Call highlights

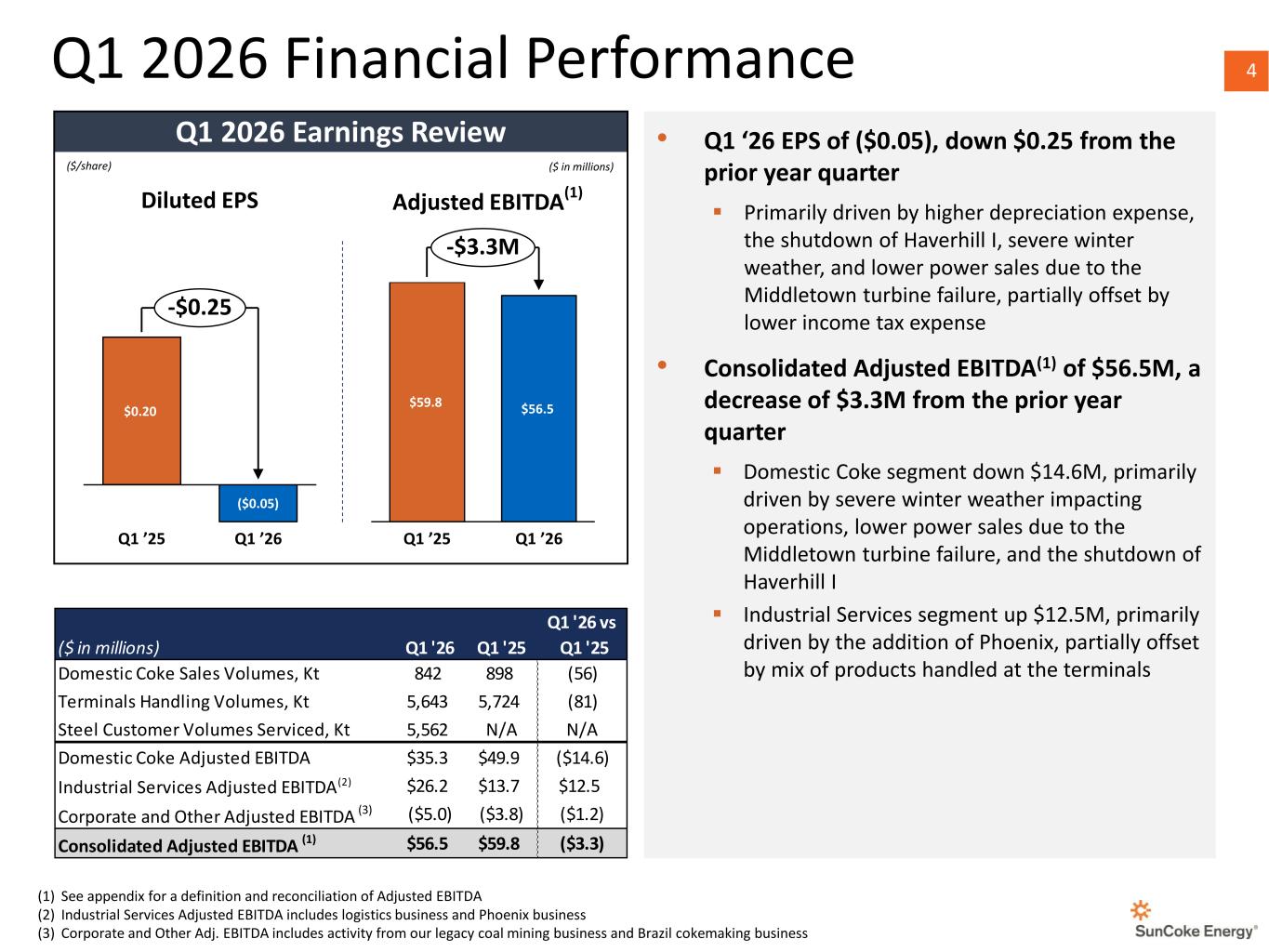

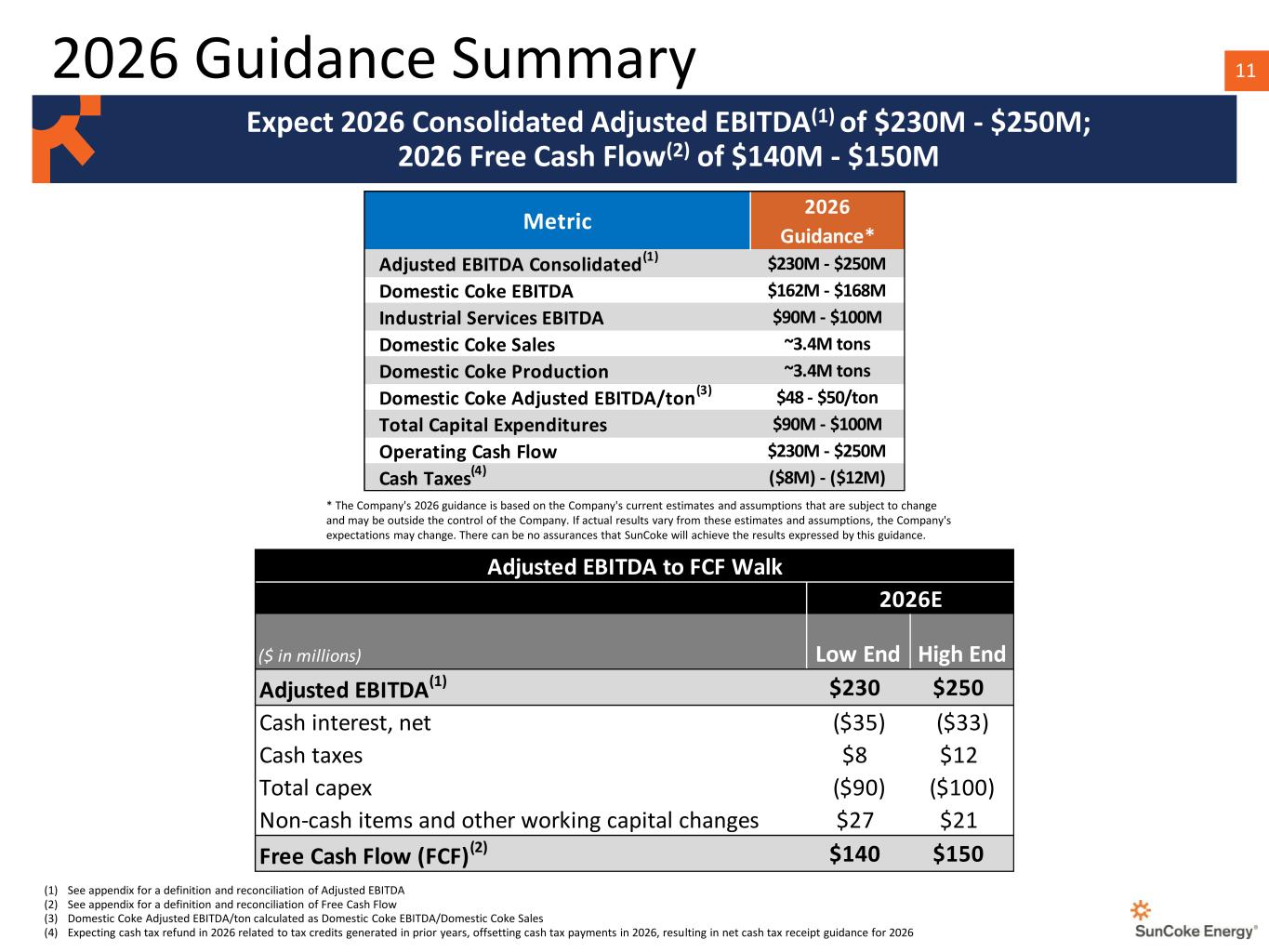

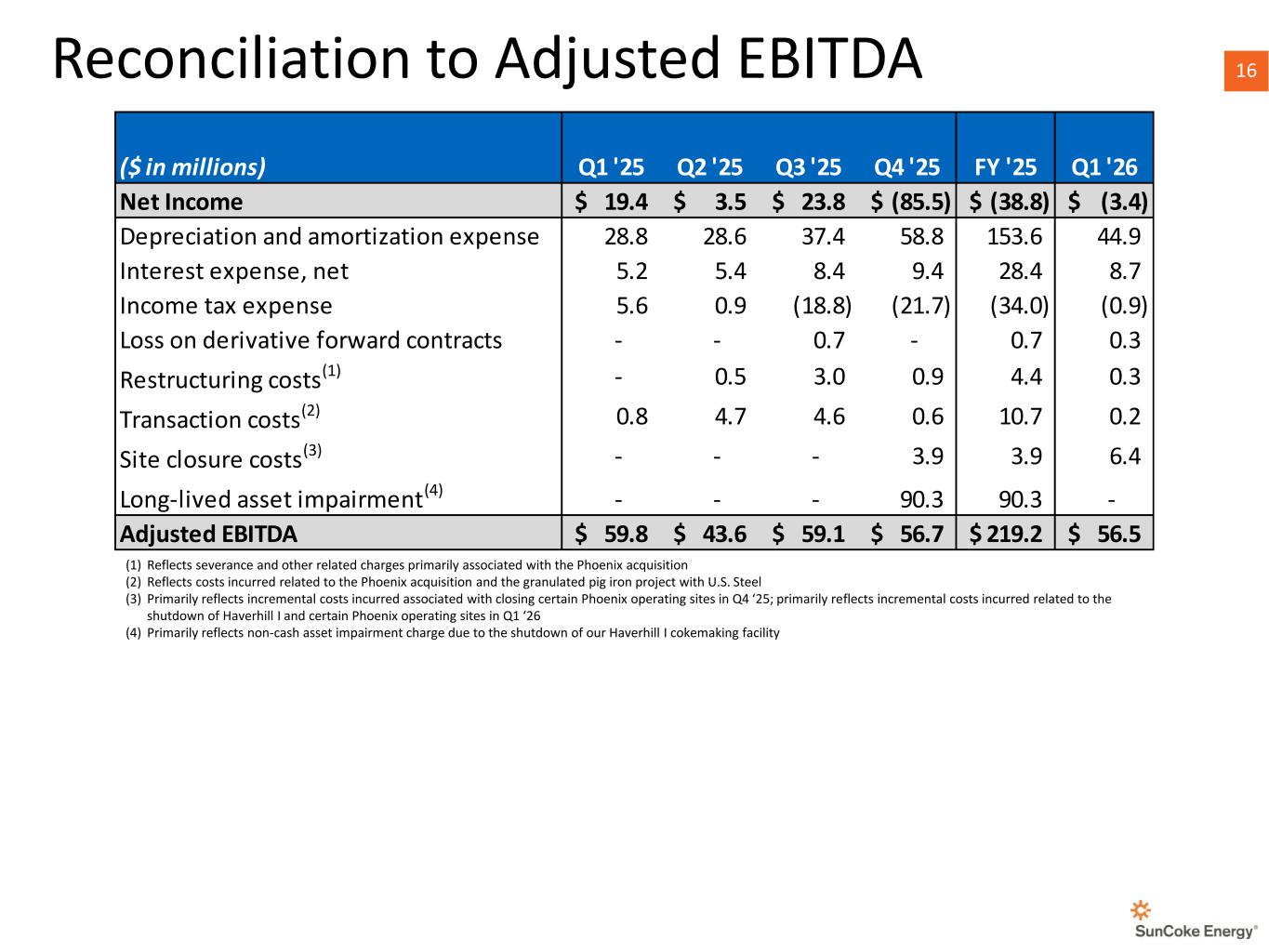

SunCoke reported Q1 2026 consolidated Adjusted EBITDA of $56.5 million (vs. $59.8M prior year) on a net loss of $3.4 million, with results pressured by severe winter weather, the Middletown turbine failure, and the Haverhill 1 shutdown, partially offset by the Phoenix acquisition. Management reaffirmed full-year 2026 consolidated