Western New England Bancorp, Inc. 8-K

Exhibit 99.1

| |

For

further information contact:

James C. Hagan, President and CEO

Guida R. Sajdak, Executive Vice President and CFO

Meghan Hibner, Vice President and Investor Relations Officer

413-568-1911 |

| |

|

WESTERN

NEW ENGLAND BANCORP, INC. REPORTS RESULTS FOR THREE AND SIX MONTHS

ENDED

JUNE 30, 2022 AND DECLARES QUARTERLY CASH DIVIDEND

THE

COMPANY ALSO ANNOUNCES A NEW 5% SHARE REPURCHASE PLAN

Westfield,

Massachusetts, July 26, 2022: Western New England Bancorp, Inc. (the “Company” or “WNEB”) (NasdaqGS:

WNEB), the holding company for Westfield Bank (the “Bank”), announced today the unaudited results of operations for

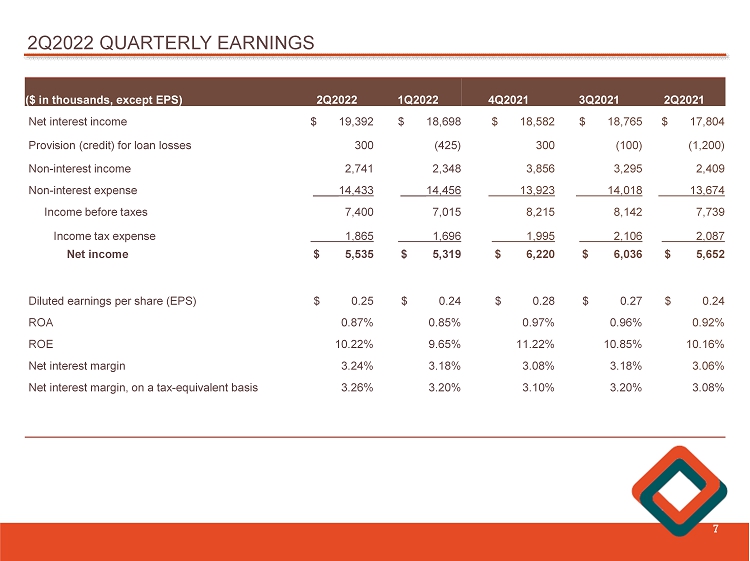

the three and six months ended June 30, 2022. For the three months ended June 30, 2022, the Company reported net income of $5.5

million, or $0.25 per diluted share, compared to net income of $5.7 million, or $0.24 per diluted share, for the three months

ended June 30, 2021. On a linked quarter basis, net income was $5.5 million, or $0.25 per diluted share, as compared to net income

of $5.3 million, or $0.24 per diluted share, for the three months ended March 31, 2022. For the six months ended June 30, 2022,

net income was $10.9 million, or $0.49 per diluted share, compared to net income of $11.4 million, or $0.47 per diluted share,

for the six months ended June 30, 2021.

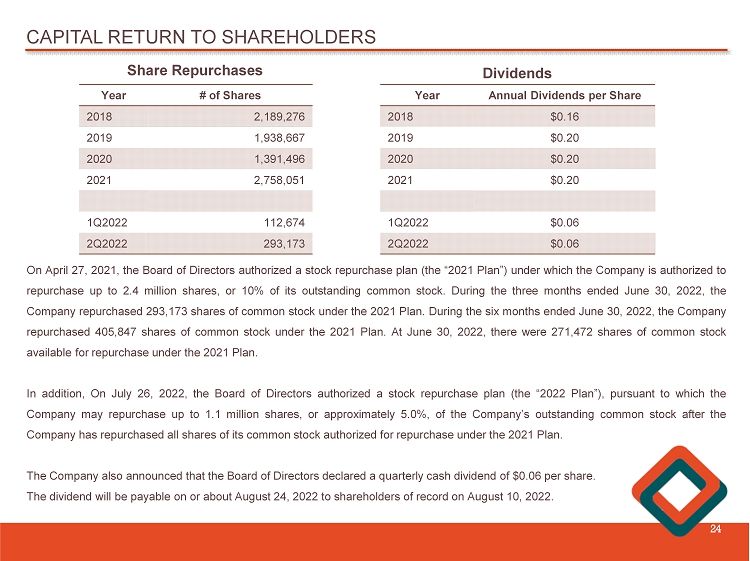

The

Company also announced that the Board of Directors declared a quarterly cash dividend of $0.06 per share on the Company’s

common stock. The dividend will be payable on or about August 24, 2022 to shareholders of record on August 10, 2022. In addition,

the Board of Directors authorized a stock repurchase plan (the “2022 Plan”), pursuant to which the Company may repurchase

up to 1.1 million shares of the Company’s common stock, or approximately 5.0%, of the Company’s outstanding shares,

of common stock as of the date the 2022 Plan was adopted. Repurchase under the 2022 Plan may begin after the Company has repurchased

all of the shares of its common stock authorized for repurchase under the stock repurchase plan adopted in 2021 (the “2021

Plan”). The 2021 Plan was announced on April 27, 2021 and as of June 30, 2022, there were 271,472 shares of common stock

available for purchase under the 2021 Plan.

“The

Company continues to experience strong quarterly earnings adding to the momentum from last year’s record profitability.

We are pleased to report solid earnings for the second quarter of 2022 along with strong overall loan growth. We remain focused

on executing our strategy of driving commercial loan growth, which has been a key contributor to the Company’s ongoing profitability,”

said James C. Hagan, President and Chief Executive Officer. “We remain optimistic about the Company’s growth opportunities

in 2022 and we continue to be successful despite the current economic environment.

The

Company continues to show strong loan growth in key loan categories funded by excess cash generated through increases in our core

deposits. We saw strong organic core deposit grow of $96.7 million, or 5.2%, since year-end, which will be beneficial in a rising

interest rate environment. We are pleased to report that our total loan portfolio increased $133.7 million, or 7.3% during the

six months ended June 30, 2022, excluding Paycheck Protection Program (“PPP”) loans that were forgiven by the Small

Business Administration (“SBA”). As we continue to add new customer relationships throughout New England and in key

strategic lending areas, we have seen the strongest growth from our commercial real estate lending portfolio, which increased

$94.9 million, or 9.7%, during the six months ended June 30, 2022. Commercial and industrial loans continue to be added to our

loan portfolio and remain a strategic priority. We continue to be mindful of certain economic and business conditions, such as

inflation, utilization of accumulated cash to fund operations, and supply chain issues that may affect some of our business customers,

as well as the additional anticipated Federal Reserve interest rate increases, but remain optimistic about our loan portfolio

growth and meeting the needs of our business and commercial customers.

We

believe the balance sheet management steps we took in 2021 have had a positive impact on earnings and growth and have directly

resulted in an increase in net interest income and the net interest margin, which increased from 3.08% in the fourth quarter of

2021 to 3.24% in the second quarter of 2022. Our disciplined approach to managing funding costs has helped to expand our net interest

margin as we continue to deploy our excess liquidity and core deposits to fund loan growth. Our asset quality remains extremely

solid, with historical lows for nonperforming loans to total loans of 0.21%, and our capital position continues to remain strong.”

Hagan

concluded, “We will continue to implement our various strategic initiatives which have resulted in solid earnings last year

and through the first two quarters of this year and will continue our efforts to grow the Company throughout the remaining quarters

and increase overall shareholder value.”

Key

Highlights:

Loans

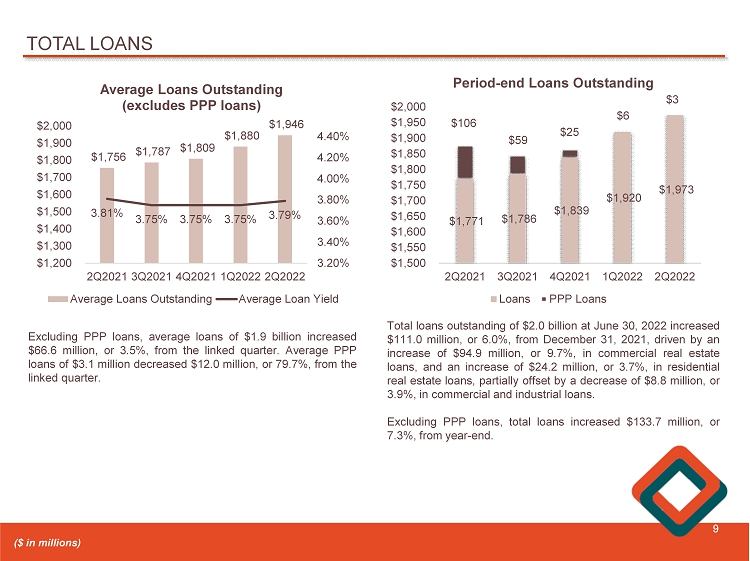

and Deposits. At June 30, 2022, total loans were $2.0 billion, an increase of $111.0 million, or 6.0%, from December 31, 2021.

Excluding PPP loans, total loans increased $133.7 million, or 7.3%, from December 31, 2021, primarily due to a $94.9 million,

or 9.7%, increase in commercial real estate loans from December 31, 2021 to June 30, 2022.

At

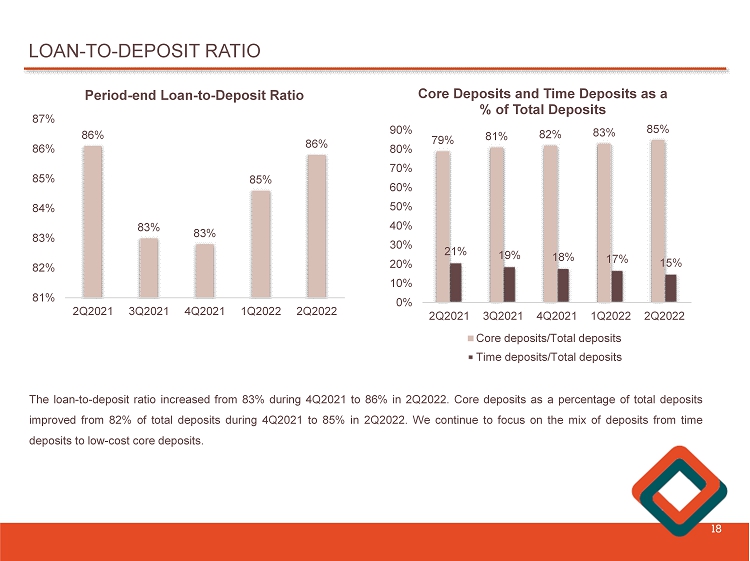

June 30, 2022, total deposits were $2.3 billion, an increase of $45.1 million, or 2.0%, from December 31, 2021. Core deposits,

which include non-interest bearing demand accounts, increased $96.7 million, or 5.2%, from $1.9 billion, or 82.2% of total deposits,

at December 31, 2021, to $2.0 billion, or 84.8% of total deposits at June 30, 2022. The loan to deposit ratio increased from 82.6%

at December 31, 2021 to 85.8% at June 30, 2022.

