Exhibit 99.1

XL

Fleet Completes Transformational Acquisition of Spruce Power, the

Largest Privately Held Solar-as-a-Service Provider

| ● | Completed

acquisition of Spruce Power from funds managed by HPS for total cash consideration of approximately

$58 million and the assumption of approximately $542 million of debt on September 9, 2022 |

| ● | Spruce

Power is the largest privately held owner and operator of residential rooftop solar systems

in the U.S. with more than 52,000 subscribers |

| ● | Acquisition

is cornerstone of XL Fleet’s new corporate strategy to become leading provider of subscription-based

solutions for rooftop solar, battery storage and EV charging |

| ● | Spruce

Power generated $15 million of net income and $51 million of Adjusted EBITDA during the twelve

months ended June 30, 2022 |

| ● | More

than $240 million of unrestricted cash on hand after completion of the transaction provides

significant capacity to support new strategy and future growth |

| ● | Implementing

leadership transition with the CEO of Spruce Power, Christian Fong, appointed President of

XL Fleet and to the Board of Directors, and expected to become CEO of XL Fleet on or prior

to February 15, 2023 |

| ● | Initiating

comprehensive review of strategic alternatives for XL Fleet’s Drivetrain segment to

maximize shareholder value |

| ● | Developing

new corporate identity and branding to reflect new corporate strategy |

WIXOM,

MI, September 12, 2022 – XL Fleet Corp. (NYSE: XL), today announced the acquisition of Spruce Power, the largest

privately held owner and operator of residential rooftop solar systems in the U.S. with more than 52,000 subscribers. In connection with

the acquisition of Spruce Power, XL Fleet also unveiled its new corporate strategy to provide subscription-based solutions for rooftop

solar, battery storage, EV charging and other distributed energy resources.

Spruce

Power Acquisition

On

September 9, 2022 after market close, XL Fleet completed the acquisition of the Spruce Power business from funds managed by HPS Investment

Partners, LLC (“HPS”) for total cash consideration of approximately $58 million and the assumption of approximately $542

million of debt. The Board of Directors of XL Fleet unanimously approved the transaction. After paying the purchase price and related

transaction fees and expenses, XL Fleet had approximately $270 million of cash and cash equivalents, of which, approximately $240 million

was unrestricted.

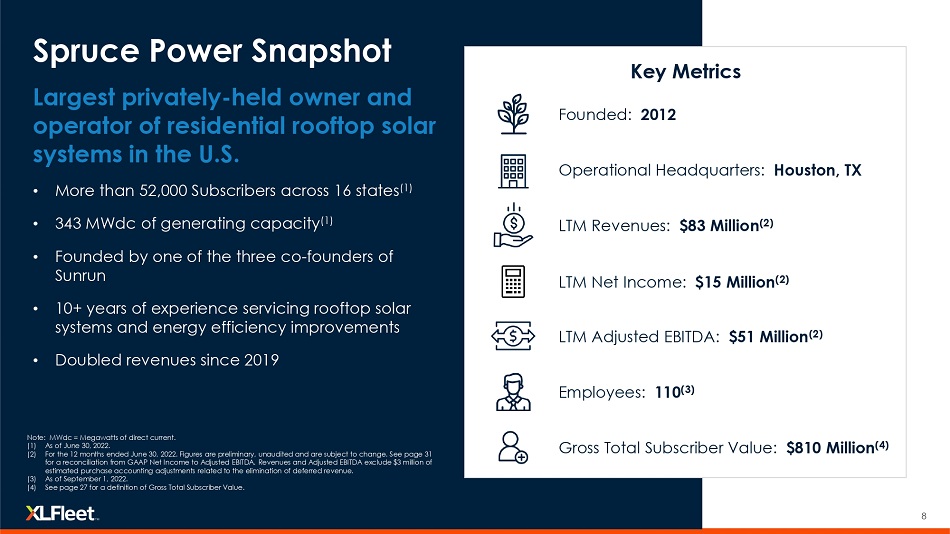

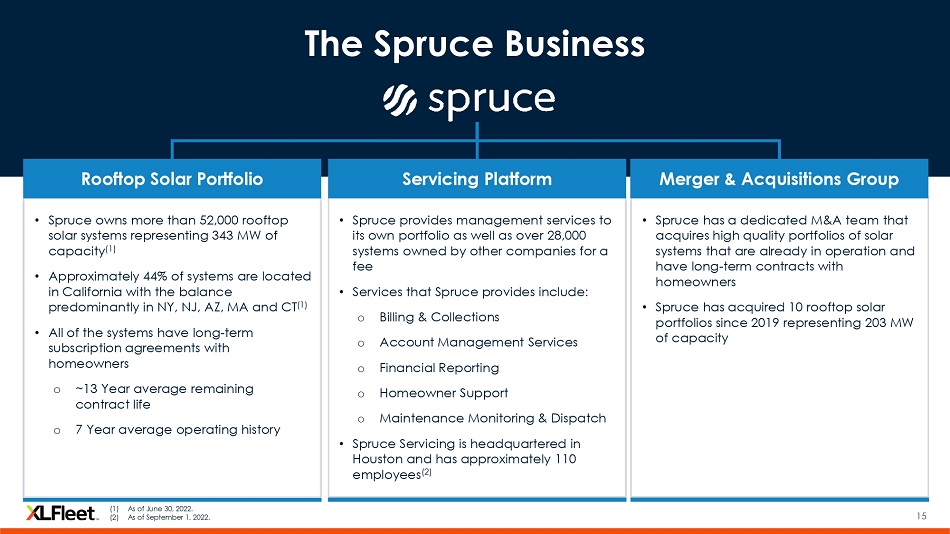

Spruce

Power owns and operates more than 52,000 residential rooftop solar systems. The company sells the power generated by its systems to homeowners

pursuant to long-term agreements that obligate the company’s subscribers to make recurring monthly payments. Including the estimated

impact of purchase accounting adjustments on a pro forma basis, Spruce Power generated revenues, net income and Adjusted EBITDA of approximately

$83 million, $15 million and $51 million, respectively, for the twelve months ended June 30, 2022. Spruce Power’s operational headquarters

are in Houston, Texas and the company had approximately 110 full time employees as of September 1, 2022.

Spruce

Power’s revenues have more than doubled since 2019, driven primarily by the acquisition of 10 rooftop solar portfolios. The company

does not have a salesforce or installation technicians. Spruce Power has grown by acquiring portfolios of residential solar systems from

other companies and investors rather than selling individual systems to homeowners through a direct-to-consumer salesforce like many

of its competitors. This approach has allowed the company to keep its customer acquisition costs low and enabled it to generate consistent

Adjusted EBITDA.

Management

Commentary

Eric

Tech, Chief Executive Officer of XL Fleet, stated, “Earlier this year, we communicated our intent to transform the company and

create shareholder value through strategic M&A. The acquisition of Spruce Power is a critical first step in that transformation and

will be the cornerstone of our new strategy to provide subscription-based solutions for rooftop solar, battery storage and EV charging

to homeowners and small businesses.”

Mr.

Tech added, “Demand for distributed generation and electric vehicles continues to grow as consumers and businesses seek to mitigate

the impact of rising energy costs and become more sustainable. Subscription-based services that make it easy for homeowners and small

businesses to own and maintain rooftop solar, battery storage and electric vehicle charging systems are in high demand. The subscription

model allows consumers access to new technology without making a significant upfront investment or incurring maintenance costs, while

enabling the service provider to earn recurring revenues over a long period of time and generate attractive returns on capital. Spruce

Power is a longstanding leader in providing solar-as-a-service solutions and is playing a major role in helping consumers to reduce their

energy costs and make meaningful contributions to decarbonizing the electricity grid.”

Mr.

Tech concluded, “The combination of Spruce’s existing subscriber-base and proven servicing platform with our capital and

small business relationships positions us to take advantage of rapid growth in rooftop solar, energy storage and electric vehicle adoption

while creating a path to more predictable revenues, profits and cash flow for our shareholders.”

Christian

Fong, Chief Executive Officer of Spruce Power and newly appointed President of XL Fleet, commented, “The Spruce team is incredibly

excited about joining the XL Fleet platform and motivated by the potential value created by combining our two companies. With XL Fleet’s

resources, we now have the tools to significantly accelerate the growth in our business, while continuing to execute on our mission to

lower the cost of energy for our customers and create a more sustainable future.”

Spruce

Power Highlights

| ● | Over

$800 million of Gross Total Subscriber Value from long-term subscriber contracts – As of June 30, 2022, the average remaining

term of Spruce Power’s customer contracts was approximately 13 years and the company’s Gross Total Subscriber Value, Gross

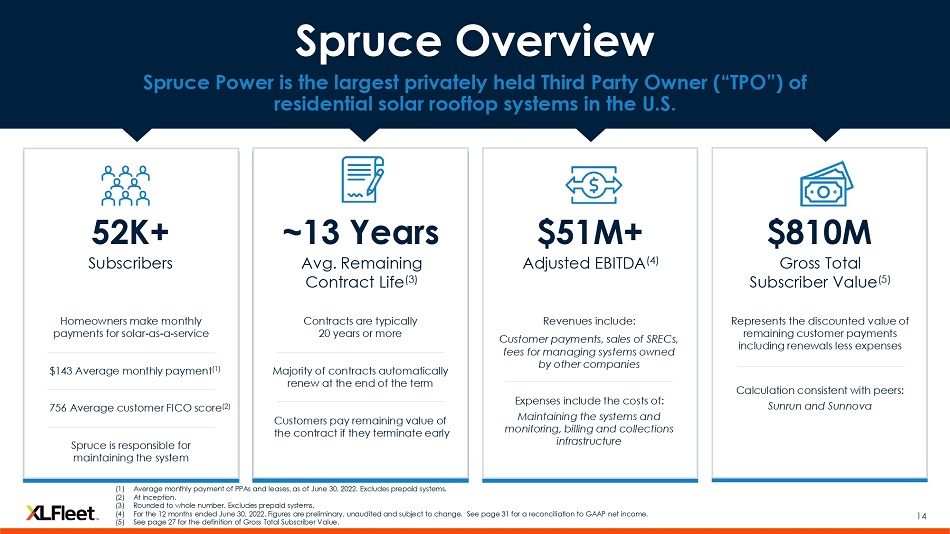

Contracted Subscriber Value and Gross Renewal Subscriber Value were $810 million, $560 million and $250 million, respectively. Definitions

of each of the foregoing terms in this paragraph are set forth at the end of this press release. |

| ● | High

quality, geographically diverse subscriber base – Spruce Power has more than 52,000 subscribers across 16 states. The company’s

subscribers are all homeowners and have an average FICO score of 756. |

| ● | Industry-leading

margins, revenues per employee and customer acquisition costs driven by a differentiated customer acquisition strategy –

