Exhibit 99.3 Lender Presentation May 2025 Lender Presentation

Disclaimer This presentation (this “Presentation”) is being furnished to a limited number of parties who have expressed an interest in a GAAP financial measures of other companies may not be calculated in the same manner. These non-GAAP financial potential transaction (the Potential Transaction ) with the Company. The Company does not intend for this Presentation to measures should be considered only as supplemental to, and not as a substitute for or superior to, financial measures form the sole basis of any transaction decision. The recipients should conduct their own investigations and analyses of the prepared in accordance with GAAP. Reconciliations between the non-GAAP financial measures and the closest GAAP Company in connection with any transaction. financial measures can be found in the Appendix section of this Presentation. This Presentation is being made available only to parties who have signed and returned a non-disclosure agreement with The Company cannot provide a reconciliation between its non-GAAP projections and the most directly comparable GAAP the Company in connection with the Potential Transaction (the Non-Disclosure Agreement ). By accepting this Presentation measures without unreasonable efforts because it is unable to predict with reasonable certainty the ultimate outcome of or any portion hereof, recipients agree to use and maintain the information in this Presentation in accordance with their certain significant items required for the reconciliation. These items are uncertain, depend on various factors and could Non-Disclosure Agreements and the recipients' compliance policies, contractual obligations and applicable laws and have a material impact on GAAP reported results. regulations, including federal and state securities laws. Financial Projections: This Presentation includes certain statements, claims, estimates, predictions and other information None of the Company, PJT Partners (“PJT”), their respective affiliates or their respective employees, directors, officers, prepared and provided by the Company with respect to the anticipated future performance of the Company and its contractors, advisors, consultants, members, successors, representatives, agents or controlling persons or any subsidiaries. Any assumptions, views or opinions (including statements, projections, forecasts or other forward-looking representatives of the foregoing, has made or makes any representation or warranty (express or implied) in respect of the statements) contained in this Presentation represent the assumptions, views or opinions of the Company as of the date accuracy, completeness or fair presentation of any information or any conclusion contained in this Presentation or in any indicated and are subject to change without notice. These statements are subject to known and unknown risks, other information provided or made available to the recipient in the course of its evaluation of the Company, and none shall uncertainties, changes in circumstances, assumptions and other important factors, many of which are outside our control, have any liability resulting from the use or content of this Presentation or any other such information provided or made that could cause actual results to differ materially and potentially adversely from the results discussed in the forward- available to the recipient including, for any representations or warranties (expressed or implied) contained in, or for any looking statements. omissions from, this Presentation or any other written or oral communications. The only information that will have any legal effect and upon which an interested party may rely will be in such representations and warranties as may be contained in a Forecasts and estimates regarding the Company’s industry and markets are based on sources the Company believes to be definitive agreement providing for a Potential Transaction, when, as and if executed, and in accordance with such terms and reliable; however, there can be no assurance these forecasts and estimates will prove accurate in whole or in part. All subject to such conditions as may be specified therein. The information in this Presentation was provided by the Company information not separately sourced is from internal data of the Company and estimates. or is from public or other sources. PJT has not assumed any responsibility for independently verifying such information and expressly disclaims any liability to any recipient in connection with such information or any transaction with the Company. There is no guarantee that any of the forecasts, estimates or projections (including projections of revenue, expenses and earnings) set forth herein will be achieved. Actual results may vary from the projections and such variations may be This Presentation is not an offer, nor a solicitation of an offer, of the sale or purchase of securities, nor shall any securities of material. Nothing contained herein is, or shall be relied upon as, a promise or representation as to the past or the future the Company or any of its subsidiaries be offered or sold, in any jurisdiction in which such an offer, solicitation or sale would performance of the Company or any of its subsidiaries or any of its or their businesses. be unlawful. In furnishing this Presentation, the Company and PJT reserve the right to amend or replace this Presentation at any time, but undertake no obligation to update, correct or supplement any information contained herein or to provide the 2025 and 2026 financial projections in this presentation are based on a 52 week calendar year. WW Fiscal Year 2025 recipient with access to any additional information. includes a 53rd week. This Presentation does not purport to be all-inclusive or to contain all of the information that the recipient may require in Forward-Looking Statements: This Presentation includes “forward-looking statements,” within the meaning of Section 27A order to make an informed investment decision. No investment or other financial decisions or actions should be based solely of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including, in on the information in this Presentation. particular, any statements about the Company’s plans, strategies, objectives, initiatives and prospects. The Company generally uses the words “may,” “will,” “could,” “expect,” “anticipate,” “believe,” “estimate,” “plan,” “intend,” “aim” and similar Non-GAAP Measures: In addition to the financial measures prepared in accordance with U.S. generally accepted expressions to identify forward-looking statements. The Company bases these forward-looking statements on its current accounting principles (“GAAP”), this Presentation contains certain non-GAAP financial measures (and projections of such views with respect to future events and financial performance. In addition, any statements that refer to expectations or measures), including EBITDAS, Adjusted EBITDAS, Adjusted EBITDAS Margin, Adjusted EBIT, Adjusted EBITDA, Adjusted Gross other characterizations of future events or circumstances, such as statements about the Company’s positioning in a Profit, Adjusted Gross Margin, Unlevered Free Cash Flow, Free Cash Flow, Net Leverage and Adjusted General and competitive environment, expected costs savings and other capital and operating expense reduction initiatives, building Administrative Expenses. The Company believes these non-GAAP financial measures are commonly used by analysts and new partnerships, utilizing new technologies, improving operational efficiency, trends in the weight management industry; investors to evaluate the performance of companies in its industry, and such non-GAAP financial measures help investors strategies and initiatives, expected interest rates and interest expense savings, and the Company’s anticipated operational evaluate its operating and financial performance and trends in its business, consistent with how management evaluates and financial performance, liquidity and net leverage are forward-looking statements. Statements that describe or relate such performance and trends. to the Company’s plans, goals, intentions, strategies, initiatives, prospects or financial projections or outlook, and statements that do not relate to historical or current fact, are examples of forward-looking statements. These statements The Company also believes that these non-GAAP financial measures may be useful in comparing its performance to the are not guarantees of future performance and are subject to certain risks, uncertainties and other important factors, some performance of other companies, although the Company’s non-GAAP financial measures are specific to it and the non- of which are beyond the Company’s control and are difficult to predict. Lender Presentation 2

Disclaimer (Cont'd) Various risks that could cause future results to differ from those expressed by the forward-looking statements included in this In light of these risks, uncertainties, assumptions and factors, the forward-looking events discussed in this Presentation and Presentation include, but are not limited to: competition from other weight management and health and wellness industry other materials provided by the Company may not occur. In particular, the projections are subject to inherent uncertainties participants or the development of more effective or more favorably perceived weight management methods; the and necessarily represent certain assumptions, and actual performance may differ. In addition, there is a risk the Company Company's failure to continue to retain and grow its subscriber base; the Company’s ability to be a leader in the rapidly is unable to deliver any anticipated cost savings (or recognize the expected benefits therefrom) either from an inability to evolving and increasingly competitive clinical weight management and weight loss market; the Company's ability to identify appropriate opportunities, anticipate implementation cost, delays in implementation or other factors. Do not place continue to develop new, innovative services and products and enhance its existing services and products or the failure of undue reliance on these forward-looking statements, which speak only as of the date stated, or if no date is stated, as of its services, products or brands to continue to appeal to the market, or its ability to successfully expand into new channels of the date hereof. Forward-looking statements are not guarantees of future performance. Additional risks that could cause distribution or respond to consumer trends or sentiment; regulatory, reputational and other risks associated with the future results to differ from those expressed by any forward-looking statement are described in the Company’s periodic Company’s new compounded GLP-1 offering; the ability to successfully implement strategic initiatives; the Company’s ability reports filed with the United States Securities and Exchange Commission (the “SEC”)”, including the disclosure contained in to evolve its community offerings to meet the evolving tastes and preferences of its members; the effectiveness and Item 1A. Risk Factors in the Company’s 2024 Annual Report on Form 10-K. Except as required by law, the Company does not efficiency of the Company's advertising and marketing programs, including the strength of the Company's social media undertake any obligation to update or revise these forward-looking statements to reflect new information or events or presence; the impact on the Company's reputation of actions taken by its franchisees, licensees, suppliers, affiliated provider circumstances that occur after the date of this Presentation or to reflect the occurrence of unanticipated events or entities, PCs’ healthcare professionals, and other partners, including as a result of its acquisition of Weekend Health, Inc., otherwise. You are advised to review the Company’s filings with the SEC (which are available on the SEC’s EDGAR database doing business as Sequence (“Sequence”) (the “Acquisition”); the recognition of asset impairment charges; the loss of key at www.sec.gov and via the Company’s website at http://corporate.ww.com). personnel, strategic partners or consultants or failure to effectively manage and motivate the Company's workforce; the Company’s chief executive officer transition; the Company’s ability to successfully make acquisitions or enter into Market Data: Certain market data information in this Presentation is based on management’s estimates. The Company collaborations or joint ventures, including its ability to successfully integrate, operate or realize the anticipated benefits of obtained the competitive position data used throughout this Presentation from internal estimates and research as well as such businesses, including with respect to Sequence; uncertainties related to a downturn in general economic conditions or from industry publications and research, surveys and studies conducted by third parties. The Company believes its consumer confidence, including as a result of the existing inflationary environment, rising interest rates, the potential impact estimates to be reasonably accurate as of the date of this Presentation or as of the date indicated with respect to such of political and social unrest and increased volatility in the credit and capital markets; the seasonal nature of the estimates, as applicable. However, this information may prove to be inaccurate because of the method by which the Company's business; the Company's failure to maintain effective internal control over financial reporting; the impact of Company obtained some of the data or estimates or because this information cannot always be verified due to the limits events that impede accessing resources or discourage or impede people from gathering with others; the early termination of the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and by the Company of leases; the inability to renew certain of the Company's licenses, or the inability to do so on terms that are uncertainties. Unless otherwise indicated, the information contained herein speaks only as of the date hereof and is subject favorable to the Company; the impact of the Company's substantial amount of debt, debt service obligations and debt to change, completion or amendment without notice. covenants, and its exposure to variable rate indebtedness; the ability to generate sufficient cash to service the Company's debt and satisfy its other liquidity requirements; uncertainties regarding the satisfactory operation of the Company's This Presentation contains trademarks, service marks, copyrights and trade names of other companies, which are the technology or systems; the impact of data security breaches and other malicious acts or privacy concerns, including the property of their respective owners. We do not intend to use or display other companies’ trademarks, service marks, costs of compliance with evolving privacy laws and regulations; the Company’s ability to successfully integrate and use copyrights and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies. artificial intelligence in its business; the Company's ability to enforce its intellectual property rights both domestically and internationally, as well as the impact of its involvement in any claims related to intellectual property rights; the impact of existing and future laws and regulations, including federal and state regulations relating to compounded medications; risks related to the Company's exposure to extensive and complex healthcare laws and regulations as a result of the Acquisition; the outcomes of litigation or regulatory actions; risks and uncertainties associated with the Company's international operations, including regulatory, economic, political, social, intellectual property, and foreign currency risks, which risks may be exacerbated as a result of war and terrorism; risks related to the Acquisition, including risks that the Acquisition may not achieve its intended results; the possibility that the Company could fail to maintain the listing of its common stock on Nasdaq; and risks related to the actions of activist shareholders. Other unknown or unpredictable factors also could have material adverse effects on the Company’s future results, performances or achievements. Lender Presentation 3

Table of Contents Executive Summary 1 Company Overview 2 3 State of the Union 4 Path to Stabilization 5 5-Year Forecast 6 Growth Levers Lender Presentation 4

Executive Summary 1 Lender Presentation

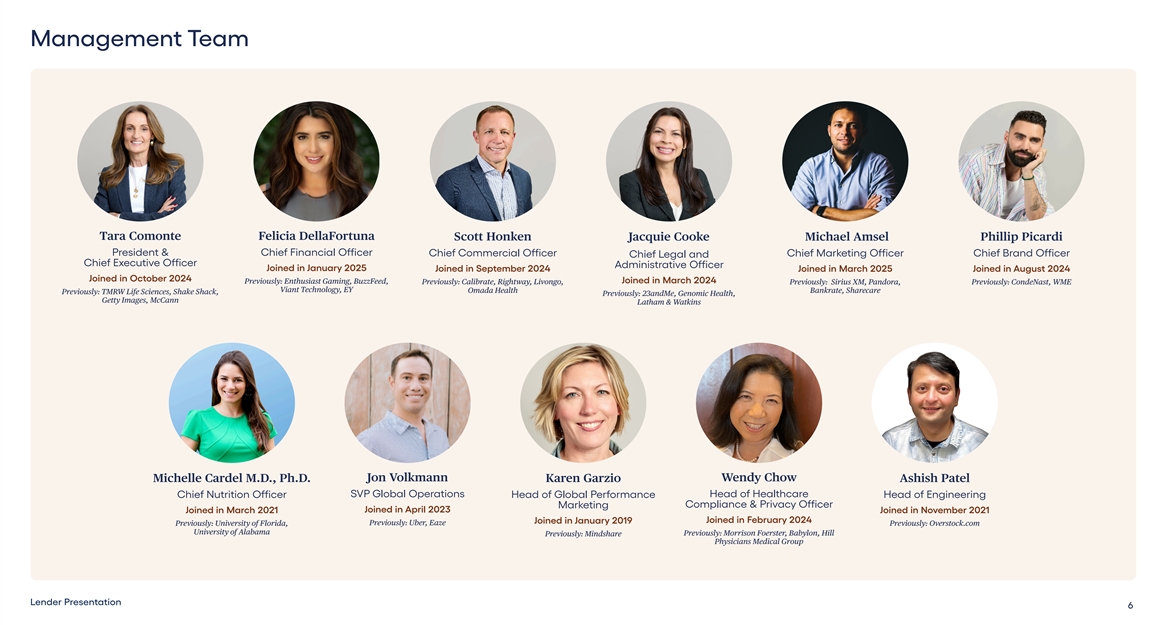

Management Team Tara Comonte Felicia DellaFortuna Scott Honken Jacquie Cooke Michael Amsel Phillip Picardi President & Chief Financial Officer Chief Commercial Officer Chief Marketing Officer Chief Brand Officer Chief Legal and Chief Executive Officer Administrative Officer Joined in January 2025 Joined in September 2024 Joined in March 2025 Joined in August 2024 Joined in October 2024 Joined in March 2024 Previously: Enthusiast Gaming, BuzzFeed, Previously: Calibrate, Rightway, Livongo, Previously: Sirius XM, Pandora, Previously: CondeNast, WME Viant Technology, EY Omada Health Bankrate, Sharecare Previously: TMRW Life Sciences, Shake Shack, Previously: 23andMe, Genomic Health, Getty Images, McCann Latham & Watkins Jon Volkmann Wendy Chow Michelle Cardel M.D., Ph.D. Karen Garzio Ashish Patel SVP Global Operations Head of Healthcare Chief Nutrition Officer Head of Global Performance Head of Engineering Compliance & Privacy Officer Marketing Joined in April 2023 Joined in March 2021 Joined in November 2021 Joined in February 2024 Joined in January 2019 Previously: Uber, Eaze Previously: University of Florida, Previously: Overstock.com University of Alabama Previously: Morrison Foerster, Babylon, Hill Previously: Mindshare Physicians Medical Group Lender Presentation 6