Adjusted EBITDA guidance of $230–$250 million and declared a $0.12 quarterly dividend (27th consecutive).

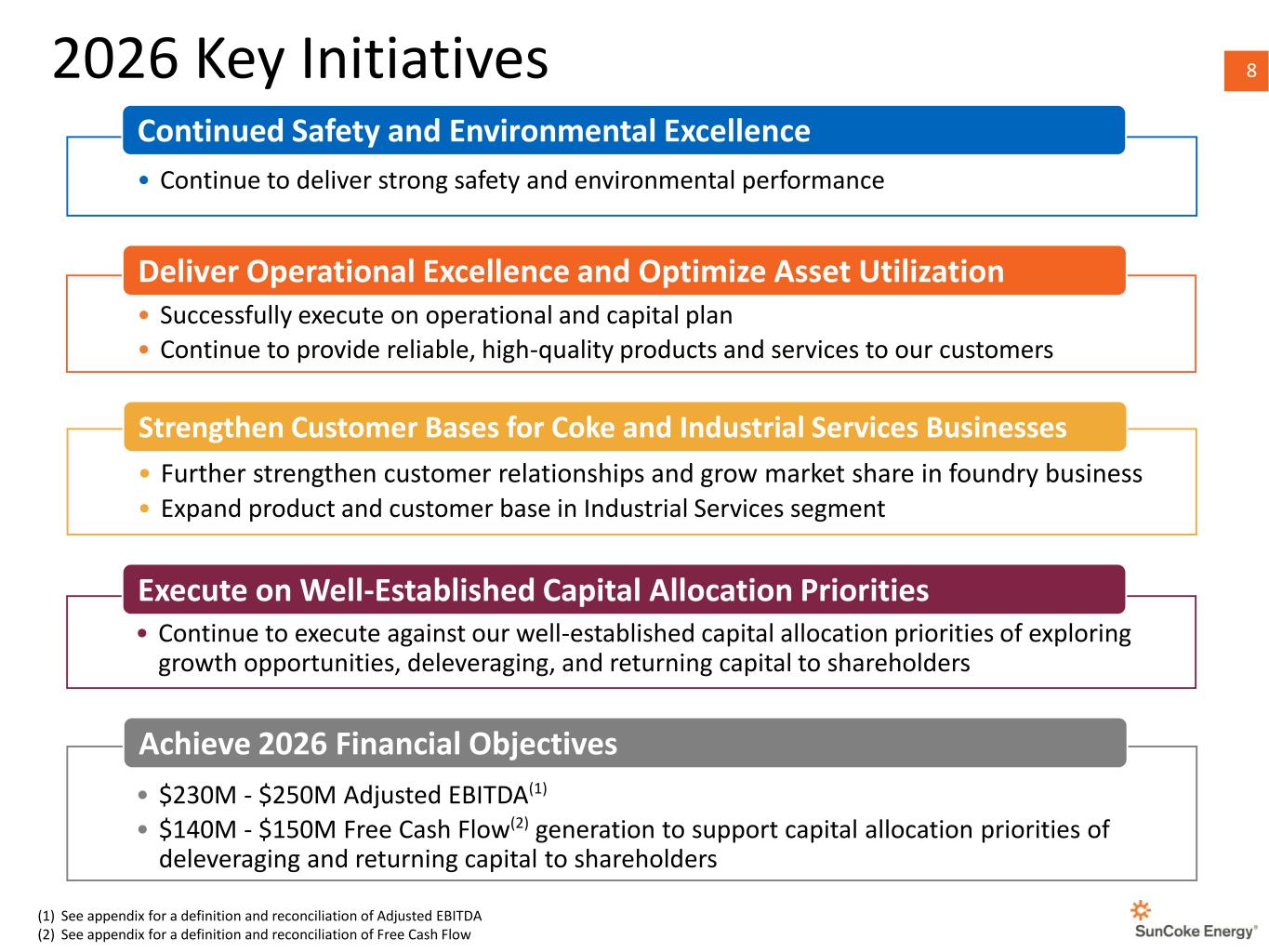

“We will use excess cash to continue paying down our revolver balance with the goal of gross leverage below three times by the end of 2026 and beyond. We also plan to continue returning capital via the quarterly dividend as approved by our board, which has always been well-received by our long-term shareholders.”

