Chicago Atlantic Real Estate Finance, Inc. Q1 FY2026 Earnings Call

Chicago Atlantic Real Estate Finance, Inc. (REFI)

Call highlights

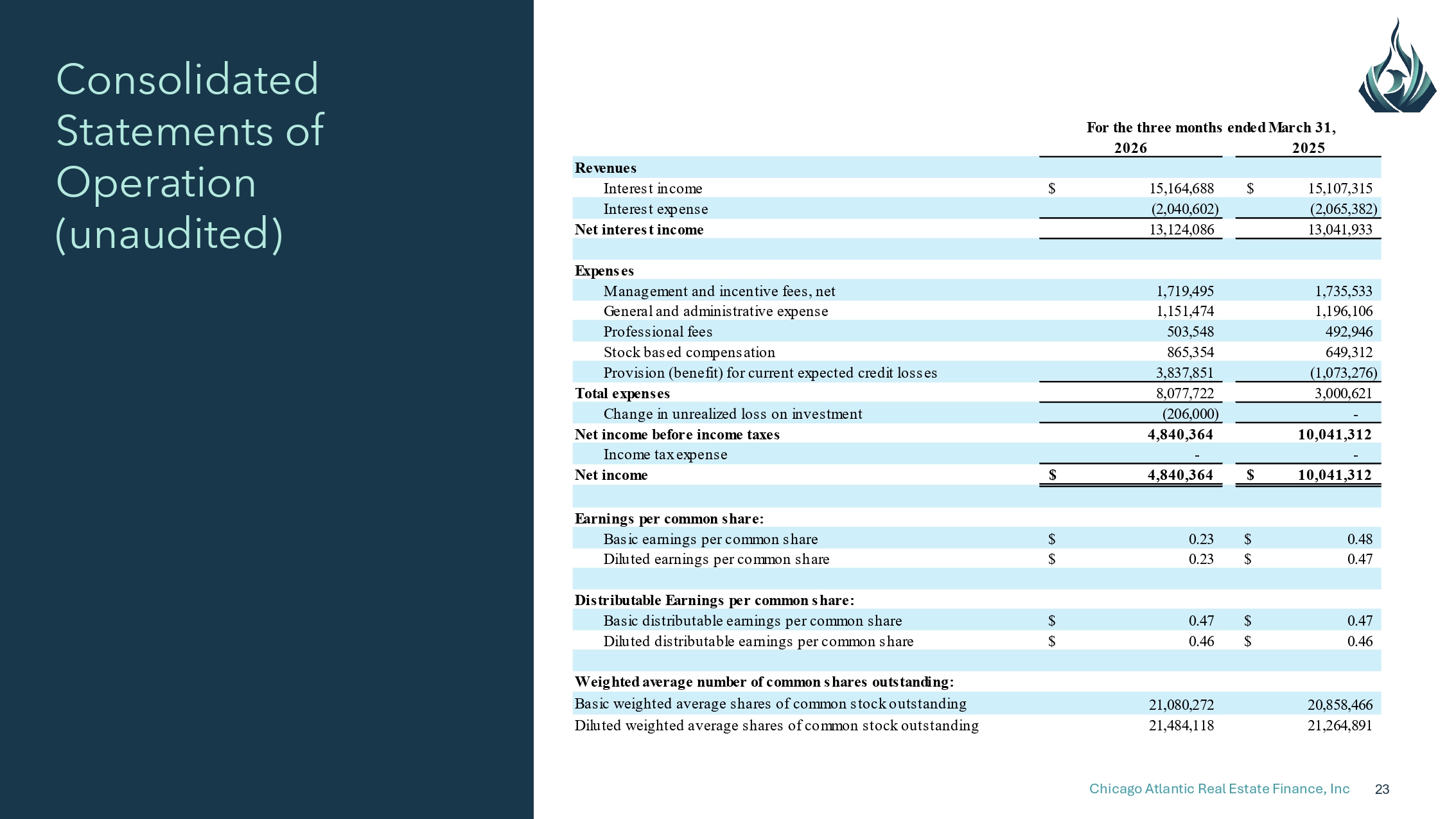

AI-EXTRACTEDChicago Atlantic Real Estate Finance reported stable Q1 2026 results with net interest income of $13.1M and distributable earnings of $0.47 per share, highlighted by the restoration of loan #9 to accrual status and the federal rescheduling of medical cannabis to Schedule III.

