Call highlights

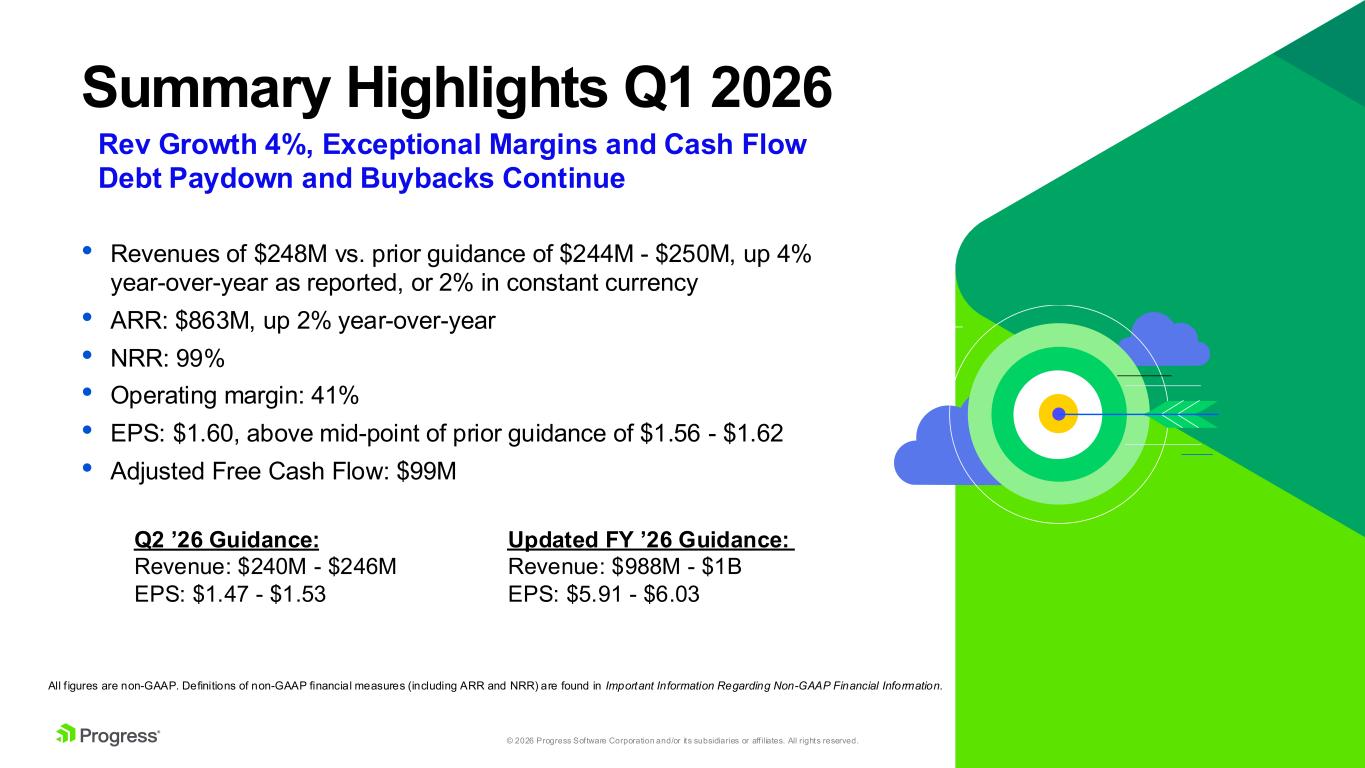

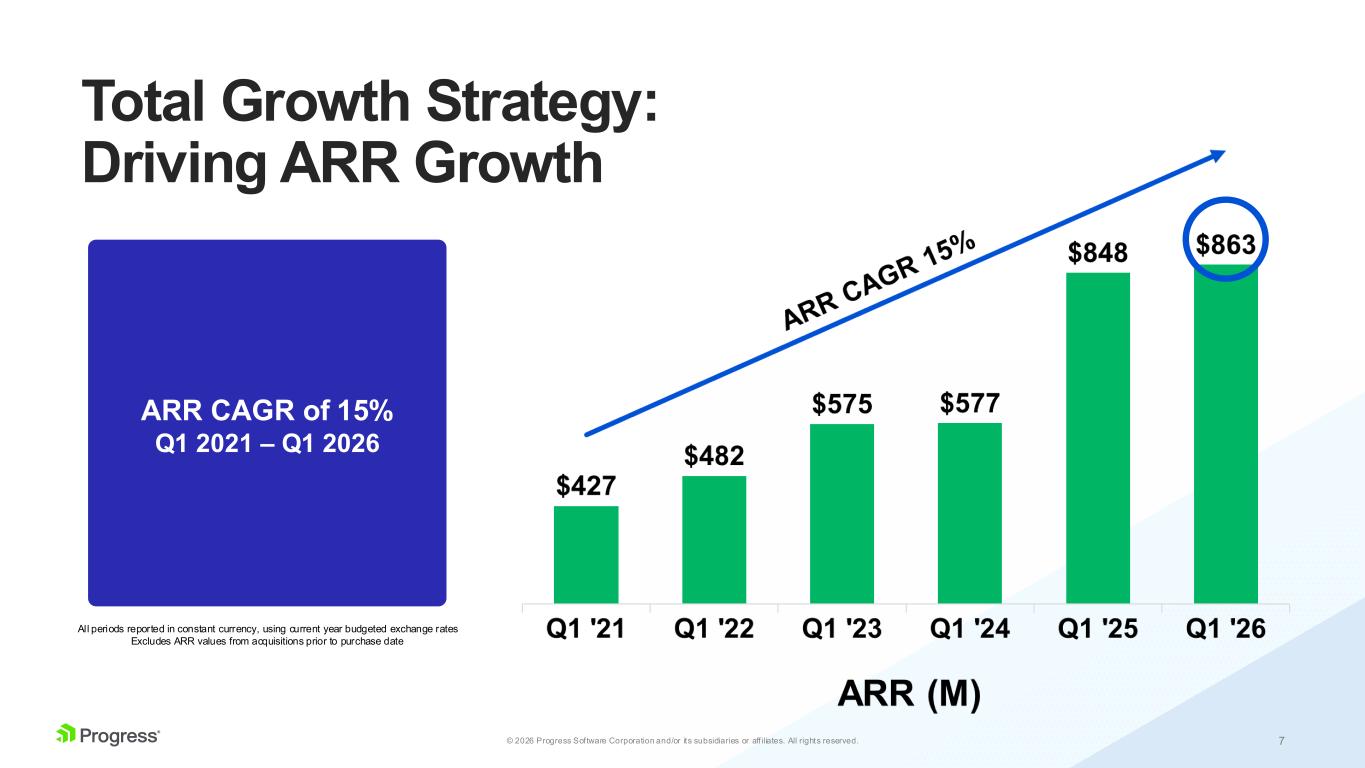

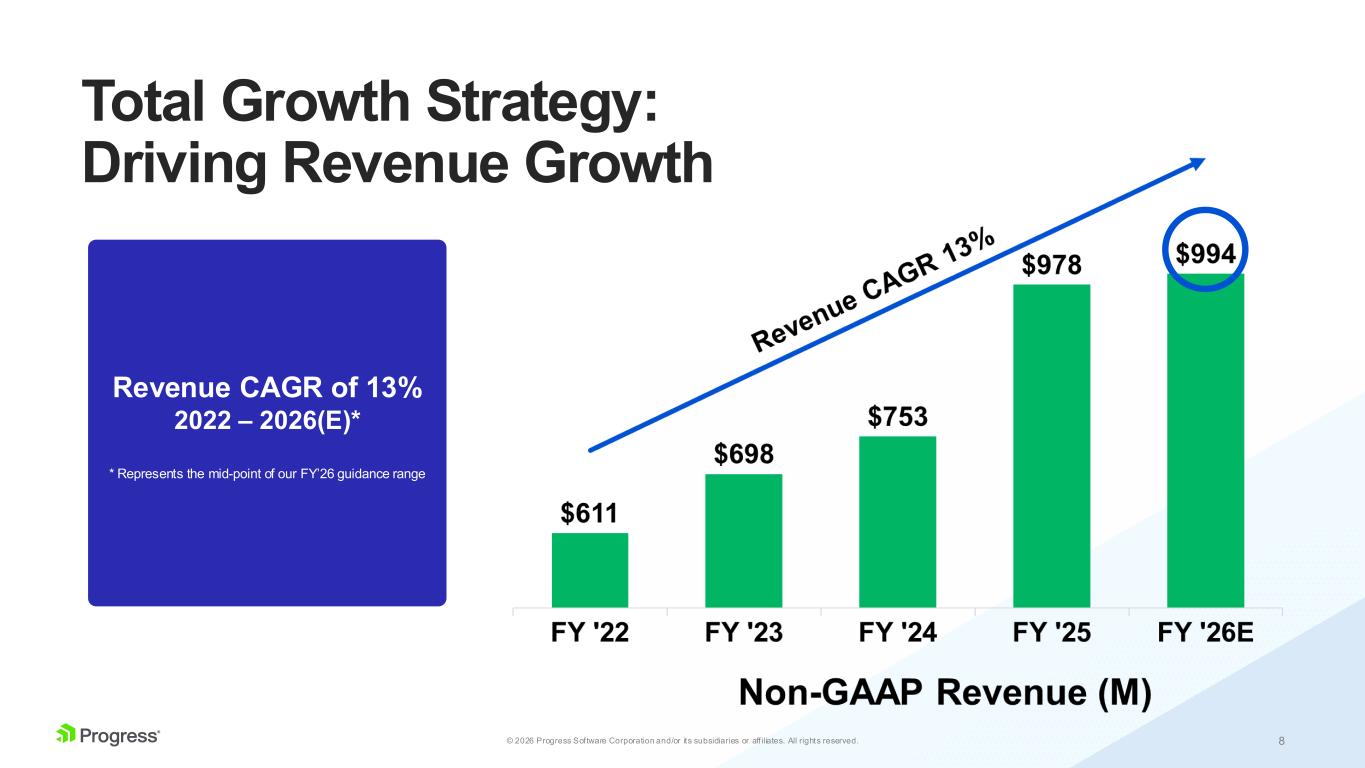

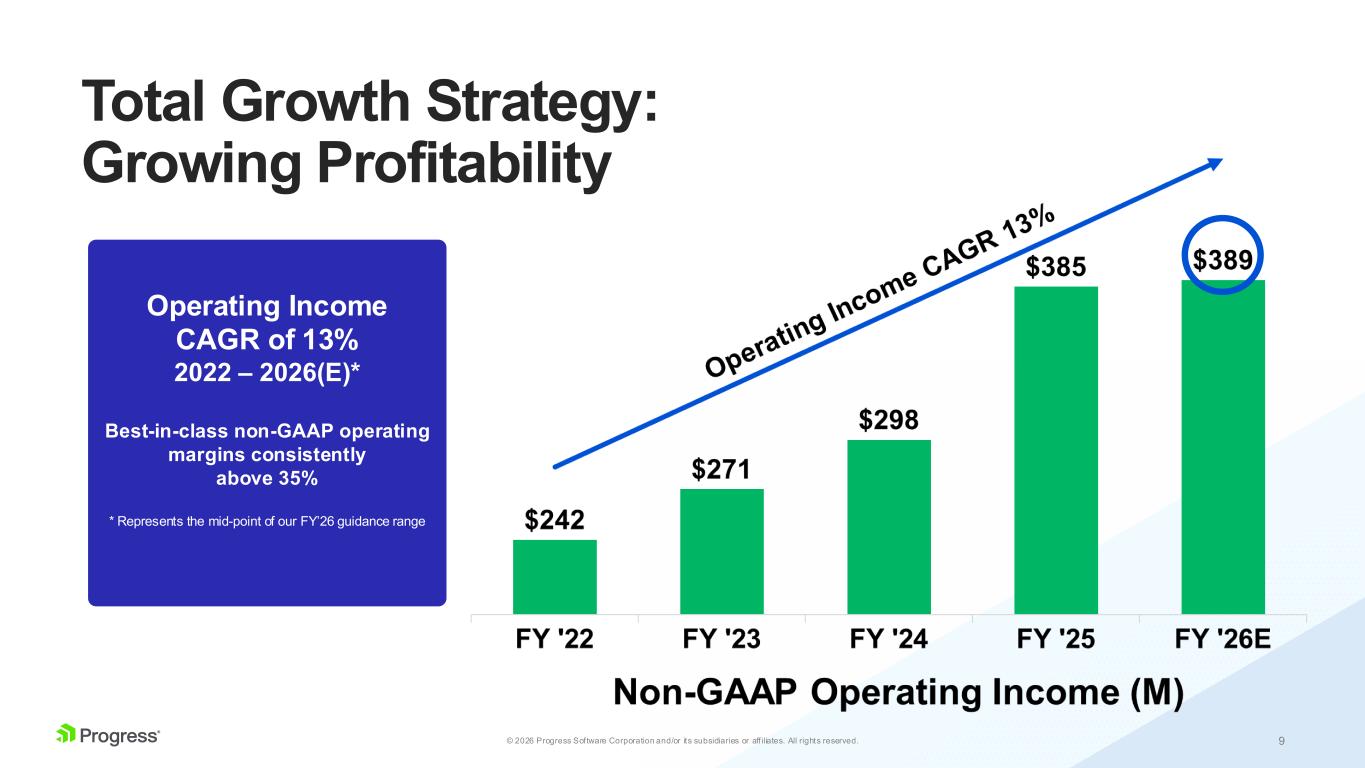

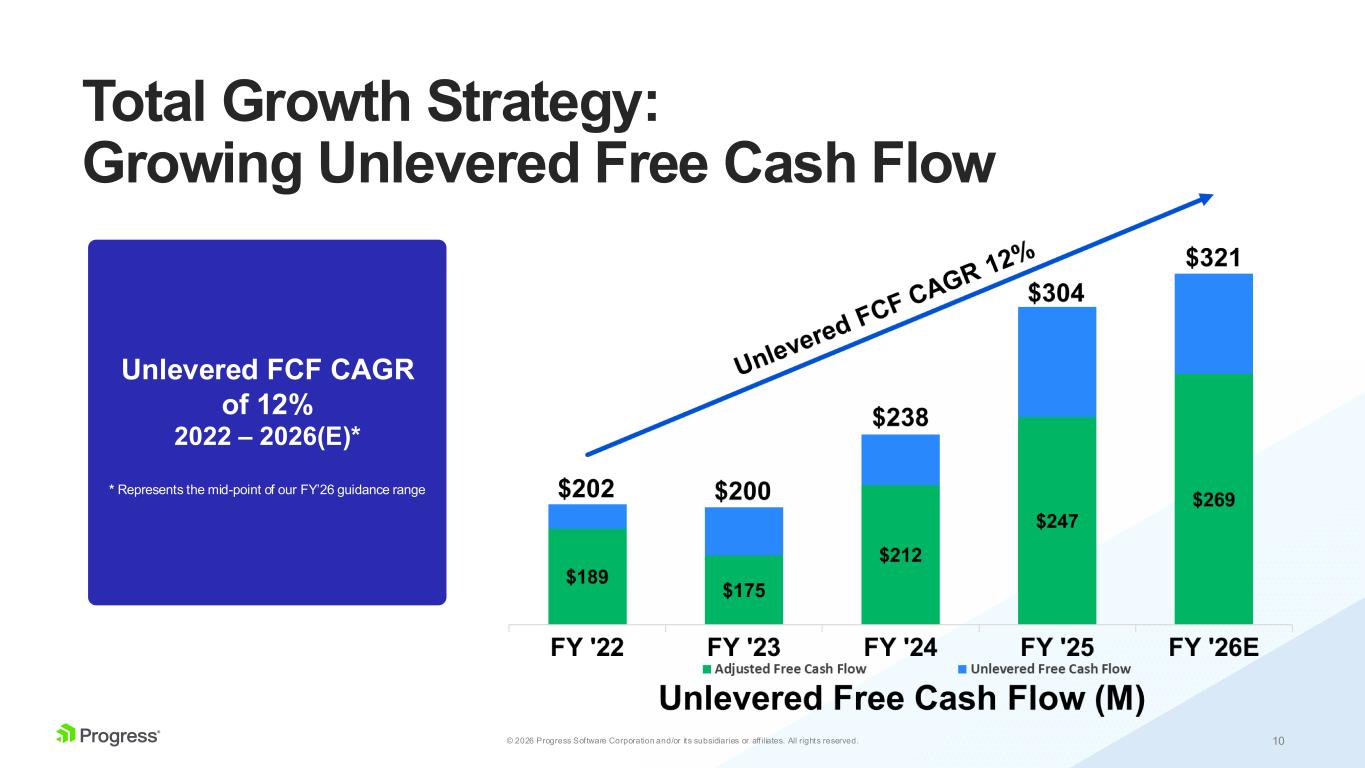

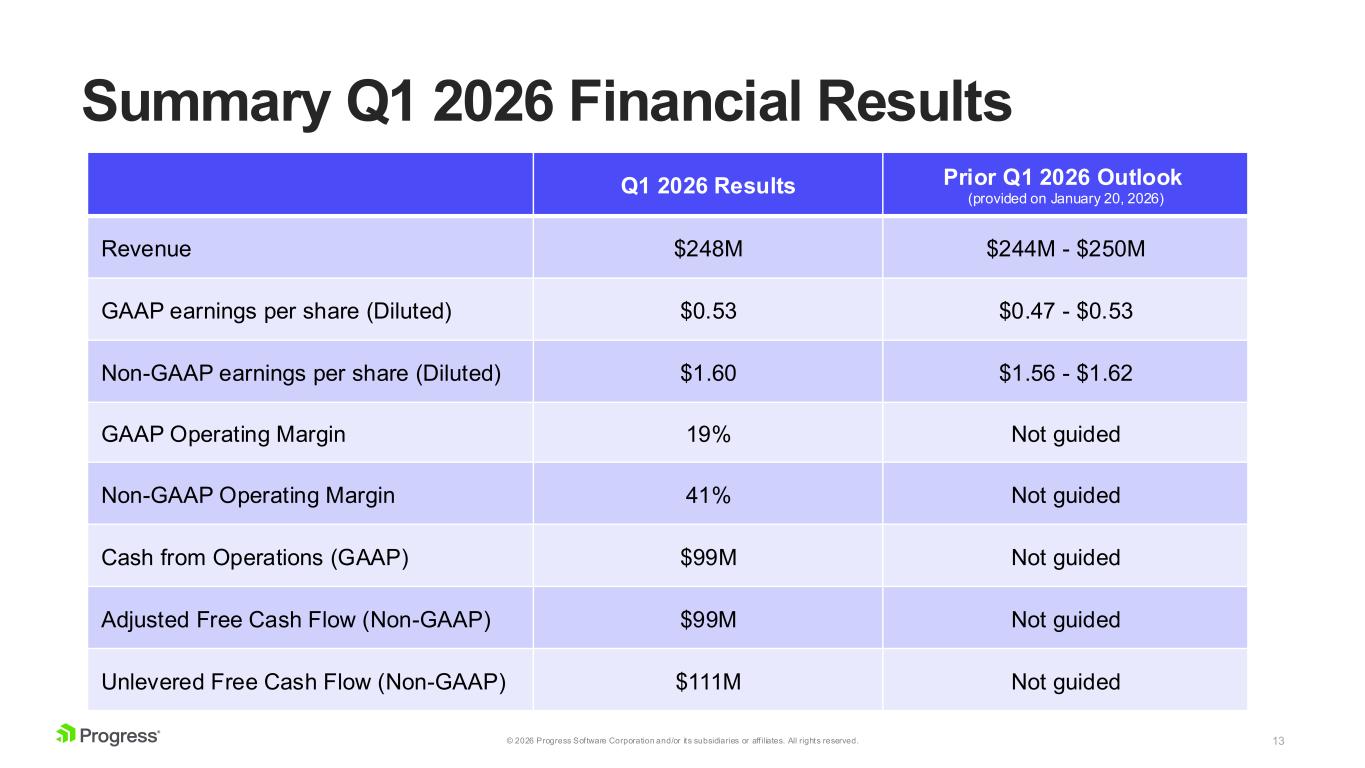

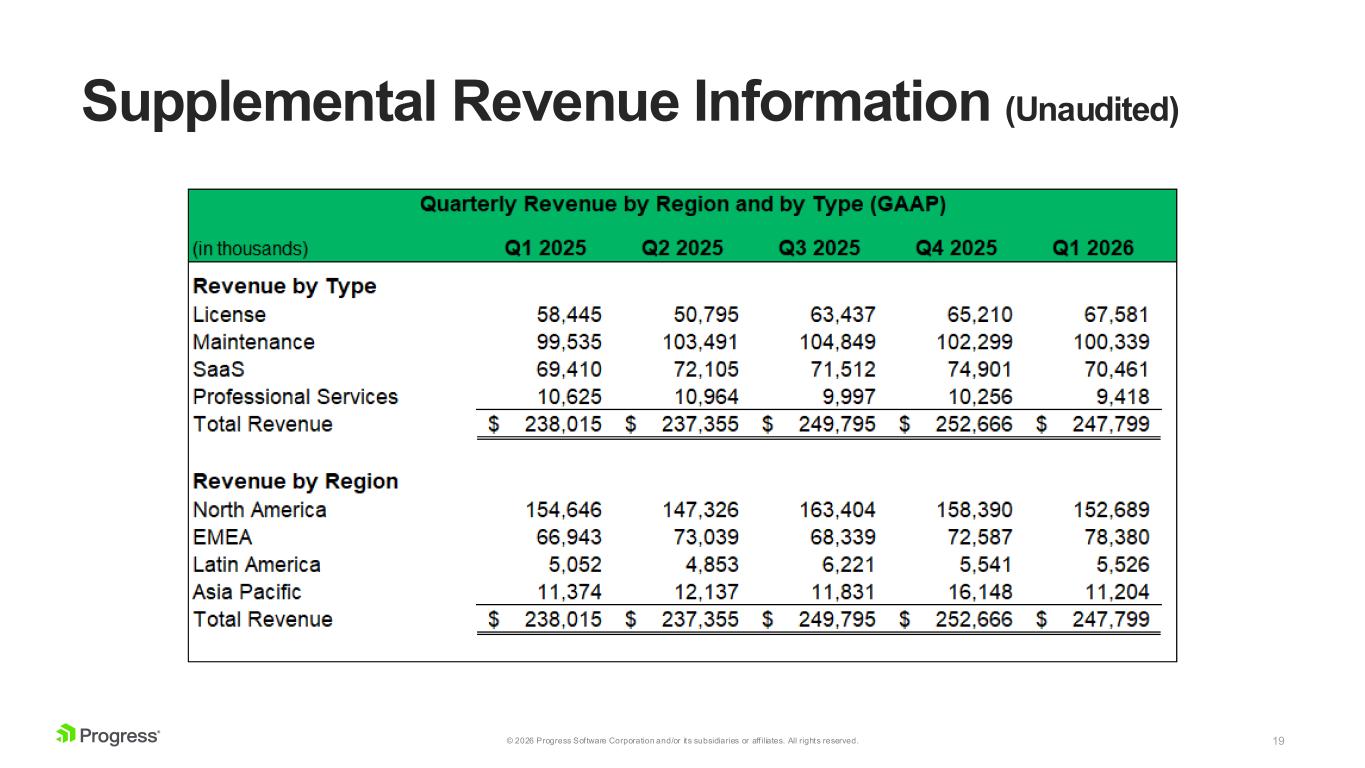

Progress Software reported Q1 FY2026 revenue of $248 million, up 4% year-over-year, with non-GAAP EPS of $1.60 (up 22%), ARR of $863 million (up 2% in constant currency), non-GAAP operating margin of 41%, and adjusted free cash flow of $99 million, while paying down $60 million of debt and repurchasing $20 million of stock.

