Call highlights

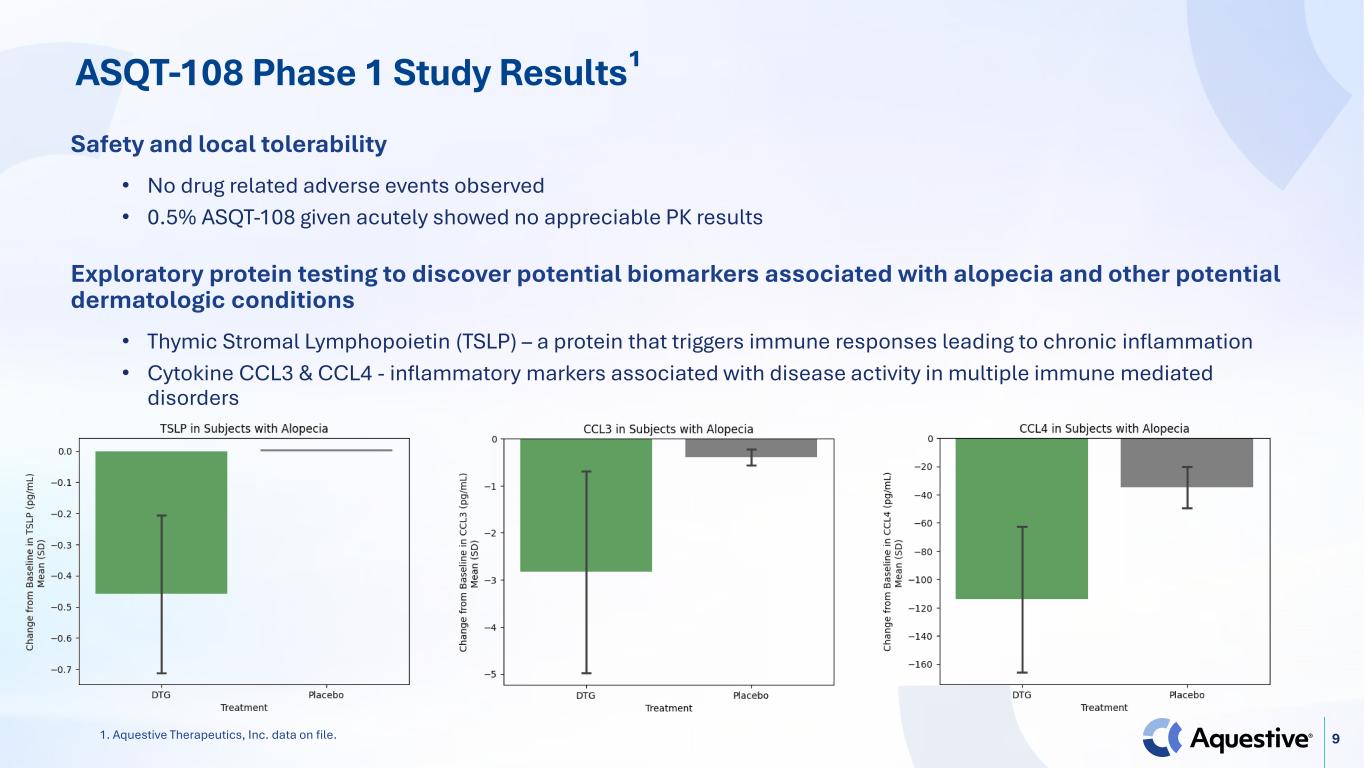

Aquestive Therapeutics reported Q1 2026 results while continuing to advance Anifilm toward a guided Q3 NDA resubmission, supported by a new $150 million Oaktree term loan facility and completed regulatory interactions with the FDA, MHRA, and EMA. The company also reported initial Phase I safety data for AQST-108 in androgenetic alopecia showing no drug-related adverse events and directional TSLP biomarker changes.

“Taken together with our existing cash and the RTW deal, we currently project that we will have greater than $150 million in cash at launch, and this is before considering ex-U.S. Anifilm and U.S. Libervin outlicensing deals.”

“We now know that we can submit applications in the EU, UK, and Canada without conducting further clinical studies. Between the US, Canada, the UK, and the European Union, our product, if approved in each of these regions, could eventually be available to almost one billion people in the next several”

- Closed a $150 million five-year term loan facility with Oaktree, including a $55 million Tranche A funded on May 12, 2026, with improved interest terms and principal payments deferred.

- Projects greater than $150 million in cash at launch when combined with existing cash and RTW funding, before any ex-U.S. Anifilm or Libervant outlicensing deals.

- MHRA confirmed no additional clinical studies are required before submitting an application for Anifilm in the UK.

- Submitted Pediatric Investigational Plan to the EMA, enabling Anifilm applications in the EU, UK, and Canada without further clinical studies.

- Phase I safety study of AQST-108 in men with androgenetic alopecia reported no drug-related adverse events and no appreciable systemic absorption of epinephrine prodrug or epinephrine.

