Transcript

Welcome to the Five Star Bancorp Second Quarter Earnings Webcast. Please note, this is a closed conference call, and you are encouraged to listen via the webcast. Before we get started, we would like to remind you that today's meeting will include some forward-looking statements within the meaning of applicable securities laws. These forward-looking statements relate to, among other things, current plans, expectations, events and industry trends that may affect the company's future operating results and financial position. Such statements involve risks and uncertainties, and future activities and results may differ materially from these expectations. For a more complete discussion of the risks and uncertainties that may cause actual results to differ materially from the company's forward-looking statements, please see the company's annual report on Form 10-K for the year ended December 31, 2024, and the quarterly report on Form 10-Q for the 3 months ended March 31, 2025, and in particular, the information set forth in Item 1A, Risk Factors in those reports. Please refer to Slide 2 of the presentation, which includes disclaimers regarding forward-looking statements, industry data, unaudited financial data and non-GAAP financial information included in this presentation. Reconciliations of non-GAAP financial measures to their most directly comparable GAAP figures are included in the appendix to the presentation. The presentation will be referenced during this call, but not followed exactly and is available for close reviewing on the company's website under the Investor Relations tab. Please also note today's event is being recorded. At this time, I'd like to turn the presentation over to James Beckwith, Five Star Bancorp President and CEO. Please go ahead.

