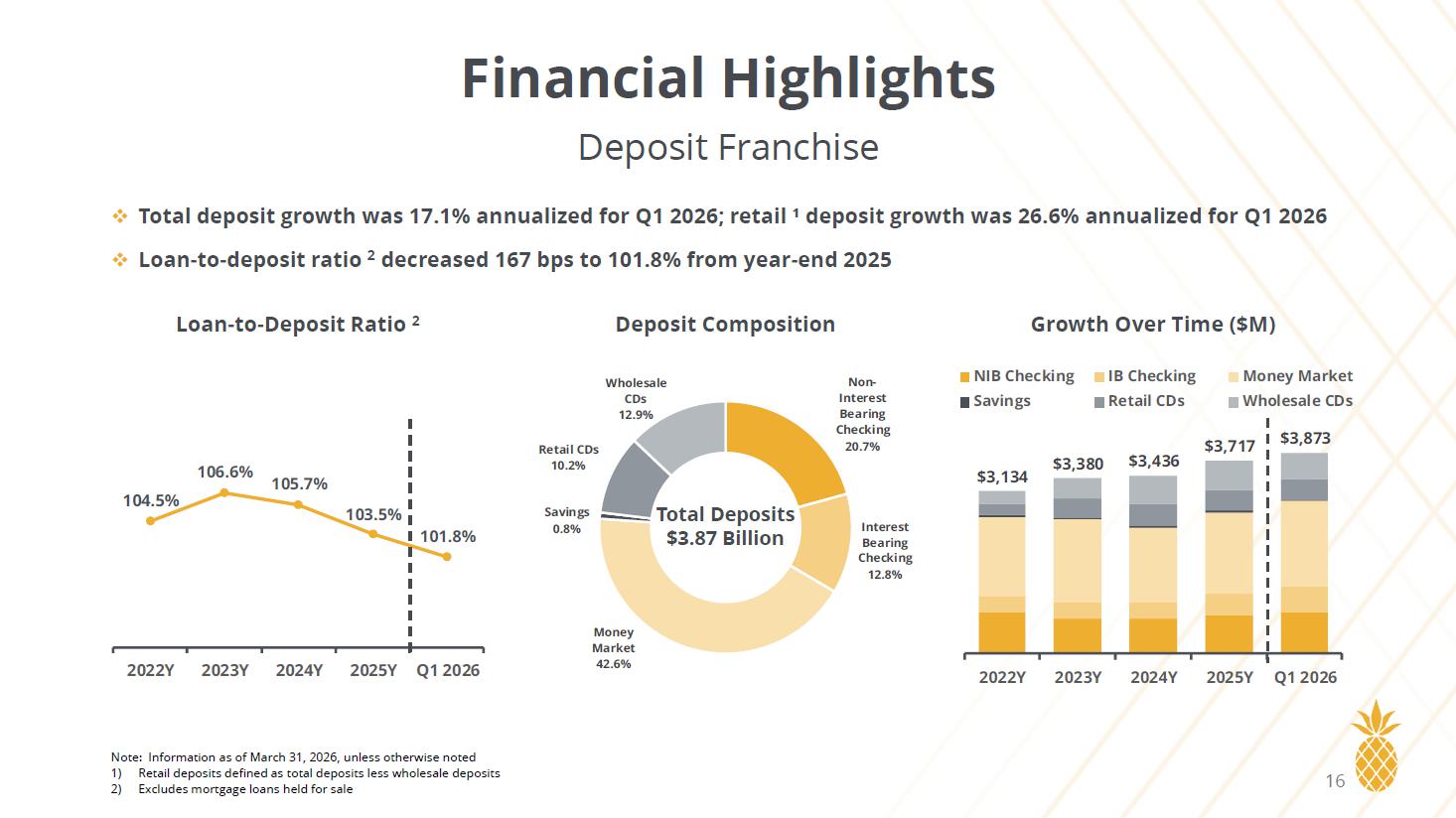

□ Total deposit growth was 17.1% annualized for Q1 2026; retail ¹ deposit growth was 26.6% annualized for Q1 2026 □ Loan - to - deposit ratio 2 decreased 167 bps to 101.8% from year - end 2025 Financial Highlights Deposit Franchise Note: Information as of March 31, 2026, unless otherwise noted 1) Retail deposits defined as total deposits less wholesale deposits 2) Excludes mortgage loans held for sale Loan - to - Deposit Ratio 2 Deposit Composition Growth Over Time ($M) 1RQ ΖQWHUHVW %HDULQJ &KHFNLQJ ΖQWHUHVW %HDULQJ &KHFNLQJ 0RQH\ 0DUNHW 6DYLQJV 5HWDLO&'V :KROHVDOH &'V < < < < 4 Total Deposits $3.87 Billion 16

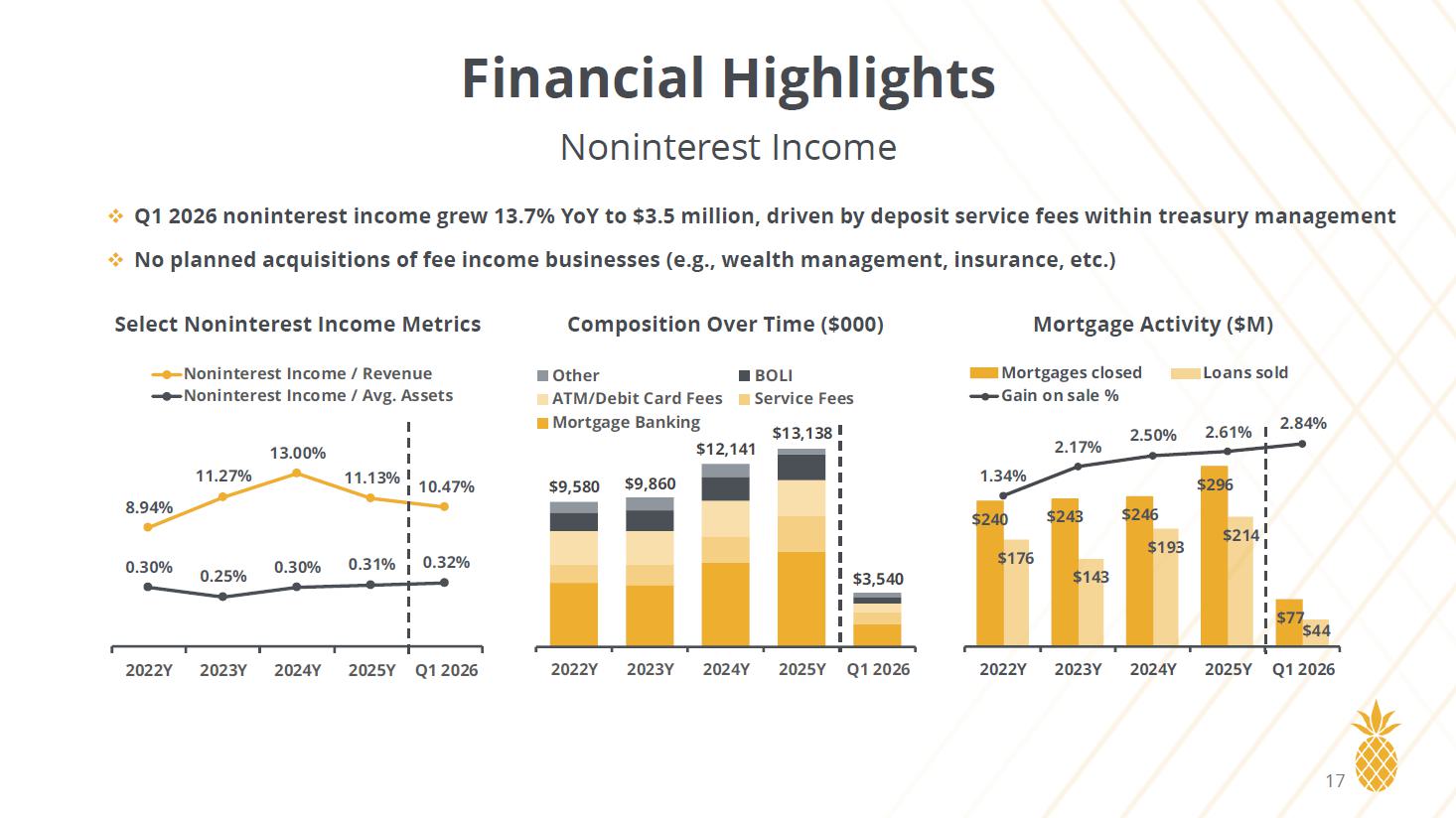

□ Q1 2026 noninterest income grew 13.7% YoY to $3.5 million, driven by deposit service fees within treasury management □ No planned