Spruce Power has acquired 10 rooftop solar portfolios since 2019 representing more than 30,000 systems. By acquiring portfolios of existing

systems rather than selling one system at a time to individual homeowners, Spruce Power has achieved significant growth while avoiding

the expense, operational complexity and risks associated with a large salesforce and teams of installers. In 2021, Spruce Power’s

Adjusted EBITDA margin, revenue per employee and customer acquisition cost per subscriber acquired were approximately 60%, $830,000 and

$420, respectively. |

| ● | Proven

platform for servicing a wide-range of distributed generation and energy efficiency products – Spruce Power has originated

and serviced its own as well as third parties’ distributed generation and energy efficiency assets for over a decade. In addition

to servicing rooftop solar systems, the company’s experience includes servicing battery storage systems, raising tax equity and

project financing, monetizing environmental credits and utility incentives as well as originating and servicing solar and energy efficiency

loans. The company’s experience and capabilities are underscored by the fact that in addition to servicing its own systems,

Spruce Power is paid to manage more than 28,000 solar systems owned by other publicly traded residential solar companies, financial institutions

and non-profit organizations. |

| ● | Robust

near-term M&A opportunities – Spruce Power has a robust set of M&A opportunities that the combined company intends

to pursue, with the goal of delivering additional growth in subscribers, revenues and Adjusted EBITDA and increased value for shareholders. |

Transaction

Highlights

| ● | Gain

exposure to the rapidly growing rooftop solar market – Spruce Power has been

a direct beneficiary of growing demand for rooftop solar. Rising electricity prices, falling

battery costs and increasing EV adoption as well as the recently passed Inflation Reduction

Act are making rooftop solar more attractive to homeowners and small businesses. The number

of homes with rooftop solar is expected to more than double over the next five years, according

to Wood Mackenzie. |

| ● | Creates

visibility on future results through long-term, contracted cash flows –

Spruce Power derives approximately 90% of its revenues from recurring monthly payments

that are contractual obligations of the company’s subscribers and fees from third parties

that pay Spruce Power to manage their systems under long-term agreements. The cumulative,

undiscounted remaining payments due to Spruce Power pursuant to its agreements with customers

was approximately $975 million as of June 30, 2022. |

| ● | Maintains

significant capacity to invest in future growth – XL Fleet had more

than $240 million of unrestricted cash on hand following the closing of the Spruce Power

acquisition, giving the combined company significant resources to potentially make future

acquisitions to further grow the company’s subscriber base. |

| ● | Takes

advantage of low cost, non-recourse debt financing – The transaction was structured

to allow Spruce Power’s existing debt to remain in place following the acquisition,

which eliminated the need for XL Fleet to raise new financing resulting in significant savings

for the company. The Spruce Power debt that XL Fleet will assume as part of the transaction

has a weighted average interest cost of approximately 5.5% and is non-recourse to XL Fleet

Corp. |

| ● | Does

not dilute shareholders – The acquisition of Spruce Power was funded

with cash on hand and the assumption of existing Spruce Power debt. XL Fleet did not issue

any stock to HPS, the owner of Spruce Power, in the transaction. |

New

Corporate Strategy

Over

the past several quarters, XL Fleet’s management and Board of Directors conducted a comprehensive review of the company’s

existing business as well as potential acquisitions that could accelerate growth and increase profitability. Based on that review, as

well as learnings from the operation of the XL Grid segment which provides energy efficiency upgrades to small businesses, XL Fleet determined

that refocusing the company’s business on providing subscription-based solutions to homeowners and small businesses for rooftop

solar, energy storage, EV charging and other energy-related products would yield greater value for the company’s shareholders.

Key elements of XL Fleet’s new corporate strategy include:

| ● | Leveraging

the Spruce Power platform to become a leading provider of subscription-based solutions for distributed energy resources –

Spruce Power has more than a decade of experience owning and operating rooftop solar systems as well as energy efficiency upgrades.

XL Fleet believes that Spruce Power’s proven platform for managing residential solar can be extended to other categories of distributed

energy resources. Through leveraging the Spruce Power platform, XL Fleet intends to grow its revenues by providing subscription-based

solutions for rooftop solar, energy storage, EV charging and other energy-related products to homeowners and small businesses. |

| ● | Growing

profitably by focusing on channels with the lowest customer acquisition cost – XL Fleet will seek to grow its subscriber

revenues by focusing on the channels that have the lowest customer acquisition costs, including: acquiring existing systems from other

companies or investment funds, selling additional services to existing subscribers, selling services to new customers online and partnering

with selected independent installers to provide a subscription-based solution for their customers. |

| ● | Increasing

shareholder value by delivering predictable revenues, profits and cash flow – By focusing on subscription-based solutions

with long-term customer agreements, XL Fleet will seek to generate consistent revenues, profits and cash flow. |

Leadership

Transition Plan

To

support XL Fleet’s new corporate strategy, Christian Fong, the current Chief Executive Officer of Spruce Power, has been appointed

President of XL Fleet and to the XL Fleet Board of Directors. Additionally, the company intends to appoint Christian Fong as Chief Executive

Officer of XL Fleet on or prior to February 15, 2023. Eric Tech will remain the Chief Executive Officer of XL Fleet until the planned

appointment of Christian Fong.

Review

of Strategic Alternatives for the Drivetrain Segment

In

parallel with the acquisition of Spruce Power and the company’s new corporate strategy, XL Fleet’s Board of Directors recently

initiated a comprehensive review of strategic alternatives for XL Fleet’s Drivetrain segment with the goal of maximizing shareholder

value and streamlining the company’s operations. XL Fleet expects to complete the review by the end of 2022.

New

Corporate Name and Brand Identity

In

connection with the acquisition of Spruce Power and implementation of the company’s new corporate strategy, XL Fleet intends to

change its corporate name and introduce a new brand identity. The company’s new name will reflect its focus on providing subscription-based

solutions for rooftop solar, energy storage, EV charging and other energy-related products to homeowners and small businesses.

Additional

Information

Shareholders

and interested investors can find a presentation that contains additional information regarding XL Fleet’s new strategy and the

Spruce Power acquisition on the company’s investor relations website at https://investors.xlfleet.com.

Webcast

& Conference Call Information

The

XL Fleet management team will host a conference call to discuss the Spruce Power transaction and new corporate strategy today, September

12, 2022 at 8:30 a.m. Eastern Time. The call can be accessed via a live webcast accessible on the Events & Presentations page in

the Investor Relations section of the company’s website at www.xlfleet.com. Alternatively, the call can be accessed live over the

telephone by dialing (877) 407-3982, or for international callers, (201) 493-6780 and referencing XL Fleet. An archive of the webcast

will be available on the company’s website for a period of time shortly after the call. A telephonic replay will also be available

shortly after the call and can be accessed by dialing (844) 512-2921, or for international callers, (412) 317-6671. The passcode for

the replay is 13732695. The replay will be available until September 26, 2022.

Advisors

Guggenheim

Securities, LLC served as exclusive financial advisor and WilmerHale served as outside counsel to XL Fleet in connection with the transaction.

About

XL Fleet Corp.

With

this transaction, XL Fleet provides subscription-based services that make it easy for homeowners and small businesses to own and maintain

rooftop solar, battery storage and electric-vehicle charging systems. Our as-a-service model

allows consumers to access new technology without making a significant upfront investment or incurring maintenance costs. XL Fleet has

more than 52,000 subscribers across the United States. For additional information, please visit www.xlfleet.com.

About

HPS Investment Partners, LLC

HPS

Investment Partners is a leading global investment firm with over $89 billion of assets under management as of July 2022. HPS seeks to

provide creative capital solutions and generate attractive risk-adjusted returns for clients. HPS manages various strategies across the

capital structure that include syndicated leveraged loans and high yield bonds to privately negotiated senior secured debt and mezzanine

instruments, asset-based leasing and private equity.

Use

of Non-GAAP Financial Information

To

supplement certain financial information, which is prepared and presented in accordance with U.S. generally accepted accounting principles

(“GAAP”), XL Fleet Corp. (“XL”) reports certain non-GAAP financial information relating to each of XL and Spruce

Power (“Spruce”) and which have been reconciled to the nearest GAAP measures in the tables within this press release. This

prospective financial information was not prepared with a view toward compliance with published guidelines of the SEC or the guidelines

established by the American Institute of Certified Public Accountants for preparation and presentation of prospective financial information

or U.S. GAAP with respect to forward looking financial information. Non-GAAP financial measures are subject to material limitations as

they are not in accordance with, or a substitute for, measurements prepared in accordance with GAAP. We believe that these non-GAAP measures,

viewed in addition to and not in lieu of reported GAAP financial information, provides useful information to investors by providing a

more focused measure of operating results, enhances the overall understanding of past financial performance and future prospects, and

allows for greater transparency with respect to key metrics of XL and Spruce. The non-GAAP measures presented herein may not be comparable

to similarly titled measures presented by other companies.