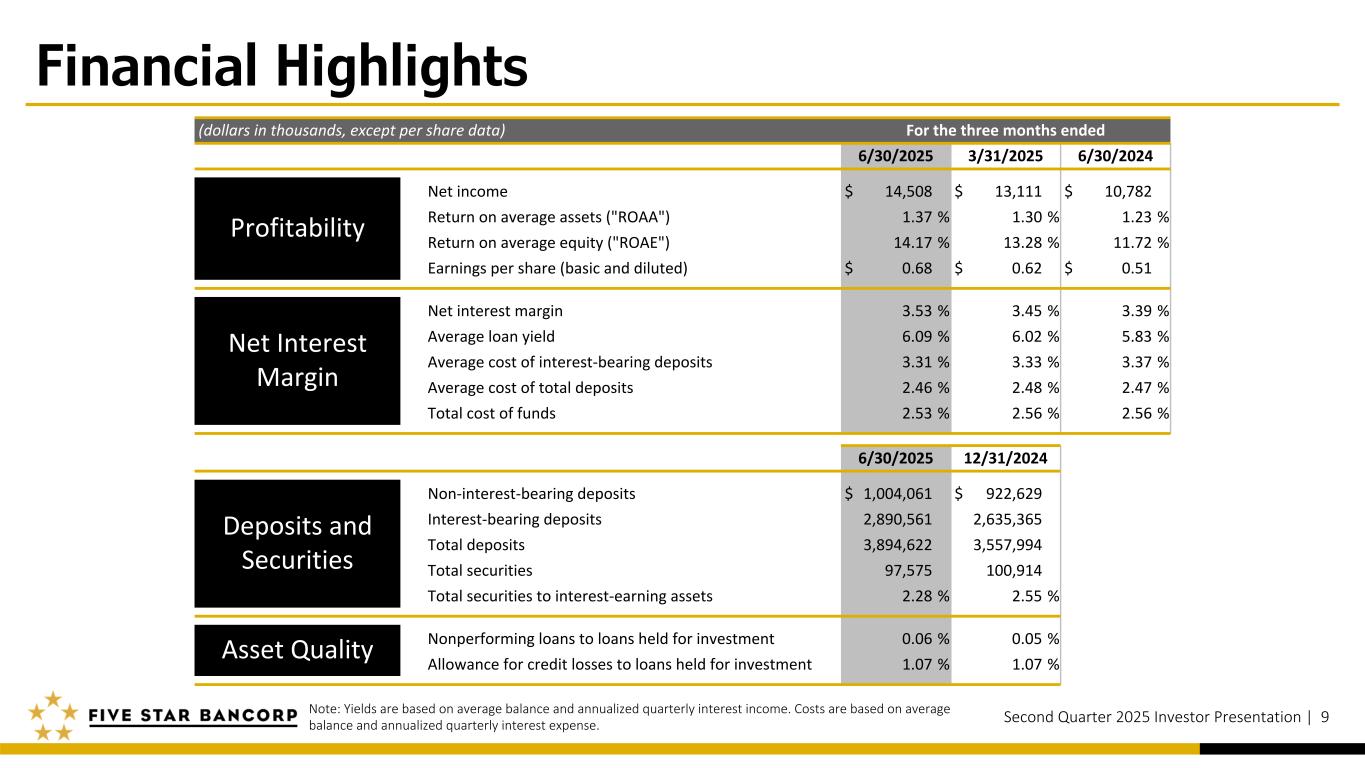

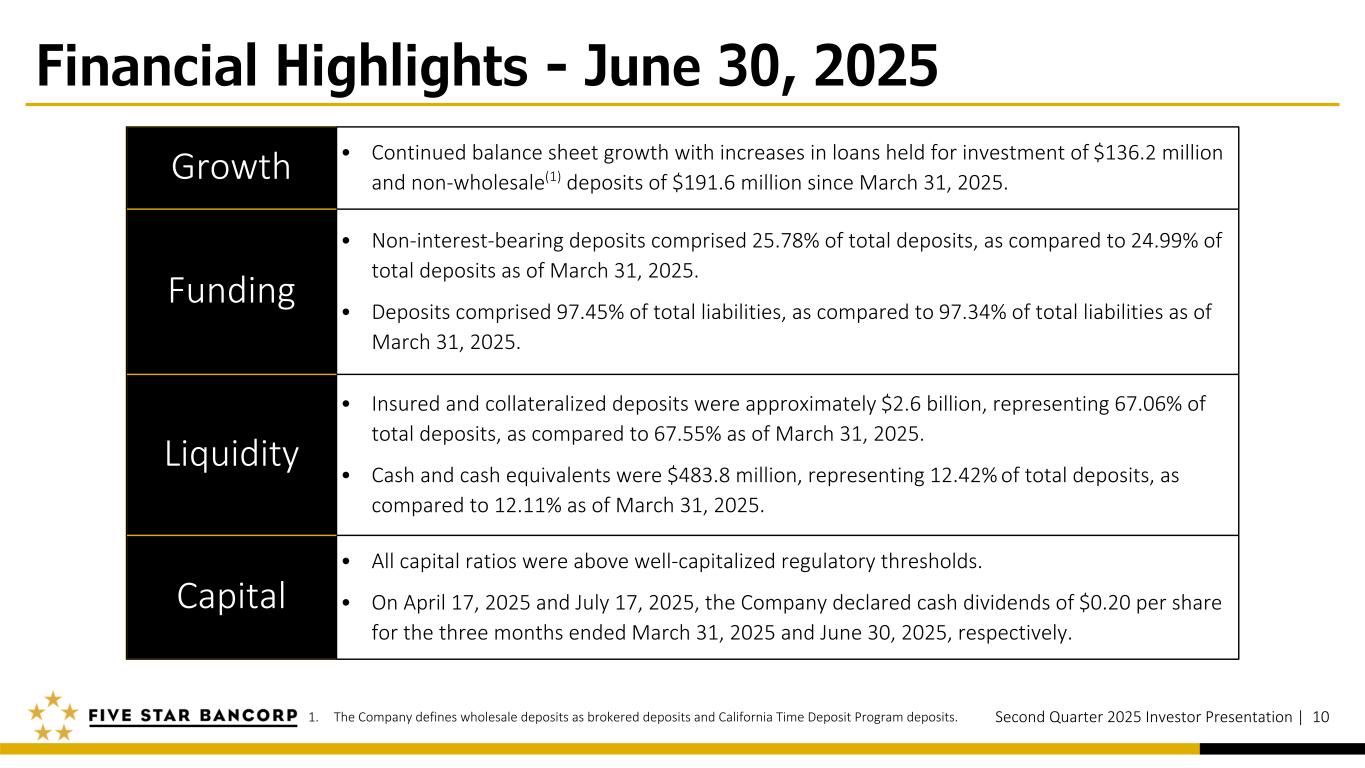

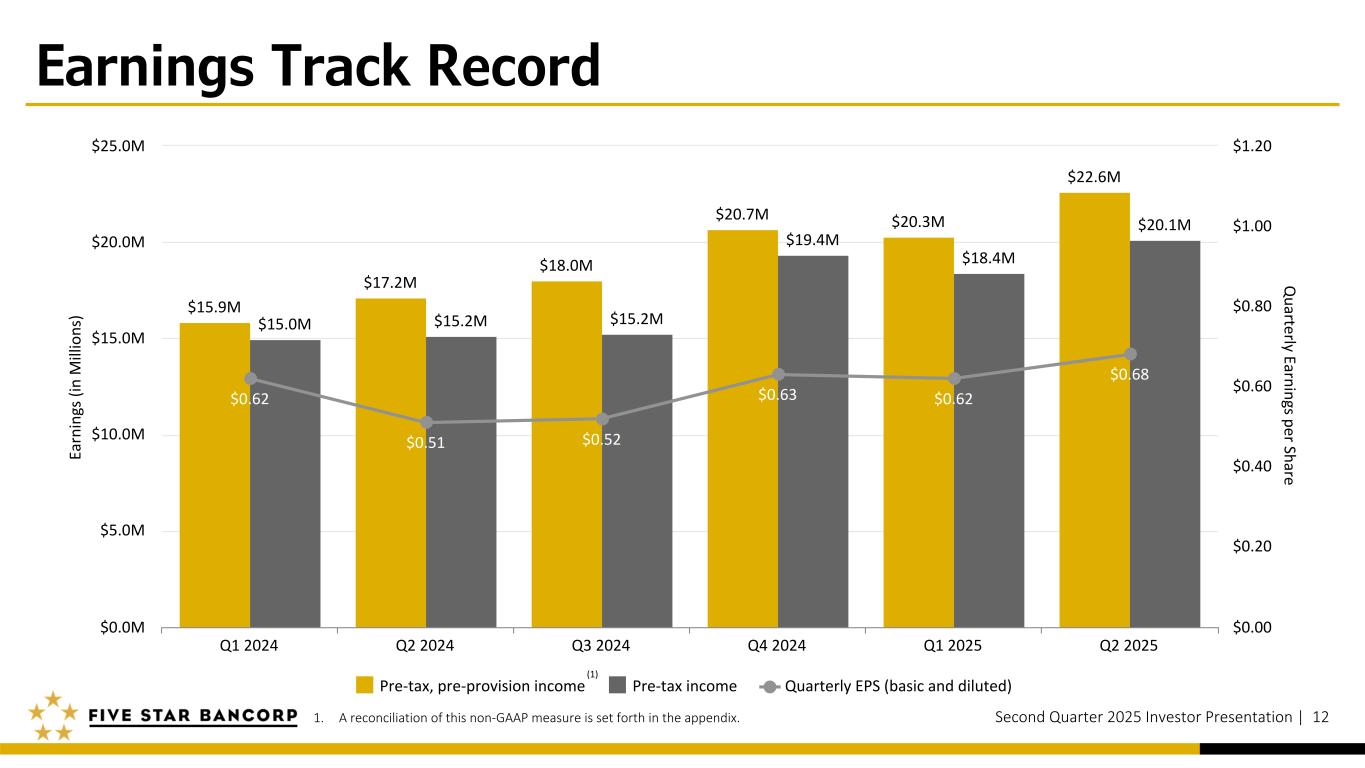

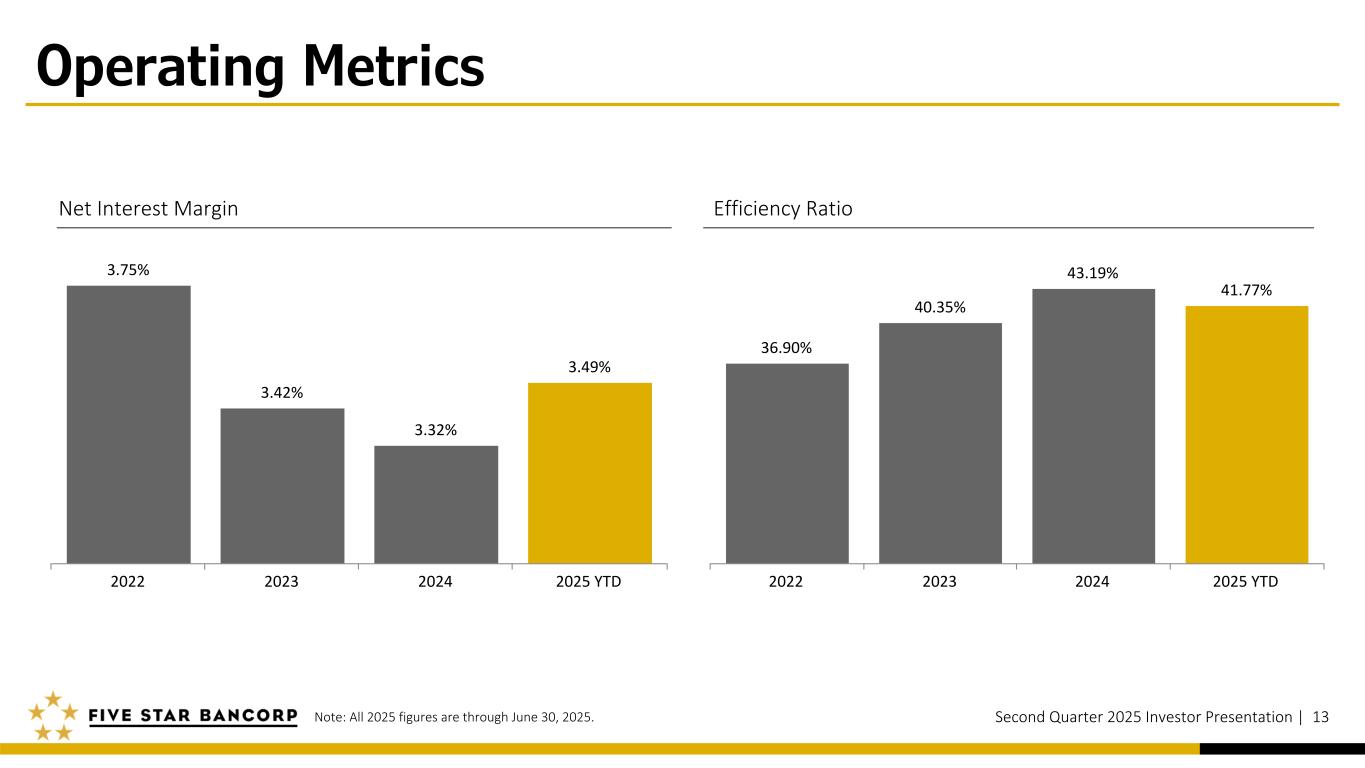

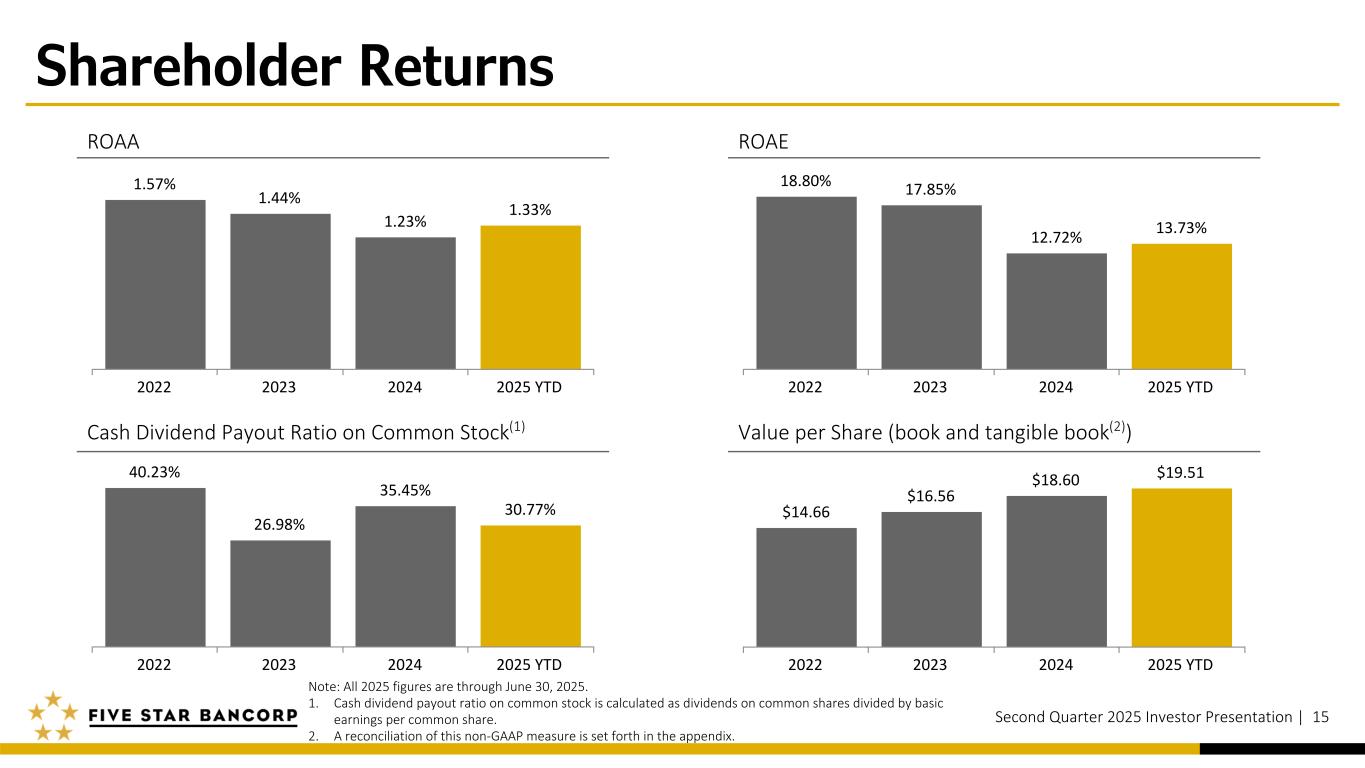

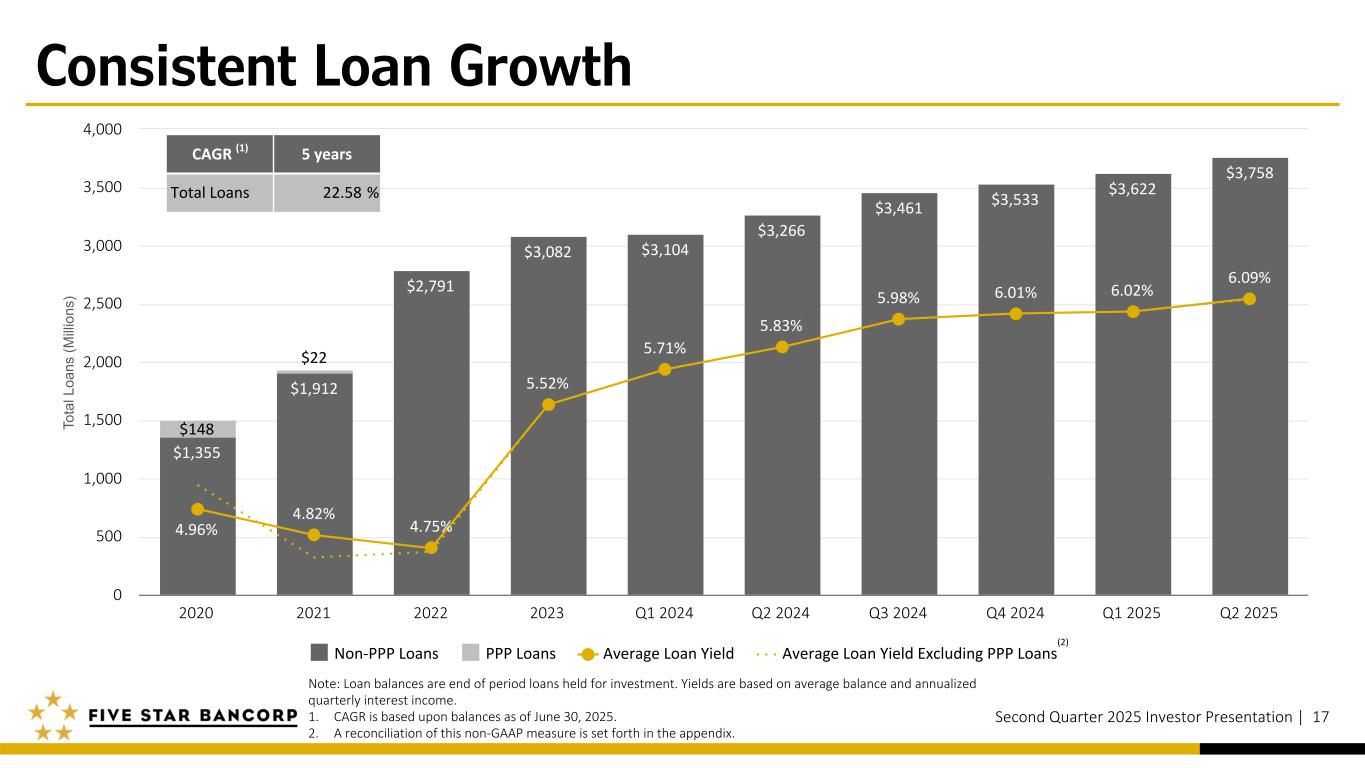

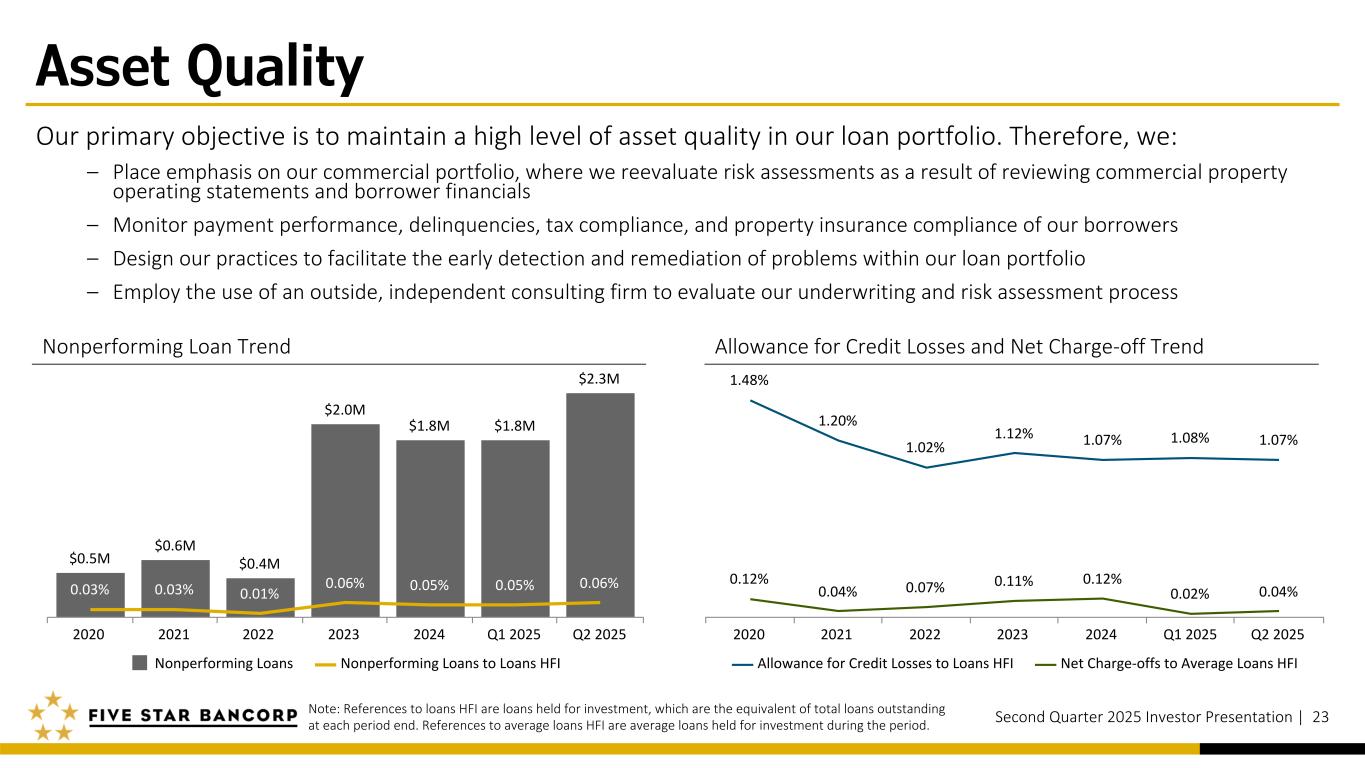

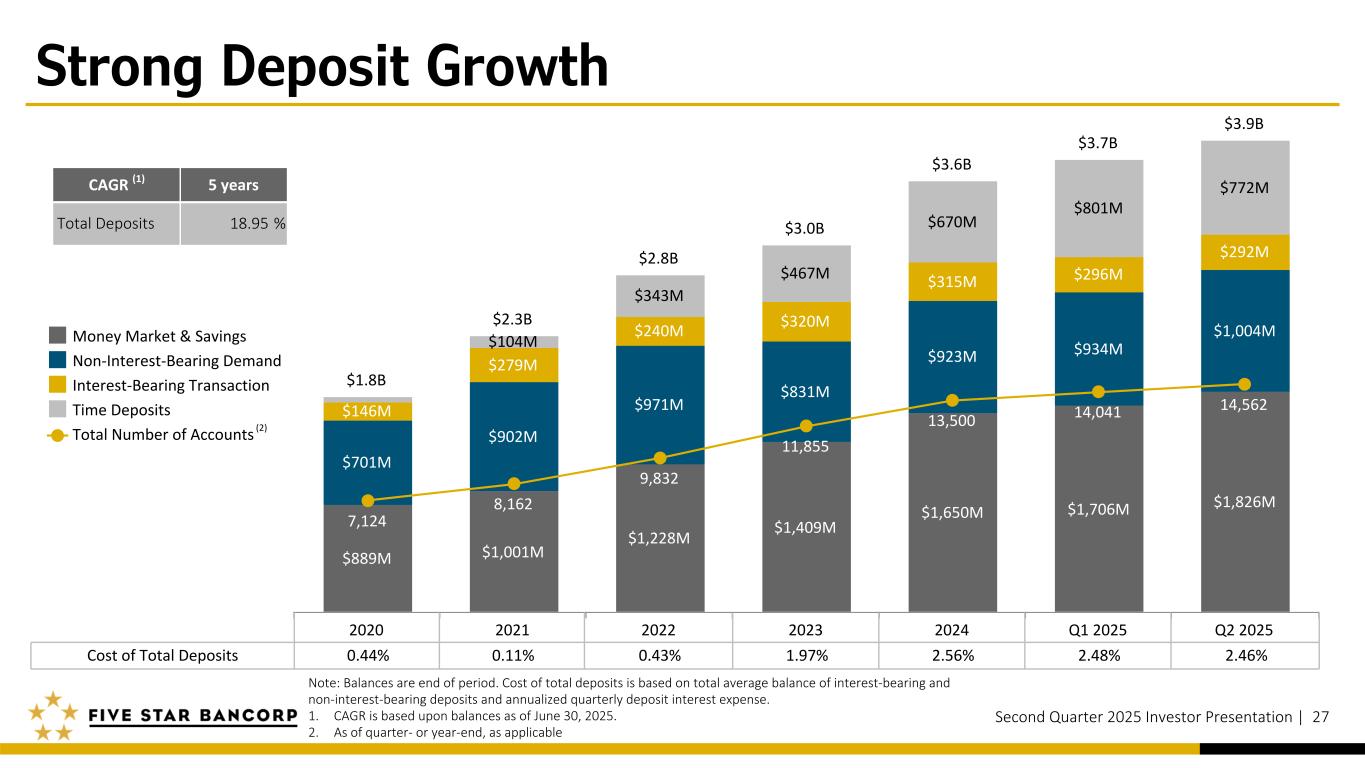

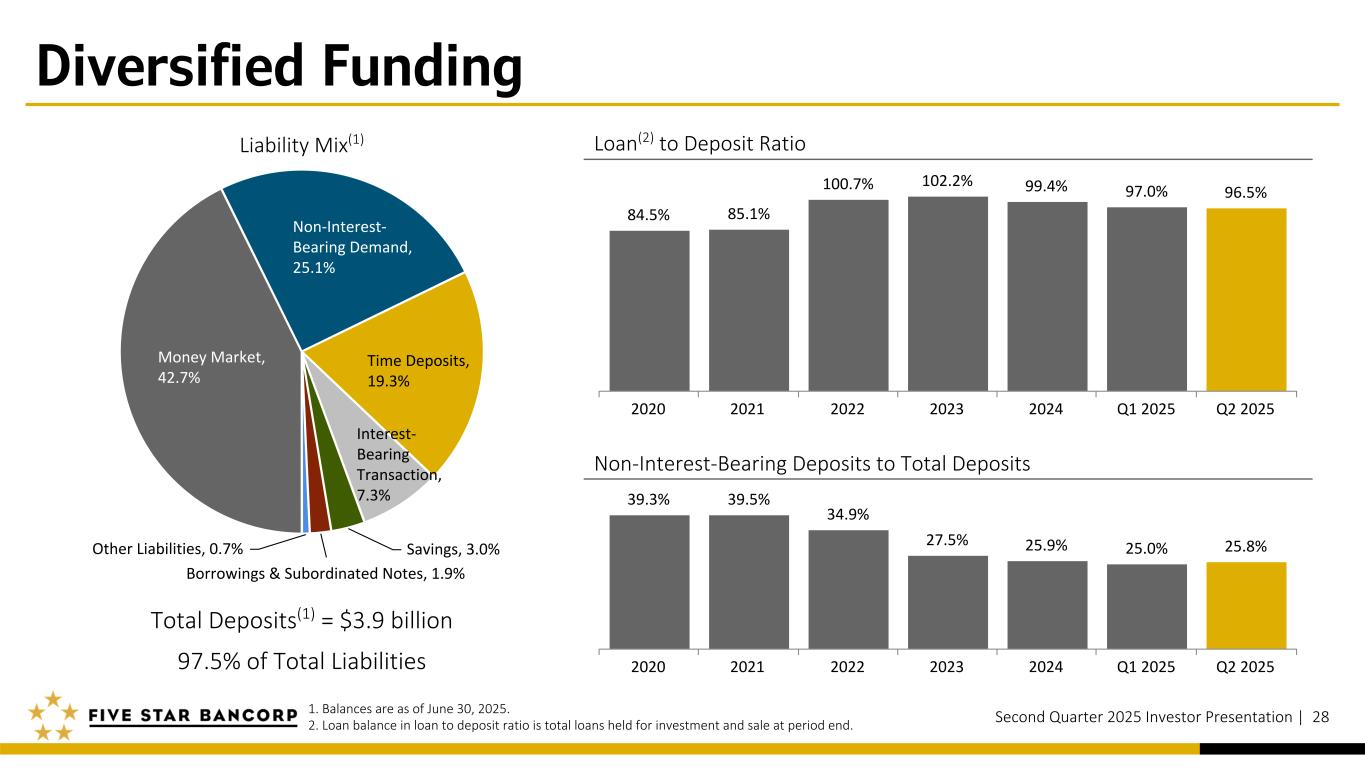

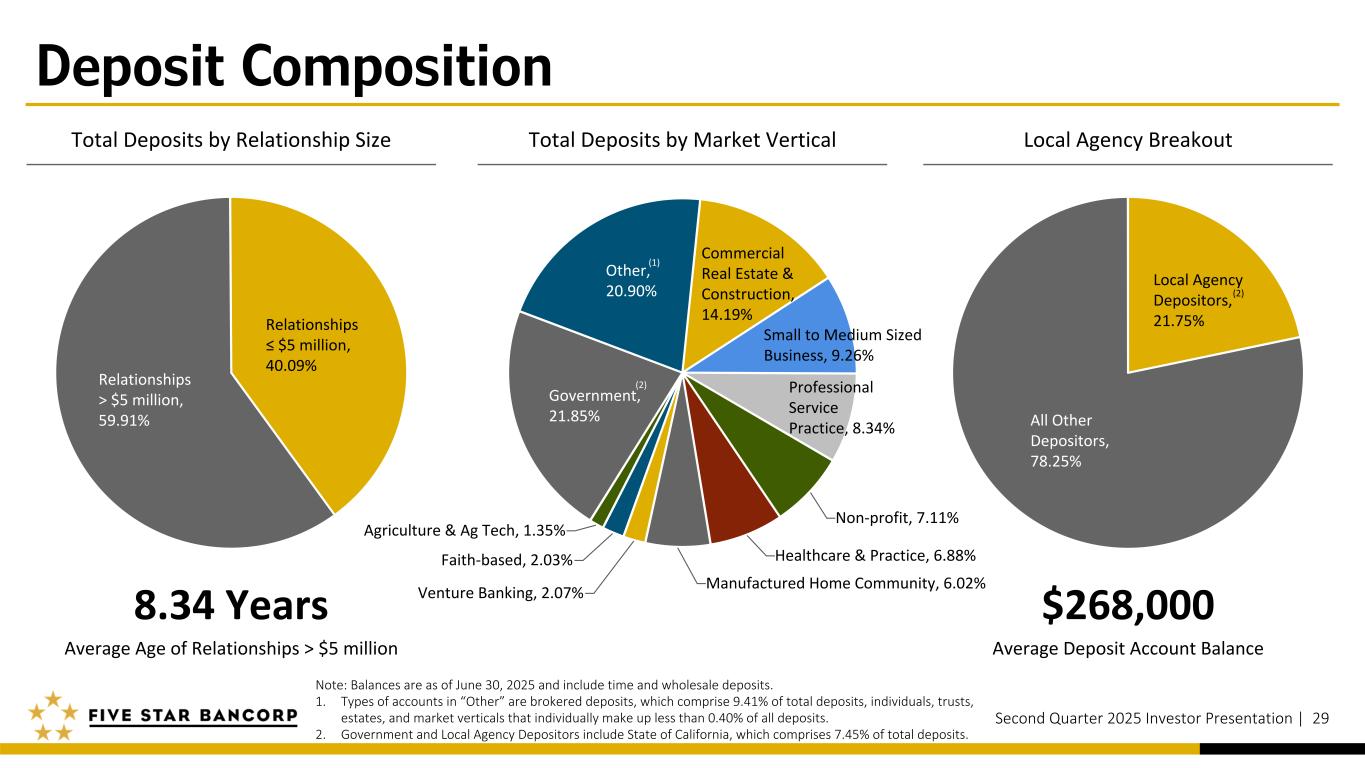

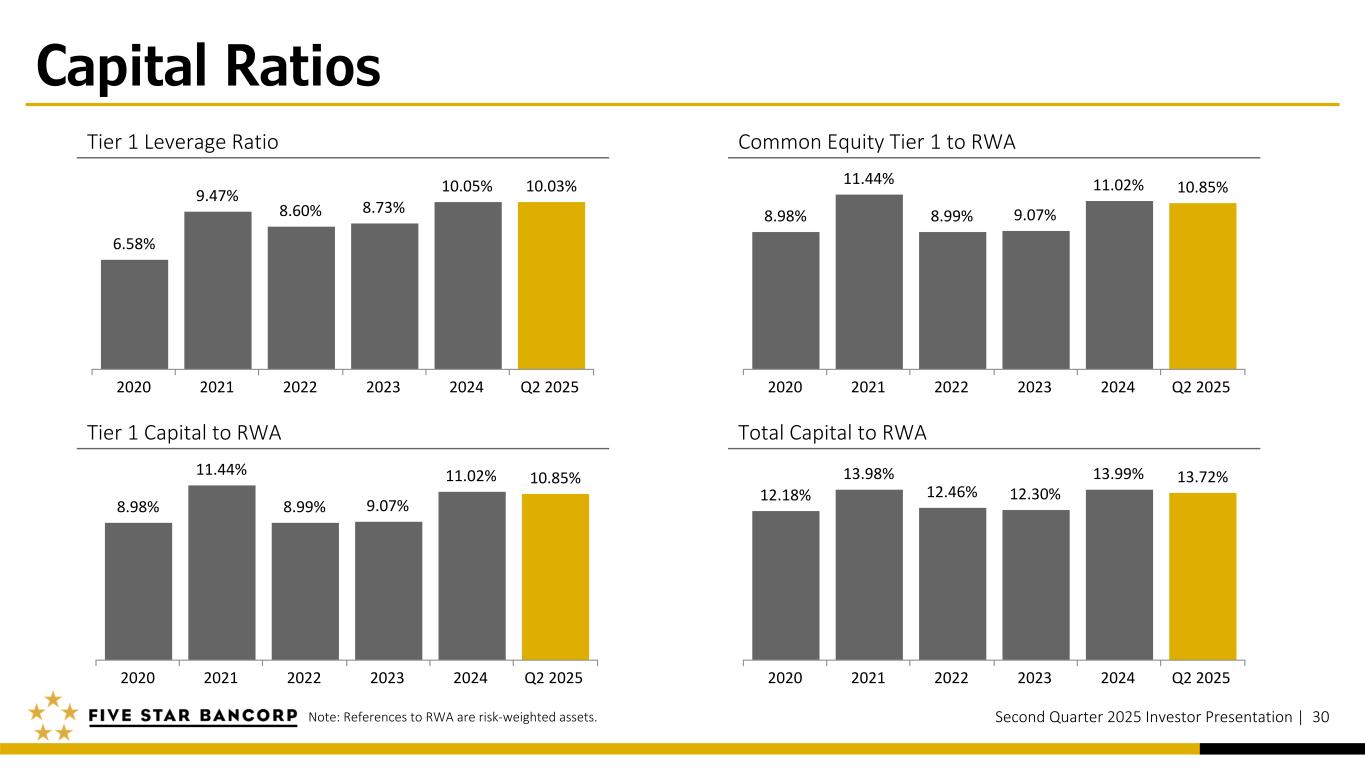

Thank you for joining us to review Five Star Bancorp's financial results for the second quarter of 2025, which were released yesterday. The release is available on our website at fivestarbank.com under the Investor Relations tab. Joining me today is Heather Luck, Executive Vice President and Chief Financial Officer. The strength of our second quarter results is emblematic of our differentiated client experience through our unwavering commitment to clients and community partners throughout Northern California. Financial highlights during the second quarter included $14.5 million of net income, earnings per share of $0.68, return on average assets of 1.37% and