Allowance

for Loan Losses and Credit Quality. At June 30, 2022, the allowance for loan losses as a percentage of total loans and as

a percentage of nonperforming loans was 0.99% and 476.5%, respectively. At June 30, 2022, nonperforming loans totaled $4.1 million,

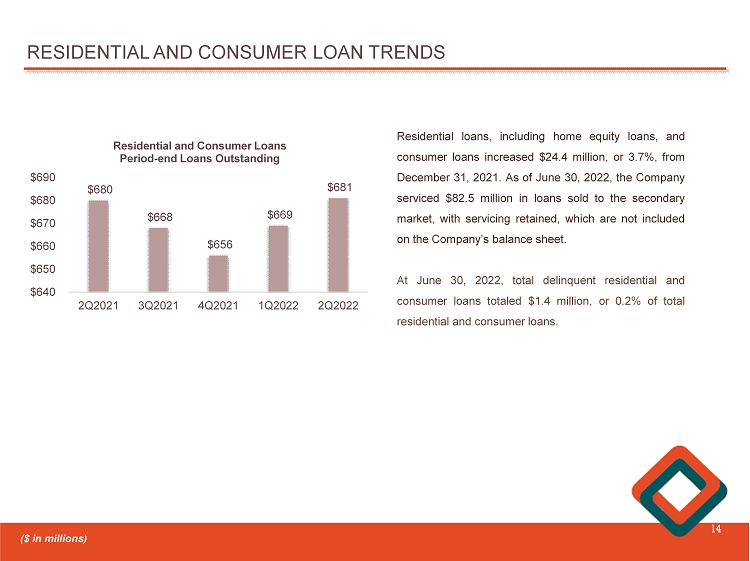

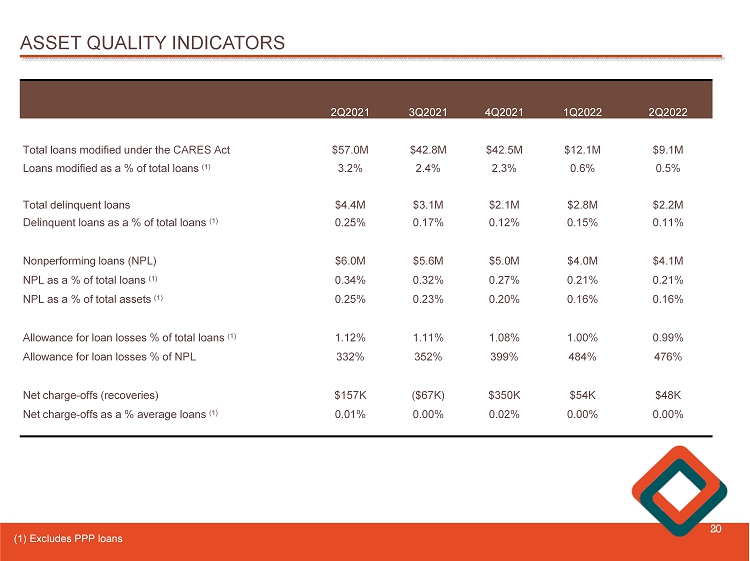

or 0.21% of total loans, compared to $5.0 million, or 0.27% of total loans, at December 31, 2021. Total delinquency increased

$71,000, or 3.3%, from $2.1 million, or 0.11% of total loans at December 31, 2021 to $2.2 million, or 0.11% of total loans at

June 30, 2022.

Net

Interest Margin. The net interest margin was 3.24% for the three months ended June 30, 2022 compared to 3.18% for the three

months ended March 31, 2022. The net interest margin, on a tax-equivalent basis, was 3.26% for the three months ended June 30,

2022, compared to 3.20% for the three months ended March 31, 2022.

Repurchases.

On April 27, 2021, the Board of Directors authorized the 2021 Plan, pursuant to which the Company is authorized to repurchase

up to 2.4 million shares, or 10% of its outstanding common stock, as of the date the 2021 Plan was adopted. During the three months

ended June 30, 2022, the Company repurchased 293,173 shares of common stock under the 2021 Plan. During the six months ended June

30, 2022, the Company repurchased 405,847 shares of common stock under the 2021 Plan. At June 30, 2022, there were 271,472 shares

of common stock available for repurchase under the 2021 Plan.

On

July 26, 2022, the Board of Directors authorized the 2022 Plan, pursuant to which the Company may repurchase up to 1.1 million

shares of common stock, which is approximately 5.0% of the Company’s outstanding shares as of the date the 2022 Plan was

adopted. Repurchases under the 2022 Plan may commence after the Company has repurchased all of the shares of common stock authorized

for repurchase under the 2021 Plan.

The

shares of common stock repurchased under the 2021 Plan and the 2022 Plan will be purchased from time to time at prevailing market

prices, through open market or privately negotiated transactions, or otherwise, depending upon market conditions. There is no

guarantee as to the exact number, or value, of shares that will be repurchased by the Company, and the Company may discontinue

repurchases at any time that management determines additional repurchases are not warranted. The timing and amount of additional

share repurchases under the 2021 Plan and the 2022 Plan will depend on a number of factors, including the Company’s stock

price performance, ongoing capital planning considerations, general market conditions, and applicable legal requirements.

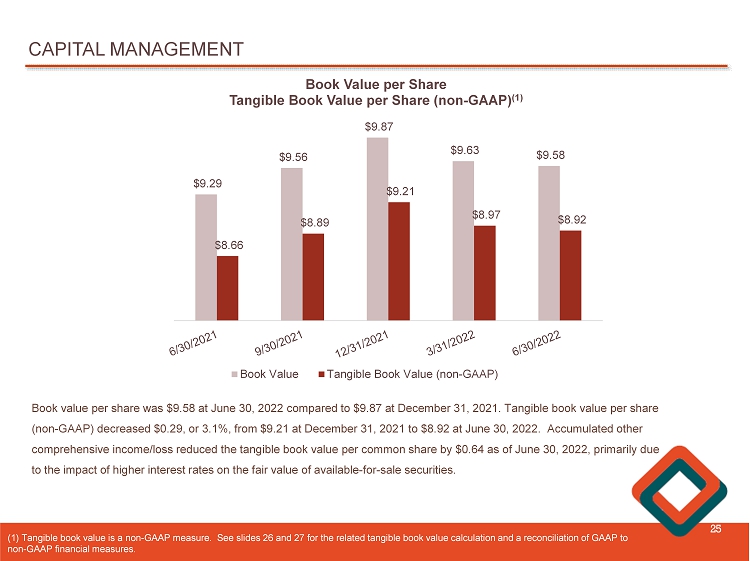

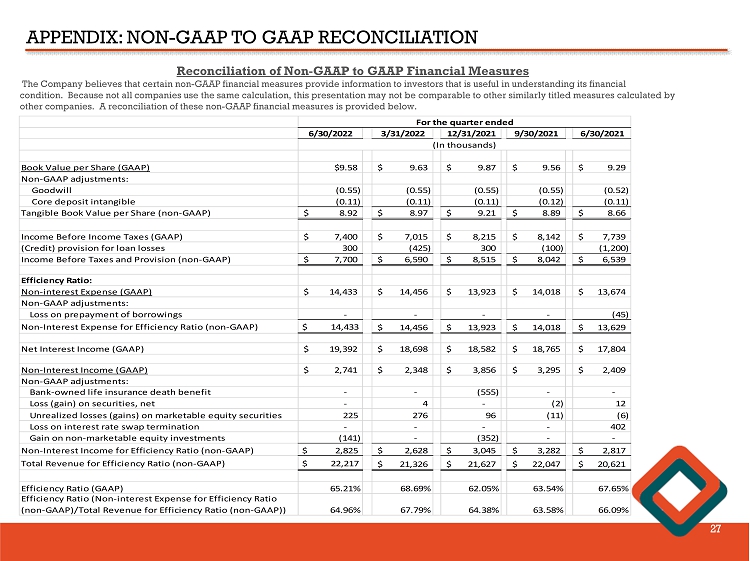

Capital

Management. Book value per share was $9.58 at June 30, 2022, compared to $9.87 at December 31, 2021, while tangible book value

per share, a non-GAAP financial measure, decreased $0.29, or 3.1%, from $9.21 at December 31, 2021 to $8.92 at June 30, 2022.

During the six months ended June 30, 2022, the change in accumulated other comprehensive income/loss (“AOCI”) reduced

the tangible book value per common share by $0.64 as of June 30, 2022, primarily due to the impact of higher interest

rates on the fair value of available-for-sale securities. Tangible book value is a non-GAAP measure. See pages 18-21 for

the related tangible book value calculation and a reconciliation of GAAP to non-GAAP financial measures. As of June 30, 2022,

the Company’s and the Bank’s regulatory capital ratios continued to exceed the levels required to be considered “well-capitalized”

under federal banking regulations.

Net

Income for the Three Months Ended June 30, 2022 Compared to the Three Months Ended March 31, 2022.

The

Company reported net income of $5.5 million, or $0.25 per diluted share, for the three months ended June 30, 2022, compared to

net income of $5.3 million, or $0.24 per diluted share, for the three months ended March 31, 2022. Net interest income increased

$694,000, or 3.7%, non-interest income increased $393,000, or 16.7%, and non-interest expense decreased $23,000, or 0.2%, while

the provision for loan losses increased $725,000, or 170.6%, during the same period. Return on average assets and return on average

equity were 0.87% and 10.22%, respectively, for the three months ended June 30, 2022, compared to 0.85% and 9.65%, respectively,

for the three months ended March 31, 2022.

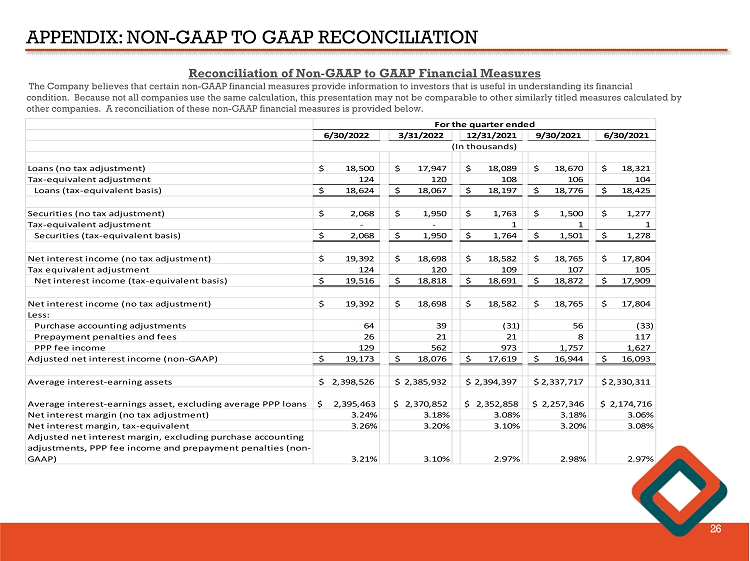

Net

Interest Income and Net Interest Margin

On

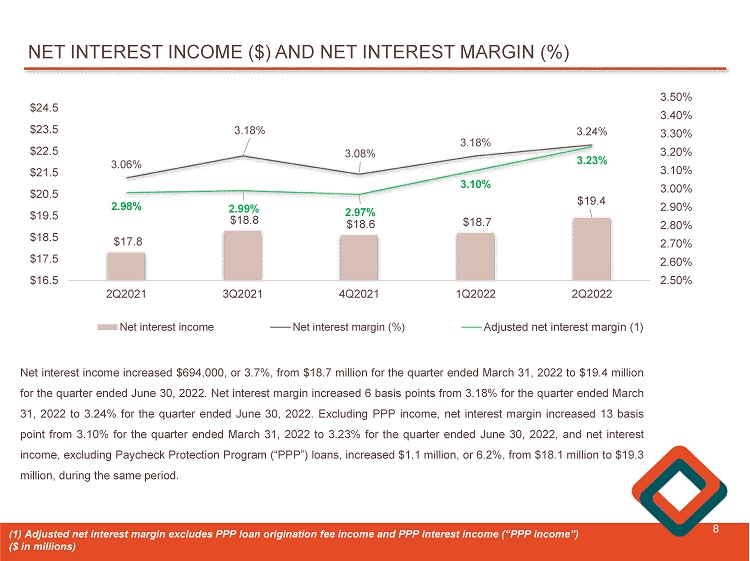

a sequential quarter basis, net interest income increased $694,000, or 3.7%, to $19.4 million for the three months ended June

30, 2022, from $18.7 million for the three months ended March 31, 2022. The increase in net interest income was primarily due

to an increase in interest and dividend income of $703,000, or 3.5%. During the three months ended June 30, 2022 and the three

months ended March 31, 2022, interest and dividend income included PPP interest and fee income (“PPP income”) of $129,000

and $562,000, respectively. During the three months ended June 30, 2022, the Company recorded $64,000 in positive purchase accounting

adjustments, compared to positive purchase accounting adjustments of $39,000 during the three months ended March 31, 2022. Excluding

PPP income and purchase accounting adjustments, net interest income increased $1.1 million, or 6.1%, from the three months ended

March 31, 2022 to the three months ended June 30, 2022.