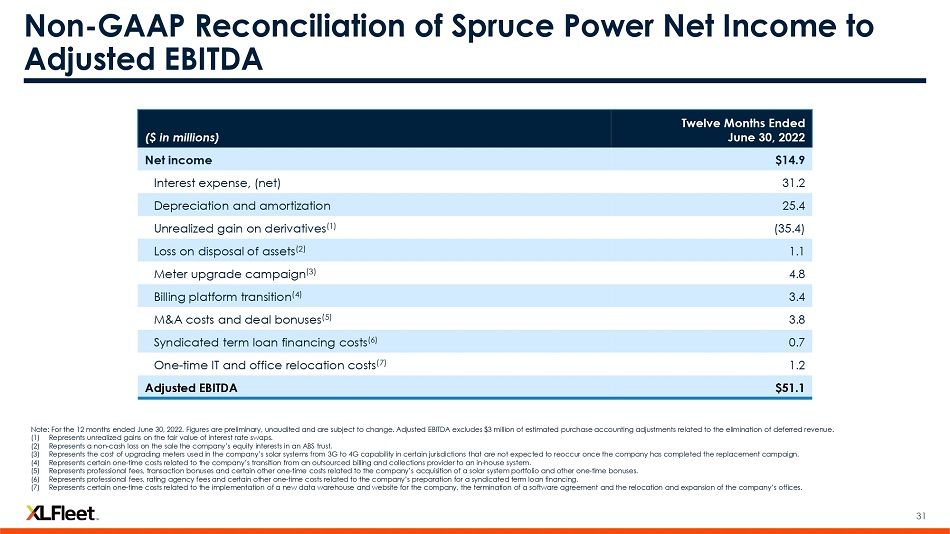

Adjusted

EBITDA: We define Adjusted EBITDA as consolidated net income (loss) plus interest expense,

unrealized (gain) loss on derivatives, income taxes, depreciation and amortization, loss (gain) on disposal of assets and certain identified

items that we do not consider to be part of the ongoing businesses of XL and Spruce. We believe Adjusted EBITDA provides meaningful

information to the performance of XL’s and Spruce’s respective businesses and therefore use it to supplement reported GAAP

metrics. We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to

perform additional analyses of operating results of XL and Spruce.

Reconciliation

of Net Income to Adjusted EBITDA (in millions):

| | |

Twelve

Months Ended

June 30,

2022(1) | |

| Net income | |

$ | 14.9 | |

| Interest expense, net | |

| 31.2 | |

| Depreciation and amortization | |

| 25.4 | |

| Unrealized gain on derivatives(a) | |

| (35.4 | ) |

| Loss on disposal of assets(b) | |

| 1.1 | |

| Meter upgrade campaign(c) | |

| 4.8 | |

| Billing platform transition(d) | |

| 3.4 | |

| M&A costs and deal bonuses(e) | |

| 3.8 | |

| Syndicated term loan financing costs(f) | |

| 0.7 | |

| One-time IT and office relocation costs(g) | |

| 1.2 | |

| Adjusted EBITDA | |

$ | 51.1 | |

| (a) | Represents

unrealized gains on the fair value of interest rate swaps. |

| (b) | Represents

a non-cash loss on the sale the company’s equity interests in an ABS trust. |

| (c) | Represents

the cost of upgrading meters used in the company’s solar systems from 3G to 4G capability

in certain jurisdictions that are not expected to reoccur once the company has completed

the replacement campaign. |

| (d) | Represents

certain one-time costs related to the company’s transition from an outsourced billing

and collections provider to an in-house system. |

| (e) | Represents

professional fees, transaction bonuses and certain other one-time costs related to the company’s

acquisition of a solar system portfolio and other one-time bonuses. |

| (f) | Represents

professional fees, rating agency fees and certain other one-time costs related to the company’s

preparation for a syndicated term loan financing. |

| (g) | Represents

certain one-time costs related to the implementation of a new data warehouse and website

for the company, the termination of a software agreement and the relocation and expansion

of the company’s offices. |

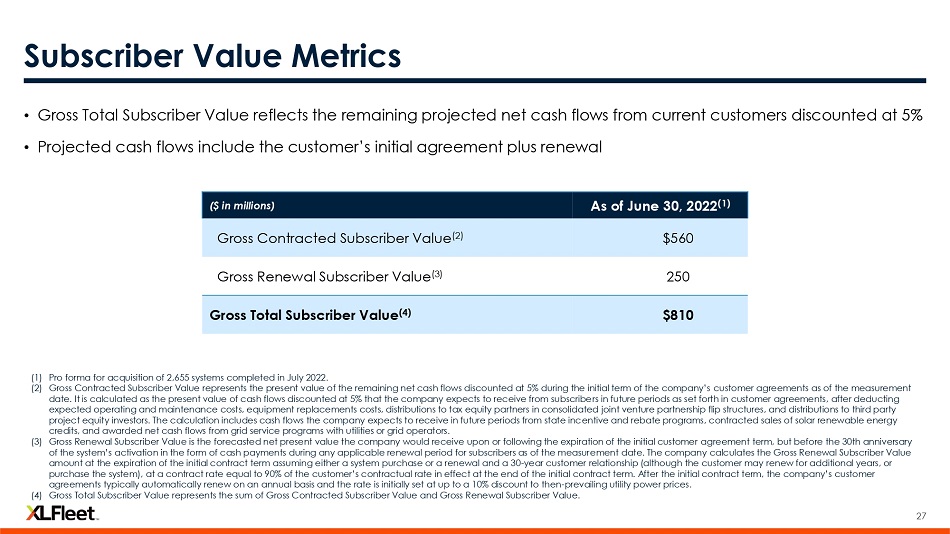

Subscriber

Value Metrics (in millions):

| | |

As of

June 30,

2022 | |

| Gross Contracted Subscriber Value(a) | |

$ | 560.0 | |

| Gross Renewal Subscriber Value(a) | |

| 250.3 | |

| Gross Total Subscriber Value(a) | |

$ | 810.3 | |

| (a) | Pro forma

for the acquisition of Level Solar completed in July 2022. |

Gross

Total Subscriber Value represents the sum of Gross Contracted Subscriber Value and Gross Renewal Subscriber Value.

Gross

Contracted Subscriber Value represents the present value of the remaining net cash flows discounted at 5% during the initial term of

the company’s customer agreements as of the measurement date. It is calculated as the present value of cash flows discounted at

5% that the company expects to receive from subscribers in future periods as set forth in customer agreements, after deducting expected

operating and maintenance costs, equipment replacements costs, distributions to tax equity partners in consolidated joint venture partnership

flip structures, and distributions to third party project equity investors. The calculation includes cash flows the company expects to

receive in future periods from state incentive and rebate programs, contracted sales of solar renewable energy credits, and awarded net

cash flows from grid service programs with utilities or grid operators.

Gross

Renewal Subscriber Value is the forecasted net present value the company would receive upon or following the expiration of the initial

customer agreement term, but before the 30th anniversary of the system’s activation in the form of cash payments during any applicable

renewal period for subscribers as of the measurement date. The company calculates the Gross Renewal Subscriber Value amount at the expiration

of the initial contract term assuming either a system purchase or a renewal and a 30-year customer relationship (although the customer

may renew for additional years, or purchase the system), at a contract rate equal to 90% of the customer’s contractual rate in

effect at the end of the initial contract term. After the initial contract term, the company’s customer agreements typically automatically

renew on an annual basis and the rate is initially set at up to a 10% discount to then-prevailing utility power prices.

Forward

Looking Statements

Certain

statements in this press release may constitute “forward-looking statements” within the meaning of the federal securities

laws. Forward-looking statements generally are accompanied by words such as “believe,” “may,” “will,”

“estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,”

“would,” “plan,” “predict,” “potential,” “seem,” “seek,” “future,”

“outlook,” and similar expressions that predict or indicate future events or trends or that are not statements of historical

matters. These statements are based on various assumptions, whether or not identified in this press release, and on the current expectations

of management and are not predictions of actual performance. Forward-looking statements are subject to a number of risks and uncertainties

that could cause actual results to differ materially from the forward-looking statements, including but not limited to: the effects of

pending and future legislation; the highly competitive nature of the Company’s business and markets; litigation, complaints, product

liability claims and/or adverse publicity; cost increases or shortages in the components or chassis necessary to support the Company’s

products and services; the introduction of new technologies; the impact of the COVID-19 pandemic on the Company’s business, results

of operations, financial condition, regulatory compliance and customer experience; the potential loss of certain significant customers;

privacy and data protection laws, privacy or data breaches, or the loss of data; general economic, financial, legal, political and business

conditions and changes in domestic and foreign markets; the inability to convert its sales opportunity pipeline into binding orders;

risks related to the rollout of the Company’s business and the timing of expected business milestones, including the ongoing global

microchip shortage and limited availability of chassis from vehicle OEMs and our reliance on our suppliers; the effects of competition

on the Company’s future business; the availability of capital; expectations regarding the growth of the solar industry, home electrification,

electric vehicles and distributed energy resources; the ability to successfully integrate the Spruce Power acquisition; the ability of

XL Fleet to implement its plans, forecasts and other expectations with respect to Spruce Power’s business and realize the expected

benefits of the acquisition; the ability to identify and complete future acquisitions; the ability to develop and market new products

and services; and the other risks discussed under the heading “Risk Factors” in the Company’s Annual Report on Form

10-K filed on March 31, 2022, and other documents that the Company files with the SEC in the future. If any of these risks materialize

or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements.

These forward-looking statements speak only as of the date hereof and the Company specifically disclaims any obligation to update these

forward-looking statements.

Certain

Additional Matters

This

press release includes operational metrics such as number of customers, number of systems and Gross Total Subscriber Value, Gross Contracted

Subscriber Value and Gross Renewal Subscriber Value. These operational metrics are not necessarily comparable to the same or similar

metrics as calculated by other companies.