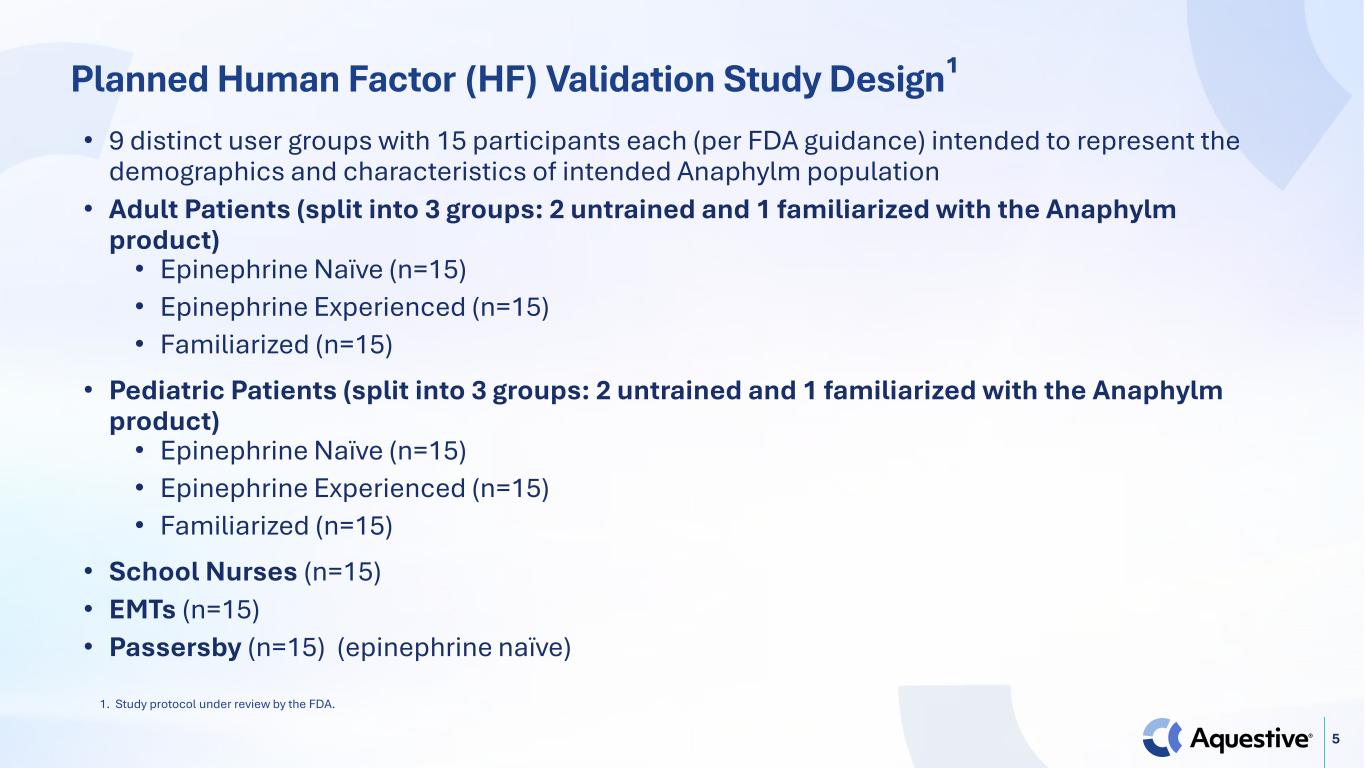

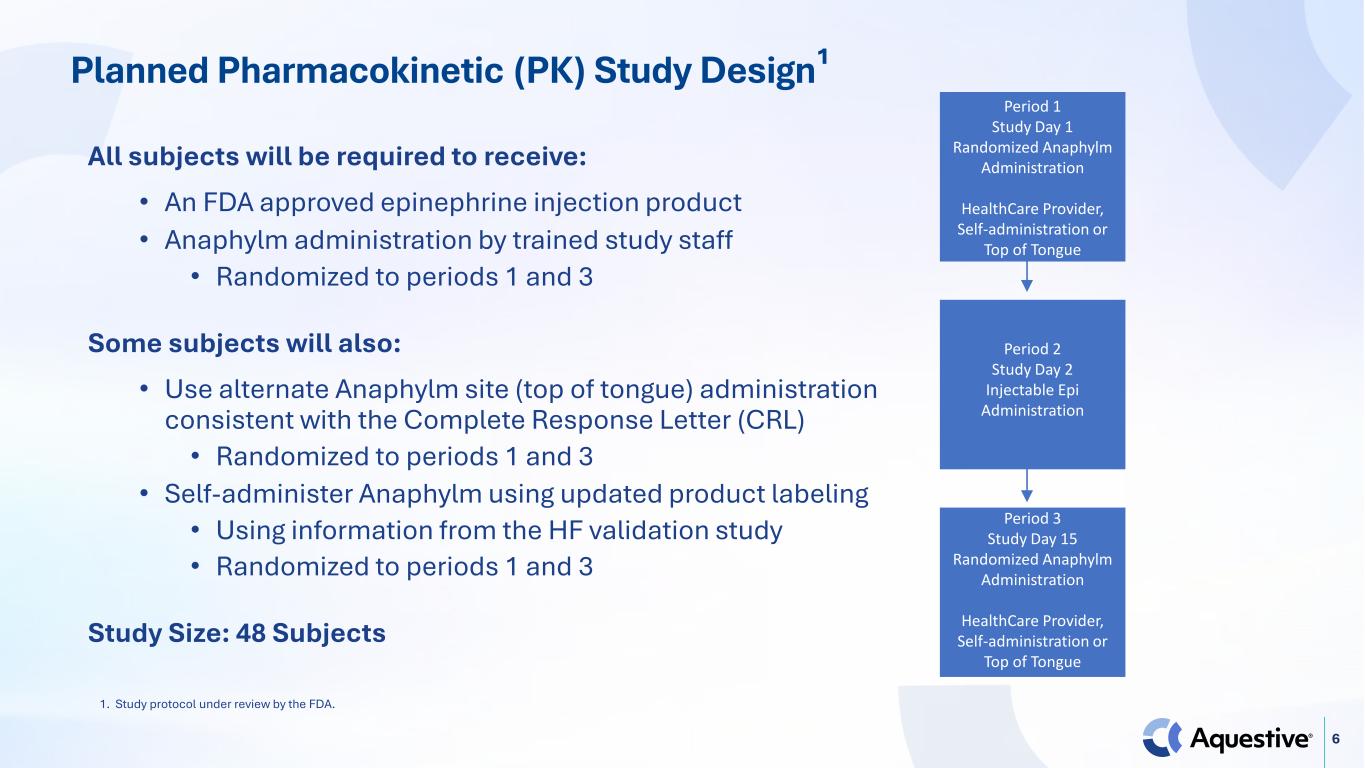

- Expects human factors data and potentially pharmacokinetic data for Anifilm in time for the August earnings call.

- Resubmission timing remains subject to FDA feedback, including scope and content of responses to the human factors protocol.

- Final FDA review classification (Type 2, six-month review) and any expedited review are solely at the FDA's discretion and cannot be guaranteed.

- Tranche B ($20M) availability is conditioned on FDA approval of Anifilm by June 30, 2027; Tranche C ($25M) is conditioned on a net sales milestone by December 31, 2027.

- Term Loan carries interest of three-month SOFR (with a 2.75% floor) plus 6.25%, with an Exit Fee of 1.00%–2.00% on repayments and a make-whole/yield protection premium on prepayments.

- Company must maintain minimum unrestricted cash of $27.5 million (pre-Tranche B) and $15 million (post-Tranche B), and is subject to a Minimum Net Sales Covenant after Tranche B funding.

- AQST-108 TSLP biomarker findings are directional, not statistically powered, and the company described the Phase I data as very early.

Good day and thank you for standing by. Welcome to the first quarter 2026 Equest of Therapeutics earnings conference call. At this time, all participants are in a listen-only mode. After the speaker's presentation, we'll open up for questions. To ask a question during a session, you will need to press star one one on your telephone. You then hear an automated message advising your hand is raised. To withdraw your question, please press star one one again. Please be advised that today's call is being recorded. I want to hand it over to our first speaker, Faith Pomeroy Ward. Please go ahead.