“we are running at full capacity and sold out for the full year. With the continued seamless integration of Phoenix, the resumption of power production at Middletown, and continued strong operational execution, we are confident we will achieve full year 2026 consolidated adjusted EBITDA within our guidance range of $230 to $250 million.”

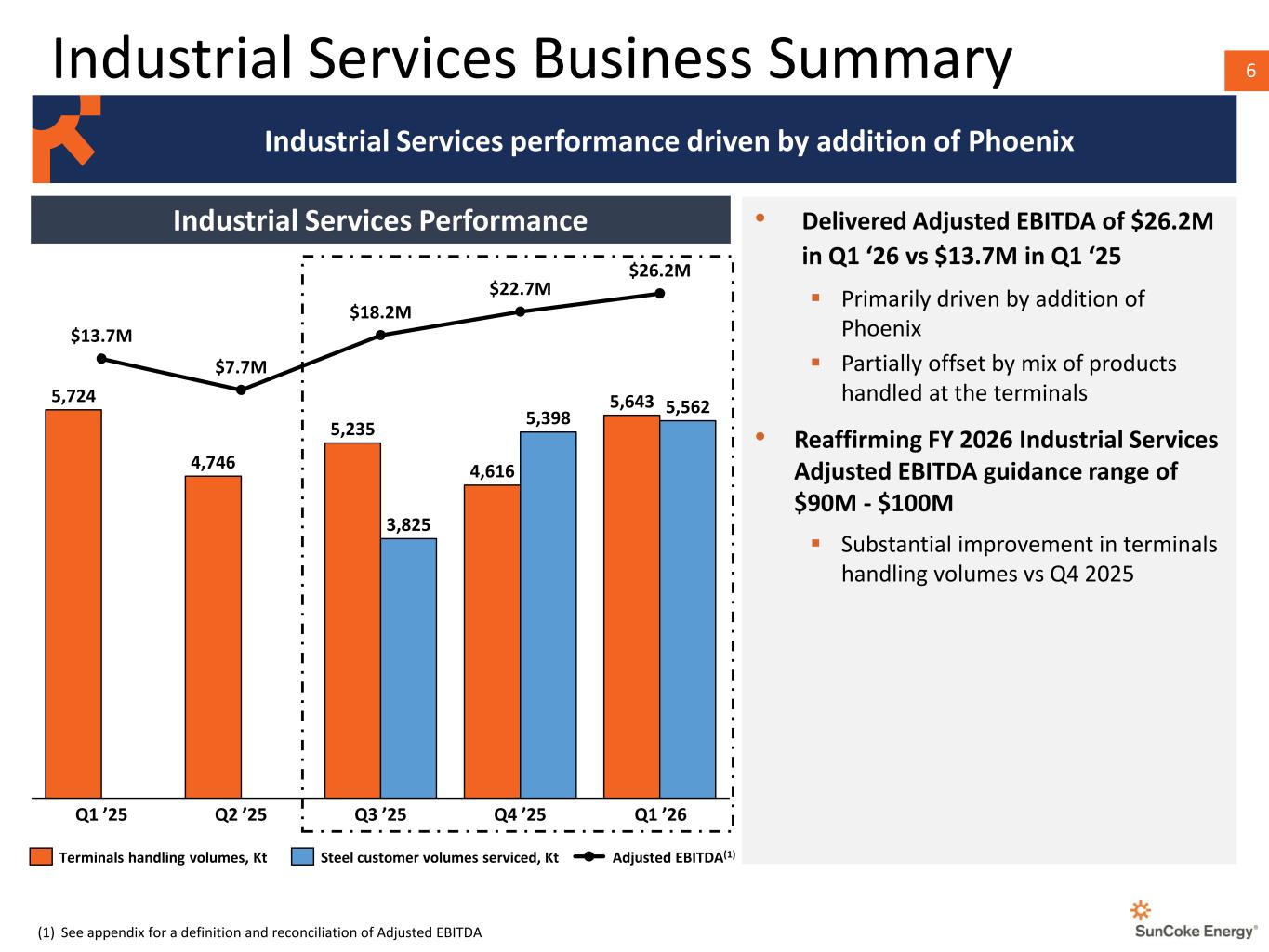

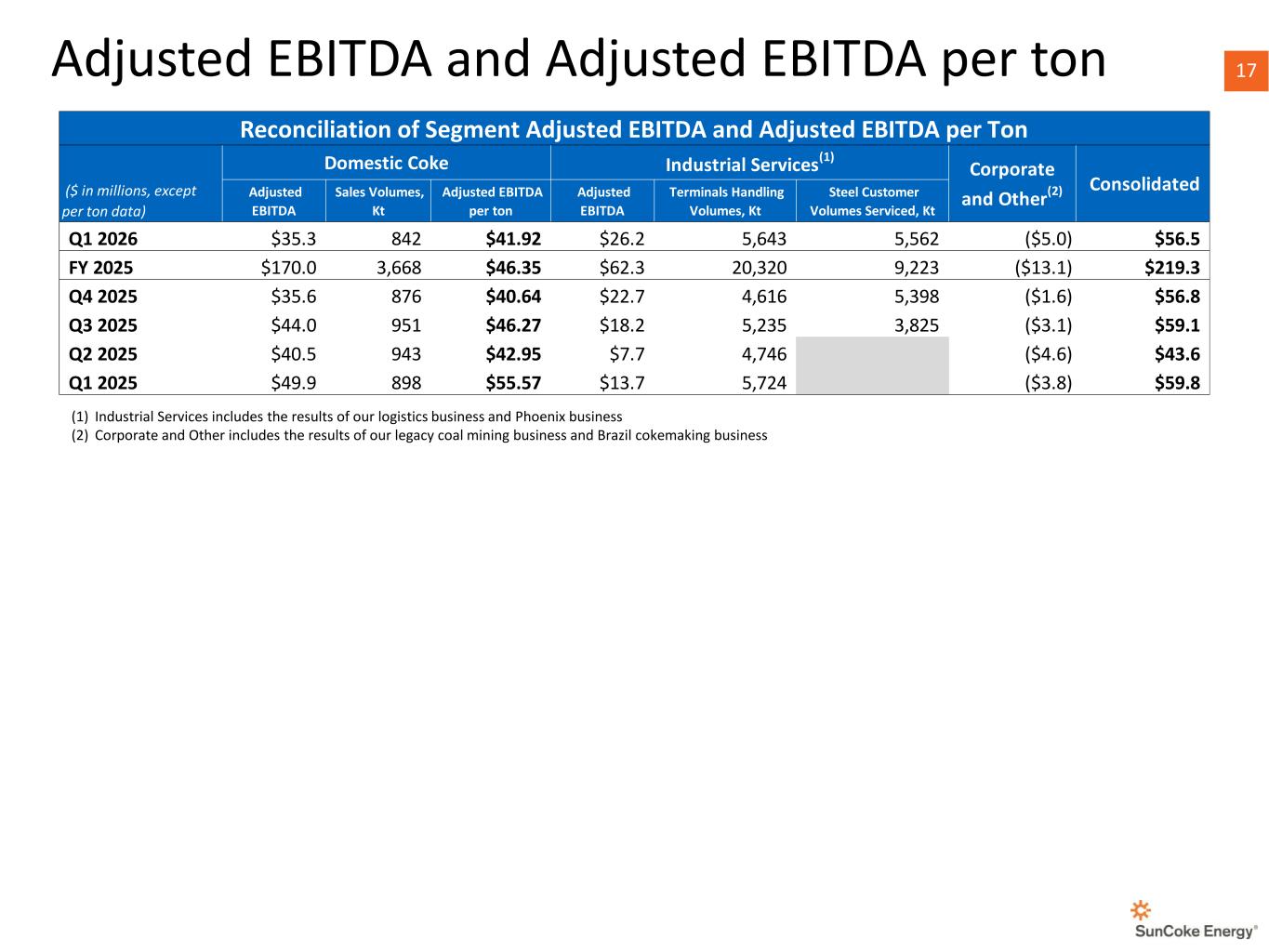

- Industrial Services Adjusted EBITDA nearly doubled YoY to $26.2M from $13.7M, driven by the Phoenix acquisition

