Call highlights

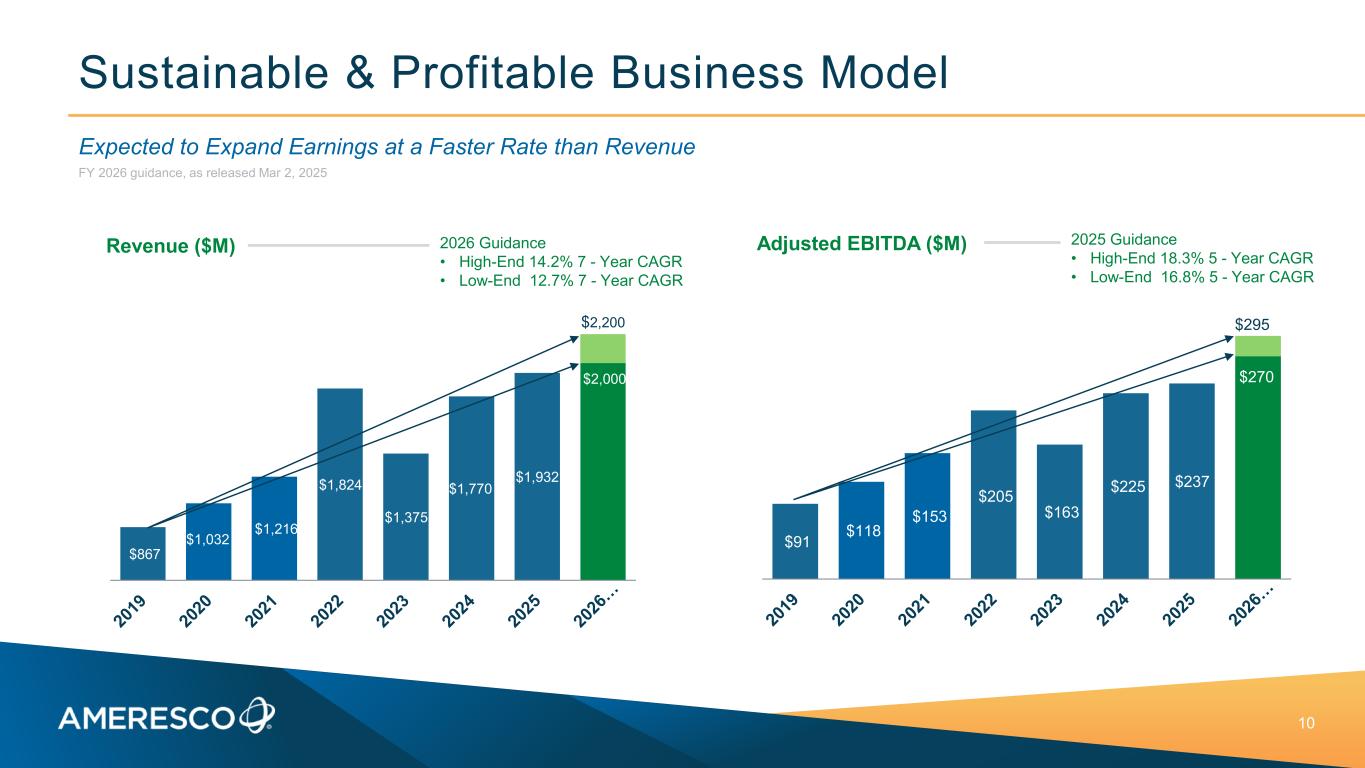

Ameresco delivered record Q4 revenue of $581 million (up 9% year-over-year) and full-year 2025 revenue of $1,932.1 million, reaching the mid-to-high end of guidance despite DOGE-related concerns and the six-week Q4 government shutdown, and is guiding to another year of strong profitable growth in 2026.

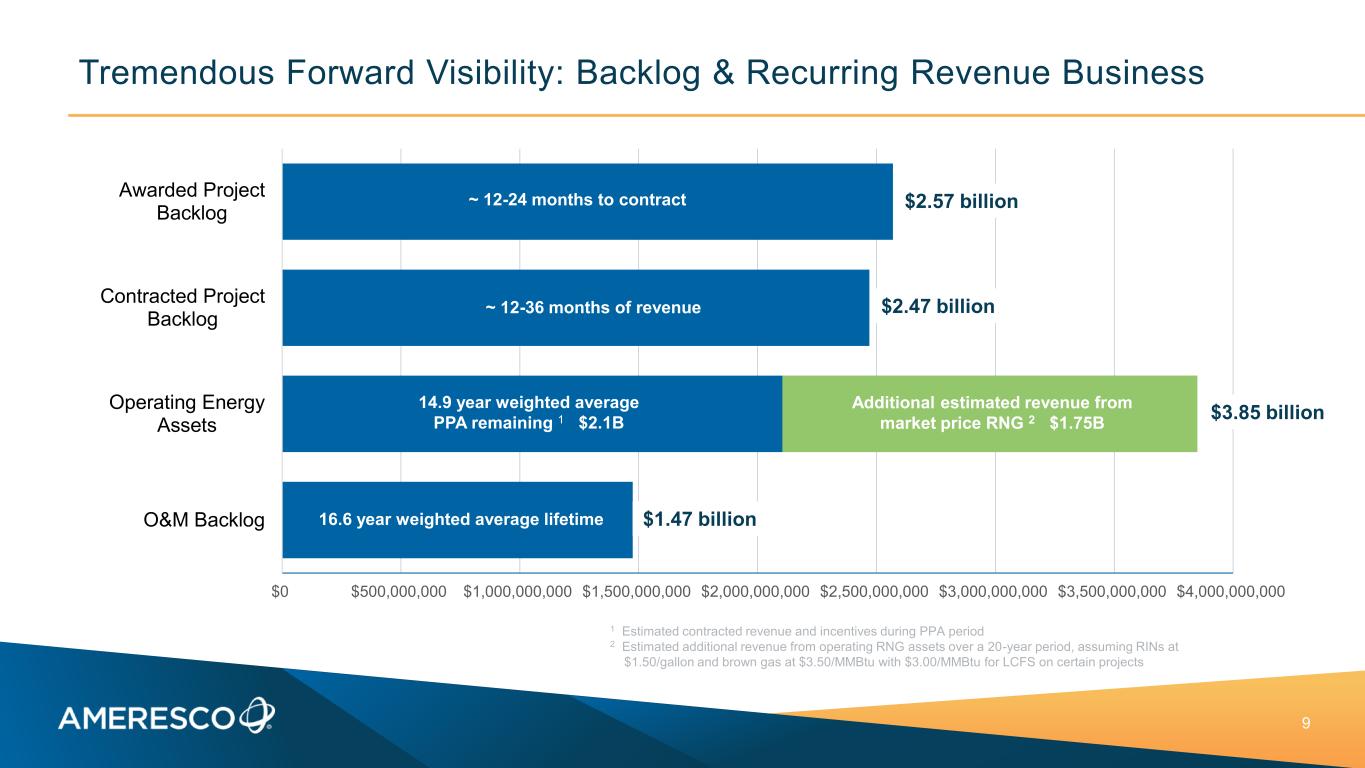

“When you combine our project backlog and the future revenue streams from our recurring O&M business and portfolio of operating energy assets, we have over $10 billion in long-term revenue visibility. We believe that level of visibility is a real strength in this challenging environment.”

“for 2026, we are guiding to approximately $2.1 billion of revenue and $283 million of adjusted EBITDA at the midpoints of our ranges, representing growth of 9% and 19% respectively. We expect to place approximately 100 to 120 megawatts of energy assets into service, including two RNG plants.”