This

press release also contains market data, statistical data, estimates and forecasts that are based on independent industry publications

or other publicly available information, as well as other information based on our internal sources. This information involves many assumptions

and limitations, and you are cautioned not to give undue weight to such information. Some data are also based on XL Fleet’s good

faith estimates, which are derived from its review of internal sources as well as the independent sources described above. Although XL

Fleet believes these sources are reliable, we have not independently verified the accuracy or completeness of the information contained

in the industry publications and other publicly available information. Accordingly, XL Fleet makes no representations as to the accuracy

or completeness of that information nor do we undertake to update such information after the date of this presentation

XL

Fleet Investor Contact:

Marc

Silverberg, Partner (ICR)

[email protected]

XL

Fleet Media Contact:

[email protected]

7

Exhibit

99.2

Acquisition of Spruce Power and New Corporate Strategy September 12, 2022

2 Disclaimer Use of Forward - Looking Statements Certain statements in this presentation may constitute “forward - looking statements” within the meaning of the federal securities laws . Forward - looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters . These statements are based on various assumptions, whether or not identified in this presentation, and on the current expectations of management and are not predictions of actual performance . Forward - looking statements are subject to a number of risks and uncertainties that could cause actual results to differ materially from the forward - looking statements, including but not limited to : the effects of pending and future legislation ; the highly competitive nature of the Company’s business and markets ; litigation, complaints, product liability claims and/or adverse publicity ; cost increases or shortages in the components or chassis necessary to support the Company’s products and services ; the introduction of new technologies ; the impact of the COVID - 19 pandemic on the Company’s business, results of operations, financial condition, regulatory compliance and customer experience ; the potential loss of certain significant customers ; privacy and data protection laws, privacy or data breaches, or the loss of data ; general economic, financial, legal, political and business conditions and changes in domestic and foreign markets ; the inability to convert its sales opportunity pipeline into binding orders ; risks related to the rollout of the Company’s business and the timing of expected business milestones, including the ongoing global microchip shortage and limited availability of chassis from vehicle OEMs and our reliance on our suppliers ; the effects of competition on the Company’s future business ; the availability of capital ; expectations regarding the growth of the solar industry, home electrification, electric vehicles and distributed energy resources ; the ability to successfully integrate the Spruce Power acquisition ; the ability of XL Fleet to implement its plans, forecasts and other expectations with respect to Spruce Power’s business and realize the expected benefits of the acquisition ; the ability to identify and complete future acquisitions ; the ability to develop and market new products and services ; and the other risks discussed under the heading “Risk Factors” in the Company’s Annual Report on Form 10 - K filed on March 31 , 2022 , and other documents that the Company files with the SEC in the future . If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results implied by these forward - looking statements . These forward - looking statements speak only as of the date hereof and the Company specifically disclaims any obligation to update these forward - looking statements . Use of Non - GAAP Financial Information To supplement certain financial information, which is prepared and presented in accordance with U . S . generally accepted accounting principles (“GAAP”), XL Fleet Corp . (“XL”) reports certain non - GAAP financial information relating to each of XL and Spruce Power (“Spruce”) and which have been reconciled to the nearest GAAP measures in the tables within this presentation . This prospective financial information was not prepared with a view toward compliance with published guidelines of the SEC or the guidelines established by the American Institute of Certified Public Accountants for preparation and presentation of prospective financial information or U . S . GAAP with respect to forward looking financial information . Non - GAAP financial measures are subject to material limitations as they are not in accordance with, or a substitute for, measurements prepared in accordance with GAAP . We believe that these non - GAAP measures, viewed in addition to and not in lieu of reported GAAP financial information, provides useful information to investors by providing a more focused measure of operating results, enhances the overall understanding of past financial performance and future prospects, and allows for greater transparency with respect to key metrics of XL and Spruce . The non - GAAP measures presented herein may not be comparable to similarly titled measures presented by other companies . Copyright Statement

3 Disclaimer (Cont’d) Adjusted EBITDA We define Adjusted EBITDA as consolidated net income (loss) plus interest expense, unrealized (gain) loss on derivatives, income taxes, depreciation and amortization, and certain identified items that we do not consider to be part of the ongoing businesses of XL and Spruce . We believe Adjusted EBITDA provides meaningful information to the performance of XL’s and Spruce’s respective businesses and therefore use it to supplement reported GAAP metrics . We have chosen to provide this supplemental information to investors, analysts and other interested parties to enable them to perform additional analyses of operating results of XL and Spruce . Certain Additional Matters This presentation includes operational metrics such as number of customers, number of systems and Gross Total Subscriber Value, Gross Contracted Subscriber Value and Gross Renewal Subscriber Value . Gross Total Subscriber Value represents the sum of Gross Contracted Subscriber Value and Gross Renewal Subscriber Value . Gross Contracted Subscriber Value represents the present value of the remaining net cash flows discounted at 5 % during the initial term of the company’s customer agreements as of the measurement date . It is calculated as the present value of cash flows discounted at 5 % that the company expects to receive from subscribers in future periods as set forth in customer agreements, after deducting expected operating and maintenance costs, equipment replacements costs, distributions to tax equity partners in consolidated joint venture partnership flip structures, and distributions to third party project equity investors . The calculation includes cash flows the company expects to receive in future periods from state incentive and rebate programs, contracted sales of solar renewable energy credits, and awarded net cash flows from grid service programs with utilities or grid operators . Gross Renewal Subscriber Value is the forecasted net present value the company would receive upon or following the expiration of the initial customer agreement term, but before the 30 th anniversary of the system’s activation in the form of cash payments during any applicable renewal period for subscribers as of the measurement date . The company calculates the Gross Renewal Subscriber Value amount at the expiration of the initial contract term assuming either a system purchase or a renewal and a 30 - year customer relationship (although the customer may renew for additional years, or purchase the system), at a contract rate equal to 90 % of the customer’s contractual rate in effect at the end of the initial contract term . After the initial contract term, the company’s customer agreements typically automatically renew on an annual basis and the rate is initially set at up to a 10 % discount to then - prevailing utility power prices . These operational metrics are not necessarily comparable to the same or similar metrics as calculated by other companies . This presentation also contains market data, statistical data, estimates and forecasts that are based on independent industry publications or other publicly available information, as well as other information based on our internal sources . This information involves many assumptions and limitations, and you are cautioned not to give undue weight to such information . Some data are also based on XL Fleet’s good faith estimates, which are derived from its review of internal sources as well as the independent sources described above . Although XL Fleet believes these sources are reliable, we have not independently verified the accuracy or completeness of the information contained in the industry publications and other publicly available information . Accordingly, XL Fleet makes no representations as to the accuracy or completeness of that information nor do we undertake to update such information after the date of this presentation . Copyright Statement

4 Management Presenters Eric Tech CEO, XL Fleet Don Klein CFO, XL Fleet Christian Fong CEO, Spruce Power President, XL Fleet

5 Agenda 01 Introduction Eric Tech, Chief Executive Officer, XL Fleet 03 Market Overview & Growth Strategy Christian Fong, Chief Executive Officer, Spruce Power and President, XL Fleet 02 Spruce Overview Eric Tech, Chief Executive Officer, XL Fleet 04 Financial Overview Don Klein, Chief Financial Officer, XL Fleet

1. Introduction

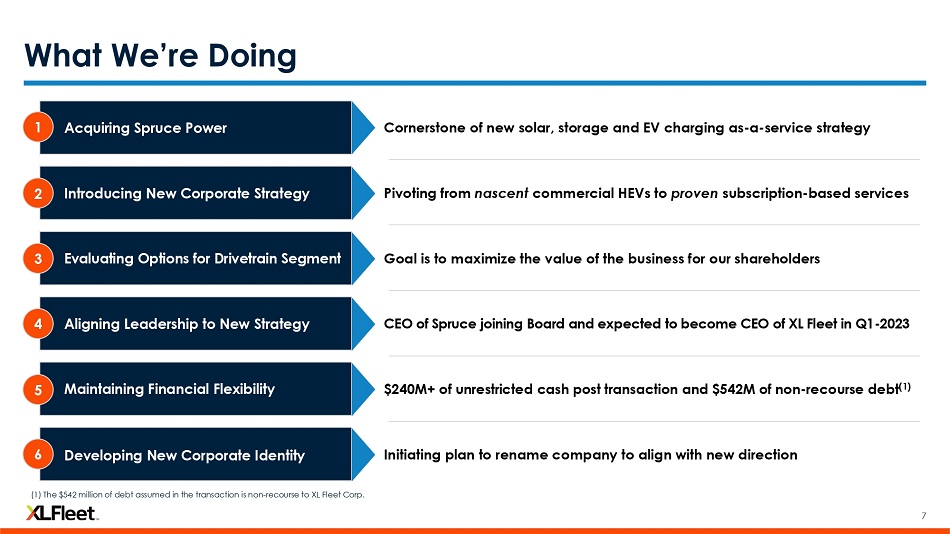

7 Acquiring Spruce Power Introducing New Corporate Strategy Evaluating Options for Drivetrain Segment Aligning Leadership to New Strategy Maintaining Financial Flexibility Pivoting from nascent commercial HEVs to proven subscription - based services Goal is to maximize the value of the business for our shareholders CEO of Spruce joining Board and expected to become CEO of XL Fleet in Q1 - 2023 $240M+ of unrestricted cash post transaction and $542M of non - recourse debt (1) Cornerstone of new solar, storage and EV charging as - a - service strategy What We’re Doing Developing New Corporate Identity Initiating plan to rename company to align with new direction (1) The $542 million of debt assumed in the transaction is non - recourse to XL Fleet Corp. 5 3 2 2 3 5 4 6 1

8 Founded: 2012 Largest privately - held owner and operator of residential rooftop solar systems in the U.S. • More than 52,000 Subscribers across 16 states (1) • 343 MWdc of generating capacity (1) • Founded by one of the three co - founders of Sunrun • 10+ years of experience servicing rooftop solar systems and energy efficiency improvements • Doubled revenues since 2019 Spruce Power Snapshot Key Metrics Note: MWdc = Megawatts of direct current. (1) As of June 30, 2022. (2) For the 12 months ended June 30, 2022. Figures are preliminary, unaudited and are subject to change. See page 31 for a reconciliation from GAAP Net Income to Adjusted EBITDA. Revenues and Adjusted EBITDA exclude $3 million of estimated purchase accounting adjustments related to the elimination of deferred revenue. (3) As of September 1, 2022. (4) See page 27 for a definition of Gross Total Subscriber Value.