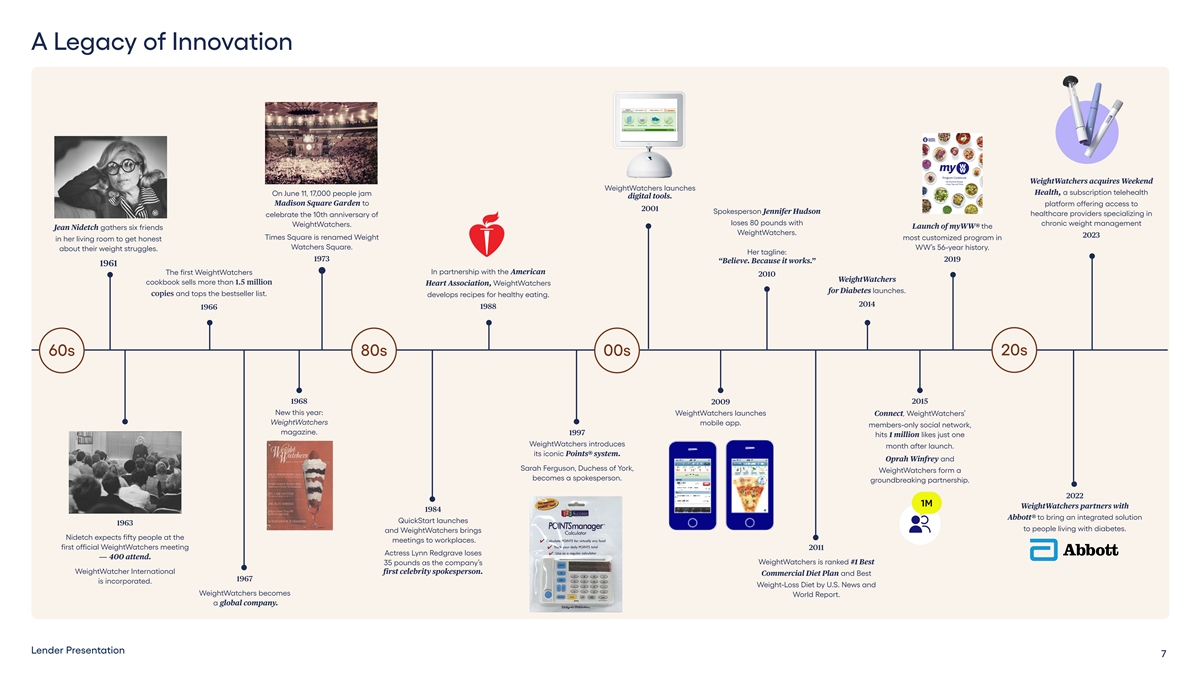

A Legacy of Innovation WeightWatchers acquires Weekend WeightWatchers launches Health, a subscription telehealth On June 11, 17,000 people jam digital tools. Madison Square Garden to platform offering access to 2001 Spokesperson Jennifer Hudson healthcare providers specializing in celebrate the 10th anniversary of loses 80 pounds with chronic weight management WeightWatchers. Launch of myWW® the Jean Nidetch gathers six friends WeightWatchers. 2023 Times Square is renamed Weight most customized program in in her living room to get honest Watchers Square. WW’s 56-year history. about their weight struggles. Her tagline: 1973 2019 “Believe. Because it works.” 1961 In partnership with the American The first WeightWatchers 2010 WeightWatchers cookbook sells more than 1.5 million Heart Association, WeightWatchers for Diabetes launches. copies and tops the bestseller list. develops recipes for healthy eating. 2014 1988 1966 20s 60s 80s 00s 1968 2015 2009 New this year: WeightWatchers launches Connect, WeightWatchers’ WeightWatchers mobile app. members-only social network, magazine. 1997 hits 1 million likes just one WeightWatchers introduces month after launch. its iconic Points® system. Oprah Winfrey and Sarah Ferguson, Duchess of York, WeightWatchers form a becomes a spokesperson. groundbreaking partnership. 2022 WeightWatchers partners with 1984 Abbott® to bring an integrated solution QuickStart launches 1963 to people living with diabetes. and WeightWatchers brings Nidetch expects fifty people at the meetings to workplaces. first official WeightWatchers meeting 2011 Actress Lynn Redgrave loses — 400 attend. WeightWatchers is ranked #1 Best 35 pounds as the company’s WeightWatcher International first celebrity spokesperson. Commercial Diet Plan and Best 1967 is incorporated. Weight-Loss Diet by U.S. News and WeightWatchers becomes World Report. a global company. Lender Presentation 7

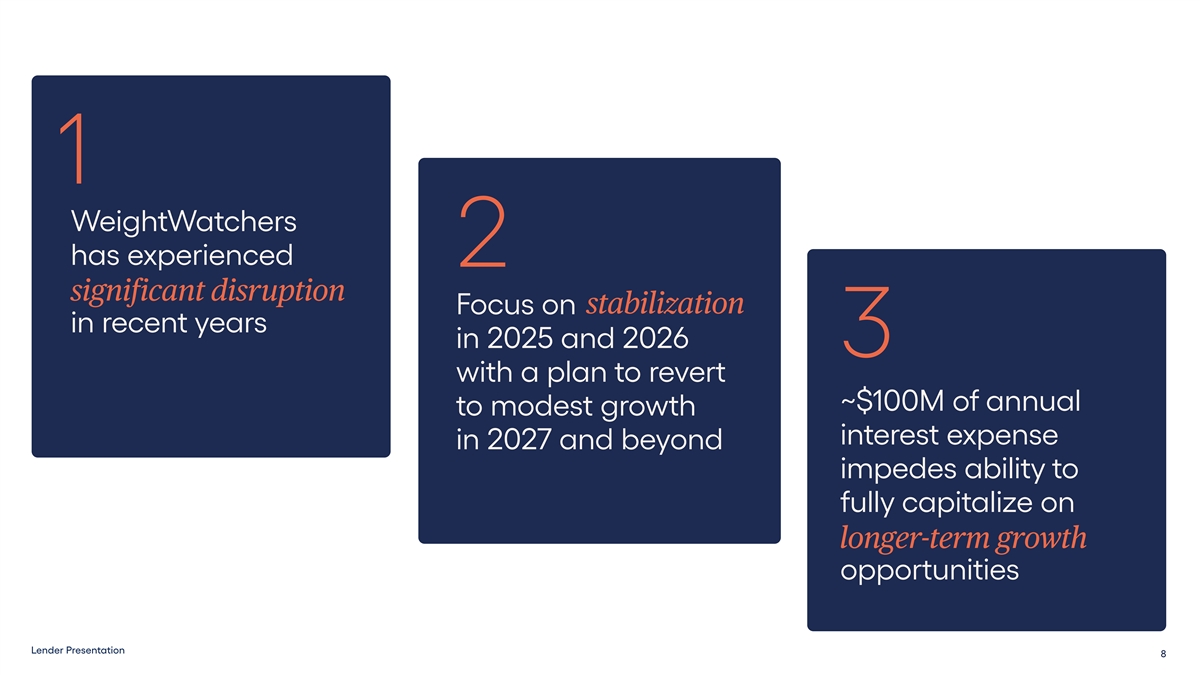

1 WeightWatchers has experienced 2 significant disruption significant disruption stabilization Focus on stabilization in recent years in 2025 and 2026 3 with a plan to revert ~$100M of annual to modest growth interest expense in 2027 and beyond impedes ability to fully capitalize on longer-term growth longer-term growth opportunities Lender Presentation 8

Company 2 Overview Lender Presentation

2024 by the Numbers $786M 3.3M Revenue Subscribers 1.1M ~3,000 Clinic prescriptions Coaches 11 27B 68% Month retention 1 Adjusted gross margins Foods tracked More than $149M 20,000 Adjusted EBITDAS meetings per month 10M ~410 2 Workshop check-ins Clinicians 19% 6.5B Adjusted EBITDAS 1 Activities tracked margin Source: Company’s audited financials for FY24 and represent Non-GAAP Financial Measures and Internal Company Data 1 Tracking events since 2015 2 Includes Registered Dietitians Please see Appendix for reconciliations of non-GAAP financial measures to the closest GAAP financial measures. Lender Presentation 10

62 years later and we're still the most effective most effectiv weight loss program #1 Best Weight-Loss Diet—for the 15th Year by U.S. News & #1 1 World Report 2 US doctor-recommended weight-loss program #1 More effective for weight loss than reliance on standard 3.5x 3 nutritional guidance 4 More effective for weight loss than physician counseling or 2x 5 do-it-yourself ® More weight loss by combining our Points program with 54% 6 weight-loss medication than medication alone Members who transitioned from Clinic program to Behavioral 1.8% 7 program continued to lose an additional 1.8% of their body weight 1 U.S. News (2024). 2 Based on a 2023 Cerner Inviza survey of 500 doctors who recommend weight-loss programs to patients. 3 Palacios et al. 4 Tate et al. 2022. 5 Jebb et al. 6 Based on a 12-week randomized controlled trial (n=101) that compared taking bupropion & naltrexone medications on their own to taking bupropion & naltrexone with the Ⓡ WeightWatchers behavioral program, including the Points Program. Jones et al. Manuscript in draft. Funded by WW International, Inc. 7 On average, after 13 weeks. Based on observational data from 200 individuals. Le Len nd de er r P Pr re es se en nt ta at tiio on n 11

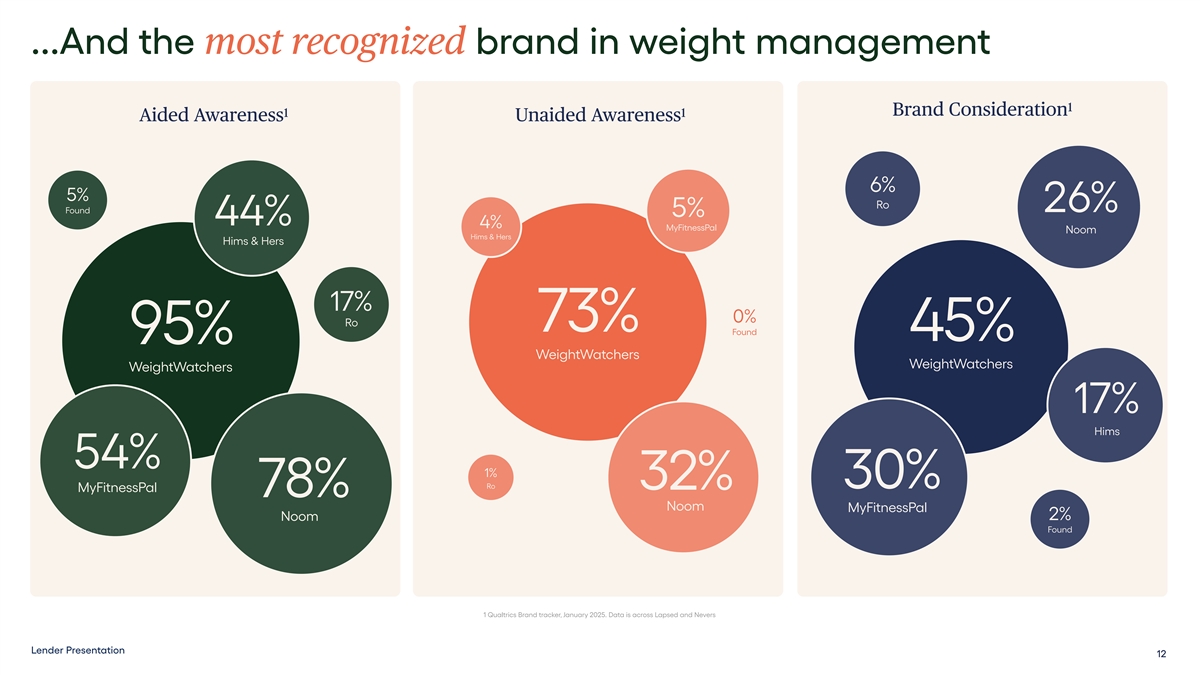

...And the most recognized brand in weight management 1 Brand Consideration 1 1 Aided Awareness Unaided Awareness 6% 5% Ro 26% Found 5% 44% 4% MyFitnessPal Noom Hims & Hers Hims & Hers 17% 0% Ro 73% Found 45% 95% WeightWatchers WeightWatchers WeightWatchers 17% Hims 54% 1% 30% Ro 32% MyFitnessPal 78% Noom MyFitnessPal 2% Noom Found 1 Qualtrics Brand tracker, January 2025. Data is across Lapsed and Nevers Lender Presentation 12

WeightWatchers offers a holistic model of care Community Points® Support & Program & Coaching Digital Tools B2B & Clinical Strategic Support Partnerships Programs Lender Presentation 13

50+ years of impac global t 50+ Years in global markets Canada Sweden UK Netherlands Germany Belgium 3.3M Switzerland USA France Members globally ~30% International revenue Australia 11 Markets New Zealand Source: Company data Fiscal Year Ended 2024 Lender Presentation 14

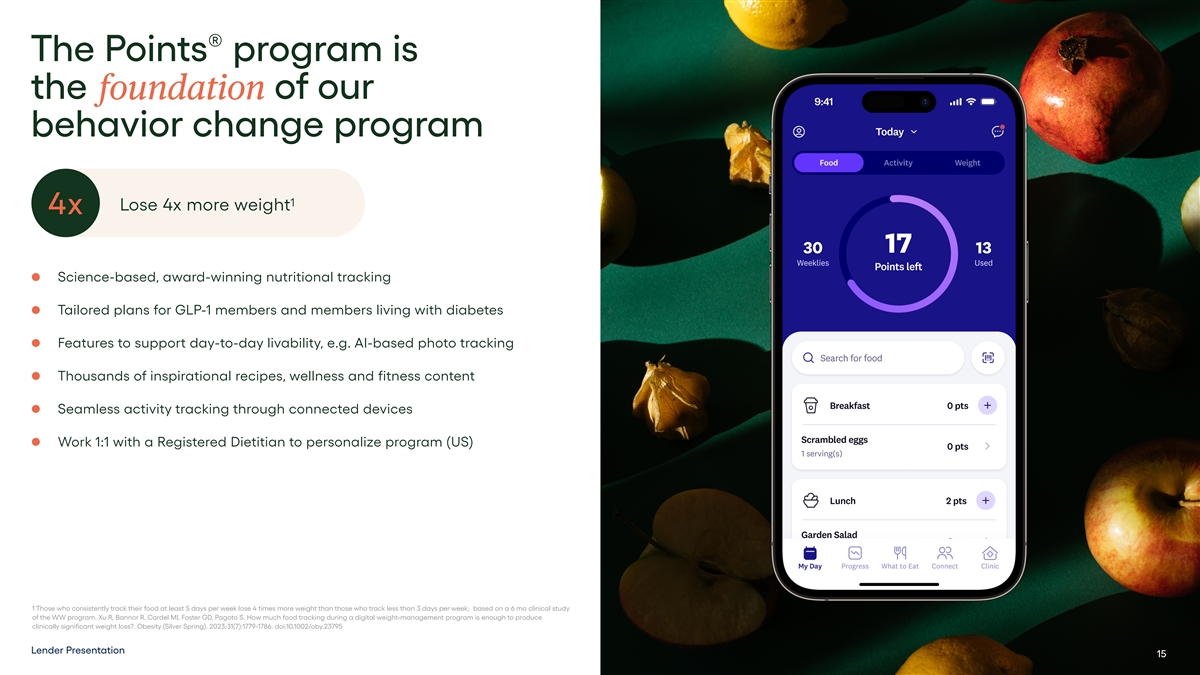

® The Points program is the foundatio of our foundation behavior change program 1 Lose 4x more weight 4x Science-based, award-winning nutritional tracking Tailored plans for GLP-1 members and members living with diabetes Features to support day-to-day livability, e.g. AI-based photo tracking Thousands of inspirational recipes, wellness and fitness content Seamless activity tracking through connected devices Work 1:1 with a Registered Dietitian to personalize program (US) 1 Those who consistently track their food at least 5 days per week lose 4 times more weight than those who track less than 3 days per week; based on a 6 mo clinical study of the WW program. Xu R, Bannor R, Cardel MI, Foster GD, Pagoto S. How much food tracking during a digital weight-management program is enough to produce clinically significant weight loss?. Obesity (Silver Spring). 2023;31(7):1779-1786. doi:10.1002/oby.23795 Lender Presentation 15

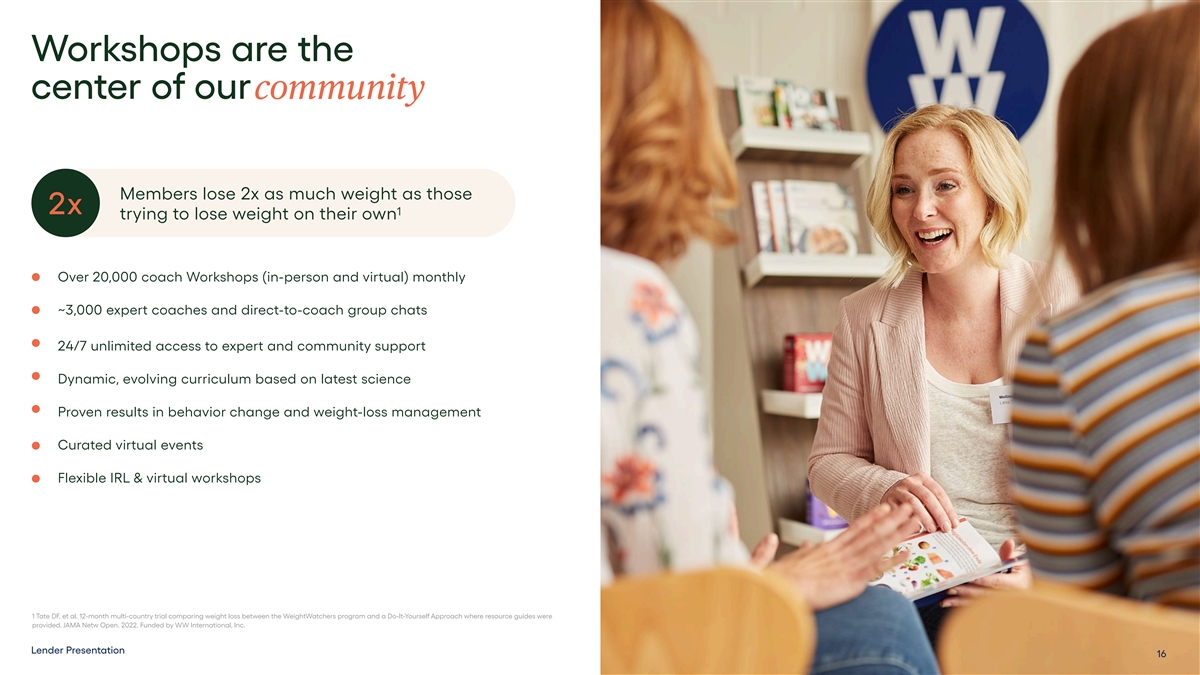

Workshops are the center of ourcommunity Members lose 2x as much weight as those 2x 1 trying to lose weight on their own Over 20,000 coach Workshops (in-person and virtual) monthly ~3,000 expert coaches and direct-to-coach group chats 24/7 unlimited access to expert and community support Dynamic, evolving curriculum based on latest science Proven results in behavior change and weight-loss management Curated virtual events Flexible IRL & virtual workshops 1 Tate DF, et al. 12-month multi-country trial comparing weight loss between the WeightWatchers program and a Do-It-Yourself Approach where resource guides were provided. JAMA Netw Open. 2022. Funded by WW International, Inc. Lender Presentation 16