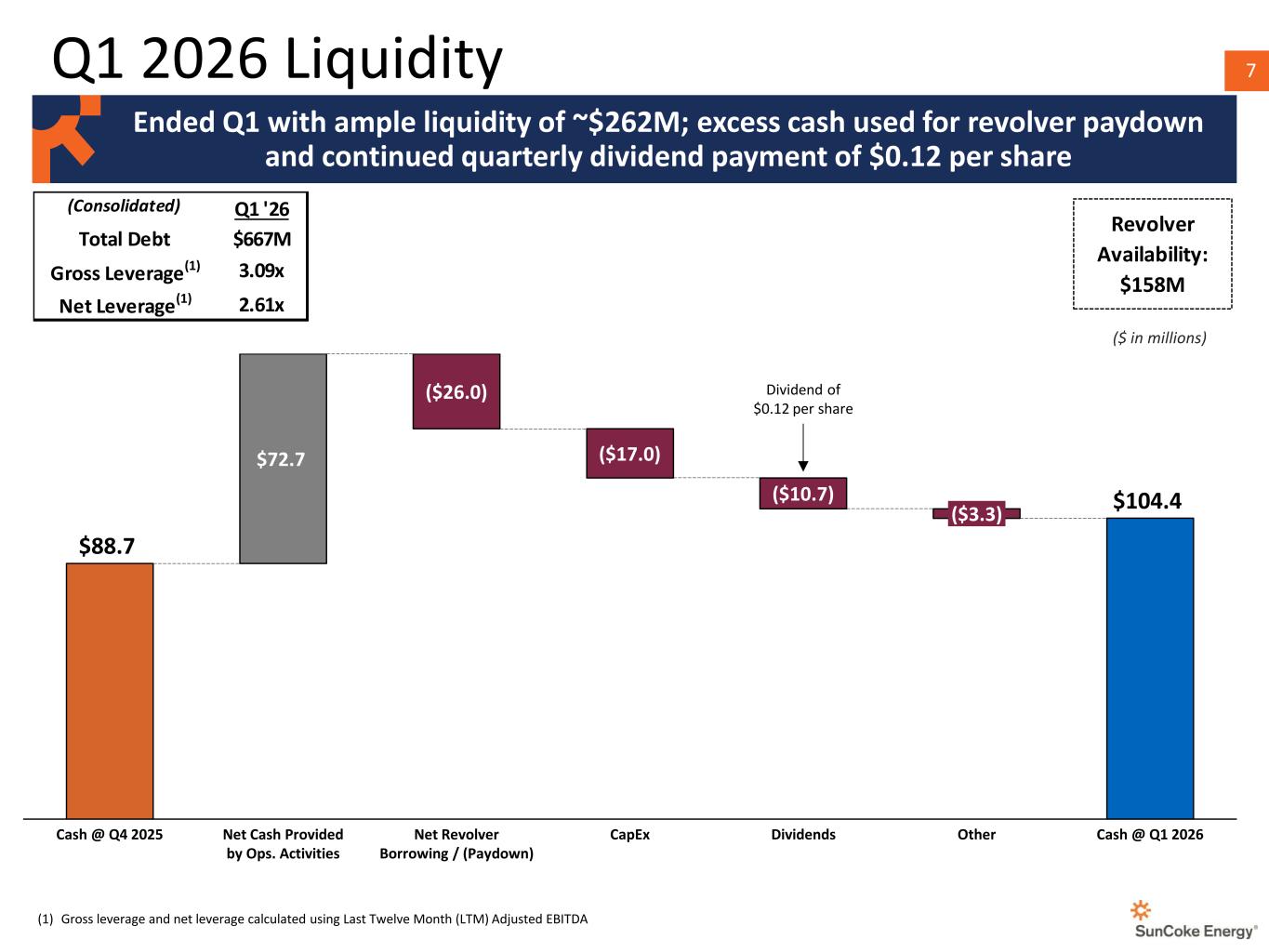

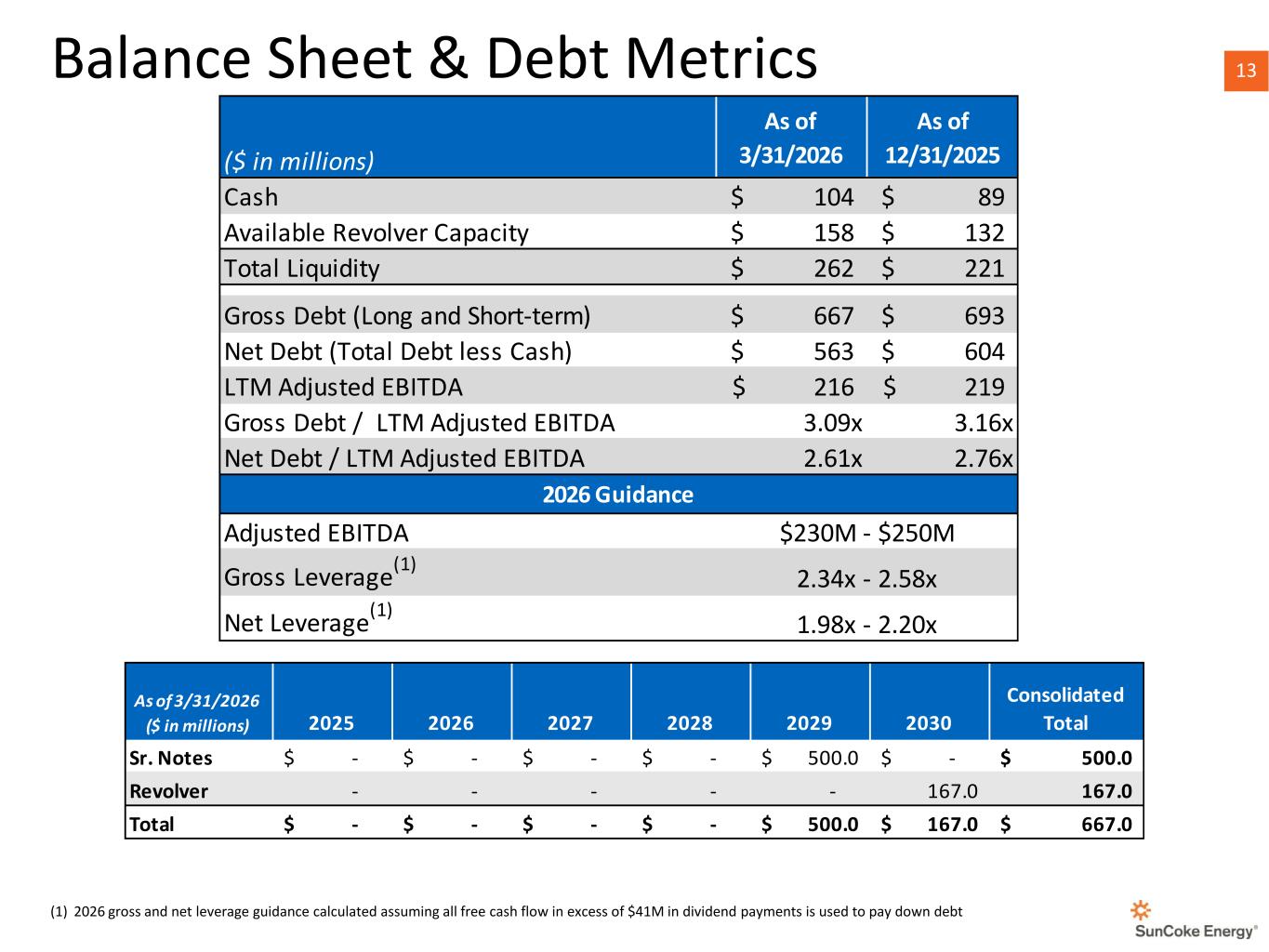

- Operating cash flow of $72.7M and ample liquidity of $262M ($104.4M cash plus $158M revolver availability)