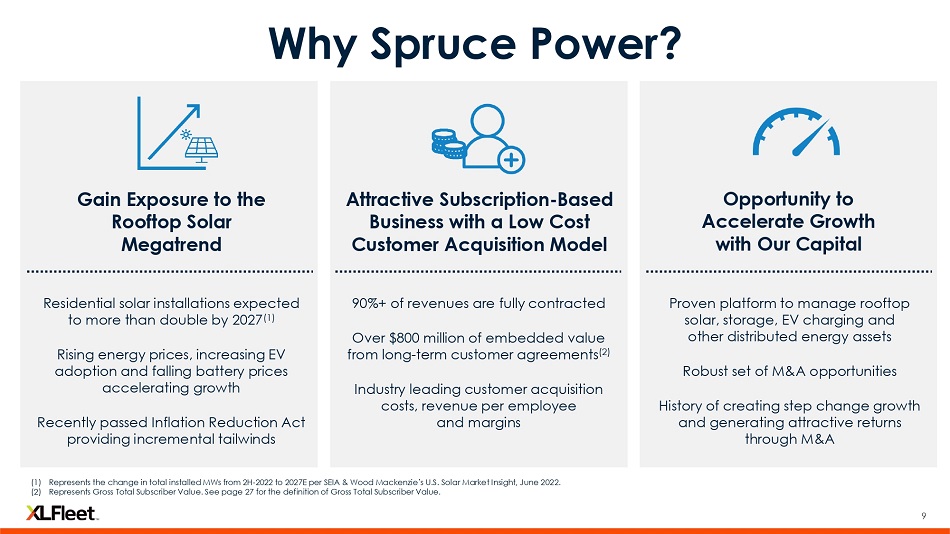

9 Gain Exposure to the Rooftop Solar Megatrend Attractive Subscription - Based Business with a Low Cost Customer Acquisition Model Opportunity to Accelerate Growth with Our Capital Residential solar installations expected to more than double by 2027 (1) Rising energy prices, increasing EV adoption and falling battery prices accelerating growth Recently passed Inflation Reduction Act providing incremental tailwinds Proven platform to manage rooftop solar, storage, EV charging and other distributed energy assets Robust set of M&A opportunities History of creating step change growth and generating attractive returns through M&A 90%+ of revenues are fully contracted Over $800 million of embedded value from long - term customer agreements (2) Industry leading customer acquisition costs, revenue per employee and margins Why Spruce Power? (1) Represents the change in total installed MWs from 2H - 2022 to 2027E per SEIA & Wood Mackenzie’s U.S. Solar Market Insight, June 2 022. (2) Represents Gross Total Subscriber Value. See page 27 for the definition of Gross Total Subscriber Value.

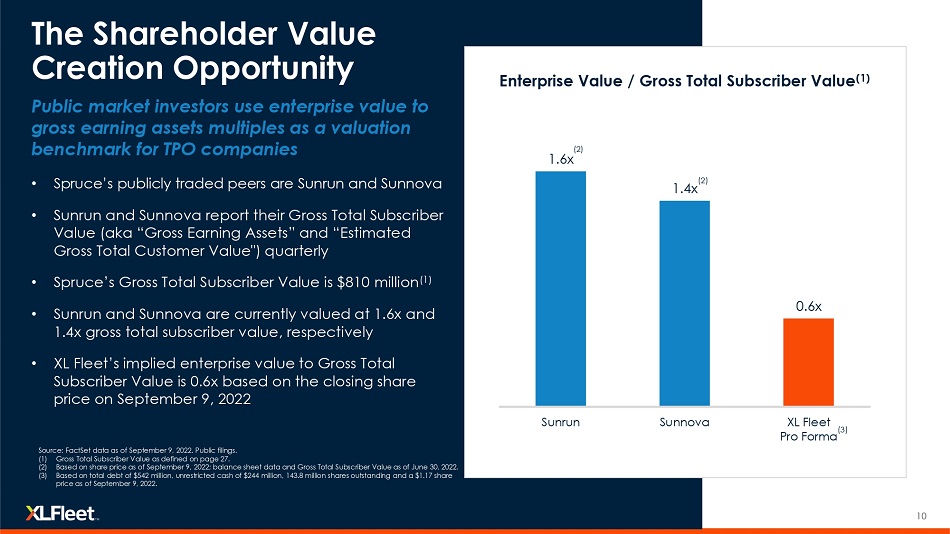

10 Public market investors use enterprise value to gross earning assets multiples as a valuation benchmark for TPO companies • Spruce’s publicly traded peers are Sunrun and Sunnova • Sunrun and Sunnova report their Gross Total Subscriber Value (aka “Gross Earning Assets” and “Estimated Gross Total Customer Value") quarterly • Spruce’s Gross Total Subscriber Value is $810 million (1) • Sunrun and Sunnova are currently valued at 1.6x and 1.4x gross total subscriber value, respectively • XL Fleet’s implied enterprise value to Gross Total Subscriber Value is 0.6x based on the closing share price on September 9, 2022 The Shareholder Value Creation Opportunity Enterprise Value / Gross Total Subscriber Value (1) 1.6x 1.4x 0.6x Sunrun Sunnova XL Fleet Pro Forma Source: FactSet data as of September 9, 2022. Public filings. (1) Gross Total Subscriber Value as defined on page 27. (2) Based on share price as of September 9, 2022; balance sheet data and Gross Total Subscriber Value as of June 30, 2022. (3) Based on total debt of $542 million, unrestricted cash of $244 million, 143.8 million shares outstanding and a $1.17 share price as of September 9, 2022. (3)

2. Spruce Overview

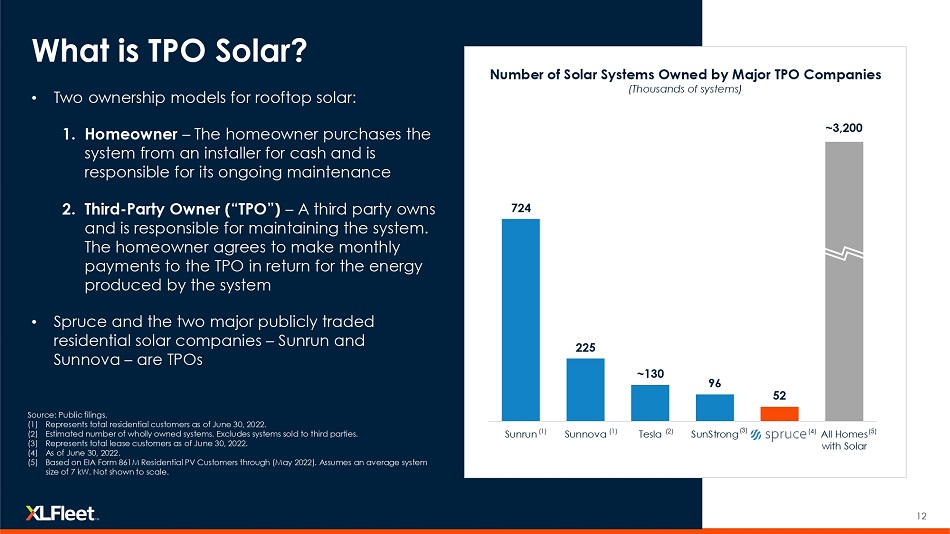

12 724 225 ~ 130 96 52 Sunrun Sunnova Tesla SunStrong All Homes with Solar • Two ownership models for rooftop solar: 1. Homeowner – The homeowner purchases the system from an installer for cash and is responsible for its ongoing maintenance 2. Third - Party Owner (“TPO”) – A third party owns and is responsible for maintaining the system. The homeowner agrees to make monthly payments to the TPO in return for the energy produced by the system • Spruce and the two major publicly traded residential solar companies – Sunrun and Sunnova – are TPOs What is TPO Solar? Number of Solar Systems Owned by Major TPO Companies Source: Public filings. (1) Represents total residential customers as of June 30, 2022. (2) Estimated number of wholly owned systems. Excludes systems sold to third parties. (3) Represents total lease customers as of June 30, 2022. (4) As of June 30, 2022. (5) Based on EIA Form 861M Residential PV Customers through (May 2022). Assumes an average system size of 7 kW. Not shown to scale. (3) (4)

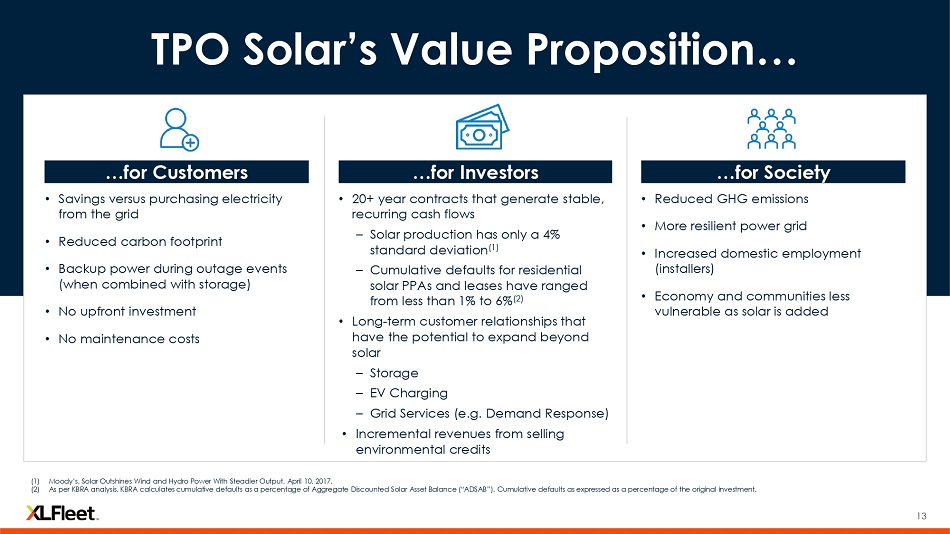

13 TPO Solar’s Value Proposition… …for Customers • Savings versus purchasing electricity from the grid • Reduced carbon footprint • Backup power during outage events (when combined with storage) • No upfront investment • No maintenance costs • 20+ year contracts that generate stable, recurring cash flows – Solar production has only a 4% standard deviation (1) – Cumulative defaults for residential solar PPAs and leases have ranged from less than 1% to 6% (2) • Long - term customer relationships that have the potential to expand beyond solar – Storage – EV Charging – Grid Services (e.g. Demand Response) • Incremental revenues from selling environmental credits • Reduced GHG emissions • More resilient power grid • Increased domestic employment (installers) • Economy and communities less vulnerable as solar is added …for Investors …for Society

14 Spruce Overview Spruce Power is the largest privately held Third Party Owner (“TPO”) of residential solar rooftop systems in the U.S.