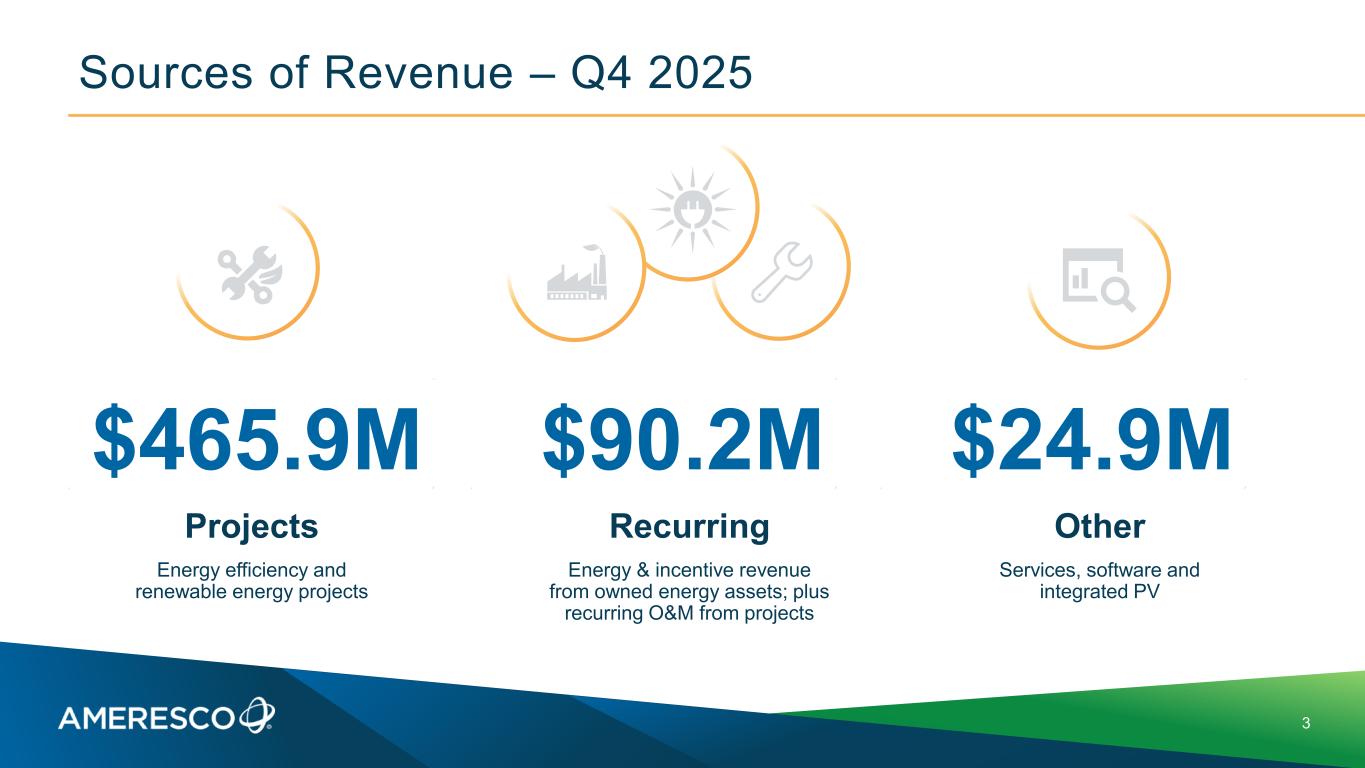

- Q4 revenue grew 9% year-over-year to a record $581 million, with growth across all three core business lines.