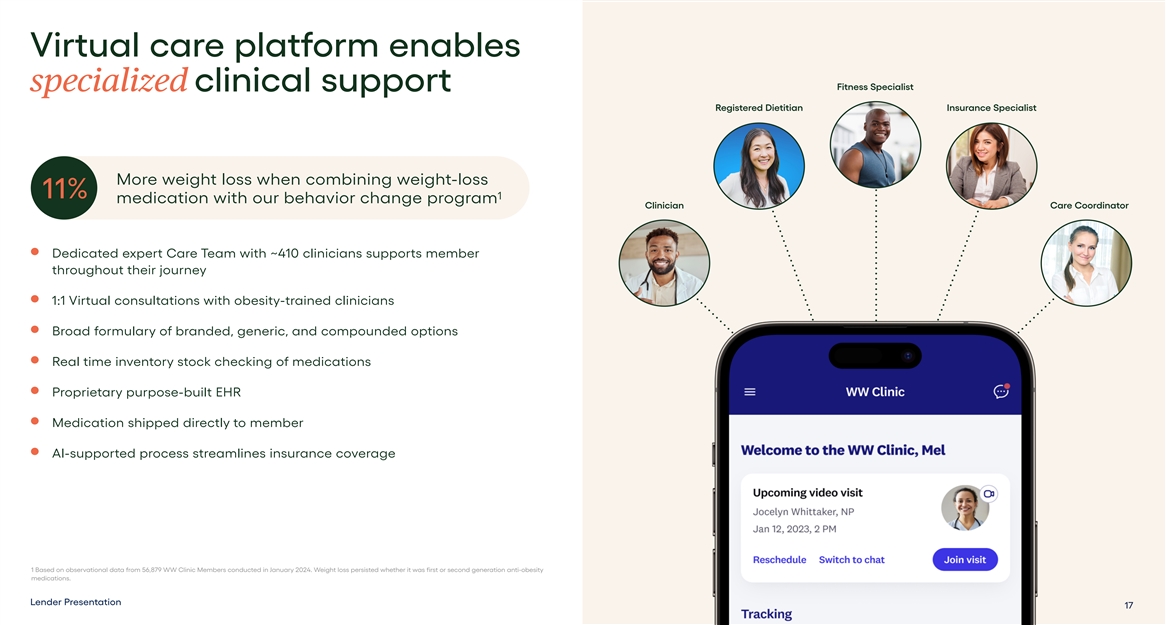

Virtual care platform enables Fitness Specialist specialized specializ clinical support Registered Dietitian Insurance Specialist More weight loss when combining weight-loss 11% 1 medication with our behavior change program Clinician Care Coordinator Dedicated expert Care Team with ~410 clinicians supports member throughout their journey 1:1 Virtual consultations with obesity-trained clinicians Broad formulary of branded, generic, and compounded options Real time inventory stock checking of medications Proprietary purpose-built EHR Medication shipped directly to member AI-supported process streamlines insurance coverage 1 Based on observational data from 56,879 WW Clinic Members conducted in January 2024. Weight loss persisted whether it was first or second generation anti-obesity medications. Lender Presentation 17

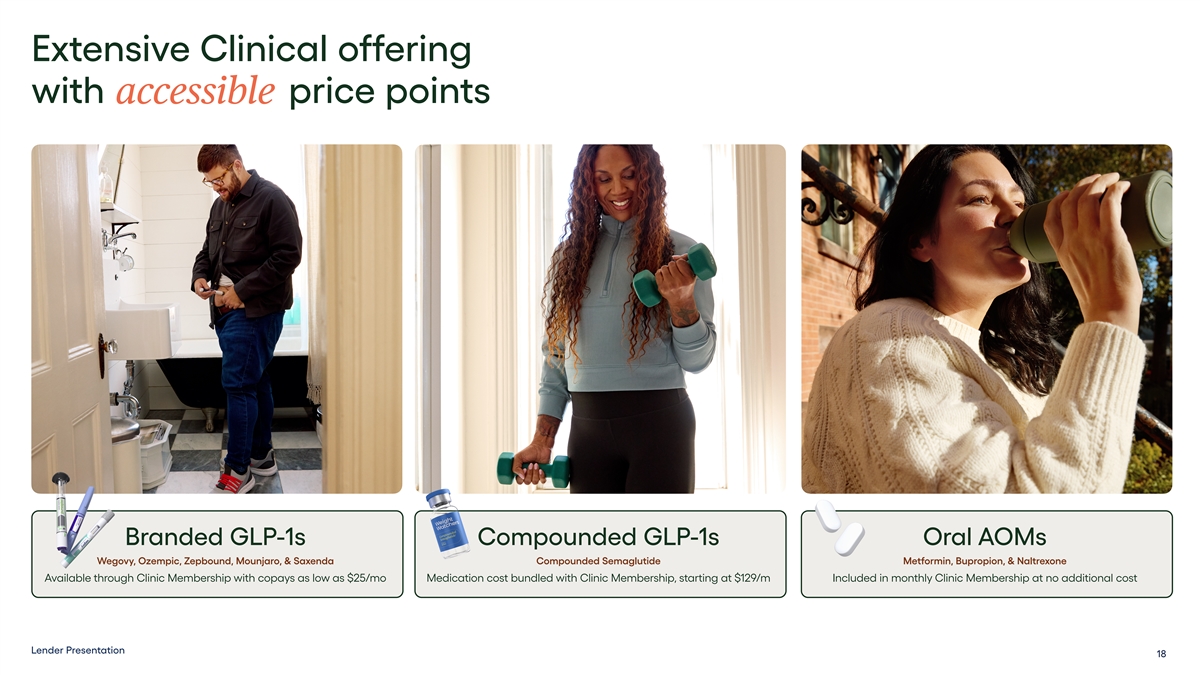

Extensive Clinical offering with price poin accessible ts Branded GLP-1s Compounded GLP-1s Oral AOMs Wegovy, Ozempic, Zepbound, Mounjaro, & Saxenda Compounded Semaglutide Metformin, Bupropion, & Naltrexone Available through Clinic Membership with copays as low as $25/mo Medication cost bundled with Clinic Membership, starting at $129/m Included in monthly Clinic Membership at no additional cost Lender Presentation 18

WW4B: Meeting the unique needs of emp emplo loy y er e s s and pay payer erss Tailored programming WeightWatchers for Business (WW4B) delivers a full- spectrum weight health platform designed to meet the dynamic needs of employers, health plans, and PBMs Flexible delivery model Members engage how, when, and where is convenient for them, digitally and in person Aligned with client strategies Employers and health plans approach GLP-1 coverage Kim Beck in varying ways—WW4B delivers best-in-class support Head of Health & Wellness, Labcorp whether their members are on or off medication Our goal was to offer our clients a singular “ solution for their weight management needs Impactful ROI —from meaningful behavior change for all, Clients realize a strong and 3rd party validated to the necessary and life-saving clinical return on their investment through enhanced interventions like medication for those who outcomes and enduring behavior changes qualify. WeightWatchers for Business helped us meet all those needs and more, all in one seamless experience. ” Lender Presentation 19

Leading obesity experts ground our program in the latest clinical evidence Clinical Research Partners Scientific Advisory Board Amy Ahern, Ph.D. Cheryl A.M. Anderson Gary G. Bennett, Ph.D. Ania Jastreboff, M.D., Ph.D. Ph.D., MPH, M.S. Duke University Yale University University of Cambridge UC San Diego Robert Kushner, M.D., M.S. Stephanie Faubion, Gary Foster, Ph.D. M.D., M.B.A Northwestern University University of Pennsylvania Mayo Clinic Lender Presentation 20

50 years Grounded in of scientific innovation 180+ 64 43 Scientific From Randomized Measured Impact Across Publications Controlled Trials (RCTs) Clinical and Behavioral Metrics Formative Pilots Agile research initiatives designed to answer key program development questions and drive continuous improvement of the WW program Internal Trials Rigorous, ethically conducted studies addressing emerging scientific questions to refine and validate program components External Trials Independent, scientifically robust evaluations confirming the efficacy and real-world effectiveness of the WW program Lender Presentation 21

With superior results, WeightWatchers outpaces competition Clinic offering Weight Loss at 3 months Weight Loss at 12 months 1 WeightWatchers Clinic 19.4% 1 WeightWatchers Clinic 8.9% 4 Ro 16% 2 Hims & Hers 7% 3 Calibrate Hims 16% 7% 3 Calibrate 5 7% Form 15% 1 WeightWatchers: Ard JD, Hong YR, Foster GD, Medcalf A, Nadolsky S, Cardel MI. Twelve-month analysis of real-world evidence from a telehealth obesity treatment provider using anti-obesity medications. Obesity. 2024. Online ahead of print. 2 Hims and Hers https://investors.hims.com/events-and-presentations/default.aspx 3 Calibrate https://www.joincalibrate.com/pages/results-report 4 Ro https://ro.co/press/body-twelve-month-outcomes/ 5 Form Health Blog https://www.formhealth.co/blog/weight-loss-medication-guide Note: All percentages are percent of body weight lost over the specified time period. The weight loss comparisons shown represent data available according to company websites as of April 29, 2025, at this subset of companies that also offer access to GLP-1 medications. The patient populations measured, study methodologies and medications used by study participants may vary across companies. Lender Presentation 22

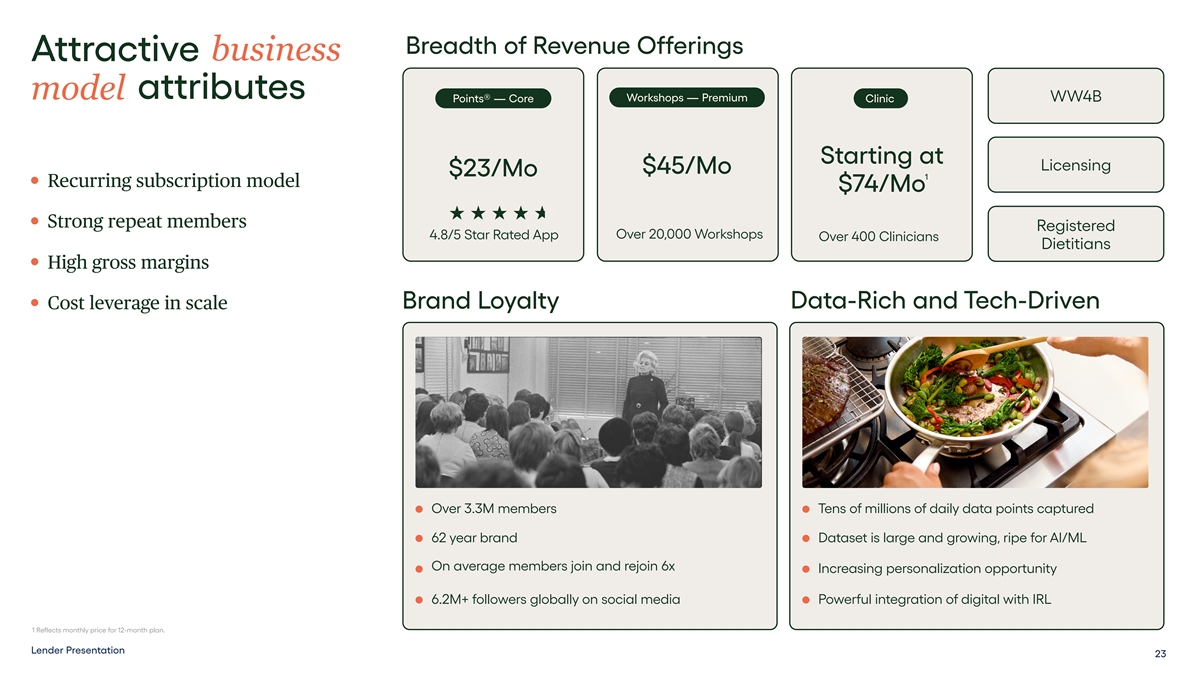

Breadth of Revenue Offerings business Attractive business attributes model Workshops — Premium WW4B Points® — Core Clinic Starting at Licensing $45/Mo $23/Mo 1 Recurring subscription model $74/Mo Strong repeat members Registered Over 20,000 Workshops 4.8/5 Star Rated App Over 400 Clinicians Dietitians High gross margins Data-Rich and Tech-Driven Brand Loyalty Cost leverage in scale Over 3.3M members Tens of millions of daily data points captured 62 year brand Dataset is large and growing, ripe for AI/ML On average members join and rejoin 6x Increasing personalization opportunity 6.2M+ followers globally on social media Powerful integration of digital with IRL 1 Reflects monthly price for 12-month plan. Lender Presentation 23

State of 3 the Union Lender Presentation

Key Challenges Impacting Business Performance 1 Evolving consumer consumer preferences behavior and the 2 growth of GLP-1s Es Esca calatin latin g c g ompetition in a rapidly 3 expanding market Strategic ov shifts erpivots in reaction to market dynamics Lender Presentation 25

Shift toward wellness over traditional dieting Consumers are increasingly prioritizing holistic health and rejecting traditional weight-loss narratives Rise of free digital tools Evolving Consumer Preferences The rise of free and low-cost DIY weight-loss apps reflects consumers’ growing demand for self-guided, flexible solutions The weight loss radically landscape has radically Social media influence The DIY trend is further fueled by influencers sharing changed change — and with it, personal success stories and guidance via Instagram, TikTok, and YouTube consumer preferences Rapid GLP-1 adoption reshaping the market The introduction and widespread adoption of GLP-1 medications have revolutionized weight management, challenging conventional programs Lender Presentation 26

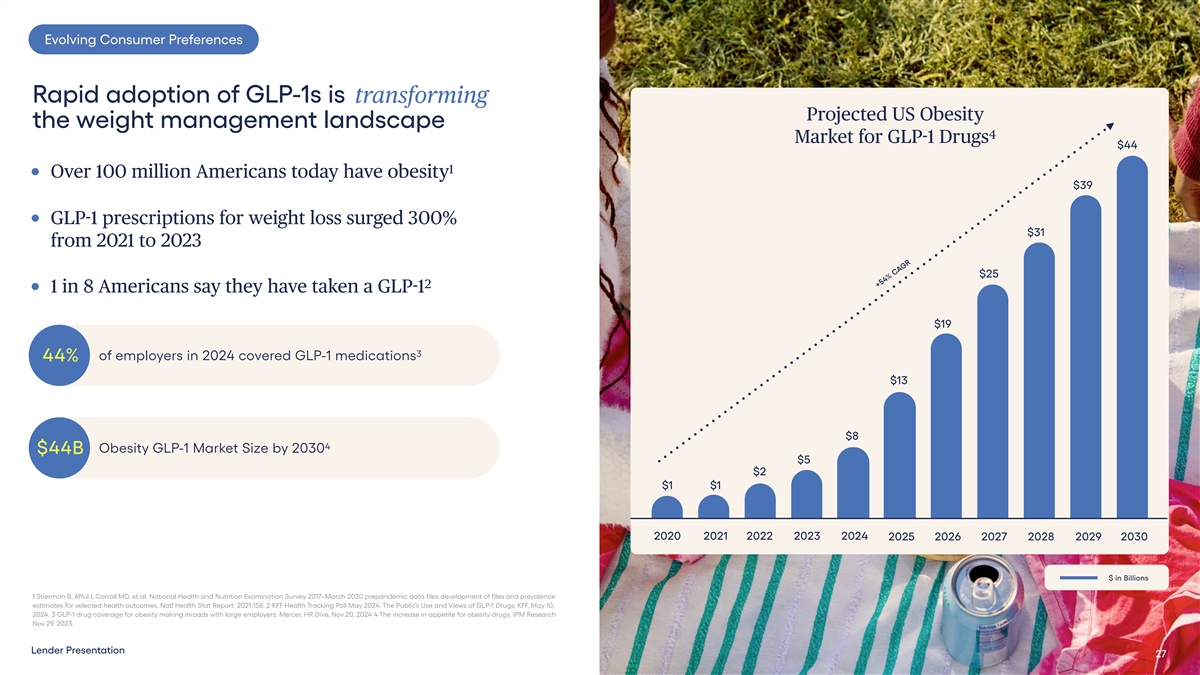

Evolving Consumer Preferences Rapid adoption of GLP-1s is tr trans ansfformin orming g Projected US Obesity the weight management landscape 4 Market for GLP-1 Drugs $44 1 Over 100 million Americans today have obesity $39 GLP-1 prescriptions for weight loss surged 300% $31 from 2021 to 2023 $25 2 1 in 8 Americans say they have taken a GLP-1 $19 3 of employers in 2024 covered GLP-1 medications 44% $13 $8 4 Obesity GLP-1 Market Size by 2030 $44B $5 $2 $1 $1 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 $ in Billions 1 Stierman B, Afful J, Carroll MD, et al. National Health and Nutrition Examination Survey 2017–March 2020 prepandemic data files development of files and prevalence estimates for selected health outcomes. Natl Health Stat Report. 2021;158. 2 KFF Health Tracking Poll May 2024. The Public’s Use and Views of GLP-1 Drugs, KFF, May 10, 2024. 3 GLP-1 drug coverage for obesity making inroads with large employers: Mercer, HR Dive, Nov 20, 2024 4 The increase in appetite for obesity drugs, JPM Research Nov 29, 2023. Lender Presentation 27 +54% CAGR 4,245 4,423 4,169 3,546 3,798