Thank you, Operator. Good morning and welcome to today's call. On today's call, I'm joined by Dan Barber, Chief Executive Officer, and Ernie Toth, Chief Financial Officer, who are going to provide an overview of the company's reported financial results for the first quarter ended March 31st, 2026, and a progress update on the company's key 2026 objectives, followed by a Q&A session. During the Q&A session, the team will be joined by Dr. Matt Greenhaut, Chief Medical Officer, Melina Chaffee, Senior Vice President, Regulatory Affairs, Sherry Korchinski, Chief Commercial Officer, and Dr. Matthew Davis, Chief Development Officer. As a reminder, the company's remarks today correspond with the earnings release that was issued after market close yesterday. In addition, a recording of today's call and related supplemental materials will be made available on Equestive's website within the Investors section shortly following the conclusion of this call. To remind you, the Equestive team will be discussing some non-GAAP financial measures this morning as part of its review of first quarter 2026 results. A description of these measures, along with the reconciliation to GAAP, can be found in the earnings release issued yesterday, which is posted on the Investor's section of Equestib's website. During the call, the company will be making forward-looking statements. We remind you of the company's safe harbor language as outlined in today's earnings release, as well as the risks and uncertainties affecting the company as described in the risk factor section and in other sections included in the company's annual report on Form 10-K filed with the U.S. Securities and Exchange Commission on March 4, 2026. As with any pharmaceutical company with product candidates under development and products being commercialized, there are significant risks and uncertainties with respect to the company's business and the development, regulatory approval, and commercialization of its products and other matters related to operations. Given these uncertainties, you should not place undue reliance on these forward-looking statements, which speak only as of the date made. Actual results may differ materially from these statements. All forward-looking statements attributable to a Questive or any person acting on its behalf are expressly qualified in their entirety by this cautionary statement and the cautionary statements contained in the earnings release issued yesterday. The company assumes no obligation to update its forward-looking statements after the date of this conference call whether as a result of new information future events or otherwise except as required under applicable law now i would like to turn the call over to dan