“We had another very good quarter. Revenue was $248 million, up 4% from last year's Q1. ARR grew 2% in constant currency over the same period, and NRR remained strong at 99%. EPS for the quarter was $1.60, up 22% year-over-year, as operating margins finished above 41%.”

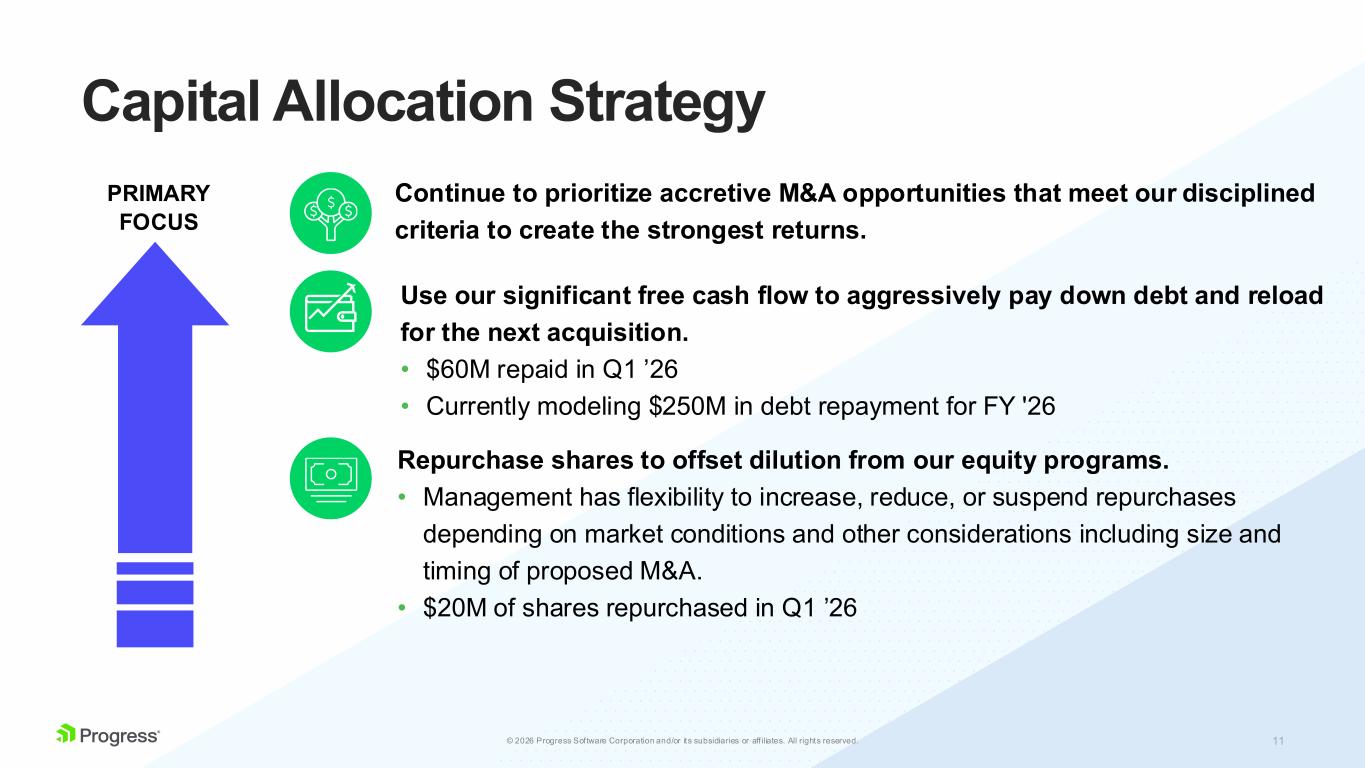

“Our capital allocation priorities remain very clear. We will continue to, number one, invest in our business and innovate. Number two, aggressively reduce debt and be opportunistic on buybacks. And number three, maintain our commitment to generate excess returns through disciplined M&A, followed by rapid synergistic integration.”

- Revenue grew 4% year-over-year to $248 million, with ARR up 2% in constant currency to $863 million.

- Non-GAAP EPS rose 22% to $1.60 and GAAP EPS more than doubled to $0.53 (up 121%).

- Non-GAAP operating margin expanded 200 bps to 41%, with GAAP operating margin up 500 bps to 19%.

- Adjusted free cash flow of $99 million (up 35%) and unlevered free cash flow of $111 million (up 26%).

- Paid down $60 million of debt and repurchased $20 million of stock in Q1.

- AI-powered products driving measurable customer wins, including a U.S. state government now a seven-figure ARR customer identifying tens of millions in annual waste/fraud savings.