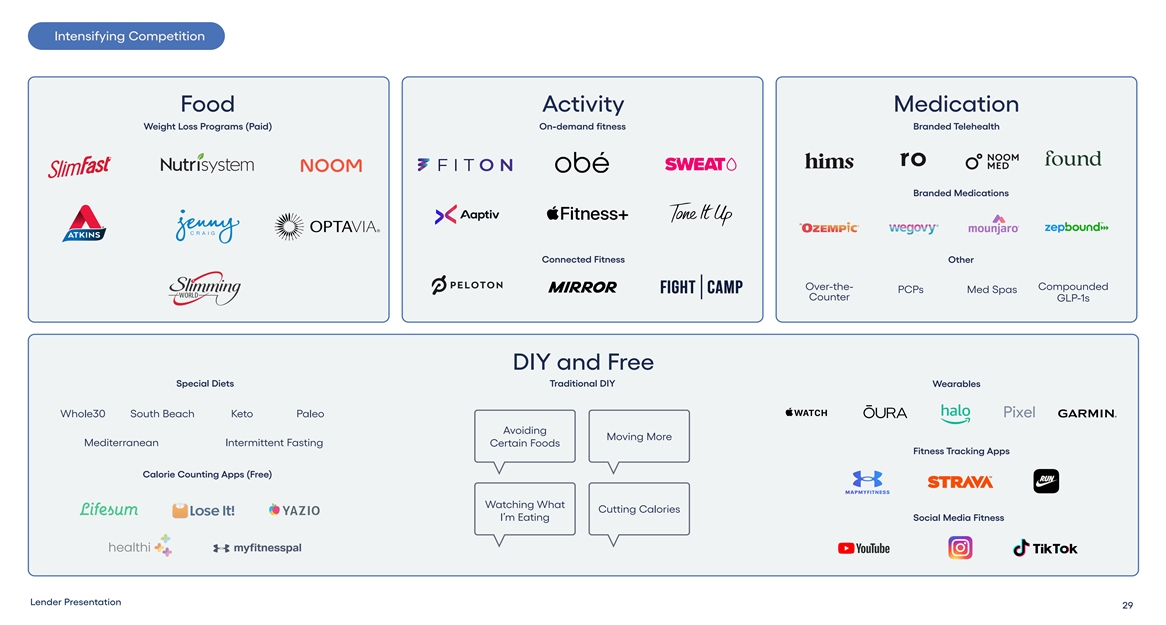

Intensifying Competition New competitors and innovations are reshaping the weight management market The rise of wearables, social media content, free apps and prescription medications is rapidly changing Escalating competition consumer behavior in a r rapidly apidly expanding Increasingly fragmented market with explosive growth in competition market Lender Presentation 28

Intensifying Competition Food Activity Medication Weight Loss Programs (Paid) On-demand fitness Branded Telehealth Branded Medications Connected Fitness Other Over-the- Compounded PCPs Med Spas Counter GLP-1s DIY and Free Special Diets Traditional DIY Wearables Whole30 South Beach Keto Paleo Avoiding Moving More Mediterranean Intermittent Fasting Certain Foods Fitness Tracking Apps Calorie Counting Apps (Free) Watching What Cutting Calories I’m Eating Social Media Fitness Lender Presentation 29

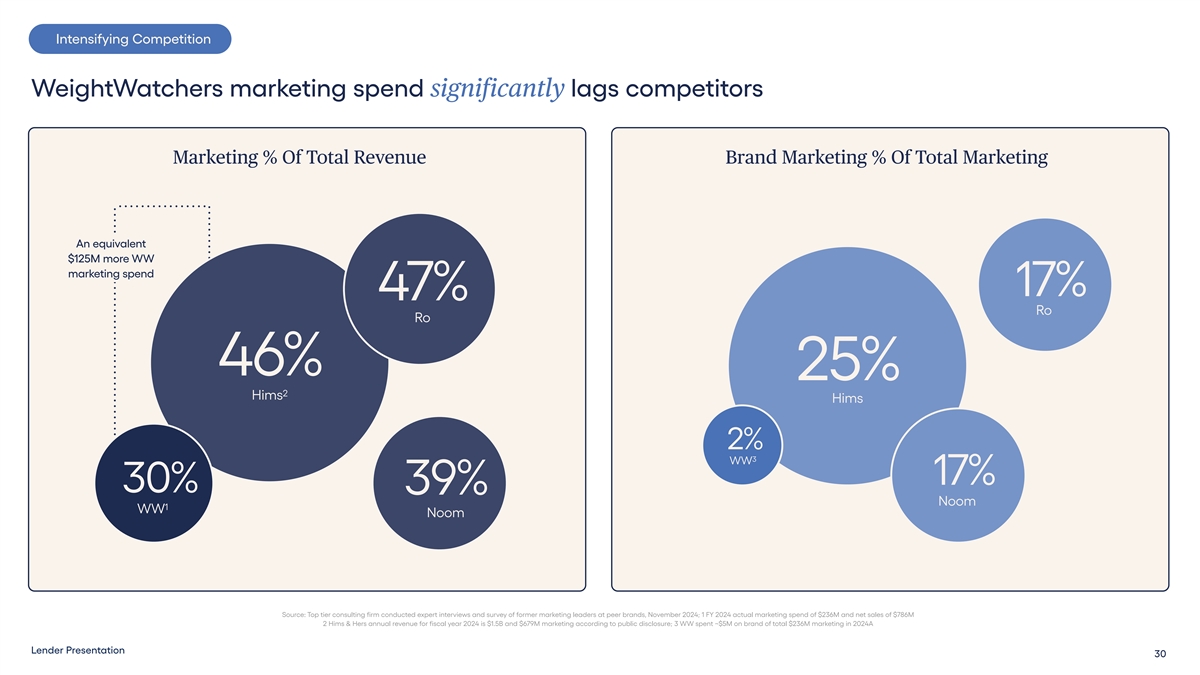

Intensifying Competition WeightWatchers marketing spend significantly lags competitors Marketing % Of Total Revenue Brand Marketing % Of Total Marketing An equivalent Hims & Hers $125M more WW marketing spend 17% 47% Ro Ro 46% 25% 2 Hims Hims 2% 3 WW 17% 30% 39% Noom 1 WW Noom Source: Top tier consulting firm conducted expert interviews and survey of former marketing leaders at peer brands, November 2024; 1 FY 2024 actual marketing spend of $236M and net sales of $786M 2 Hims & Hers annual revenue for fiscal year 2024 is $1.5B and $679M marketing according to public disclosure; 3 WW spent ~$5M on brand of total $236M marketing in 2024A Lender Presentation 30

Strategic Shifts Abrupt pivot from in-person workshops An exit from consumer products & licensing strategy shifts Reactive strategy shift Centralization of international operations have driven long-term Overreliance on performance marketing revenue headwinds and discounting Lender Presentation 31

Strategic Shifts Legacy business channels created significant brand awareness; organic growth strategy pivots under way Consumer products Celebrity endorsements Physical workshops Brand awareness Lender Presentation 32

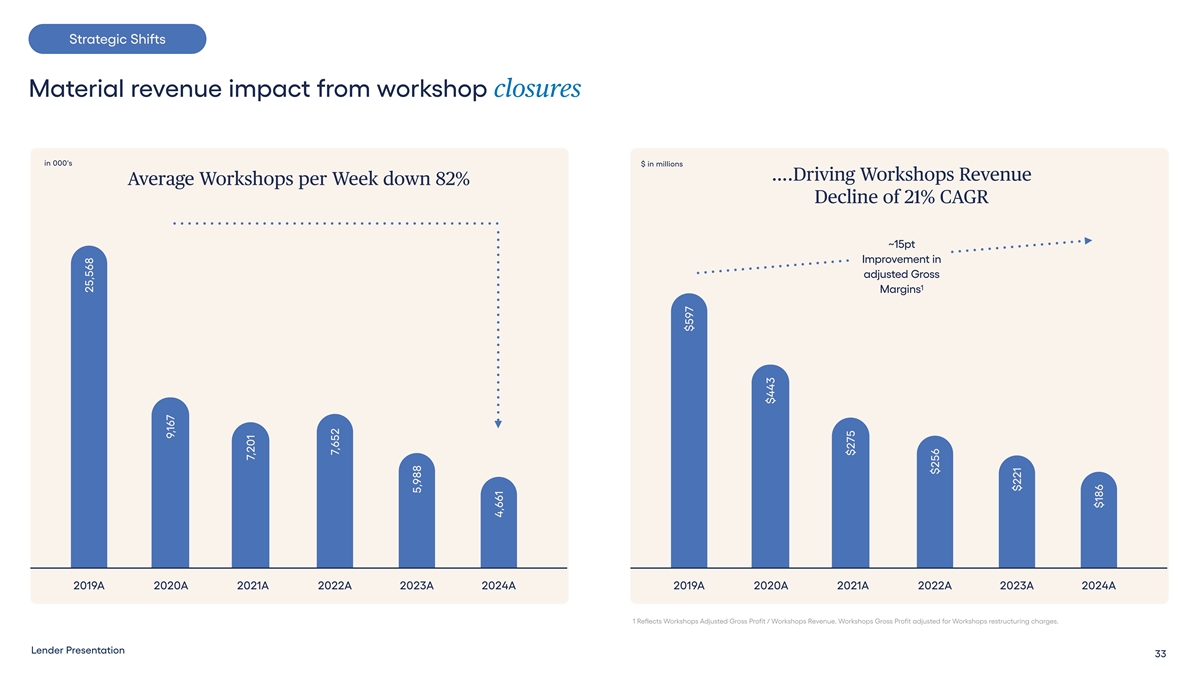

Strategic Shifts Material revenue impact from workshop closures in 000's $ in millions ….Driving Workshops Revenue Average Workshops per Week down 82% Decline of 21% CAGR ~15pt Improvement in adjusted Gross 1 Margins 2019A 2020A 2021A 2022A 2023A 2024A 2019A 2020A 2021A 2022A 2023A 2024A 1 Reflects Workshops Adjusted Gross Profit / Workshops Revenue. Workshops Gross Profit adjusted for Workshops restructuring charges. Lender Presentation 33 25,568 9,167 7,201 7,652 5,988 4,661 $597 $443 $275 $256 $221 $186

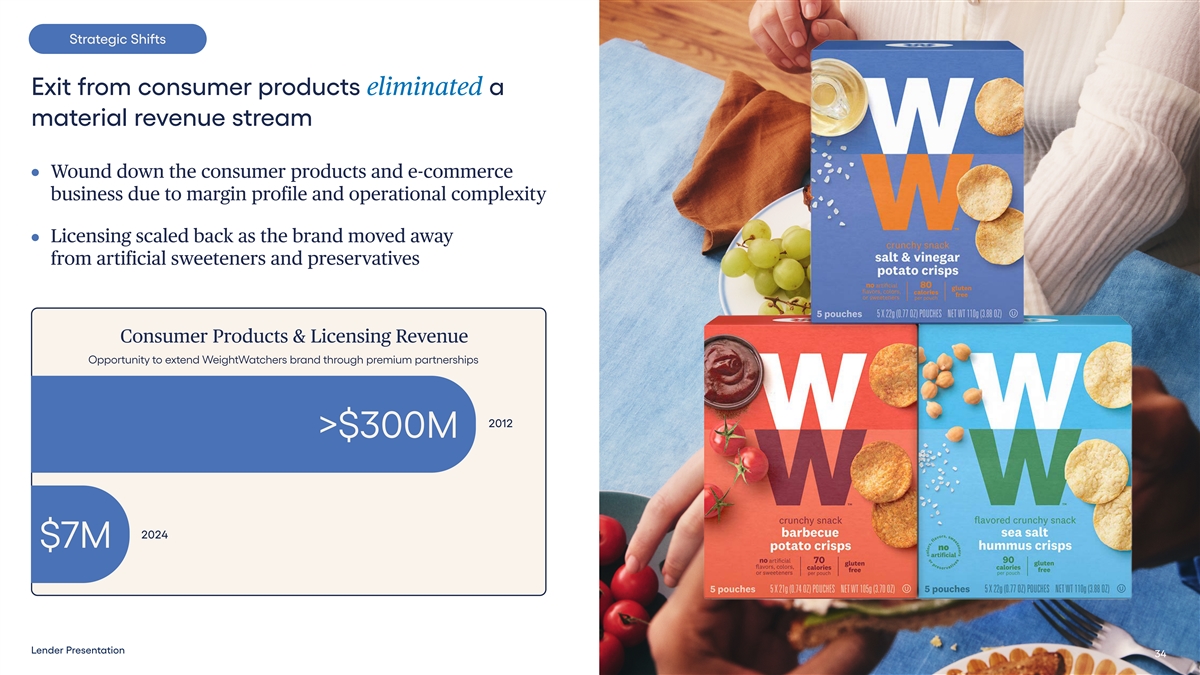

Strategic Shifts Exit from consumer products eliminated a material revenue stream Wound down the consumer products and e-commerce business due to margin profile and operational complexity Licensing scaled back as the brand moved away from artificial sweeteners and preservatives Consumer Products & Licensing Revenue Opportunity to extend WeightWatchers brand through premium partnerships 2012 >$300M Hims Hims 2024 $7M Lender Presentation 34

Strategic Shifts Led to headwind across key growth metrics… headwinds Subs in 000's $5. $5.14 14 $4.6 $4.67 7 $4.37 $4.37 $4.26 $4.26 $3. $3.97 97 $3. $3.9 95 5 2019 2019A A 2020 2020A A 2021A 2021A 2022 2022A A 2023 2023A A 2024 2024A A To Tot ta al l E Eo oP P S Su ub bs sc cr ri ib be er rs s Av Avg g. . R Re ev v P Pe er r P Pa aiid d W We ee ek k Le Len nd de er r P Pr re es se en nt ta at tiio on n 35 4,245 4,245 4, 4,423 423 4, 4,16 169 9 3,546 3,546 3, 3,79 798 8 3,335 3,336

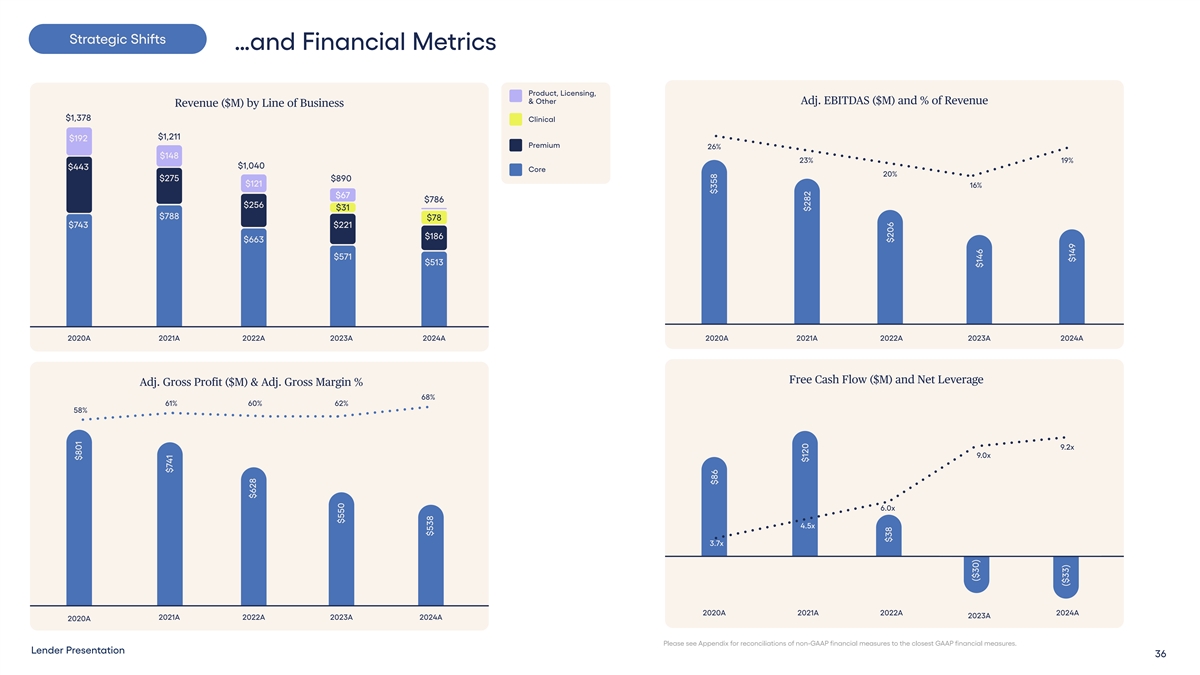

Strategic Shifts …and Financial Metrics Product, Licensing, & Other Adj. EBITDAS ($M) and % of Revenue Revenue ($M) by Line of Business $1,378 Clinical $1,211 $192 Premium 26% $148 23% 19% $1,040 $443 Core 20% $275 $890 $121 16% $67 $786 $256 $31 $788 $78 $743 $221 $186 $663 $571 $513 2020A 2021A 2022A 2023A 2024A 2020A 2021A 2022A 2023A 2024A Free Cash Flow ($M) and Net Leverage Adj. Gross Profit ($M) & Adj. Gross Margin % 68% 61% 60% 62% 58% 9.2x 9.0x 6.0x 4.5x 3.7x 2020A 2021A 2022A 2024A 2023A 2021A 2022A 2023A 2024A 2020A Please see Appendix for reconciliations of non-GAAP financial measures to the closest GAAP financial measures. Lender Presentation 36 $801 $741 $628 $550 $538 4,423 $358 $86 $120 $282 $38 $206 ($30) $146 ($33) $149