The

net interest margin was 3.24% for the three months ended June 30, 2022 compared to 3.18% for the three months ended March 31,

2022. The net interest margin, on a tax-equivalent basis, was 3.26% for the three months ended June 30, 2022, compared to 3.20%

for the three months ended March 31, 2022. The average yield on interest-earning assets was 3.47% for the three months ended June

30, 2022, compared to 3.41% for the three months ended March 31, 2022. The average loan yield was 3.83% for the three months ended

June 30, 2022, compared to 3.87% for the three months ended March 31, 2022. Excluding PPP income, the net interest margin was

3.23% for the three months ended June 30, 2022, compared to 3.10% for the three months ended March 31, 2022.

During

the three months ended June 30, 2022, average interest-earning assets increased $12.6 million, or 0.5%, to $2.4 billion, primarily

due to an increase in average loans of $54.6 million, or 2.9%, partially offset by a decrease in short-term investments of $32.1

million, or 56.3%, and a decrease in average securities of $9.9 million, or 2.3%. Excluding PPP loans, average loans increased

$66.6 million, or 3.5%, from the three months ended March 31, 2022 to the three months ended June 30, 2022.

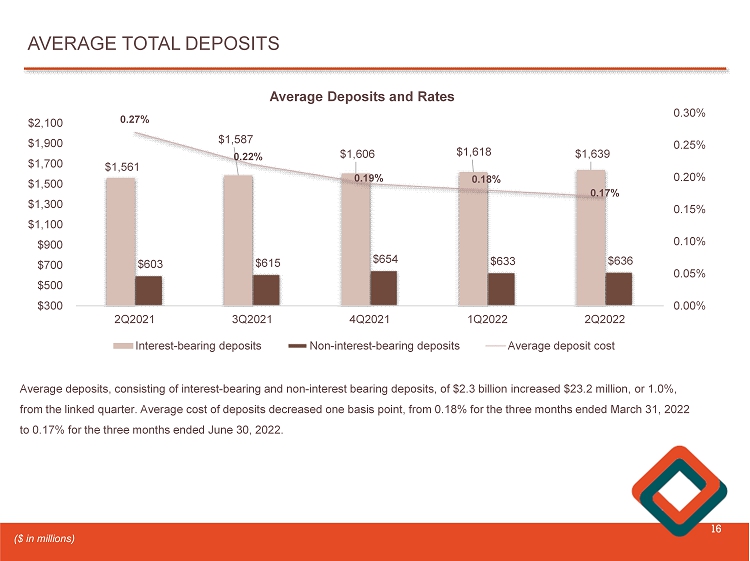

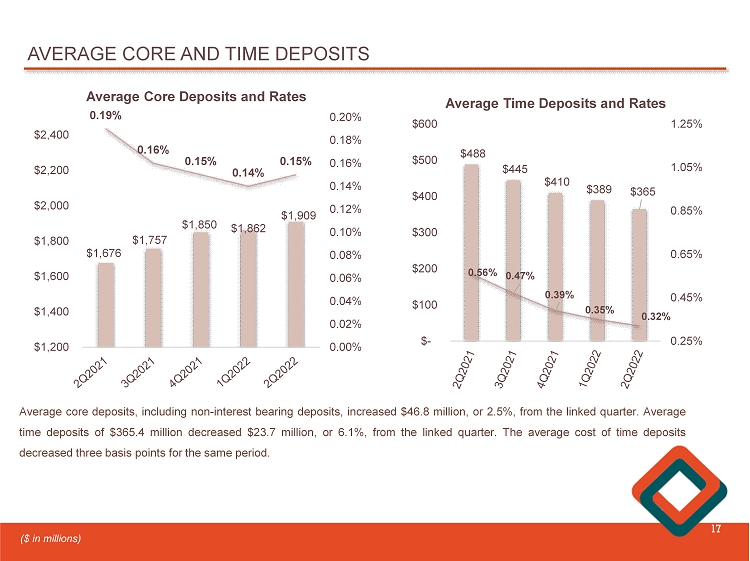

The

average cost of total funds, including non-interest bearing accounts and borrowings, remained unchanged at 0.22% for the three

months ended June 30, 2022, compared to the three months ended March 31, 2022. The average cost of core deposits, including non-interest

bearing demand deposits, increased one basis point to 15 basis points for the three months ended June 30, 2022, from 14 basis

points for the three months ended March 31, 2022. The average cost of time deposits decreased three basis points from 0.35% for

the three months ended March 31, 2022 to 0.32% for the three months ended June 30, 2022. The average cost of borrowings, including

subordinated debt, decreased 55 basis points from 4.65% for the three months ended March 31, 2022 to 4.10% for the three months

ended June 30, 2022. Average demand deposits, an interest-free source of funds, increased $2.6 million, or 0.4%, from $633.1 million,

or 28.1% of total average deposits, for the three months ended March 31, 2022, to $635.7 million, or 28.0% of total average deposits,

for the three months ended June 30, 2022.

Provision

for Loan Losses

During

the three months ended June 30, 2022, the provision for loan losses increased $725,000, from a credit for loan losses of $425,000

for the three months ended March 31, 2022, to a provision for loan losses of $300,000. The increase in the provision for loan

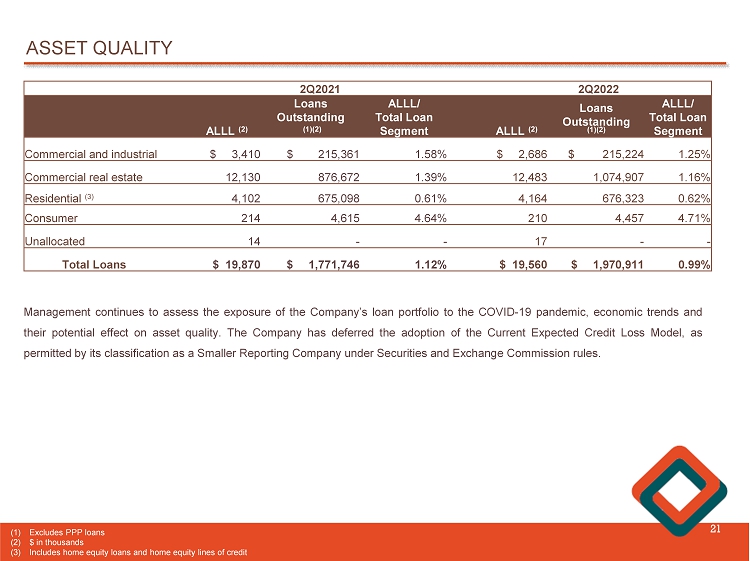

losses was due to strong organic loan growth during the quarter. Management continues to assess the exposure of the Company’s

loan portfolio to the COVID-19 pandemic, economic trends and their potential effect on asset quality. The Company has deferred

the adoption of the Current Expected Credit Loss allowance methodology, as permitted by its classification as a Smaller Reporting

Company under Securities and Exchange Commission rules. Management will continue to closely monitor portfolio conditions and re-evaluate

the adequacy of the allowance.

The

Company recorded net charge-offs of $48,000 for the three months ended June 30, 2022, as compared to net charge-offs of $54,000

for the three months ended March 31, 2022. At June 30, 2022, nonperforming loans totaled $4.1 million, or 0.21% of total loans,

and total delinquency as a percentage of total loans was 0.11%.

Non-Interest

Income

On

a sequential quarter basis, non-interest income increased $393,000, or 16.7%, to $2.7 million for the three months ended June

30, 2022, from $2.3 million for the three months ended March 31, 2022. Service charges and fees increased $172,000, or 8.0%, from

the three months ended March 31, 2022 to $2.3 million for the three months ended June 30, 2022. The Company reported unrealized

losses on marketable equity securities of $225,000 for the three months ended June 30, 2022, compared to unrealized losses of

$276,000 for the three months ended March 31, 2022. Income from bank-owned life insurance increased $10,000, or 2.2%, from the

three months ended March 31, 2022 to $458,000, for the three months ended June 30, 2022. During the three months ended June 30,

2022, the Company reported $21,000 in other income from loan-level swap fees on commercial loans and a gain of $141,000 on non-marketable

equity investments. During the three months ended March 31, 2022, the Company reported a net loss of $4,000 on securities sales.

The Company did not sell any securities during the three months ended June 30, 2022.

Non-Interest

Expense

For

the three months ended June 30, 2022, non-interest expense decreased $23,000, or 0.2%, to $14.4 million from the three months

ended March 31, 2022. Salaries and employee benefits decreased $3,000 to $8.2 million, occupancy expense decreased $186,000, or

13.6%, FDIC insurance expense decreased $52,000, or 18.2%, and furniture and equipment expenses decreased $4,000, or 0.7%. These

decreases were partially offset by increases in professional fees of $142,000, or 24.6%, advertising expense of $13,000, or 3.3%,

data processing expense of $8,000, or 1.1%, and other non-interest expense of $59,000, or 2.5%. For the three months ended June

30, 2022, the adjusted efficiency ratio, a non-GAAP financial measure, was 65.0%, compared to 67.8% for the three months ended

March 31, 2022. The adjusted efficiency ratio is a non-GAAP measure. See pages 18-21 for the related ratio calculation and a reconciliation

of GAAP to non-GAAP financial measures.

Income

Tax Provision

Income

tax expense for the three months ended June 30, 2022 was $1.9 million, or an effective tax rate of 25.2%, compared to $1.7 million,

or an effective tax rate of 24.2%, for three months ended March 31, 2022. The increase in the effective tax rate reflects higher

projected pre-tax income for the year ending December 31, 2022.

Net

Income for the Three Months Ended June 30, 2022 Compared to the Three Months Ended June 30, 2021.

The

Company reported net income of $5.5 million, or $0.25 per diluted share, for the three months ended June 30, 2022, compared to

net income of $5.7 million, or $0.24 per diluted share, for the three months ended June 30, 2021. Return on average assets and

return on average equity was 0.87% and 10.22%, respectively, for the three months ended June 30, 2022, as compared to 0.92% and

10.16%, respectively, for the three months ended June 30, 2021.

Net

Interest Income and Net Interest Margin

Net

interest income increased $1.6 million, or 8.9%, to $19.4 million, for the three months ended June 30, 2022, from $17.8 million

for the three months ended June 30, 2021. The increase was due to an increase in interest and dividend income of $994,000, or

5.1%, and a decrease in interest expense of $594,000, or 32.2%. Interest expense on deposits decreased $476,000, or 32.5%, and

interest expense on borrowings decreased $118,000, or 30.9%. For the three months ended June 30, 2022, net interest income included

$129,000 in PPP income, compared to $1.6 million for the three months ended June 30, 2021. Excluding PPP income, net interest

income increased $3.1 million, or 19.1%, primarily due to an increase in interest and dividend income of $2.5 million, or 13.8%.

The

net interest margin was 3.24% for the three months ended June 30, 2022, compared to 3.06% for the three months ended June 30,

2021. The net interest margin, on a tax-equivalent basis, was 3.26% for the three months ended June 30, 2022, compared to 3.08%

for the three months ended June 30, 2021. The increase in the net interest margin was due to an increase in average loans outstanding

of $38.1 million, or 2.0%, from the three months ended June 30, 2021, compared to the three months ended June 30, 2022.

