Call highlights

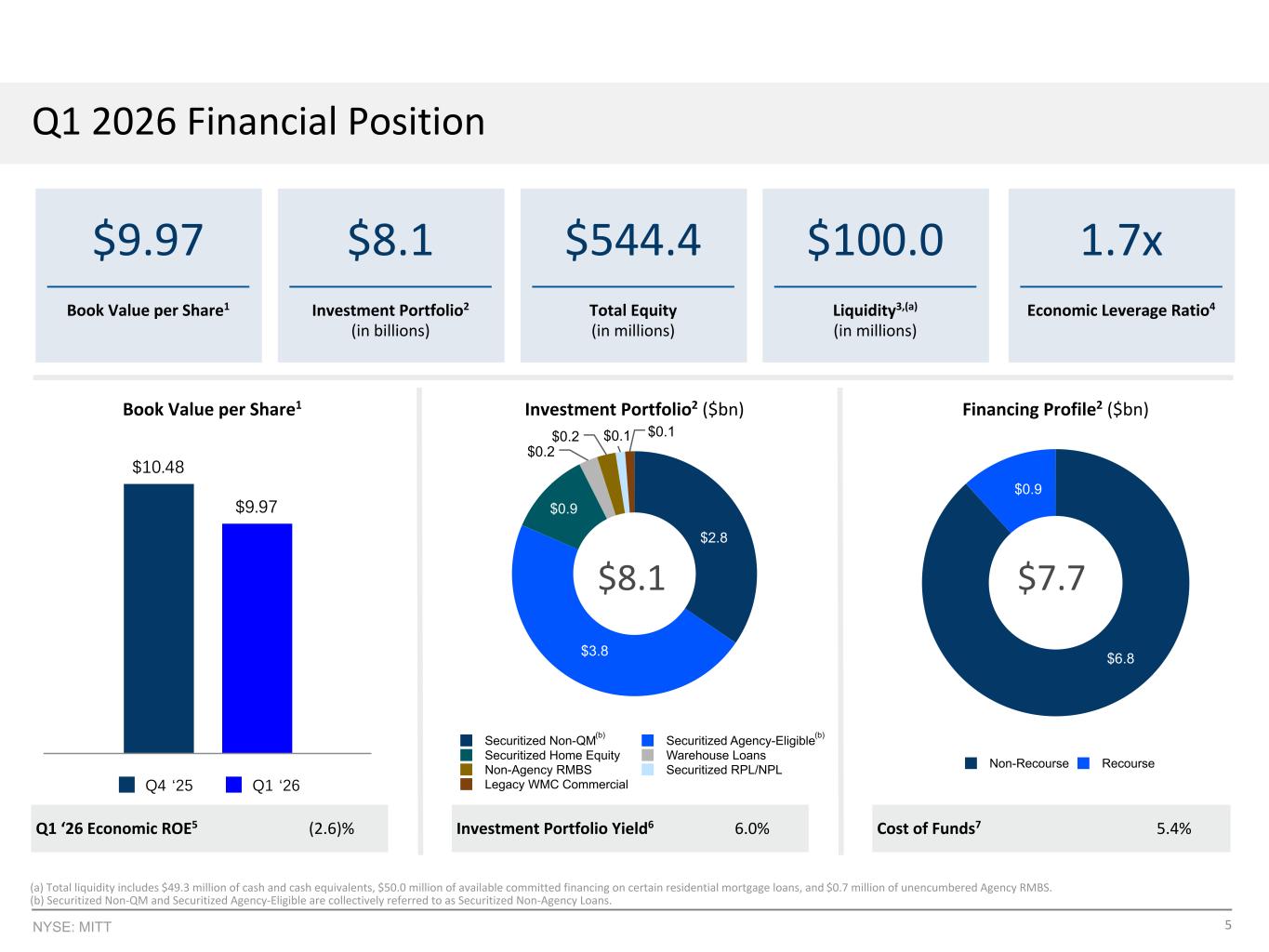

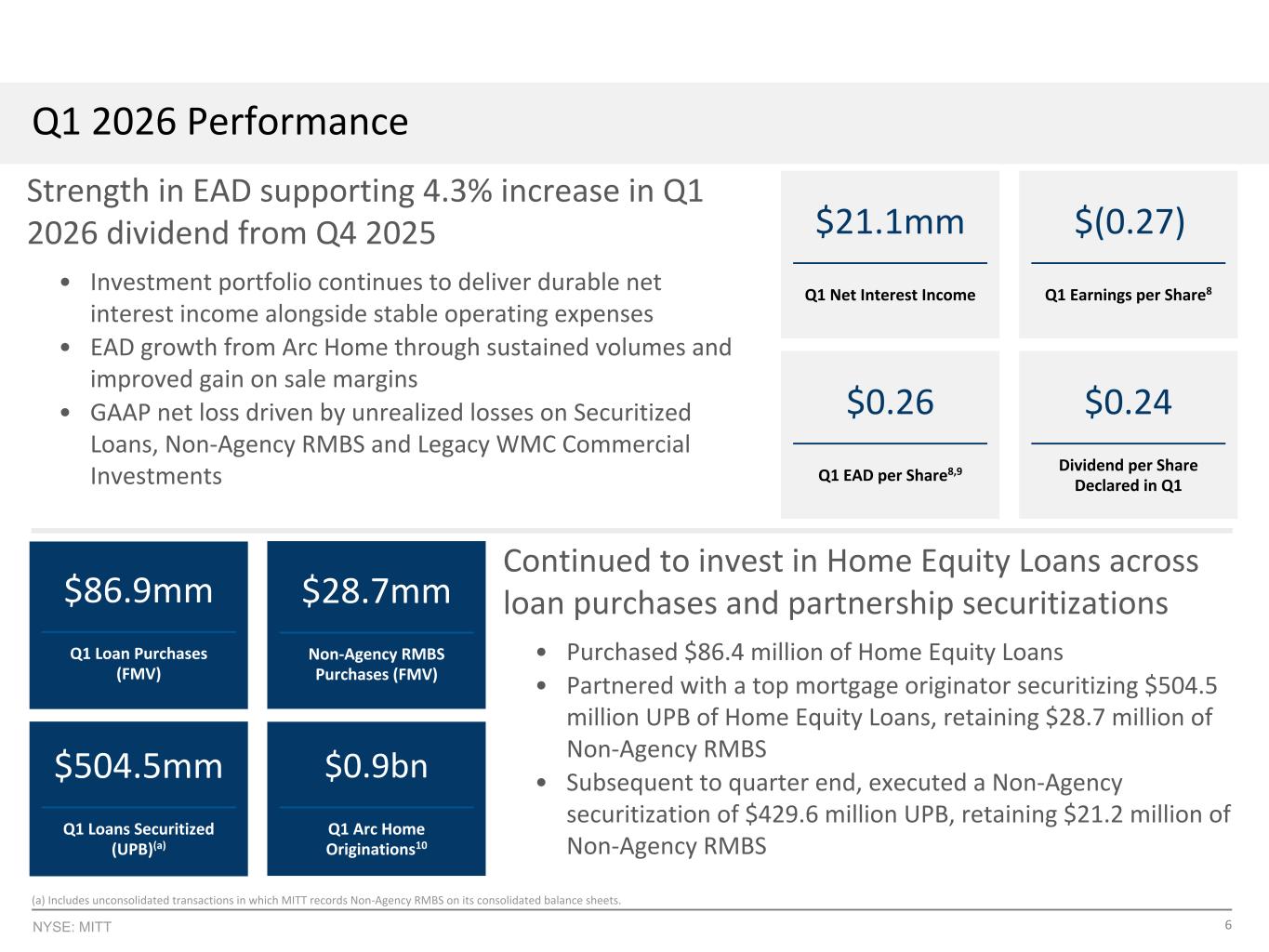

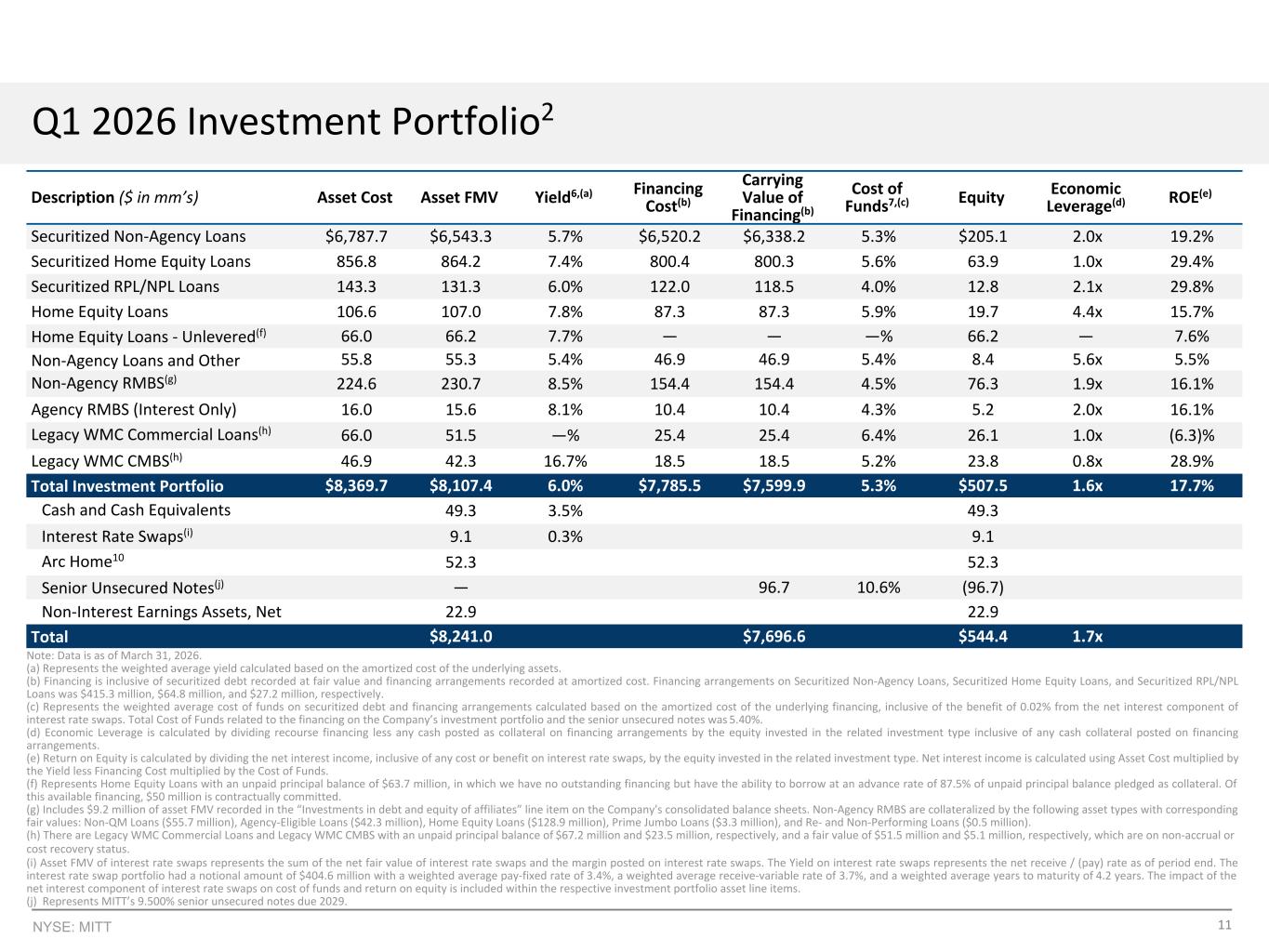

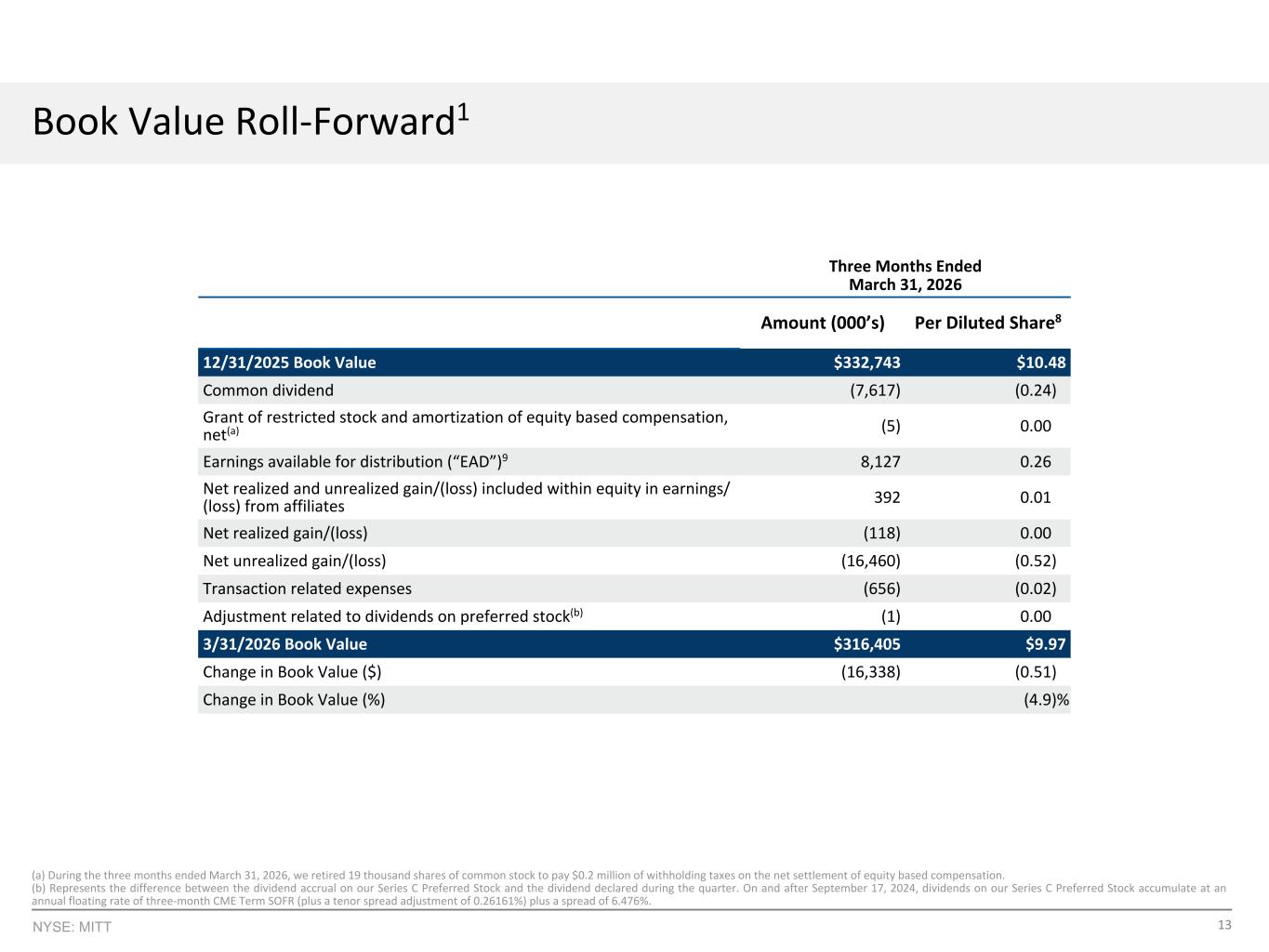

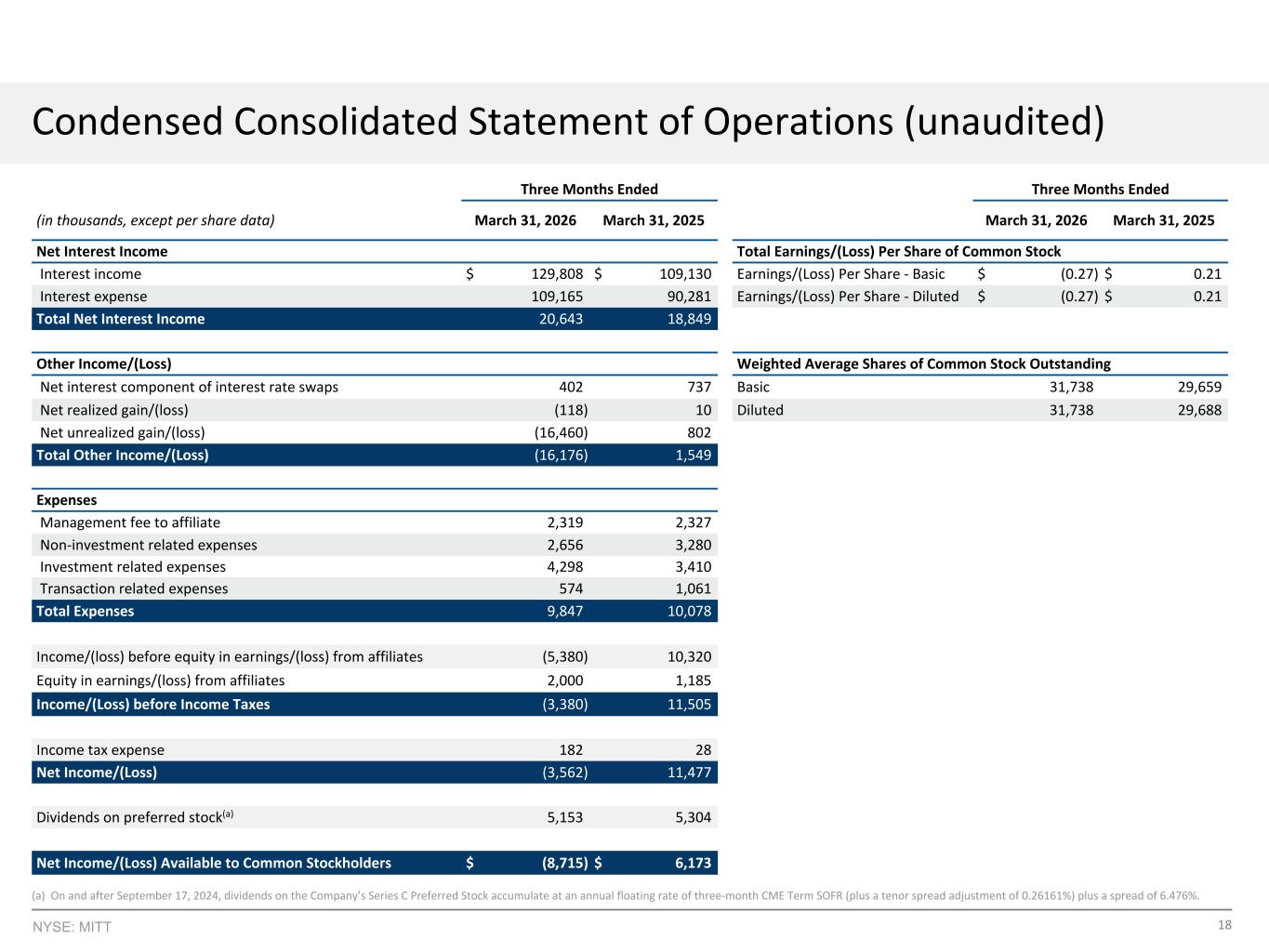

MITT reported Q1 2026 EAD of $0.26 per share covering the raised $0.24 dividend, but posted a GAAP net loss of $0.27 per share and a 4.9% book value decline to $9.97 