return on average equity of 14.17%. Our net interest margin expanded by 8 basis points to 3.53% and our cost of total deposits declined by 2 basis points to 2.46%. Our efficiency ratio was 41.03% for the second quarter. During the second quarter, we saw continued balance sheet growth as loans held for investment grew by $136.2 million or 15% on an annualized basis. Deposit growth was approximately $158.3 million or 17% on an annualized basis. Our asset quality remains strong with nonperforming loans representing only 6 basis points of total loans held for investment. We continue to be well capitalized with all capital ratios well above regulatory thresholds for the quarter. On July 17, our Board declared a cash dividend of $0.20 per share on the company's common stock expected to be paid in August. We continue to deliver value to our shareholders. Our total assets increased during the second quarter by $168.4 million, largely driven by loan portfolio growth within our commercial real estate portfolio, which grew by $125.4 million. Our loan pipeline remains strong. The credit quality of our overall loan portfolio remains strong due to our conservative underwriting practices, robust monitoring program throughout the life of a loan and our relationship-based approach to lending. As a result, we have a very low volume of nonperforming loans despite a $0.5 million increase during the second quarter. This increase was due to one commercial real estate loan being put on nonaccrual status during the quarter. We recorded a $2.5 million provision for credit losses during the quarter. The increase in our total liabilities during the second quarter was primarily the result of increases in both interest-bearing and noninterest-bearing deposits. Interest-bearing deposit growth was largely due to new money market deposit accounts being opened in the quarter, adding $87.4 million in new balances. Noninterest-bearing deposits were mainly driven by the opening of new accounts during the quarter, adding $68.7 million in new balances. Noninterest-bearing deposits made up 26% of total deposits as of June 30, 2025, an increase from 25% at the end of the prior quarter. Approximately 59.9% of our deposit relationships total more than $5 million. These