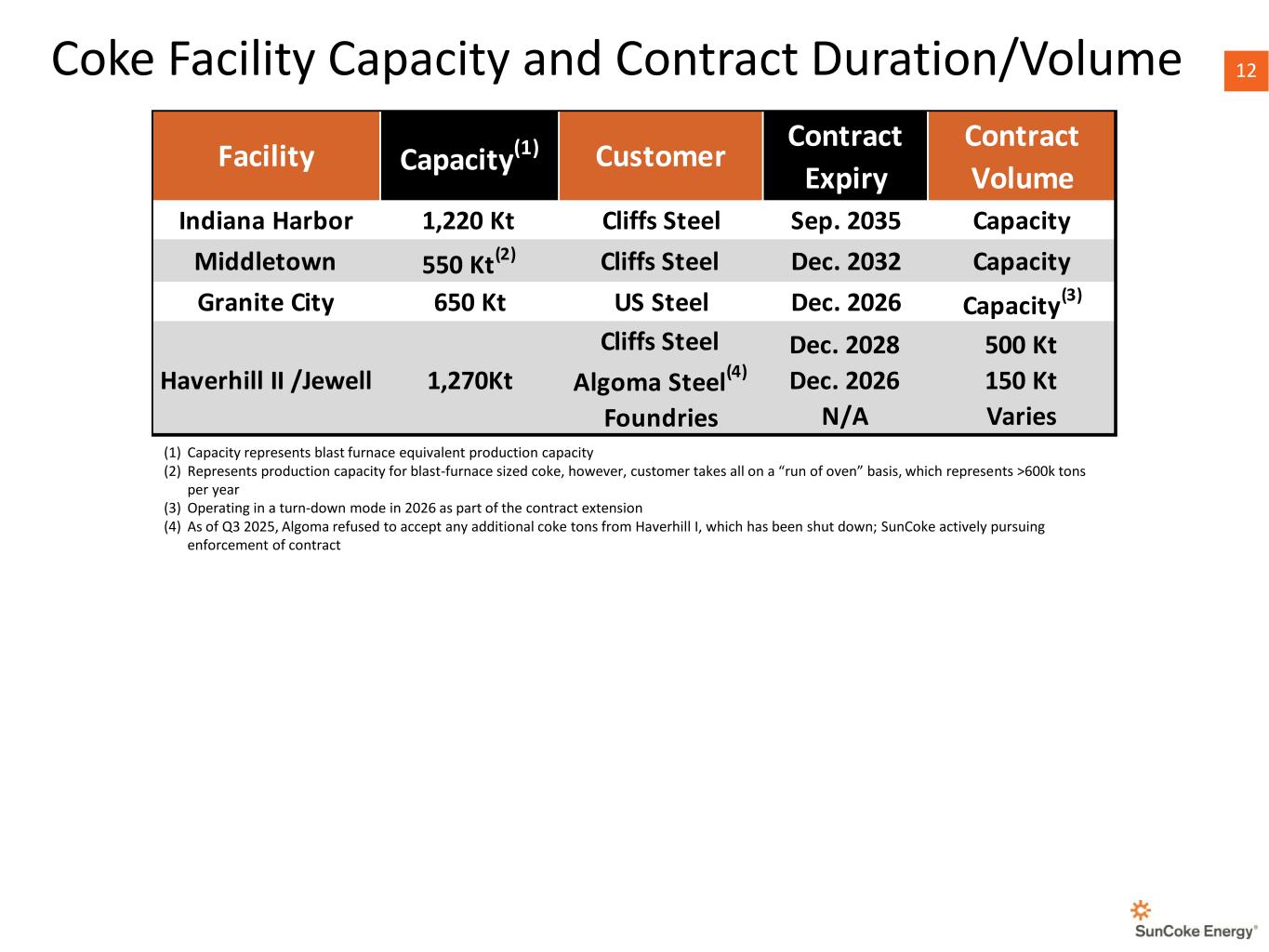

- Sold out for the full year with all spot blast and foundry coke sales finalized; Haverhill II and Granite City contracts extended