The

average yield on interest-earning assets increased seven basis points from 3.40% for the three months ended June 30, 2021 to 3.47%

for the three months ended June 30, 2022. During the three months ended June 30, 2022, the average cost of funds, including non-interest-bearing

demand accounts and borrowings, decreased 11 basis points, from 0.33% for the three months ended June 30, 2021 to 0.22% for the

three months ended June 30, 2022. The average cost of core deposits, which include non-interest-bearing demand accounts, decreased

four basis points, from 0.19% for the three months ended June 30, 2021 to 0.15% for the three months ended June 30, 2022. The

average cost of time deposits decreased 24 basis points from 0.56% for the three months ended June 30, 2021 to 0.32% for the three

months ended June 30, 2022. The average cost of borrowings increased 129 basis points during the same period due to the full quarter

impact of the $20.0 million in subordinated debt issued on April 19, 2021. For the three months ended June 30, 2022, average demand

deposits, an interest-free source of funds, increased $32.4 million, or 5.4%, to $635.7 million, or 28.0% of total average deposits,

from $603.3 million, or 27.9% of total average deposits for the three months ended June 30, 2021.

During

the three months ended June 30, 2022, average interest-earning assets increased $68.2 million, or 2.9%, to $2.4 billion compared

to the three months ended June 30, 2021, primarily due to an increase in average securities of $120.0 million, or 39.5%, and an

increase in average loans of $38.1 million, or 2.0%, partially offset by a decrease in short-term investments of $89.9 million,

or 78.3%. Excluding average PPP loans, average interest-earning assets increased $220.7 million, or 10.2%, and average loans increased

$190.7 million, or 10.9%, from the three months ended June 30, 2021 to the three months ended June 30, 2022.

Provision

for Loan Losses

The

Company recorded a provision for loan losses of $300,000 for three months ended June 30, 2022, compared to a credit for loan losses

of $1.2 million for the three months ended June 30, 2021. The increase in the provision for loan losses was due to strong organic

loan growth during the second quarter of 2022. The Company recorded net charge-offs of $48,000 for the three months ended June

30, 2022, as compared to net charge-offs of $157,000 for the three months ended June 30, 2021. Management continues to assess

the exposure of the Company’s loan portfolio to the COVID-19 pandemic related factors, economic trends and their potential

effect on asset quality.

Non-Interest

Income

Non-interest

income increased $332,000, or 13.8%, to $2.7 million for the three months ended June 30, 2022, from $2.4 million for the three

months ended June 30, 2021. During the three months ended June 30, 2022, service charges and fees on deposits increased $271,000,

or 13.1%, primarily due to the $177,000, or 19.1%, increase in ATM and debit card interchange income from increased card-based

transaction usage across our checking account base. Other income from loan-level swap fees on commercial loans increased $21,000

from the three months ended June 30, 2021 to the three months ended June 30, 2022. Income from bank-owned life insurance decreased

$42,000, or 8.4%, from the three months ended June 30, 2021 to the three months ended June 30, 2022. During the three months ended

June 30, 2021, mortgage banking income from the sale of fixed rate residential real estate loans totaled $242,000. The Company

did not sell any loans to the secondary market during the three months ended June 30, 2022. The Company reported a gain of $141,000

on non-marketable equity investments and reported an unrealized loss on marketable equity securities of $225,000, during the three

months ended June 30, 2022, compared to unrealized gains on marketable equity securities of $6,000 during the three months ended

June 30, 2021. The Company also reported realized losses on the sale of securities of $12,000 during the three months ended June

30, 2021. Gains and losses from the investment portfolio vary from quarter to quarter based on market conditions, as well as the

related yield curve and valuation changes.

During

the three months ended June 30, 2021, the Company recognized a loss on interest rate swap termination of $402,000 representing

the unamortized portion of a $3.4 million loss associated with the previous termination of a $32.5 million interest rate swap

on March 16, 2016. The unamortized portion of the loss was previously reported in accumulated other comprehensive income and amortized

through interest expense, however, as the previously hedged item was discontinued, the Company accelerated the remaining unamortized

loss.

Non-Interest

Expense

For

the three months ended June 30, 2022, non-interest expense increased $759,000, or 5.6%, to $14.4 million from $13.7 million, for

the three months ended June 30, 2021. The increase in non-interest expense was partially due to an increase in salaries and benefits

of $263,000, or 3.3%, due to normal annual salary increases. Other non-interest expense increased $260,000, or 12.2%, professional

fees increased $130,000, or 22.1%, occupancy expense increased $78,000, or 7.1%, advertising expense increased $65,000, or 18.7%,

furniture and equipment expense increased $26,000, or 5.1%, and FDIC insurance expense increased $9,000, or 4.0%. During the same

period, data processing expense decreased $27,000, or 3.6%. During the three months ended June 30, 2021, the Company prepaid $32.5

million of FHLB borrowings resulting in a loss of $45,000. For the three months ended June 30, 2022, the adjusted efficiency ratio,

a non-GAAP financial measure, was 65.0%, compared to 66.1% for the three months ended June 30, 2021. The adjusted efficiency ratio

is a non-GAAP measure. See pages 18-21 for the related efficiency ratio calculation and a reconciliation of GAAP to non-GAAP financial

measures.

Income

Tax Provision

Income

tax expense for the three months ended June 30, 2022 was $1.9 million, representing an effective tax rate of 25.2%, compared to

$2.1 million, representing an effective tax rate of 27.0%, for three months ended June 30, 2021.

Net

Income for the Six Months Ended June 30, 2022 Compared to the Six Months Ended June 30, 2021

For

the six months ended June 30, 2022, the Company reported net income of $10.9 million, or $0.49 per diluted share, compared to

$11.4 million, or $0.47 per diluted share, for the six months ended June 30, 2021. Return on average assets and return on average

equity were 0.86% and 9.93% for the six months ended June 30, 2022, respectively, compared to 0.95% and 10.25% for the six months

ended June 30, 2021, respectively.

Net

Interest Income and Net Interest Margin

During

the six months ended June 30, 2022, net interest income increased $2.3 million, or 6.3%, to $38.1 million, compared to $35.8 million

for the six months ended June 30, 2021. The increase in net interest income was due to a decrease in interest expense of $1.4

million, or 35.2%, and an increase in interest and dividend income of $904,000, or 2.3%. The decrease in interest expense was

due to a decrease in interest expense on deposits of $1.2 million, or 38.1%, and a decrease of $138,000, or 21.1%, in interest

expense on borrowings. For the six months ended June 30, 2022, interest and dividend income included $691,000 in PPP income, compared

to $4.0 million during the six months ended June 30, 2021. Excluding PPP income, net interest income increased $5.6 million, or

17.6% for the same period.

The

net interest margin for the six months ended June 30, 2022 was 3.21%, compared to 3.15% during the six months ended June 30, 2021.

The net interest margin, on a tax-equivalent basis, was 3.23% for the six months ended June 30, 2022, compared to 3.17% for the

six months ended June 30, 2021. Excluding the PPP income, the net interest margin increased from 3.01% for the six months ended

June 30, 2021 to 3.16% for the six months ended June 30, 2022.

The

average yield on interest-earning assets decreased seven basis points from 3.51% for the six months ended June 30, 2021 to 3.44%

for the six months ended June 30, 2022. During the six months ended June 30, 2022, the average cost of funds, including non-interest-bearing

demand accounts and borrowings, decreased 14 basis points from 0.36% for the six months ended June 30, 2021 to 0.22% for the six

months ended June 30, 2022. For the six months ended June 30, 2022, the average cost of core deposits, including non-interest-bearing

demand deposits, decreased six basis points from 0.20% for the six months ended June 30, 2021 to 0.14% for the six months ended

June 30, 2022. The average cost of time deposits decreased 28 basis points from 0.62% for the six months ended June 30, 2021 to

0.34% during the same period in 2022. The average cost of borrowings, which include FHLB advances and subordinated debt, increased

184 basis points from 2.47% for the six months ended June 30, 2021 to 4.31% for the six months ended June 20, 2022. For the six

months ended June 30, 2022, average demand deposits, an interest-free source of funds, increased $51.8 million, or 8.9%, from

$582.5 million, or 27.4% of total average deposits, for the six months ended June 30, 2021, to $634.4 million, or 28.0% of total

average deposits.

During

the six months ended June 30, 2022, average interest-earning assets increased $99.2 million, or 4.3%, to $2.4 billion. The increase

in average interest-earning assets was due to an increase in average loans of $5.0 million, or 0.3%, as well as an increase in

average securities of $158.3 million, or 58.5%. Both were partially offset by a decrease of $64.1 million, or 61.1%, in short-term

investments. Excluding average PPP loans, average interest-earning assets increased $251.2 million, or 11.8%, and average loans

increased $157.0 million, or 8.9%.

Provision

for Loan Losses

For

the six months ended June 30, 2022, the credit for loan losses decreased $1.0 million, or 88.9%, from $1.1 million for the six

months ended June 30, 2021 to $125,000 for the six months ended June 30, 2022. During the six months ended June 30, 2021, the

Company adjusted its qualitative factors related to the impact of the COVID-19 pandemic and other economic trends used in the

Company’s allowance calculation which resulted in a credit for loan losses of $1.1 million. The Company recorded net charge-offs

of $102,000 for the six months ended June 30, 2022, as compared to net charge-offs of $162,000 for the six months ended June 30,

2021.

Non-Interest

Income

For

the six months ended June 30, 2022, non-interest income was $5.1 million, compared to $5.4 million for the six months ended June

30, 2021. During the same period, service charges and fees increased $562,000, or 14.2%. Other income from loan-level swap fees

on commercial loans decreased $37,000, or 63.8%, and income from bank-owned life insurance decreased $35,000, or 3.7%. Mortgage

banking income was $469,000 for the six months ended June 30, 2021 due to the sale of fixed rate residential real estate loans

to the secondary market. The Company sold $17.6 million of low coupon residential real estate loans to the secondary market during

the six months ended June 30, 2021, compared to $277,000 during the six months ended June 30, 2022.

During

the six months ended June 30, 2022, the Company reported unrealized losses on marketable equity securities of $501,000, compared

to unrealized losses of $83,000 during the six months ended June 30, 2021. During the six months ended June 30, 2022, the Company

also reported realized losses on the sale of securities of $4,000, compared to realized losses of $74,000 on the sale of securities

during the six months ended June 30, 2021. The Company reported a gain of $141,000 on non-marketable equity investments during

the six months ended June 30, 2022, compared to $546,000 during the six months ended June 30, 2021. Gains and losses from the

investment portfolio vary from quarter to quarter based on market conditions, as well as the related yield curve and valuation

changes.

During

the six months ended June 30, 2021, the Company recognized a loss on interest rate swap termination of $402,000 representing the

unamortized portion of a $3.4 million loss associated with the previous termination of a $32.5 million interest rate swap on March

16, 2016. The unamortized portion of the loss was previously reported in accumulated other comprehensive income and amortized

through interest expense, however, as the previously hedged item was discontinued, the Company accelerated the remaining unamortized

loss.

Non-Interest

Expense

For

the six months ended June 30, 2022, non-interest expense increased $1.9 million, or 7.0%, to $28.9 million, compared to $27.0

million for the six months ended June 30, 2021. The increase in non-interest expense was primarily due to an increase in salaries

and employee benefits of $739,000, or 4.7%, due to normal annual salary increases as well as higher compensation incentive costs

to support overall franchise growth. The increase in salary related expenses was also partially due to a decrease of $279,000

in deferred direct origination costs associated with Round 3 of PPP loans. The origination costs were recorded against salary

expense during the six months ended June 30, 2021.