Path to Stabilization 4 Lender Presentation

The trus trust ted leade ed leader in weight management, combining science and commu science and community to help our millions o millions of member f member s live their healthiest lives Lender Presentation 38

2025 Strategic Priorities 1 Deliver a unified unified 2 and engaging Revitalize member our brand and experience 3 reclaimour reclaim Innovate Innovat and 4 leadership expand expandadjacent position Drive revenue streams operational excellence excellence efficiency and efficiency Lender Presentation 39

Strategic Priorities 1 Deliver a unified unified 2 and engaging Revitalize member our brand and experience 3 reclaimour reclaim Innovate Innovat and 4 leadership expand expandadjacent position Drive revenue streams operational excellence excellence efficiency and efficiency Lender Presentation 40

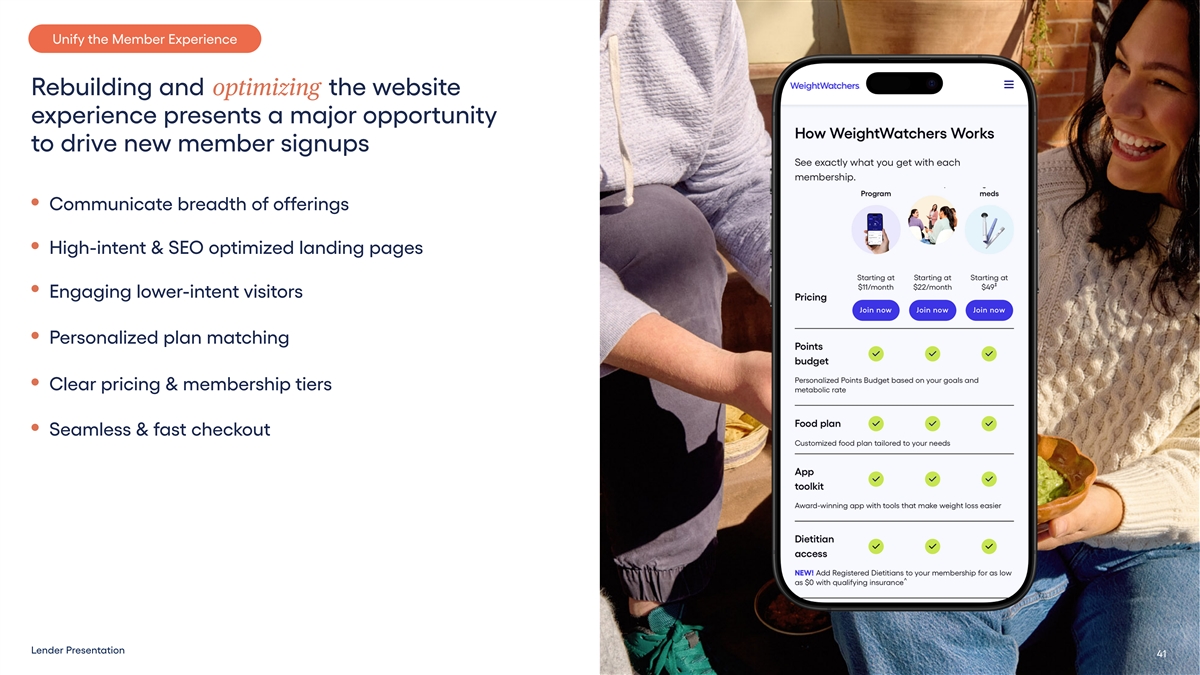

Unify the Member Experience Rebuilding and op optimizin timizin g the website experience presents a major opportunity to drive new member signups Communicate breadth of offerings High-intent & SEO optimized landing pages Engaging lower-intent visitors Personalized plan matching Clear pricing & membership tiers Seamless & fast checkout Lender Presentation 41

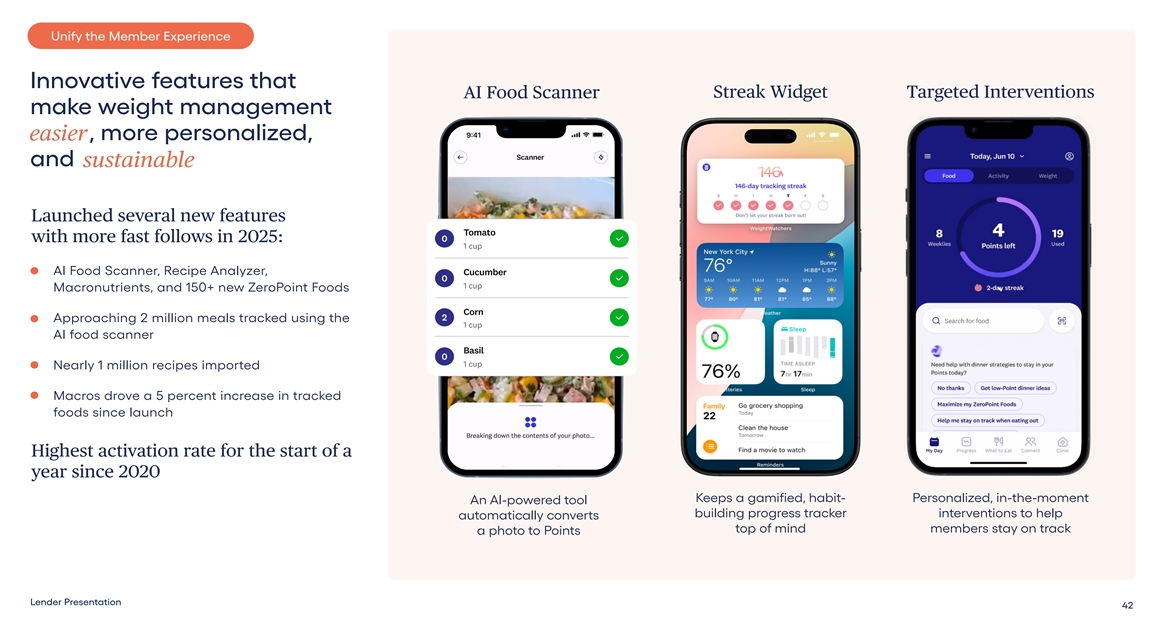

Unify the Member Experience Innovative features that Streak Widget Targeted Interventions AI Food Scanner make weight management easie, more personalized, easier and sustainable sustainable Launched several new features with more fast follows in 2025: AI Food Scanner, Recipe Analyzer, Macronutrients, and 150+ new ZeroPoint Foods ` Approaching 2 million meals tracked using the AI food scanner Nearly 1 million recipes imported Macros drove a 5 percent increase in tracked foods since launch Highest activation rate for the start of a year since 2020 Keeps a gamified, habit- Personalized, in-the-moment An AI-powered tool building progress tracker interventions to help automatically converts top of mind members stay on track a photo to Points Lender Presentation 42

Unify the Member Experience Revitalize the Workshop program and expand member base Expand and advance Modernize digital Invest in Optimize workshop virtual programming workshop experience Coaches footprint Lender Presentation 43

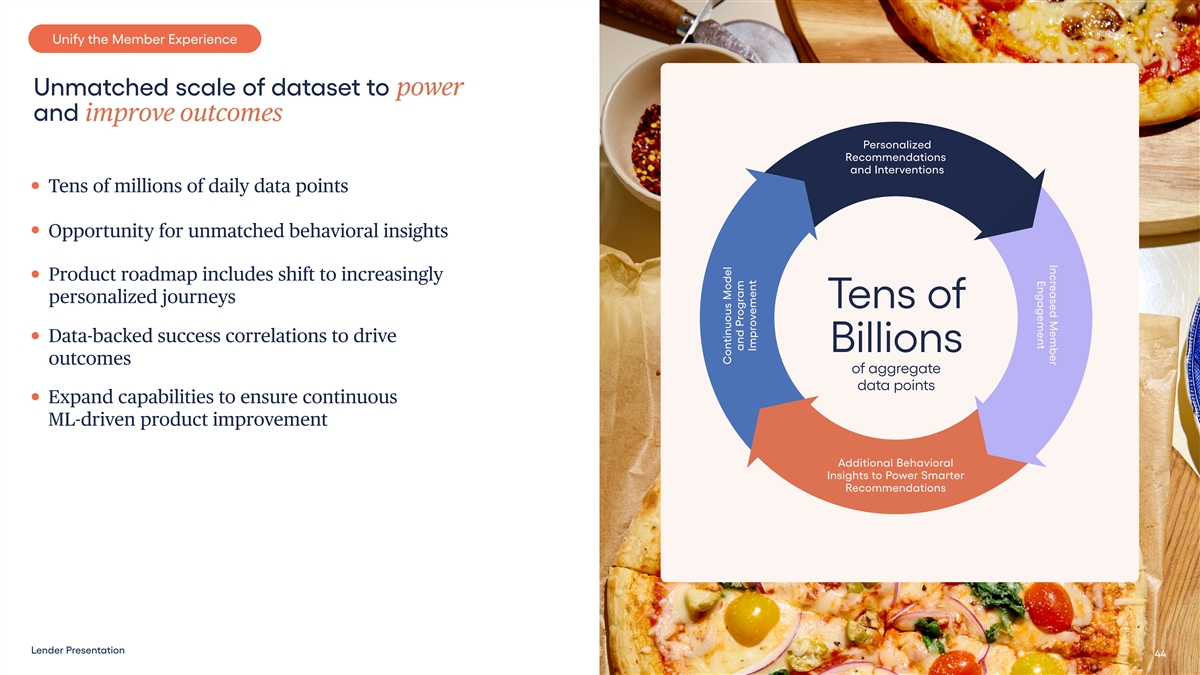

Increased Member Engagement Unify the Member Experience power Unmatched scale of dataset to power and impr impro ov ve ou ed out tcomes comes Personalized Recommendations and Interventions Tens of millions of daily data points Opportunity for unmatched behavioral insights Product roadmap includes shift to increasingly personalized journeys Tens of Data-backed success correlations to drive Billions outcomes of aggregate data points Expand capabilities to ensure continuous ML-driven product improvement Additional Behavioral Insights to Power Smarter Recommendations Lender Presentation 44 44 Continuous Model and Program Improvement

Strategic Priorities 1 Deliver a unified unified 2 and engaging Revitalize member our brand and experience 3 reclaimour reclaim Innovate Innovat and 4 leadership expand expandadjacent position Drive revenue streams operational excellence excellence efficiency and efficiency Lender Presentation 45

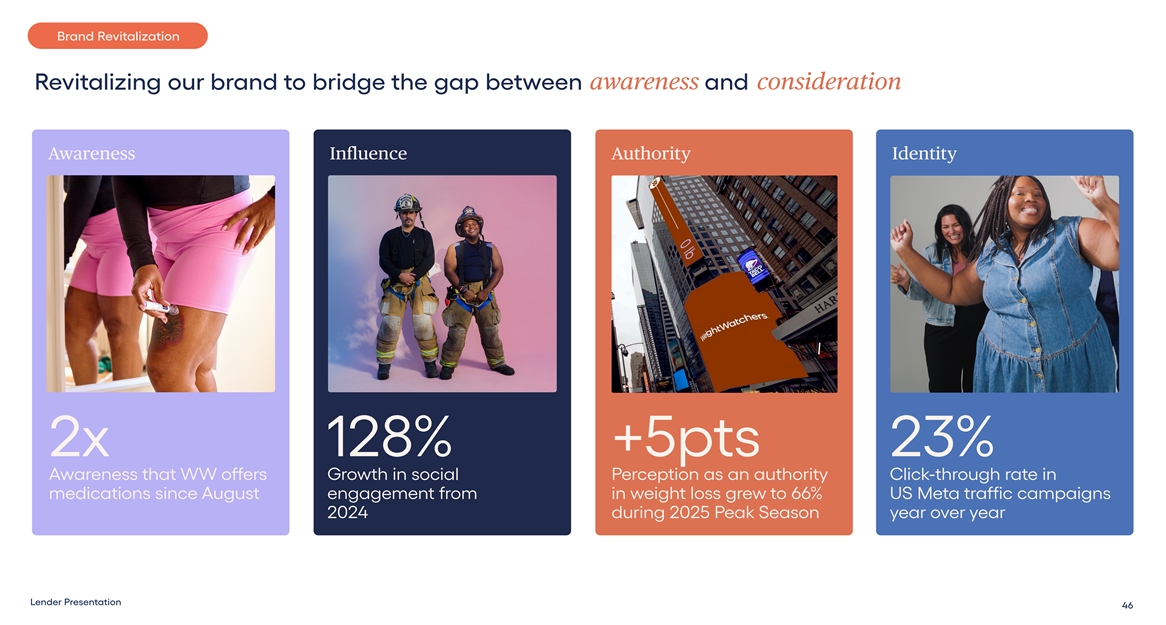

Brand Revitalization awareness consideration Revitalizing our brand to bridge the gap between awarenes and consideration Awareness Influence Authority Identity 2x 128% +5pts 23% Awareness that WW offers Growth in social Perception as an authority Click-through rate in medications since August engagement from in weight loss grew to 66% US Meta traffic campaigns 2024 during 2025 Peak Season year over year Lender Presentation 46

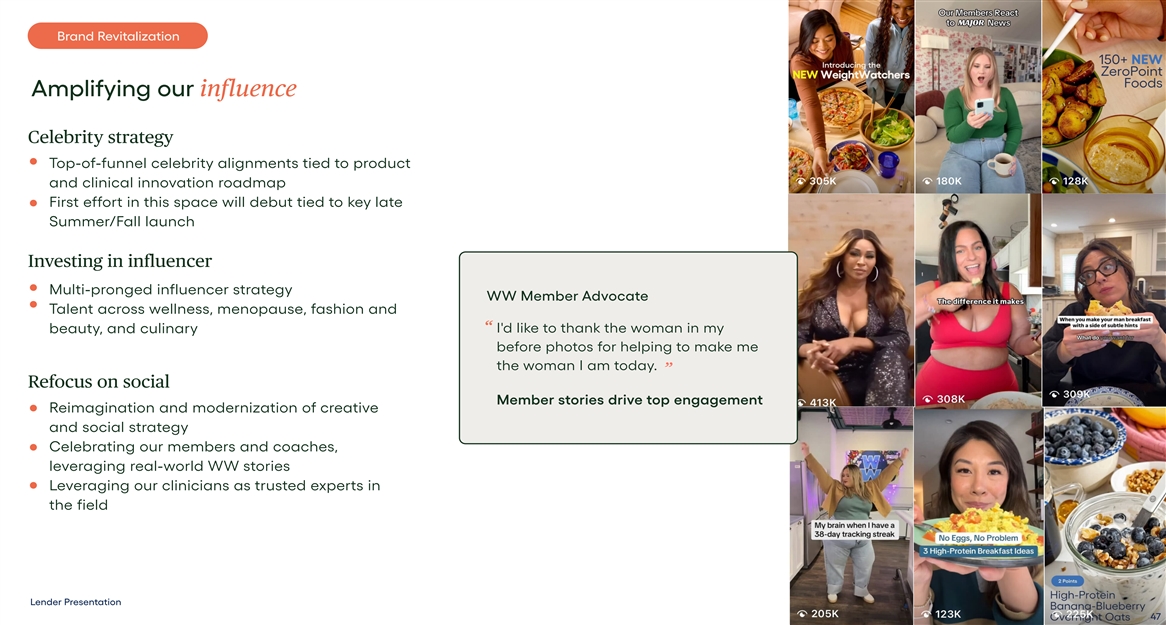

Brand Revitalization Amplifying our influence Celebrity strategy Top-of-funnel celebrity alignments tied to product and clinical innovation roadmap First effort in this space will debut tied to key late Summer/Fall launch Investing in influencer Multi-pronged influencer strategy WW Member Advocate Talent across wellness, menopause, fashion and “ I'd like to thank the woman in my beauty, and culinary before photos for helping to make me the woman I am today. ” Refocus on social Member stories drive top engagement Reimagination and modernization of creative and social strategy Celebrating our members and coaches, leveraging real-world WW stories Leveraging our clinicians as trusted experts in the field Lender Presentation 47