driven by March macro volatility and net unrealized losses on the investment portfolio.

“we believe we've already recovered at least 50%. We are well positioned to navigate this volatility and continue to grow earnings while delivering superior risk-adjusted returns.”

“WE SEE MEANINGFUL UPSIDE AS WE OPTIMIZE THE BALANCE SHEET. SPECIFICALLY, THE DEPLOYMENT OF LIQUIDITY FROM UNLEVERED HOME EQUITY LOANS AND THE RESOLUTION OF NON-ACCRUAL COMMERCIAL LOANS REPRESENT CLEAR CATALYSTS TO DEPLOY CAPITAL INTO HIGHER YIELDING RESIDENTIAL INVESTMENTS, FURTHER ENHANCING SHAREHOLDER RETURNS.”

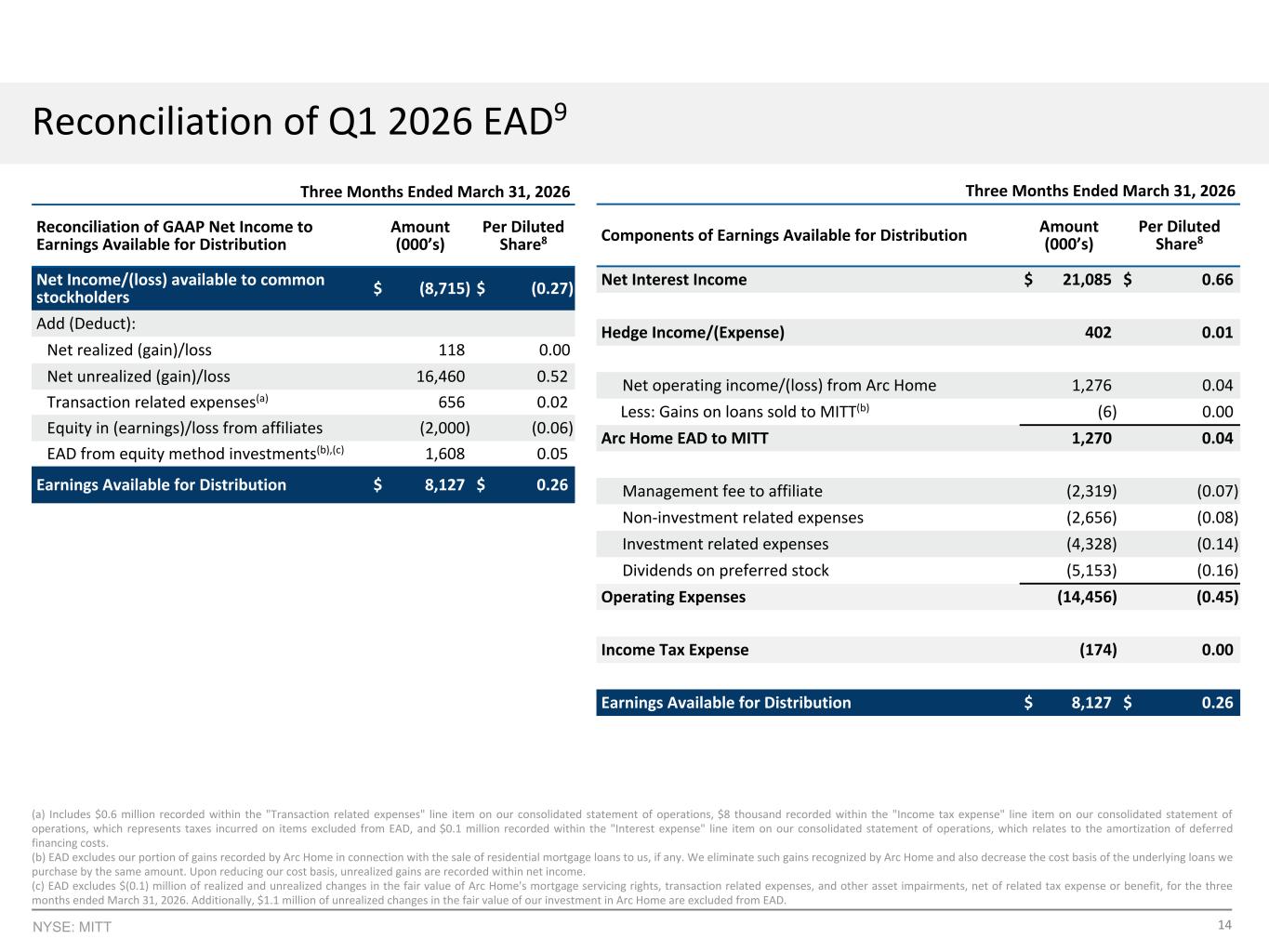

- EAD of $0.26 per share fully covered the $0.24 quarterly dividend, the fourth dividend increase since the beginning of 2025 (up 4.3% from $0.23).