acquisitions of fee income businesses (e.g., wealth management, insurance, etc.) Financial Highlights Noninterest Income Select Noninterest Income Metrics Composition Over Time ($000) Mortgage Activity ($M) < < < < 4 2WKHU %2/Ζ $70 'HELW&DUG)HHV 6HUYLFH)HHV 0RUWJDJH%DQNLQJ < < < < 4 1RQLQWHUHVWΖQFRPH 5HYHQXH 1RQLQWHUHVWΖQFRPH $YJ $VVHWV 17

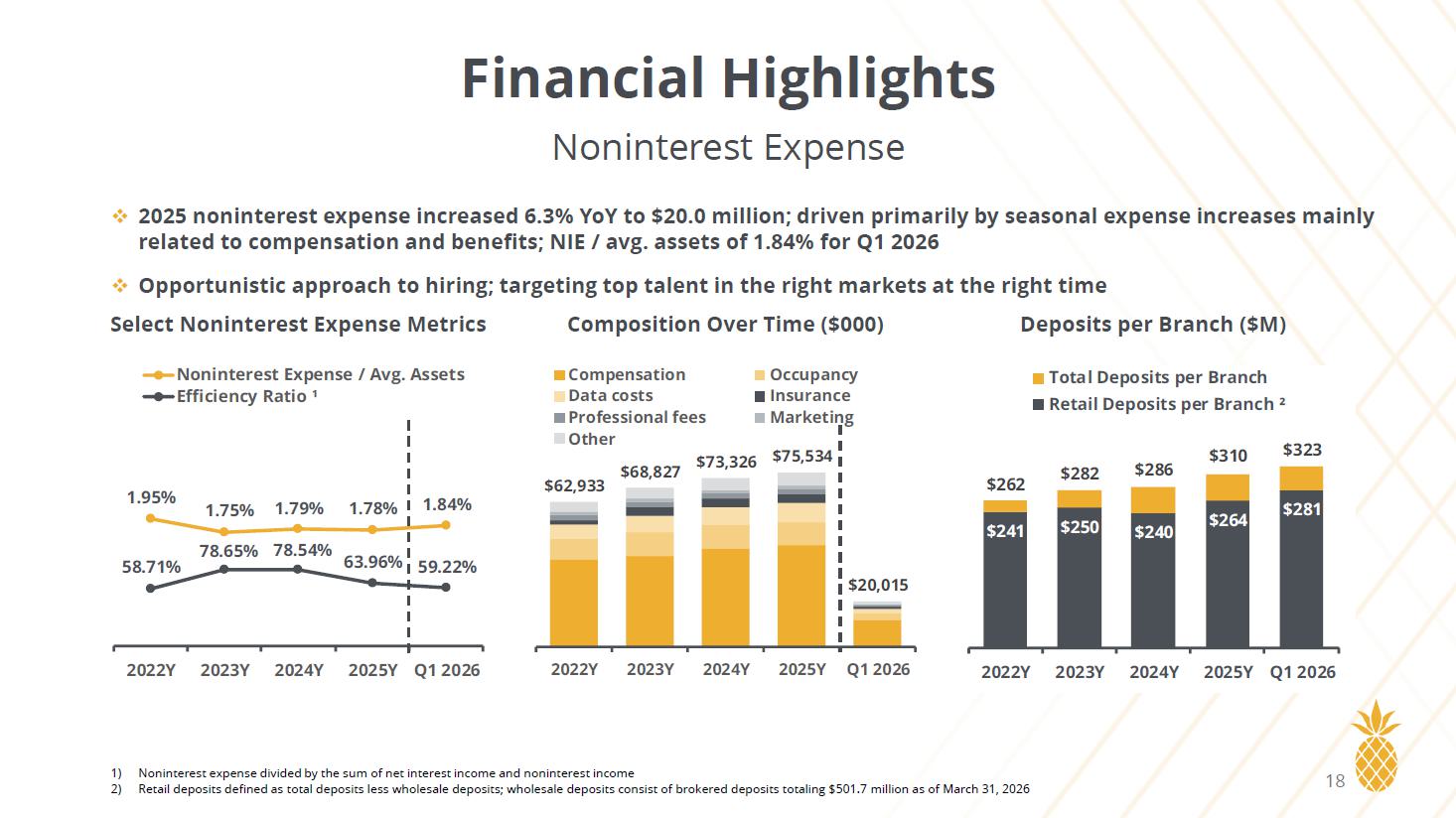

< < < < 4 1RQLQWHUHVW([SHQVH $YJ $VVHWV (ɝFLHQF\5DWLR { □ 2025 noninterest expense increased 6.3% YoY to $20.0 million; driven primarily by seasonal expense increases mainly related to compensation and benefits; NIE / avg. assets of 1.84% for Q1 2026 □ Opportunistic approach to hiring; targeting top talent in the right markets at the right time Financial Highlights Noninterest Expense 1) Noninterest expense divided by the sum of net interest