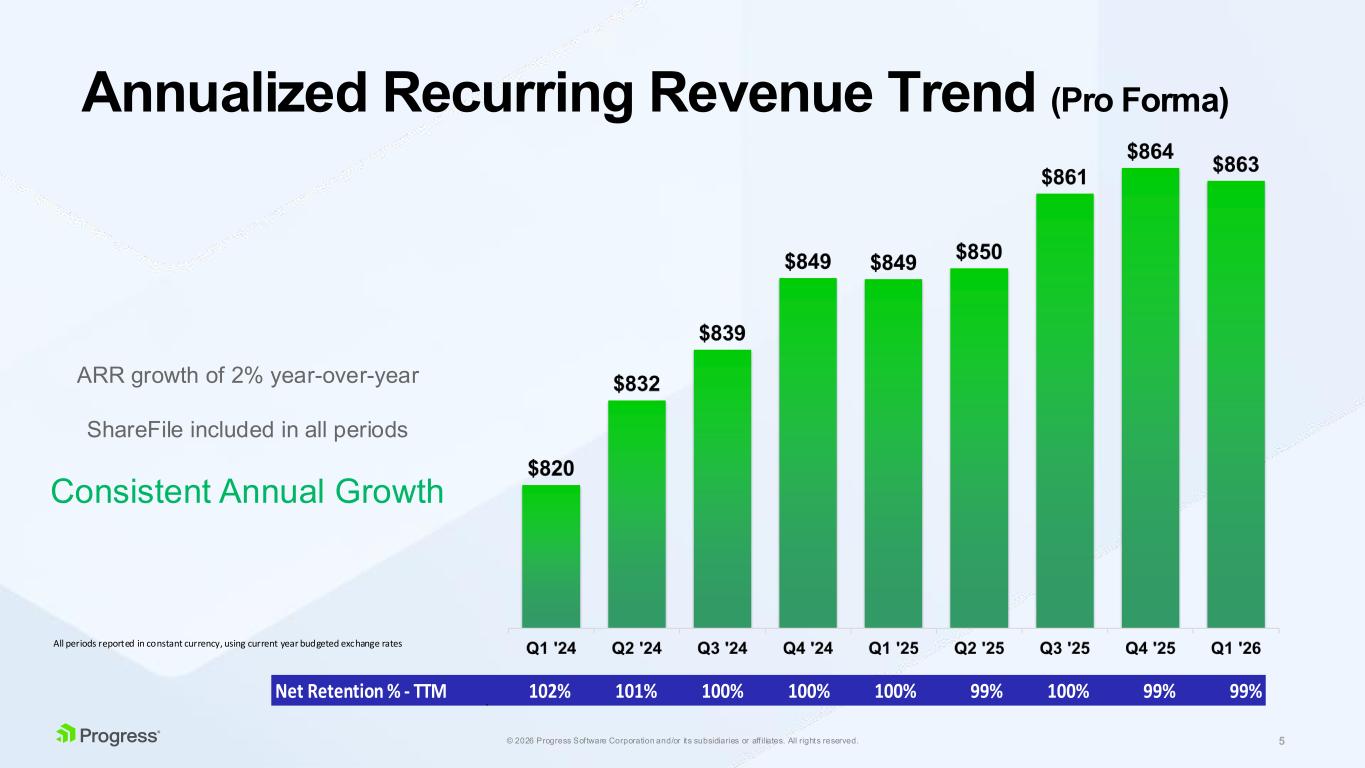

- Net Revenue Retention was 99%, below the company's 100% target, due to an isolated churn event tied to an Eastern European government/court ruling halting call data retention.

- Constant currency revenue growth was only 2% versus 4% on an actual currency basis.

- ShareFile SaaS revenue showed some noise from billing cleanups; CEO acknowledged potential for modest sequential movement.

- Management flagged macro and geopolitical uncertainty and said it will continue to monitor conditions closely.

- GAAP operating margin remains low at 19%, indicating significant non-GAAP adjustments.

Guidance

from the 8-K filed Mar 30, 2026| Metric | Period | Guided | Basis | Actual |

|---|---|---|---|---|

|

Diluted earnings per share

table

Initiated

Fiscal Year Ending November 30, 2026

|

$5.91 – $6.03 | Non-GAAP | — | |

|

Revenue

table

Initiated

Fiscal second quarter ending May 31, 2026

|

$240M – $246M | Non-GAAP | — | |

|

Operating margin

table

Initiated

Fiscal Year Ending November 30, 2026

|

39% | Non-GAAP | — | |

|

Diluted earnings per share

table

Initiated

Fiscal second quarter ending May 31, 2026

|

$0.35 – $0.41 | GAAP | $0.50 above | |

|

Effective tax rate

table

Initiated

Fiscal Year Ending November 30, 2026

|

20% | Non-GAAP | — | |

|

Diluted earnings per share

table

Initiated

Fiscal second quarter ending May 31, 2026

|

$1.47 – $1.53 | Non-GAAP | — |

Hello, and thank you for standing by. Welcome to Progress Software Corp. First Quarter 2026 Earnings Conference Call. At this time, all participants are on a listen-only mode. After the speaker's presentation, there will be a question and answer session. To ask the question during the session, you will need to press star 11 on your telephone. You will then hear an automatic message advising your hand is raised. To withdraw your question, please press star 11 again. I would now like to hand the call over to Michael Michique, Senior Vice President of Investor Relations. You may begin.

Okay, thank you, Tawanda. Good afternoon, everyone, and thanks for joining us for Progress Software's first fiscal quarter 2026 Financial Results Conference Call. Joining me on the call are Yogesh Gupta, President and CEO, and Anthony Folger, our Chief Financial Officer. Before we get started, please consider our safe harbor statement as follows. During this call, we will discuss our outlook for future financial and operating performance, corporate strategies, product plans, cost initiatives, and other information that might be considered forward-looking. Such forward-looking information represents Progress Software's outlook and guidance only as of today and is subject to risks and uncertainties, and our actual results may vary materially. For a description of the factors that may affect our future results and operations, please refer to the risk factors in our SEC filings, particularly the risk factor section of our most recent Form 10-Q and the latest 10-Q being filed in conjunction with this announcement. Progress assumes no obligation to update forward-looking statements included in this call. Additionally, please note that all the financial figures referenced on this call are non-GAAP measures unless otherwise indicated. You can find a reconciliation of these non-GAAP financial measures to the most directly comparable GAAP figures in our earnings press release, which was issued after the market closed today. This document contains additional information related to our financial results for the first quarter of fiscal 26, and I recommend that you reference it for specific details. We've also provided a slide presentation that contains supplemental data for our first quarter and provides additional highlights and financial metrics. Both the earnings release and the supplemental presentation are available on the investor relations section of our website at investors.progress.com. Today's call is being recorded in its entirety and will be available for replay on the Investor Relations section of our website shortly after we finish.

Yogesh, let me turn it over to you. Thanks, Mike. Good afternoon, everyone, and thank you for joining us. We're very pleased to share our first quarter results with you today, so let's get right to it. We had another very good quarter. Revenue was $248 million, up 4% from last year's Q1. ARR grew 2% in constant currency over the same period, and NRR remained strong at 99%. EPS for the quarter was $1.60, up 22% year-over-year, as operating margins finished above 41%. We saw record cash flows as a result of strong focus on collections. Adjusted free cash flow was $99 million, and unlevered free cash flow was $111 million. The balance sheet remains in great shape as we continue to aggressively pay down debt while also repurchasing shares. This strong performance is driven by AI and other innovations across our portfolio that are resonating with our customers. Now, more than ever, our products remain mission critical, our customers remain loyal, and our team continues to execute at a high level. are also the reasons why we remain positive about our outlook. As always, the foundation underpinning our success is our total growth strategy. We continue to run the business with discipline as we innovate across the product portfolio and provide increasing value to our customers. That formula has worked for us through multiple technology shifts and industry transformations, and it continues to work today. On M&A, our corporate development team is vetting deals aggressively, and we further fine-tuned share file operations, which continues to perform very well as one of our best acquisitions. Lastly, customer success remains our key focus. Now, let me address the three topics that we know are top of mind. First, our business remains strong. We see solid retention and good performance across our products. Our product portfolio is broad and continues to power our customers' businesses, resulting in solid year-over-year growth, both in ARR and in revenue. As we've previously said, our goal for NRR is 100%, and over the past few years, our Our NRR has consistently ranged between 99% and 101%. This quarter, NRR was 99%, and ARR growth was solid, driven by the strength in our new customer acquisition, as well as existing customer expansions, both of which were positively influenced by our AI investments and innovation. And this leads to the second topic, AI. We continue to see AI as an exciting opportunity for our business. We've discussed for several quarters how we're using AI internally to be better, more efficient operators, which we can demonstrate to improve productivity in every department. Our savings from these efforts are enabling us to continue to invest in our AI-related product efforts while delivering exceptional operating margins. Speaking of our product efforts, AI has enabled us to accelerate our innovation cycles as well as helped us transform our product capabilities to be more relevant for the future. We have been building AI into our products and that is delivering meaningful business value to our customers today. It is our belief that trusted software companies like ourselves with excellent customer relationships who leverage AI effectively will be the winners of this AI opportunity. Our customers are eager to understand how they can benefit from AI while ensuring that their businesses remain secure and trustworthy. They continue to look to us to deliver AI capabilities that increase their competitiveness and improve their efficiency so that they can thrive in this new world. One such example is a global beverage company that wanted to dramatically improve the way they serve their more than 20,000 employees worldwide. By leveraging our Progress Agent Tech RAG product, they streamlined their HR operations, resulting in improved employee satisfaction at a significantly lower cost. Similarly, the tax authority and finance ministry of an overseas government is using the same product so that all employees and citizens can get trusted, verifiable answers from a host of data across that organization. And a state government in the U.S. is using the Progress Data Platform to harmonize and synthesize large volumes of data from different sources to identify and eliminate waste, fraud, and abuse. They first became a Progress customer less than 18 months ago, and they continue to identify new use cases for the data platform, targeting efficiencies and elimination of fraud in the range of tens of millions of dollars annually. Today, they are a seven-figure ARR customer of ours. Progress Data Platform and Progress Agent Tick RAG transformed business data, unstructured files, archives, websites, knowledge bases, and multimedia into an information system that instantly and securely delivers fact-based, trusted, and verifiable answers. Our AI-powered infrastructure management products are also being used to manage and secure modern tech infrastructure. For example, a leading financial payment company that annually processes over $100 billion of transactions, is using Progress WhatsApp Gold, Loadmaster, and Flowmon to improve the availability and security of the infrastructure and to reduce the time to detect, analyze, and prevent security threats. And ShareFile customers are doing work in minutes that used to take hours with its AI document summarization and Q&A capability. Additionally, ShareFile's AI-powered security capabilities proactively detect sensitive information and recommend actions to significantly reduce security risk. Our customers rely on progress to support their journey because they trust us to focus on practical business outcomes. Across our product, AI is contributing to measurable customer value from workflow automation and productivity gains to monetization. Every product of progress is now an active participant in our customers' AI efforts, and we have embedded AI into our products with attention to governance, observability, cost, and LLM flexibility. The third topic, capital allocation and M&A. It's worth noting that in Q1, we paid down $60 million in debt