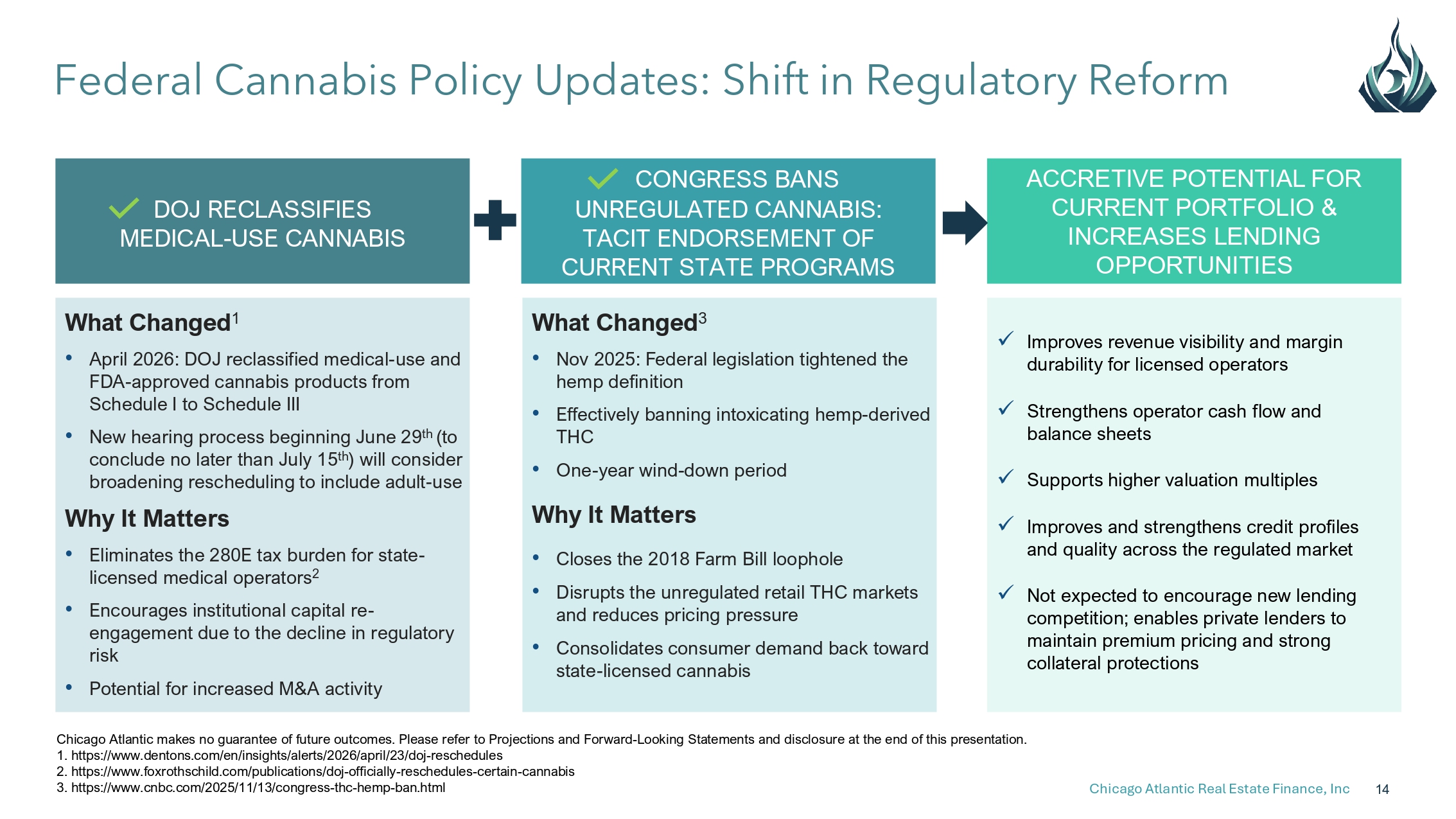

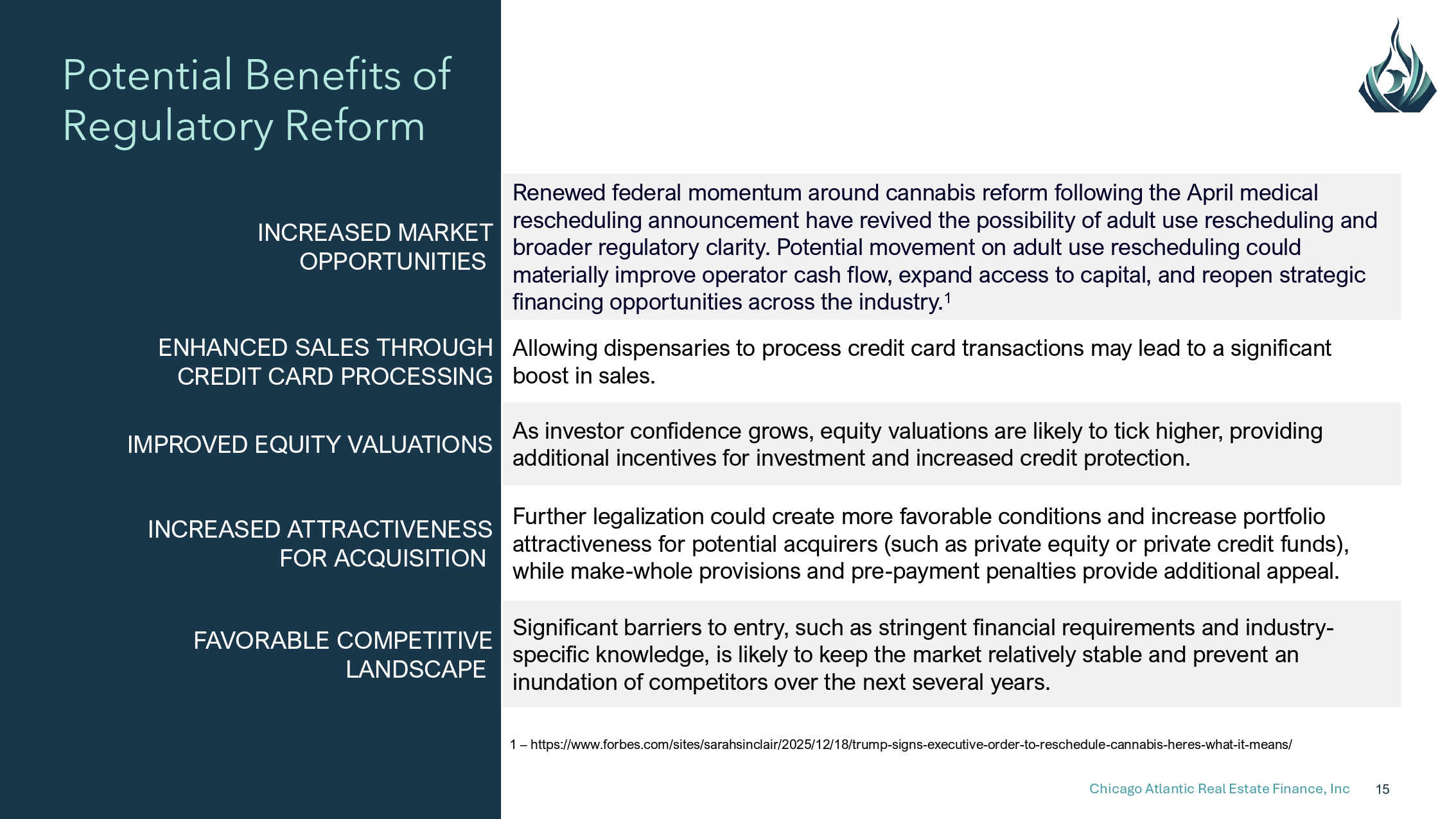

“The Department of Justice announced on April 23rd that it is rescheduling certain medical marijuana products to Schedule 3 from Schedule 1. This is the most significant federal policy change in years and perhaps in the history of the industry.”

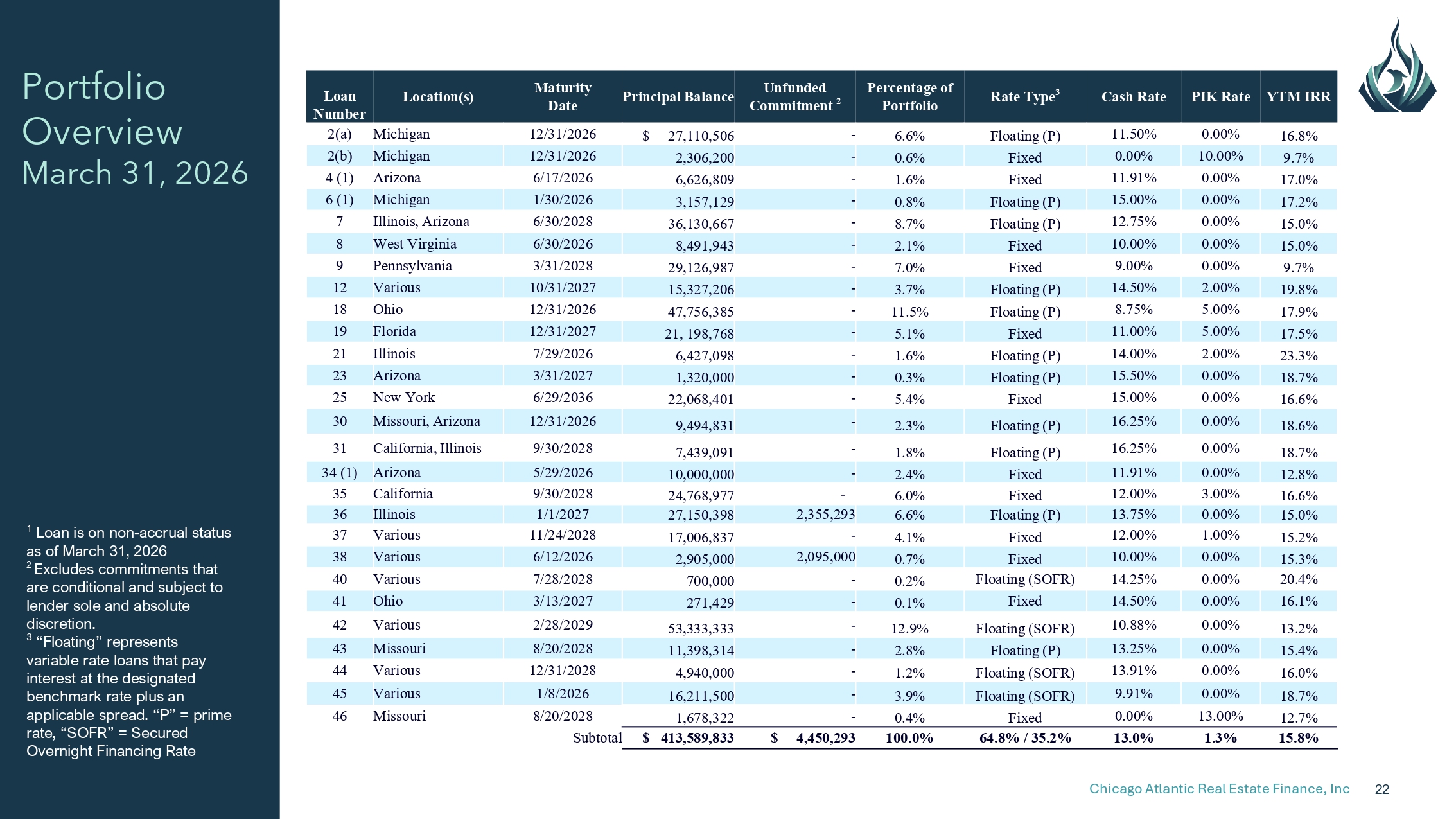

“As of March 31, 2026, approximately 10.7% of our portfolio is risk-rated four or higher, compared with 4.8% as of December 31, 2025. This risk-rating shift, primarily attributable to loan number 36 being downgraded from three to a four, contributed to an increase in CESA reserves of approximately $3.8 million.”