Brand Revitalization Expanding our Authority The Scientific Authority A new slate of initiatives—from medical myth-busting to pioneering studies Focus on the advancement of medication access and health equity Assert our trusted expertise and advocacy Food & Recipe Development Re-activate WW nutritional expertise in social channels WW Clinic Member Advocate Focus on everyday high-protein and high-fiber recipes You're going to reach a point where “ “ Convey modernity, livability, and the potential for scale someone believes you deserve treatment on social media and help in a way that's not stigmatizing.” Earned Media Refocused press and content strategy showing early positive results Top tier placements occurring almost weekly 3.8B press impressions since December ‘24 Lender Presentation 48

Strategic Priorities 1 Deliver a unified unified 2 and engaging Revitalize member our brand and experience 3 reclaimour reclaim Innovate Innovat and 4 leadership expand expandadjacent position Drive revenue streams operational excellence excellence efficiency and efficiency Lender Presentation 49

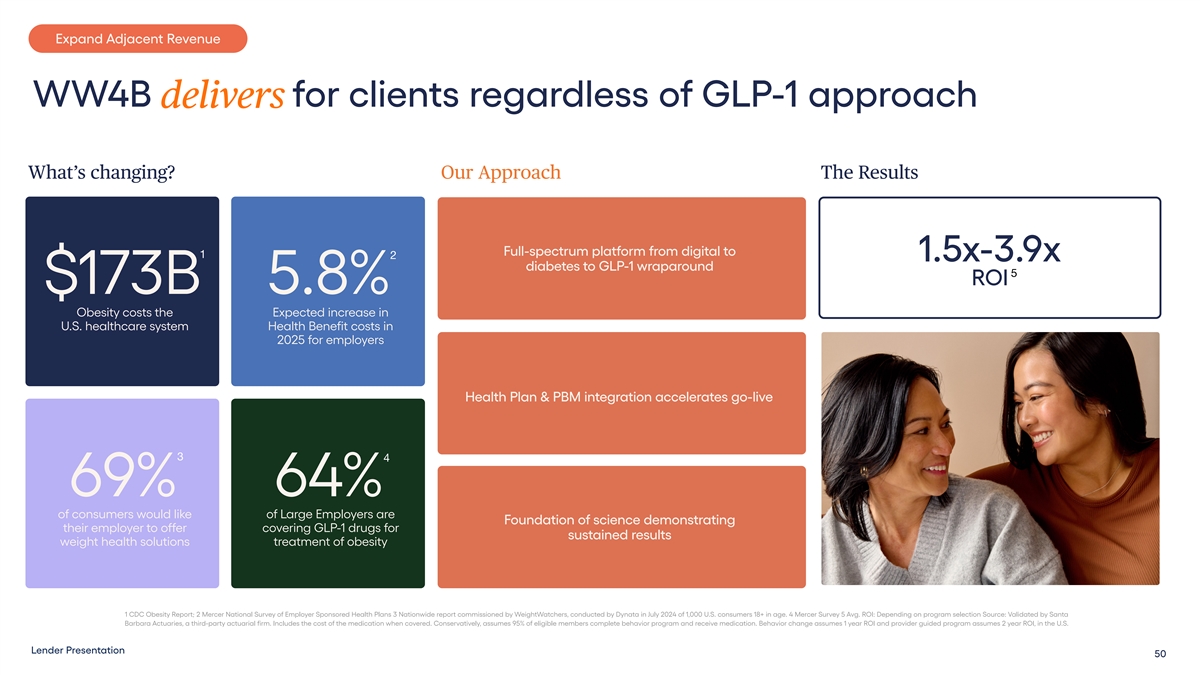

Expand Adjacent Revenue WW4B deliversfor clients regardless of GLP-1 approach delivers What’s changing? Our Approach The Results Full-spectrum platform from digital to 1 2 1.5x-3.9x diabetes to GLP-1 wraparound 5 ROI $173B 5.8% Obesity costs the Expected increase in U.S. healthcare system Health Benefit costs in 2025 for employers 5 Health Plan & PBM integration accelerates go-live 3 4 4 69% 64% of consumers would like of Large Employers are Foundation of science demonstrating their employer to offer covering GLP-1 drugs for sustained results weight health solutions treatment of obesity 1 CDC Obesity Report; 2 Mercer National Survey of Employer Sponsored Health Plans 3 Nationwide report commissioned by WeightWatchers, conducted by Dynata in July 2024 of 1,000 U.S. consumers 18+ in age. 4 Mercer Survey 5 Avg. ROI: Depending on program selection Source: Validated by Santa Barbara Actuaries, a third-party actuarial firm. Includes the cost of the medication when covered. Conservatively, assumes 95% of eligible members complete behavior program and receive medication. Behavior change assumes 1 year ROI and provider guided program assumes 2 year ROI, in the U.S. Lender Presentation 50

Expand Adjacent Revenue Direct to Employer Expanded channel options to unlock accelerating growth 300+ Enterprise clients 6.9M Covered lives Foundational Channels Health Plan PBM Channel Partnership Lender Presentation 51

Expand Adjacent Revenue R Re evit vita aliz lize and gr e and grow our global licensing business Unique legacy as a trusted brand Kickstart licensing rebuild leveraging agency relationships Resource-light approach High margin incremental business Support the needs of our members while enhancing brand value $357B 1 Global Sales of licensed brands 1 Global Licensing Industry Study January 2024 Lender Presentation 52

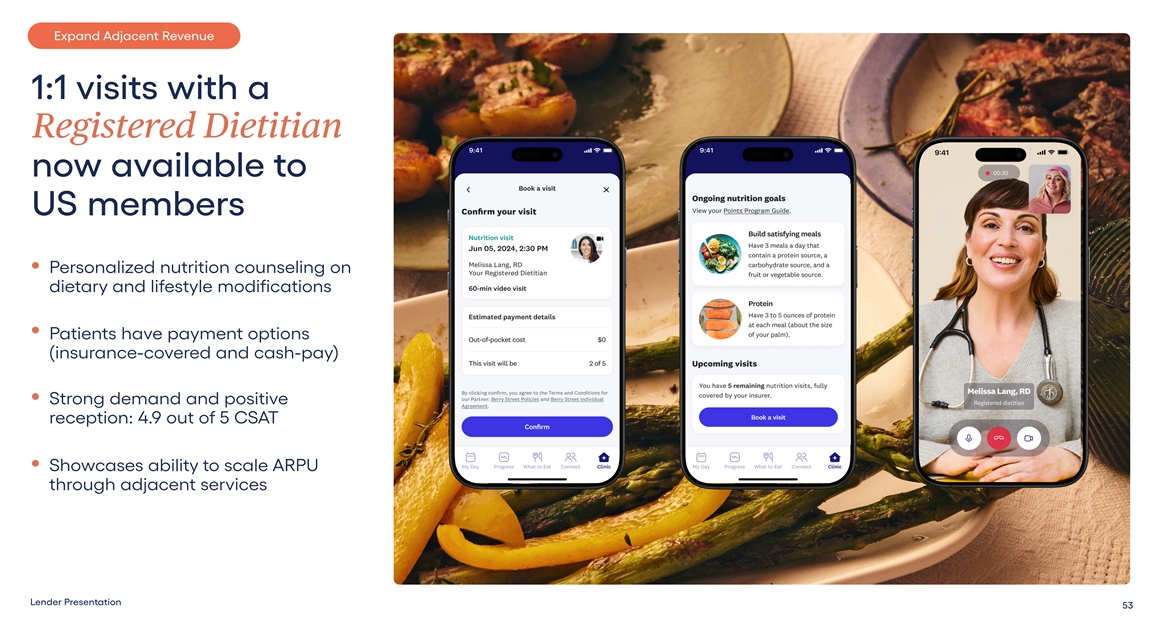

Expand Adjacent Revenue 1:1 visits with a Registered Dietitian now available to US members Personalized nutrition counseling on dietary and lifestyle modifications Patients have payment options (insurance-covered and cash-pay) Strong demand and positive reception: 4.9 out of 5 CSAT Showcases ability to scale ARPU through adjacent services Lender Presentation 53

Strategic Priorities 1 Deliver a unified unified 2 and engaging Revitalize member our brand and experience 3 reclaimour reclaim Innovate Innovat and 4 leadership expand expandadjacent position Drive revenue streams operational excellence excellence efficiency and efficiency Lender Presentation 54

Operational Excellence Complete Weekend Health integration to maximize efficiency, improve member experience and extend LTV Deliver efficiencies through systems, data and team integrations Consolidation of vendors and platforms Build a seamless member experience in a holistic model of care Leverage clinicians and coaches across a more integrated member experience Drive increased engagement and retention through personalized and expanded journeys Le Len nd de er r P Pr re es se en nt ta at tiio on n 55

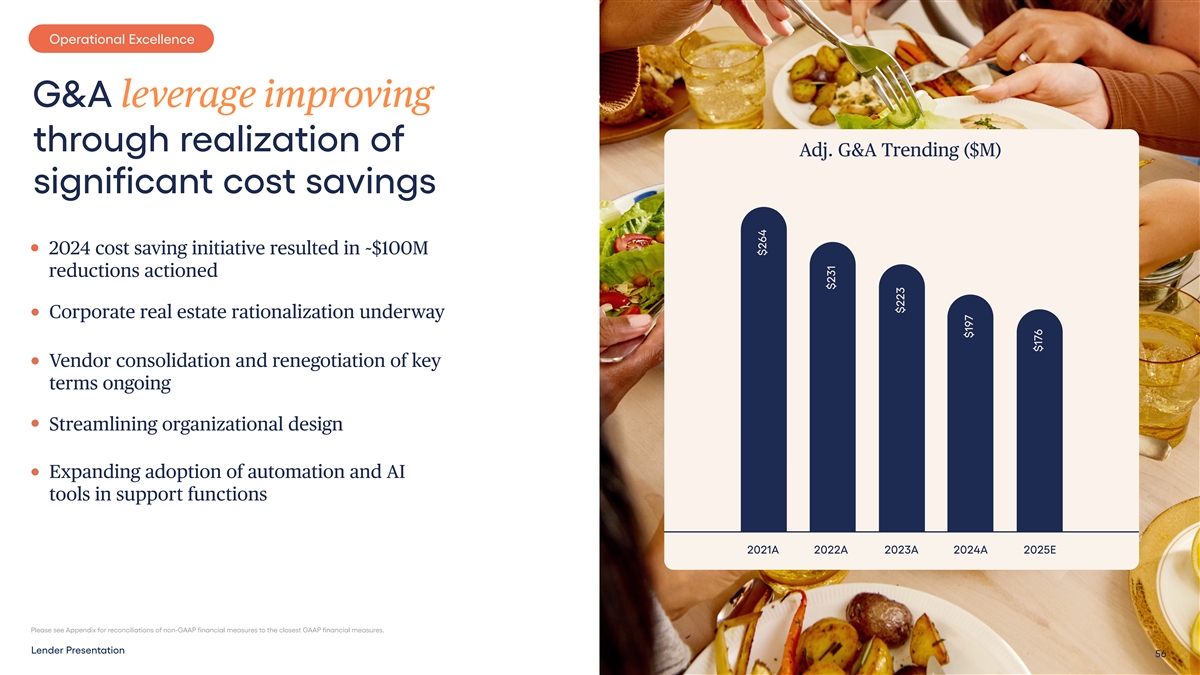

Operational Excellence G&A leverage improving Name for Chart through realization of Adj. G&A Trending ($M) significant cost savings Personalized Member Experience 2024 cost saving initiative resulted in ~$100M reductions actioned Corporate real estate rationalization underway Vendor consolidation and renegotiation of key terms ongoing Streamlining organizational design Expanding adoption of automation and AI Better Outcomes tools in support functions & Success More Data for Personalization 2021A 2022A 2023A 2024A 2025E Please see Appendix for reconciliations of non-GAAP financial measures to the closest GAAP financial measures. Lender Presentation 56 $264 3,798 $231 3,798 $223 3,798 $197 $176

5-Year Forecast 5 Lender Presentation

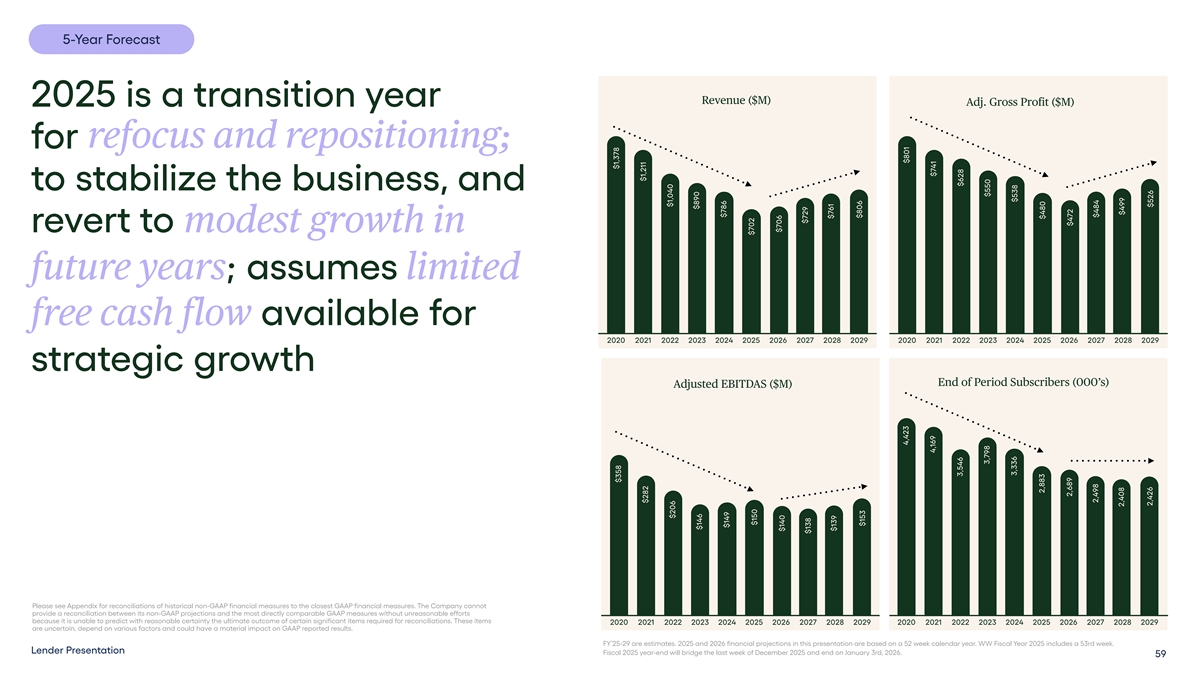

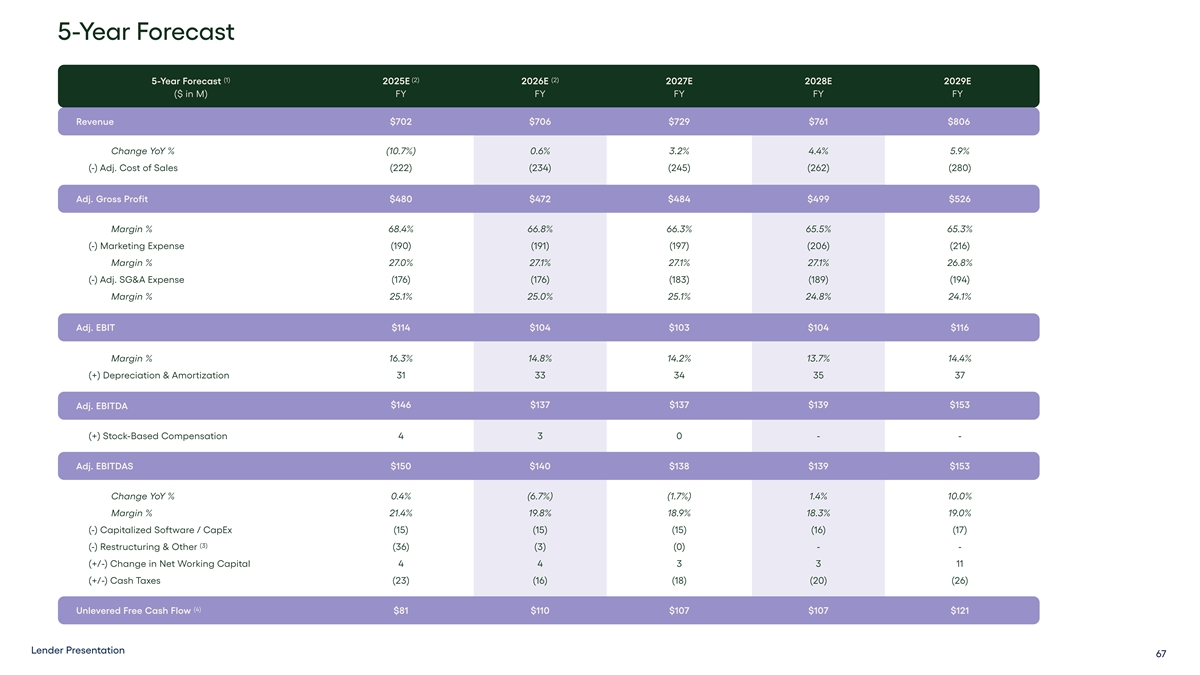

Business Plan reflects the priorities of stabilizing the business and returning to growth Subscribers projected to stabilize in 5-Year Forecast 2028 but revenue trough in 2025 as LTV shifts with Clinic mix 2029 Adjusted EBITDAS is projected to be $153M Lender Presentation 58