and repurchased $20 million of stock.

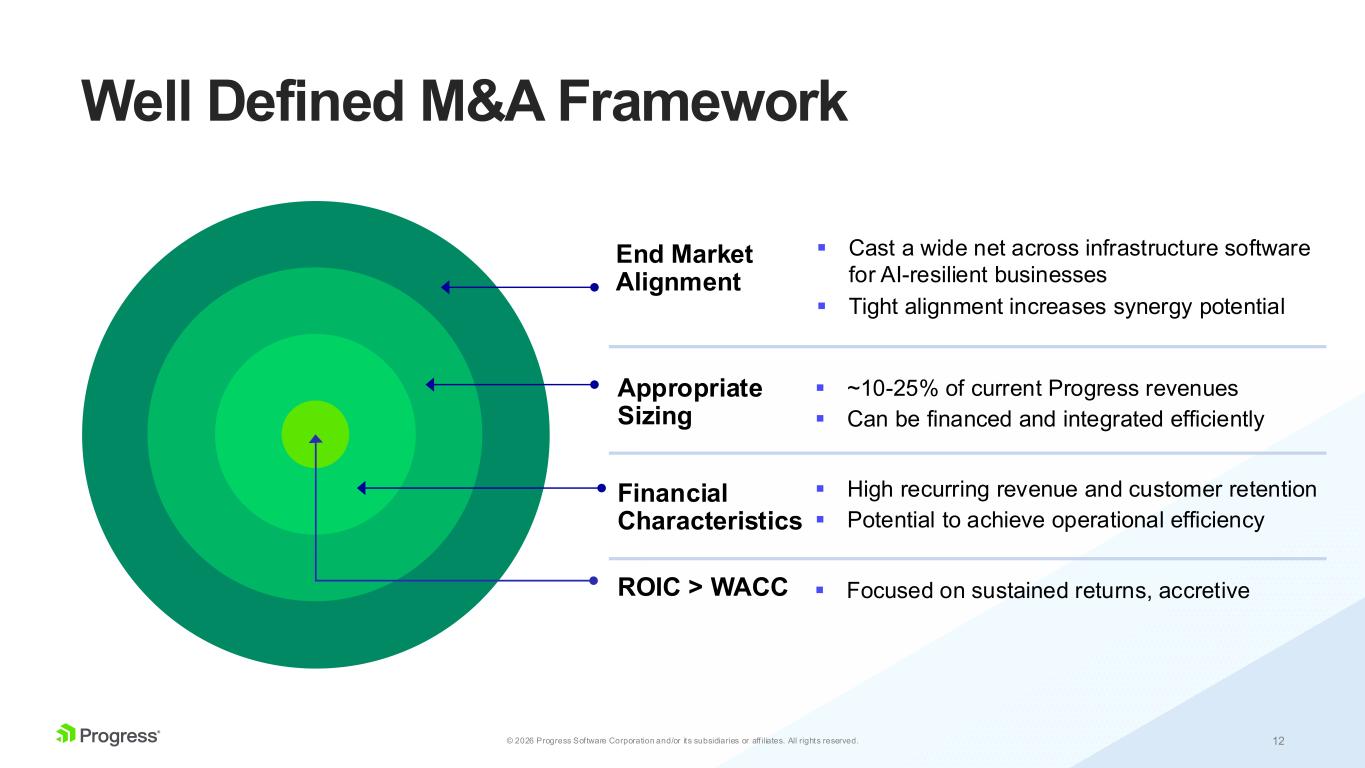

Our balance sheet remains in good shape, and our cash generation gives us significant flexibility. Our capital allocation priorities remain very clear. We will continue to, number one, invest in our business and innovate. Number two, aggressively reduce debt and be opportunistic on buybacks. And number three, maintain our commitment to generate excess returns through disciplined M&A, followed by rapid synergistic integration. We will use the same M&A lens we have always used to acquire good companies with strong infrastructure technology products, loyal customers, high recurring revenue and customer retention, and a compatible culture. It's also worth expanding on how ShareFile continues to create additional value. While it was the largest and most complex acquisition and integration to date, ShareFile has strengthened and scaled our recurring RebNumix, expanded our SaaS capabilities, and contributed meaningfully to the bottom line and cash flow. Just as important, it has enhanced our ability to evaluate and integrate future SaaS opportunities while keeping the same discipline we've always had around returns and fit. I'm also excited to share that Progress recently opened our new innovation hub in Bangalore. This consolidates the office space for our former Progress and Sharefile offices and also demonstrates our long-term commitment to the region as we continue to scale our engineering, product development, sales, and customer success teams. Our people in India are critical to our global growth and our innovation strategy. And this logical next step will enable us to efficiently deliver greater value to our customers worldwide. Finally, we continue to be positive as we look ahead, and Anthony will give you all the details in a minute. From my perspective, what we're seeing in our own business supports our confidence for the rest of this year. We're also maintaining a closed watch on the macro environment and geopolitical events. So to summarize, the business is performing well. The model remains durable. AI is making our products and operations stronger. ShareFile is delivering. And our top line, margins, and cash flow reflect solid execution across the company. As always, I want to thank our employees around the world for their hard work and commitment. And I want to thank our customers and partners for their continued trust. With that, I'll turn it over to Anthony.