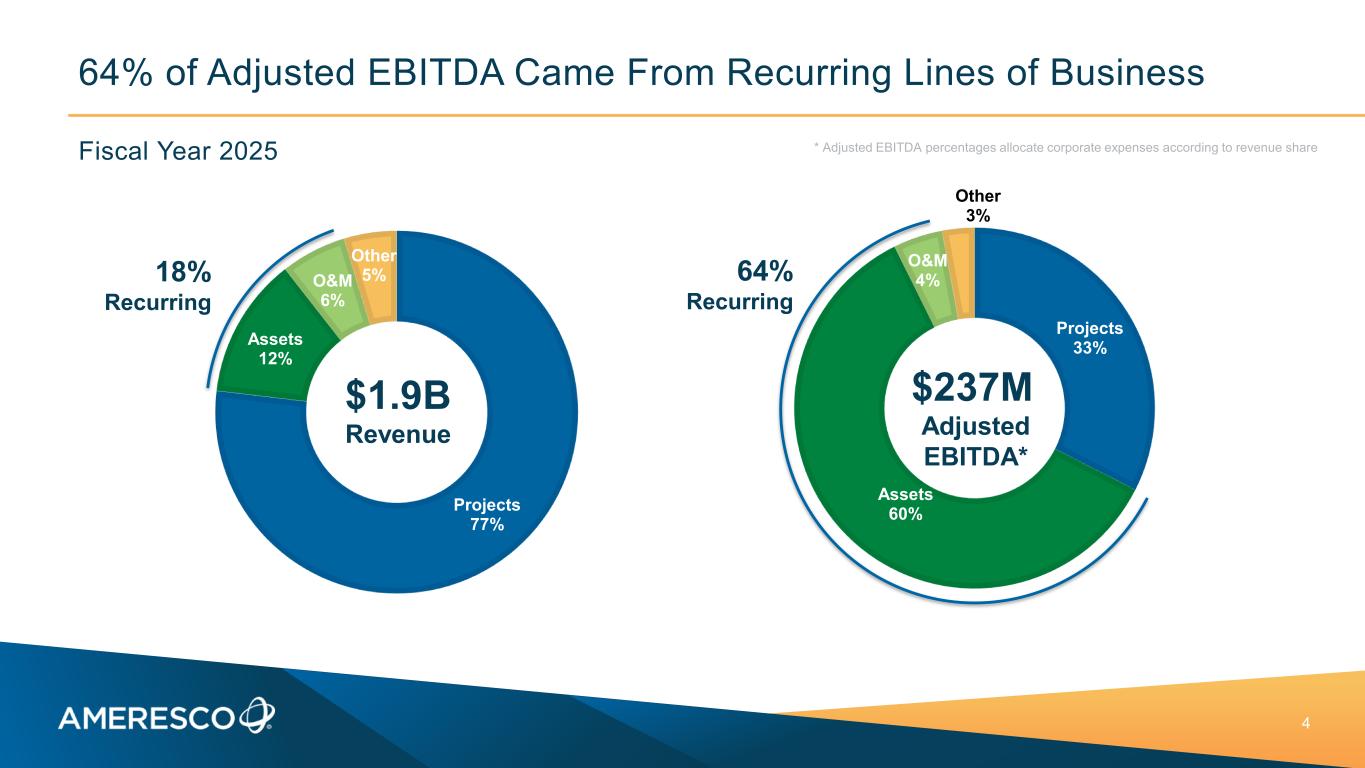

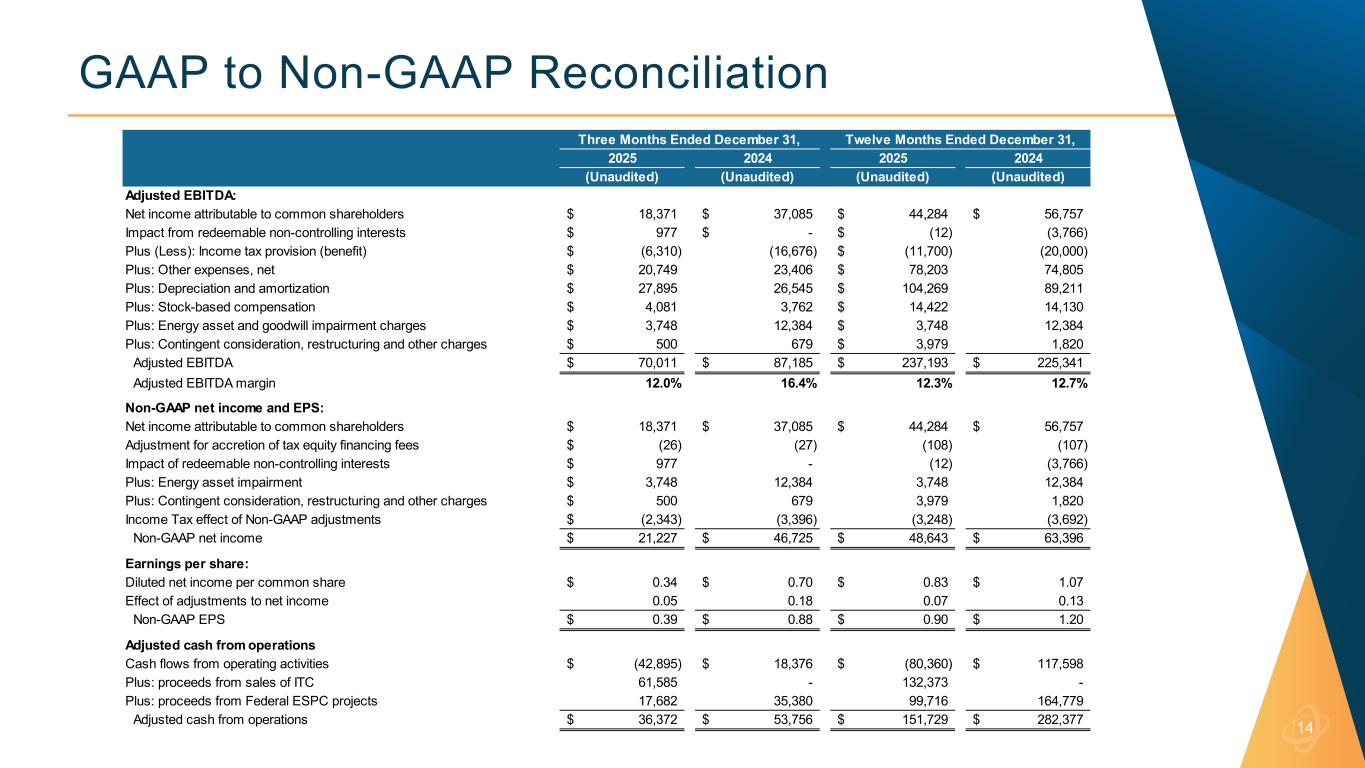

- Full-year revenue of $1,932.1 million, net income of $44.3 million, non-GAAP EPS of $0.90, and Adjusted EBITDA of $237.2 million reached the mid-to-high end of annual guidance.

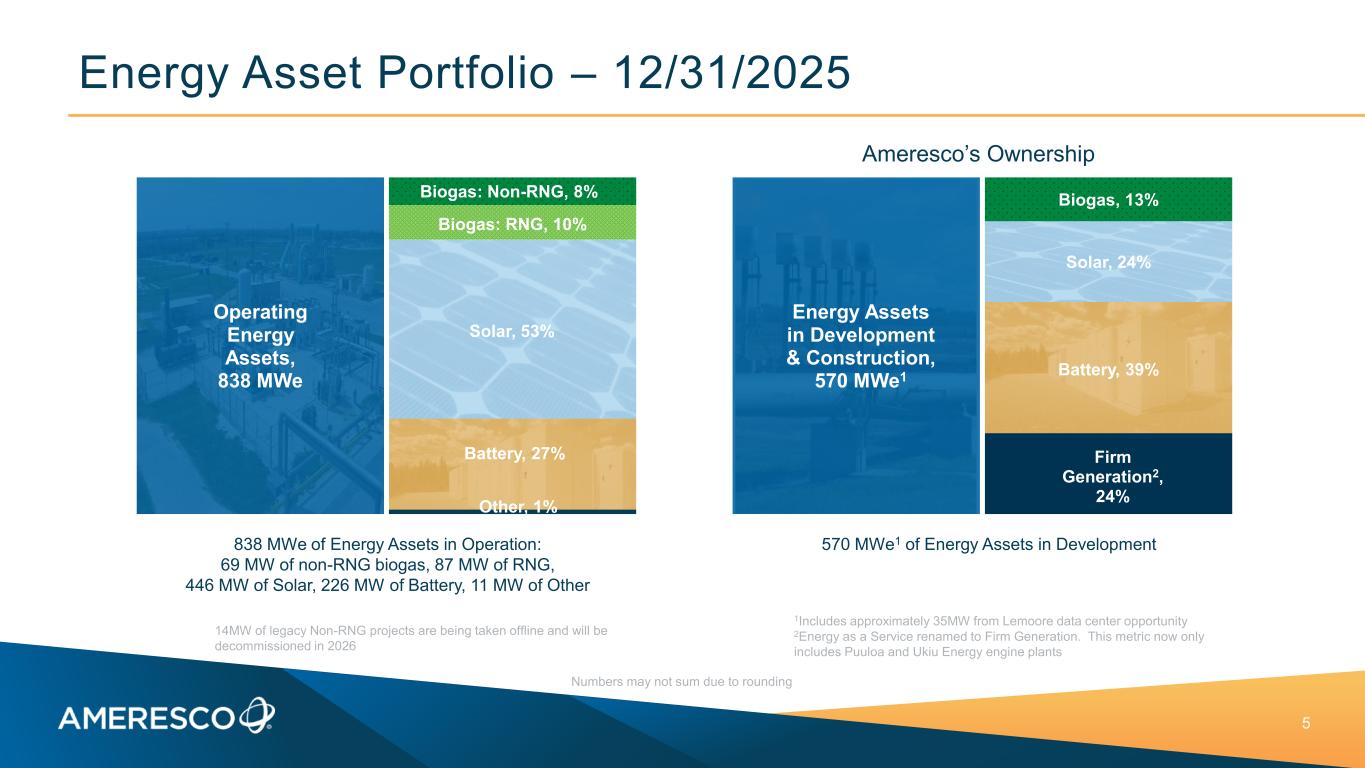

- Energy asset placements of 121 MWe in 2025 exceeded guidance, bringing total operating assets to 838 MWe, with 87 MWe placed in Q4 including the 9th RNG facility and the Nucor BESS.