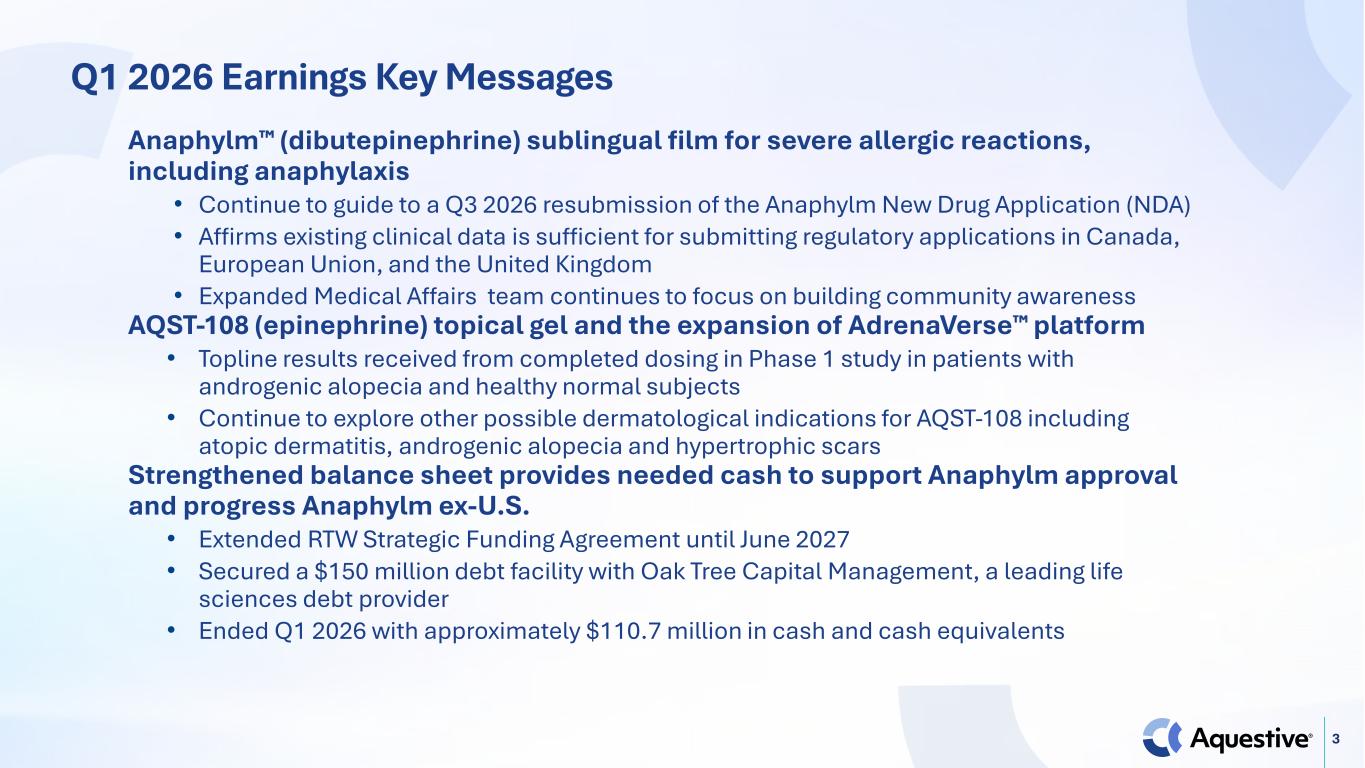

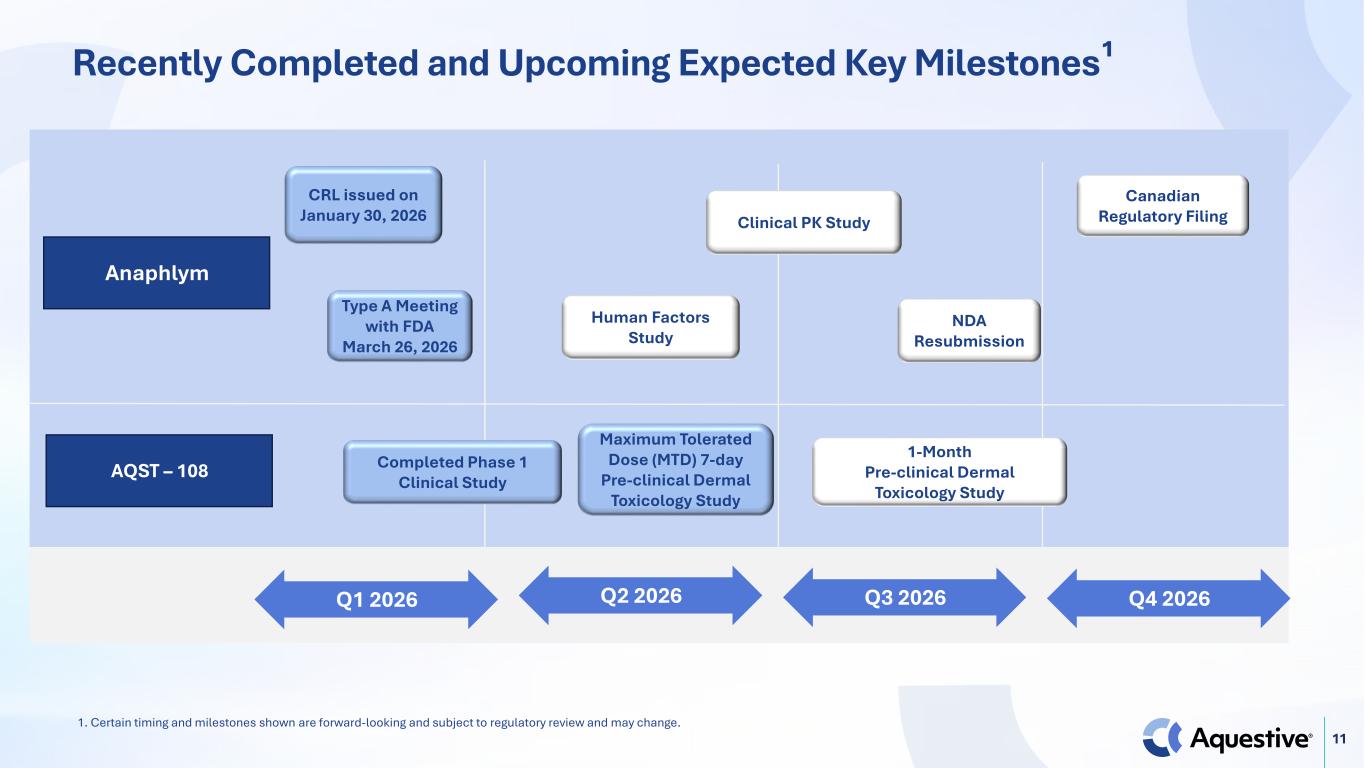

good morning and thank you for joining us today in the last 62 days since our earnings call we have progressed the company significantly for anisome dibute epinephrine sublingual film We have completed our Type A face-to-face meeting with the FDA, completed a teleconference with the UK regulatory body known as MHRA, submitted our pediatric investigational plan to the European Medicines Agency, and submitted our human factors protocol for review by the In addition, we have closed on a new debt facility with a leading life sciences debt provider and completed our Phase I safety study in humans for our pipeline program AQST-108. We are also on track to attend over 40 conferences and submit over 20 publications this year. It is a testament to the Equestive team that they were able to complete so much important work in such a brief period of time. The question, of course, is where does this work take us and how do we expect the coming months to unfold? Today, I am providing guidance that we currently expect to have our human factors data and potentially our pharmacokinetic data for Anifilm available in time for our August earnings call. Now, the completion of this data is dependent on the FDA providing responses to our human factors protocol on time and the responses being within expectations, including with respect to the scope and content of that feedback. With these assumptions in mind, we continue to guide to a third quarter resubmission to the FDA, recognizing this timing remains subject to FDA feedback and ongoing review processes. As we've stated in the past, we currently expect our resubmission of the NDA for Anafilm to be classified as a type 2 submission with a six-month review, although final classification is determined by the FDA. We will request an expedited review upon our submission and will do everything we can to communicate with the FDA and support their review process, recognizing that any decision on review timing rests solely with the FDA. We believe the comments by FDA's leadership on the need for the agency to provide more timely feedback and review points to a broader agency focus, and in this case, may create the possibility of aligning with the FDA on a faster process. This, of course, cannot be guaranteed. Our commercial preparations continue to progress. Importantly, we were pleased to enter into a $150 million debt facility with Oaktree, a leading life sciences debt provider. While Ernie will talk about this in more detail, at a global level, this agreement unlocks several important things for Equestive. One, we have improved the interest rate terms on our existing debt, and principal payments will not begin for several years. Two, this completes the pre-approval requirements for the RTW funding, and three, we have the ability to access $20 million in additional capital if Anafilm is approved by the FDA. Taken together with our existing cash and the RTW deal, we currently project that we will have greater than $150 million in cash at launch, and this is before considering ex-U.S. Anifilm and U.S. Libervin outlicensing deals. We plan on using this cache to focus on building intense awareness and access within the allergy community for Anifilm. We have already shared our plans for launch of Anifilm with you, if approved by the FDA, including a strong medical affairs presence, a 75-person sales force, and a focused marketing effort. We have also been watching and learning from the launch of a nasal spray product in the market. Our research within the allergy community indicate that building clarity, trust, and support for allergists is key to unlocking prescriptions. This may seem obvious, but just think of the daily pressures allergists face in running their practices. Fitting into their world in a meaningful and credible way in furtherance of patient access to Anifilm is task number one, two, and three for us. While the U.S. market is incredibly important to us, we can't forget that 96% of the world's population does not live in the U.S. I truly believe Anifilm is a product that will save lives, and we want as many people as possible on this planet to ultimately have access to it. Our lead ex-US strategy continues to be Canada and Europe, and we've made significant progress. As I mentioned before, we recently completed a comprehensive and positive interaction with MHRA, the UK's regulatory body. I'm pleased to say we received confirmation that we do not need to conduct additional studies before submitting our application to MHRA in the UK. We also recently submitted our Pediatric Investigational Plan to the European Medicines Agency, or EMA, for the European Union. Aligning with EMA on this plan is essential to submitting our application. We now know that we can submit applications in the EU, UK, and Canada without conducting further clinical studies. Between the US, Canada, the UK, and the European Union, our product, if approved in each of these regions, could eventually be available to almost one billion people in the next several Now, let's talk about our product pipeline. Given the excitement around Anifilm, people often forget that we are utilizing our epinephrine prodrug platform, Adrenoverse, to advance treatment in other indications. Our lead asset is AQST-108, and we recently completed a Phase I safety study in men with androgenic areata. I am pleased to say that there were no drug-related adverse events observed in the study, and we also saw no appreciable signs of systemic absorption of our epinephrine prodrug or of epinephrine itself. We did, however, see something intriguing. Now, keep in mind, this is very early Phase I study data. Our Chief Development Officer, Dr. Matthew Davis, added biomarker assays to the study to see if we could detect changes in key proteins associated with both alopecia areata and androgenic areata, along with other dermatological conditions such as atopic dermatitis. While this information is not statistically powered and should be viewed as directional only, we were pleased to see in subjects with alopecia that the cytokine TSLP appeared to be impacted by AQST-108. This was not the case when subjects were given placebo. This is very exciting as the signaling pathway for TSLP involves the activation of JAK1 and of JAK2. We have included preliminary data on this work in our supplemental material available under the presentations section of the investor page on our website. We will talk more about the next studies for AQST 108 in the coming months once we have resubmitted our Anifilm application in the U.S. Our business development efforts and base business continue to move forward. Our business development team is currently in active negotiations on multiple programs for Europe, the U.S., and South America. We have also had outreach from additional regions of the world, including China and Australia. We are prioritizing this work based on the territory and program involved. We expect to have more to say on this topic in the months to come. In summary, we expect to provide a significant data update in August, assuming the FDA keeps to its review timeline and provides constructive comments to our human factor study protocol. We continue to drive awareness in the epilepsy community ahead of a potential product launch of anafilm if approved by the FDA. Our international filing efforts continue to be a priority, and our AQSC 108 program continues to show promise for expansion into potential multiple indications. With that, I will turn the call over to Ernie.