- Loan #9 was restored to accrual status after three consecutive months of timely payments, reducing non-accrual portfolio to 4.8% from 11.1%

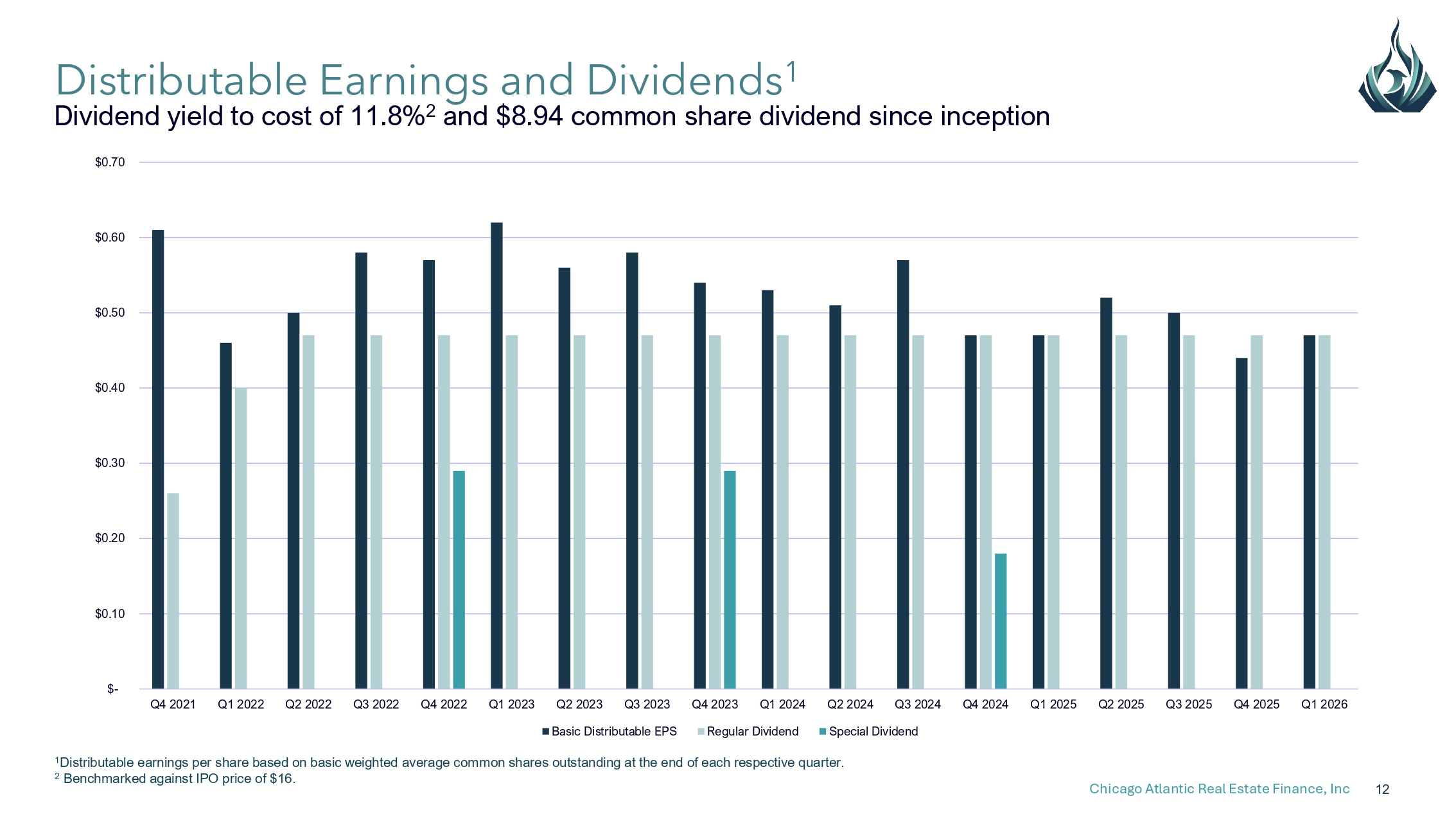

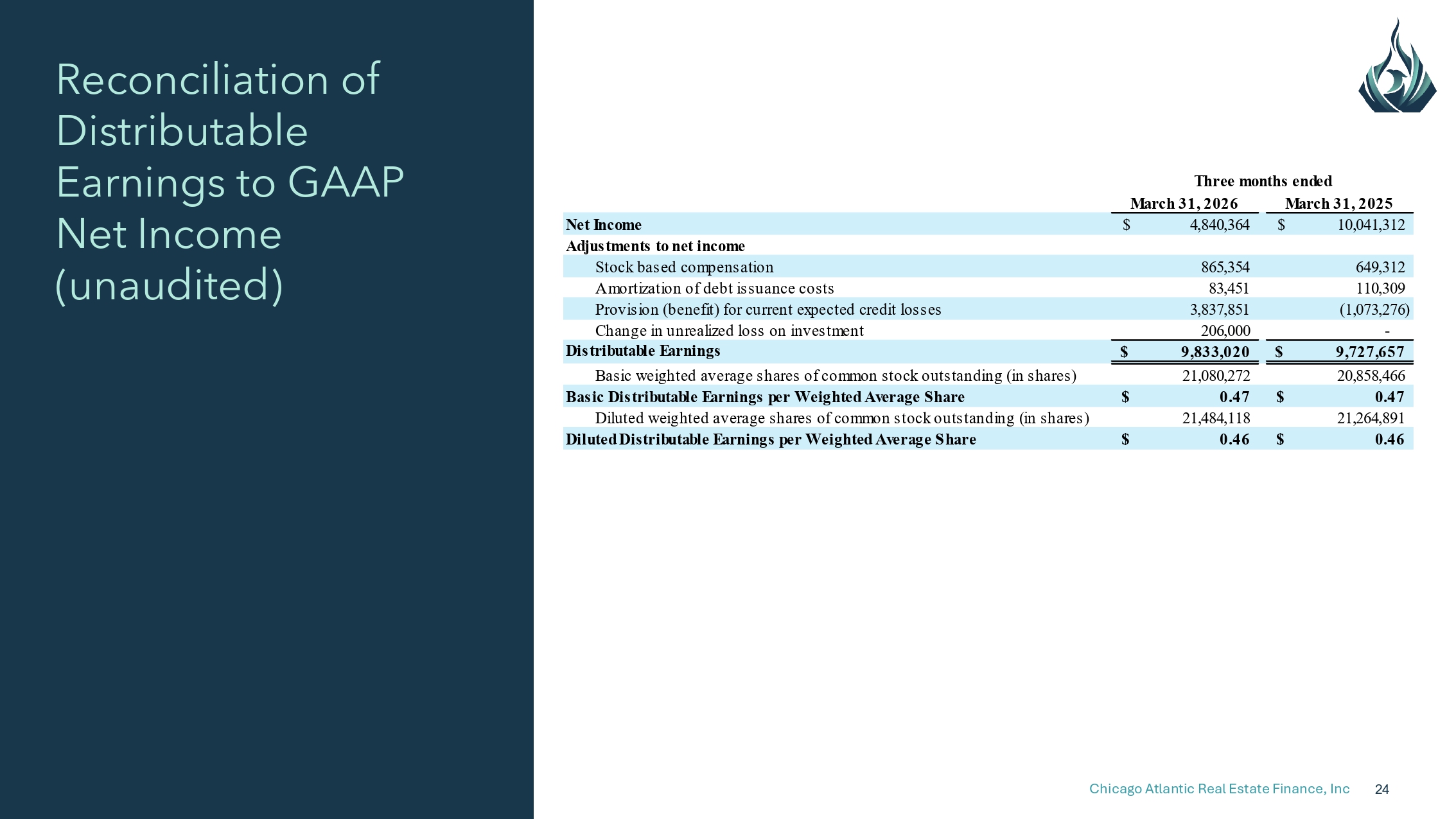

- Distributable earnings of $9.83M ($0.47 per share, basic and diluted) increased from $9.25M ($0.44) in Q4 2025