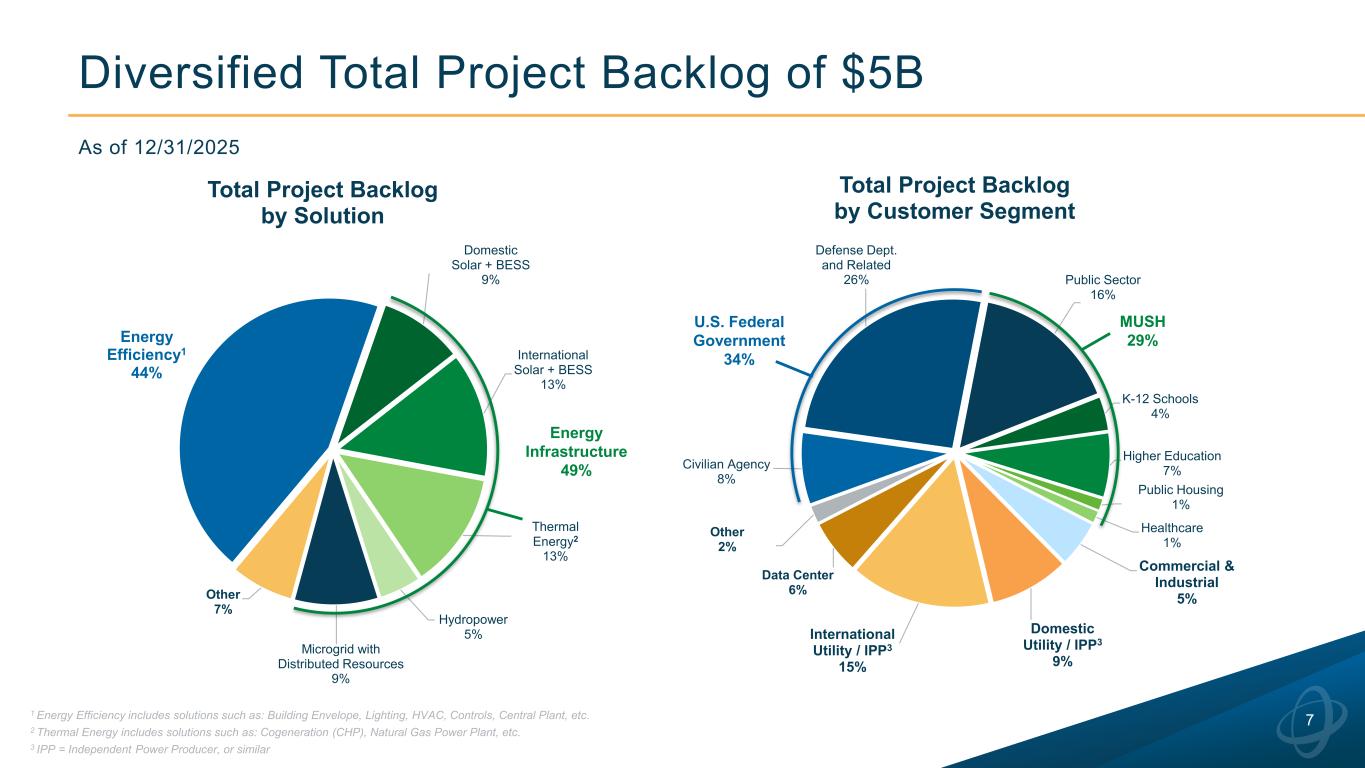

- Total project backlog exceeded $5 billion, with awarded backlog up 13% year-over-year to over $2.5 billion.

- Total revenue visibility exceeds $10 billion when project backlog is combined with recurring Energy Asset and O&M businesses (O&M backlog ~$1.5 billion).

- European operations delivered strong growth, including recent large wins in Romania via the 51%-owned Greek joint venture, providing geographic diversification.

- Q4 Energy Assets segment posted a net loss of $3.558 million versus $8.899 million of net income in Q4 2024.

- Results were achieved amid concerns about potential Department of Government Efficiency actions and the six-week federal government shutdown in Q4.

- Quarterly operating cash flow was described as lumpy, with tighter working capital tied to milestone-based large projects; CFO indicated working capital should normalize across the year.

- The 8-K notes results were achieved despite a 'dynamic business environment,' and CFO cited potential project execution delays (referencing weather) as a risk to hitting the top end of 2026 guidance.

Good afternoon, ladies and gentlemen, and thank you for standing by. My name is Kelvin, and I will be your conference operator today. At this time, I would like to welcome everyone to MRESCO Inc.'s Q4 2025 Earnings Conference Call. All lines have been placed on mute to prevent any background noise. After the speaker's remarks, there will be a question and answer session. If you would like to ask a question during this time, simply press star, followed by the number 1 on your telephone keypad. If you would like to withdraw your question, please press star 1 again. Thank you. I would now like to turn the call over to Lila Villan, Chief Marketing Officer. Please go ahead.

Thank you, Kelvin, and good afternoon, everyone. We appreciate you joining us for today's call. Our speakers on the call today will be George Saccolaris, Amoresco's Chairman and Chief Executive Officer, and Mark Chiplock, Chief Financial Officer. In addition, Josh Barabow, our Chief Investment Officer, will be available during Q&A to help answer questions. Before I turn the call over to George, I would like to make a brief statement regarding forward-looking remarks. Today's earnings materials contain forward-looking statements, including statements regarding our expectations. All forward-looking statements are subject to risks and uncertainties. Please refer to today's earnings materials, the safe harbor language on slide two of our supplemental information, and our SEC filings for a discussion of the major risk factors that could cause our actual results to differ from those in our forward-looking statements. In addition, we use several non-GAAP measures when presenting our financial results. We have included the reconciliations of these measures and additional information in are supplemental slides that were posted to our website. Please note that all comparisons that we will be discussing today are on a year-over-year basis, unless otherwise noted. I will now turn the call over to George. George?

Thank you, Lila, and good afternoon, everyone. I am pleased to report that our fourth quarter results represented a great finish to a year of strong performance. with annual results reaching the mid-to-high end of our revenue and profit guidance. Excellent execution by the MRSCO team, together with the recurring revenue contributions from our energy assets and O&M businesses, were key drivers to our success. And this success was achieved even amid concerns surrounding potential Department of Government Efficiency Actions early in the year, and the six-week federal government shutdown in the fourth quarter. Importantly, our results were broad-based, with growth across all three of our core business lines, including strong growth from our European operations. And while our team continues to be laser-focused on contract execution, converting a record 1.5 billion dollars of project backlog into revenue this year we also saw excellent new business activity including meaningful project scope increases in our federal backlog it's helped to drive our total awarded backlog to over 2.5 billion dollars up 13 from last year Also, Europe was a strong contributor this year and represents a real success story. We first entered Europe over 10 years ago with a small acquisition of a UK-based energy consulting firm. But more recently, we have focused on expanding our business in continental Europe. As doing business in Europe requires a localized presence, our European growth strategy has been driven by opportunistic acquisitions such as Italy-based anarchists and partnerships in various target countries. We focus on smaller opportunities and then use the power of M-R-ESCO, our technology and process know-how and financial resources to accelerate and drive growth. Geographically, we have focused on Southern and Eastern Europe, areas which are experiencing higher rates of growth with fewer large domestic and transit competitors. Our 51% owned joint venture with a Greek-based Ronell Group is an excellent example of this approach. The joint venture was created on April of 2023 to pursue utility-scale PV and battery energy storage opportunities. After great success in Greece, the joint venture has since expanded this business, including a few recent large wins in Romania. We expect to continue to grow in Europe organically and through opportunistic acquisitions and partnerships. Europe not only represents an excellent growth market, but it also provides important diversification, as demand drivers in Europe are not subject to the same U.S. political and policy variables. We look forward to providing additional updates on this important aspect of our company's future growth. Before I hand the call over to Mark to cover our results and outlook, I would like to briefly highlight the number of key industry growth drivers and how we believe MRSCO can benefit from them for years to come. The first key driver is the rapidly growing demand for electricity. This has been driven by the electrification of built-ins and transportation, the power needs for many high-technology industries, and the growth in industrial manufacturing. Overall, electricity demand is expected to increase by 78% by 2050, needing 80 gigawatts of capacity added every year for the next 20 years. Meeting this demand will be a significant challenge to our aging system of centralized generation and the associated transmission infrastructure. As a result, many of our customers are choosing to install on-site, behind the mirror generation, and storage solutions. Ameresco has been providing a portfolio of these solutions since the founding of the company, including not only solar, but also battery energy storage systems, natural gas engines, gas turbines, fuel cells, and microgrids. We are also exploring the next generation of energy infrastructure technologies, like micro and small modular nuclear reactors. These power and storage solutions will be a key element to supporting ongoing global energy demand needs. Second, increasing energy costs is another key industry driver for which Moresco is well-positioned to benefit from, particularly through our built-in efficiency solutions. As electricity prices rise, energy efficiency investments made by our customers deliver faster payback and stronger returns. Energy efficiency is often the most economical solution for existing buildings. According to Frost & Sullivan, MRASCO is the nation's largest provider of energy efficiency services which represent nearly half of our current project backlog. Third, the increasing stress on the country's aging energy infrastructure from high demand and the critical natural oil and interruptible power is quickly driving a growing demand for resilient energy solutions. High 9th power is not only a must-have for critical high-technology industries, such as data centers, but also for industrial customers, where even limited downtime can have significant cost and production consequences. Advancements in lithium battery technologies, as well as rapidly declining costs, have driven tremendous growth in the use of battery energy storage solutions over the last five years. And Maresco has a very long track record of providing resilient solutions at military bases across the country, keeping their mission-critical functions running in case of grid power interruptions, and that's making us a go-to provider across all end markets. As you can see, we believe Amoresco is very well positioned to benefit from these long-term trends that should help drive profitable growth for many more years to come. Now, I would like to turn the call over to Mark to provide financial commentary on this quarter's excellent results, as well as provide our outlook for 2026. Mark?