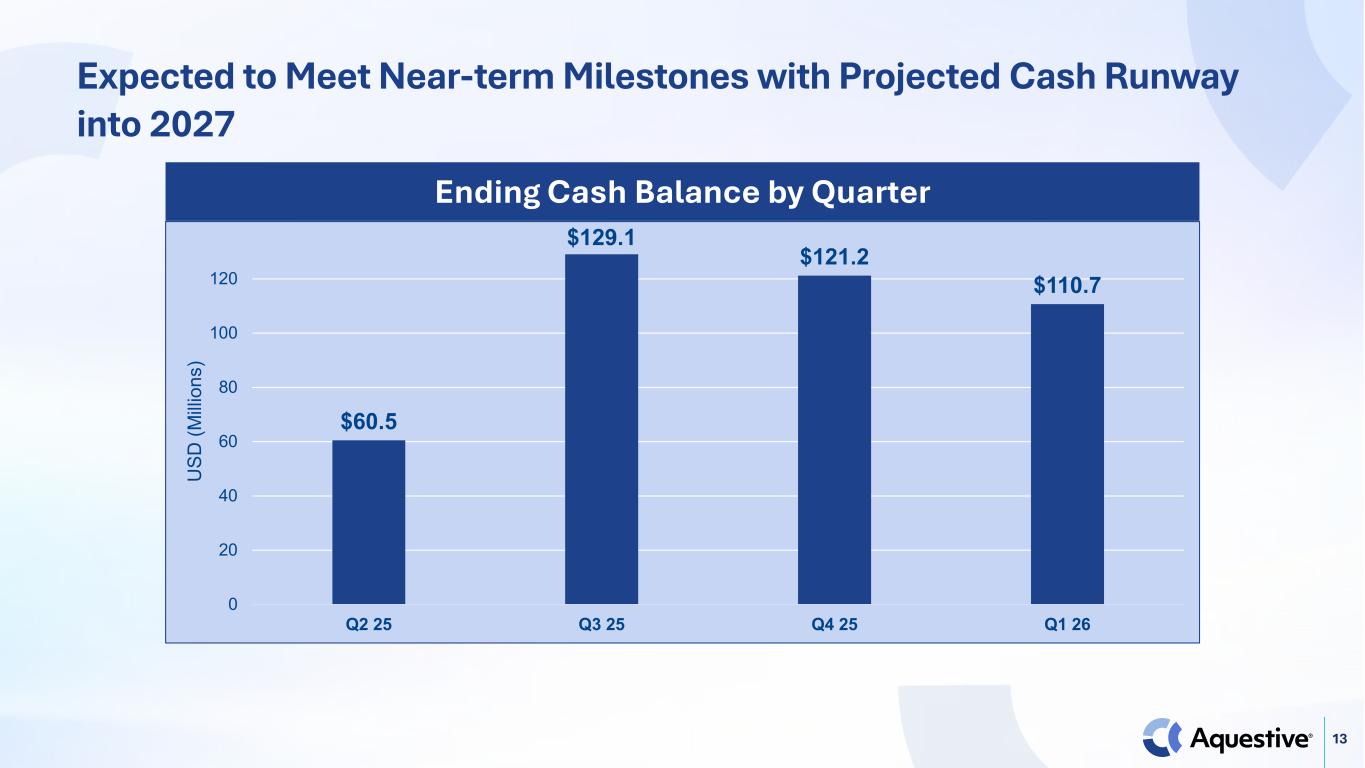

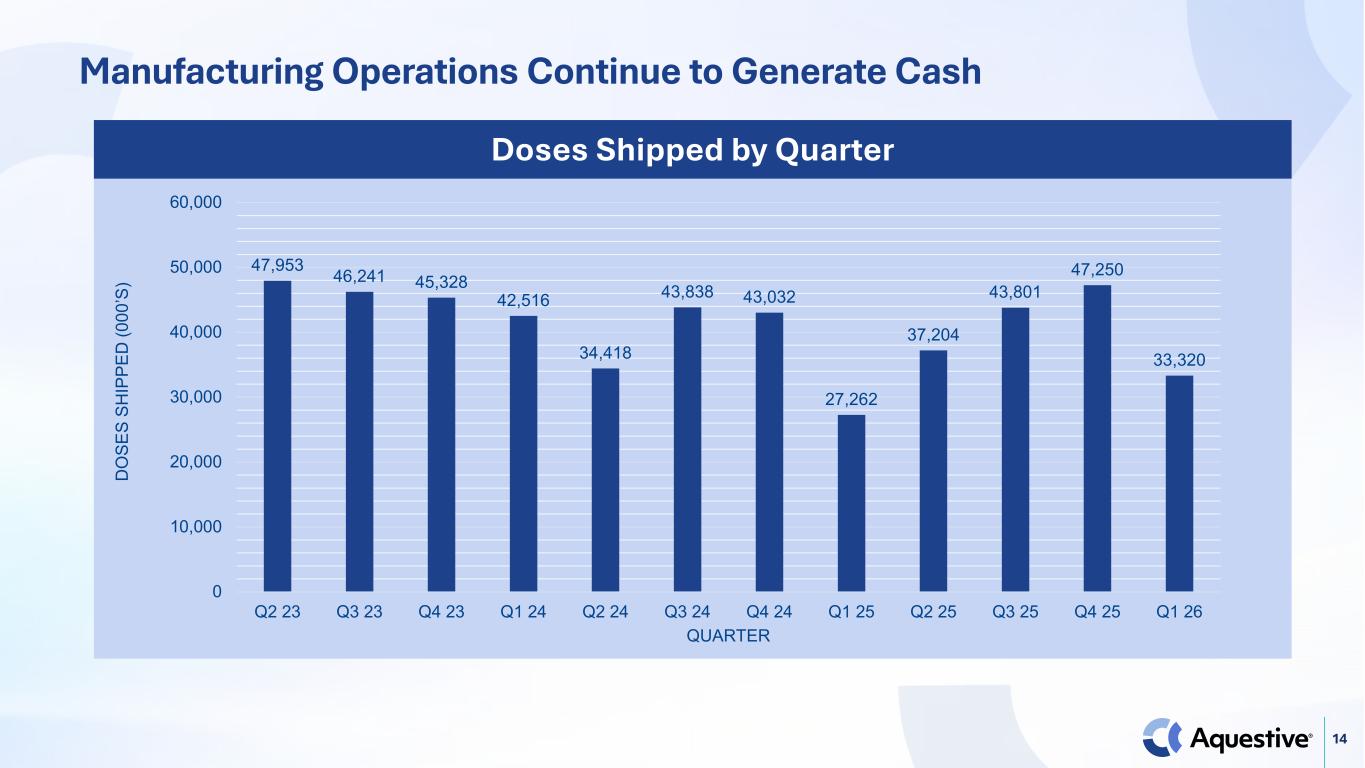

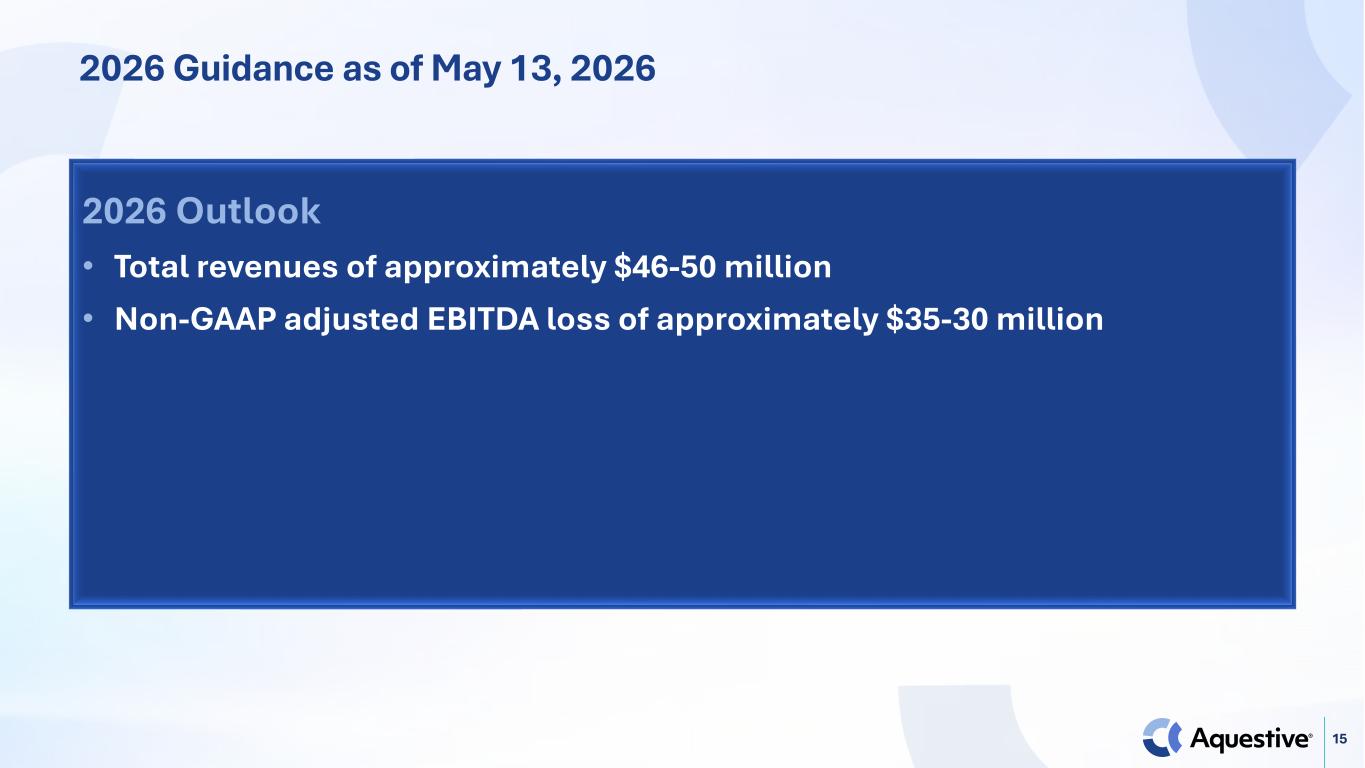

Thank you, Dan, and good morning, everyone. By now, you will have seen our first quarter 2026 financial results in the earnings release issued last evening and detailed in our Form 10Q filing. As we typically do, we will address most of the detailed discussion regarding the quarter during Q&A, and I will focus my remarks on financial performance, operating spend, and liquidity. During the first quarter, our primary financial focus remained supporting progress on Anafilm following receipt of the FDA complete response letter on January 30th, 2026, while maintaining a strong balance sheet and financial flexibility. Subsequent to quarter N, we completed a type A meeting with the FDA and aligned on the remaining requirements for approval, including a human factors validation study and a PK study, both of which are currently underway. During the quarter, we extended our strategic funding agreement with RTW Investments through June 30th, 2027, further strengthening our liquidity runway financial flexibility as we work towards anafilm resubmission additionally we announced the refinancing of our existing debt with a new 150 million dollar debt facility with certain funds and accounts managed by oak tree capital management this transaction reduces our interest rate extends the interest only period saving 45 million dollars in principal payments over the next three years on the existing debt that were scheduled to commence on June 30th, and provides additional flexibility to fund the launch of Anifilm if approved by the FDA. The new debt facility is available in four tranches, with tranche A of $55 million refinancing the existing debt, tranche B of $20 million available upon FDA approval of Anifilm, tranche C of $25 million, available upon achieving certain sales levels, and tranche D of $50 million, available upon mutual consent of Oaktree and the company. Now, let me walk you through our first quarter results. Total revenues increased to $14.4 million in the first quarter of 2026 from $8.7 million in the first quarter of 2025. The 66% increase was primarily driven by increases in license and royalty revenue and increases in manufacturer and supply revenue. License and royalty revenue increased to $5.4 million in the first quarter of 2026 from $0.8 million in the first quarter of 2025, primarily due to the recognition of royalty revenue from Zebra. manufacturer and supply revenue increased to $8.8 million in the first quarter of 2026 from $7.2 million in the first quarter of 2025, primarily due to increases in suboxone revenues partially offset by lower on-deaf revenues. Research and development expenses decreased to $4.2 million in