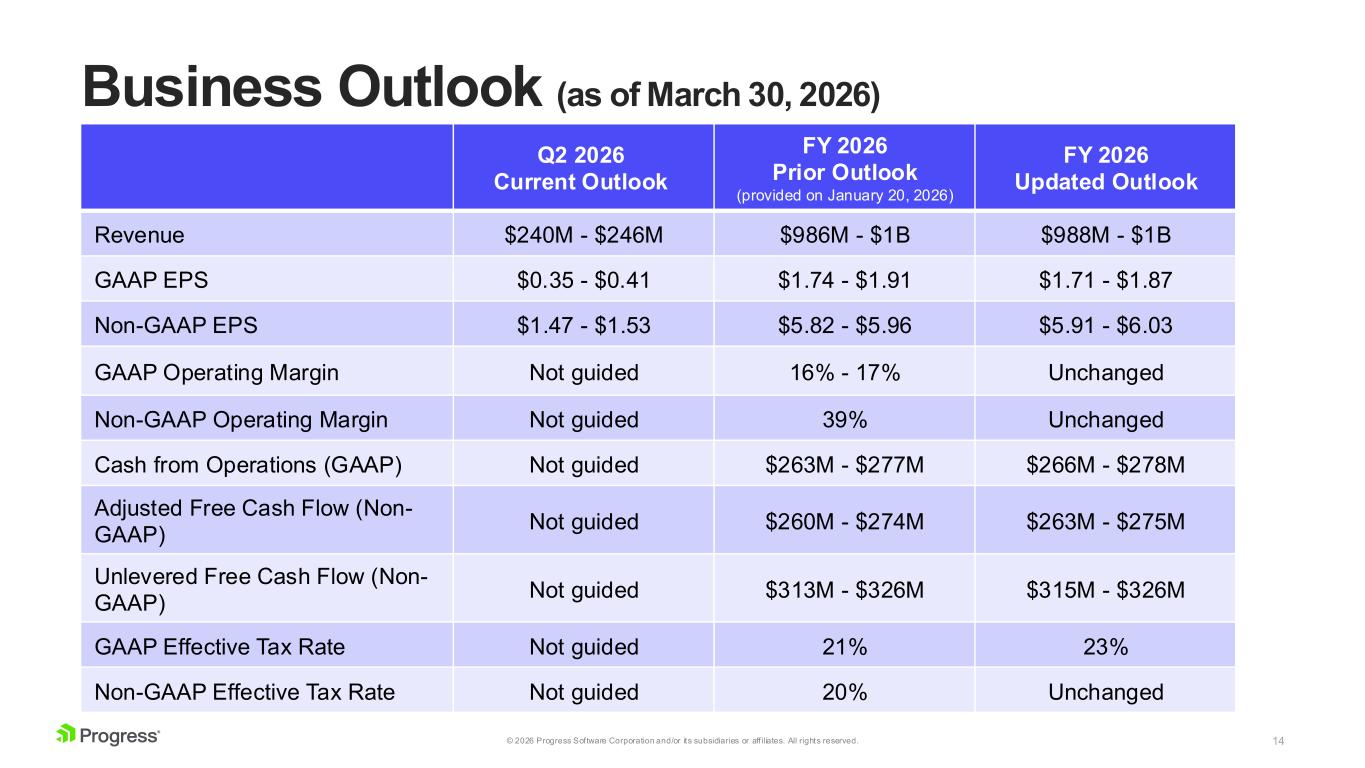

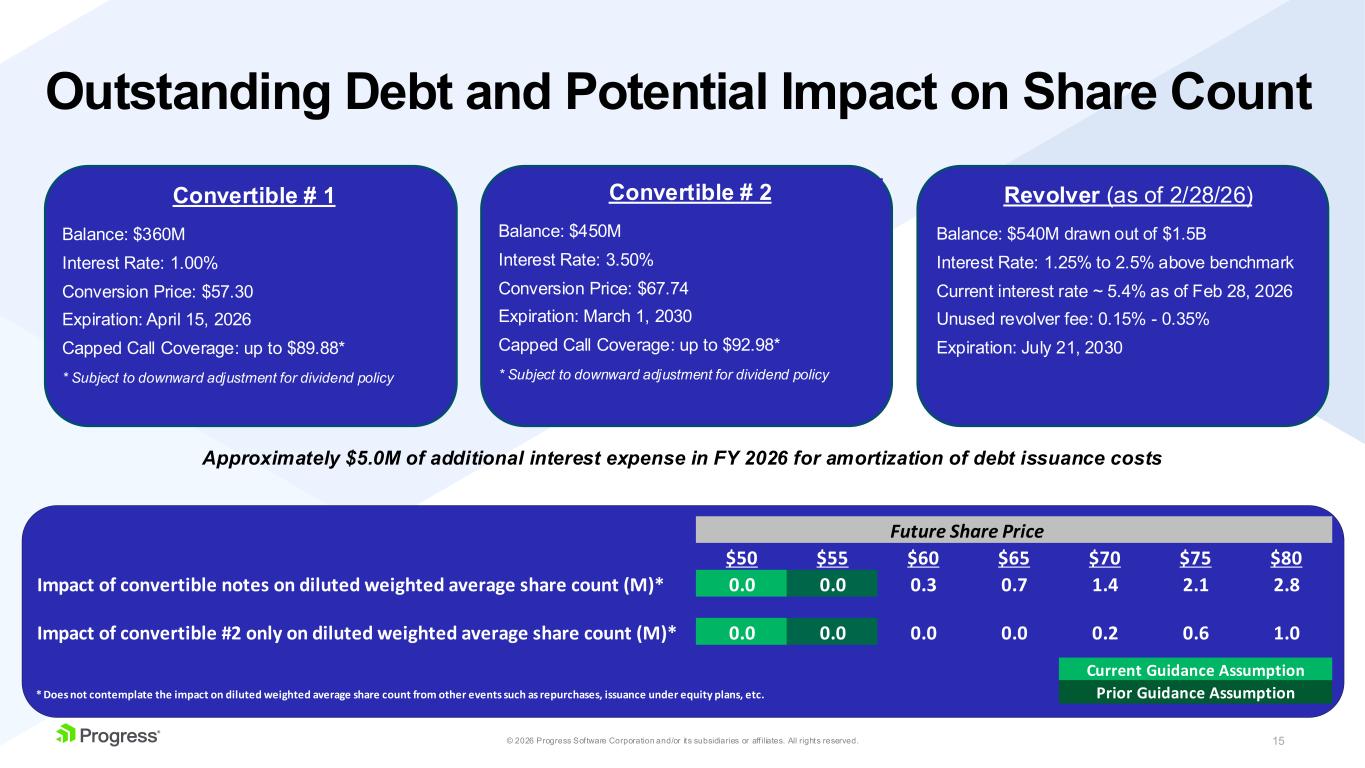

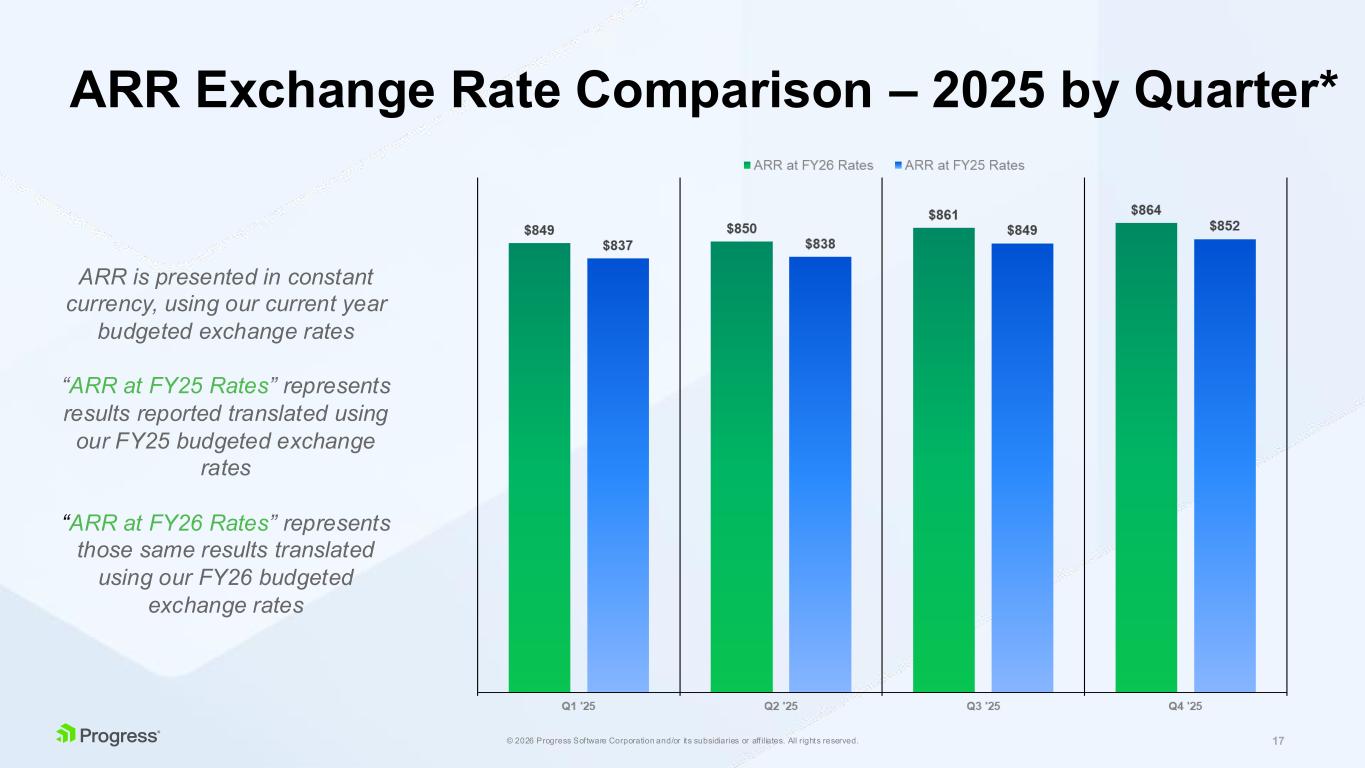

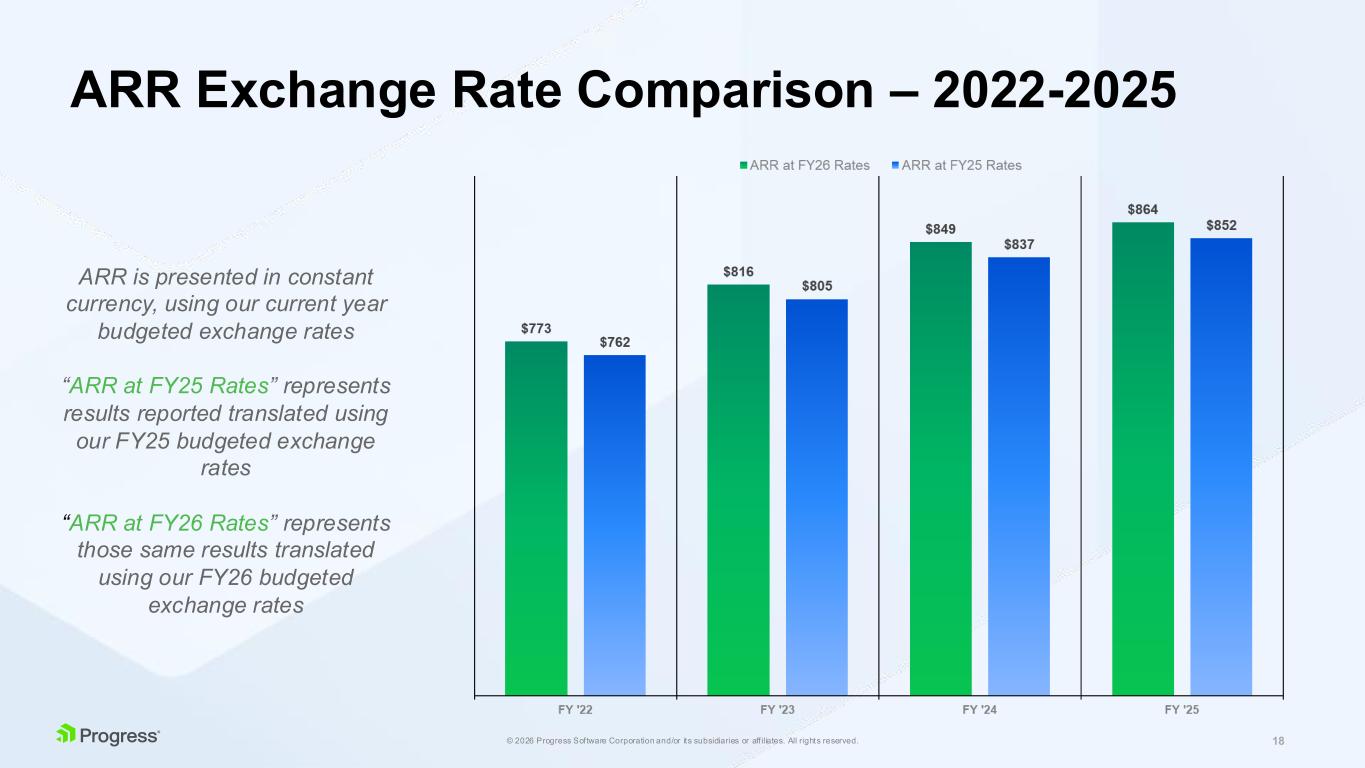

All right. Thanks, Yogesh, and good afternoon, everyone. As you heard in Yogesh's remarks, we're very pleased with our Q1 results, and we're excited to share a strong start to our fiscal year. So let's get right into the numbers, starting with ARR, which, as we've discussed, provides the best view into our top-line performance. We closed Q1 with ARR of approximately $863 million, representing 2% pro forma year-over-year growth. For clarity, our pro forma results include ARR from acquired businesses in all periods presented. This growth in ARR reflects a broad-based contribution from across our portfolio, including OpenEdge, ShareFile, LoadMaster, What's Up Gold, MoveIt, and our DevTools products. Consistent with prior quarters, our net retention rate remained strong, coming in at 99%, underscoring the resilience of our customer base and the mission-critical nature of our products. We did see some isolated churn in the quarter, which we expect to work through quickly, and we still delivered solid growth thanks to strength in new customer wins and expansion in the install base, two areas positively influenced by our investments in AI and innovation. As a reminder, we calculate ARR in constant currency with all periods presented at current year budgeted exchange rates. Consistent with past practice, we've updated ARR using 2026 budgeted exchange rates, and as a result, ARR reported in prior periods has changed. The change is not material and doesn't alter the trend in ARR growth, although the previously reported ARR and NRR numbers change slightly. The details of this update are included in the supplemental financial presentation filed with our press release. In addition to solid ARR growth, Q1 revenue of $248 million came in ahead of our expectations and reflects 4% growth on a year-over-year basis, led by strong performance in OpenEdge. As we've mentioned on previous earnings calls, the renewal timing of subscription contracts, especially multi-year subscriptions, can have a meaningful impact on our revenue in any given quarter. And for this reason, we continue to focus on ARR as the best barometer of top-line performance. Turning to expenses, our total costs and operating expenses were approximately $146 million, which was favorable to our internal forecast and largely flat compared to the year-ago quarter as we continue to demonstrate disciplined cost management across the business. Operating income of $102 million was also better than our internal forecast, resulting in an operating margin of 41% solid year-over-year margin expansion. Earnings per share of $1.60 for the quarter came in better than our internal expectations, the result of solid execution on the top line, coupled with strong cost management. Turning now to a few balance sheet and cash flow metrics, we ended the quarter with cash and cash equivalents of $113 million and total debt of $1.35 billion for a net debt position of approximately $1.24 billion. As a reminder, our total debt includes our revolving credit facility with $540 million drawn, a $360 million convertible note maturing this April, and a $450 million convertible note maturing in 2030. At the end of this quarter, our net leverage ratio was 3.1 times, down meaningfully from when we acquired ShareFile a little over a year ago. DSO for the quarter was 52 days, a significant improvement from 73 days reported in Q4. Deferred revenue was approximately $425 million at the end of the first quarter, up roughly $25 million year over year. Adjusted free cash flow was $99 million for the quarter, a significant increase compared to the $73 million in the prior year quarter. The improvement, primarily the result of increased collections. During the quarter, we paid down $60 million against our revolving line of credit and repurchased $20 million of progress stock. We ended the quarter with $540 million drawn on our revolving line of credit and $182 million remaining under our current share repurchase authorization. Okay, now I'd like to turn to our outlook for Q2 in the full year 2026, Before I get into the numbers, I'll highlight a few items. First, we continue to focus on ARR as a key metric and expect ARR growth to be generally in line with revenue growth for the full year. Second, we plan to roll our 2026 convertible notes into our revolving credit facility when they mature in April. At the end of Q1, we had approximately $960 million of unused revolver capacity, positioning us well to absorb the convert maturity and continue executing our strategy. Our updated EPS outlook reflects higher interest expense associated with the expected refinancing of the 2026 converts. Finally, on capital allocation, we remain focused on deploying capital where we see the strongest returns. At current levels, that means repaying debt and remaining disciplined in pursuit of accretive acquisitions against a high return threshold. It also includes opportunistic share repurchases. We continue to forecast debt repayment of $250 million for the full year, bringing our net leverage ratio to approximately 2.7 times by year end. With that, for the second quarter of 2026, we expect revenue between $240 and $246 million, and earnings per share between $1.47 and $1.53. For the full year 2026, we expect revenue of between $988 million and $1 billion, approximately 1% to 2% growth over 2025, an operating margin for the year of approximately 39%, Adjusted free cash flow of between $263 million and $275 million. And unlevered free cash flow of between $315 and $326 million. And finally, earnings per share between $5.91 and $6.03. Our guidance for the full year, EPS, assumes a tax rate of 20%. percent, the repurchase of approximately $30 million in progress shares, total debt repayment of $250 million, and approximately $43 million weighted shares outstanding. In closing, we are very pleased to deliver a strong Q1 to start fiscal 26. Our diversified product portfolio continues to demonstrate resilience, our cost discipline remains strong, and we continue to focus our capital allocation strategy on generating the highest returns through a combination of aggressive debt repayment and opportunistic share repurchases. In short, we believe we're very well positioned to execute our total growth strategy throughout 2026 and beyond. With that, I'd like to open the call for Q&A.