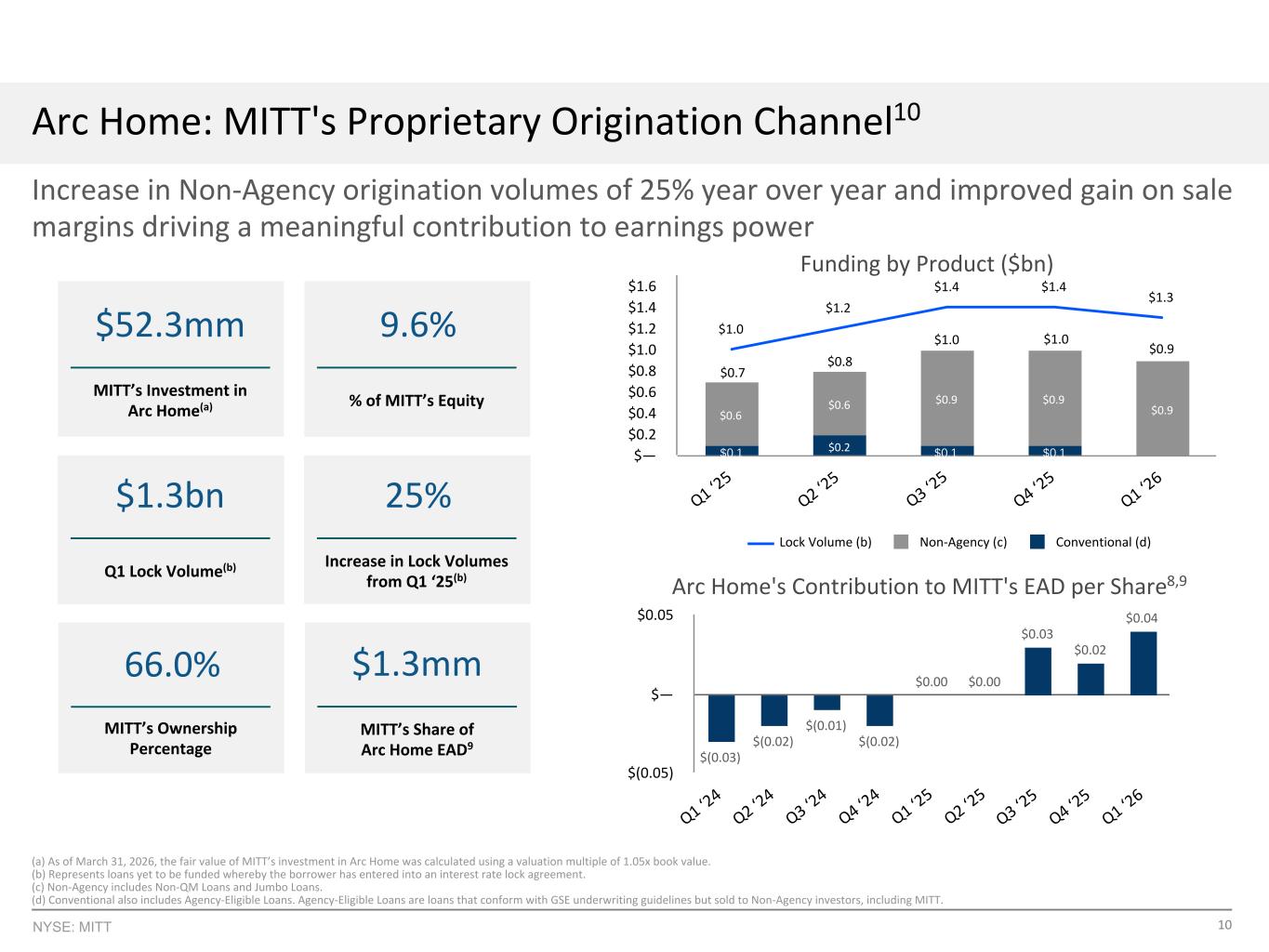

- Arc Home contributed approximately $0.04 per share to EAD, with lock volumes of $1.3 billion, a 25% year-over-year increase, driven by strong non-agency originations.

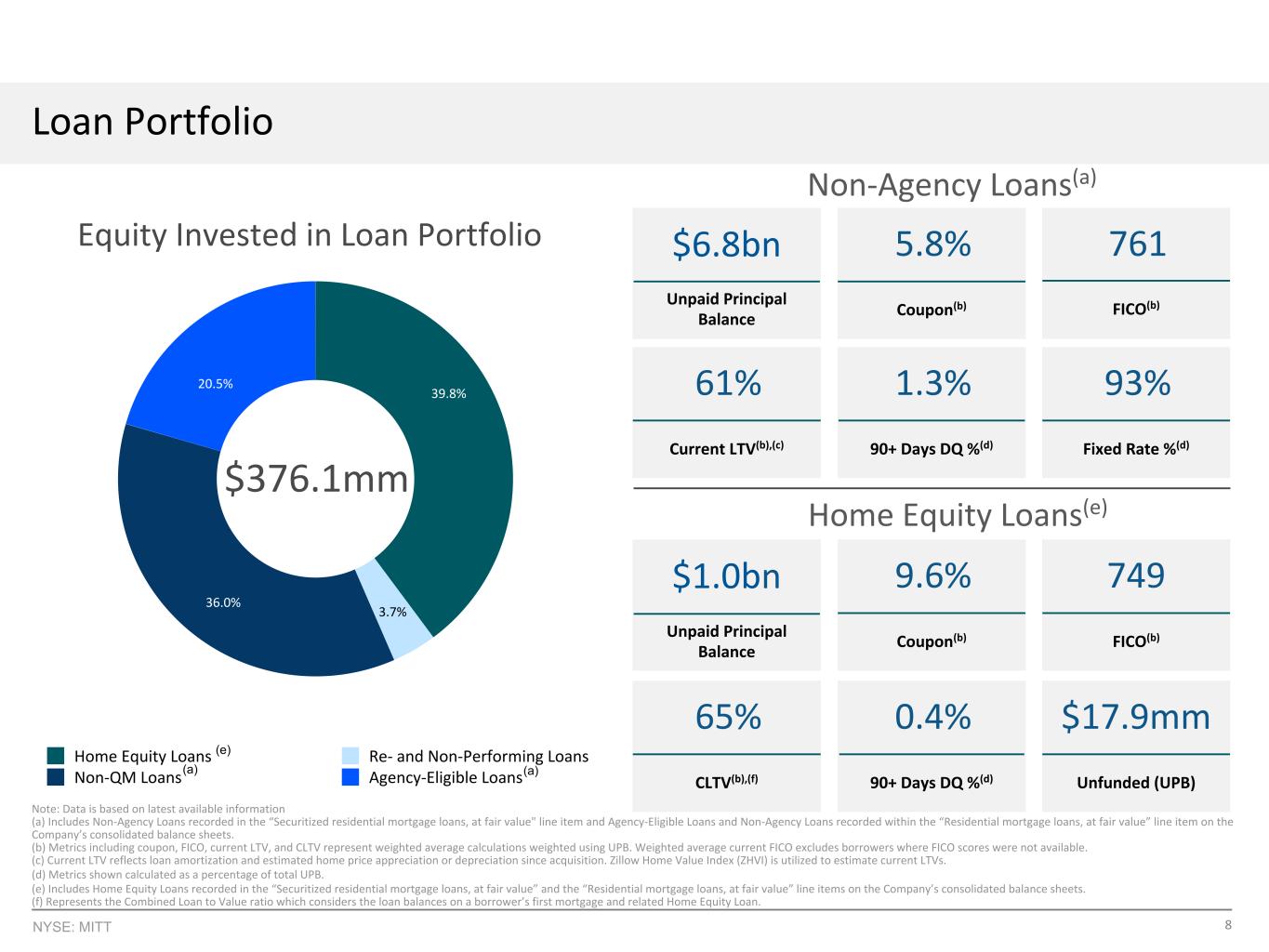

- Strong residential credit performance: serious delinquencies of 1.3% in the non-agency portfolio and 0.4% in the home equity portfolio, with average LTV in the low 60% range.