5-Year Forecast Revenue ($M) Adj. Gross Profit ($M) 2025 is a transition year refocus and repositioning; for refocus and repositioning; to stabilize the business, and revert to modest growth in future years; assumes limited free cash flow available for 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 strategic growth End of Period Subscribers (000’s) Adjusted EBITDAS ($M) Please see Appendix for reconciliations of historical non-GAAP financial measures to the closest GAAP financial measures. The Company cannot provide a reconciliation between its non-GAAP projections and the most directly comparable GAAP measures without unreasonable efforts because it is unable to predict with reasonable certainty the ultimate outcome of certain significant items required for reconciliations. These items 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 are uncertain, depend on various factors and could have a material impact on GAAP reported results. FY’25-29 are estimates. 2025 and 2026 financial projections in this presentation are based on a 52 week calendar year. WW Fiscal Year 2025 includes a 53rd week. Lender Presentation Fiscal 2025 year-end will bridge the last week of December 2025 and end on January 3rd, 2026. 59 $1,378 $358 3,798 3,798 $1,211 $282 3,798 3,798 $1,040 $206 $890 3,798 $146 3,798 $786 $149 3,798 3,798 $702 $150 $706 3,798 $140 3,798 $729 $138 3,798 3,798 $761 $139 $806 3,798 $153 3,798 4,423 $801 3,798 4,169 $741 3,798 3,546 $628 3,798 $550 3,798 3,336 $538 3,798 2,883 $480 2,689 $472 3,798 2,498 $484 3,798 2,408 $499 2,426 $526 3,798

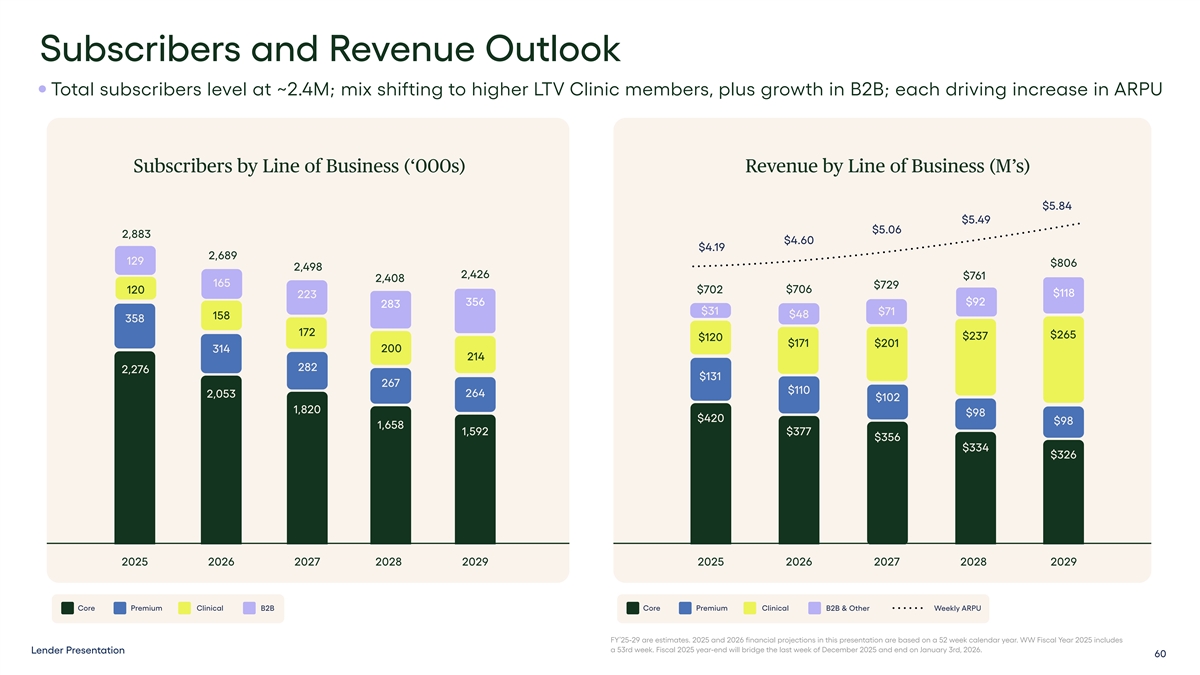

Subscribers and Revenue Outlook Total subscribers level at ~2.4M; mix shifting to higher LTV Clinic members, plus growth in B2B; each driving increase in ARPU Subscribers by Line of Business (‘000s) Revenue by Line of Business (M’s) $5.84 $5.49 $5.06 2,883 $4.60 $4.19 2,689 129 $806 2,498 2,426 $761 2,408 165 $729 $702 $706 120 $118 223 356 $92 283 $31 $71 $48 158 358 172 $265 $237 $120 $171 $201 200 314 214 282 2,276 $131 267 $110 264 2,053 $102 1,820 $98 $420 $98 1,658 1,592 $377 $356 $334 $326 2025 2026 2027 2028 2029 2025 2026 2027 2028 2029 Core Premium Clinical B2B Core Premium Clinical B2B & Other Weekly ARPU FY’25-29 are estimates. 2025 and 2026 financial projections in this presentation are based on a 52 week calendar year. WW Fiscal Year 2025 includes a 53rd week. Fiscal 2025 year-end will bridge the last week of December 2025 and end on January 3rd, 2026. Lender Presentation 60

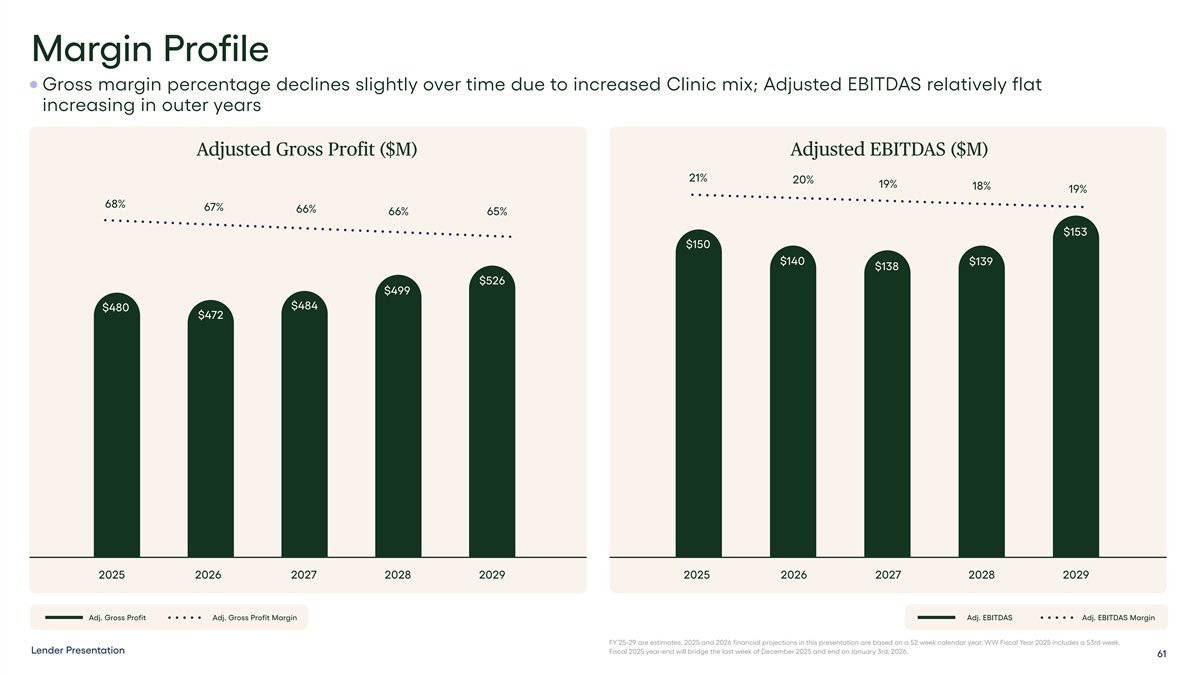

Margin Profile Gross margin percentage declines slightly over time due to increased Clinic mix; Adjusted EBITDAS relatively flat increasing in outer years Adjusted Gross Profit ($M) Adjusted EBITDAS ($M) 21% 20% 19% 18% 19% 68% 67% 66% 66% 65% $153 $150 $140 $139 $138 $138 $526 $499 $484 $480 $472 2025 2026 2027 2028 2029 2025 2026 2027 2028 2029 Adj. Gross Profit Adj. Gross Profit Margin Adj. EBITDAS Adj. EBITDAS Margin FY’25-29 are estimates. 2025 and 2026 financial projections in this presentation are based on a 52 week calendar year. WW Fiscal Year 2025 includes a 53rd week. Lender Presentation Fiscal 2025 year-end will bridge the last week of December 2025 and end on January 3rd, 2026. 61

6 Growth Levers Lender Presentation

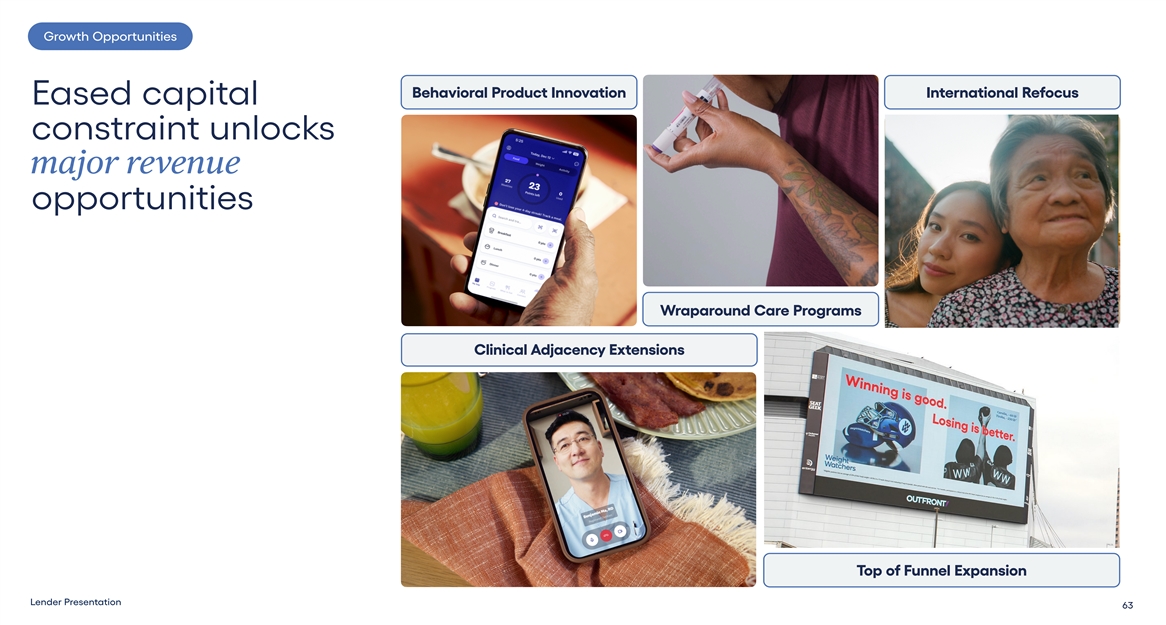

Growth Opportunities Behavioral Product Innovation International Refocus Eased capital constraint unlocks major revenue major revenue opportunities Wraparound Care Programs Clinical Adjacency Extensions Top of Funnel Expansion Lender Presentation 63

Lost 60 lbs You reach a point where “ someone believes you deserve help that is not demeaning or stigmatizing—and they recognize you’re a human being, that you deserve to be happy and healthy.” — WeightWatchers Member Lender Presentation 64

Thank You Lender Presentation

Appendix Lender Presentation

5-Year Forecast (1) (2) (2) 5-Year Forecast 2025E 2026E 2027E 2028E 2029E ($ in M) FY FY FY FY FY Revenue $702 $706 $729 $761 $806 Change YoY % (10.7%) 0.6% 3.2% 4.4% 5.9% (-) Adj. Cost of Sales (222) (234) (245) (262) (280) Adj. Gross Profit $480 $472 $484 $499 $526 Margin % 68.4% 66.8% 66.3% 65.5% 65.3% (-) Marketing Expense (190) (191) (197) (206) (216) Margin % 27.0% 27.1% 27.1% 27.1% 26.8% (-) Adj. SG&A Expense (176) (176) (183) (189) (194) Margin % 25.1% 25.0% 25.1% 24.8% 24.1% Adj. EBIT $114 $104 $103 $104 $116 Margin % 16.3% 14.8% 14.2% 13.7% 14.4% (+) Depreciation & Amortization 31 33 34 35 37 $146 $137 $137 $139 $153 Adj. EBITDA (+) Stock-Based Compensation 4 3 0 - - Adj. EBITDAS $150 $140 $138 $139 $153 Change YoY % 0.4% (6.7%) (1.7%) 1.4% 10.0% Margin % 21.4% 19.8% 18.9% 18.3% 19.0% (-) Capitalized Software / CapEx (15) (15) (15) (16) (17) (3) (-) Restructuring & Other (36) (3) (0) - - (+/-) Change in Net Working Capital 4 4 3 3 11 (+/-) Cash Taxes (23) (16) (18) (20) (26) (4) Unlevered Free Cash Flow $81 $110 $107 $107 $121 Lender Presentation 67

5-Year Forecast Note: Totals may not sum due to rounding. (1) Please see Appendix for reconciliations of historical non-GAAP financial measures to the closest GAAP financial measures. The Company cannot provide a reconciliation between its non-GAAP projections and the most directly comparable GAAP measures without unreasonable efforts because it is unable to predict with reasonable certainty the ultimate outcome of certain significant items required for reconciliations. These items are uncertain, depend on various factors and could have a material impact on GAAP reported results. (2) 2025 and 2026 financial projections in this presentation are based on a 52 week calendar year. WW Fiscal Year 2025 includes a 53rd week. Fiscal 2025 year-end will bridge the last week of December 2025 and end on January 3rd, 2026. (3) Includes Sequence anniversary payment, transaction costs, and restructuring payments. (4) Adjusted EBITDAS as further adjusted for capitalized software / capEx, restructuring & other, change in net working capital and provision for cash taxes. Lender Presentation 68