Other

non-interest expense increased $702,000, or 17.5%, professional fees increased $163,000, or 14.4%, occupancy expense increased

$152,000, or 6.4%, advertising expense increased $126,000, or 18.4%, furniture and equipment expense increased $79,000, or 7.9%,

data processing expenses decreased $25,000, or 1.7%, and FDIC insurance expense decreased $3,000, or 0.6%. During the six months

ended June 30, 2021, the Company prepaid $32.5 million of FHLB borrowings resulting in a loss of $45,000. For the six months ended

June 30, 2022, the adjusted efficiency ratio, a non-GAAP financial measure, was 66.4%, compared to 65.3% for the six months ended

June 30, 2021. The adjusted efficiency ratio is a non-GAAP measure. See pages 18-21 for the related efficiency ratio calculation

and a reconciliation of GAAP to non-GAAP financial measures.

Income

Tax Provision

Income

tax expense for the six months ended June 30, 2022 was $3.6 million, representing an effective tax rate of 24.7%, compared to

$3.9 million, representing an effective tax rate of 25.5%, for six months ended June 30, 2021.

Balance

Sheet

At

June 30, 2022, total assets were $2.6 billion, an increase of $38.9 million, or 1.5%, from December 31, 2021. During the six months

ended June 30, 2022, cash and cash equivalents decreased $55.9 million, or 54.1%, to $47.5 million, investment securities decreased

$22.3 million, or 5.2%, to $406.2 million and total loans increased $111.0 million, or 6.0%, to $2.0 billion.

Investments

At

June 30, 2022, the Company’s available-for-sale securities portfolio decreased $33.4 million, or 17.2%, from $194.4 million

at December 31, 2021 to $160.9 million at June 30, 2022. The held-to-maturity securities portfolio, recorded at amortized cost,

increased $11.5 million, or 5.2%, from $222.3 million at December 31, 2021 to $233.8 million at June 30, 2022. The marketable

equity securities portfolio decreased $443,000, or 3.7%, from $11.9 million at December 31, 2021 to $11.5 million at June 30,

2022. The primary objective of the investment portfolio is to provide liquidity and maximize income while preserving the safety

of principal.

Total

Loans

At

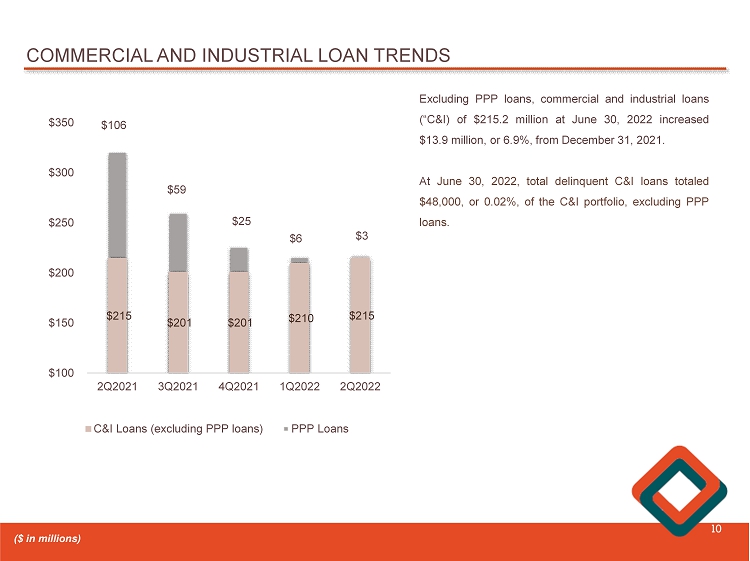

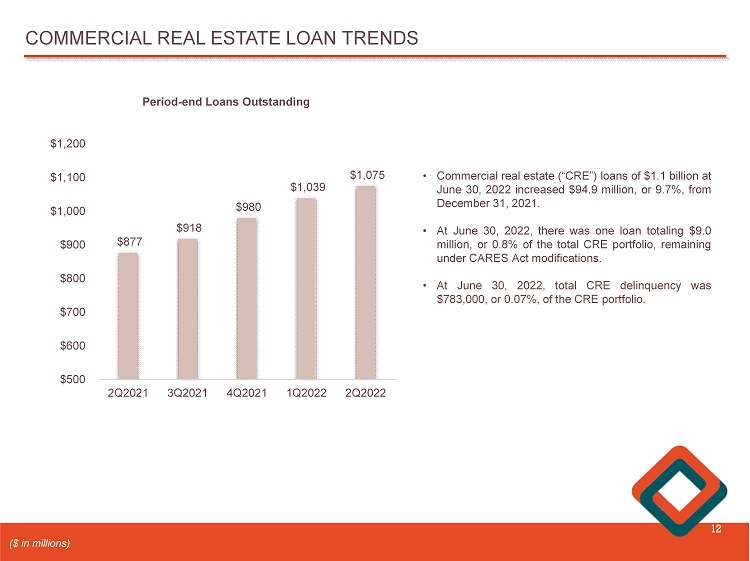

June 30, 2022, total loans were $2.0 billion, an increase of $111.0 million, or 6.0%, from December 31, 2021. Excluding PPP loans,

total loans increased $133.7 million, or 7.3%, driven by an increase in commercial real estate loans of $94.9 million, or 9.7%,

partially offset by a decrease in total commercial and industrial loans of $8.8 million, or 3.9%. Excluding a decrease in PPP

loans of $22.7 million, or 89.6%, from December 31, 2021, commercial and industrial loans increased $13.9 million, or 6.9%, at

June 30, 2022. Residential real estate loans, which include home equity loans, increased $24.2 million, or 3.7%. In accordance

with the Company’s asset/liability management strategy, at June 30, 2022, the Company serviced $82.5 million in loans sold

to the secondary market, compared to $88.2 million at December 31, 2021. Servicing rights will continue to be retained on all

loans written and sold to the secondary market.

The

following table is a summary of our outstanding loan balances for the periods indicated:

| | |

June 30, 2022 | | |

December 31, 2021 | |

| | |

(Dollars in thousands) | |

| | |

| |

| Commercial real estate loans | |

$ | 1,074,907 | | |

$ | 979,969 | |

| | |

| | | |

| | |

| Residential real estate loans: | |

| | | |

| | |

| Residential | |

| 572,700 | | |

| 552,332 | |

| Home equity | |

| 103,623 | | |

| 99,759 | |

| Total residential real estate loans | |

| 676,323 | | |

| 652,091 | |

| | |

| | | |

| | |

| Commercial and industrial loans: | |

| | | |

| | |

| PPP loans | |

| 2,631 | | |

| 25,329 | |

| Commercial and industrial loans | |

| 215,224 | | |

| 201,340 | |

| Total commercial and industrial loans | |

| 217,855 | | |

| 226,669 | |

| Consumer loans | |

| 4,457 | | |

| 4,250 | |

| Total gross loans | |

| 1,973,542 | | |

| 1,862,979 | |

| Unamortized PPP loan fees | |

| (133 | ) | |

| (781 | ) |

| Unamortized premiums and net deferred loans fees and costs | |

| 2,291 | | |

| 2,518 | |

| Total loans | |

$ | 1,975,700 | | |

$ | 1,864,716 | |

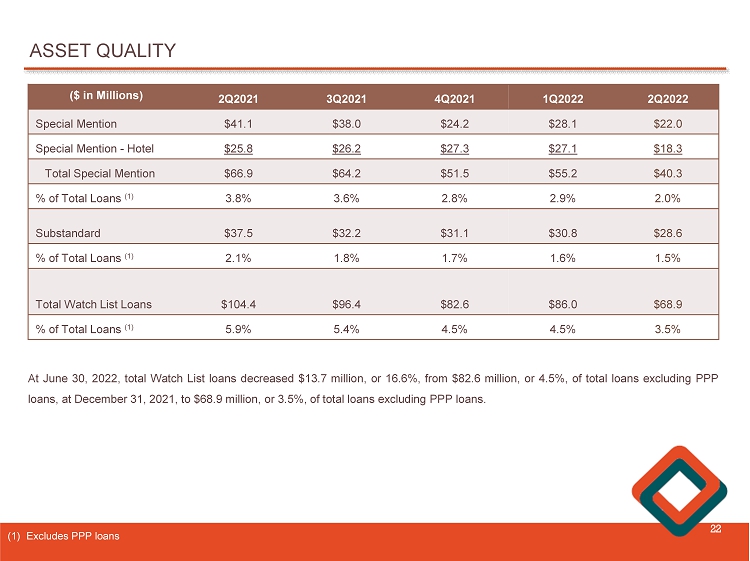

Credit

Quality

Management

continues to remain attentive to any signs of deterioration in borrowers’ financial conditions and is proactive in taking

the appropriate steps to mitigate risk. At June 30, 2022, nonperforming loans totaled $4.1 million, or 0.21% of total loans, compared

to $5.0 million, or 0.27% of total loans, at December 31, 2021. At June 30, 2022, there were no loans 90 or more days past due

and still accruing interest. Nonperforming assets to total assets, was 0.16% at June 30, 2022, compared to 0.20% at December 31,

2021. The allowance for loan losses as a percentage of total loans was 0.99% at June 30, 2022, compared to 1.06% at December 31,

2021. At June 30, 2022, the allowance for loan losses as a percentage of nonperforming loans was 476.5%, compared to 398.6%, at

December 31, 2021.

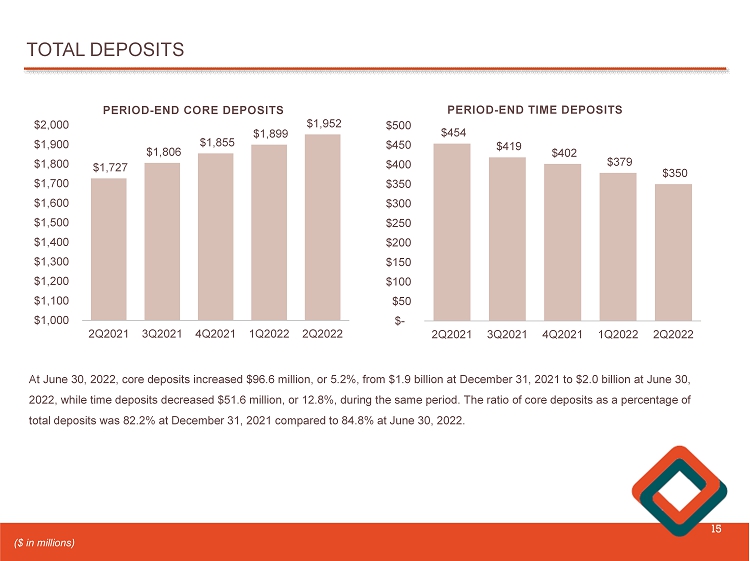

Deposits

At

June 30, 2022, total deposits were $2.3 billion, an increase of $45.1 million, or 2.0%, from December 31, 2021, primarily due

to an increase in core deposits of $96.7 million, or 5.2%. Core deposits, which the Company defines as all deposits except time

deposits, increased from $1.9 billion, or 82.2% of total deposits, at December 31, 2021, to $2.0 billion, or 84.8% of total deposits,

at June 30, 2022. Non-interest-bearing deposits increased $6.3 million, or 1.0%, to $647.6 million, interest-bearing checking

accounts increased $8.3 million, or 5.7%, to $154.0 million, savings accounts increased $9.1 million, or 4.2%, to $226.7 million,

and money market accounts increased $72.9 million, or 8.6%, to $923.2 million. Time deposits decreased $51.6 million, or 12.8%,

from $402.0 million at December 31, 2021 to $350.4 million at June 30, 2022. The Company did not have any brokered deposits at

June 30, 2022 or December 31, 2021.

Borrowings

and Subordinated Debt

At

June 30, 2022, total borrowings increased $3.5 million, or 15.7%, from $22.3 million at December 31, 2021, to $25.8 million. Other

borrowings increased $3.5 million, or 129.6%, to $6.2 million and subordinated debt outstanding totaled $19.7 million at June

30, 2022 and $19.6 million at December 31, 2021.