income and noninterest income 2) Retail deposits defined as total deposits less wholesale deposits; wholesale deposits consist of brokered deposits totaling $ 501 .7 million as of March 31, 2026 Select Noninterest Expense Metrics Composition Over Time ($000) Deposits per Branch ($M) < < < < 4 &RPSHQVDWLRQ 2FFXSDQF\ 'DWDFRVWV ΖQVXUDQFH 3URIHVVLRQDOIHHV 0DUNHWLQJ 2WKHU 18

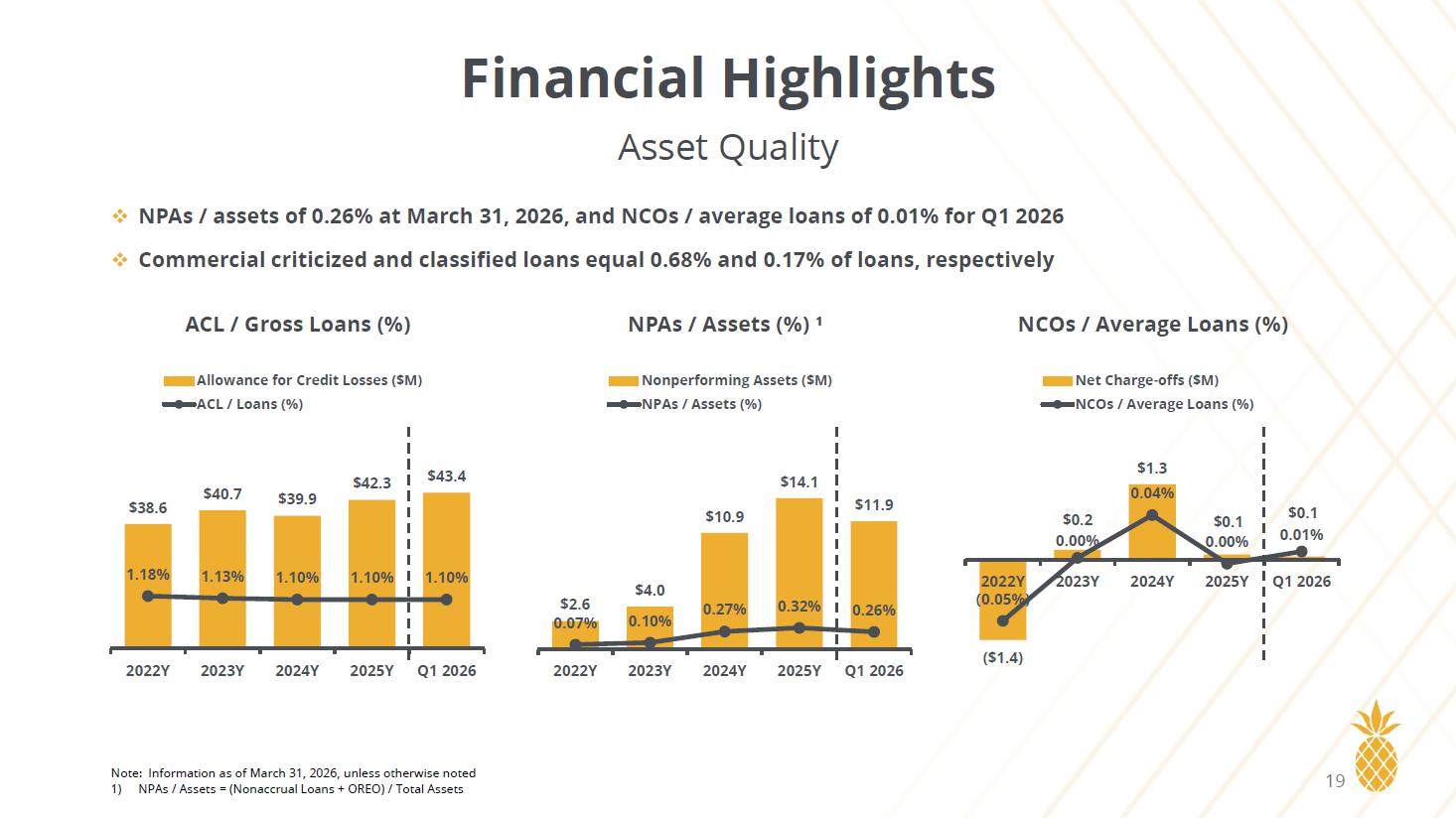

$2.6 $4.0 $10.9 $14.1 $11.9 0.07% 0.10% 0.27% 0.32% 0.26% $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 2022Y 2023Y 2024Y 2025Y Q1 2026 Nonperforming Assets ($M) NPAs / Assets (%) ($1.4) $0.2 $1.3 $0.1 $0.1 (0.05%) 0.00% 0.04% 0.00% 0.01% ($1.5) ($1.0) ($0.5) $0.0 $0.5 $1.0 $1.5 $2.0 $2.5 $3.0 2022Y 2023Y 2024Y 2025Y Q1 2026 Net Charge-offs ($M) NCOs / Average Loans (%) $38.6 $40.7 $39.9 $42.3 $43.4 1.18% 