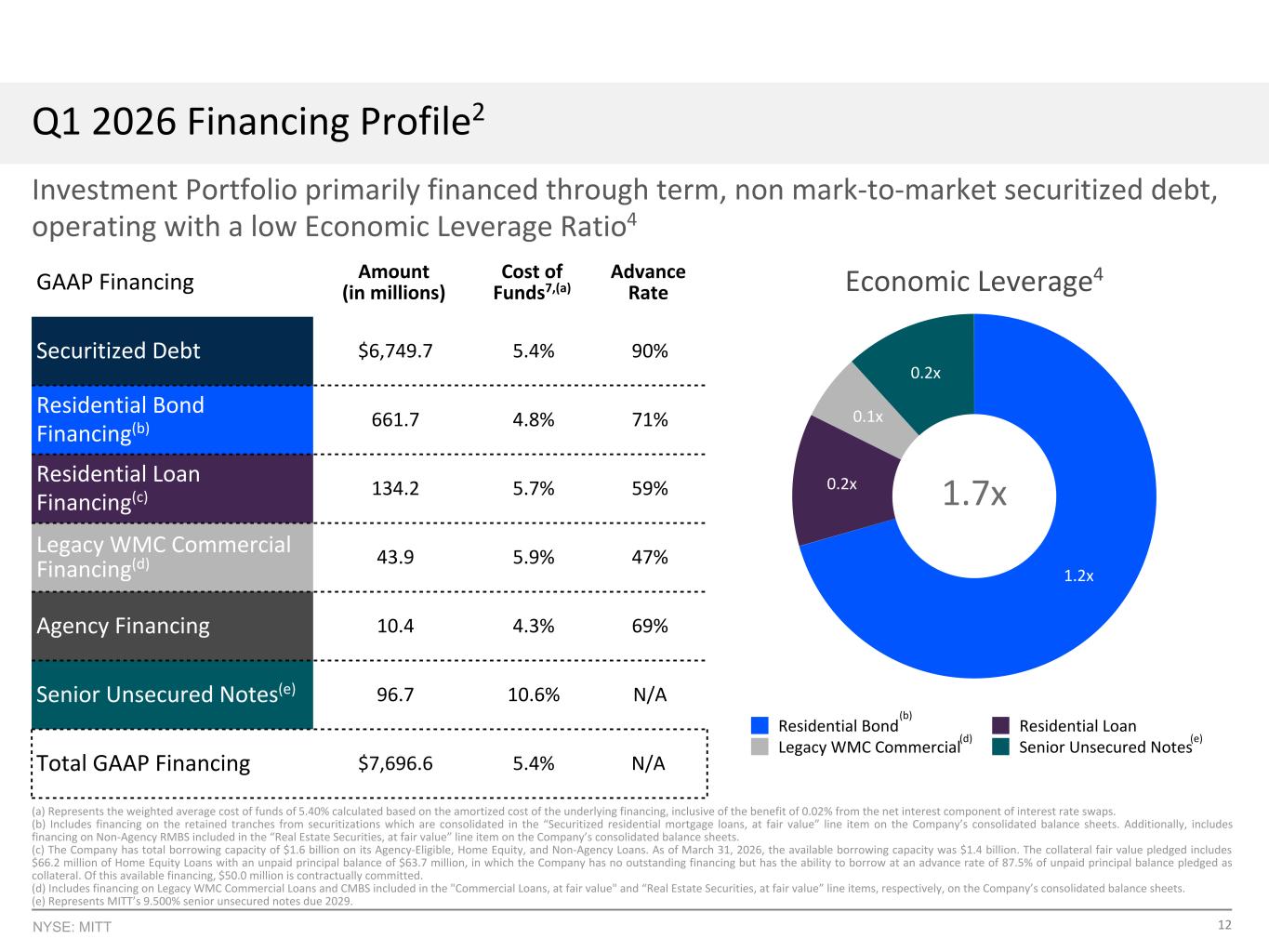

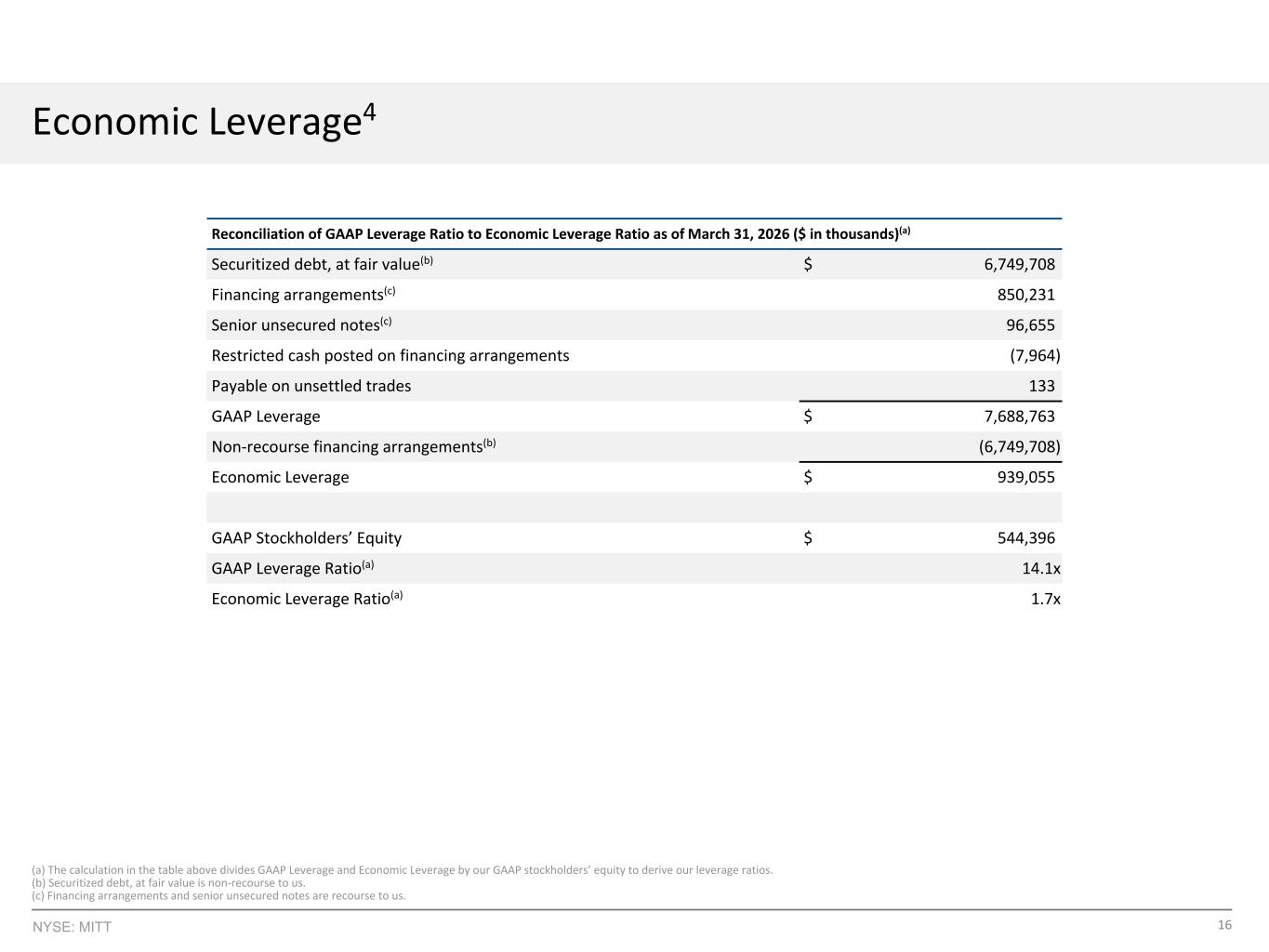

- Conservative economic leverage of 1.7 turns with ~$100 million in total liquidity, and management indicated leverage can prudently move higher to drive additional earnings.