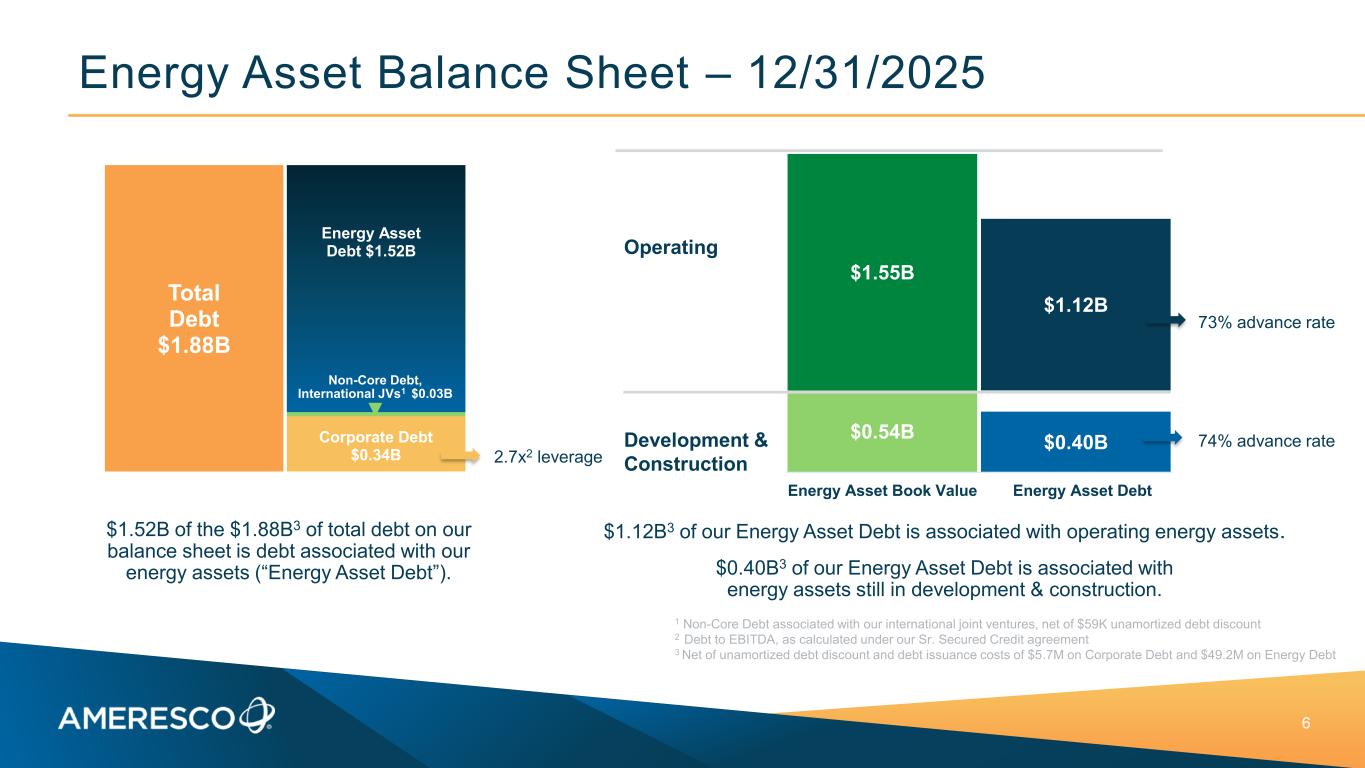

Thank you, George. This was another strong quarter for Amoresco. in a year defined by consistent execution. Despite the Q4 government shutdown, we delivered record quarterly revenue of $581 million, up 9% year-over-year, with growth across all of our core business lines. These results underscore the durability of our diversified business model and the disciplined execution of our team. Project's revenue grew 11%, driven by strong backlog conversion and continued solid performance from our European joint venture with CINAHL. While we converted a significant amount of backlog in the quarter, we still maintained our total project backlog above $5 billion, reflecting sustained demand for our comprehensive energy infrastructure solutions. Energy asset revenue increased 5%, driven by the growth of our operating asset portfolio. We placed 87 megawatts into operation during the quarter, including our ninth RNG facility, a large military solar plus storage installation, and the Nucor BEST system. For the year, we exceeded our guidance, placing 121 megawatts of energy assets into operations, bringing our total operating assets to 838 megawatts. We also added 30 megawatts to our energy assets in development. continuing to balance backfilling our energy asset pipeline with our disciplined financial approach to new asset opportunities. Our recurring O&M revenue increased 11%, reflecting continued attachment of long-term service agreements to our completed project work. Our long-term O&M revenue backlog now stands at approximately $1.5 billion. When you combine our project backlog and the future revenue streams from our recurring O&M business and portfolio of operating energy assets, we have over $10 billion in long-term revenue visibility. We believe that level of visibility is a real strength in this challenging environment. And finally, our other line of business, excluding the sale of our AEG business at the end of 2024, delivered solid year-over-year results. Gross margin was 16.2%, up both sequentially and year-over-year. This reflects continued improvement in project mix, higher quality backlog, and disciplined cost management. Operating expenses in the fourth quarter were $50.9 million, compared to $47.8 million last year. The increase reflects targeted investments in people, project development, and execution support as we manage revenue growth, more complex infrastructure projects, and continue replenishing backlog. Importantly, operating expenses are growing materially slower than gross profit, so we're still preserving operating leverage in the business. As we move into 2026, we expect to continue investing prudently to support demand and drive growth, which is reflected in our guidance. Net income attributable to common shareholders was $18.4 million, dollars, with GAAP EPS of 34 cents and non-GAAP EPS at 39 cents. Adjusted EBITDA was 70 million dollars, resulting in a margin of 12 percent. As a reminder, last year's fourth quarter, adjusted EBITDA results included the 38 million dollar gain on the sale of AEG. Turning to our balance sheet, we ended the quarter with approximately 72 million dollars in cash and corporate debt of approximately $300 million. Leverage under our senior secured facility was 2.7 times, comfortably below the covenant level of 3.5 times. During the quarter, we secured approximately $175 million in new project financing commitments. Adjusted cash flow from operations was approximately $36 million, including proceeds from ITC sales. On a longer-term basis, our eight-quarter rolling average adjusted cash from operations was approximately $54 million. Now let me move on to our 2026 guidance. We entered the year with strong business momentum and visibility supported by continued strength across our end markets. Increased industry demand combined with the recurring revenue from our growing energy asset and O&M businesses provides clear visibility into another year of strong growth. As detailed in our press release, for 2026, we are guiding to approximately $2.1 billion of revenue and $283 million of adjusted EBITDA at the midpoints of our ranges, representing growth of 9% and 19% respectively. We expect to place approximately 100 to 120 megawatts of energy assets into service, including two RNG plants. For some quarterly shaping, the cadence of the year should follow our historical seasonal pattern, with a heavier weighting towards the second half. We expect revenues in the second half of the year to represent approximately 60% of our total revenue for 2026. This is consistent with our performance from the past couple of years. As we look to the first quarter, which is seasonally our lowest revenue quarter, we expect revenue and adjusted EBITDA to be generally consistent with Q1 of last year. The quarter reflects normal project timing and the recent severe weather that has impacted execution across several regions. As noted in the earnings release, Q1 EPS is expected to be lower year over year, primarily reflecting higher interest and depreciation expenses from our growing energy asset portfolio, as well as continued investment as we scale the business. Before closing on guidance, I want to briefly clarify how certain structural items impact both adjusted EBITDA and EPS. As George mentioned, we operate certain parts of our business through joint venture structures, including our Senel JV in Europe. Where we have control, we consolidate 100% of revenue and expenses. However, a portion of both adjusted EBITDA and net income is attributable to our JV partners and reflected as non-controlling interest. As a result, the adjusted EBITDA and EPS we report reflect only Amoresco's ownership share of those consolidated entities. Given these factors have a significant impact on our results, we've provided estimated ranges for income attributable to non-controlling interest in our 2026 guidance as detailed in our press release. In summary, 2025 demonstrated the durability of our model. We delivered consistent growth, expanded backlog, improved margins, and maintained financial discipline. 2026 is shaping up to be another year of sustained, profitable growth for the company as we believe we can continue to benefit from the many positive secular trends driving demand for our energy solutions. Now I'd like to turn the call back to George for closing comments. Thank you, Mark.