Thank you. Ladies and gentlemen, as a reminder to ask a question, please press start 1-1 on your telephone, then wait for your name to be announced. To withdraw your question, please press start 1-1 again. Please stand by while we compile the Q&A roster. Our first question comes from the line of Itai Kidrum with Oppenheimer & Company. The line is open.

thanks hey guys solid numbers I have a couple of questions you guess maybe starting with you on the M&A front I mean one would think that in this current environment it'll be even easier for you to buy companies I'm kind of wondering I know you've always been very disciplined of course on the metrics that you're looking for but why is it still taking you this long to find the

next one so it I you know two two part answer to that question one is that as Anthony just mentioned right there is a clearly a higher bar today given where our own company stock is and our valuation is compared to what it historically was right so we are trading now at an EBITDA multiple that we would need to pay less to generate additional incremental value for our shareholders. So I think that creates a constraint on what we can pay. So that's part A. And I'm not saying that that's why we haven't bought companies, but that's an important consideration in terms of the filter we can apply to the companies we can look at. The second one is, you know, we want to make sure that we find the right assets. And we are truly very active at this point looking at those. But again, as I said, that combination creates a challenge. And the flip side is that even though the public markets are where they are, the private markets at high are still, let's just say, disconnected from reality if what the public markets are is the reality, right? So at least they're disconnected from the public market on the valuation side. So I think those two things are really it. We actually, you know, see tremendous activity in the market. We are seeing all kinds of companies come around. And, you know, obviously everybody on this call will be the first to know when we do one.

Got it.

And Anthony, for you, can you talk about your SaaS revenue? It's actually done quite substantially on a quarter-over-quarter basis. You guys talked about ShareFile actually doing well for you. But you did mention on the call some elevated churn, isolated churn, I think you called it. So we'd love to get a little bit more color on what isolated churn means and why is the SaaS revenue declining quarter-over-quarter.

Yeah, sure, Itai. And maybe I'll take the isolated churn comment first. because I do think they're a little bit different in terms of, you know, the isolated churn and the SaaS revenue. But in terms of isolated churn, yeah, we had, you know, a couple of, I'd say, customer-specific events that weren't really related to product value or competitive dynamics or really a broader trend in the business. And to give you an example, you know, we had a seven-figure government contract in Eastern Europe for data retention services, and a European court ruled the government had to cease retaining the data. And so as a result, the contract churns out, right? So not because of any dissatisfaction with our product or a competitive loss, but the underlying use case effectively gets eliminated by a court rule. And so, occasionally, we see issues like that. You know, we've seen them in the past. We've talked about it. M&A sometimes can be, you know, something that may cause a little bit of churn in our business. So, like in times past, you know, not material overall and really specific to a particular situation. And I think something we'll probably work through pretty quickly. And despite that, you know, having put up 2% ARR growth for the quarter, you know, was a pretty good testament to new customer acquisition and some of the expansion that we got out of the base. So that was what I was referring to in terms of the, you know, any sort of isolated churn. In terms of the SaaS dynamics on revenue, if you'll recall back in Q4, you know, we were asked about a big sequential increase in our SAS revenue and I think I said at the time that it was a you know a little bit of an upside surprise and we expected things to to normalize in 2026 and and sort of you know come back in line with the maybe closer to the annual number for 2025 so the Q4 number wasn't something we expected to sustain if you look at it sequentially on a year-over-year basis, obviously the SAS revenue number is still growing. And the reason for it, what's underlying it, is just a lot of the cleanup that we have been doing on the share file business, right? We mentioned, I think, on the Q2 call last year that CSG was doing, still doing the billings for us up until April of 2025. And, you know, then we had to stand up a billing system internally um and you know it probably took us until the back half of last year to get our arms around that completely and so there's a lot of data cleanup that goes on some of it in q4 some of it in q1 and there'll be a little bit of it that continues throughout 2026 again you know not material in total but it may bump numbers around a little bit from time to time um and And, you know, I guess from the other side of it is as we get our arms around the data and as we sort of get, you know, more and more control around the share file business, the positive aspects that we saw, especially this quarter, were enhanced collections, right? And the free cash flow of almost $100 million for the quarter, I think the significant improvement we saw was largely the result of improved collections and share file. So, you know, on the one hand, there's a lot of data to clean up, but as we get that data cleaned and as we get our arms around the systems, we certainly make up for lost time on the collections front, which was nice.