Capital

At

June 30, 2022, shareholders’ equity was $215.3 million, or 8.4% of total assets, compared to $223.7 million, or 8.8% of

total assets, at December 31, 2021. The decrease in shareholders’ equity reflects $3.7 million for the repurchase of the

Company’s common stock, the payment of regular cash dividends of $2.7 million and an increase in accumulated other comprehensive

loss of $14.4 million, partially offset by net income of $10.9 million. Total shares outstanding as of June 30, 2022 were 22,465,991.

Capital

Management

The

Company’s book value per share was $9.58 at June 30, 2022 compared to $9.87 at December 31, 2021, while tangible book value

per share, a non-GAAP financial measure, decreased $0.29, or 3.1%, from $9.21 at December 31, 2021 to $8.92 at June 30, 2022.

The change in AOCI reduced the tangible book value per common share by $0.64 as of June 30, 2022, primarily due

to the impact of higher interest rates on the fair value of available-for-sale securities. Tangible book value is a non-GAAP

measure. See pages 18-21 for the related tangible book value calculation and a reconciliation of GAAP to non-GAAP financial measures.

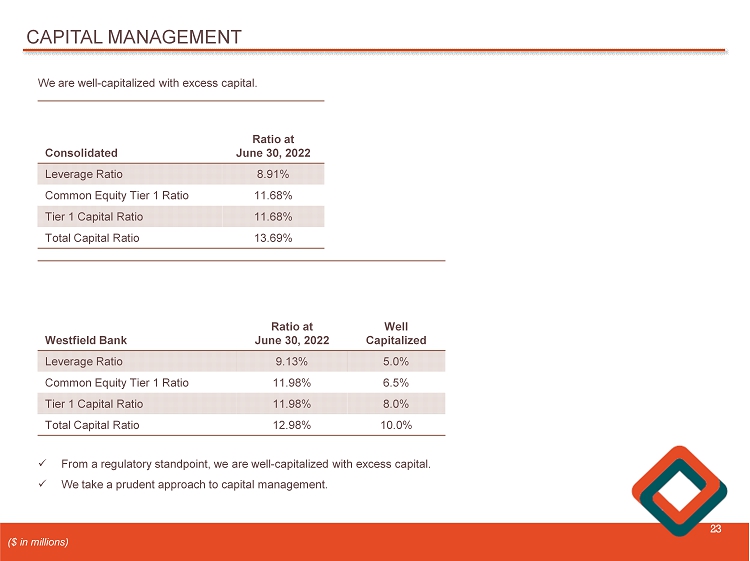

The

Company’s regulatory capital ratios remain in compliance with regulatory “well capitalized” requirements and

internal target minimal levels. At June 30, 2022, the Company’s Tier 1 leverage, common equity tier 1 capital, and total

risk-based capital ratios were 8.9%, 11.7%, and 13.7%, respectively, and the Bank’s Tier 1 leverage, common equity tier

1 capital, and total risk-based capital ratios were 9.1%, 12.0%, and 13.0%, respectively, compared with regulatory “well

capitalized” minimums of 5.00%, 6.5%, and 10.00%, respectively.

Dividends

Although

the Company has historically paid quarterly dividends on its common stock and currently intends to continue to pay such dividends,

the Company’s ability to pay such dividends depends on a number of factors, including restrictions under federal laws and

regulations on the Company’s ability to pay dividends, and as a result, there can be no assurance that dividends will continue

to be paid in the future.

About

Western New England Bancorp, Inc.

Western

New England Bancorp, Inc. is a Massachusetts-chartered stock holding company and the parent company of Westfield Bank, CSB Colts,

Inc., Elm Street Securities Corporation, WFD Securities, Inc. and WB Real Estate Holdings, LLC. Western New England Bancorp, Inc.

and its subsidiaries are headquartered in Westfield, Massachusetts and operate 25 banking offices throughout western Massachusetts

and northern Connecticut. To learn more, visit our website at www.westfieldbank.com.

Forward-Looking

Statements

This

press release contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933,

as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, with respect to the Company’s financial

condition, liquidity, results of operations, future performance, business, measures being taken in response to the COVID-19 pandemic

and the impact of the COVID-19 impact on the Company’s business. Forward-looking statements may be identified by the use

of such words as “believe,” “expect,” “anticipate,” “should,” “planned,”

“estimated,” and “potential.” Examples of forward-looking statements include, but are not limited

to, estimates with respect to our financial condition, results of operations and business that are subject to various factors

which could cause actual results to differ materially from these estimates. These factors include, but are not limited to:

| ● | the

duration and scope of the COVID-19 pandemic and the local, national and global impact of COVID-19; |

| ● | actions

governments, businesses and individuals take in response to the COVID-19 pandemic; |

| ● | the

speed and effectiveness of vaccine and treatment developments and their deployment, including public adoption rates of COVID-19

vaccines; |

| ● | the

emergence of new COVID-19 variants, such as the Omicron variant, and the response thereto; |

| ● | the

pace of recovery when the COVID-19 pandemic subsides; |

| ● | changes

in the interest rate environment that reduce margins; |

| ● | the

effect on our operations of governmental legislation and regulation, including changes in accounting regulation or standards,

the nature and timing of the adoption and effectiveness of new requirements under the Dodd-Frank Act Wall Street Reform and Consumer

Protection Act of 2010 (“Dodd-Frank Act”), Basel guidelines, capital requirements and other applicable laws and regulations; |

| ● | the

highly competitive industry and market area in which we operate; |

| ● | general

economic conditions, either nationally or regionally, resulting in, among other things, a deterioration in credit quality; |

| ● | changes

in business conditions and inflation; |

| ● | changes

in credit market conditions; |

| ● | the

inability to realize expected cost savings or achieve other anticipated benefits in connection with business combinations and

other acquisitions; |

| ● | changes

in the securities markets which affect investment management revenues; |

| ● | increases

in Federal Deposit Insurance Corporation deposit insurance premiums and assessments; |

| ● | changes

in technology used in the banking business; |

| ● | the

soundness of other financial services institutions which may adversely affect our credit risk; |

| ● | certain

of our intangible assets may become impaired in the future; |

| ● | our

controls and procedures may fail or be circumvented; |

| ● | new

lines of business or new products and services, which may subject us to additional risks; |

| ● | changes

in key management personnel which may adversely impact our operations; |

| ● | severe

weather, natural disasters, acts of war or terrorism and other external events which could significantly impact our business;

and |

| ● | other

factors detailed from time to time in our SEC filings. |

Although

we believe that the expectations reflected in such forward-looking statements are reasonable, actual results may differ materially

from the results discussed in these forward-looking statements. You are cautioned not to place undue reliance on these forward-looking

statements, which speak only as of the date hereof. We do not undertake any obligation to republish revised forward-looking statements

to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except to the extent

required by law.

WESTERN

NEW ENGLAND BANCORP, INC. AND SUBSIDIARIES

Consolidated

Statements of Net Income and Other Data

(Dollars

in thousands, except per share data)

(Unaudited)

| | |

Three Months Ended | | |

Six Months Ended | |

| | |

June 30, | | |

March 31, | | |

December 31, | | |

September 30, | | |

June 30, | | |

June 30, | |

| | |

2022 | | |

2022 | | |

2021 | | |

2021 | | |

2021 | | |

2022 | | |

2021 | |

| INTEREST AND DIVIDEND INCOME: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans | |

$ | 18,500 | | |

$ | 17,947 | | |

$ | 18,089 | | |

$ | 18,670 | | |

$ | 18,321 | | |

$ | 36,447 | | |

$ | 37,441 | |

| Securities | |

| 2,068 | | |

| 1,950 | | |

| 1,763 | | |

| 1,500 | | |

| 1,277 | | |

| 4,018 | | |

| 2,131 | |

| Other investments | |

| 30 | | |

| 25 | | |

| 25 | | |

| 28 | | |

| 28 | | |

| 55 | | |

| 63 | |

| Short-term investments | |

| 48 | | |

| 21 | | |

| 49 | | |

| 40 | | |

| 26 | | |

| 69 | | |

| 50 | |

| Total interest and dividend income | |

| 20,646 | | |

| 19,943 | | |

| 19,926 | | |

| 20,238 | | |

| 19,652 | | |

| 40,589 | | |

| 39,685 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| INTEREST EXPENSE: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Deposits | |

| 990 | | |

| 992 | | |

| 1,091 | | |

| 1,217 | | |

| 1,466 | | |

| 1,982 | | |

| 3.200 | |

| Short-term borrowings | |

| 10 | | |

| — | | |

| — | | |

| — | | |

| — | | |

| 10 | | |

| 458 | |

| Long-term debt | |

| — | | |

| — | | |

| — | | |

| — | | |

| 185 | | |

| — | | |

| 197 | |

| Subordinated debt | |

| 254 | | |

| 253 | | |

| 253 | | |

| 256 | | |

| 197 | | |

| 507 | | |

| — | |

| Total interest expense | |

| 1,254 | | |

| 1,245 | | |

| 1,344 | | |

| 1,473 | | |

| 1,848 | | |

| 2,499 | | |

| 3,855 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest and dividend income | |

| 19,392 | | |

| 18,698 | | |

| 18,582 | | |

| 18,765 | | |

| 17,804 | | |

| 38,090 | | |

| 35,830 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| PROVISION (CREDIT) FOR LOAN LOSSES | |

| 300 | | |

| (425 | ) | |

| 300 | | |

| (100 | ) | |

| (1,200 | ) | |

| (125 | ) | |

| (1,125 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest and dividend income after provision (credit) for loan losses | |

| 19,092 | | |

| 19,123 | | |

| 18,282 | | |

| 18,865 | | |

| 19,004 | | |

| 38,215 | | |

| 36,955 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| NON-INTEREST INCOME: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Service charges and fees | |

| 2,346 | | |

| 2,174 | | |

| 2,270 | | |

| 2,132 | | |

| 2,075 | | |

| 4,520 | | |

| 3,958 | |

| Income from bank-owned life insurance | |

| 458 | | |

| 448 | | |

| 486 | | |

| 485 | | |

| 500 | | |

| 906 | | |

| 941 | |

| Bank-owned life insurance death benefits | |

| — | | |

| — | | |

| 555 | | |

| — | | |

| — | | |

| — | | |

| — | |

| (Loss) gain on sales of securities, net | |

| — | | |

| (4 | ) | |

| — | | |

| 2 | | |

| (12 | ) | |

| (4 | ) | |

| (74 | ) |

| Unrealized (loss) gain on marketable equity securities | |

| (225 | ) | |

| (276 | ) | |

| (96 | ) | |

| 11 | | |

| 6 | | |

| (501 | ) | |

| (83 | ) |

| Gain on sale of mortgages | |

| — | | |

| 2 | | |

| 289 | | |

| 665 | | |

| 242 | | |

| 2 | | |

| 469 | |

| Gain on non-marketable equity investments | |

| 141 | | |

| — | | |

| 352 | | |

| — | | |

| — | | |

| 141 | | |

| 546 | |

| Loss on interest rate swap terminations | |

| — | | |

| — | | |

| — | | |

| — | | |

| (402 | ) | |

| — | | |

| (402 | ) |

| Other income | |

| 21 | | |

| 4 | | |

| — | | |

| — | | |

| — | | |

| 25 | | |

| 58 | |

| Total non-interest income | |

| 2,741 | | |

| 2,348 | | |

| 3,856 | | |

| 3,295 | | |

| 2,409 | | |

| 5,089 | | |

| 5,413 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| NON-INTEREST EXPENSE: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Salaries and employees benefits | |