1.13% 1.10% 1.10% 1.10% $20.0 $25.0 $30.0 $35.0 $40.0 $45.0 $50.0 $55.0 $60.0 2022Y 2023Y 2024Y 2025Y Q1 2026 Allowance for Credit Losses ($M) ACL / Loans (%) □ NPAs / assets of 0.26% at March 31, 2026, and NCOs / average loans of 0.01% for Q1 2026 □ Commercial criticized and classified loans equal 0.68% and 0.17% of loans, respectively Financial Highlights Asset Quality Note: Information as of March 31, 2026, unless otherwise noted 1) NPAs / Assets = (Nonaccrual Loans + OREO) / Total Assets ACL / Gross Loans (%) NPAs / Assets (%) ¹ NCOs / Average Loans (%) 19

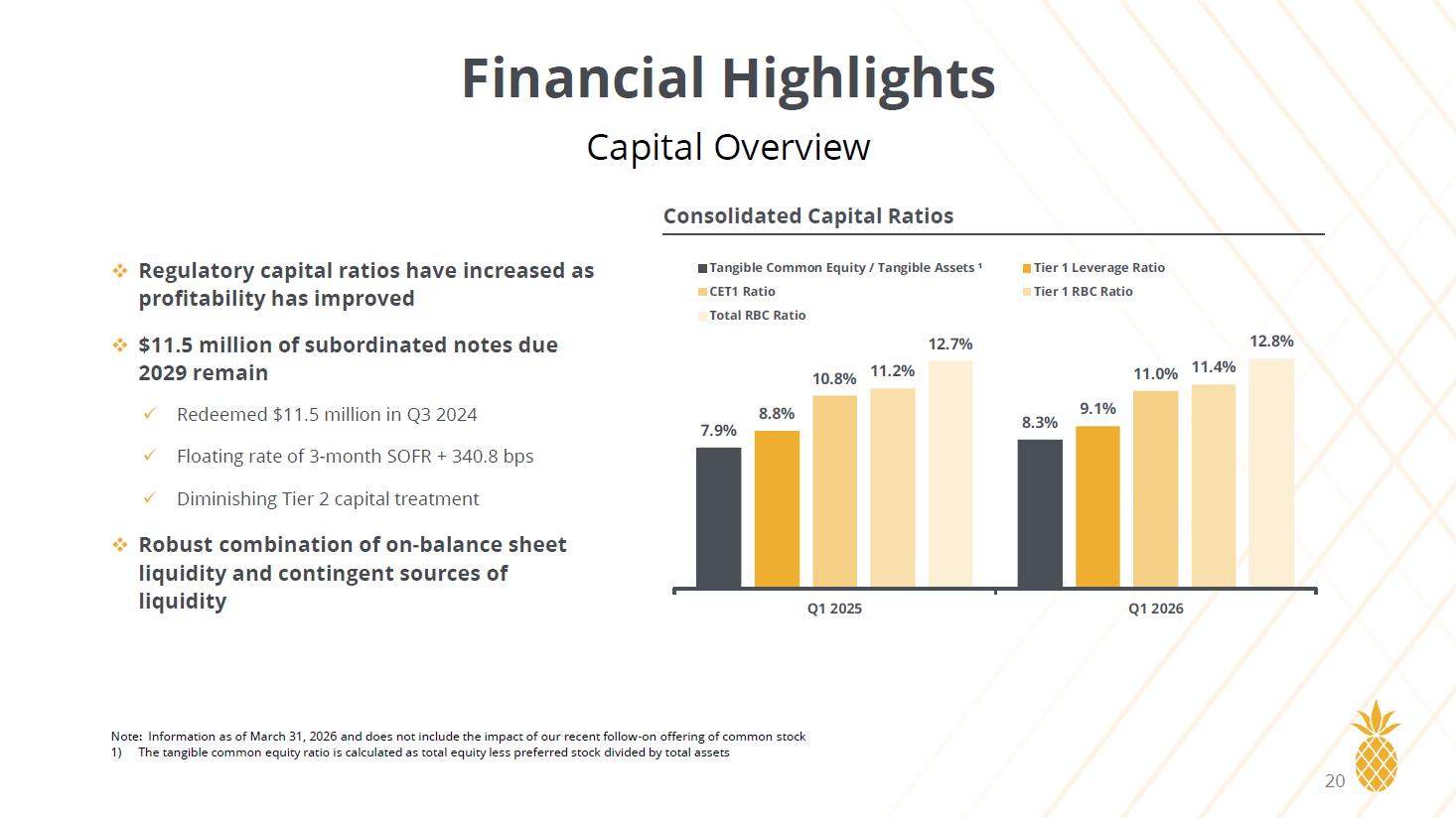

□ Regulatory capital ratios have increased as profitability has improved □ $11.5 million of subordinated notes due 2029 remain x Redeemed $11.5 million in Q3 2024 x Floating rate of 3 - month SOFR + 340.8 bps x Diminishing