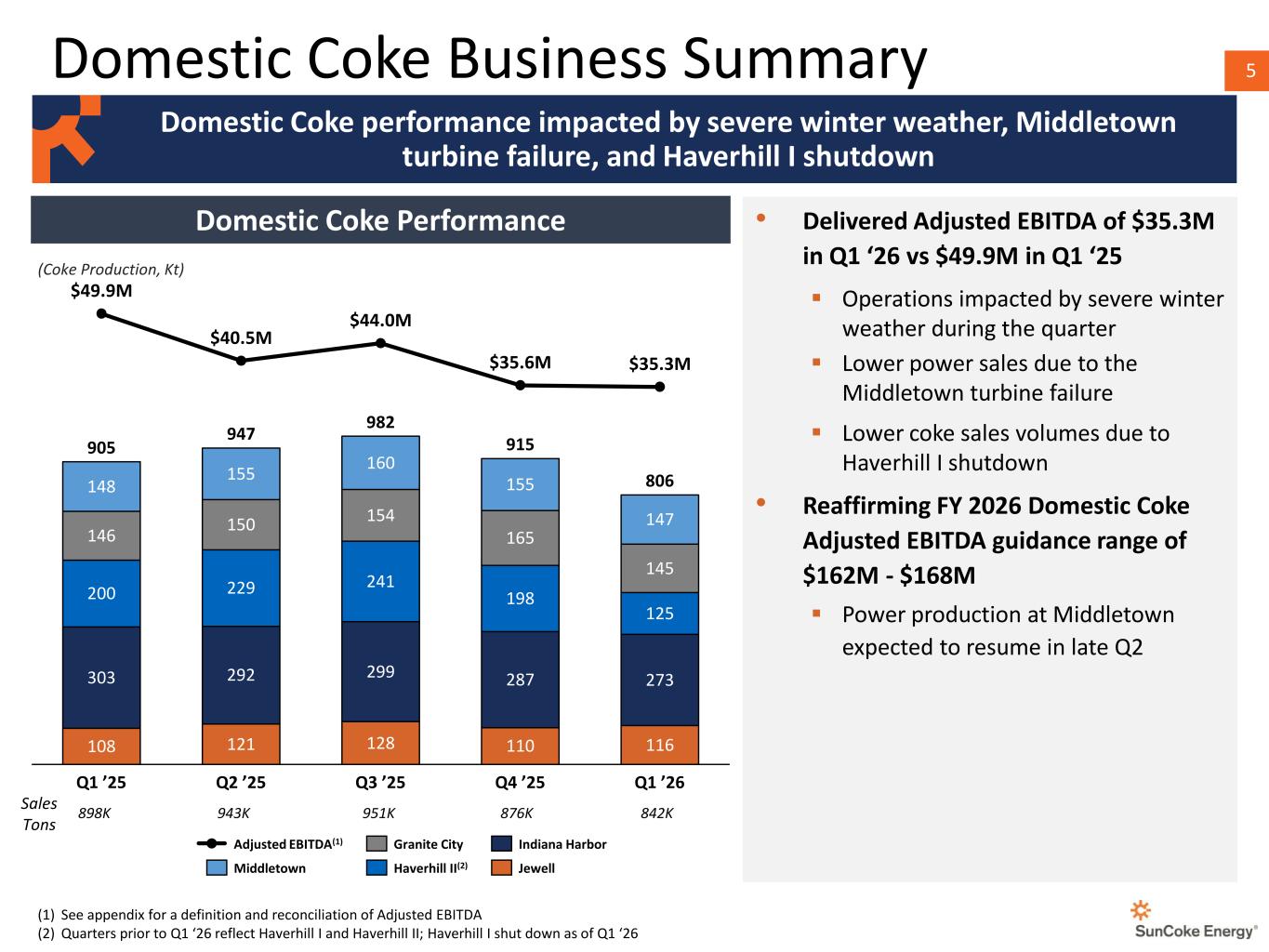

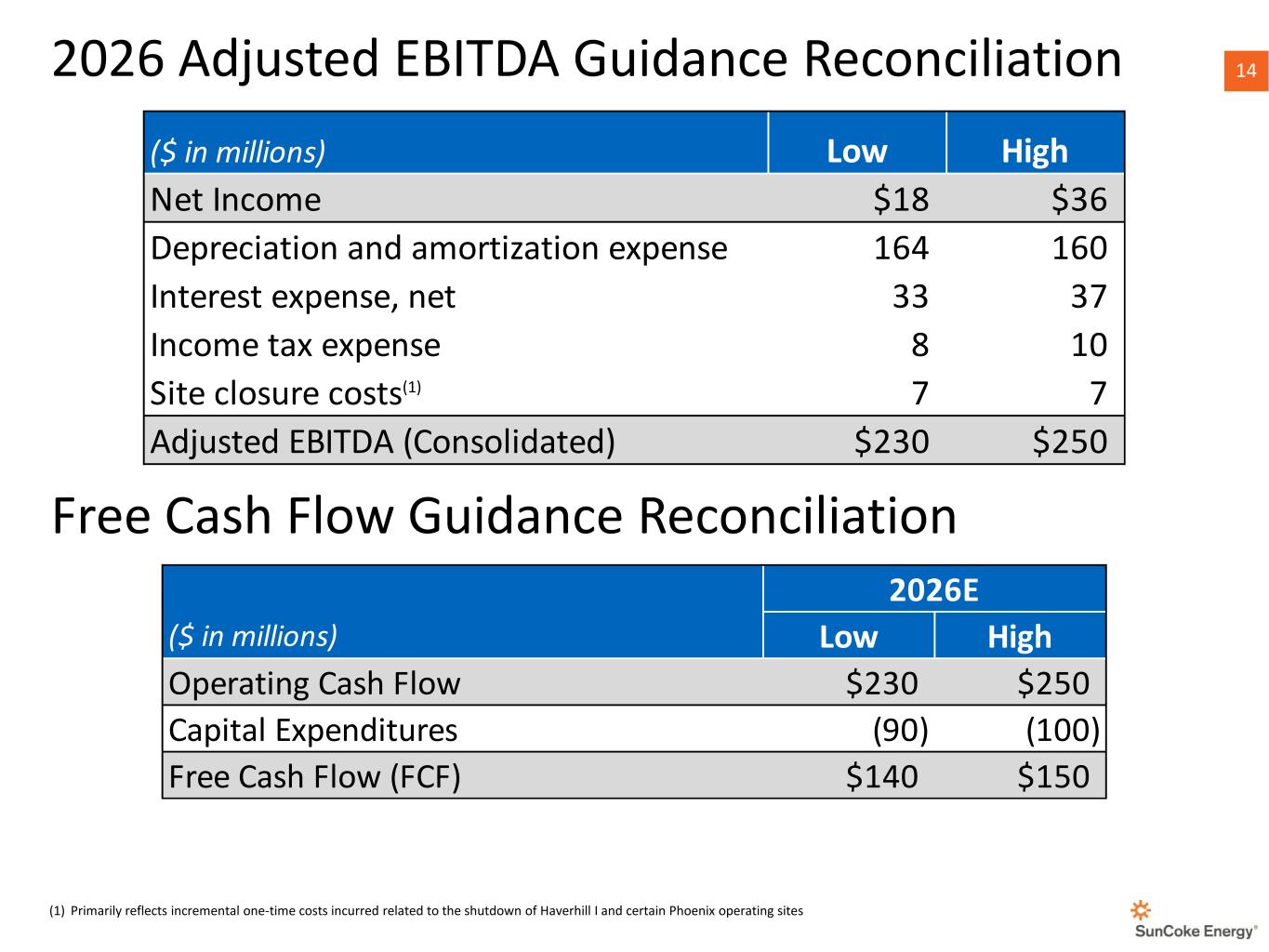

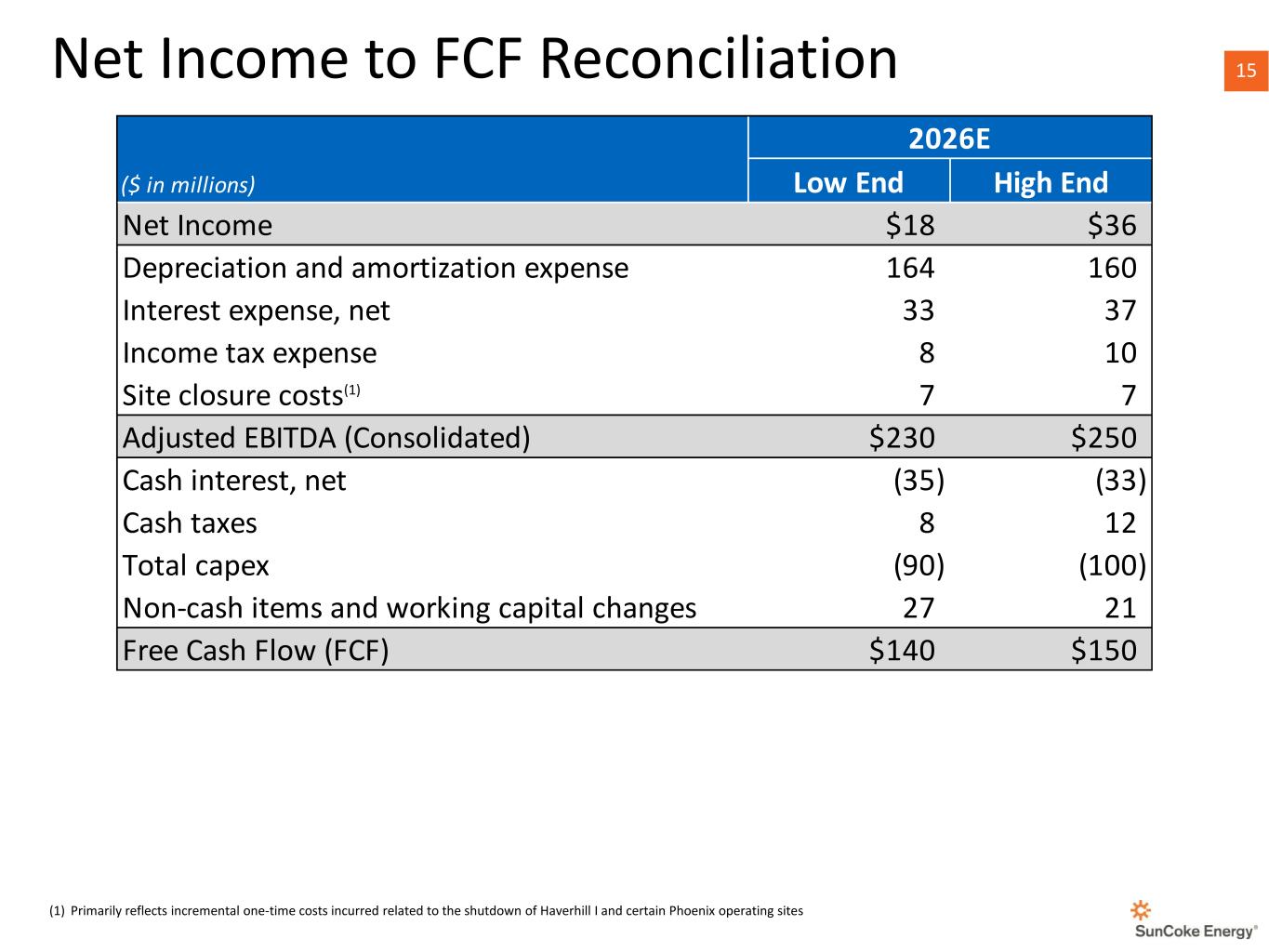

- Full-year 2026 guidance reaffirmed at $230–$250M consolidated, $162–$168M Domestic Coke, and $90–$100M Industrial Services Adjusted EBITDA

- 27th consecutive quarterly dividend of $0.12 per share declared

- Expect lost Q1 production to be made up in the balance of the year, with Middletown power production resuming late in Q2

- Net loss attributable to SXC of $4.4M ($0.05/diluted share) vs. income of $17.3M ($0.20) in the prior year period

- Consolidated Adjusted EBITDA declined to $56.5M from $59.8M YoY

- Domestic Coke Adjusted EBITDA fell to $35.3M from $49.9M and Coke sales volumes dropped to 842,000 tons from 898,000 tons YoY

- Severe winter weather, the Middletown turbine failure, and the Haverhill 1 shutdown pressured Q1 results, with Middletown expected to have no power production through most of Q2

- Higher depreciation expense contributed to the YoY earnings decline

Guidance from the call

stated verbally on the call, extracted from the transcript| Metric | Period | Guided | Basis |

|---|---|---|---|

| Consolidated adjusted EBITDA Maintained | full year 2026 | $230M – $250M | Non-GAAP |

| Domestic coke adjusted EBITDA Maintained | full-year | $162M – $168M | Non-GAAP |

Good day, and welcome to the Q1-2026 Suncoke Energy, Inc. Earnings Conference Call. All participants will be in a listen-only mode. Should you need assistance, please signal a conference specialist by pressing the star key followed by zero. After today's presentation, there will be an opportunity to ask questions. To ask a question, you may press star, then one on a touch-tone phone. To withdraw your question, please press star, and then two. Please note, this event is being recorded. I would now like to turn the conference over to Sharon Doyle, IR Manager. Please go ahead.

Thanks, Nick. Good morning, and thank you for joining us to discuss Suncoke Energy's first quarter 2026 results. With me today are Catherine Gates, President and Chief Executive Officer, and Shantanu Agrawal, Senior Vice President and Chief Financial Officer. This conference call is being webcast live on the Investor Relations section of our website, and a replay will be available later today. Following management's prepared remarks, we will open the call for Q&A. If we do not get to your questions on the call today, please feel free to reach out to our investor relations team. Before I turn things over to Catherine, let me remind you that the various remarks we make on today's call regarding future expectations constitute forward-looking statements. The cautionary language regarding forward-looking statements in our SEC filings apply to the remarks we make today. These documents are available on our website as are reconciliations to non-GAAP financial measures discussed on today's call. With that, I'll now turn things over to Catherine.

Thanks, Sharon. Good morning, and thank you for joining us on today's call. This morning, we announced Suncoke Energy's first quarter results. I want to share a few highlights before turning it over to Shantanu to discuss the results in detail. We're pleased with our performance in the first quarter, delivering consolidated adjusted EBITDA of $56.5 million, reflecting strong operational execution. Our industrial services business performed well during the quarter with sequential improvement in terminals handling volumes and with Phoenix performing to our expectations. As discussed on our fourth quarter 2025 earnings call, our co-plants were impacted by severe winter weather and the Middletown turbine failure. Earlier today, we also announced a quarterly dividend of $0.12 per share, payable to shareholders on June 2, 2026. This is our 27th consecutive quarter announcing a dividend. While the dividend is evaluated on a quarterly basis by our board, we expect the dividend to continue as part of our well-balanced capital allocation strategy. We had strong operating cash flow generation of $72.7 million and ended the quarter with ample liquidity of $262 million. As previously discussed, we are running at full capacity and sold out for the full year. With the continued seamless integration of Phoenix, the resumption of power production at Middletown, and continued strong operational execution, we are confident we will achieve full year 2026 consolidated adjusted EBITDA within our guidance range of $230 to $250 million. With that, I'll turn it over to Shantanu to review our first quarter earnings in detail. Shantanu. Thanks, Catherine. Turning to slide four. Net loss