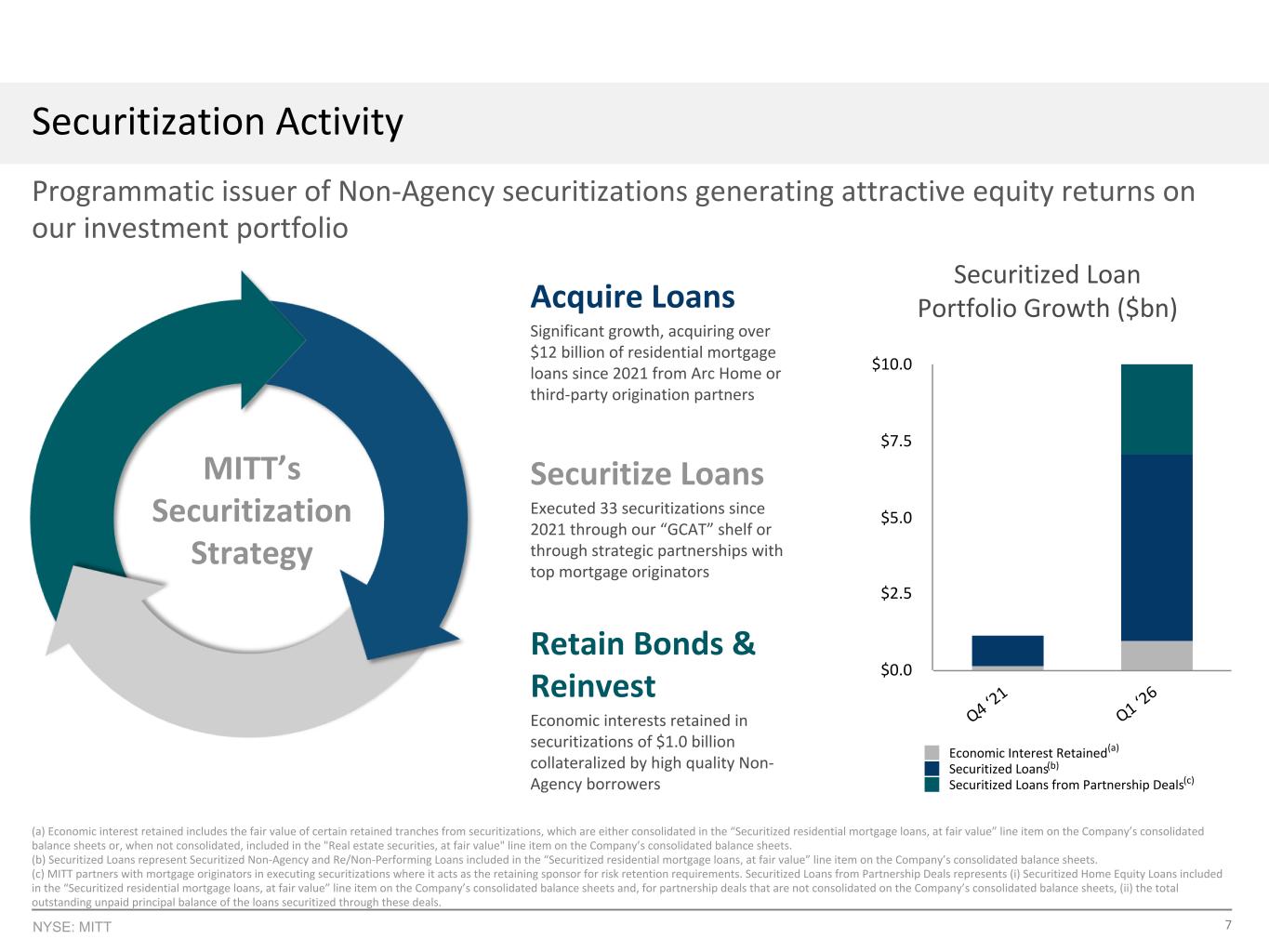

- Executed a ~$430 million non-agency residential mortgage loan securitization during the quarter and a subsequent home equity securitization in April.

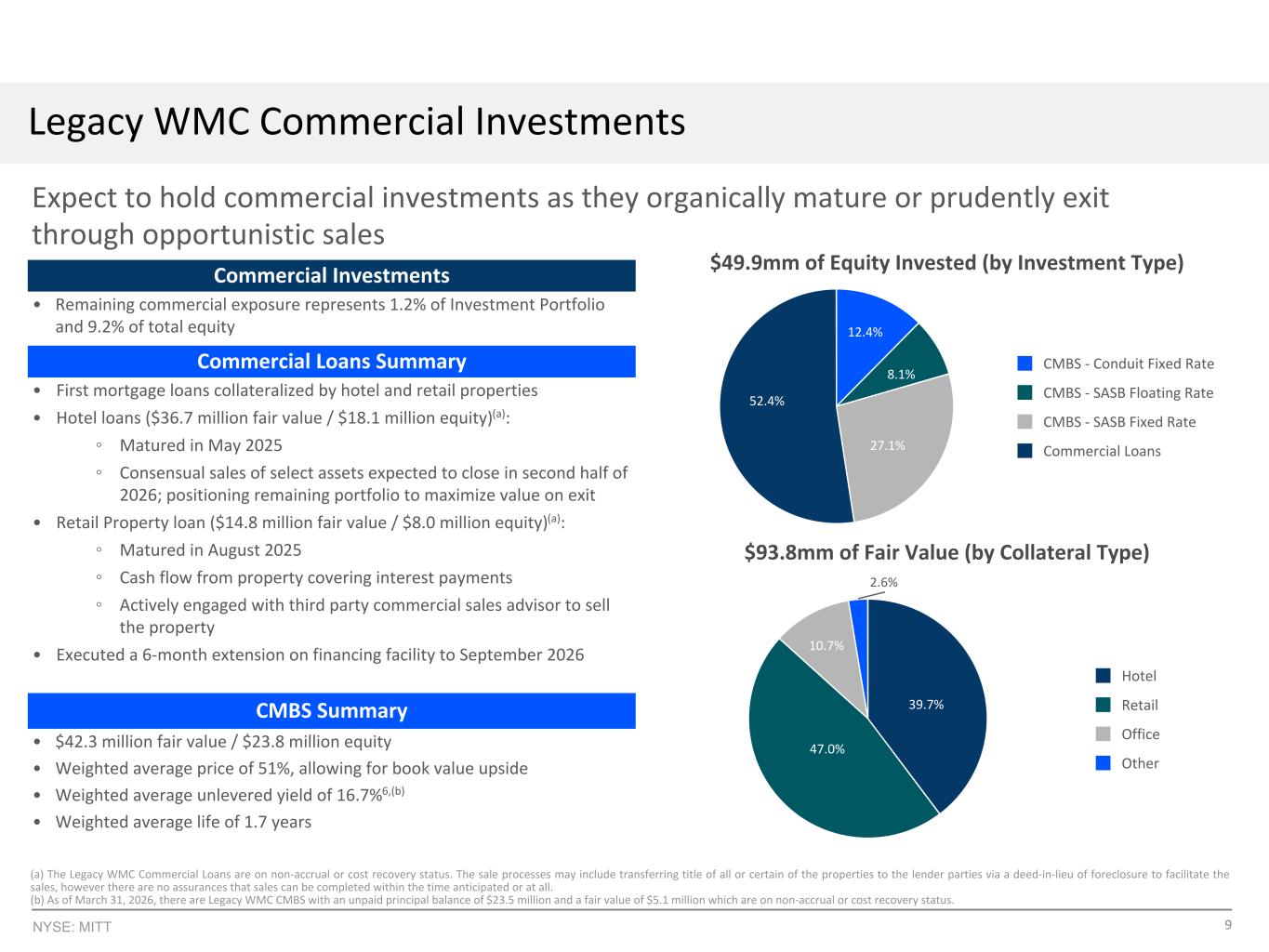

- CRE exit progressing: retail asset sale process advancing with detailed information expected next quarter, two of four hotel assets under signed LOI, and lender facility extended through September.

- Book value per share declined 4.9% to $9.97, resulting in a negative 2.6% economic return for the quarter.