As Mark mentioned, during 2026, we will be building on our excellent momentum from 2025 to deliver another year of strong, profitable growth. Our highly differentiated portfolio of energy infrastructure and built-in efficiency solutions are well aligned with customer demand. Over our 26-year history, Moresco has proven to be one of the most consistent providers of these solutions. We are making targeted investments this year as we focus on technical innovation and drive long-term growth. As we have here today, we are very excited about our growth of prospects for 2026 and beyond. We look forward to seeing many of you at upcoming meetings and conferences. In closing, I would like to once again thank our employees, customers, and stakeholders for our great success in 2025 and for their continued support in 2026. Operator, we would like to open the call to question.

Ladies and gentlemen, we will now begin the question and answer session. As a reminder, to ask a question, please press the star button, followed by the number one on your telephone keypad. If you would like to withdraw your question, please press star one again.

One moment, please, for your first question.

Your first question comes from the line of Noreke of Oppenheimer. Please go ahead.

There was a lot of anticipation there. Thanks for taking the questions. I guess, you know, I know you don't formally guide to the segments in the Outlook, but maybe just some shaping on energy assets as contemplating the guide. You know, the 121 megawatts placed in service did exceed. So how do we think about the revenue trajectory there and kind of the margin profile? It seems like it should be a nice step up.

Josh, we'll get it. So I think as in previous years, the majority of the assets placed in service will kind of be towards the middle to the back half of the year. That's just kind of how things work with interconnection queues and development cycle, heavy construction in the summer months, et cetera.

And so that will generally look like this year.

This year was very heavily Q4 weighted, I think 80 plus megawatts placed in service. So it may not look quite like that, but certainly more back half and middle loaded than linear. In terms of the margin contributions, really no reason to believe that the margins are any different per segment, battery, gas or solar, as they are historically. And the mix is about the same. We've kind of given you the rough mix of what we expect to place this year. So and as you know, most of the assets we placed in service in any given year don't meaningfully contribute that year. It takes sort of a little while to ramp up to get commissioned and then to and then the real the real contribution is the following year. So this year has a lot of the impacts of the assets we place in service in 2025, especially because it was back half loaded, much like the 2026 assets placed in service. We'll have more of a meaningful impact on our 27 numbers, which we haven't provided yet.

Yep. Yep. Very clear. And then I think you mentioned the prepared remarks, Mark, around, you know, kind of the first quarter shaping. You mentioned weather had an impact. Obviously, we all experienced firsthand, at least most of us, that weather. So not a huge surprise, but can you maybe comment on what that meant for, you know, just some of the project work and how you think about, you know, the sort of sequencing of, you know, getting rid of some of the associated labor inefficiencies and the like so that that flows a little bit better into Q in the back half?

Yeah, I mean, you know, the weather, again, as you can imagine, impacted our ability to access certain sites. It impacted our assets. But, you know, so it's really just impacting the timing, you know, the cadence of conversion. And, you know, we expect to see, certainly on the project side, that revenue to come in, you know, in Q2 as we get kind of on the other side of it. But, yeah, I mean, it was, you know, we always try to look at Q1 with the best visibility we have coming out of backlog. You know, this was unusual just given how severe the weather was. But, again, we feel pretty good that that is just timing and, you know, we'll see that revenue come back in as we get out, you know, outside of Q1 later into the year.

If I might add a little bit there, Noah, we had the freeze-up on three of our assets, you know, the renewable assets, and that's not really recoverable. But we have taken all that into account for our guidance for the year and the numbers for the first work.

Super helpful, George and Mark. I'll turn it over.

Thanks, Noah. Thank you.

Your next question comes from the line of George Giannarikas of Canecker Genuity. Please go ahead.

Hi, everyone. Thank you for taking the questions.

Hi there. I'd like to focus a little bit on Europe and the momentum you're seeing now. In order to scale further, do you expect to do it organically, or are you looking at maybe adding acquisitions to bolster your scale?

like i said in my commentary we are looking for a creative acquisition strategically located and we'd be very opportunistic in that regard and partnerships and expanding uh the partnership that partnership that we have with sonel and as pointed out we had great great success up in romania and we are looking at a couple other countries working with them and that the samaria that come out and we're planning to go ahead and go after that particular business with that entity but as i said though the growth in europe especially on solar and the next one wave that's coming the battery storage because they're those countries they have so much solar and we're in installations and that uh and we are well positioned to take good advantage of that so So we're looking at very good growth opportunities in Europe. And, of course, we don't have to put up with the U.S. political things that are going on over here. It's a great diversity for us, diversification.

Thank you. And maybe as a follow-up, just to ask a little bit about recent momentum in data centers. You specifically mentioned momentum in behind the meter. Any update on what you're seeing in the data center market?

Look, we're getting more requests than we can handle. Once we announce really more data center, and of course, we have, I would say, a little bit of strategic advantage of the other competitors. A, because we can put the package together and provide high, nice power for the data centers. Otherwise, they might have gas turbines or it might need battery storage. And the micro-greeter, we have a company, we have been doing that for a long time. And... We have a great, great pipeline. That's all I can say. But as you know, we're a little bit conservative when we announce those particular projects. But we think it's going to be a great, great contributor for us down a little bit this year and much more down the next couple of years.

Yeah, maybe what I'll just add to that, you know, when we think about the timing of when those opportunities can start to come into backlog, you know, we're going to really maintain some strong discipline and risk management as we look at those projects. You know, there's a number of gating items that we need to make sure are de-risk, like engineering, permitting, equipment sourcing, financing, you know, commercial structuring. So, a lot goes into making sure that those opportunities are real, and I think that's the approach we've been taking in bringing these assets or bringing these projects into the backlog. So, as George said, pipeline is strong, but conversion timing is going to reflect, you know, how well we can de-risk some of these gating items.