- 100% of prime rate loans are at their floors, with only ~4% of loan principal exposed to further rate declines

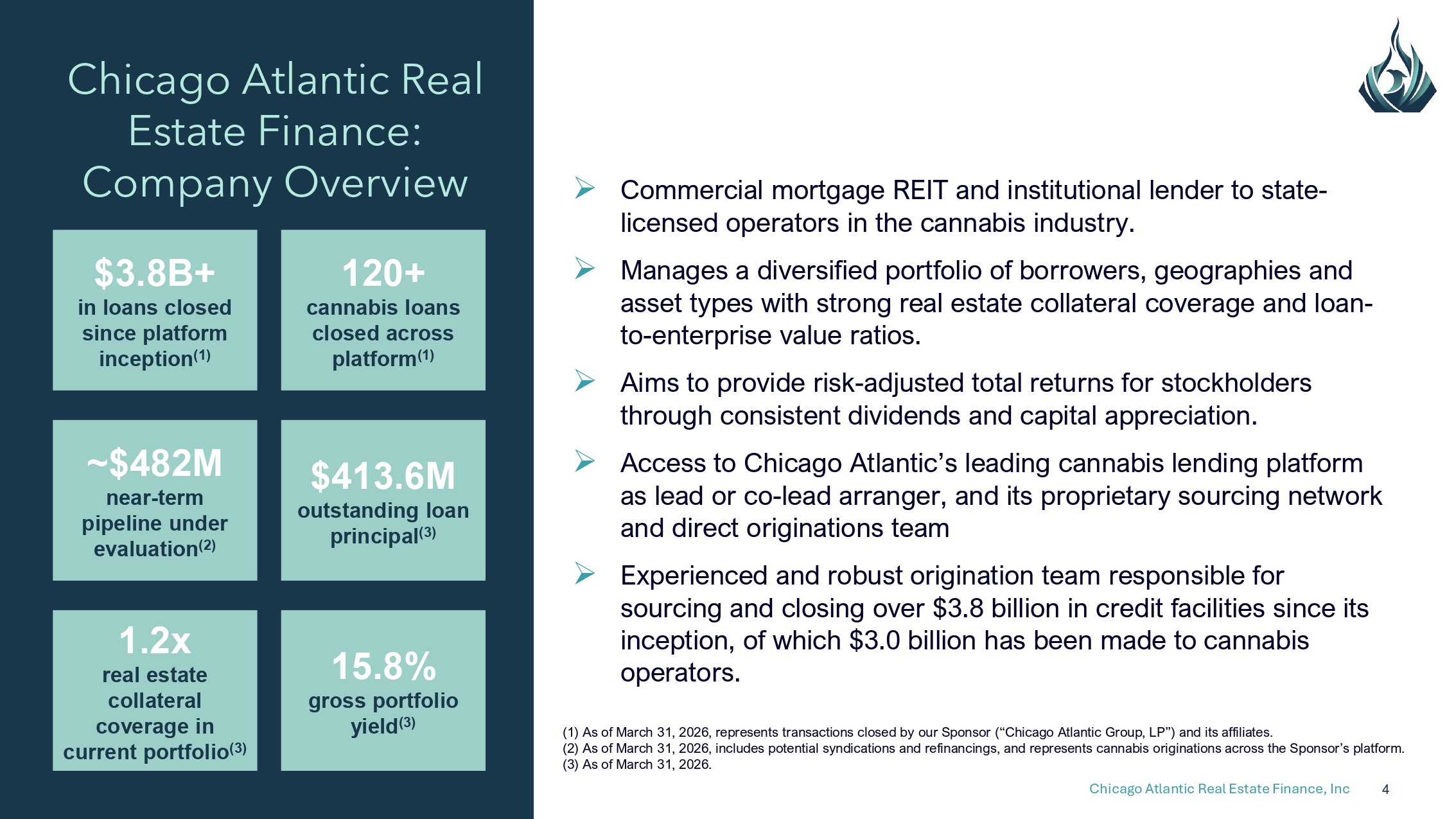

- Pipeline of cannabis opportunities stands at $482M, of which ~$133M is backed by real estate collateral

- DOJ announced on April 23 the rescheduling of medical marijuana from Schedule 1 to Schedule 3, potentially eliminating 280E tax burden on borrowers

- Originations of ~$54M during the quarter, with $16.2M funded to new borrowers

- Weighted average yield to maturity declined to 15.8% from 16.3% in Q4 2025

- Net income declined to $4.84M ($0.23/share) from $8.16M ($0.38/share) in Q4 2025

- Net interest income decreased to $13.12M ($0.61/share) from $14.24M ($0.66/share) in Q4 2025

- Risk-rated 4+ portfolio increased to 10.7% from 4.8%, driven by loan #36 downgrade, contributing to a ~$3.8M increase in CECL reserves

- Total leverage increased to 38% of book equity from 32% at year-end 2025

- Rescheduling benefits remain uncertain, with an administrative hearing scheduled June 29–July 15 and potential need to parse medical vs. adult-use operations

Documents & deck

Good day, and welcome to the Chicago Atlantic Real Estate Finance Inc. post-quarter 2026 earnings conference call. As a reminder, all participants will be in the listen-only mode. Should you need assistance, please signal a conference specialist by pressing the star key followed by zero. After today's presentation, there will be an opportunity to ask questions. To ask a question, you may press star then 1 on a touchstone phone. To withdraw your question, please press star and then two. Please note that this event is being recorded. I would now like to turn the conference over to Lisa Camps. Please go ahead.

Thank you. Good morning. Welcome to the Chicago Atlantic Real Estate Finance Conference Call to review the company's results. On the call today will be Peter Sack, Co-Chief Executive Officer, David Kite, President and Chief Operating Officer, and Phil Silverman, Chief Financial Officer. Our results were released this morning in our earnings press release, which can be found on our Investor Relations section of our website, along with our supplemental filed with the SEC. A live audio webcast of this call is being made available today. For those who listened to the replay of this webcast, we remind you that the remarks made herein are as of today and will not be updated subsequent to this call. During the call, certain comments and statements we make may be deemed forward-looking statements within the meaning prescribed by securities laws, including statements related to the future performance of our portfolio, our pipeline of potential loans, and other investments, future dividends, and financing activity. All forward-looking statements represent Chicago Atlantic's judgment as of the date of this conference call and are subject to risks and uncertainties that can cause actual results to differ materially from our current expectations. Investors are urged to carefully review various disclosures made by the company, including the risks and other information disclosed in the company's filings with the SEC. We also will discuss certain non-GAAP measures, including but not limited to distributable earnings. Definitions of these non-GAAP measures and reconciliations to the most comparable GAAP measures are included in our filings with the SEC. I'll now turn the call over to Peter Stack. Please go ahead.