the first quarter of 2026 from $5.4 million in the first quarter of 2025. The decrease in research and development expenses was primarily due to lower clinical trial costs associated with the anafilm development program, partially offset by increases in R&D personnel costs. Selling general and administrative expenses decreased to $11 million in the first quarter of 2026 from $19.1 million in the first quarter of 2025. The decrease primarily represents the one-time NFL PDUFA fee of $4.3 million in the prior year period, lower legal fees of approximately $3.4 million, lower commercial spending of approximately $2 million, and lower regulatory and licensing fees of approximately $0.5 million, partially offset by higher severance costs of approximately $0.6 million, higher personnel costs of approximately 0.5 million dollars and higher share-based compensation expenses of approximately 0.5 million dollars. Equesta's net loss for the first quarter 2026 was 8.1 million dollars or 7 cents for both basic and diluted loss per share compared to the net loss in the first quarter 2025 of 22.9 million dollars or 24 cents for both basic and diluted loss per share. The decrease in net loss was primarily driven by increases in revenues, decreases in selling general administrative expenses, and research and development expenses, partially offset by decreases in interest income and other income net. Non-GAAP adjusted EBITDA loss was $1.7 million in the first quarter of 2026, compared to non-GAAP adjusted EBITDA loss of $17.6 million dollars in the first quarter of 2025. Turning to the balance sheet, we ended the first quarter of 2026 with approximately $110 million in cash and cash equivalents. This cash position provides us with sufficient capital to complete the remaining FDA-required studies for anafilm, continue advancing AQST-108 and our Adrenoverse platform, and support ongoing operations and regulatory planning, including potential ex-U.S. regulatory filing, and preparing for the U.S. commercial launch of Anafilm if approved by the FDA. At this time, we are not updating full-year financial guidance, as our near-term focus remains on execution of the remaining antifilm study requirements and achieving regulatory milestones. We expect to provide additional financial and operational updates as those milestones are reached. For 2026, the company expects total revenue of $46 million to $50 million and non-GAAP adjusted EBITDA loss of $35 million to $30 million as of May 13, 2026. In summary, the first quarter of 2026 reflects disciplined financial execution, a strong cash position, and continued focus on advancing Anafilm towards resubmission while carefully managing expenses across the organization. With that, I will now turn the line back to the operator to open