Tier 2 capital treatment □ Robust combination of on - balance sheet liquidity and contingent sources of liquidity Financial Highlights Capital Overview Note: Information as of March 31, 2026 and does not include the impact of our recent follow - on offering of common stock 1) The tangible common equity ratio is calculated as total equity less preferred stock divided by total assets Consolidated Capital Ratios 7.9% 8.3% 8.8% 9.1% 10.8% 11.0% 11.2% 11.4% 12.7% 12.8% Q1 2025 Q1 2026 Tangible Common Equity / Tangible Assets ¹ Tier 1 Leverage Ratio CET1 Ratio Tier 1 RBC Ratio Total RBC Ratio 20

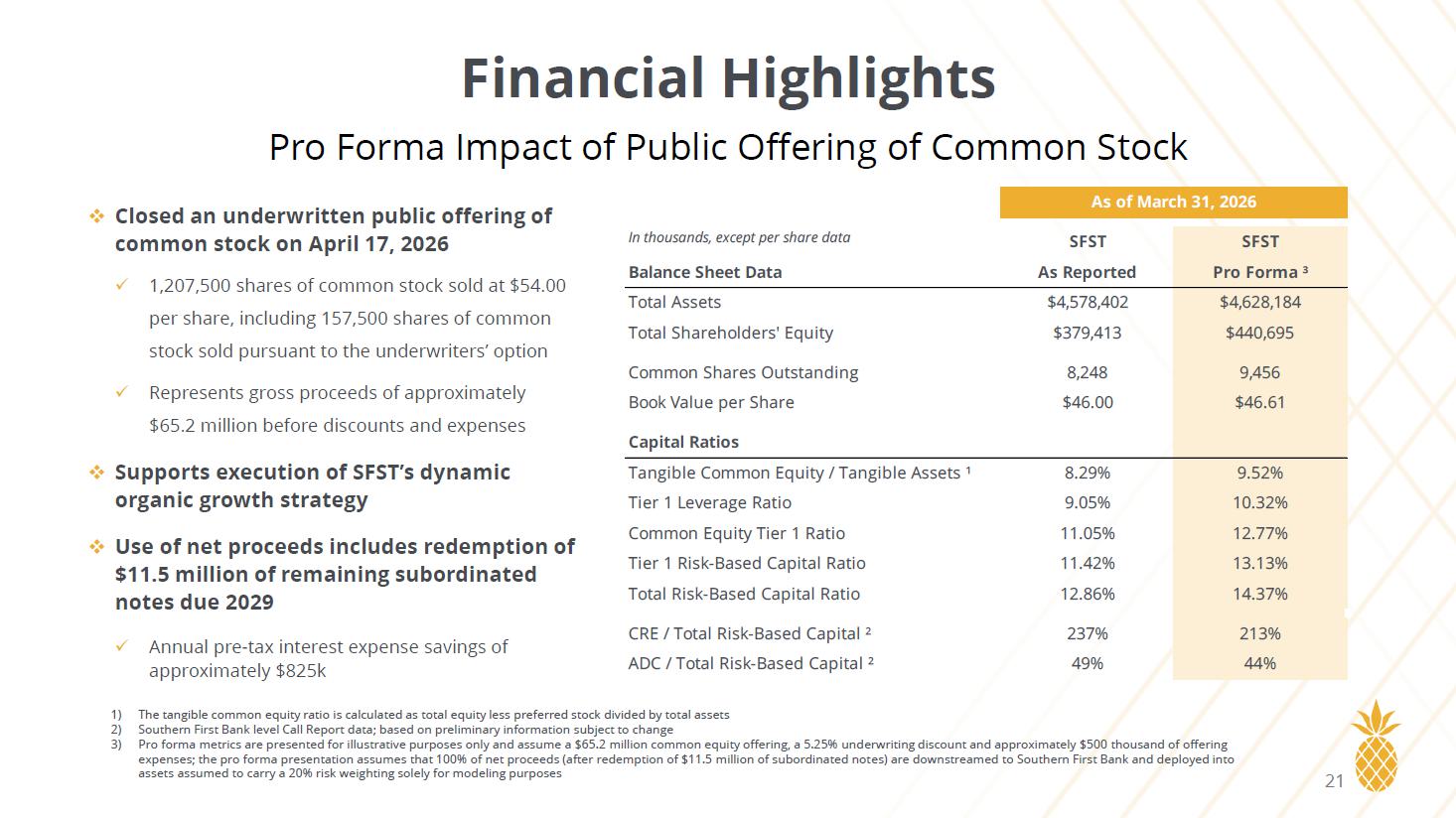

□ Closed an underwritten public offering of common stock on April 17, 2026 x 1,207,500 shares of common stock sold at $54.00 per share, including 157,500 shares of common stock sold pursuant to