deposits have a long tenure with the bank, with an average age of 8.3 years. We believe our deposit portfolio to be a stable funding base for our future growth. Heather?

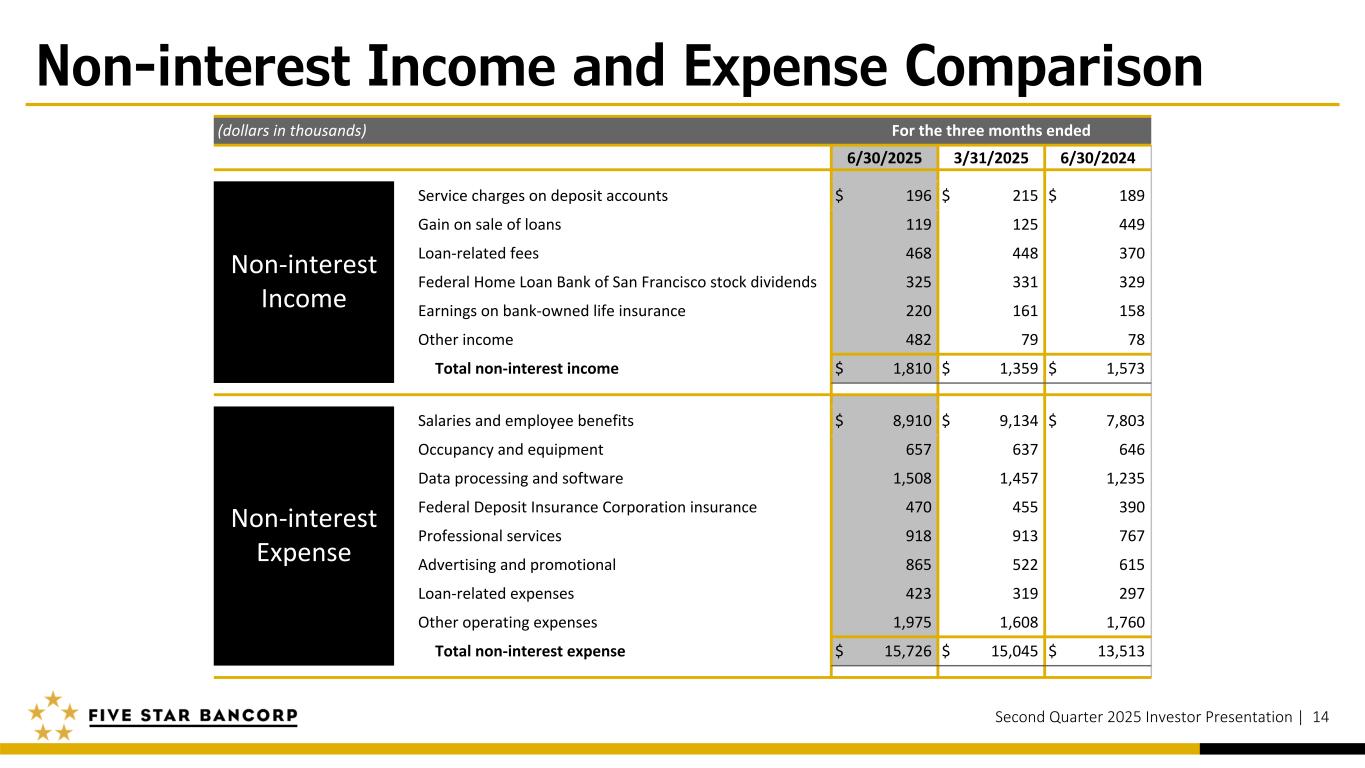

Thank you, James. Net interest income increased $2.5 million from the previous quarter, primarily due to a $3.5 million increase in interest income, driven by loan growth and improvement in the average yield on loans. This is partially offset by a $1 million increase in interest expense related to deposit growth. Noninterest income increased to $1.8 million in the second quarter from $1.4 million in the previous quarter, primarily due to an overall improvement in the estimated earnings related to investments in venture-backed funds during the 3 months ended June 30, 2025. Noninterest expense grew by $700,000 in the 3 months ended June 30, primarily due to increases in business travel, conferences, training and promotional expenses associated with the expansion of business development teams. This was partially offset by an increase in deferred loan origination costs. I'll now hand it back to James.