I appreciate it. Thank you.

Our next question comes from the line of John DeFucci with Guggenheim Securities. Your line is open.

Thank you. My first question is for Yogesh. So, I guess it was interesting that you mentioned Chef's doing really well in one of your best acquisitions performance-wise. As you know, the developer seat count, and I'm glad you said that, because there's a lot of concern out there with the developer seat count, and there's a huge debate out there. I guess you're doing well here, but are you seeing – take Chef out of it. But I mean, when you talk to your customers, when you see what they're doing, are you seeing any change in developer numbers at your customer base? And whether that could be like they're not hiring as much as they used to be, or they're actually declining, or they're not declining, whatever you're seeing. And then secondly, why is it, regardless of what that answer is, why is it that Chef's doing so well?

So I think, by the way, I don't know whether it was the audio or whether it was me or which end, but John, the product I mentioned that's doing really well was ShareFile, not Chef. Oh, I'm sorry. I'm misunderstanding. But anyway, let me talk about the developer scenario, though, because our developer products are doing well, right? And so the reason I think, so there are two parts. So I think first talking about our customers, what we are seeing, I believe that there is a change in trend, but I wouldn't say that the absolute developer numbers overall appear to be dropping. The absolute numbers have dropped in what I would call a small number of customers. But by and large, I think the trend is less growth than historic. And so I think that the developer seats and seat-based developer businesses, which primarily is DevTools for us, which is a relatively small business, it's about, you know, it's a single-digit, mid-single-digit percentage business for us, right? That business is where if we didn't do the right things, we would see challenges. So what we've done is we've actually done significant AI investments there to make our developer tools, which are primarily libraries for developing a great UI and so on, be more relevant in the agentic age, help with developers who are building agentic apps and provide them with the right tooling for that. So, you know, we are effectively doing a significant amount of change in that, what I call the value proposition for the developer and so we feel good about how that business continues to perform but it is a it is it is a business that has the greatest potential risk which is why it has also had the greatest acceleration on our part in terms of the AI work that we have done with it and so we're seeing good business there and we continue to see good business there I think that the you know products like chef continue to do well because infrastructure needs to be managed infrastructure needs to be configured infrastructure needs to be set up so that you know things run well and so you know that product is a workhorse for many large enterprises including you know the the largest credit card, pretty much every credit card company, pretty much, you know, many of the Silicon Valley tech companies, etc. I mean, literally, you know, two of the Mag7 have been customers forever. So it is a very, very strong and solid product. And we continue to see, you know, basically the need for that product. And we win some new customers as well. But I think the ShareFile product, on the other hand, is doing well from a customer perspective as well because of the AI efforts there. So I'm sorry about the confusion

about my voice. I'm sorry about that. No, you know what, Yogesh, it wasn't you. I'm sure to me, I can't hear it that well sometimes. But thank you for answering the second question, which was, I think more important anyway. Thank you. And I guess just to follow up for Anthony, I want to follow up to Etai's question on the SaaS business, because it does sound like ShareFile is doing really well. And it's a big acquisition, and it's your first big SaaS acquisition, big SaaS acquisition. But the SaaS revenue didn't just decline sequentially. It declined to less than it was the last three quarters. And so that, I mean, it's not like just the fourth quarter was stronger it's like the last three quarters were stronger so can you help us a little bit because something odd happened and and it sounds like the business doing really well you guys have said it several times even if i heard it wrong but if what is it that that what happened this quarter like it wouldn't have been just like recognition you know sometimes i i can imagine you know you You don't get the renewal, and you're not recognizing it, and then you recognize it, but it's not just the fourth quarter that was stronger than this quarter. Sorry.

Sorry, I get it, John. And, yeah, I think the range of SaaS revenue for the business overall has been, you know, if I were to normalize for the cleanup issues that I sort of referred to, it's between 72 and 73 million going back to, I don't know, to one of last year. That's if I sort of normalize each one of these quarters. And all that's happening is, you know, we talked about it a little bit last year that, you know, taking over the billing system from from csg was a pretty significant milestone in terms of integration and in the back half of the year as we started to get our arms around the data there was a lot of cleanup that needed to be done you know in some cases you had customers that hadn't been billed and needed to get invoiced they you know required some catch-up invoicing and there And there were some that, you know, that needed to be written out of ARR or reserved against revenue for whatever reason. And there was just a lot of data that we really didn't have access to pre-acquisition. And even with CSG doing a lot of the billings under the TSA, in the back half of last year as we started to clean that up, you know, again, not material overall. But if it's a few million dollars here and there as we go quarter to quarter, it may move that number around a little bit. And that's really all it was. I mean, otherwise, you're right. The share file business, you know, if I were to sort of normalize these things out, like I said, you know, $72 to $73 million for total SaaS revenue on a quarterly basis is where it's been.

Okay. And that's helpful. But is it cleaned up now, Anthony? Should we assume that this should behave like a, you know, listen, we don't expect a lot of growth out of it, but just even if it's solid or steady, or could we potentially see some declines going forward, too?

No, I think it is largely cleaned up, and any of these cleanup issues that we need to do will get smaller and smaller as we go forward. So I don't expect, you know, significant issues with it. And as your guest said, the business fundamentally from an operational perspective has been incredibly solid.

Great. Great. Thank you very much, guys.

Thank you. Our next question comes from the line of Lucky Schreiner with DA Davison. Your line is open.

Great. Maybe an apologies to follow up again on the line of questioning here. But on that isolated churn event, you know, if I remember last quarter, I believe you guys talked to not seeing an impact of multi-year contracts for this year. And so it sounds like maybe visibility there changed. Is that related to the isolated churn event or is that something different?

Lucky, not really. You know, when the, you know, the EU court puts out a statement saying that shall stop immediately. you know this was an eastern european government uh they basically instantly told that they were going to stop paying and so this was actually the customers were local uh telephone customers local uh and this was called records of phone calls that people make and when that became quote that was deemed illegal the country immediately government immediately said to all those call record companies and all the telephone companies saying hey can't retain this anymore delete it all and we will not pay you anymore starting right now so so it was what i would call a surprise turn right it was one of those things where they just happened to say sorry we can't pay you anymore because we've got this we're not getting paid anymore so it's a weird thing, right? I mean, we could go and tell them, hey, you have a contract. It doesn't expire for a little bit. But at the same time, you know, we really, you know, when governments do those kind of things, I think it's tough to get folks to comply. So we wanted to basically take the

churn and we've taken the churn. Gotcha. So, yeah, it sounds like visibility hasn't changed then.

No, not at all. This was unusual. This was truly unusual. The decision came out, the government acted, and the service providers had to act. I mean, it was within a matter of two weeks and completely from left field.

Gotcha. That's helpful. Maybe then on NRR, you know, I know you guys are within your target framework, but, you know, what's it going to take to get that above the 100% target? Is that a function of just working through the recent churn event? And, you know, you mentioned maintaining a

close watch on the macro. Is that at all playing a factor here? So, I don't feel that today macro is playing a factor for our business. I can't speak for the rest of the world, but for progress, I believe this is purely because of the isolated churn that we saw. And as you know, Lucky, because our NRR is a trailing four quarter number, it moves rather slowly. And so it'll take us a little bit to get us back. Our target continues to be, you know, being at or above 100. I mean, our goal says, hey, 100% NRR ARR is our goal, but you know, we've actually fluctuated between 99 and 101 by and large for the last few years. I think occasionally we've touched 102, but by and large it's been between 99 and 101. So we actually feel good about our business, and we also feel good, lucky, that we were able to grow ARR by 2% year over year, which is another point, because when you think about it, when NRR is somewhat light, you know, it doesn't take much to, you know, for a few tens of basis points for things to move. You know, the fact that we were able to grow our ARR 2% year over year means that, you know, obviously new customers are embracing us and our expansions continue to be good, So we continue to be confident. We are not concerned about the way the business is going at this stage. And the reason why I caveat it at this stage is, you know, the macro and the geopolitical events going on, which I think, I mean, the uncertainty around those, I don't have to sort of share with anyone. You know, we all know that, you know, basically some days people think in the morning, it's going to be okay in the evening it's going to be not okay so with that kind of uncertainty with unclear what will happen in the market we will continue to monitor that very very closely but so far we have not seen any instance or any example or any anecdotal evidence anything at all

to say that macro is having an impact on us got it makes a lot of sense thanks for taking my

questions. Thank you. Ladies and gentlemen, as a reminder to ask the questions, please press start 1-1 on your telephone. I'm sure no further questions in the queue. I would now like to turn

the call back over to Yogesh for closing remarks. Well, thank you everyone for joining. It's a pleasure to speak with you all, and we look forward to speaking with you again next quarter. Bye-bye.

Ladies and gentlemen, that concludes today's conference call. Thank you for your participation. You may now disconnect.