the underwriters’ option x Represents gross proceeds of approximately $65.2 million before discounts and expenses □ Supports execution of SFST’s dynamic organic growth strategy □ Use of net proceeds includes redemption of $11.5 million of remaining subordinated notes due 2029 x Annual pre - tax interest expense savings of approximately $825k Financial Highlights Pro Forma Impact of Public Offering of Common Stock 21 As of March 31, 2026 In thousands, except per share data SFST SFST Balance Sheet Data As Reported Pro Forma ³ Total Assets $4,578,402 $4,628,184 Total Shareholders' Equity $379,413 $440,695 Common Shares Outstanding 8,248 9,456 Book Value per Share $46.00 $46.61 Capital Ratios Tangible Common Equity / Tangible Assets ¹ 8.29% 9.52% Tier 1 Leverage Ratio 9.05% 10.32% Common Equity Tier 1 Ratio 11.05% 12.77% Tier 1 Risk-Based Capital Ratio 11.42% 13.13% Total Risk-Based Capital Ratio 12.86% 14.37% CRE / Total Risk-Based Capital ² 237% 213% ADC / Total Risk-Based Capital ² 49% 44% 1) The tangible common equity ratio is calculated as total equity less preferred stock divided by total assets 2) Southern First Bank level Call Report data; based on preliminary information subject to change 3) Pro forma metrics are presented for illustrative purposes only and assume a $65.2 million common equity offering, a 5.25% und erw riting discount and approximately $500 thousand of offering expenses; the pro forma presentation assumes that 100% of net proceeds (after redemption of $11.5 million of subordinated not es) are downstreamed to Southern First Bank and deployed into assets assumed to carry a 20% risk weighting solely for modeling purposes