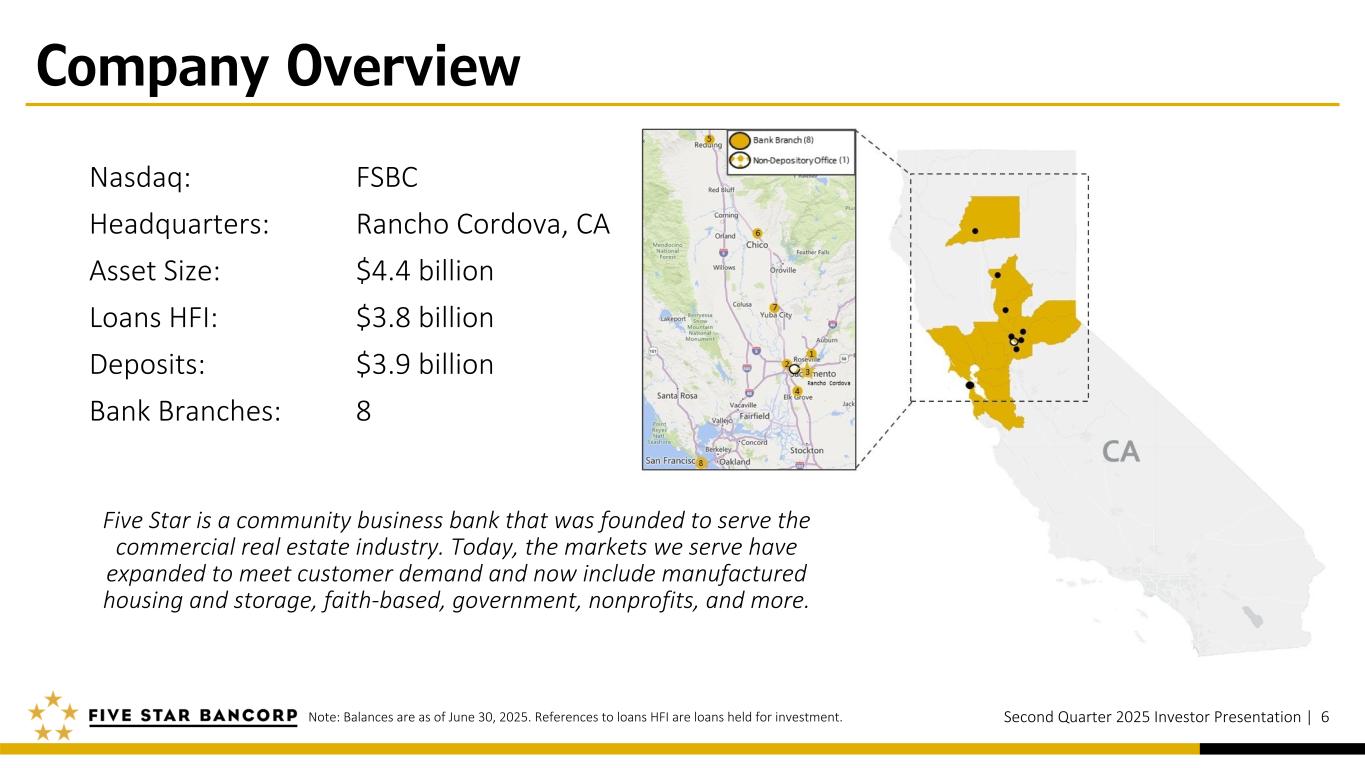

Thank you, Heather. During the quarter, we announced the expansion of our food and agribusiness vertical. We also announced the expected opening of our Walnut Creek office in September of 2025 and added 5 new business development officers to the team to support these efforts. We continue to grow our presence in the San Francisco Bay Area with 34 employees and $456.9 million in deposits as of June 30, 2025. Five Star Bank has a reputation built on trust, speed to serve and certainty of execution, all of which support our clients' success. Our financial performance is the result of a truly differentiated client experience, which continues to power the demand for Five Star Bank's relationship-based services. We are proud to have earned the trust and confidence of those we serve, including our shareholders. As we move into the third quarter of 2025, we are confident in the company's resilience and demonstrated ability to adapt to changing economic conditions while remaining focused on the future and execution of our long-term strategic plan. The beneficiaries of our focused business approach are our clients, employees and community. We believe that if we support these constituents well, our shareholders will realize the benefits. We appreciate your time today. This concludes today's presentation. Now we will be happy to take any questions you might have.

Our first question today comes from David Feaster from Raymond James.

I want to start. I mean, obviously, you guys have had good loan growth. But to me, the most impressive thing that you guys have been able to do is your core deposit growth. I mean it is extremely impressive, and I know it's not easy to do. Could you just touch on where you're having success? Obviously, some in the Bay Area. Could you just touch on your thoughts on your ability to continue to drive core deposit growth and the ability to reduce deposit costs? I mean, is there much funding cost leverage left?

Well, let me take the first part of your question first, if I could. So we saw growth across our entire platform, all of our verticals and all of our geographies. And so I think the reason for that, David, is fundamentally that we've got a lot of feet on the street. We've got 40 business development officers now that are highly motivated, very experienced and well connected into the communities and the industries they serve. So that's what's really driving this. Everybody is having success. And we're very supportive of those efforts. We spent a lot of time. Personally, I spent a lot of time with them in terms of bringing in new relationships to the bank. From a funding cost perspective, I think we've kind of seen the end of any effects of any rate cuts. And I know we're all standing around in the kitchen waiting for the Fed to make cuts again. But we're not really expecting that to happen. And we're not sure when that might happen, but we’re not relying on that happening. I think you're seeing our funding costs will continue to maybe go down just a little bit more, but it's really about the mix. And to the extent that we have a very successful last half of 2025 in terms of raising noninterest-bearing deposits, we believe we've got some really great opportunities in our deposit pipeline right now to achieve that. So it's really about fundamental execution, David, and the fact that we just have so many feet on the street.

That's great. And then maybe just touching on the Bay Area maybe a bit more broadly. I mean, you've obviously had a lot of success in San Francisco. It's been really impressive. You've got the Walnut Creek office opening here soon. I'm curious, maybe, first of all, could you maybe touch on the pulse of the Bay Area from your standpoint? And how much opportunity you see left there in terms of both hiring and expansion in that market? Obviously, it's a huge market, but just kind of curious the opportunities and the potential that you see in the Bay Area.

Sure. We're excited about the Walnut Creek opening. I was there this week, a couple of days ago. And the business environment in the Bay Area has changed in the last couple of years. Just take San Francisco, in particular, there's a new mayor there, very energetic, business-minded. I think that city is turning around. It's just palpable in terms of — if you're in downtown in the financial district, you get that sense. So I'm excited about that. And Walnut Creek is a beautiful place. It has a great shopping district, great food scene, and it's growing. It has done well as a stand-alone area since the pandemic, especially considering the migration to the East Bay. So we're excited about what we're doing in the Bay Area. Future expansions in the Bay, I think you could probably expect to see in the South Bay. Those efforts are underway right now. I can't really share any visibility on that with you right now, but certainly, that's where we're headed. We’ve got to ensure that our Walnut Creek operations are sound and solid, and grow robustly. We have some great business development people focused on Walnut Creek in the East Bay who have joined us in the last year and the last 6 months. So — but anyway, that's how we see it. We're not done expanding in the Bay, and the next expansion outside of Walnut Creek will probably be somewhere in the South Bay.

That's great. And then maybe last one for me. Your business model is extremely scalable. You've done a great job driving substantial revenue growth with the infrastructure you've got, still continuing to invest. I mean, we're sitting here with the low 40% efficiency ratio. Look, the stage is set for continued outsized loan growth and revenue growth, with the potential for further margin expansion as we continue to reprice the back book. Is a sub-40% efficiency ratio in the cards? Or are there other investments or expenses that you may wish to accelerate just given the strength you're seeing? Just kind of curious, how do you think about that?