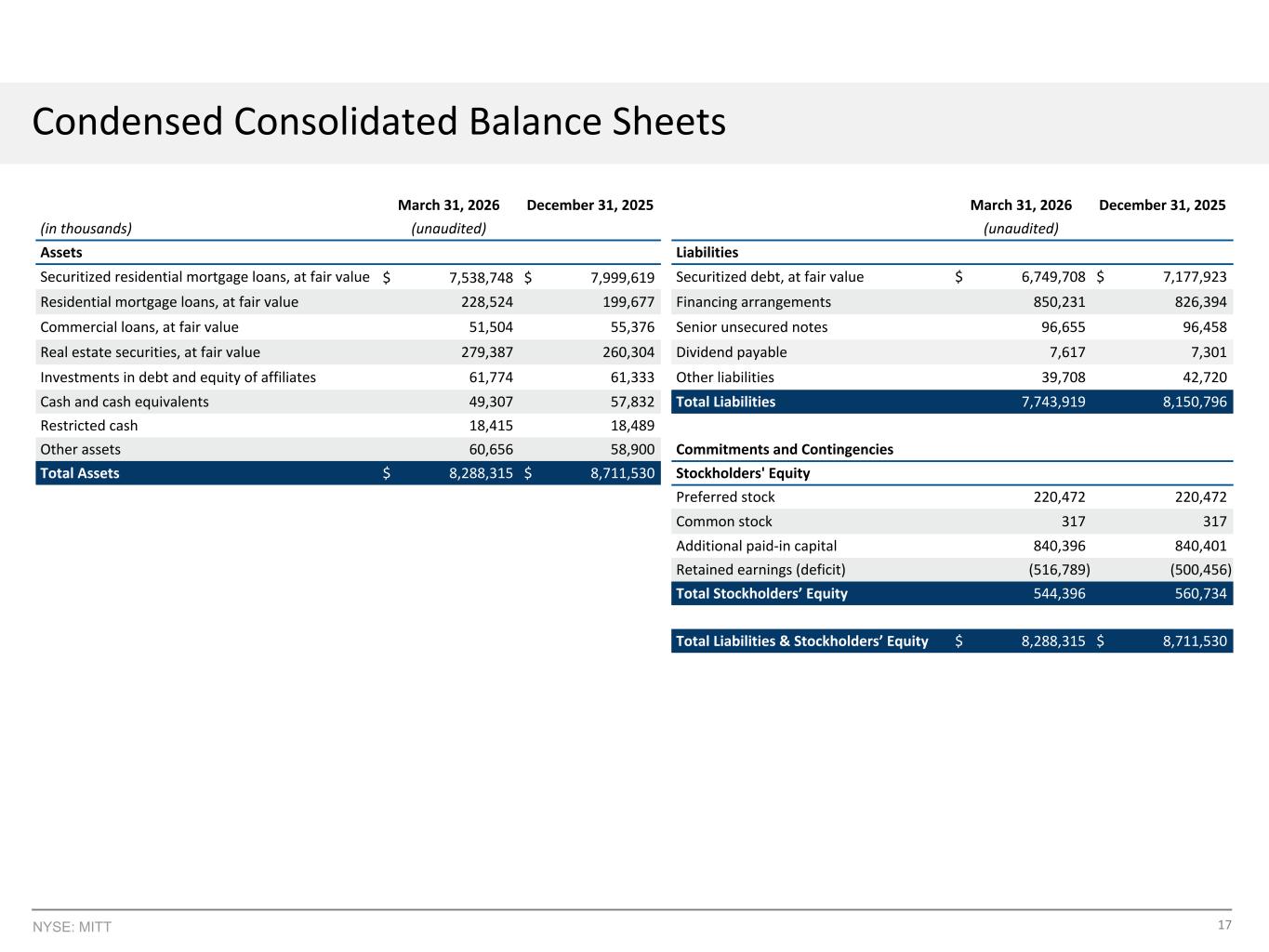

- GAAP net loss of approximately $8.7 million, or $0.27 per share, driven entirely by net unrealized losses on the investment portfolio due to March rate/spread volatility.

- GAAP leverage ratio of 14.1x and a notably low 0.6% net interest margin.

- CRE resolution is taking longer than expected; last two hotel assets may not be wrapped up until 2027, tying up capital that management wants to redeploy.

- 9.50% Senior Notes due 2029 (MITN/MITP) represent the most expensive part of the capital stack and will be coming callable later this year, creating a refinancing overhang.

remains core to our strategy and we believe this segment will provide the company compelling opportunities as this residential housing segment continues to grow in addition to this transaction we executed another securization subsequent to quarter rent comprised of approximately 430 million non-agency residential mortgage loans importantly we maintained our disciplined leverage profile the company's economic leverage stands at a conservative 1.7 turns While we have been able to grow earnings at these leverage ratios, we believe we can prudently move this up over time to drive additional earnings power. The credit performance of the company's residential portfolio continues to be a core strength. Serious delinquencies in our non-agency portfolio stand at just 1.3 percent, while our home equity portfolio is even lower at 0.4 percent. The portfolio is comprised of high-quality borrowers with significant equity in their On average, the non-agency and home equity portfolios have a low 60% loan-to-value. On the commercial side, we are seeing positive momentum as we manage our legacy WMC commercial holdings toward exit. We are focused on de-rescuing these positions, which will further free up equity for redeployment and our core strategies, higher-returning residential. Moving on to ARCOM. ARCOM has reached a clear inflection point. Despite the macroeconomic headwinds this quarter, our home delivered a meaningful contribution to our EAD of approximately $0.04 per share. We saw continued strength in lock volumes of $1.3 billion, a 25 percent increase year-over-year, driven by strong non-agency originations. Our decision to increase the ownership stake to 66 percent is starting to pay off as the platform gains market share and improves gain on sale margins. We're handing the call over to Anthony. I'd like to close with some thoughts around our strategy and the macro outlook. We entered the second quarter with significant ometra. While market volatility impacted our book value this period, we see a path to recovery. Since quarter end, we observed an improving, though admittedly fragile, macroeconomic environment. If this continues, we expect a return to trends we saw in the earlier parts of this year and believe this environment is likely to lead the market to revisit the tights of the year, which would reverse much, if not all, of the book value decline we saw in Q1. As TJ mentioned in his remarks, at this point, we believe we've already recovered at least 50%. We are well positioned to navigate this volatility and continue to grow earnings while delivering superior risk-adjusted returns. Anthony, over to you.

Anthony Acosta, Thank you, Nick, and good morning, everyone. During the first quarter, we continued to focus on rotating capital into our home equity portfolio. We successfully executed one home equity loan securitization and maintained our momentum in the securitization markets with an additional deal in April. Most importantly, we realized continued strength in our earnings available for distribution or EAD. This performance was supported by earnings growth at our home, despite a volatile quarter, which resulted in our EAD once again exceeding our increased dividend level. Reflecting this ongoing improvement in earnings, we announced our fourth dividend increase since the beginning of 2025, raising our quarterly dividend to $0.24 per share. Moving to our financial results, book value decreased 4.9% to $9.97 per share, resulting in a negative 2.6% economic return when considering our $0.24 dividend. We reported a gap net loss of approximately $8.7 million, or $0.27 per share, entirely driven by net unrealized losses on our investment portfolio, which were partially offset by gains on our hedge portfolio and investment in our home. Overall, these unrealized losses reflect the March macroeconomic volatility, which drove rates higher and caused spreads to widen. Despite these unrealized losses, which have begun to retrace in April, the company's operating performance remains strong, delivering durable net interest income, earnings growth at our home, and a controlled expense load, all of which supported our increased dividend and demonstrate the embedded value of our strategy. Specifically, EAD of $0.26 per share increased from the prior quarter and fully covered our

$0.24 dividend.

on. Net interest income, including hedge income, was $0.67, which exceeded $0.45 of operating expenses and preferred dividends to generate net earnings of $0.22 per share. ARC Home contributed an additional $0.04 to EAD, driven by continued strength in origination volumes and improved gain-on-sale margins. While the performance of our investment portfolio and ARC Home delivered LOWERED A DOUBLE-DIGIT ROE ON BOOK VALUE, WE SEE MEANINGFUL UPSIDE AS WE OPTIMIZE THE BALANCE SHEET. SPECIFICALLY, THE DEPLOYMENT OF LIQUIDITY FROM UNLEVERED HOME EQUITY LOANS AND THE RESOLUTION OF NON-ACCRUAL COMMERCIAL LOANS REPRESENT CLEAR CATALYSTS TO DEPLOY CAPITAL INTO HIGHER YIELDING RESIDENTIAL INVESTMENTS, FURTHER ENHANCING SHAREHOLDER RETURNS. LASTLY, WE ENDED THE QUARTER WITH APPROXIMATELY 100 MILLION IN TOTAL LIQUIDITY, CONSISTING of $49 million in cash, $50 million of committed financing on unlevered home equity loans and $1 million of unencumbered agency RMDS. This concludes our prepared remarks and we now like to open the call for questions. Operator. Thank you. At this time, if you would like

to ask a question, please press star 1 on your telephone keypad now. To withdraw yourself from the queue you may press star two again to ask a question that is star one on your telephone keypad one moment while we queue we'll take our first question from doug harder with btig your

line is open please go ahead thanks um can you talk about your you know your thoughts on um you you know, on increased, continuing to increase the dividend versus, you know, some ability to retain some capital, just given your commentary that you expect, you know, further upside in earnings power?

Yeah, Doug, it's T.J., good to hear from you. I think we're running, you know, fairly conservative economic leverage. So in terms of, you know, having excess liquidity for, you know, margin call risk, I think we've done a good job of alleviating a cash drag. And then, you know, as we think about growing earnings power, it's, you know, continuing to rotate the equity out of the CRE loans, which I'm happy to talk about, and then, you know, other capital rotation from, you know, potentially calling season deals, et cetera. So, I mean, I think we see a pretty linear path of how to rotate capital without needing to reserve a ton for it.