Thank you, Lisa. Good morning, everyone. This quarter, Chicago Atlantic reported a quarter of consistent results against the backdrop of continuing concerns in the private credit market, the Fed pausing the interest rate easing cycle following three consecutive rate cuts in Q4 of last year, and volatility caused by the Middle East conflict. This quarter's results reflect the strength and resilience of our business model. We are a leading capital provider in the cannabis ecosystem. Our experience in this industry provides us with the expertise, relationships, and the ability to redeploy capital more quickly than the typical mortgage rate. Our rigorous underwriting and stringent risk standards, led by our cannabis-focused underwriting, real estate, and analytics team, ensures an acceptable risk-first reward. I continue to be optimistic about the current environment. The pipeline of cannabis opportunities remains strong and currently stands at $482 million, of which approximately $133 million of this pipeline is backed by real estate collateral. Given the recent medical rescheduling news in late April, I'd be remiss in not highlighting the latest major federal initiative and policy setting for the cannabis industry. The Department of Justice announced on April 23rd that it is rescheduling certain medical marijuana products to Schedule 3 from Schedule 1. This is the most significant federal policy change in years and perhaps in the history of the industry. There are nuances to work out as we wait for a more definitive framework and how this policy will apply to existing individual state laws. And we expect these policy changes to impact each operator differently based on their medical market exposure. But after many years of delays, this is a tremendous step in the right direction. How we expect to immediately benefit from this order is predominantly through the elimination of the extra tax burden on cannabis companies resulting from Section 280E, and retrospective relief on legacy tax liabilities that should improve operator cash flows and strengthen balance sheets, driving higher valuation multiples and improving the credit profiles of our borrowers. The federal order requires and sets up an expedited process for state-licensed medical cannabis operators to register with the DEA, and in effect, legalizing state-licensed medical cannabis on a federal level. Additional benefits from this would be lowering barriers to U.S. exchanges, for which we have been an advocate. An administrative hearing is scheduled for June 29th to July 15th. This hearing provides a pathway to reschedule cannabis more broadly, possibly rescheduling adult-use products. We will continue to be measured in our outlook for a positive outcome and not jump ahead to any conclusions. We believe Chicago Atlantic is well-positioned to benefit from the initial order. And as I've stated before, the success of our strategy is not dependent on any of these changes. We have remained conservative and underwrite every investment, assuming no regulatory-driven credit improvements. Leading up to the June 29th hearing, we've begun forecasting for a range of outcomes from the rulemaking process, but currently remain in a wait-and-see mode. Overall, ReFi delivered consistent, stable financial results for the first quarter of 2026 against an unstable macro environment. Our differentiated business model lending to operators and property owners in the cannabis industry enables us to operate in a niche market with limited competition, with favorable terms, and delivering competitive yields. This year is proving to be a transformative time for the cannabis industry following the federal government's rescheduling medical marijuana from Schedule 1 to Schedule 3 and the potential for broader policy shifts for cannabis later this year. We are encouraged by the validation of our business model and the potential impact of regulatory orders flowing through to refi. I look forward to updating you on our progress throughout the rest of this exciting year. David will now speak to the portfolio in greater detail.