15 Servicing Platform Merger & Acquisitions Group Rooftop Solar Portfolio The Spruce Business

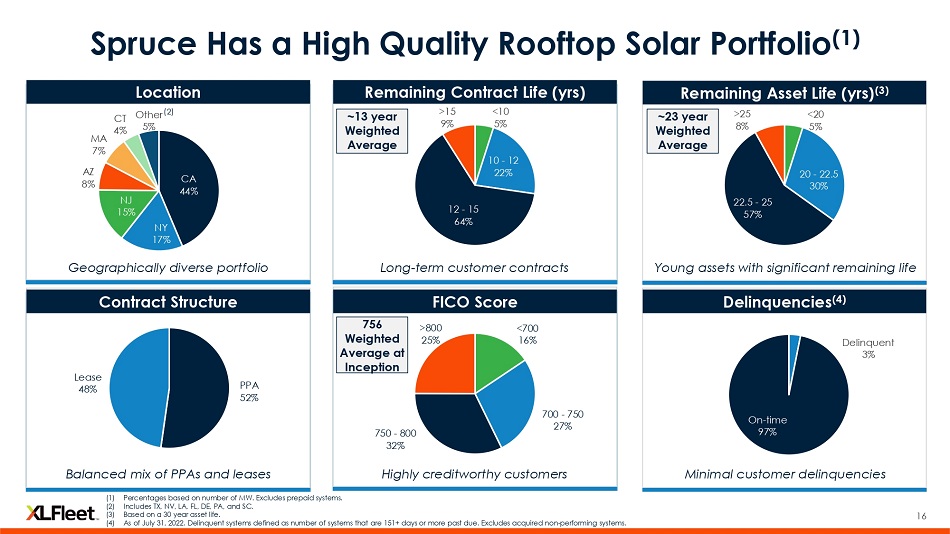

16 <700 16% 700 - 750 27% 750 - 800 32% >800 25% <20 5% 20 - 22.5 30% 22.5 - 25 57% >25 8% ~23 year Weighted Average <10 5% 10 - 12 22% 12 - 15 64% >15 9% Remaining Asset Life (yrs) (3) Remaining Contract Life (yrs) CA 44% NY 17% NJ 15% AZ 8% MA 7% CT 4% Other 5% Spruce Has a High Quality Rooftop Solar Portfolio (1) Location Contract Structure FICO Score Delinquencies (4) ~13 year Weighted Average 756 Weighted Average at Inception (1) Percentages based on number of MW. Excludes prepaid systems. (2) Includes TX, NV, LA, FL, DE, PA, and SC. (3) Based on a 30 year asset life. (4) As of July 31, 2022. Delinquent systems defined as number of systems that are 151+ days or more past due. Excludes acquired n on - performing systems. Highly creditworthy customers Minimal customer delinquencies Long - term customer contracts Young assets with significant remaining life Geographically diverse portfolio Balanced mix of PPAs and leases PPA 52% Lease 48% Delinquent 3% On - time 97%

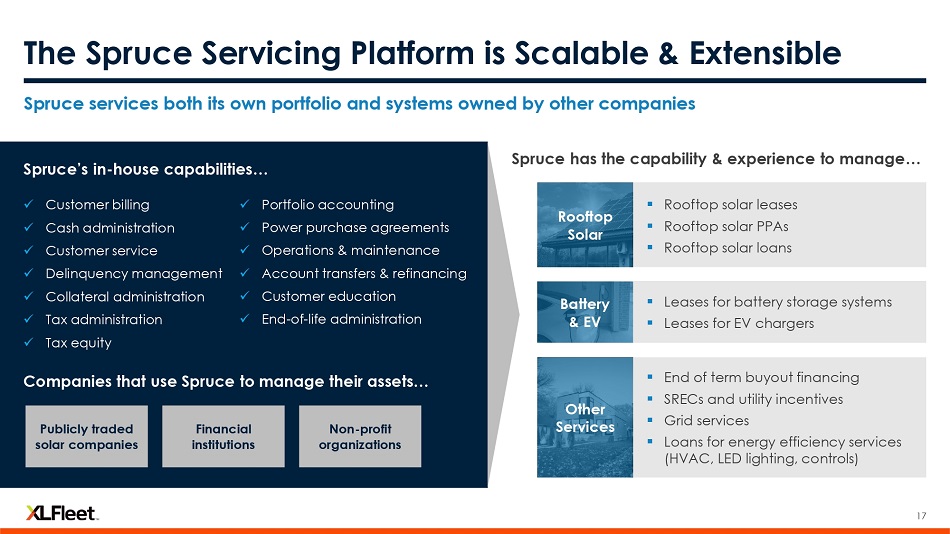

17 The Spruce Servicing Platform is Scalable & Extensible Spruce services both its own portfolio and systems owned by other companies Rooftop Solar Battery & EV Other Services ▪ Rooftop solar leases ▪ Rooftop solar PPAs ▪ Rooftop solar loans ▪ Leases for battery storage systems ▪ Leases for EV chargers ▪ End of term buyout financing ▪ SRECs and utility incentives ▪ Grid services ▪ Loans for energy efficiency services (HVAC, LED lighting, controls) Companies that use Spruce to manage their assets… Spruce’s in - house capabilities… Publicly traded solar companies Financial institutions Non - profit organizations x Customer billing x Cash administration x Customer service x Delinquency management x Collateral administration x Tax administration x Tax equity x Portfolio accounting x Power purchase agreements x Operations & maintenance x Account transfers & refinancing x Customer education x End - of - life administration Spruce has the capability & experience to manage…

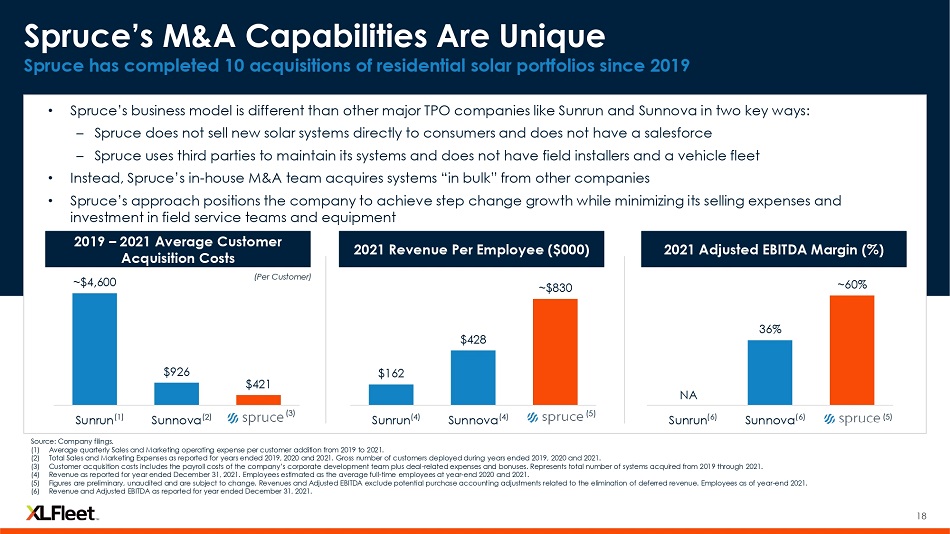

18 Spruce’s M&A Capabilities Are Unique Spruce has completed 10 acquisitions of residential solar portfolios since 2019 • Spruce’s business model is different than other major TPO companies like Sunrun and Sunnova in two key ways: – Spruce does not sell new solar systems directly to consumers and does not have a salesforce – Spruce uses third parties to maintain its systems and does not have field installers and a vehicle fleet • Instead, Spruce’s in - house M&A team acquires systems “in bulk” from other companies • Spruce’s approach positions the company to achieve step change growth while minimizing its selling expenses and investment in field service teams and equipment Source: Company filings. (1) Average quarterly Sales and Marketing operating expense per customer addition from 2019 to 2021. (2) Total Sales and Marketing Expenses as reported for years ended 2019, 2020 and 2021. Gross number of customers deployed during ye ars ended 2019, 2020 and 2021. (3) Customer acquisition costs includes the payroll costs of the company’s corporate development team plus deal - related expenses and bonuses. Represents total number of systems acquired from 2019 through 2021. (4) Revenue as reported for year ended December 31, 2021. Employees estimated as the average full - time employees at year - end 2020 an d 2021. (5) Figures are preliminary, unaudited and are subject to change. Revenues and Adjusted EBITDA exclude potential purchase account ing adjustments related to the elimination of deferred revenue. Employees as of year - end 2021. (6) Revenue and Adjusted EBITDA as reported for year ended December 31, 2021. ~ $4,600 $926 $421 Sunrun Sunnova $162 $428 ~ $830 Sunrun Sunnova (Per Customer) 36% ~ 60% Sunrun Sunnova NA (3) (5) (5) (1) (2) (4) (4) (6) (6) 2019 – 2021 Average Customer Acquisition Costs 2021 Revenue Per Employee ($000) 2021 Adjusted EBITDA Margin (%)