Well, we're very keen to continue to invest in our business. We did announce in the second quarter that we've expanded our food and agribusiness business, and we've brought in some very seasoned professionals that have great connectivity to the space. We're continuing to invest in our business. These folks are in mid-career and not necessarily inexpensive, let me say that much, but we're happy to have them. We think we're going to expect great things. I single that out, David, just as an example of how we continuously invest in our business. We're always looking to add talent. To achieve something that's sub-40% is not necessarily a goal per se, but I could see it happening. We do have a lot of operating leverage in our business right now. So we’ll see what the rest of the year looks like.

And then, David, just to add on to that, while we have expanded our headcount from a business development and customer-facing side, we have also continued to build out our back-office support teams as well. So in those mixtures, you're seeing not only sales growth, but you are seeing back-office support as well. From my perspective, there's no real significant investments that we need to make to either improve our technology or improve the support side. So really, we're just adding more headcount to ensure that we're supporting our customers and staff as appropriate.

Our next question comes from Woody Lay from KBW.

Maybe just one quick follow-up on expenses. Just how should we think about the run rate in the third quarter with the Walnut Creek office coming online?

Yes. I would say, add about $500,000 to $750,000 for next quarter. We will have a little bit of increased expense for Walnut Creek. So that should probably bake in enough for your estimate.

All right. Very helpful. And then I had a follow-up on deposits as well in the noninterest-bearing segment; I saw really strong growth in the quarter. I was just curious how sticky do you view that growth? I know you've got some wealthier clients and wasn't sure if it was kind of just a one-quarter increase or if you think that the jump up is sustainable from here.

Woody, we believe it to be sustainable. As we continue to bring on new relationships, that all have some component of noninterest-bearing deposits in those relationships. So we think that will continue to grow. There’s nothing that stands out in terms of an anomaly at all. It's just — it's growth in accounts, number one, in new accounts.

All right. And then last for me. Just looking at the growth in the quarter, it looks like it was mostly driven from the CRE bucket. I was just curious about the sub-verticals where you're seeing the best growth opportunities and vice versa, maybe other verticals where you're not looking to grow at this time.