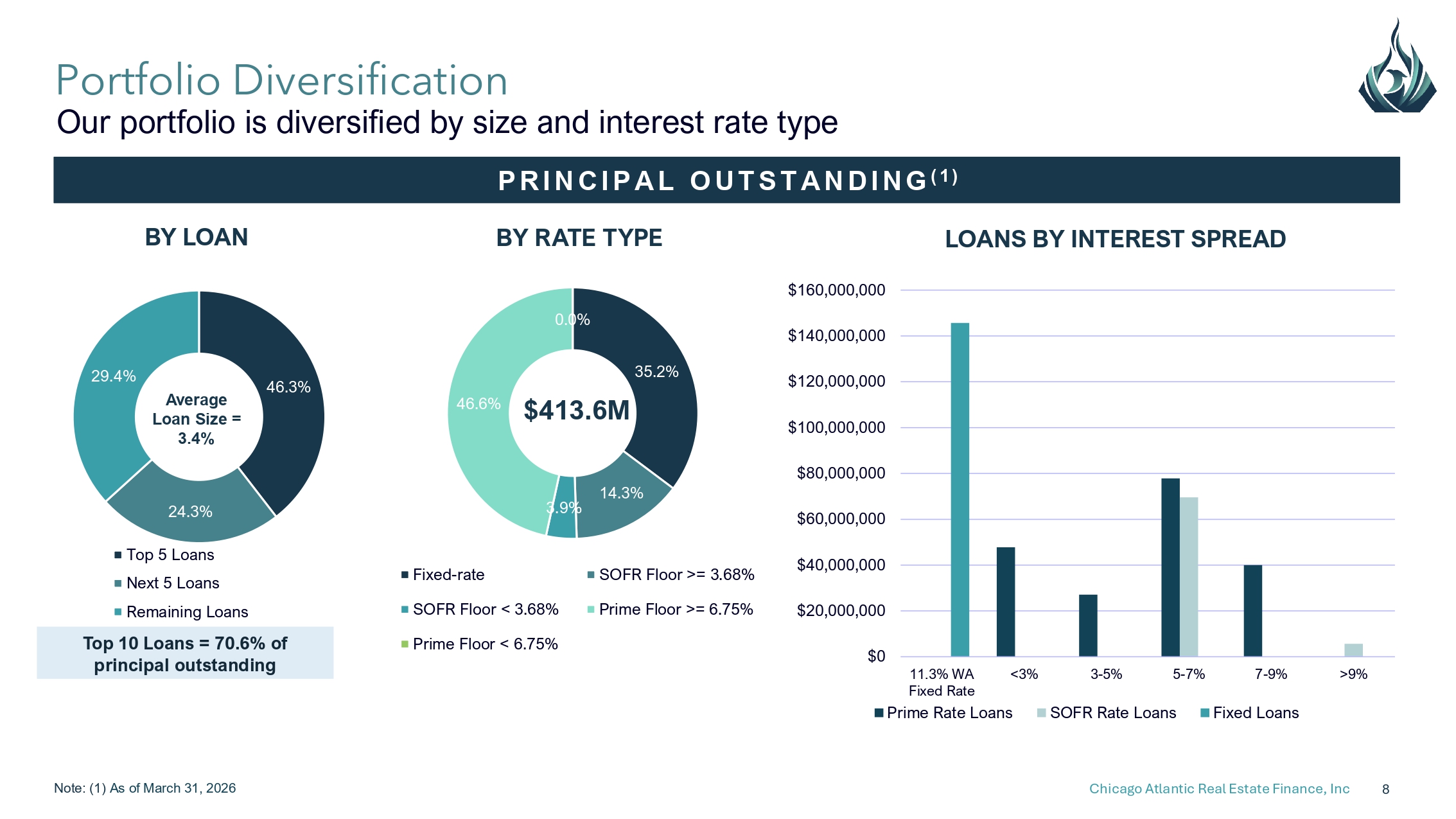

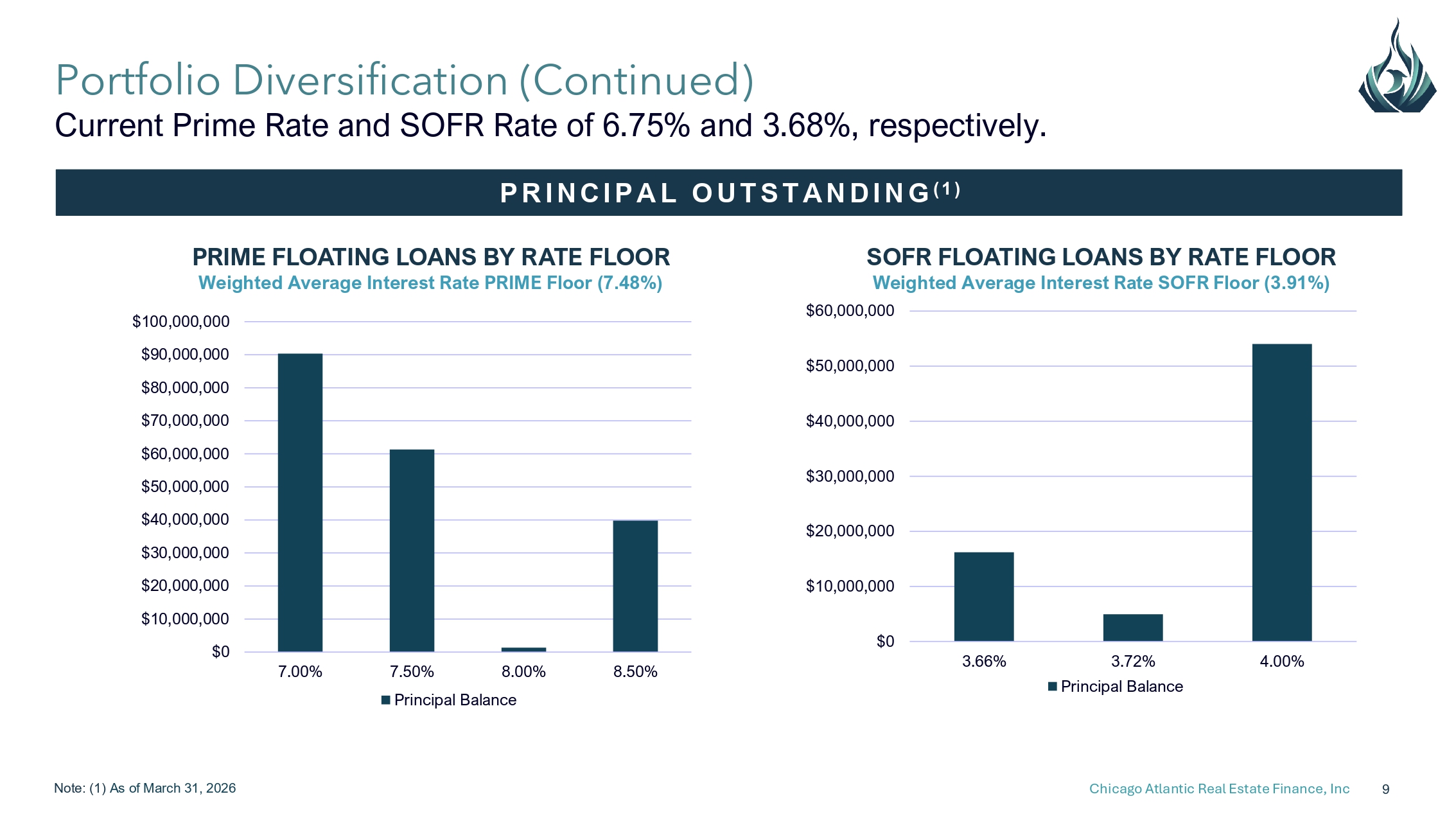

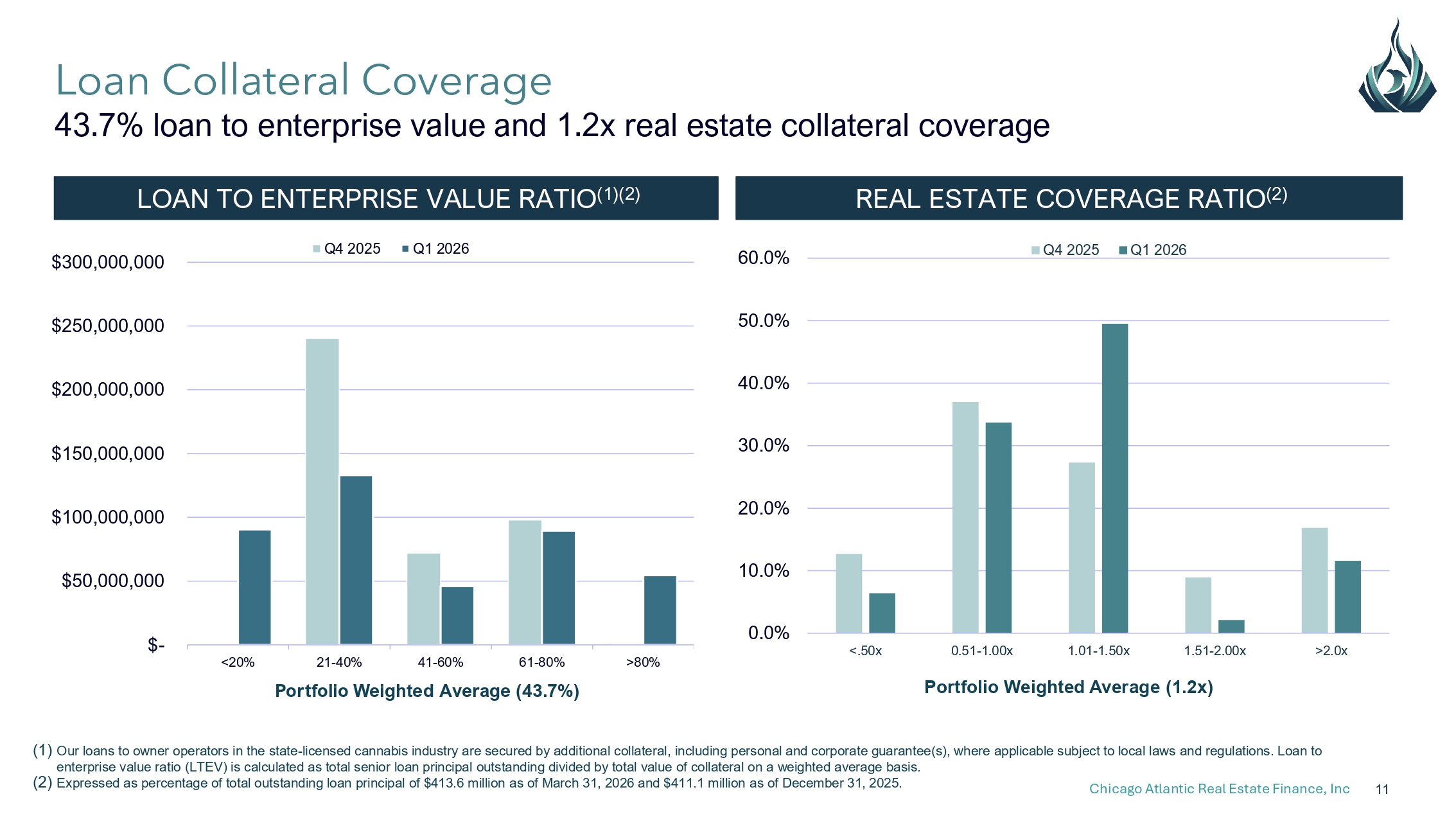

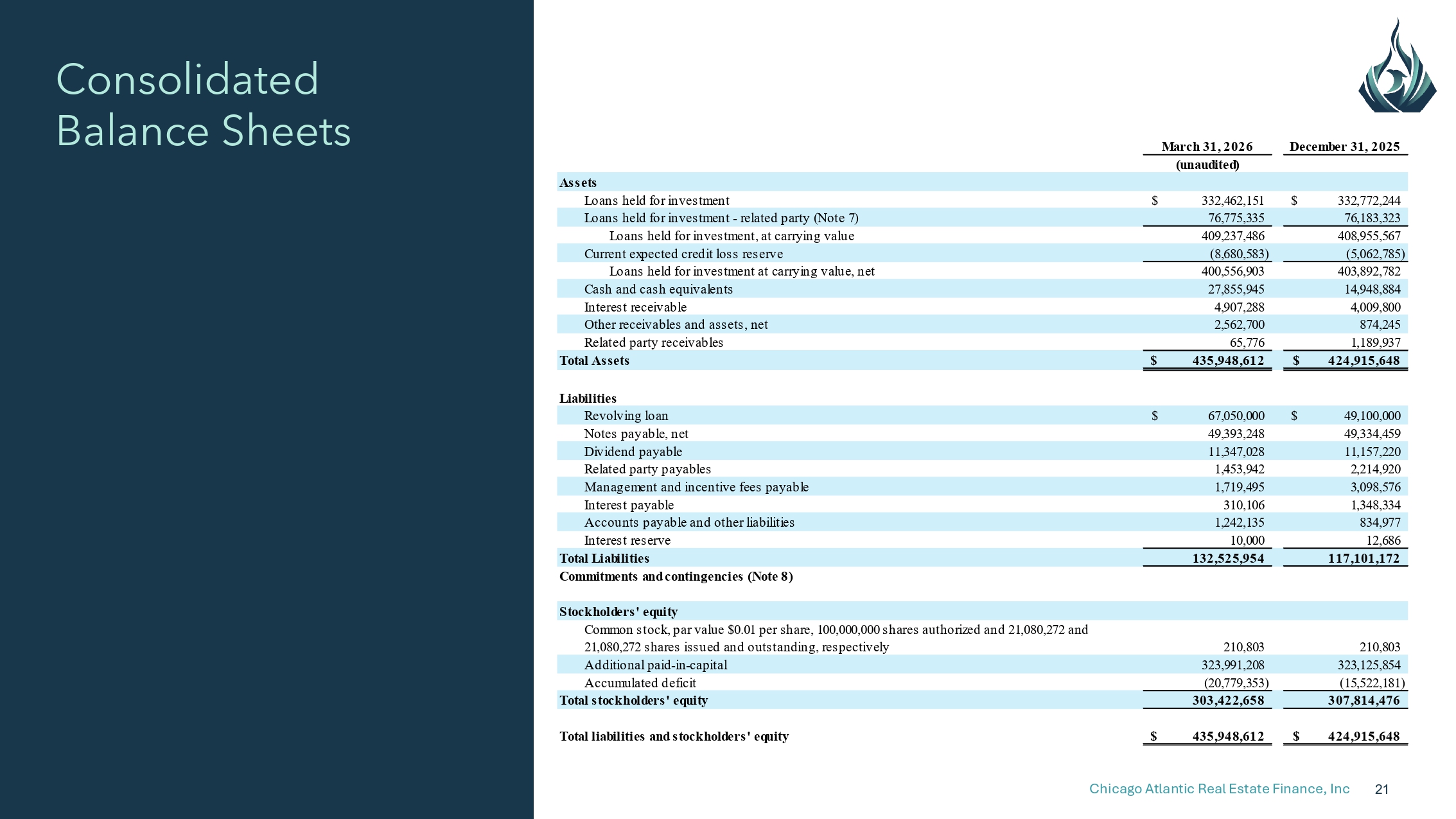

Thank you, Peter. As of March 31, our loan portfolio principal totaled approximately $414 million across 25 portfolio companies with a weighted average yield to maturity of 15.8%, compared with 16.3% for the fourth quarter of 2025. Most originations during the quarter were approximately $54 million of principal fundings, of which $16.2 million and $37.8 million were funded to new borrowers and existing borrowers, respectively. These were offset by approximately $52 million of repayments, comprised of $3.3 million in scheduled amortization payments and $48.2 million from full and partial loan prepayments. As of March 31, 2026, approximately 10.7% of our portfolio is risk-rated four or higher, compared with 4.8% as of December 31, 2025. This risk-rating shift, primarily attributable to loan number 36 being downgraded from three to a four, contributed to an increase in CESA reserves of approximately $3.8 million. As I mentioned on our last call, we made significant progress on loan number nine last quarter, funding in advance for the borrower to allow for accretive acquisitions. As of December 31, 2025, the loan was brought current, and as of March 31, we're pleased to announce that we've moved the loan back to accrual status after three consecutive months of timely payment and demonstration of sustained performance improvement, which we expect to lead to the ability to continue to meet debt service obligations. This is a prime example of how we utilize the operational and workout expertise amongst our team and the broader Chicago Atlantic platform, using creativity and deal management to drive successful turnaround efforts. As of March 31, 2026, approximately 4.8% of our portfolio was on non-accrual status, a decrease from approximately 11.1% as of December 31, 2025, primarily relating to the restoration of loan number 9 to accrual. As of March 31, 2026, our portfolio consisted of 35.2% fixed-rate loans and 64.8% floating-rate 71.9% and 28.1% of floating-rate loans are benchmarked to the prime rate and SOFR. respectively. With the current prime rate at 6.75, 100 percent of our prime rate loans are at their floors, and in total, approximately only four percent of our loan principal is exposed to further rate declines across the total portfolio. Importantly, our floating rate loans are not exposed to interest rate caps, which, combined with our rate floor protections, provides a structural advantage in portfolio construction that compares favorably to most other mortgage rates. Total leverage equaled 38% of book equity at March 31, compared to 32% as of December 31. As of March 31, we had $67.1 million outstanding on our senior secured revolving credit facility and $49.4 million outstanding on our unsecured term loan. As of today, we have approximately $59 million available on the senior credit facility and total liquidity. Net of estimated liabilities of approximately $54 million. I now turn it over to Phil.

Thanks, David. Our net interest income of $13.1 million for the first quarter represented a $1.2 million, or 8% decrease from $14.2 million during the fourth quarter of 2025. The decrease was primarily attributed to the fourth quarter collection of past due unaccrued interest on loan number nine, totaling $1.7 million, which was recognized last quarter. Total interest expense, including non-cash amortization of financing costs for the first quarter of 2026, was approximately $2 million and increased from $1.8 million in the fourth Deleted average borrowings on our revolving loan increased to $48 million compared to $33.6 million during the fourth quarter. Our CESOL reserve on our loans held for investment as of March 31, 2026, was approximately $8.7 On a relative size basis, our reserve for expected credit losses represents 2.1% of our outstanding principle of our loans held for investment. The reserve