the line for questions. Thank you. As a reminder to ask a question, you need to press star one one on your telephone and wait for your name to be announced. To withdraw your question, please press star one one again. Please stand by while we compile the Q&A roster. One moment for our first question. Our first question will come from the line of Rhonda Reese from

Lyric Partners. Your line is open. Great. Good morning, everyone. So a couple from me. First on Anatham, can you give us a little bit more detail on how things are going preparing for the U.S. filing and ongoing study interactions or activities? It sounds like you reiterated your timeline. What gives you added conviction to be able to hit that milestone? To think about this

standing by ready to timing of when we, the only trigger that we are waiting for, the FDA

commitment from the FDA. Sounds good. And I wanted to ask a question about AQST 108 as well. The biomarker data sounds interesting. Can you help frame that? How does that compare to other programs you've seen going after similar indications, even if they're different mechanism agents? Like, how should we think about this early signal?

And I'll let Matthew Davis take that one.

Hi, Mona. Think about TSLP. What's intriguing about this signal is the fact that, one, it crosses across Th1, Th2-driven inflammation, JAKSAT1, JAKSAT2. So when you think of dermatology, you would think of mechanisms that would be beneficial for alopecia areata, androgenic alopecia, atopic derm, and there's a lot of optionality that this gives us. The fact that We also saw the correct orientation with CCL-3 and CCL-4 would be confirmational, remember this is directional only data, that we're looking at the right things right now. So this gives 108 topical a lot of optionality in the dermatologic space. Sounds great.

Thanks.

Next question will come from the line of Kirsten Kluska from Canter, your line is open.

Hi, good morning, everybody, and congrats on all of the progress. So I wanted to ask how your market research and conversations have been going about coverage and reimbursement. I think there's been a lot of great work to support. The enthusiasm is there, but assuming you get an approval, what gives you confidence that you will get the coverage that the patients that want ANIFM will be able to get their hands on it?

Sure. Good morning, Kristen. And look, I think I hopefully have been...

Thanks, Dan. Hi, Kristen. Good morning. You know, as we've been talking about, ensuring as many patients have access to anafilm is our number one priority. And rapid payer coverage and reducing the friction at our HCP's office is key. As Dan mentioned, we have watched and learned from the recent nasal launch. We see what has worked, what hasn't worked. We're adjusting our strategy. accordingly. And we continue to have very robust discussions with the PBMs and the payers. From the research and from our one-on-one meetings, there is significant interest in our product. But as Dan has mentioned, it's going to take some time. But what I can assure you with, Kristen, is we are setting up a best-in-class hub and patient support services. We are investing heavily into ensuring that there is as little friction, even with those prior offs, that there's as little friction and pain for our physicians' offices. That's the one thing we've learned, and so we've taken our learnings and we're applying them to how and what we will do. And so at the end of the day, we are very, very invested in ensuring that both patients and HCPs are aware of anafilm and then are prepared to prescribe anafilm and ultimately that our

patient gets their anafilm prescription. Okay, thank you. And then just on that awareness angle, what do you think is going to be the biggest push that you're going to have to do in terms of getting the word out there? And how would you say potentially having this extra time since the CRL and your original planning has benefited that.

When it comes to awareness, I'm incredibly pleased with where, in my view, our weight is second, but a lot of that is because of his efforts in the field. This year we'll be at 40 conferences and have 20 publications, and that is extensive.

Hope everybody's doing well. I mean, we've been busy. We've gone to, what, 13 conferences to date. We're going to hit over 40, ideally. Writing papers is a lot of data. There's a great story to tell here. And, you know, I'm doing my best to get this out. Reassuring it to really get out and meet everybody. And, again, these are shared. Thanks, everyone.

Thank you. And our next question comes from David Amselim from Piper Sandler. Your line is open.

Hi, everyone. This is now John for David. Thanks for taking our questions. Just a couple quick ones from us. of us. So first with Nessie, now that that's been on the market for around 18 months, can you elaborate on the learnings from that launch that are influencing any changes to your commercialization strategy? That's number one. And number two, with the Oak Tree financing in place and the pre-approval conditions for the additional RTW financing net, is that sufficient runway through the launch of and a film, so if you can provide some clarification there, that would be great.

Sure. Well, let me go in reverse order, and let's start with Oaktree, and I'm going to pass it

over to Irv a minute here, and now, well, you mentioned with the refinancing.

Thanks so much, and thanks so much for the question.