3. Market Overview & Growth Strategy

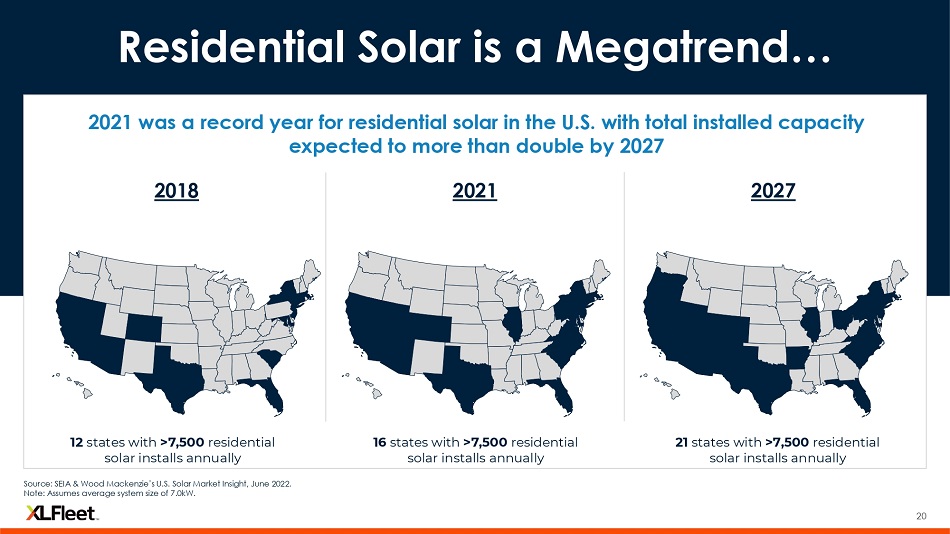

20 2027 2021 Residential Solar is a Megatrend… 2018 2021 was a record year for residential solar in the U.S. with total installed capacity expected to more than double by 2027 12 states with >7,500 residential solar installs annually 16 states with >7,500 residential solar installs annually 21 states with >7,500 residential solar installs annually Source: SEIA & Wood Mackenzie’s U.S. Solar Market Insight, June 2022. Note: Assumes average system size of 7.0kW.

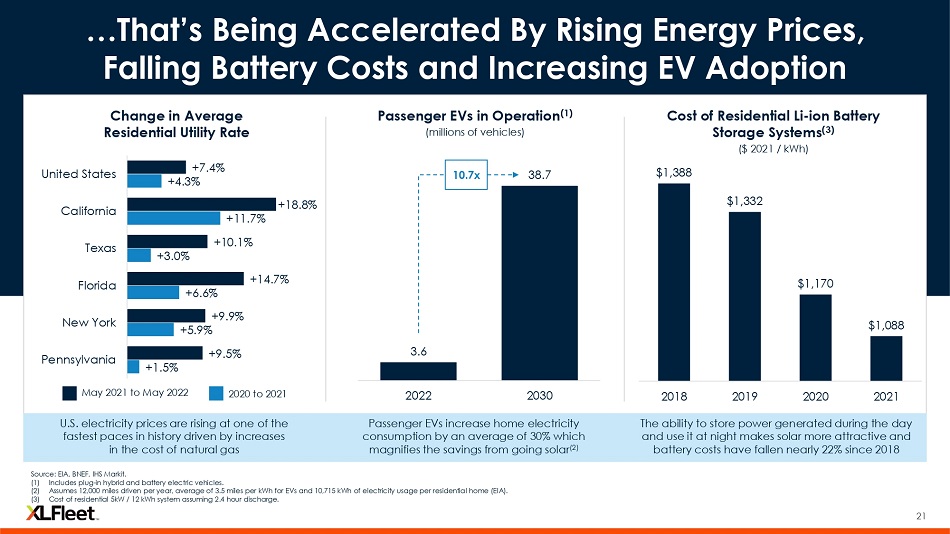

21 3.6 38.7 2022 2030 …That’s Being Accelerated By Rising Energy Prices, Falling Battery Costs and Increasing EV Adoption Change in Average Residential Utility Rate U.S. electricity prices are rising at one of the fastest paces in history driven by increases in the cost of natural gas Passenger EVs increase home electricity consumption by an average of 30% which magnifies the savings from going solar (2) The ability to store power generated during the day and use it at night makes solar more attractive and battery costs have fallen nearly 22% since 2018 Passenger EVs in Operation (1) (millions of vehicles) Cost of Residential Li - ion Battery Storage Systems (3) ($ 2021 / kWh) 2020 to 2021 May 2021 to May 2022 +1.5% +5.9% +6.6% +3.0% +11.7% +4.3% +9.5% +9.9% +14.7% +10.1% +18.8% +7.4% Pennsylvania New York Florida Texas California United States $1,388 $1,332 $1,170 $1,088 2018 2019 2020 2021

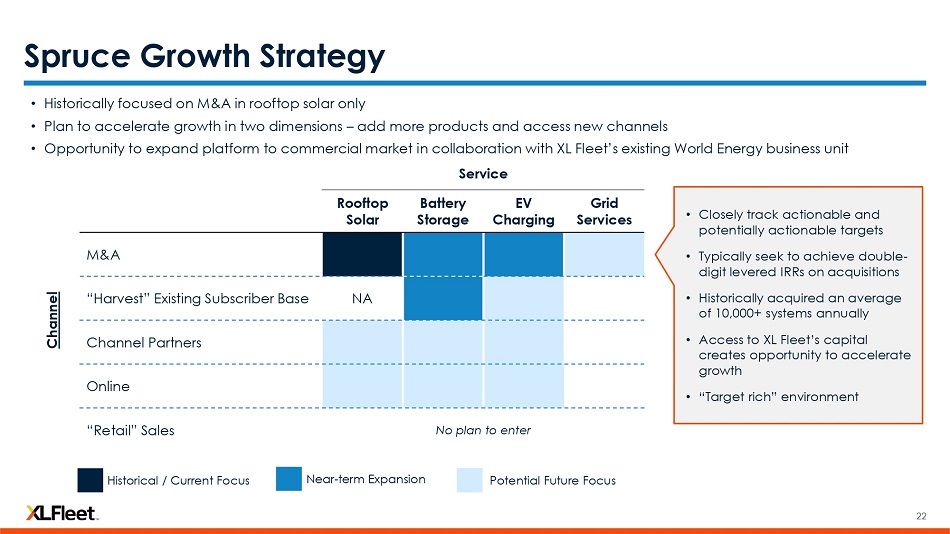

22 Spruce Growth Strategy • Historically focused on M&A in rooftop solar only • Plan to accelerate growth in two dimensions – add more products and access new channels • Opportunity to expand platform to commercial market in collaboration with XL Fleet’s existing World Energy business unit Service Rooftop Solar Battery Storage EV Charging Grid Services Channel M&A “Harvest” Existing Subscriber Base NA Channel Partners Online “Retail” Sales No plan to enter Near - term Expansion Historical / Current Focus Potential Future Focus • Closely track actionable and potentially actionable targets • Typically seek to achieve double - digit levered IRRs on acquisitions • Historically acquired an average of 10,000+ systems annually • Access to XL Fleet’s capital creates opportunity to accelerate growth • “Target rich” environment

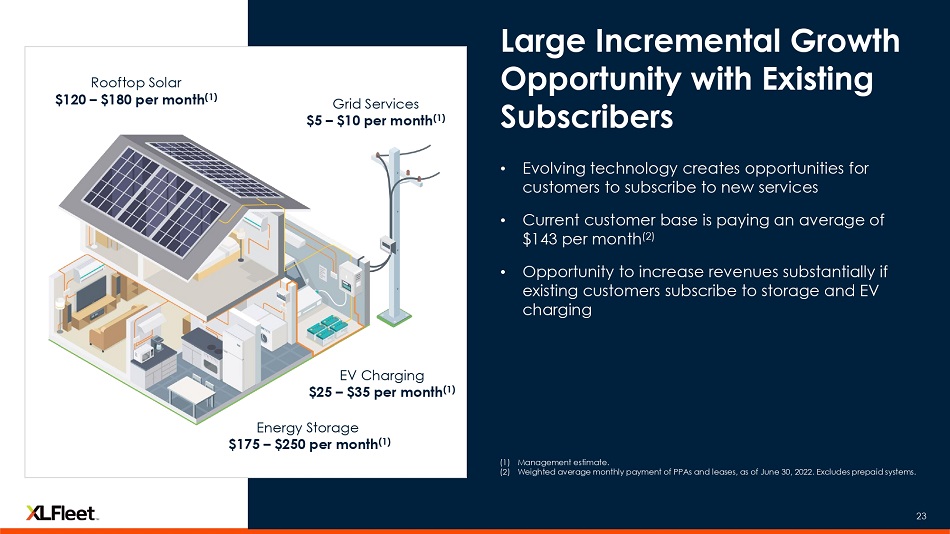

23 23 (1) Management estimate. (2) Weighted average monthly payment of PPAs and leases, as of June 30, 2022. Excludes prepaid systems. • Evolving technology creates opportunities for customers to subscribe to new services • Current customer base is paying an average of $143 per month (2) • Opportunity to increase revenues substantially if existing customers subscribe to storage and EV charging Large Incremental Growth Opportunity with Existing Subscribers Energy Storage $175 – $250 per month (1) Grid Services $5 – $10 per month (1) EV Charging $25 – $35 per month (1)