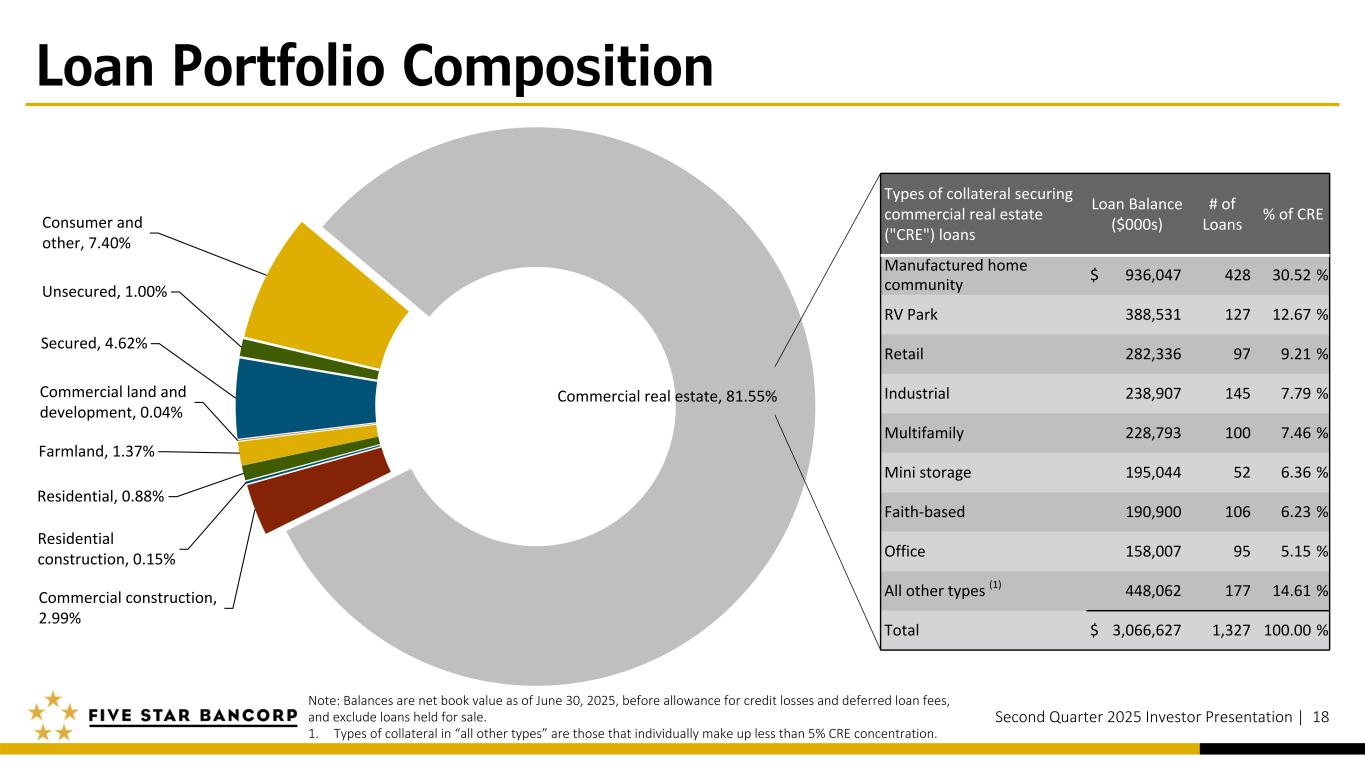

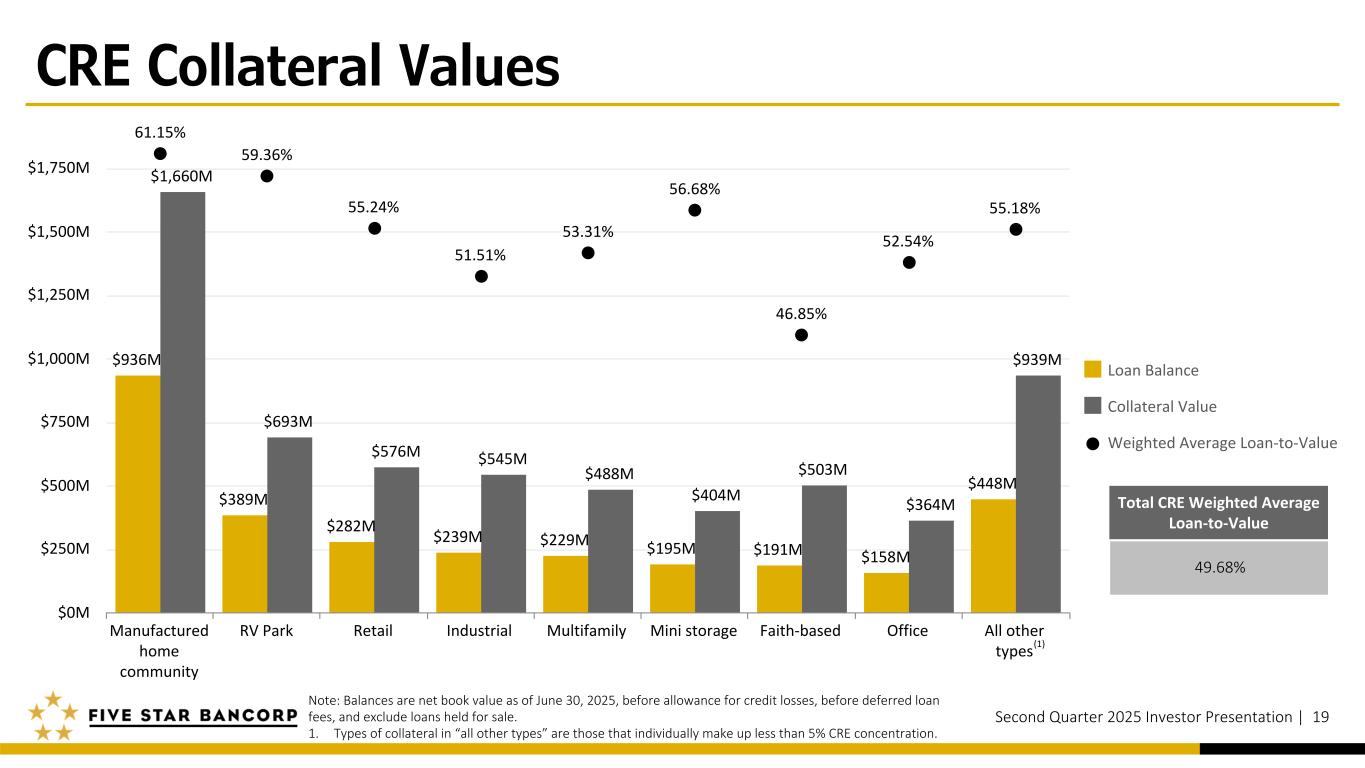

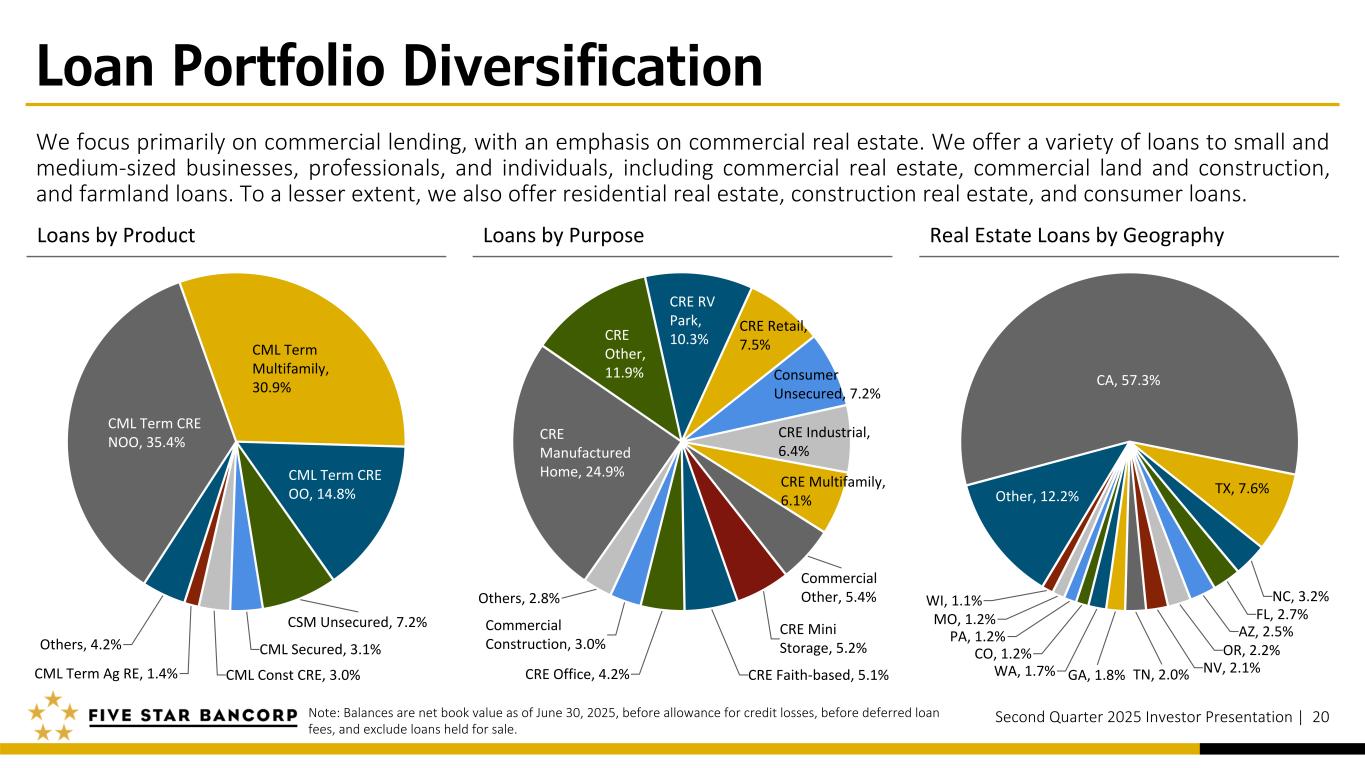

I think we're looking to grow all of our verticals across the board. I mean, we continue to be very active in mobile home parks, RV parks, along with storage. We are doing pretty well in multifamily, particularly student housing. So those are areas that I think we've done a decent job on. We've also financed some office buildings. Now I don't want you to worry or anything, Woody, but these are buildings in which new capital came to the table. Along with this massive reset that’s going on, new equity comes to the table, and price per square foot is now $250 to $350 a foot as opposed to $900 to $1,000 a foot of what it was 5 years ago. We feel these loans are incredibly safe. This is about the turnaround that we’re seeing, particularly in downtown San Francisco. So those particular categories make up a lot of the growth that we saw in our CRE portfolio.

Our next question comes from Gary Tenner from D.A. Davidson.

Ahmad Hasan on for Gary here. Can you talk about — can you give us a specific number on loan purchases in this quarter? And what's in the docket for the next half of the year?

On loan purchases? Yes. What we're doing is maintaining our balances that we've had. I think we established this probably last — third quarter of last year. So we're running about — we try to target $300 million of what we call Bankers Health Group purchases, not purchases, but outstanding balance. And because these loans amortize quickly, we constantly have to...

Yes. We made during the quarter about $44 million in purchases, but really, that's just to keep the concentration within that $300 million range. So you'll see purchases there, but it's just a renewal payoff.

Yes. So we're targeting an average outstanding of around $300 million for those loans.

Okay. That makes sense. And great NIM expansion this quarter. Anything unusual in the loan yield expansion of 7 basis points?

No. It's just — it's a combination of a bunch of different things. One, as our loan book continues to reprice, most of the loans that we do have 5-year resets in our commercial real estate space. These loans that were put on in 2020 are now resetting from very low rates. So you have that impact. But you also have all of our current production, which is at a much higher rate.

Yes. The Q2 production that we did had a weighted average rate of 7.03%. So that was a nice pickup to the NIM.

So that's how we've been able to expand our yields in our loan portfolio — repricing combined with our new production driving it.

That's great to hear. And last one for me. On the tax rate outlook for the remainder of '25 and beyond, with regards to the new California tax law change. Can you give us your outlook on that?

Yes. For your modeling purposes, I would use a tax rate of about 26.83%. That's our statutory rate. We're forecasting an effective tax rate of about 26.65%. So that tends to fluctuate a little bit depending on permanent items, but within that range should be good for your model.

We were very happy to see the governor sign that bill, by the way.

And our next question comes from Andrew Terrell from Stephens.

This is Jackson Laurent on for Andrew Terrell. Most of my questions have been asked, but if I could just piggyback on loan growth. Obviously, growth was very impressive this quarter. I believe we were talking about a 10% to 12% balance sheet growth number for 2025 last quarter. I was just wondering if you could kind of give us some updates on how you expect loan growth to trend in the back half of the year? And if you're still thinking about growth in the 10% to 12% range for the full year?

Yes. Obviously, we've done a little better than that. But when I look at our pipeline and what I expect to pay off, I still feel comfortable in that particular range. We've got some large construction loans that will probably pay off sometime in the next year, and they're doing quite well. Lease-up has actually done really well. So we expect them to probably close with another shop, probably — excuse me, with an agency, not another bank, for bid. We’re going to stick with that guide on both sides of the balance sheet; we think if we can achieve that low teen growth, we believe we’ll do quite well at the bottom line. Our pipelines are good, a very strong loan pipeline and our deposit pipelines. So we’re excited about that. We think that’s a reasonable assumption in terms of growth as we move forward to the last half of 2025.

Got it. That's great color. And then just lastly for me, if you could give us a little bit more color on the new food and agribusiness vertical, as well as just a little bit more about the team in place. I know it's early innings, but I would love to get a sense of the growth potential you see from that business going forward.

Sure. The group that we hired is led by Cliff Cooper. He's got a very experienced team that he works with. They’re going after large — initially large processors, all types of ag commodities that exist on the West Coast. These credits that we're going after are C&I middle-market type of credits, companies whose revenue could be $50 million to $0.5 billion and that have been in business for generations. We believe this particular market to be underserved by the majors. This is why we're stepping in here. California is a big ag state. We were doing some ag prior to Cliff and his team joining us, but we never felt like we were taking advantage of the opportunity. With Cliff and his team, we see a tremendous amount of opportunity. One, in terms of it will help us maybe balance out our loan portfolio. Maybe over the long run, we’ll be able to reduce our concentrations in commercial real estate if Cliff is successful. We have every reason to believe he will be. And so we’re very excited about that.

Ladies and gentlemen, at this time, that will end today's question-and-answer session. I'd like to turn the floor back over to Mr. Beckwith for any closing remarks.

Thank you. It is with deep appreciation and gratitude that we have advocated for our clients and championed the communities we serve. We always will. As our expansion in the San Francisco Bay Area continues and as we build on the legacy of superior community banking in the capital region and North State, we answer the call of businesses and organizations who desire a time-honored banking partner. Five Star Bancorp is here to stay. We are proud to have experienced another quarter of significant organic growth built upon a sturdy foundation of client service, expanded relationships and products, and the loyalty of our exceptional clients. We will always remember that we exist because our clients trust us. And we believe in them. It's our privilege to continue as a driving force of economic development, a trusted resource for our clients and a committed advocate for our communities. We look forward to speaking with you again in October to discuss earnings for the third quarter of 2025. Have a great day, and thank you for listening.

The conference has now concluded. We thank you for attending today's presentation.