attributable to Sun Coke was $0.05 per share in the first quarter of 2026, down $0.25 versus the prior year period. The decrease was primarily driven by higher depreciation expense, the shutdown of our Haverhill One Coke-making facility, severe winter weather, and the lower power sales due to Middletown turbine failure, partially offset by lower income tax expense. Consolidated adjusted EBITDA for the first quarter of 2026 was $56.5 million compared to $59.8 million in the prior year period. The decrease in adjusted EBITDA was primarily driven by the impact of severe winter weather on our coke operations, lower power sales from the Middletown turbine failure, and the shutdown of Everhill 1, mostly offset by the addition of Phoenix. Moving to slide 5 to discuss our domestic Coke business performance in detail. First quarter domestic Coke adjusted EBITDA was $35.3 million and Coke sales volumes were 842,000 tons compared to $49.9 million and 898,000 tons in the prior year period. The decrease in adjusted EBITDA was primarily driven by severe winter weather impacting our operations, lower power sales due to the turbine failure at Middletown, and lower Coke sales volume due to the Haverhill 1 shutdown. While we experienced a slow start to the year, we are already seeing improvement in our Coke operations in the second quarter with more favorable weather conditions. We are confident we'll make up the lost production from the first quarter during the balance of the year. Additionally, we are expecting power production to resume at Middletown late in the second quarter. We are reaffirming our full-year domestic coke adjusted EBITDA guidance of $162 to $168 million. Now, moving on to slide 6 to discuss our industrial services results. Our industrial services segment generated $26.2 million of adjusted EBITDA in the first quarter of 2026, compared to $13.7 million in the prior year period. The increase in adjusted EBITDA was primarily driven by the addition of Phoenix results, partially offset by a change in mix of products handled at the terminals. First quarter, total terminal handling volumes were 5.6 million tons, representing a substantial improvement versus the fourth quarter of 2025. Steel customer volumes serviced were 5.6 million tons in the first quarter. We expect our industrial services segment to continue delivering strong results throughout the balance of the year and are reaffirming our full year 2026 industrial services adjusted EBITDA guidance range of $90 to $100 million. Now, turning to slide 7 to discuss our liquidity position for Q1, SunCoke ended the first quarter with a cash balance of $104.4 million and revolver availability of $158 million, representing ample liquidity of $262 million. We generated strong operating cash flow of $72.7 million during the quarter, mainly driven by a reduction in coal and coke inventory, and used $26 million for debt paydown. We spent $17 million on CapEx and paid $10.7 million in dividends at the rate of $0.12 per share this quarter. SunCoke has a strong track record of generating steady free cash flow, and we expect the trend to continue throughout the year. As Catherine mentioned earlier, we intend to continue utilizing our free cash flow to pay down debt as well as to reward our long-term shareholders via dividends, which is reviewed and approved on a quarterly basis by our board of directors. With that, I'll turn it back over to Catherine.