increased by approximately $3.8 million from the fourth quarter, primarily due to increases in LTV attributed to specific loans, primarily loan number 4, 34, and loan number 36. On a weighted average basis, our portfolio maintains strong real estate coverage of 1.2 times. Distributable earnings per weighted average share on a basic and fully diluted basis were approximately 47 cents and 46 cents for the first quarter. And in April, we distributed the fourth quarter dividend of 47 cents per common share declared by our board. Since inception, the company has distributed $8.94 per common share in dividends, which represents a yield on cost of approximately 11.8% when measured against our IPO price. Our book value for common share outstanding was $14.39 as of March 31, 2026, and there were approximately 21.5 million common shares outstanding on a fully diluted basis as of such date. During the subsequent period from April 1, 2026 through today, the company advanced new gross loan principle of approximately 15.8 million, comprised of $13.1 million advanced to one new borrower and $2.7 million to existing borrowers on delayed draw on existing credit facilities. Additionally, the company received a total of $14.3 million in loan repayments, comprised of $1.8 million of scheduled amortization and $12.5 million in early prepayments, which included the full repayment of loans number 6 and number 30. We expect to continue to maintain a dividend payout ratio based on our basic distributable earnings per share of 90 to 100 percent for the 2026 tax year. If our taxable income requires additional distributions in excess of the regular quarterly dividend to meet our taxable income requirements, we expect to meet that requirement with a special dividend in the fourth quarter. Operator, we're now ready to take questions. Thank you. We will now begin with the

question and answer session. To ask a question, you may press star then one on your touchstone phone. If you are using a speakerphone, please pick up your handset before pressing the keys. If at any time your question has been addressed and you would like to withdraw your question, please press star, then two. At this time, we will pause momentarily to assemble a roster. The first question comes from Pablo Zuanic from Zuanic & Associates. Please go ahead.

thank you and good morning everyone and uh thanks peter for uh the commentary on the on the regulatory front and of course the positive news that we've been receiving um recently look i just want to start with uh with loan number 36 um obviously foreign 34 are arizona loans and we know that's a tough market for growers you mentioned foreign 34 are in uh in an accruals or a part of the reserve in the case of 36 that's an Illinois loan right and it's a larger loan 27 million whatever color you can provide more on that loan would be helpful Arizona I understand Illinois of course we've seen forefront and other companies have issues there but if you can just give more color on that particular loan number 36 would be helpful please especially in the context that was issued in december 2024 which is not that long ago i think bye-bye thanks thank you um

illinois market is experiencing uh consolidation on the retail front and i think it's and is experiencing increasing competition on on cultivation this one in particular has strong real estate coverage and is a vertically integrated operator um and the um i think the reserving activity reflects our ordinary course evaluation of portfolio company performance and risk um uh the the um discussions with the borrower are are very constructive and and um we expect that this can be that that um this company's performance can be improved and resolved in a in a constructive and collaborative manner. And I'm hopeful that in the months ahead we'll find this reserving activity conservative. But regardless, this is part of our ongoing process to show reserving activity that reflects a conservative appreciation of performance and the portfolio.