| 8,236 | | |

| 8,239 | | |

| 8,193 | | |

| 8,175 | | |

| 7,973 | | |

| 16,475 | | |

| 15,736 | |

| Occupancy | |

| 1,177 | | |

| 1,363 | | |

| 1,144 | | |

| 1,124 | | |

| 1,099 | | |

| 2,540 | | |

| 2,388 | |

| Furniture and equipment | |

| 539 | | |

| 543 | | |

| 548 | | |

| 533 | | |

| 513 | | |

| 1,082 | | |

| 1,003 | |

| Data processing | |

| 731 | | |

| 723 | | |

| 726 | | |

| 698 | | |

| 758 | | |

| 1,454 | | |

| 1,479 | |

| Professional fees | |

| 719 | | |

| 577 | | |

| 477 | | |

| 575 | | |

| 589 | | |

| 1,296 | | |

| 1,133 | |

| FDIC insurance | |

| 234 | | |

| 286 | | |

| 202 | | |

| 273 | | |

| 225 | | |

| 520 | | |

| 523 | |

| Advertising | |

| 412 | | |

| 399 | | |

| 262 | | |

| 345 | | |

| 347 | | |

| 811 | | |

| 685 | |

| Loss on prepayment of borrowings | |

| — | | |

| — | | |

| — | | |

| — | | |

| 45 | | |

| — | | |

| 45 | |

| Other | |

| 2,385 | | |

| 2,326 | | |

| 2,371 | | |

| 2,295 | | |

| 2,125 | | |

| 4,711 | | |

| 4,009 | |

| Total non-interest expense | |

| 14,433 | | |

| 14,456 | | |

| 13,923 | | |

| 14,018 | | |

| 13,674 | | |

| 28,889 | | |

| 27,001 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| INCOME BEFORE INCOME TAXES | |

| 7,400 | | |

| 7,015 | | |

| 8,215 | | |

| 8,142 | | |

| 7,739 | | |

| 14,415 | | |

| 15,367 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| INCOME TAX PROVISION | |

| 1,865 | | |

| 1,696 | | |

| 1,995 | | |

| 2,106 | | |

| 2,087 | | |

| 3,561 | | |

| 3,924 | |

| NET INCOME | |

$ | 5,535 | | |

$ | 5,319 | | |

$ | 6,220 | | |

$ | 6,036 | | |

$ | 5,652 | | |

$ | 10,854 | | |

$ | 11,443 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Basic earnings per share | |

$ | 0.25 | | |

$ | 0.24 | | |

$ | 0.28 | | |

$ | 0.27 | | |

$ | 0.24 | | |

$ | 0.49 | | |

$ | 0.47 | |

| Weighted average shares outstanding | |

| 21,991,383 | | |

| 22,100,076 | | |

| 22,097,968 | | |

| 22,620,387 | | |

| 23,722,903 | | |

| 22,045,052 | | |

| 24,102,416 | |

| Diluted earnings per share | |

$ | 0.25 | | |

$ | 0.24 | | |

$ | 0.28 | | |

$ | 0.27 | | |

$ | 0.24 | | |

$ | 0.49 | | |

$ | 0.47 | |

| Weighted average diluted shares outstanding | |

| 22,025,687 | | |

| 22,172,909 | | |

| 22,203,876 | | |

| 22,714,429 | | |

| 23,773,562 | | |

| 22,098,620 | | |

| 24,156,450 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Other Data: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Return on average assets (1) | |

| 0.87 | % | |

| 0.85 | % | |

| 0.97 | % | |

| 0.96 | % | |

| 0.92 | % | |

| 0.86 | % | |

| 0.95 | % |

| Return on average equity (1) | |

| 10.22 | % | |

| 9.65 | % | |

| 11.22 | % | |

| 10.85 | % | |

| 10.16 | % | |

| 9.93 | % | |

| 10.25 | % |

| Efficiency ratio (2) | |

| 64.96 | % | |

| 67.79 | % | |

| 64.38 | % | |

| 63.58 | % | |

| 66.09 | % | |

| 66.35 | % | |

| 65.34 | % |

| Net interest margin, on a fully tax-equivalent basis | |

| 3.26 | % | |

| 3.20 | % | |

| 3.10 | % | |

| 3.20 | % | |

| 3.08 | % | |

| 3.23 | % | |

| 3.17 | % |

| (2) | The

efficiency ratio (non-GAAP) represents the ratio of operating expenses divided by the sum of net interest and dividend income

and non-interest income, excluding realized and unrealized gains and losses on securities, bank-owned life insurance death benefits,

gain on non-marketable equity investments, loss on interest rate swap termination and loss on prepayment of borrowings. |

WESTERN

NEW ENGLAND BANCORP, INC. AND SUBSIDIARIES

Consolidated

Balance Sheets

(Dollars

in thousands)

(Unaudited)

| | |

June 30, | | |

March 31, | | |

December 31, | | |

September 30, | | |

June 30, | |

| | |

2022 | | |

2022 | | |

2021 | | |

2021 | | |

2021 | |

| Cash and cash equivalents | |

$ | 47,513 | | |

$ | 62,898 | | |

$ | 103,456 | | |

$ | 148,496 | | |

$ | 105,494 | |

| Available-for-sale securities, at fair value | |

| 160,925 | | |

| 173,910 | | |

| 194,352 | | |

| 208,030 | | |

| 231,166 | |

| Held to maturity securities, at amortized cost | |

| 233,803 | | |

| 237,575 | | |

| 222,272 | | |

| 154,403 | | |

| 107,783 | |

| Marketable equity securities, at fair value | |

| 11,453 | | |

| 11,643 | | |

| 11,896 | | |

| 11,970 | | |

| 11,936 | |

| Federal Home Loan Bank of Boston and other restricted

stock - at cost | |

| 1,882 | | |

| 2,594 | | |

| 2,594 | | |

| 2,698 | | |

| 4,036 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans | |

| 1,975,700 | | |

| 1,926,285 | | |

| 1,864,716 | | |

| 1,846,150 | | |

| 1,876,988 | |

| Allowance for loan losses | |

| (19,560 | ) | |

| (19,308 | ) | |

| (19,787 | ) | |

| (19,837 | ) | |

| (19,870 | ) |

| Net loans | |

| 1,956,140 | | |

| 1,906,977 | | |

| 1,844,929 | | |

| 1,826,313 | | |

| 1,857,118 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Bank-owned life insurance | |

| 73,801 | | |

| 73,343 | | |

| 72,895 | | |

| 74,286 | | |

| 73,801 | |

| Goodwill | |

| 12,487 | | |

| 12,487 | | |

| 12,487 | | |

| 12,487 | | |

| 12,487 | |

| Core deposit intangible | |

| 2,375 | | |

| 2,469 | | |

| 2,563 | | |

| 2,656 | | |

| 2,750 | |

| Other assets | |

| 76,978 | | |

| 71,542 | | |

| 70,981 | | |

| 69,459 | | |

| 70,035 | |

| TOTAL ASSETS | |

$ | 2,577,357 | | |

$ | 2,555,438 | | |

$ | 2,538,425 | | |

$ | 2,510,798 | | |

$ | 2,476,606 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Total deposits | |

$ | 2,301,972 | | |

$ | 2,278,164 | | |

$ | 2,256,898 | | |

$ | 2,230,884 | | |

$ | 2,186,459 | |

| Short-term borrowings | |

| 4,790 | | |

| — | | |

| — | | |

| — | | |

| — | |

| Long-term debt | |

| 1,360 | | |

| 1,686 | | |

| 2,653 | | |

| 3,829 | | |

| 4,990 | |

| Subordinated debt | |

| 19,653 | | |

| 19,643 | | |

| 19,633 | | |

| 19,623 | | |

| 19,614 | |

| Securities pending settlement | |

| — | | |

| 146 | | |

| — | | |

| — | | |

| 461 | |

| Other liabilities | |

| 34,252 | | |

| 36,736 | | |

| 35,553 | | |

| 38,120 | | |

| 41,411 | |

| TOTAL LIABILITIES | |

| 2,362,027 | | |

| 2,336,375 | | |

| 2,314,737 | | |

| 2,292,456 | | |

| 2,252,935 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| TOTAL SHAREHOLDERS' EQUITY | |

| 215,330 | | |

| 219,063 | | |

| 223,688 | | |

| 218,342 | | |

| 223,671 | |

| TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY | |

$ | 2,577,357 | | |

$ | 2,555,438 | | |

$ | 2,538,425 | | |

$ | 2,510,798 | | |

$ | 2,476,606 | |

WESTERN

NEW ENGLAND BANCORP, INC. AND SUBSIDIARIES

Other

Data

(Dollars

in thousands, except per share data)

(Unaudited)

| | |

Three Months Ended | |

| | |

June 30, | | |

March 31, | | |

December 31, | | |

September 30, | | |

June 30, | |

| | |

2022 | | |

2022 | | |

2021 | | |

2021 | | |

2021 | |

| Shares outstanding at end of period | |

| 22,465,991 | | |

| 22,742,189 | | |

| 22,656,515 | | |

| 22,848,781 | | |

| 24,070,399 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Operating results: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest income | |

$ | 19,392 | | |

$ | 18,698 | | |

$ | 18,582 | | |

$ | 18,765 | | |

$ | 17,804 | |

| Provision (credit) for loan losses | |

| 300 | | |

| (425 | ) | |

| 300 | | |

| (100 | ) | |

| (1,200 | ) |

| Non-interest income | |

| 2,741 | | |

| 2,348 | | |

| 3,856 | | |

| 3,295 | | |

| 2,409 | |

| Non-interest expense | |

| 14,433 | | |

| 14,456 | | |

| 13,923 | | |

| 14,018 | | |

| 13,674 | |

| Income before income provision for income taxes | |

| 7,400 | | |

| 7,015 | | |

| 8,215 | | |

| 8,142 | | |

| 7,739 | |

| Income tax provision | |

| 1,865 | | |

| 1,696 | | |

| 1,995 | | |

| 2,106 | | |

| 2,087 | |

| Net income | |

| 5,535 | | |

| 5,319 | | |

| 6,220 | | |

| 6,036 | | |

| 5,652 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Performance Ratios: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net interest margin, on a fully tax-equivalent basis | |

| 3.26 | % | |

| 3.20 | % | |

| 3.10 | % | |

| 3.20 | % | |

| 3.08 | % |

| Interest rate spread, on a fully tax-equivalent basis | |

| 3.17 | % | |

| 3.10 | % | |

| 2.99 | % | |

| 3.09 | % | |

| 2.94 | % |

| Return on average assets | |

| 0.87 | % | |

| 0.85 | % | |

| 0.97 | % | |

| 0.96 | % | |

| 0.92 | % |

| Return on average equity | |

| 10.22 | % | |

| 9.65 | % | |

| 11.22 | % | |

| 10.85 | % | |

| 10.16 | % |

| Efficiency ratio (non-GAAP) | |

| 64.96 | % | |

| 67.79 | % | |

| 64.38 | % | |

| 63.58 | % | |

| 66.09 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Per Common Share Data: | |