You're right. But I guess just as you think about that increased earnings power, how do you think about how much of that kind of gets passed through the dividend versus how much of that could be retained to support future growth?

I mean, I think we're looking to continue to pass that through to our shareholders in the form of the dividend and then satisfy the retest.

Great. Appreciate that. And, T.J., if I could take you up on your offer to kind of talk a little bit more about the CRE loans and, you know, kind of how we should think about the timing of resolution there and, you know, freeing up that capital?

William A. Yes, I think big picture we're making good progress on the remaining assets. It's, it's, you know, taking longer than, than any of us would like. I think this is evidence, the progress is evidence. We've been able to extend our facility with our lender out six months. So, so we have clean financing through September this year. From an asset perspective, I would really, you know, sort of break it up into three distinct situations. The retail asset sale process is moving along nicely. We would hope to have much more detailed information to share with you on next quarter's call. And then two of the four hotel assets have a signed LOI, and we're progressing accordingly, albeit behind probably where the retail asset process is. And then I think the last two hotel assets are going to, you know, be behind that and take a bit longer. And we're working, you know, through those locations and hope to have them sort of wrapped up by the end of this year, but it may drift into 27 for the last two.

Great. Appreciate it. Thank you.

Thank you. We'll move next to Marissa Lobo with UBS. Your line is open.

Thank you. Can you give us some more information on remissibility exercise call, right? Much of that remains to be executed. How do you feel about the current rate?

Thanks for your question, Marissa. As we've stated in previous remarks and Q&A historically, a lot of that has to do with outright levels of spreads. and interest rates, obviously, over the last quarter we saw retracement to higher rates, higher volatility, higher spreads. Into the beginning of this quarter, obviously, we've gotten a good amount of that back, maybe not completely in the front of the curve. All of these elements play into what, you know, the economics on calling transactions. You know, we're not going to hold out for every last penny, but we'll look for a stabilization of the market, which is happening pretty quickly. So, you know, hopefully we have good news in the coming quarters on actually executing on them and then sort of the path forward from there. That answers your question.

Okay, thank you. And could you also expand on the opportunity in agency-eligible loans? You know, what is your outlook there for volume and aggregation in your terms?

I mean, on the agency-eligible side, we've done a decent amount of this issuance in previous years, previous quarters. You know, a lot of our focus has really been more on higher returning opportunities in the non-agency and home equity space. There's still compelling opportunities, although less compelling in our view. you know, there have been new market participants that have entered that space with lower cost of capital, which maybe makes it a little bit less interesting to ourselves. That being said, I do expect to see others continue to grow and participate in that marketplace. Thank you.

Appreciate the caller. Thank you. We'll move on now to Crispin Love with Piper Sandler. Your line

is now open. Thank you. Good morning. I could follow up on earnings power and ROEs. You're generating, I think, roughly 10% core ROEs today. I'm curious where you think that could trend, what ROE targets are attainable, and over what time frame as R continues to be a larger contributor to EAD, and as you rotate capital into higher returning resi investments as the WMC investments

for sure yeah so if you thanks for the question thanks for dialing in so this is nick when you think about you know growing the roe of the company it's going to be derived from three primary sources which we you know said over previous uh quarters really you know the returning of equity capital in the commercial book growing roes um at our home and then then the calls all of that gives us line of sight into sort of achieving the ROEs that are being achieved across the broader business as we just have disclosed in the earning presentation. And that's really the path towards is really just taking those pockets and redeploying capital. Obviously, in our home side, that's less of a redeployment story, but we believe that there's strong momentum there and we expect we expect that to continue okay uh great and then um just

on our clone can you discuss a little bit what you've seen so far in in the second quarter just high level trends volumes and mortgage rates uh mortgage rates peak around quarter end have improved a sense uh approved improved a bit since then so getting into a little bit of a seasonally more conducive environment for mortgage but still a little bit of a challenging backdrop so just curious uh where you stand right now on our home and trends are seeing yeah normalizing for the

seasonality maybe slightly below budget but it's still early um you know we're still seeing you know gains so maybe that just you know speaks to the ambition of of the budget of our ambition of our budget there um so there has been a lot of healing um the gain on sales have been have been healthy um and the expectation is that the the the budgeted volumes will normalize and achieve what what we originally penciled out so you know early signs are good for for q2 and as you as you alluded to obviously you know seasonally this is an important part of the year for them great i

appreciate it thanks for taking my questions thank you we'll move next to bose george with kbw

your line is open thank you good morning this is a Frankie libetti on for Bose I just want to start with a follow-up on the commercial discussion do you think we could expect additional marks on some of the sales I know so they're continue to be ongoing but any color there would be great yes I think as we

as we continue to go through the sales process get more information from the market I think we're generally reflecting that in the current valuation so barring surprises I would say the answer is no.

Okay great then pivoting to the home equity you know it's you failed it nicely for the past few quarters trying to think about how large can that get as a percentage of portfolio and then you know 29 percent ROEs is that are those returns still available on new production and where's the best risk adjusted returns in that market today?

David Pacheco, Yeah, thanks, Frank. So, this market has expanded pretty, you know, with a good pace, call it 25 percent a year, really in earnest since, call it, 23. We expect that pace to continue or to accelerate. We expect it to be the largest non-agency sort of, or securitized product non-agency sector or in this, you know, at some point this year, if not next. So we still think there's a lot of runway for the opportunity. From a return standpoint, while there is increased competition, it's not nearly as competitive as other segments of the non-NC market, and that's despite its performance having been a standout versus the broader non-NC market. So we still continue to see a good amount of opportunity in this segment. And from a deployable capital standpoint, you know, we don't have any concerns on being able to recycle capital into this segment for a minute.

Great. Thank you.

Thank you. And we'll take our next question from Trevor Cranston with Citizens. Your line is now open.

All right. Thanks. There's been some reports about, you know, increasing delinquency levels in some of the recent vintage non-QM product. Can you guys comment specifically on, you know, your non-QM segment of the portfolio if you guys are seeing any sort of deterioration in performance, or just an update, that would Great.

Yeah, so one, the sort of underperformance of non-QM is less relevant to MIT, given our transition over to other segments, you know, over two years ago, you know, most notably really the agency-eligible segment and then the home equity segment. Our agency-eligible book is performing better than Prime Jumbo, which is shocking to say out loud, but that's a fact. And then our home equity segment, the delinquencies are, you know, less than a quarter of the delinquencies of the broader non-QM market, which is where most of the concern is. So MIT as a vehicle is inflated versus sort of the underperformance versus underwrite. You know, we still are constructed broadly in the non-QM space. But I think it's worth noting that, generally, our credit selection has been tighter than the broader universe, which is driving some of that outperformance. So we don't view our book as a comp versus other folks. Over the years, there's been some degradation in performance for various reasons. We don't see MIT as being exposed to that.

Okay. Appreciate the comments. Thank you. And once again, if you would like to ask a question, please press the star, then 1 on your telephone keypad now. We'll move on to Jason Weaver with Jones Trading. Your line is open.

I was just curious about the 9.5 notes of 29. Those are obviously the most expensive part of the capital stack right now. It's three years out, but I believe they've become callable relatively shortly. And with your EID coverage, have you – tell us how you're thinking about maybe doing a refinancing, tender, partial pay down. Any thoughts there?

Yeah, no, I mean, we're always evaluating the entire capital structure. To your point, they are coming call, but there's two separate notes that are not too far away from each other, and they'll be coming up later this year to the extent rates in the market move in the right direction. We'll certainly be looking to explore refinancing.

Got it. Thanks. Then on just overall purchase activity, your volume this quarter was well below, you know, the fourth quarter, I think $87 million versus $284 million or so. Is that more of a strategic or a timing issue over time? Were you waiting for wider spreads to get involved, or can you talk about that a bit?

it's it's a little more complicated than that so while the portfolio decreased my gap basis it's really because the structures of the most recent transactions uh result in the company not consolidating these deals um you know had we consolidated those deals we actually would have modest growth um so i think you know there's a little bit of form over substance um you know

given those nuances all right that makes sense thank you for that caller thank you at this time

there are no further questions in queue and I'll turn the meeting back to our hosts for any closing

comments thank you to everyone for joining us this morning and for your questions we appreciate it and look forward to speaking with you again next quarter a great day thank you this brings us to

the end of today's meeting we appreciate your time and participation you may now disconnect

Thank you.