Thank you.

Your next question comes from the line of Ben Calo of Baird.

Please go ahead.

Hey, good evening, guys. Congrats on the results. Just maybe following on, I know that you had, you know, you put in a very high, if not record number of assets in the service in Q4. Just on timing of adding, you know, new products to backlog, you know, following on George's last question with data center, when should we expect to, you know, kind of get some of this stuff in the backlog? And then my second question is just around, you know, any kind of tightness in labor, equipment, or other that you'd like to call out that are impacting kind of your speed, you know, to market here? Thank you, guys.

I think, as George mentioned, you know, the pipeline is really strong for, you know, these behind-the-meter data center load opportunities. We're really trying to maintain some strong discipline, you know, how we manage these projects from a risk management perspective. You know, there's a lot of gating items, you know, that you need to go through from engineering, you know, or permitting, how we source the equipment. You know, we obviously need to work out commercial terms. So, you know, it's going to take time, and we want to make sure that these opportunities are grounded in something real before we start to bring them into the backlog. So, you know, as we work through de-risking those gating items, you'll start to see more of those opportunities come out of the pipeline and into our recorded backlog.

And as far as the supply, you know, we still have some challenges, but it has gotten better than where it used to be, you know, during COVID. But we are not 100% there where we should be. We have challenges. We manage the flow, but it has been a little bit better. And I think some of the things that they trip us up besides the tariffs, like, for example, what's happening with the lithium prices and so on. And so far, we have learned to live with him, and we have incorporated it into our forecast and our guidance as much as possible.

Okay, thank you. Thanks, Pat. Your next question comes from the line of Stephen Jankaro of SPFL.

Please go ahead.

Thanks. Good afternoon, everybody.

Hey, Stephen.

So two things for me. The first, just based on your guide, you have kind of a bit of upward momentum on the margin side. Can you just talk about what's driving that? Is it a specific segment? Is it just execution on certain areas? What's the big driver we should be thinking about for margins in 26?

Yeah, I think it's a great question. I think it's discipline and it's execution. We, you know, we've been talking about this for the last couple of years, but, you know, we've really tightened our discipline in terms of how we select projects, how we price them, how we manage the cost. And so, you know, we're starting to see that coming through in some of the margin improvements. I think, you know, as we continue to take that approach to bringing new projects through the backlog and converting them, you know, as well as bringing more assets online and just growing out those recurring streams, I think that's where we're starting to get confidence in more of the quality of earnings and what we're seeing in this gradual movement in margins.

Great. Thanks. And the follow-up to that is, and I'd have to go back and look historically to get the snapshot exactly, but when you look at your total project backlog that you show in the presentation, are there any sub-segments of that pie chart that tend to have higher margins or on the project size at all fairly similar?

Yeah, I mean, I think as we see some of these larger, more complex infrastructure projects come in, I think the margin profile will be somewhat higher. Not, you know, I don't think it would be a, you know, a spike in margins, but I think that, you know, with those mix of projects coming more into the backlog, they do bring a bit higher of a margin profile.

Okay, great. That's all for me.

Your next question comes from the line of Manish Sumayev, Cancer Fitzgerald.

please go ahead. The initial line might be on mute. Your next question comes from the line

of Ryan Finks of BeRiley Securities. Please go ahead. Hey, guys. Thanks for taking my questions.

Hey, I'm just curious if you can give a broader update on the R&G market in terms of new project opportunities going forward, and if you're considering any larger M&A as part of the

strategy there i would say yes to both of them uh our backlog i think um uh mark mentioned we have at least 10 rng facilities that they are in the backlog right now that will be built over the next few years in addition to that there's no shortage of new projects out there but it takes a considerable amount of money in order to develop this project and we try to be disciplined as to how many we take on at any given time as far as emergence and acquisitions uh we are open to it and we are looking at some stuff but nothing that is mature enough to to talk about it yeah but look we grew we have done 26 acquisitions for this company we grew it that way as well as organically and we always look for good opportunities as long as they are creative They add value at the end of the day to the company.

Yeah, I mean, we're still very excited about the opportunities that we're seeing. I think the demand from the compliance market is still pretty durable, but the voluntary markets are starting to see some growth as well. So the opportunities are there, and I think we're going to continue to be disciplined in how we bring more of those RNG assets into development and into operations to meet the demand that we're seeing.

I appreciate that. And then for my second one, firm generation ticked higher in terms of energy assets in development. I'm curious if that's going to continue to be the case, just based on the type of demand that you guys are seeing going forward. Thanks. Yeah, I think we're going to see

the firm generation that comes to some of these behind the meter opportunities will absolutely be there. You know, I think from, you know, where we will either decide to bring these into our assets in development or turn them into EPC opportunities, I mean, that's still, you know, a decision that we need to have. You know, the larger these projects are, it's more likely that we'll want to go an EPC path. But yeah, I think that, you know, that behind that firm generation will be a large driver of those opportunities and, you know, projects coming through our backlog.

Appreciate it, guys. Your next question comes from the line of Julian Dumoulin-Smith of Jefferies. Please go ahead. Hey, good afternoon. This is Hannah Velasquez

on for Julian. Thank you for the update and congrats on the strong quarter. I just wanted to ask around the tariff landscape. You know, we've seen some fluctuations in tariff policy following the Supreme Court order and then some commentary from the White House suggesting that there could be different levers to pull across different statutes like Section 301, Section 232, et cetera, can you just go ahead and maybe outline the general risk in that area, maybe how you are managing that if it's reflected in PPAs you're negotiating today? Yeah, to the extent you see that as risk.

Yeah, I think, and George, and probably Mark's prepared remarks, we all talked about the challenging environment of 2025, largely driven by policy and things like that. So we're not, I would say, overexposed or underexposed than our peers to these sort of global things. And obviously, whatever the president may or may not do and what the Supreme Court may or may not do in response to that, yada, yada, yada, is not really where we're prepared to comment. but we have said previously that some of our newer contracts have protections for for tariffs we're building that into the contract where if there are tariffs there are there are potential price adjustment mechanisms and other than that we're sort of we're just playing it by ear we're building contingency into our deals we're doing some pricing like i said some price adjustment potential and contracts and we're sort of crossing our fingers and just hoping things stabilize but But we're managing through it just as our peers are.

Well, if I might add there one thing, though, about the State of the Union message for the president, that he said that the hyperscalers, they should be doing their own power plants in order to provide their capacity. We thought that was a good opening and it will help us in the long term. Because as many of you know, I've been writing some articles saying that if we wait for the hyperscale of the wait for the utilities in order to interconnect their power plants, we will lose the AI race. The only way that it can happen is they develop their own power plants at the end of the day. Of course, they will get better reliability, and ultimately, it will be less expensive than doing it the other way. And, of course, to get transmission lines, even though you have a large central power plant, it's going to cost you as much to bring that power to the load as it does to build the generation. So, ultimately, everybody's going to be better off. So, I think it's a great, great sales pitch for our business.

Okay, that makes sense. And this is a follow-up. It's going off to that point. On the hyper-sailer front, can you give us a sense of what the general, you know, if there is a generic mix between resources that some of the conversations you're having with hyperscalers look like? Is it more so biased towards firm power? Are you seeing any surprises, perhaps more of a weighting towards renewables, solar plus storage? But generally, what does the resource mix look like that they're interested in?