| | | |

| | | |

| | | |

| | | |

| | |

| Basic earnings per share | |

$ | 0.25 | | |

$ | 0.24 | | |

$ | 0.28 | | |

$ | 0.27 | | |

$ | 0.24 | |

| Per diluted share | |

| 0.25 | | |

| 0.24 | | |

| 0.28 | | |

| 0.27 | | |

| 0.24 | |

| Cash dividend declared | |

| 0.06 | | |

| 0.06 | | |

| 0.05 | | |

| 0.05 | | |

| 0.05 | |

| Book value per share | |

| 9.58 | | |

| 9.63 | | |

| 9.87 | | |

| 9.56 | | |

| 9.29 | |

| Tangible book value per share (non-GAAP) | |

| 8.92 | | |

| 8.97 | | |

| 9.21 | | |

| 8.89 | | |

| 8.66 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Asset Quality: | |

| | | |

| | | |

| | | |

| | | |

| | |

| 30-89 day delinquent loans | |

$ | 1,063 | | |

$ | 1,407 | | |

$ | 1,102 | | |

$ | 1,619 | | |

$ | 2,607 | |

| 90 days or more delinquent loans | |

| 1,149 | | |

| 1,401 | | |

| 1,039 | | |

| 1,446 | | |

| 1,808 | |

| Total delinquent loans | |

| 2,212 | | |

| 2,808 | | |

| 2,141 | | |

| 3,065 | | |

| 4,415 | |

| Total delinquent loans as a percentage of total loans | |

| 0.11 | % | |

| 0.15 | % | |

| 0.11 | % | |

| 0.17 | % | |

| 0.24 | % |

| Total delinquent loans as a percentage of total loans, excluding PPP | |

| 0.11 | % | |

| 0.15 | % | |

| 0.12 | % | |

| 0.17 | % | |

| 0.25 | % |

| Nonperforming loans | |

$ | 4,105 | | |

$ | 3,988 | | |

$ | 4,964 | | |

$ | 5,632 | | |

$ | 5,989 | |

| Nonperforming loans as a percentage of total loans | |

| 0.21 | % | |

| 0.21 | % | |

| 0.27 | % | |

| 0.31 | % | |

| 0.32 | % |

| Nonperforming loans as a percentage of total loans, excluding PPP | |

| 0.21 | % | |

| 0.21 | % | |

| 0.27 | % | |

| 0.32 | % | |

| 0.34 | % |

| Nonperforming assets as a percentage of total assets | |

| 0.16 | % | |

| 0.16 | % | |

| 0.20 | % | |

| 0.22 | % | |

| 0.24 | % |

| Nonperforming assets as a percentage of total assets, excluding PPP | |

| 0.16 | % | |

| 0.16 | % | |

| 0.20 | % | |

| 0.23 | % | |

| 0.25 | % |

| Allowance for loan losses as a percentage of nonperforming loans | |

| 476.49 | % | |

| 484.15 | % | |

| 398.61 | % | |

| 352.22 | % | |

| 331.77 | % |

| Allowance for loan losses as a percentage of total loans | |

| 0.99 | % | |

| 1.00 | % | |

| 1.06 | % | |

| 1.07 | % | |

| 1.06 | % |

| Allowance for loan losses as a percentage of total loans, excluding PPP | |

| 0.99 | % | |

| 1.01 | % | |

| 1.08 | % | |

| 1.11 | % | |

| 1.12 | % |

| Net loan charge-offs (recoveries) | |

$ | 48 | | |

$ | 54 | | |

$ | 350 | | |

$ | (67 | ) | |

$ | 157 | |

| Net loan charge-offs as a percentage of average assets | |

| 0.00 | % | |

| 0.00 | % | |

| 0.01 | % | |

| 0.00 | % | |

| 0.01 | % |

The

following tables set forth the information relating to our average balances and net interest income for the three months ended

June 30, 2022, December 31, 2021, and June 30, 2021 and reflect the average yield on interest-earning assets and average cost

of interest-bearing liabilities for the periods indicated.

| | |

Three

Months Ended | |

| | |

June

30, 2022 | | |

December

31, 2021 | | |

June

30, 2021 | |

| | |

Average | | |

| | |

Average Yield/ | | |

Average | | |

| | |

Average Yield/ | | |

Average | | |

| | |

Average Yield/ | |

| | |

Balance | | |

Interest(8) | | |

Cost(9) | | |

Balance | | |

Interest(8) | | |

Cost(9) | | |

Balance | | |

Interest(8) | | |

Cost(9) | |

| | |

(Dollars in thousands) | |

| ASSETS: | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Interest-earning assets | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Loans(1)(2) | |

$ | 1,949,464 | | |

$ | 18,624 | | |

| 3.83 | % | |

$ | 1,850,162 | | |

$ | 18,197 | | |

| 3.90 | % | |

$ | 1,911,323 | | |

$ | 18,425 | | |

| 3.87 | % |

| Securities(2) | |

| 414,226 | | |

| 2,068 | | |

| 2.00 | | |

| 401,811 | | |

| 1,764 | | |

| 1.74 | | |

| 293,991 | | |

| 1,278 | | |

| 1.74 | |

| Other investments | |

| 9,892 | | |

| 30 | | |

| 1.22 | | |

| 10,654 | | |

| 25 | | |

| 0.93 | | |

| 10,114 | | |

| 28 | | |

| 1.11 | |

| Short-term investments(3) | |

| 24,944 | | |

| 48 | | |

| 0.77 | | |

| 131,770 | | |

| 49 | | |

| 0.15 | | |

| 114,883 | | |

| 26 | | |

| 0.09 | |

| Total

interest-earning assets | |

| 2,398,526 | | |

| 20,770 | | |

| 3.47 | | |

| 2,394,397 | | |

| 20,035 | | |

| 3.32 | | |

| 2,330,311 | | |

| 19,757 | | |

| 3.40 | |

| Total

non-interest-earning assets | |

| 153,939 | | |

| | | |

| | | |

| 149,151 | | |

| | | |

| | | |

| 147,545 | | |

| | | |

| | |

| Total

assets | |

$ | 2,552,465 | | |

| | | |

| | | |

$ | 2,543,548 | | |

| | | |

| | | |

$ | 2,477,856 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| LIABILITIES AND EQUITY: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing liabilities | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing checking accounts | |

$ | 137,984 | | |

| 105 | | |

| 0.31 | % | |

$ | 132,028 | | |

| 106 | | |

| 0.32 | % | |

$ | 100,455 | | |

| 92 | | |

| 0.37 | % |

| Savings accounts | |

| 224,487 | | |

| 48 | | |

| 0.09 | | |

| 214,961 | | |

| 36 | | |

| 0.07 | | |

| 206,302 | | |

| 47 | | |

| 0.09 | |

| Money market accounts | |

| 910,801 | | |

| 549 | | |

| 0.24 | | |

| 849,023 | | |

| 546 | | |

| 0.26 | | |

| 766,378 | | |

| 650 | | |

| 0.34 | |

| Time deposit accounts | |

| 365,383 | | |

| 288 | | |

| 0.32 | | |

| 410,149 | | |

| 403 | | |

| 0.39 | | |

| 487,712 | | |

| 677 | | |

| 0.56 | |

| Total interest-bearing deposits | |

| 1,638,655 | | |

| 990 | | |

| 0.24 | | |

| 1,606,161 | | |

| 1,091 | | |

| 0.27 | | |

| 1,560,847 | | |

| 1,466 | | |

| 0.38 | |

| Short-term borrowings

and long-term debt | |

| 25,829 | | |

| 264 | | |

| 4.10 | | |

| 22,614 | | |

| 253 | | |

| 4.44 | | |

| 54,459 | | |

| 382 | | |

| 2.81 | |

| Total

interest-bearing liabilities | |

| 1,664,484 | | |

| 1,254 | | |

| 0.30 | | |

| 1,628,775 | | |

| 1,344 | | |

| 0.33 | | |

| 1,615,306 | | |

| 1,848 | | |

| 0.46 | |

| Non-interest-bearing deposits | |

| 635,678 | | |

| | | |

| | | |

| 654,334 | | |

| | | |

| | | |

| 603,270 | | |

| | | |

| | |

| Other non-interest-bearing

liabilities | |

| 35,076 | | |

| | | |

| | | |

| 40,428 | | |

| | | |

| | | |

| 36,043 | | |

| | | |

| | |

| Total

non-interest-bearing liabilities | |

| 670,754 | | |

| | | |

| | | |

| 694,762 | | |

| | | |

| | | |

| 639,313 | | |

| | | |

| | |

| Total liabilities | |

| 2,335,238 | | |

| | | |

| | | |

| 2,323,537 | | |

| | | |

| | | |

| 2,254,619 | | |

| | | |

| | |

| Total

equity | |

| 217,227 | | |

| | | |

| | | |

| 220,011 | | |

| | | |

| | | |

| 223,237 | | |

| | | |

| | |

| Total

liabilities and equity | |

$ | 2,552,465 | | |

| | | |

| | | |

$ | 2,543,548 | | |

| | | |

| | | |

$ | 2,477,856 | | |

| | | |

| | |

| Less: Tax-equivalent adjustment

(2) | |

| | | |

| (124 | ) | |

| | | |

| | | |

| (109 | ) | |

| | | |

| | | |

| (105 | ) | |

| | |

| Net interest and dividend

income | |

| | | |

$ | 19,392 | | |

| | | |

| | | |

$ | 18,582 | | |

| | | |

| | | |

$ | 17,804 | | |

| | |

| Net interest rate spread (4) | |

| | | |

| | | |

| 3.15 | % | |

| | | |

| | | |

| 2.97 | % | |

| | | |

| | | |

| 2.92 | % |

| Net interest rate spread, on a tax-equivalent

basis (5) | |

| | | |

| | | |

| 3.17 | % | |

| | | |

| | | |

| 2.99 | % | |

| | | |

| | | |

| 2.94 | % |

| Net interest margin (6) | |

| | | |

| | | |

| 3.24 | % | |

| | | |

| | | |

| 3.08 | % | |

| | | |

| | | |

| 3.06 | % |

| Net interest margin, on a tax-equivalent basis

(7) | |

| | | |

| | | |

| 3.26 | % | |

| | | |

| | | |

| 3.10 | % | |

| | | |

| | | |

| 3.08 | % |

| Ratio of average

interest-earning assets to average interest-bearing liabilities | |

| | | |

| | | |

| 144.10 | % | |

| | | |

| | | |

| 147.01 | % | |

| | | |

| | | |

| 144.26 | % |

The

following tables set forth the information relating to our average balances and net interest income for the six months ended June

30, 2022 and 2021 and reflect the average yield on interest-earning assets and average cost of interest-bearing liabilities for

the periods indicated.

| | |

Six

Months Ended June 30, | |

| | |

2022 | | |

2021 | |

| | |

Average

Balance | | |

Interest

(8) | | |

Average

Yield/

Cost(9) | | |

Average

Balance | | |

Interest

(8) | | |

Average

Yield/

Cost(9) | |

| | |

(Dollars in thousands) | |

| ASSETS: | |

| | |

| | |

| | |

| | |

| | |

| |

| Interest-earning assets | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loans(1)(2) | |

$ | 1,922,318 | | |

$ | 36,690 | | |

| 3.85 | % | |

$ | 1,917,366 | | |

$ | 37,648 | | |

| 3.96 | % |

| Securities(2) | |

| 418,806 | | |

| 4,019 | | |

| 1.94 | | |

| 260,845 | | |

| 2,131 | | |

| 1.65 | |

| Other investments | |

| 10,241 | | |

| 55 | | |

| 1.08 | | |

| 9,889 | | |

| 63 | | |

| 1.28 | |

| Short-term investments(3) | |

| 40,899 | | |

| 69 | | |

| 0.34 | | |

| 104,999 | | |

| 50 | | |

| 0.10 | |

| Total

interest-earning assets | |

| 2,392,264 | | |

| 40,833 | | |

| 3.44 | | |

| 2,293,099 | | |

| 39,892 | | |

| 3.51 | |

| Total

non-interest-earning assets | |

| 148,815 | | |

| | | |

| | | |

| 146,709 | | |

| | | |

| | |

| Total

assets | |

$ | 2,541,079 | | |

| | | |

| | | |

$ | 2,439,808 | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| LIABILITIES AND EQUITY: | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing liabilities | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Interest-bearing checking accounts | |

$ | 135,104 | | |

| 200 | | |

| 0.30 | % | |

$ | 95,507 | | |

| 198 | | |

| 0.42 | % |

| Savings accounts | |