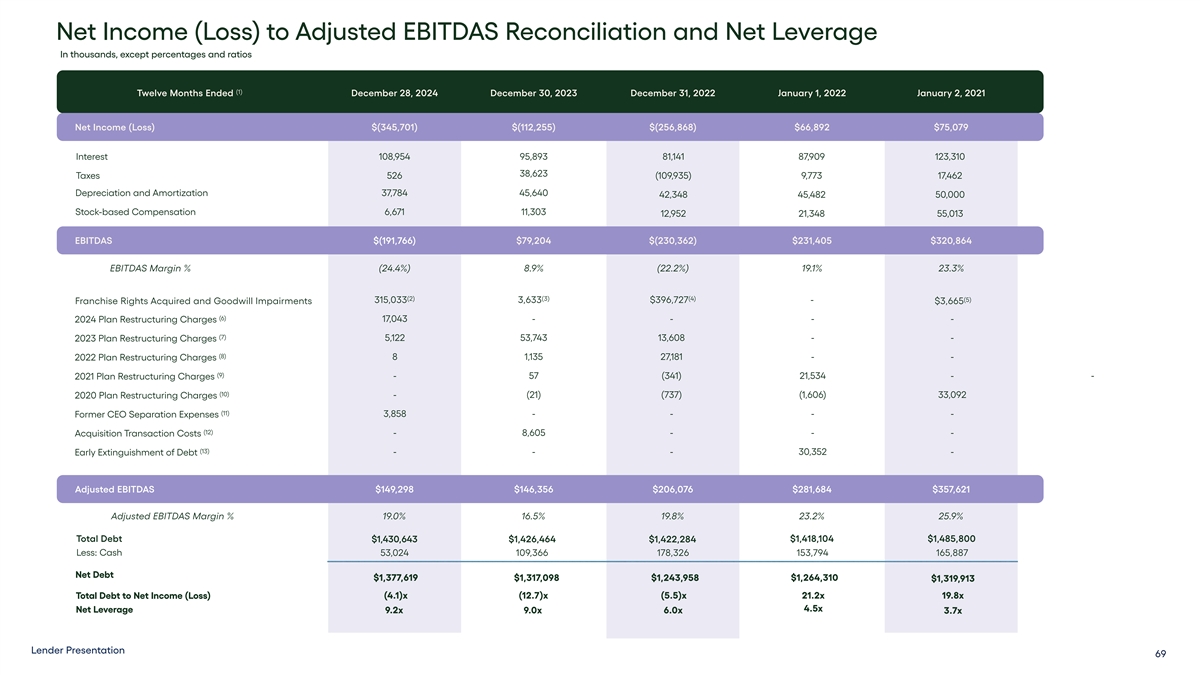

Net Income (Loss) to Adjusted EBITDAS Reconciliation and Net Leverage In thousands, except percentages and ratios (1) Twelve Months Ended December 28, 2024 December 30, 2023 December 31, 2022 January 1, 2022 January 2, 2021 Net Income (Loss) $(345,701) $(112,255) $(256,868) $66,892 $75,079 Interest 108,954 95,893 81,141 87,909 123,310 38,623 Taxes 526 (109,935) 9,773 17,462 Depreciation and Amortization 37,784 45,640 42,348 45,482 50,000 Stock-based Compensation 6,671 11,303 12,952 21,348 55,013 EBITDAS $(191,766) $79,204 $(230,362) $231,405 $320,864 EBITDAS Margin % (24.4%) 8.9% (22.2%) 19.1% 23.3% (2) (3) (4) (5) 315,033 3,633 $396,727 - Franchise Rights Acquired and Goodwill Impairments $3,665 (6) 17,043 - - - - 2024 Plan Restructuring Charges (7) 5,122 53,743 13,608 - - 2023 Plan Restructuring Charges (8) 8 1,135 27,181 - - 2022 Plan Restructuring Charges (9) - 57 (341) 21,534 - - 2021 Plan Restructuring Charges (10) - (21) (737) (1,606) 33,092 2020 Plan Restructuring Charges (11) 3,858 - - - - Former CEO Separation Expenses (12) - 8,605 - - - Acquisition Transaction Costs (13) - - - 30,352 - Early Extinguishment of Debt Adjusted EBITDAS $149,298 $146,356 $206,076 $281,684 $357,621 Adjusted EBITDAS Margin % 19.0% 16.5% 19.8% 23.2% 25.9% Total Debt $1,430,643 $1,426,464 $1,418,104 $1,485,800 $1,422,284 Less: Cash 53,024 109,366 178,326 153,794 165,887 Net Debt $1,377,619 $1,317,098 $1,243,958 $1,264,310 $1,319,913 Total Debt to Net Income (Loss) (4.1)x (12.7)x (5.5)x 21.2x 19.8x 4.5x Net Leverage 9.2x 9.0x 6.0x 3.7x Lender Presentation 69

Net Income (Loss) to Adjusted EBITDAS Reconciliation and Net Leverage In thousands, except percentages and ratios Note: Totals may not sum due to rounding. (1) The Company cannot provide a reconciliation between its non-GAAP projections and the most directly comparable GAAP measures without unreasonable efforts because it is unable to predict with reasonable certainty the ultimate outcome of certain significant items required for reconciliations. These items are uncertain, depend on various factors and could have a material impact on GAAP reported results. (2) Impairment charges of the Company's franchise rights acquired of $305,726, $4,074, $2,905 and $2,328 related to its United States, Australia, United Kingdom and New Zealand units of account, respectively. (3) Impairment charges of the Company's goodwill of $2,383 and $1,203 related to its Republic of Ireland and Northern Ireland reporting units, respectively, and the impairment charge of the Company's franchise rights acquired of $47 related to its Northern Ireland unit of account. (4) Impairment charges of the Company's franchise rights acquired of $324,030, $57,454, $8,275, $1,972 and $1,872 related to its United States, Canada, United Kingdom, New Zealand and Australia units of account, respectively, and impairment charges of the Company's goodwill related to its Republic of Ireland reporting unit and Kurbo operations of $2,023 and $1,101, respectively. (5) Impairment charge of the Company's goodwill related to its Brazil operations. (6) Charges associated with the Company's previously disclosed 2024 restructuring plan. (7) The reversal of charges or charges, as applicable, associated with the Company's previously disclosed 2023 restructuring plan. (8) The reversal of charges or charges, as applicable, associated with the Company's previously disclosed 2022 restructuring plan. (9) The reversal of charges or charges, as applicable, associated with the Company's previously disclosed 2021 restructuring plan. (10) The reversal of charges or charges, as applicable, associated with the Company's previously disclosed 2020 restructuring plan. (11) Certain non-recurring expenses in connection with the separation from the Company of its former Chief Executive Officer. (12) Certain non-recurring transaction costs in connection with the Company's acquisition of Sequence. (13) Charges associated with the Company's previously disclosed April 2021 debt refinancing and voluntary debt prepayments. Lender Presentation 70

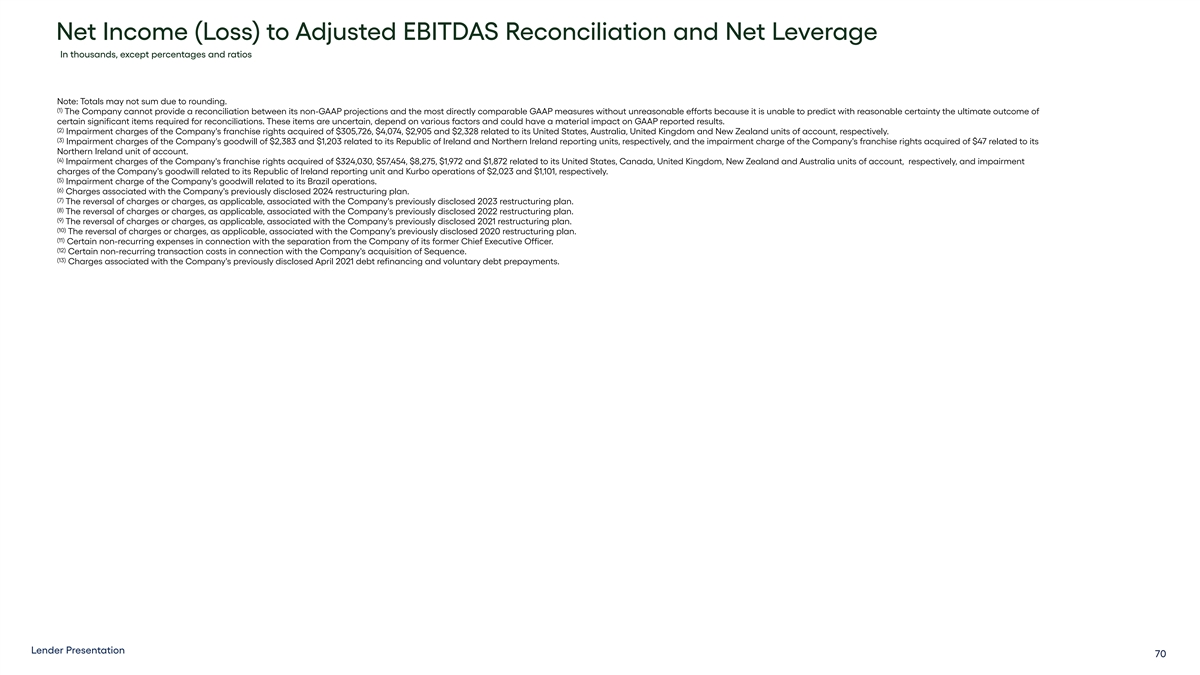

Gross Profit Reconciliation In thousands, except percentages (1) Twelve Months Ended December 28, 2024 December 30, 2023 December 31, 2022 January 1, 2022 January 1, 2021 December 31, 2022 Gross Profit (4) GAAP $533,103 $529,303 $621,379 $726,355 $777,841 Gross Margin % 59.5% 67.8% 59.8% 59.9% 56.4% (2) (3) (5) (6) 5,033 (7) 21,187 15,426 Adjustment 6,981 23,300 (4) $538,136 $550,490 $628,360 $741,782 $801,141 Adjusted Gross Profit Adjusted Gross Margin % 68.5% 61.9% 60.4% 61.2% 58.1% Note: Totals may not sum due to rounding. (1) The Company cannot provide a reconciliation between its non-GAAP projections and the most directly comparable GAAP measures without unreasonable efforts because it is unable to predict with reasonable certainty the ultimate outcome of certain significant items required for reconciliations. These items are uncertain, depend on various factors and could have a material impact on GAAP reported results. (2) Excludes the net impact of $2,497 of charges associated with the Company's previously disclosed 2024 restructuring plan, $2,510 of charges associated with the Company's previously disclosed 2023 restructuring plan and $26 of charges associated with the Company's previously disclosed 2022 restructuring plan. (3) Excludes the net impact of $21,116 of charges associated with the Company's previously disclosed 2023 restructuring plan, the reversal of $4 of charges associated with the Company's previously disclosed 2022 restructuring plan, $96 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan and the reversal of $21 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. (4) Certain amounts have been revised for full year 2022 to correct immaterial misstatements related to certain matters, which is described in the Company's Form 10-K filing for the fiscal year ended December 30, 2023. (5) Excludes the net impact of $1,798 of charges associated with the Company's previously disclosed 2023 restructuring plan, $6,476 of charges associated with the Company's previously disclosed 2022 restructuring plan, the reversal of $564 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan and the reversal of $729 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. (6) Excludes $16,727 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan and the reversal of $1,301 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. (7) Excludes $23,300 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. Lender Presentation 71

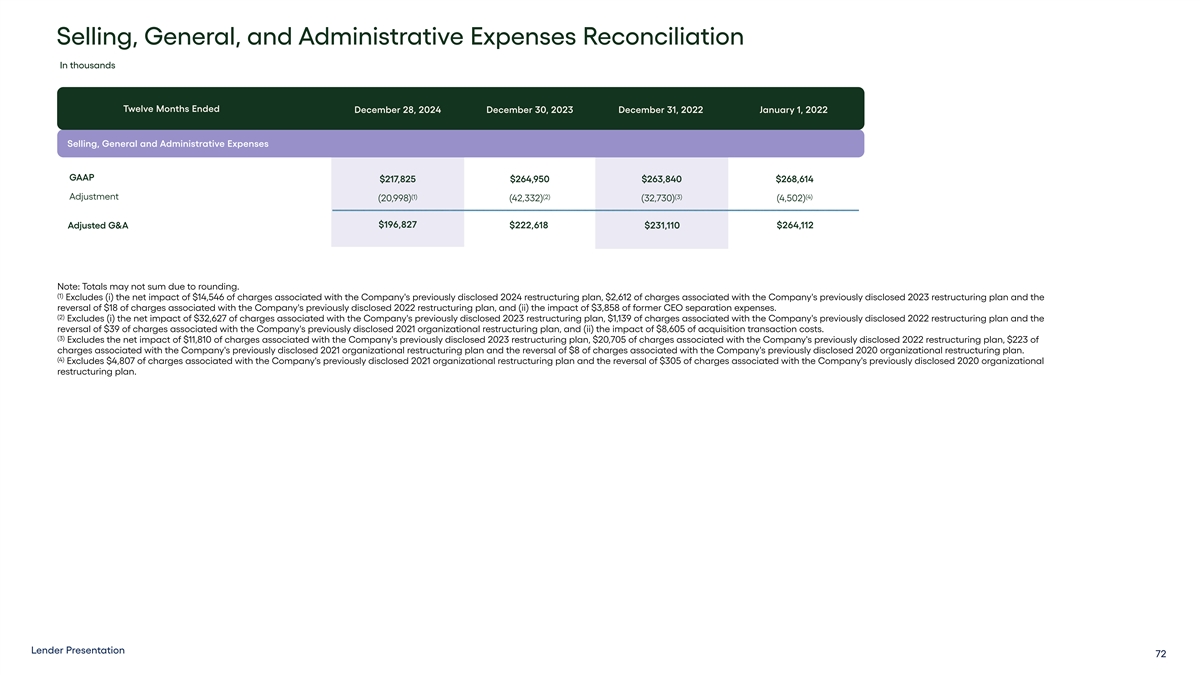

Selling, General, and Administrative Expenses Reconciliation In thousands Twelve Months Ended December 28, 2024 December 30, 2023 December 31, 2022 January 1, 2022 Selling, General and Administrative Expenses GAAP $217,825 $264,950 $263,840 $268,614 (1) (2) (3) (4) Adjustment (20,998) (42,332) (32,730) (4,502) $196,827 Adjusted G&A $222,618 $231,110 $264,112 Note: Totals may not sum due to rounding. (1) Excludes (i) the net impact of $14,546 of charges associated with the Company's previously disclosed 2024 restructuring plan, $2,612 of charges associated with the Company's previously disclosed 2023 restructuring plan and the reversal of $18 of charges associated with the Company's previously disclosed 2022 restructuring plan, and (ii) the impact of $3,858 of former CEO separation expenses. (2) Excludes (i) the net impact of $32,627 of charges associated with the Company's previously disclosed 2023 restructuring plan, $1,139 of charges associated with the Company's previously disclosed 2022 restructuring plan and the reversal of $39 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan, and (ii) the impact of $8,605 of acquisition transaction costs. (3) Excludes the net impact of $11,810 of charges associated with the Company's previously disclosed 2023 restructuring plan, $20,705 of charges associated with the Company's previously disclosed 2022 restructuring plan, $223 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan and the reversal of $8 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. (4) Excludes $4,807 of charges associated with the Company's previously disclosed 2021 organizational restructuring plan and the reversal of $305 of charges associated with the Company's previously disclosed 2020 organizational restructuring plan. Adjusted EBITDA Lender Presentation 72

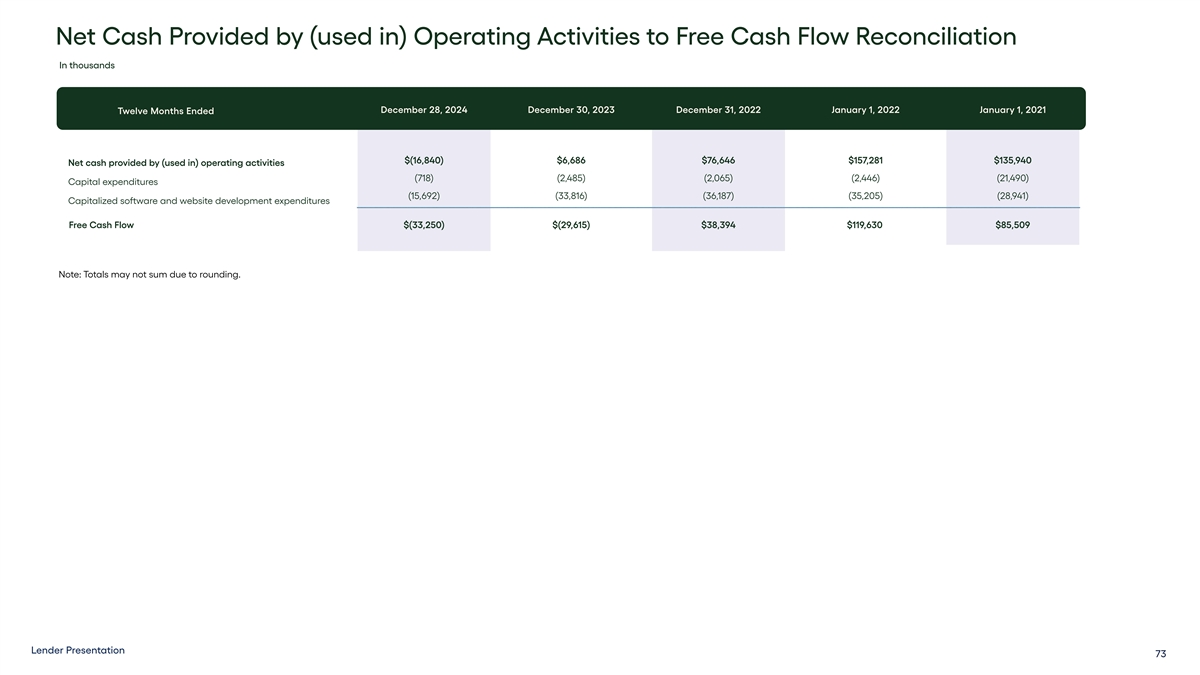

Net Cash Provided by (used in) Operating Activities to Free Cash Flow Reconciliation In thousands December 28, 2024 December 30, 2023 December 31, 2022 January 1, 2022 January 1, 2021 Twelve Months Ended December 31, 2022 Gross Profit $(16,840) $6,686 $76,646 $157,281 $135,940 Net cash provided by (used in) operating activities (718) (2,485) (2,065) (2,446) (21,490) Capital expenditures (15,692) (33,816) (36,187) (35,205) (28,941) Capitalized software and website development expenditures Free Cash Flow $(33,250) $(29,615) $38,394 $119,630 $85,509 Note: Totals may not sum due to rounding. Adjusted EBITDA Lender Presentation 73