Thanks, Shantanu. Wrapping up on slide eight, as always, safety is our first priority. Our excellent safety performance in 2025 has continued into the beginning of 2026, and the team remains committed to maintaining strong safety and environmental performance throughout the year. Robust safety and environmental standards set SunCoke apart and are central to our reliable delivery of high-quality Coke and industrial services. We continue to be confident in our operations for 2026 with our profitable, long-term coke business underpinned by the three pillars of Indiana Harbor, Middletown, and Jewel Foundry, which have consistently delivered excellent performance and results. With our Haverhill II and Granite City coke-making contracts extended and all spot blasts and foundry coke sales finalized, we're sold out for the full year. We also maintain a positive outlook for our industrial services segment. 2026 will benefit from a full year of Phoenix adjusted EBITDA contribution and improvement in market conditions at our terminals. Our efforts will continue on the seamless integration of Phoenix, maintaining the strength of our core businesses, as well as assessing new growth opportunities across all of our businesses. As always, we take a balanced yet opportunistic approach to capital allocation. On the back of our steady and healthy cash flow generation, our focus will remain on utilizing our free cash flow to support our capital allocation priorities. We will use excess cash to continue paying down our revolver balance with the goal of gross leverage below three times by the end of 2026 and beyond. We also plan to continue returning capital via the quarterly dividend as approved by our board, which has always been well-received by our long-term shareholders. We continuously evaluate the capital needs of the business, our capital structure, and the need to reward our shareholders, and will make capital allocation decisions accordingly. We are committed to maximizing value for all of our stakeholders, which means operating and investing in our assets in the best and most efficient way possible. Overall, we see the strong fundamentals of our business and expect our 2026 results to be reflective of that. We are confident that we will be able to deliver full-year consolidated adjusted EBITDA within our guidance range of $230 to $250 million. With that, let's go ahead and open up the call for Q&A.

Thank you. We will now begin the question and answer session. To ask a question, you may press star, then 1 on your touchstone phone. If you are using a speakerphone, please pick up your handset before pressing the keys. If at any time your question has been addressed and you would like to withdraw your question, please press star and then two. At this time, we'll pause for a moment to assemble the roster. The first question will come from Nathan Martin with the Benchmark Company. Please go ahead.

Thanks, Operator Gworn, everyone. Just to start out, within the domestic Coke segment, adjusted EBITDA per ton, I guess roughly $42, obviously below the $48 to $50 per ton for your guidance that you guys just reiterated. And what was the main driver of drivers there? You know, how much of that was lower power sales, maybe at Middletown? And then, you know, can you guys help us bridge kind of that four-year range as we move throughout the rest of the year?

Yeah, Nate, I mean, as we mentioned, you know, the two main factors of us performing, you know, lower versus kind of our full-year guidance is the winter weather impact to our operations and the Middletown turbine impact, right? And they were both very comparable. Right. And if you recall, when we gave out our Q, when we were in the Q4 2025 earnings call, we talked about that this quarter is roughly $10 million off versus kind of the run rate. So I think that still holds true from that perspective. And then, you know, looking forward, as we mentioned, the Middletown turbine is expected to be back in late Q2. So you will see that impact through majority of Q2 with no power production there. But then we should be able to make that back up in Q3 and Q4. So you should see a much significant improvement in Q3 and Q4 as the power production comes back up.

I appreciate that, Shanu. Is it fair to consider the middle talent impact in 2Q could be roughly half of that 10 million, so maybe 5 million headwind or so in the second quarter?

that's that's kind of in the ballpark yes okay great appreciate that um and then maybe shifting

to the industrial segments uh it looks like revenues revenues are flat to actually slightly down quarter over quarter however you know just even that was actually up about what three three and a half million dollars so are there any cost savings or efficiency gains there we should think about driving this i know you guys previously called out potential opportunities to improve things within Phoenix, or maybe it's related to the improvements on the terminal side, just

any additional color would be helpful there. Thanks. Yeah. So on the terminal side, you know, as we lined out, you know, you're comparing Q425 to Q126, right? And we are seeing, you know, significant improvement in the volumes that we are handling in terminals when we expect the kind of the market environment to continue and to continue to improve for the rest of the year. So we are, you know, very hopeful and kind of that kind of our plan reflects that the terminals will continue to improve and do well through the rest of the year. So there is improvement coming from that. And then on the Phoenix side, obviously, right, like kind of this is our second full quarter of running Phoenix under the Suncoke umbrella. And as we go through the remainder of the 2026, we expect to see some more of those synergies come through. There are some of the drag costs, right? Like we are implementing, you know, kind of the software, kind of merging them together. So there is some drag cost of that. But as you get through the rest of the 2026, you should see some cost improvement in Phoenix. And that is built in to our guidance for industrial segment.

Okay, got it. And then those costs, just jumping to SG&A for a second, was that kind of behind the increase there in the quarter? Was that the IT, I think, bonus expense items maybe you previously mentioned as well? And how should we think about SG&A kind of going forward?

So, you know, in 2025, you know, the accrual for the bonuses are different for 25 versus 26, given the performance of the company. And that is the main driver of the difference in SG&A.

Should we expect it to kind of repeat at that level, Shantanu, or will it kind of come back down a little bit from the first?

The Q1 2026 should be the run rate for the rest of the year.

Okay. Got it. But I'll leave it there, jump back in the queue. Appreciate the time.

Thanks, mate.

Again, if you have a question, please press star and then one. The next question will come from Henry Hurl with B. Riley Securities. Please go ahead.

Thank you, operator, and good morning, everyone. To start off, I wanted to ask, to what extent could your logistics terminals be a beneficiary of the Section 303 DPA determination on the coal supply chains and export terminals? And then could you guys pursue potential DOD funding as well? Thanks.

Yeah, thanks for your question. I think as we look ahead, we see the market, as Shantanu said, improving throughout the year, and we've already seen that quarter over quarter. I don't think that those are going to be drivers to additional throughput necessarily. I mean, I think we'll have to see. But when we give our guidance with respect to industrial services and with respect to the performance of the terminal specifically, we really are looking at market conditions. And as we look back in time, there's been various regulatory initiatives over time. But at the end of the day, it really seems driven by demand primarily internationally for coal.

Got it. Thank you. And then are you guys able to share specifically what percent or what share of the volumes at CMT or thermal export tons?

So, Hendrik, going forward, you know, we like since it's one segment, the industrial services, we are not kind of breaking out. We are giving one number for our terminals and one number for like the Phoenix business, the steel customer volume service. But, you know, if you go back and look at historical data where we used to break out, the ratio should remain the same. That should kind of give you a good guidance on what those numbers are.

Got it. Thank you. And given the conflict in the Middle East over the past couple months, have you seen a kind of sizable increase in those export thermal tons? Would that be fair to say?

It's a good question. We are seeing certainly some higher pricing in the market, and that is leading to higher demand. And that is part of how we look at the market as getting stronger as we move forward throughout the year. We don't see any signs of that weakening. And so we've seen higher demand due to the higher prices. So, yes, there's definitely sort of a flow through from that conflict and the focus on coal in light of the challenges that we're seeing on the oil and gas side.

Got it. Thanks for the time, guys, and continue the best of luck.

Thank you.

This concludes our question and answer session. I would like to turn the conference back over to Catherine Gates for any closing remarks.

Thank you all again for joining us this morning and for your continued interest in SunCoke. Let's continue to work safely today and every day.

The conference has now concluded. Thank you for attending today's presentation. You may now disconnect.