Thank you. On the same topic, Peter, can you give an update on Loan 4 and 34?

for um these continue to be uh continue to evolve um i think it's too early to give specific specific

updates but they are constructive relationships and by the same token in the case of loan number nine back into accruals like you said you were actively involved with them collaborative basis um you know i'm just trying to understand the potential for loans in the portfolio that can be equitized or where you can succeed in the in bringing new buyers to those loans i mean how How should we think about that as an opportunity going forward for the book?

I think it's important to contrast loan number nine with other reserving activities in the portfolio. And loan number nine was a foreclosure process, was a judicial foreclosure process. And that takes a substantial longer amount of time for resolution than when challenging situations within portfolio companies can be resolved. constructively and collaboratively. I'd say that the markets or assets that are undergoing challenges have improved significantly over the last year, as expectations for rescheduling have moved from speculative to more definitive to, in the case of medical operators, uh uh executed and so this is both a both a environment that is uh constructive and positive for deploying capital and for and for finding solutions within the book whether that's finding new equity investors um whether that's finding new equity investors executing operational change or working towards an exit this is a better environment for both deployment and um and reorganization and problem solving than really we've seen in the last three

years right thank you and then on the topic of the the unscheduled repayments uh you know thank you for the table you you showed in the press release today about 48 million unscheduled repayment um in the first quarter and i think phil mentioned another 15 million so far in the second quarter is that out of the norm uh i'm just trying to understand what's driving those early repayments

or that just normal part for the course these work these are part part of the course um you know we labeled them unscheduled but um uh unscheduled doesn't mean necessarily it doesn't necessarily mean a surprise and these were loans many few of them when you're in we're

nearing their maturity date thank you look a couple of modern apologies if there's someone else in the in the Q&A queue looking at it thank you loan number 45 in Canada I don't know that's the first time you've done a loan outside of the US but can you comment on that and more in general opportunities in international you know Europe and even more in Canada it's not the first

It might be the first time that refi has executed a loan outside the U.S., but not the first time that Chicago Antic as a platform has executed a loan outside the U.S. and in Canada. I think we're finding that in the Canadian market, there has been stabilization of the market in some cases and rationalization of the market in terms of unprofitable operators leaving. And that's given room and air for profitable, well-executing operators to rise to the top, be recognized, to show strong results, and to provide opportunities for lenders to provide capital at very strong risk-adjusted returns. And I think in the past, we just haven't seen that opportunity set arise so meaningfully and so specifically and clearly. But I think we see this happen in a lot of markets that are oversaturated, that they go through a period of rationalization. And after that rationalization, pockets of opportunity emerge.

Thank you. One last one. And I know we've talked about this before.

Sorry to interrupt, Mr. Zwanek. May we request you to return to the queue for any follow-up questions, please? You have the next question coming from the line of Chris Muller with Citizens Capital Market. Please go ahead.

Hey, guys. Thanks for taking the question. So I wanted to ask some clarifications around Schedule 3 that you may or may not know the answers to at this point. I guess, first off, what percentage of your guys' portfolio is medical? And I guess, how is that determined? Is that done at the license level, which my understanding is some states have dual-use licenses, or is it determined by the end user being either medical or rec?

Most of our borrowers that are operating as adult use are also operating as medical operators. and each of them then parse their revenue by medical versus adult use, but they can be those medical and adult use sales in many cases can be operating out of the same dispensary. We haven't published what is medical versus adult use. I'm hopeful that within the year of 2026 that it's irrelevant, that the administrative hearings that are scheduled for June and July proceed, that adult use is rescheduled as well, and the industry doesn't have to go through this exercise of analyzing what's medical and what's adult use, that it can proceed to operate each businesses seamlessly. But we shall say, I think if adult use measures and progress around adult use rescheduling falters or slows down, then I think you're going to see a lot of work among our borrowers to parse medical versus adult use operations, to allocate costs optimally between their medical and adult use operations to maximize tax efficiency. And I think you're also going to see state regulators perhaps adjusting the definitions within their adult use program to shift more of their operations towards what they can call and designate a medical program. But I hope those types of acrobatics are unnecessary because the administration has executed on its pathway to reschedule the entire supply chain. That's helpful. And I think I saw California is doing

something along those lines, which I agree with you. Hopefully that's irrelevant and full Schedule 3 gets done in June, but we'll see how that plays out. And then I guess on the CISO reserve increase in the quarter, and I may have missed this in your guys' prepared remarks, but was that increase specific or general reserves? And how are you guys thinking about the impact on CISO reserves

following Schedule 3? That reserve activity was a mix of both specific and general. I should note that that reserve activity reflects the market and discount rates and valuations and loan-to-values as of 3.31, and they do not reflect the subsequent events of rescheduling market activity and discount rates thereafter. I think generally that rescheduling is a credit positive for all of our borrowers, and even those that don't have significant medical revenues.

And should we expect to see some CISO releases throughout 2026 as those 280E issues work through the companies?

It's certainly possible. It would be a reflection, not necessarily directly of rescheduling, but it would be a reflection of the inputs, a reflection of market sentiment, loan-to-values, cash flow calculations flowing through to the inputs that drive our CISO reserve policies and behaviors.

Got it. Appreciate you guys taking the questions, and great to hear we finally got some positive news in the sector.

Thank you. Your next question comes from Aaron Gray with Alliance Global Partners. Please go ahead.

Thank you for the question. First question, obviously, there's a hope that we get the full plan rescheduled late summer or fall following the hearings. But potentially in the near term or if full plan rescheduling takes a little bit more time, In this scenario, do you potentially get a little bit more aggressive in medical-only states where you know you have the removal of 280E, or does that change any of the potential near-term landscape opportunities? Thanks.

I think it does allow us to reflect in our underwriting the different tax treatment of medical revenues versus adult use revenues. And I think it drives us to, we will have to, if adult use does not proceed on adult use sales, then it will lead to, I think, different lenses for medical versus adult use, if only because it drives different cash flow dynamics of the operators. And that is the fundamental basis of which I think all underwriters at this space will need to adjust. Again, I hope it's not needed. But if the fundamentals of cash flows need to be reflected in this, then it will be reflected in our underwriting and deployment as well.

Thanks. That's helpful, Collar. A lot of people in the industry talk about potential impact of the hemp ban coming to fruition in November, having a broader impact on the legal cannabis market. Curious to your view on that and your borrowers, potentially there being that ban coming to fruition and helping out the fundamentals of your borrowers.

and your view on that. Thank you. We've absolutely heard anecdotal feedback that the hemp ban has driven revenue increases, particularly in states that have a larger prevalence of smoke shops and these types of black market hemp CBD and cannabis-adjacent products. I think it's been difficult to find a direct link in the data, but certainly anecdotal and correlative links between the hemp ban and regulated cannabis. Okay, great. Thank you.

Just last question for me. In terms of liquidity and pipeline, any color on timing to having some things in the pipeline come to fruition? What's the liquidity you still have available? Thanks.

I think it's – our pipeline tends to refresh itself every three to six months, and in that period of time, we have the opportunity to explore whether these transactions that are in the pipeline are transactions that we seek to close or transactions that end up not being worthy of closing. But I think it's difficult to – it's difficult to forecast within that timeframe of what that deployment will be for better or worse. And in this, I'll point out that in this quarter, we have released our, as I think at investors' request, we have released a breakdown between real estate-backed and non-real estate loans within our portfolio in an effort to give our investors a better view into what portion of our pipeline is more directly fit for Chicago Atlantic real estate financing.

Yeah, very helpful. Appreciate that. disclosure and color in response to the questions. Thank you very much. I'll go ahead and jump back into the queue.

Thank you.

As there are no further questions from the participants, this concludes our question and answer session. Also, the conference has now concluded. We thank you for attending today's presentation, and you may now disconnect.