I mean, we're across the board. You know, the energy infrastructure, it's across the board. And right now, everybody's concern, many of the industrial and commercial that we're talking about, resiliency. And the other thing that they're concerned a lot, speed to power. And that's why I say, you know, if they go, they wait for the utilities and the central power plants to happen and get the right away to transmission lines, which might take five to ten years, you will lose the AI race. So speed to power, it might be, and many not only they want gas turbines, but they want some renewable. So you will see that they have gas turbines, that we have some solar, some battery storage at the end of the day, high in nice power supply. And that's where we come in into MRS will come into the picture because we've been doing it on a military basis. Take the San Antonio Postman Naval Shipyard and I keep going on and on, Ferris Island and all of them and some of us started into the previous Trump administration because they wanted to have resiliency in every, what I would say, critical base, military base, whether it's the naval or the Marines in Paris and so on.

Thank you.

Your next question comes from the line of Manish Sumayev, Cancer Fitzgerald. Please go ahead.

Hi there. Can you hear me? Okay, fantastic. Thank you. I don't know what happened earlier. Two questions. One is, if you could just help us understand on the operating cash flow, you know, just give us a sense as to, I guess, how we should think about working capital in particular as we think about 26.

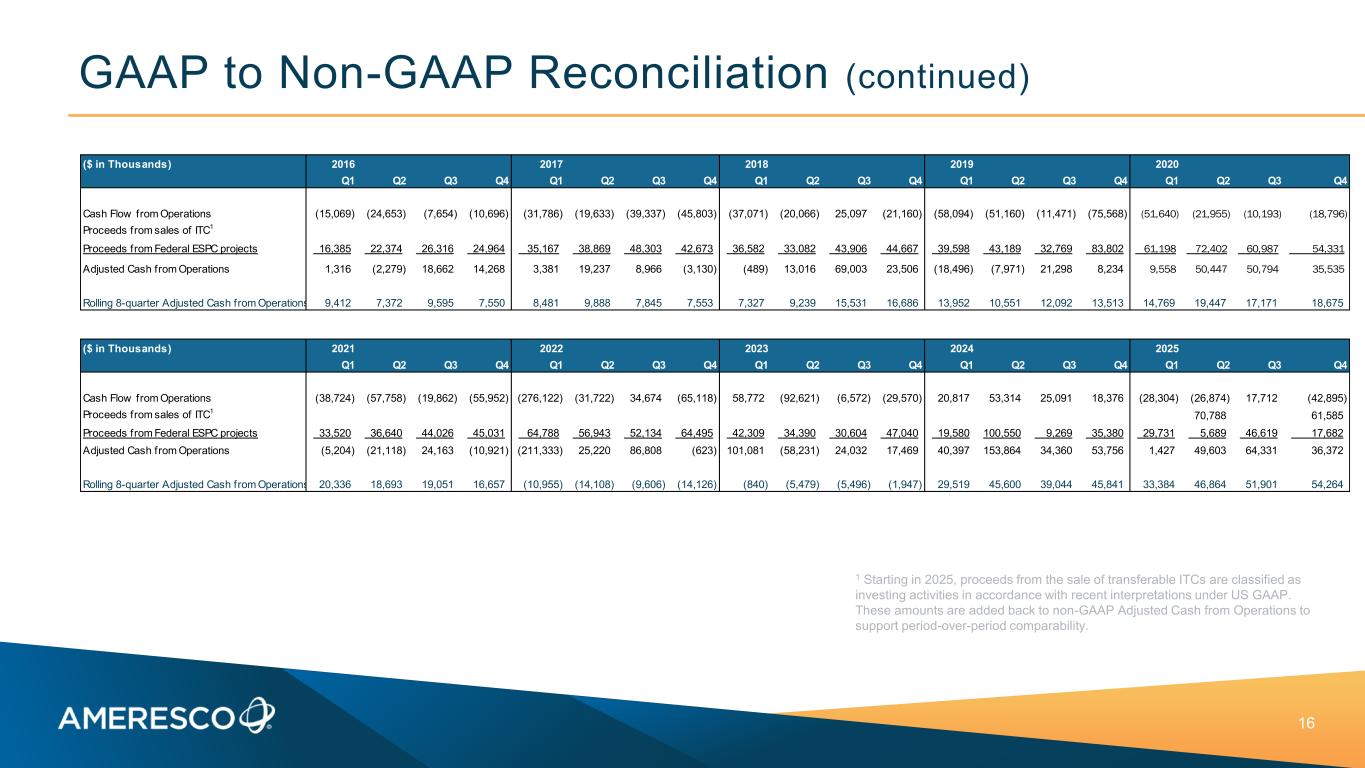

Sure. Yeah. I mean, look, if you look at kind of Q4, right, from a cash flow, and I've said this a lot, you know, quarterly cash flow can be lumpy, right? in Q4 cash flow, you know, that really reflected kind of normal project timing and working capital movements. Obviously, that was a very heavy construction period. You know, I think the right way to look at it, the right way to evaluate our cash generation is on, you know, rolling multi-quarter basis. And I think that's why we like to provide that metric. It's a more realistic reflection of our implementation cycle. Like I said, quarterly cash can kind of move around due to construction timing and milestone billings. I think, you know, working capital, we've been a bit tighter on working capital because we've got some larger projects that are coming through on build that are tied to milestones, and as we continue to progress those projects and achieve those milestones, we'll start to see unbuild, convert through AR and cash, and you'll start to see that come through our cash from operations. So timing can vary kind of quarter to quarter, but, you know, know, we would expect our working capital to normalize across the year. And we, you know, expect us to see, you know, kind of the normal, if not growing level of cash generation.

Okay, that's super helpful. And then on the guidance, what gets you to the top end of the guidance? What are some of the milestones that we should be kind of looking for?

Yeah, I mean, I think that's going to really come down to just execution, right? I think that, you know, the backlog is there, the opportunities are there. You know, when we try to put our guidance together, we need to take, you know, a bit of a prudent look at how we think things can progress through the backlog and into the P&L. So, you know, I think if we can, you know, we can execute on these projects, you know, we don't have, you know, other delays like the, you know, some of the weather stuff we're seeing early in the year. Yeah, I think it always just comes down to our ability to execute and kind of stay disciplined on how we manage costs. And I think that could represent an opportunity. But, you know, we feel really good about the midpoints just based on how anchored it is to our visibility coming out of backlog, assets we're bringing on, et cetera.

And then maybe last one for George, you know, high level, obviously look at the backlog. It's pretty impressive. A lot of opportunities ahead. You talked about growth in Europe. So as I think about the business the next couple of years out, I mean, how does Ameresco evolve?

Go ahead. Sorry, George. I think you will see us doing more and more infrastructure projects and a good chunk of business in Europe. The potential is there. And that's why we made the investment the last couple of quarters. and this quarter, we added a considerable amount of people with the engineering, development people, as well as financial and execution, construction managers, especially senior level management, construction management people to execute on these larger projects. Because I think that you will see us doing more data centers, more storage or resiliency plans for the industrial customers especially. Because, you know, the industrial sector for a long time tried to move energy efficiency projects that were very difficult. But now, because they are concerned about resiliency and the higher cost of electricity, we're getting some good traction. So, I think you will see us doing less on some of that much. The business is there. We'll be doing much work, but the company will become much larger and driven by these larger opportunities, I would say, in the energy infrastructure sector.

Okay, that's super helpful.

Thank you so much. You got it.

Again, ladies and gentlemen, if you have a question,

please press star 1 on your telephone keypad.

There are no appearing questions at this time. And with that, ladies and gentlemen, concludes today's conference call. We thank you for participating. You may now disconnect your lines.