4. Financial Overview

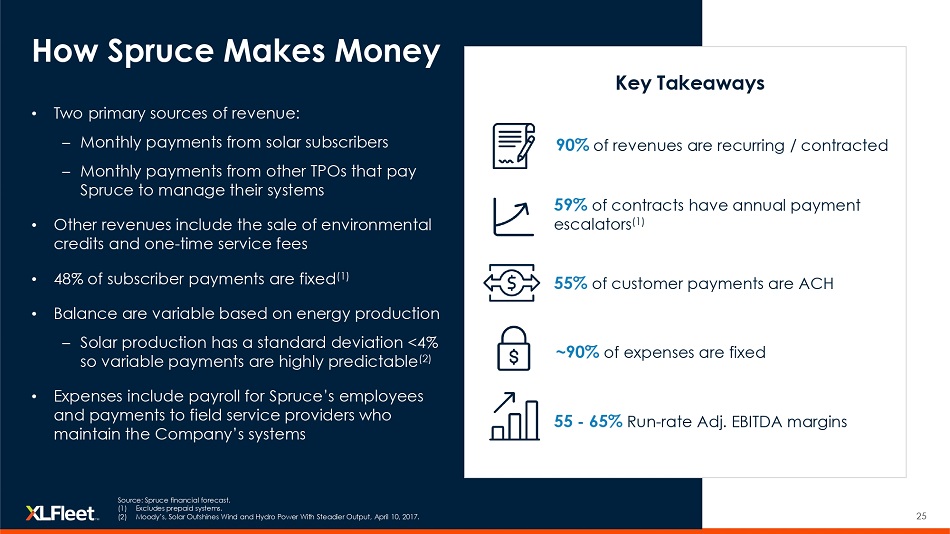

25 • Two primary sources of revenue: – Monthly payments from solar subscribers – Monthly payments from other TPOs that pay Spruce to manage their systems • Other revenues include the sale of environmental credits and one - time service fees • 48% of subscriber payments are fixed (1) • Balance are variable based on energy production – Solar production has a standard deviation <4% so variable payments are highly predictable (2) • Expenses include payroll for Spruce’s employees and payments to field service providers who maintain the Company’s systems How Spruce Makes Money Key Takeaways Source: Spruce financial forecast. (1) Excludes prepaid systems. (2) Moody’s, Solar Outshines Wind and Hydro Power With Steadier Output, April 10, 2017. 90% 59% 55% 55 - 65% ~90%

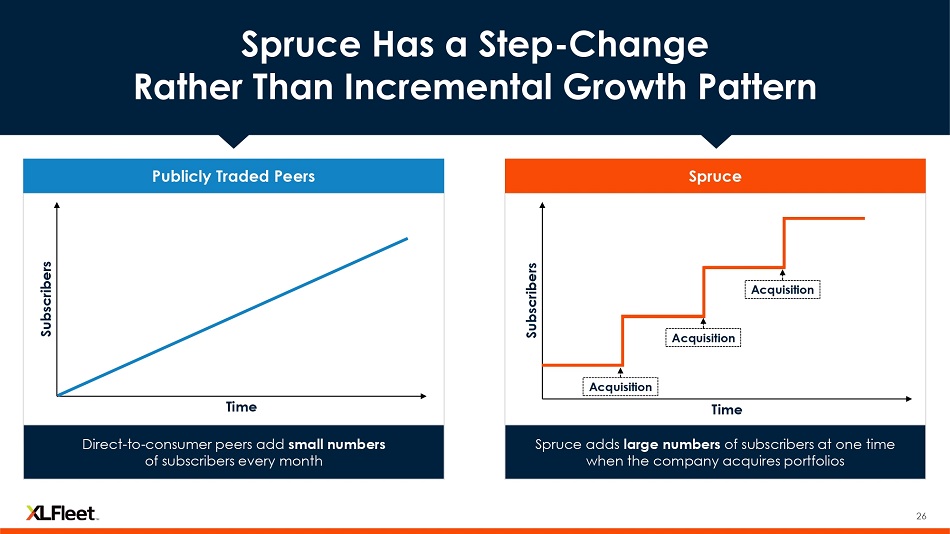

26 Direct - to - consumer peers add small numbers of subscribers every month Spruce adds large numbers of subscribers at one time when the company acquires portfolios Publicly Traded Peers Spruce Spruce Has a Step - Change Rather Than Incremental Growth Pattern

27 Subscriber Value Metrics • Gross Total Subscriber Value reflects the remaining projected net cash flows from current customers discounted at 5% • Projected cash flows include the customer’s initial agreement plus renewal (1) Pro forma for acquisition of 2,655 systems completed in July 2022. (2) Gross Contracted Subscriber Value represents the present value of the remaining net cash flows discounted at 5% during the initial term of the company’s cus tomer agreements as of the measurement date. It is calculated as the present value of cash flows discounted at 5% that the company expects to receive from subscribe rs in future periods as set forth in customer agreements, after deducting expected operating and maintenance costs, equipment replacements costs, distributions to tax equity partners in consolidated joi nt venture partnership flip structures, and distributions to third party project equity investors. The calculation includes cash flows the company expects to receive in future periods from state inc ent ive and rebate programs, contracted sales of solar renewable energy credits, and awarded net cash flows from grid service programs with utilities or grid operators. (3) Gross Renewal Subscriber Value is the forecasted net present value the company would receive upon or following the expiration of the initial customer agr eement term, but before the 30th anniversary of the system’s activation in the form of cash payments during any applicable renewal period for subscribers as of the measur eme nt date. The company calculates the Gross Renewal Subscriber Value amount at the expiration of the initial contract term assuming either a system purchase or a renewal and a 30 - year customer rela tionship (although the customer may renew for additional years, or purchase the system), at a contract rate equal to 90% of the customer’s contractual rate in effect at the end of the initial con tract term. After the initial contract term, the company’s customer agreements typically automatically renew on an annual basis and the rate is initially set at up to a 10% discount to then - prevai ling utility power prices. (4) Gross Total Subscriber Value represents the sum of Gross Contracted Subscriber Value and Gross Renewal Subscriber Value. ($ in millions) As of June 30, 2022 (1) Gross Contracted Subscriber Value (2) $560 Gross Renewal Subscriber Value (3) 250 Gross Total Subscriber Value (4) $810

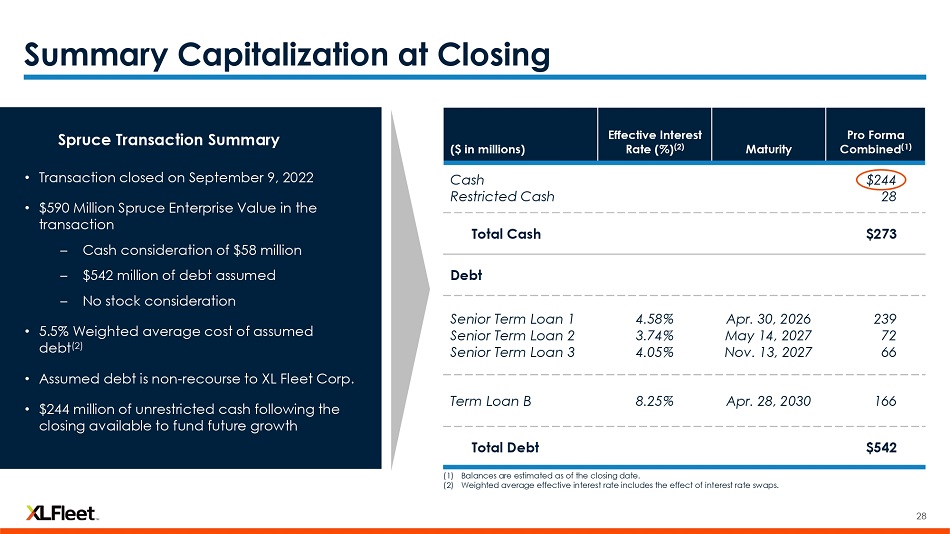

28 Summary Capitalization at Closing ($ in millions) Effective Interest Rate (%) (2) Maturity Pro Forma Combined (1) Cash Restricted Cash $244 28 Total Cash $273 Debt Senior Term Loan 1 Senior Term Loan 2 Senior Term Loan 3 4.58% 3.74% 4.05% Apr. 30, 2026 May 14, 2027 Nov. 13, 2027 239 72 66 Term Loan B 8.25% Apr. 28, 2030 166 Total Debt $542 (1) Balances are estimated as of the closing date. (2) Weighted average effective interest rate includes the effect of interest rate swaps. • Transaction closed on September 9, 2022 • $590 Million Spruce Enterprise Value in the transaction – Cash consideration of $58 million – $542 million of debt assumed – No stock consideration • 5.5% Weighted average cost of assumed debt (2) • Assumed debt is non - recourse to XL Fleet Corp. • $244 million of unrestricted cash following the closing available to fund future growth Spruce Transaction Summary

29 (1) Represents the change in total installed MWs from 2H - 2022 to 2027E per SEIA & Wood Mackenzie’s U.S. Solar Market Insight, June 2 022. (2) Spruce’s Gross Subscriber Value as defined on page 27. (3) Based on unrestricted cash of $244 million, 143.8 million of shares outstanding and a share price of $1.17 as of September 9, 2022. (4) Share price of $1.17 as of September 9, 2022. Shares outstanding of 142.8 million. Balance sheet data as of June 30, 2022 Three Reasons to Invest in XL Fleet

30 Appendix

31 Non - GAAP Reconciliation of Spruce Power Net Income to Adjusted EBITDA Note : For the 12 months ended June 30 , 2022 . Figures are preliminary, unaudited and are subject to change . Adjusted EBITDA excludes $ 3 million of estimated purchase accounting adjustments related to the elimination of deferred revenue . (1) Represents unrealized gains on the fair value of interest rate swaps . (2) Represents a non - cash loss on the sale the company’s equity interests in an ABS trust . (3) Represents the cost of upgrading meters used in the company’s solar systems from 3 G to 4 G capability in certain jurisdictions that are not expected to reoccur once the company has completed the replacement campaign . (4) Represents certain one - time costs related to the company’s transition from an outsourced billing and collections provider to an in - house system . (5) Represents professional fees, transaction bonuses and certain other one - time costs related to the company’s acquisition of a solar system portfolio and other one - time bonuses . (6) Represents professional fees, rating agency fees and certain other one - time costs related to the company’s preparation for a syndicated term loan financing . (7) Represents certain one - time costs related to the implementation of a new data warehouse and website for the company, the termination of a software agreement and the relocation and expansion of the company’s offices . ($ in millions) Twelve Months Ended June 30, 2022 Net income $14.9 Interest expense, (net) 31.2 Depreciation and amortization 25.4 Unrealized gain on derivatives (1) (35.4) Loss on disposal of assets (2) 1.1 Meter upgrade campaign (3) 4.8 Billing platform transition (4) 3.4 M&A costs and deal bonuses (5) 3.8 Syndicated term loan financing costs (6) 0.7 One - time IT and office relocation costs (7) 1.2 Adjusted EBITDA $51.1