And, you know, look, as you know, having a non-device, oral, easiest to carry epinephrine, it is a game changer in the marketplace. But again, as Dan mentioned, no matter, you know, you build a better mousetrap, that doesn't necessarily mean it will come. And we've seen this in this marketplace. As you know, I ran the EpiPen brand. And we saw the same thing happen with AviQ. So just because you build a better mousetrap doesn't mean that everyone will come. So what have we learned? I think one is how do we reduce that friction? And so as I just mentioned to Kristen, we are really working hard in our very robust discussions with the PBMs and payers, but also working on setting up the best-in-class hub and support services to support the offices. I think we heard from ARS back in their March earnings call is that they were kind of doubling down in the allergist space, increasing reach and frequency in the allergist. We know that this market is driven by the allergist and the high prescribing pediatricians. Our plan, as you know, we've moved to 75 reps as well as then obviously the managers and the support around that is critical to drive the product forward. And so, look, I think at the end of the day, reducing friction in the physician's office is critical, ensuring that physicians and patients have awareness, and really driving believability in the product. So Matt's team is out there doing a fantastic job. I mean, our market research shows the awareness with the HCPs has gone from a 33% to 66%. So the increased effort in publications and all the medical work that is being done will only continue to do that. But that only gets us so far, right? With the awareness, we have to have doctors believe in it. So all of the scientific work Matt and his team are doing, the publications we will continue to put out are critically important. And then physicians have to get experience with the product in their office. And so, you know, we will look to launch a program upon approval so physicians can get that actual real-world experience. Does that answer your question, David?

It does. Thanks. Thank you. And our next question comes from the line of Francois Brisbois from Lifeside Capital. Your line is open.

Thanks for the questions here. So I was just wondering, on that friction, pain in the physician's office, is this something where it's kind of always the same issue? Is there one problem that seems to be recurrent everywhere that's easily fixable, or is this a situation where it depends on the practice, it depends on the state, it depends on the doctor, how, you know, how far can you guys go in terms of better understanding if you have to do, like, a custom approach to each office, or is there something where it's like, I think we've got something here that is the main problem most of the time?

Morning, Frank. Good to hear your voice. So I'll say while we're working on it and Sherry gave you kind of the big overview, we definitely will be keeping a decent amount of our playbook to ourselves. So, yes, we do see opportunity on how to manage the friction we do as Sherry's company takes, like having a good hub, like being – but in terms of the tailor-made approach and how we –

Okay, great. And in terms of the FDA, there's just so much with you guys at the FDA right now. Has the personnel changed? Any updates on, there's obviously been quite a bit of change with the FDA, anything in terms of your case that has changed or has been more worrisome about this timing? I think you guys are waiting on the review from the Human Factors Protocol. If you just, in terms of timeline and expectations and comfort, and then you mentioned there could be a possibility where things even accelerate. can you just dig a little bit more into your, what you can share about FDA interactions?

Sure. To be clear, it is, we believe, however, we firmly early on during the development of the product, as well as during the review. So, we foresee no abrupt changes.

All right. Thank you very much.

Thank you. And our next question comes from I know, Mazahir Alimo-Omohad from Oppenheimer. Your line is open. Good morning, everyone. Thank you for taking

our questions, and thank you for the really comprehensive earnings call. So just a couple from us. I guess the first one is in terms of the Zebra royalty, how should we think about this $5.4 million? Is that a run rate figure, or were there any catch-up payments in Q1 that make this a high-water mark for the year? And then kind of one more, a little bit more mechanistic on the TSLP biomarker. So, it kind of seems like JAK1-2 sits downstream of TSLP signaling and that JAK inhibitors, which currently carry the black box warning largely due to their exposure, could limit the uptake. So, I guess, how confident are you that AQST's topical delivery profile would avoid the systemic JAK inhibition risks that currently limit the

oral agents. Thank you. So I'll let Ernie start with the time. So no, you should not think of

this as run rate for the year. You know, we've got to remember that what we receive from Zebra is a part of an agreement we have with them where we have an economic interest in one of their products as Taurus. Zebra recently sold as a result that received a $50 million payment of which we were entitled. So that is what accounts in the first quarter. That's an absolutely great

question. So when you think about the broad-based nature of immunomodulation when it comes to the adrenobers, you should think that we're not a specific actor inhibiting one pathway. So the healthy normal subjects that volunteer for this trial did not have an elevated TSLT. They did not have elevated CCL3, CCL4. And the topical AQST108 did not actually modulate those patients. So the Patients that had androgenic alopecia, it's not a broad-based inflammatory condition, but they did have elevated TSLT, and the topical 108 did reduce that directionally. Thank you for the added color.

Thank you. In our next question, we're going to fly in Raghuram Selvaraju from HC Wainwright. Your line is open.

Hi, good morning. Thank you for taking my question. This is Yanzu sitting in for Rome. So I have a few questions. The first is for Anifilm. So for Anifilm ex-US, you said that you have existing clinical data that's enough to support filings in Canada, EU, UK, and so on. And I'm just wondering, how are you thinking about sequencing, partnering, price access, all the works, and the retained economics across those markets?

The existing clinical piece. But Melita and her team have worked very hard. We've met with – so that's where – from that perspective, economics, we've done our work in those markets. We understand what we should retain versus what a partner should feel good about. So I think – Thank you.

And now with respect to the Oak Tree facility, would you be able to disclose what the payment – prepayment provisions are there? For example, like what are the cash restrictions, for example?

I think everything is disclosed in the 8K. It's pretty extensive disclosure on the covenants, and I would just broadly say.

Thank you so much. Thank you. Once again, that's star one one for questions, star one one. Our next question comes from Jim Malloy from Alliance Global Partners. Your line is open.

Hello. This is Laura in for Jim Malloy. Thank you for taking our questions. So for AQST-108, you've touched on this already a bit, but how do you think you're going to further look into the TSLP biomarker data in future studies for 108, and how meaningful do you think this finding is for the atopic dermatitis indication specifically that you're looking to study?

I'll pass it over to Matthew in a second, but I'm confirmatory of what we thought we would see, and I also do in the short term, so over these next few months' time, including Matthews will be heavily geared towards making sure we get our anatome resubmission right. I'm very very excited about the directional discovery of the

TSLP but please remember this is one of many biomarkers so it guides you towards inflammatory states dermatologically topically but also in additional programs we want to expand upon the biomarkers and the utilization of biomarkers because we believe, based on literature and based on our own precursor, there's a lot of opportunities, and we believe that tooth blockers and the adrenovirus in general really can have the potential of being a broad-based immunomodulator. And as we develop our programs, once we're done with what direction we'll go.

And also for Anafilm, with plans to expand globally, are you still on track to file for full submission to the EMA and Health Canada by the end of the year? And how would you just compare the overall U.S. versus ex-U.S. timing? Yeah, well, the U.S. timing, obviously, we've been

very open about. We continue to guide to a Q3 submission. We think it's a six-month review. We're going to try to get it. Great. Thank you for taking the questions.

Thank you. I'm not sure we have any further questions at this time. I would like to turn back over to Dan Barber for closing remarks. Thank you, Victor. As I said earlier in the call,

we are, in our view, ready to go. We're ready to conduct our studies. We're ready to build our awareness even further on track to law. And we look forward to updating you on our

additional progress. Thank you for joining us. Thank you for your participation in today's conference. This does conclude the program. You may now disconnect. Everyone have a great day.